activity based costing VS traditional absorption costing

ABC的基于活动的成本核算[文献翻译]

![ABC的基于活动的成本核算[文献翻译]](https://img.taocdn.com/s3/m/bada34d343323968001c920a.png)

外文文献翻译原文:The ABCs of Activity-Based CostingMost successful electrical distributors have a firm handle on revenue sources and direct costs, but many don't have a good grip on how the products they distribute and the customers they serve consume support services and contribute to other indirect costs. Without detailed visibility into sales, logistics, fulfillment and administrative expenses, it's difficult to measure the financial performance of individual products and customers or to make informed decisions that reduce overall costs and optimize profitability.Traditional cost accounting has been criticized for cost distortion and lack of relevance during the last 20 years (Johnson and Kaplan 1987). A new costing method, activity based costing (ABC), was developed and has been advocated as a means of overcoming the systematic distortions of traditional cost accounting and for bringing relevance back to managerial accounting. A traditional system reports what money is spent on and by whom, but fails to report the cost of activities and processes (Miller 1996). Many organizations including petroleum and semiconductor companies in the manufacturing industry have adopted the new costing method.Lean construction comes from recognizing the limitations of current project management and applying new production management called “lean production” to the construction industry. Koskela (1992) critiqued construction project management in that the traditionalconstruction project management models construction as a series of conversion (value-adding) activities while new production philosophy improves competitiveness by identifying and eliminating waste (non value-adding) activities. He claimed that the construction industry should adopt a new production philosophy. It is an origin of lean construction.Traditional project management is derived from an activity-centered 3 approach, which aims to optimise the project activity by activity assuming customer value isidentified in a design phase (Howell 1999).The focus on activities conceals the waste generated between connected activities by the unpredictable release of work and the arrival of needed resources (Koskela 19992). The purpose of traditional project control is to minimize the negative variance from preestablished (contracted) budgets and schedules (Halpin 1985, Howell and Ballard 1996).By contrast, the focus of lean construction is on work flow reliability. Managing the combined effects of dependence and variation is the first concern in lean construction (Howell 1999).The goal of this paper is to present a method or applying ABC in construction and an example of applying ABC in construction, exploring the relationship between activitybased costing and lean construction.The paper includes a review and evaluation of prior applications of ABC in construction. Then the paper presents a cost hierarchy and cost driver in application of ABC, and illustrates with an example. Finally the relationship between ABC and lean construction is presented.Efforts to apply ABC to construction were found in several papers, as ABC is a popular managerial accounting tool in the manufacturing industries. Fayek (2000) linked the job-costing model with activity-based costing. He conceived a schedule activity as an activity in ABC. He proposed that costing each schedule activity and job is activity-based costing. However, a schedule activity in construction differsfrom an activity in activity-based costing because each schedule activity is a task or service that a contractor or crew is supposed to provide, as opposed one of several process steps involved in its execution or production. The ‘activity’ in ABC refers to the production process. The ‘activity’ in ‘schedule activity’ refers to the product ofproduction processes, but neglects the processes themselves. Therefore, assigning costs to schedule activities in construction projects is not equivalent to activity-based costing. Back et al. (2000) and Maxwell et al. (1998) linked process modeling and simulation with activity-based costing. They expanded the concept of activity following that of process modeling. However, their model uses only one resourcedriver such as time and does not recognize activity cost drivers. The model does not recognize a cost hierarchy either. Moreover, their model concentrates on field operations neglecting other elements in the value chain such as procurement, material handling, production, and hand-over. Some accounting companies such as ABC Tech Inc. provide construction companies with ABC service (Matteson 1994, Antos 2000). However, application is limited to home office overhead costs.At the heart of construction project accounting is the job costing system. In job costing systems, the cost object is an individual unit, batch, or lot of a distinct product or service called a job (Horngren et al. 1999).These cost accounts (work packages) are the results of the project work breakdown structure. However, it is found that resources are directly assigned to a cost account (a subproject) in direct costs. Each resource becomes an individual cost account in overhead costs as seen in Table 1. We use the term ‘Resource-Based Costing’ as opposed to Activity-Based Costing. RBC assigns costs directly to sub-projects, cost accounts or work packages defined in the work breakdown structures4, as if the costs that arise in the execution of work packages also have their causes in those work packages. This traditional one-stage costing, in which resources are traced directly to products and services, is undertaken from the persp ective of a “transformation view”, which conceives production as a transformation of inputs into outputs. On the other hand, ABC uses two- stage costing, tracing resources to processes then assigning processes to products and services. ABC assigns costs to the processes involved in those work packages, thus potentially revealing problems in the reliability of work flow, the causes of which may be removed from where their effects become visible. In this regard, activity-based costing (ABC) reflects a “flow view”, which conceives production as a flow of materials and informatio n consisting of transformation, inspection, moving, and waiting (Koskela 1999).There are two possible perspectives in the application of ABC in construction: the home office perspective and the project perspective.From the home office perspective, the objective is to assign project-related home office overhead to different projects as shown in Figure 1. The scope of theactivity-based costing system is limited to project-related home office overhead. A simple illustration with regard to prevention of cost distortion is the assignment of material procurement