EXCEL第4章投资决策模型上机练习题参考答案

会计学:企业决策的基础exercises-chapter4答案

SOLUTIONS TO EXERCISESEx 4–1 a. Book valueb. Materialityc. Matching principled. Unrecorded revenuee. Adjusting entriesf. Unearned revenueg. Prepaid expensesh. None (This is an example of “depreciation expense.”)Ex. 4–2Income Statement Balance SheetAdjusting Entryab NE I D NE I Dc I NE I I NE Id NE I D NE I De NE I D D NE Df I NE I NE D IEx. 4–3 a. Rent Expense .......................................................................................... 240,000Prepaid Rent .............................................................................. 240,000 To record rent expense for May ($1,200,000 ÷ 5 months =$240,000 per month).b. Unearned Ticket Revenue ................................................................... 148,800Ticket Revenue .......................................................................... 148,800 To record earning portion of season ticket revenue relatingto May home games.Interest Payable (375)$50,000 x 9% annual rate x 1/12 = $375.(2) Accounts Receivable ...................................................................... 10,000Consulting Fees Earned .................................................... 10,000 To record ten days of unbilled consulting fees at $1,000per day.b. $2,250 ($50,000 x 9% x 6/12 = $2,250)c. $15,000 ($25,000 - $10,000 earned in December, 2002)Ex. 4–5 a. The balance of TWA’s Advance Ticket Sales account represents unearned revenue—that is, amounts collected from customers prior to rendering the relatedservices (air travel). As TWA has an obligation to render these services, theAdvanced Ticket Sales account appears among the liabilities in TWA’s balancesheet.b. TWA normally reduces the balance of this liability account by rendering services tocustomers—that is, by providing flights for which the customers have purchasedtickets. On some occasions, however, TWA reduces the balance of this liability bymaking cash refunds to customers.Interest Payable......................................................................... 1,200 To record interest accrued on bank loan during December.2. D epreciation Expense: Office Building ............................................ 1,100Accumulated Depreciation: Office Building ...................... 1,100 To record depreciation on office building ($330,000 ÷ 25years ⨯1/12 = $1,100).3. A ccounts Receivable ............................................................................ 64,000Marketing Revenue Earned .................................................... 64,000 To record accrued Marketing revenue earned in December.4. I nsurance Expense (150)Prepaid Insurance (150)To record insurance expense (1,800 ÷ 12 months = $150).5. U nearned Revenue ............................................................................... 3,500Marketing Revenue Earned .................................................... 3,500 To record portion of unearned revenue that had becomeearned in December.6. S alaries Expense .................................................................................... 2,400Salaries Payable ......................................................................... 2,400 To record accrued salaries in December.b. $62,650 ($64,000 + $3,500 - $1,200 - $1,100 - $150 - $2,400).Ex. 4–7 a. The total interest expense over the life of the note is $5,400 ($120,000 ⨯ .09 ⨯6/12 = $5,400).The monthly interest expense is $900 ($5,400 ÷ 6 = $900).b. The liability to the bank at December 31, 2002, is $121,800 (Principal, $120,000 +$1,800 accrued interest).c. 2002Oct. 31 Cash ........................................................................................ 120,000Notes Payable .......................................................... 120,000 Obtain from bank six-month loan with interest at9% a year.d. Dec. 31 Interest Expense (900)Interest Payable (900)To accrue interest expense for December on notepayable ($120,000 ⨯ 9% ⨯1/12).e. The liability to the bank at March 31, 2003, is $124,500, consisting of $120,000principal plus $4,500 accrued interest for five months.Ex. 4–8 a. May 1 Cash ........................................................................................ 300,000Notes Payable .......................................................... 300,000 Obtained a three-month loan from National Bankat 12% interest per year.May 31 Interest Expense .................................................................. 3,000Interest Payable ...................................................... 