costs to different projects. The current practice is to distribute those home-office overhead costs on the basis of contract amount or direct labor hours (Holland and Hobson 1999). In an activity-based costing system, costs are assigned based on an appropriate activity cost driver such as the number of procurement instances. From the project perspective, all costs are to be assigned to jobs/work packages except general administrative costs and direct material costs as shown Figure 2. (General administrative costs are not assigned because there is no rational basis for the assignment/allocation. There is no need to assign direct material costs since they can be directly costed to each job.) ABC from the project perspective include: 1) assignment of overhead costs to each work division, area, or individual building and 2) cost visibility as to where the costs accumulate in the business process. ABC can provide accurate costs for each project by preventing cost distortion. Besides ABC can provide detailed activity costs data, by which different procurement routes or different strategies can be compared5.We include direct labor costs in the scope of the activity-based costing system (and thus, to be assigned or allocated based on cost drivers) because construction direct labor costs often include activities which can be categorized in manufacturing overhead costs; e.g., material handling. Therefore direct labor costs conceal non-value-adding activities such as rework. In manufacturing applications of ABC, direct labor costs are usually excluded because they do not contain such activities.Activity-based costing (ABC) can accurately determine the true cost of products and services by assigning costs based on services performed by distributor resources. It's a valuable tool for managing costs and improving performance. When conducted effectively, ABC can provide rich insight into a distributor's core business processes and help managers change inefficient business practices. ABC also helps distributors uncover and adjust the drivers of cost and profitability in their businesses and get real-time feedback on any changes they make in their business processes.Optimizing profitability is a top-of-mind issue for many industry leaders. Dr.Barry Lawrence, director of the Industrial Distribution program and the Supply Chain Systems Lab at Texas A&M University, discusses the power of ABC in stratifying customers as one method of optimizing distributor profitability in the book. Optimizing Distributor Profitability: Best Practices to a Stronger Bottom Line.To manage profitability effectively, distributors need to use the proper costing method and have the right information and analytical tools. Most distributors use some method of apportioning costs that lacks rigor and prevents them from understanding the real profitability of products and customers. Unfortunately, when they attempt to optimize their profitability, many distributors use an array of desktop spreadsheets rather than a dedicated application as a method of capturing costs. Spreadsheets can be extremely difficult to use for repetitive, collaborative tasks, and especially tor analyses that involve complex sets of cost data. Relying on desktop spreadsheets can keep distributors from doing the kind of ABC needed to optimize profitability.Technology is now available to assist distributors in applying ABC to drive improved financial performance. With profitability and cost management (PCM) applications, distributors can increase visiblity into enterprise costs. PCM applications can help automate and enable the alignment of operational resources to increase revenues by focusing on the most profitable products and customers and reduce costs on those that are not.PCM applications offer improved visibility into the drivers of cost and profitability with activity-centric, multidimensional modeling and analysis. Distributors can quickly build simple or complex ABC models that can truly reflect operational costs. Having the right cost information when they need it is critical to making smart, timely business decisions. PCM puts valuable data at the fingertips of users across the enterprise, enabling distributors to be agile and flexible. It can help identify areas for cost improvements such as instances of waste or high-cost activities and facilitate proactive decision making to rectify problems. For example, a seemingly profitable high-volume customer may be unprofitable when a distributor considers the costs of all value-added services. Better understanding of customerprofitability enables distributors to improve the structure of their sales terms and to align sales commissions to focus on more profitable sales. PCM allows distributors to become more agile and align their organizations better, gain visibility into their internal operations, and gain confidence in their abilities to control costs and their operations and build out new competitive advantage in this low-margin industry.Summary:PCM offers electrical distributors a deep understanding of the levers affecting organizational costs and profitability. It allows for the identification of underlying causes of under- performance, testing of potential impacts of change and incisive actions to reduce costs and optimize profitability of products and customers.ABC analysis doesn't come without some business challenges. Some distributors may have limited visibility into cost and profitability details; inefficient cost reporting that fails to provide insights for improving financial performance; a lack of transparency into cross-charges and insufficient insight into cost of value-added-services; or annual budgets disconnected from operational reality.ABC analysis offers many profitability and cost management benefits, including visibility into key drivers affecting costs and profitability such as shared services; optimization of costs and profitability based on detailed understanding of multi-dimensional drivers such as products, services and customers; and more incisive decision making due to rapid identification of underlying causes of changes in cost and profitability, and the ability to test potential adjustments. Applying a modern profitability costing methodology means a distributor has current information technology to ensure accuracy, efficiency and agility. Doing so enables distributors to model "what-if " decisions they make every day. Your first step to improve financial performance is a candid assessment of current capabilities and needs. Activity-based costing and the related profitability and cost management applications can help you do that.Source: [U.S.] Paul Pretko. "Internationalization of Chinese enterprises: Theoretical extension Case", electrical wholesale, V olume 1 (3), 2010 (10): P40-42二、翻译文章译文:ABC的基于活动的成本核算最成功的电子分销商有一个坚定的收入来源和处理直接成本的方法,但很多人没有一个良好的抓地力,他们的产品分配和消费服务的客户,他们的支援服务,有助于其他间接费用。

作业成本法和传统成本法的比较研究以某大型机械加工企业为例

作业成本法和传统成本法的比较研究以某大型机械加工企业为例一、本文概述在当今复杂多变的商业环境中,准确的成本信息对于企业的决策至关重要。

作业成本法(ActivityBased Costing, ABC)和传统成本法(Traditional Costing)是两种主要的成本计算方法。

本文旨在比较这两种方法在某大型机械加工企业的应用效果,以期为企业在成本管理方面提供参考。

本文将介绍作业成本法和传统成本法的基本原理和计算方法。

作业成本法通过将成本分配到各个作业活动中,更准确地反映了产品或服务的成本构成。

而传统成本法则通常采用简单的成本分配标准,如直接劳动小时或机器小时。

本文将分析在某大型机械加工企业中,这两种成本法是如何被应用的。

通过实际案例分析,本文将探讨作业成本法和传统成本法在该企业的具体实施过程,以及它们在成本分配、产品定价、利润分析和决策支持等方面的表现。

本文将基于比较分析的结果,提出针对该企业的建议。

这些建议将帮助企业更好地理解和使用作业成本法和传统成本法,从而优化成本管理,提高企业的竞争力和盈利能力。

本文通过比较研究,旨在深入理解作业成本法和传统成本法在某大型机械加工企业的实际应用,以期为相关领域的研究和实践提供有价值的见解。

二、作业成本法概述作业成本法(ActivityBased Costing,简称ABC)是一种成本核算和管理方法,它通过识别企业的各种活动并计算这些活动消耗资源的成本,进而将成本更准确地分配到产品或服务上。