3,000 To record interest expense for May on notepayable to National Bank ($300,000 ⨯ 12% ⨯1/12 =$3,000).b. May 1 Prepaid Rent ......................................................................... 180,000Cash ............................................................................ 180,000 Paid rent for six months at $30,000 per month.May 31 Rent Expense ........................................................................ 30,000Prepaid Rent ............................................................ 30,000 To record rent expense for the month of May.c. May 2 Cash ........................................................................................ 910,000Unearned Admissions Revenue .......................... 910,000 Sold season tickets to the 70-day racing season.May 31 Unearned Admissions Revenue ....................................... 260,000Admissions Revenue .............................................. 260,000 To record admissions revenue from the 20 racingdays in May ($910,000 ⨯ 20/70 = $260,000).d. May 4 No entry required.e. May 6 Prepaid Printing .................................................................. 12,000Cash ............................................................................ 12,000 Printed racing forms for first 30 racing days.May 31 Printing Expense.................................................................. 8,000Prepaid Printing ...................................................... 8,000 To record printing expense for 20 racing days inMay.f. May 31 Concessions Receivable ..................................................... 16,500Concessions Revenue ............................................ 16,500 Earned 10% of refreshment sales of $165,000 duringMay.Something to Consider:Effects of omission of May 31 adjusting entry for rent expense on May 31 financialstatements:Revenue Not affectedExpenses Understated (by May’s rent of $30,000)Net Income Overstated (because May rent expense was not recognized)Assets Overstated (Prepaid Rent should be reduced by portion expiredin May)Liabilities Not affectedOwners’ Equity Overstated (because net income is overstated)Ex. 4–9 a. Materiality refers to the relative importance of an item. An item is material if knowledge of it might reasonably influence the decisions of users of financialstatements. If an item is immaterial,by definition it is not relevant to decisionmakers.Accountants must account for material items in the manner required by generallyaccepted accounting principles. However, immaterial items may be accounted forin the most convenient and economical manner.b. Whether a specific dollar amount is “material”depends upon the (1) size of theamount and (2) nature of the item. In evaluating the size of a dollar amount,accountants consider the amount in relation to the size of the organization.Based solely upon dollar amount, $2,500 is not material in relation to the financialstatements of a large, publicly owned corporation. For a small business however,this amount could be material.In addition to considering the size of a dollar amount, accountants must alsoconsider the nature of the item. The nature of an item may make the item“material”to users of the financial statements regardless of its dollar amount.Examples might include bribes paid to government officials, or theft of companyassets or other illegal acts committed by management.In summary, one cannot say whether $2,500 is a material amount. The answerdepends upon the related circumstances.c. Two ways in which the concept of materiality may save time and effort foraccountants are:1. Adjusting entries may be based upon estimated amounts if there is little or nopossibility that the use of an estimate will result in material error. For example,an adjusting entry to reflect the amount of supplies used may be based on anestimate of the cost of supplies remaining on hand.2. Adjusting entries need not be made to accrue immaterial amounts ofunrecorded expenses or unrecorded revenue. For example, no adjusting entriesnormally are made to record utility expense payable at year-end.Ex. 4–10 a. None (or Materiality). Accounting for immaterial items is not “wrong”or a “violation” of generally accepted accounting principles; it is merely a waste of time.The bookkeeperis failing to take advantage of the concept of materiality, which permits chargingimmaterial costs directly to expense, thus eliminating the need to recorddepreciation in later periods.b. Matching.c. Realization.Ex. 4–11 a. Accounts likely to have required an