与传统成本法相比,作业成本法的核心优势在于其能够提供更为精确和细致的成本信息,帮助企业更好地理解成本结构,从而做出更加合理的决策。

在大型机械加工企业中,作业成本法的应用尤为重要。

这类企业通常具有复杂的生产流程和多样化的产品线,传统的成本核算方法往往难以准确反映各个产品的实际成本。

通过实施作业成本法,企业可以将生产过程中的各种活动(如材料采购、加工、装配、检验等)识别并分类,然后根据每种活动的实际资源消耗来计算成本。

作业基础成本法

技术创新对作业基础成本法的影响

自动化与人工智能

随着自动化和人工智能技术的不断发展,企 业将能够更精确地识别和计量作业,提高成 本核算的效率和准确性。

大数据分析

大数据技术的应用将为企业提供更全面的数据支持 ,帮助企业深入挖掘作业成本信息,优化资源配置 。

云计算与物联网

云计算和物联网技术将为企业提供更灵活、 高效的数据存储和处理方式,降低作业基础 成本法的实施成本。

高成本

作业基础成本法的实施和维护可能需要大 量的资金和人力资源投入,这对于一些资 源有限的企业来说可能是一个挑战。

04

作业基础成本法在企业中的 应用

应用案例分析

案例一

某制造企业

背景介绍

该企业采用传统成本法,导致间接费用分配不合理, 产品成本信息失真。

实施过程

引入作业基础成本法,对生产过程中的各项作业进行 识别和划分,建立作业中心和作业动因。

加强企业内部培训和沟通,提高员工对作业基础 成本法的认识和应用能力。

建立科学合理的作业划分和动因确定机制,确保 成本核算的准确性和可靠性。

展望未来,随着企业竞争加剧和技术进步,作业 基础成本法将在更多行业中得到应用和推广,为 企业提供更加精细化和准确的成本信息,助力企 业持续发展。

05

作业基础成本法的未来发展

跨部门、跨组织成本管理

企业需要加强跨部门、跨组织的成本管理,以实现整体的成本优化, 作业基础成本法将更加注重跨组织的成本管理。

战略成本管理

企业需要将成本管理上升到战略高度,通过作业基础成本法实现战 略成本管理,以支持企业的战略决策。

感谢您的观看

THANKS

确定作业动因

总结词

作业量与产品或服务关联

存货管理国外学者观点

存货管理国外学者观点

国外学者对存货管理的观点主要有以下几个方面:

1. JIT(Just-in-Time)管理:JIT管理是一种精益生产理念,旨在最大程度地减少存货水平,通过准确预测需求、减少生产和交货周期,实现按需生产和交货。

国外学者普遍认为JIT管理可以降低库存成本和风险,提高生产效率和客户满意度。

2. EOQ(Economic Order Quantity)模型:EOQ模型是一种基于数学模型的存货管理方法,通过平衡订单成本和持有成本,确定最经济的订货量和订货周期。

国外学者认为EOQ模型可以帮助企业最大程度地减少库存成本,并优化供应链效率。

3. ABC(Activity-Based Costing)分析:ABC分析是一种根据存货价值和重要性进行分类和管理的方法。

国外学者认为ABC分析可以帮助企业识别和优化关键存货,提高供应链效率和利润率。

4. VMI(Vendor Managed Inventory)模式:VMI模式是一种由供应商负责存货管理和补充的模式。

国外学者认为VMI模式可以降低企业的库存风险和管理成本,提高供应链的灵活性和响应能力。

5. RFID(Radio Frequency Identification)技术:RFID技术是一种用于实时跟踪和管理存货的无线识别技术。

国外学者认为RFID技术可以提高存货管理的准确性和效率,降低存货损失和偷盗风险。

国外学者普遍认为,有效的存货管理可以降低库存成本和风险,提高生产效率和供应链的灵活性和响应能力。

他们提出了一系列的管理方法和技术,以帮助企业实现优化的存货管理。

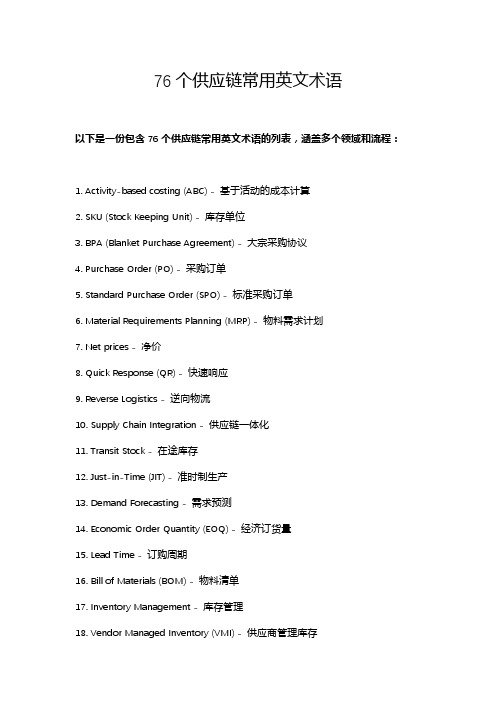

76个供应链常用英文术语

76个供应链常用英文术语以下是一份包含76个供应链常用英文术语的列表,涵盖多个领域和流程:1. Activity-based costing (ABC) - 基于活动的成本计算2. SKU (Stock Keeping Unit) - 库存单位3. BPA (Blanket Purchase Agreement) - 大宗采购协议4. Purchase Order (PO) - 采购订单5. Standard Purchase Order (SPO) - 标准采购订单6. Material Requirements Planning (MRP) - 物料需求计划7. Net prices - 净价8. Quick Response (QR) - 快速响应9. Reverse Logistics - 逆向物流10. Supply Chain Integration - 供应链一体化11. Transit Stock - 在途库存12. Just-in-Time (JIT) - 准时制生产13. Demand Forecasting - 需求预测14. Economic Order Quantity (EOQ) - 经济订货量15. Lead Time - 订购周期16. Bill of Materials (BOM) - 物料清单17. Inventory Management - 库存管理18. Vendor Managed Inventory (VMI) - 供应商管理库存19. Distribution Center (DC) - 分销中心20. Transportation Management System (TMS) - 运输管理系统21. Enterprise Resource Planning (ERP) - 企业资源规划22. Third-Party Logistics (3PL) - 第三方物流23. Fourth-Party Logistics (4PL) - 第四方物流24. Finished Goods Inventory - 成品库存25. Work in Process (WIP) - 在制品26. Cycle Counting - 循环盘点27. Cost of Goods Sold (COGS) - 销售成本28. Freight Forwarder - 货运代理29. Incoterms - 国际贸易术语解释通则30. Dock Scheduling - 码头调度31. Drop Shipping - 直接配送32. Pick and Pack - 拣选包装33. Cross-Docking - 越库作业34. Sales & Operations Planning (S&OP) - 销售与运营计划35. Customer Relationship Management (CRM) - 客户关系管理36. Total Quality Management (TQM) - 全面质量管理37. Supplier Relationship Management (SRM) - 供应商关系管理38. Return Merchandise Authorization (RMA) - 商品退货授权39. Barcode / QR Code - 条形码/二维码40. Hazardous Materials (HazMat) Handling - 危险品处理41. Cold Chain - 冷链物流42. Lean Manufacturing - 精益生产43. Six Sigma - 六西格玛44. KPIs (Key Performance Indicators) - 关键绩效指标45. Port of Origin - 起运港46. Port of Destination - 目的港47. Customs Clearance - 海关清关48. Free On Board (FOB) - 船上交货49. Cost, Insurance, and Freight (CIF) - 成本、保险费加运费50. Delivered Duty Paid (DDP) - 完税后交货51. Ex Works (EXW) - 工厂交货价52. Inbound Logistics - 入库物流53. Outbound Logistics - 出库物流54. Order-to-Cash (OTC) - 订单到收款55. Procure-to-Pay (P2P) - 采购到付款56. Global Trade Management (GTM) - 全球贸易管理57. EDI (Electronic Data Interchange) - 电子数据交换58. Takt Time - 节拍时间59. Kanban - 看板管理60. FIFO (First In, First Out) - 先进先出61. LIFO (Last In, First Out) - 后进先出62. Safety Stock - 安全库存63. Lot Size - 批量大小64. Containerization - 集装箱化65. MRP II (Manufacturing Resource Planning) - 制造资源计划66. DRP (Distribution Resource Planning) - 分销资源计划67. Drop Trailer Program - 拖车卸货计划68. Consolidation - 集拼69. Deconsolidation - 拆箱分拨70. Value-Added Services (VAS) - 增值服务71. Trade Compliance - 贸易合规72. Shipment Tracking - 运输追踪73. Carrier Selection - 承运商选择74. Multi-modal Transport - 多式联运75. Green Supply Chain - 绿色供应链76. Blockchain Technology - 区块链技术(在供应链中的应用)请注意,这并非一个详尽无遗的列表,但涵盖了供应链管理中广泛使用的许多关键术语。

ABC costing

2 作业成本法(Activity—based Costing)作业成本法(ABC)指以作业为核算对象,通过成本动因来确认和计量作业量,进而以作业量为基础分配间接费用的成本计算方法。

在ABC下,作业成本可分为四个层次的产品单位成本。

即①与生产单位产品有关的直接耗费,包括原材料、直接人工等。

该层次的作业成本与产量成正比例关系。

②生产批次成本。

即与生产批别和包装批别有关的资源耗费,包括生产某批次所需要的生产准备成本、清洁成本、质量成本等。

该层次的作业成本取决于生产批次的多少。

③产品维持成木。

即与产品种类有关的资源耗费,包括获得某种产品的生产许可、包装设计等方面的成本。

该层次的作业成本取决于产品的范围及复杂程度。

④工厂级成本。

即与维持作业生产能力有关的资源耗费,包括折旧、安全检查成本、保险等。

该层次的作业成本取决于组织规模和结构。

(1)作业成本管理的基本思想。

企业是一个为最终满足顾客需求、实现投资者报酬价值最大化而运行的一系列有密切联系的作业集合体,企业生产商品或提供劳务消耗作业,作业消耗资源,而资源消耗的同时又是价值的积累过程,最终商品或劳务既是全部作业的集合,也是全部价值的集合。

作业链同时又表现为价值链。

ABC涉及两阶段的制造费用分配过程;第一阶段,把有关生产或服务的制造费用归集互作业中心,形成作业成本;第二阶段,通过作业动因把作业成本库归集的成本分配到产品或服务中去,最终得到产出成本。

(2)作业成本法的成本计算程序。

①确认和计量耗用企业资源的成本。

将能够直观地确定为某特定产品或服务的资源成本划为直接成本,直接计入该特定产品或服务成本,其余部分则列为作业成本。

②确认和计量耗用资源的作业。

作业是指为提供服务或产品而耗用企业资源的相关生产经营管理活动。

如订单处理、产品设计、员工培训、材料处理、机器调试、质量检查、包装、销售、一般管理等。

③计量作业成本。

根据资源耗用方式的不同将间接资源成本分配给相关作业,计算出各项作业的成本,即作业成本。

时间驱动作业成本法

时间驱动作业成本法传统的作业成本计算方法往往是以作业量、作业时间或者作业单位数量作为计量依据,然后按照预算、标准成本或者固定比例进行成本分配。

然而,这种方法在实际操作过程中存在着一定的局限性。

例如,作业量和作业时间并不能完全准确地反映作业的复杂程度和资源消耗情况,导致成本计算结果不够准确。

TDABC方法通过对作业的时间分析,将成本分配关联到作业过程中实际使用的时间上,从而更加准确地计算作业的成本。

这种方法的核心思想是将作业过程分为各个环节,并通过对每个环节所需的时间进行监测和分析,以确定各个环节对总成本的消耗比例。

通过参考相关的市场数据和单价,可以将时间分配成本转化为货币金额。

TDABC方法相比传统的作业成本计算方法,有以下几个优点:1. 精确计算成本:TDABC方法通过时间分析,能够更准确地捕捉到作业所消耗的资源和支出成本,避免了传统方法中的估算误差和不准确性。

2. 简化计算过程:TDABC方法只需记录和分析作业过程中实际使用的时间,避免了传统方法中的复杂成本分析过程,降低了成本计算的难度。

3. 提高管理决策:通过更准确的成本计算,可以为企业的管理决策提供更可靠的依据。

例如,可以根据成本结构对不同作业进行优化和分配资源;可以根据成本分析结果评估作业效能和盈利能力,从而做出更合理的决策。

4. 适用范围广:TDABC方法适用于各个行业和企业规模。

无论是生产型企业还是服务型企业,无论规模大小,只要存在作业过程,都可以应用TDABC方法进行成本计算。

然而,这种方法也存在一些局限性:1. 信息收集困难:TDABC方法要求对作业过程中的时间进行详细记录和分析,需要对作业过程有较为全面的了解,但有些企业可能无法准确获取这些信息。

2. 时间成本测量误差:TDABC方法将成本分配到作业过程中使用的时间上,但是在实际操作过程中,可能存在一些不可控因素,如停机、维护和突发事件等,这些因素可能导致时间成本的测量误差。

浅析abc成本法

浅析abc成本法

ABC成本法(Activity-Based Costing),又被称为面向活动成本计算法,是一种会计识别、计量和分配过程成本的会计方法。

它扩展了传统的单一定价机制,重点关注的是产品的生产过程中的具体步骤,从而更有效地实施成本控制和管理。

ABC成本法的最大特点在于它以具体的可追溯的活动组织和工作流程为基础,分析各项活动的成本,从而进行真实的、高效的成本计算。

其中,通过识别和分析活动和成本驱动因素,以活动为基准进行成本核算,有利于发掘与费用相关联的每一步活动,实现真实有效的成本核算和管理。

ABC成本法比传统成本法拥有更多优势,即更加细致地反映不同产品所占用资源所造成的真实成本,为管理部门提供更客观、更准确的成本信息,较好地实现成本控制和监督,为预算、决策和投资等方面提供依据。

然而,尽管ABC成本法法具有诸多优势,但它更容易出现误差,耗费时间和成本,产生账务和数据处理复杂性,需要大量的历史数据作为参考。

因此,只有在适当的场景下,才有利于取得有效的控制效果。

综上所述,ABC成本法具有明显的优势,可以有效的追踪日常经营期间成本的用途,提高成本核算的准确度,加强有效的成本控制和决策依据,提高管理的灵活性和敏捷的决策能力,为企业可持续发展打下坚实的基础。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

In the traditional manufacturing environment, indirect costs constituted a relatively small proportion of total product cost compared to direct costs .But In the modern manufacturing environment, indirect costs constitute a relatively high proportion of total product cost. There are several reasons for this:

1.Modern manufacturing is characterised by shorter and more frequent production runs rather than continuous or high volume production runs.

2.With the advent of advanced manufacturing technology developed,widespread use of computer control and automation has decreased the importance and use of direct labour . Direct labour cost as a proportion of total cost has therefore declined.

3.Increased use of just-in-time production methods and customer-led manufacture has led to quality control costs and production planning costs forming a higher proportion of total cost. Traditional costing systems,which assume that all products consume all resources in proportion to their production volumes,tend to allocate too great a proportion of overheads to high volume products and too small a proportion of overheads to low volume products。

Traditional costing system is not suitable for the new economics environment any more.

ABC attempts to overcome this problem。

ABC overcomes the production cost calculation method based faults.In the method, the indirect costs allocated according to production base cost unit , and no matter whether production and indirect cost related,or if this cost drivers.The activity-based costing more accurate information.It also can change cost drivers,improve the relevant of decision-making and decrease the subjective of cost distribution. ABC also has some disadvantages.for example,in a wide variety of products in the enterprise, Distinguish activities are difficult,and cost drivers are difficult to confirm ,and the accurate is affected by certain factors.。