adjusting entry are:1. Investments2. Accounts Receivable3. Inventories4. Prepaid Expenses5. Deferred Income Taxes6. Buildings7. Machinery and Equipment8. Intangible Assets9. Accounts Payable10. Accrued Liabilities11. Income Taxes Payable12. Deferred Compensation and Other LiabilitiesNote to the Instructor: The adjustments required for many of the accounts listedabove are discussed in subsequent chapters. Some are beyond the scope of anintroductory course.SOLUTIONS TO PROBLEMS20 Minutes, Easy PROBLEM 4–1FLORIDA PALMS COUNTRY CLUBPROBLEM 4–1FLORIDA PALMS COUNTRY CLUB (concluded)b.1. Accruing unpaid expenses.2. Accruing uncollected revenue.3. Converting liabilities to revenue.4. Converting assets to expenses.5. Accruing unpaid expenses.6. Converting assets to expenses.7. No adjusting entry required.8. Accruing unpaid expenses.c. The clubhouse was built in 1925 and has been fully depreciated for financial accountingpurposes. The net book value of an asset reported in the balance sheet does not reflect the asset’s fair market value. Likewise, depreciation expense reported in the income statement does not reflect a decline in fair market value, physical obsolescence, or wear-and-tear.40 Minutes, Medium PROBLEM 4–2ENCHANTED FORESTPROBLEM 4–2ENCHANTED FOREST (concluded)b.1. Accruing uncollected revenue.2. Accruing unpaid expenses.3. Converting assets to expenses.4. No adjusting entry required.5. Accruing unpaid expenses.6. Accruing uncollected revenue.7. Converting liabilities to revenue.8. Accruing unpaid expenses.9. Accruing unpaid expenses.c.Income Statement Balance SheetAdjustment Revenue Expenses =NetIncome Assets = Liabilities +Owners’Equity1. I NE I I NE I2. NE I D NE I D3. NE I D D NE D4. NE NE NE NE NE NE5. NE I D NE I D6. I NE I I NE I7. I NE I NE D I8. NE I D NE I D9. NE I D NE I Dd. $340 ($12,000 x 0.85% x 4/12)e. Original cost of buildings .......................................................................................$600,000Accumulated depreciation: buildings (prior to adjusting entry 3 inpart a) ...........................................................................................................................$310,000 December depreciation expense from part a ..................................................2,000Accumulated depreciation, buildings, 12/31 ...................................................(312,000) Net book value at December 31 ..........................................................................$288,00025 Minutes, Strong PROBLEM 4–3SEA CATa. (1) Age of the catamaran in months = accumulated depreciation÷monthly depreciation.Useful life is given as 10 years, or 120 months.Cost $46,200 ÷ 120 months = $385 monthly depreciation expense.Accumulated depreciation of $9,240 ÷ $385 monthly depreciation = 24 months.(2) Tickets used in June (14)5Tickets outstanding on June 30 ($825÷ $15) (55)Tickets sold to resort hotel on June 1 (20)(3) Prepaid rent of $6,000 ÷ 5 months remaining = $1,200 monthly rentalexpense.(4) $1,400 x 12/8 = $2,100 original cost.Since 4 months of the 12-month life of the policy have expired, the $1,400 ofunexpired insurance applies to the remaining 8 months. This indicates a monthly costof $175, computed as $1,400 ÷ 8. Therefore, the 12-month policy originally cost$2,100, or 12 x $175.30 Minutes, Medium PROBLEM 4–4CAMPUS THEATERPROBLEM 4–4CAMPUS THEATER (concluded)b. (1) Eight months (bills received January through August). Utilities bills are recorded asmonthly bills are received. As of August 31, eight monthly bills should have beenreceived.(2) Seven months (January through July). Depreciation expense is recorded only inmonth-end adjusting entries. Thus, depreciation for August is not included in theAugust unadjusted trial balance.(3) Twenty months ($14,000 $700 per month).c. Corporations must pay their income taxes in several installment payments throughout theyear. The balance in the Income Taxes Expense account represents the total amount ofincome taxes expense recognized since the beginning of the year. But Income TaxesPayable represents only the portion of this expense that has not yet been paid. In theexample at hand, the $4,740 in income taxes payable probably represents only the income taxes expense accrued in July, as Pickwood should have paid taxes accrued in the first two quarters by June 15.50 Minutes, Strong PROBLEM 4–5KEN HENSLEY ENTERPRISES, INC.PROBLEM 4–5KEN HENSLEY ENTERPRISES, INC. (continued)c. Monthly rent expense for the last two months of 2002 was $2,000 ($6,000 ÷ 3 months). The$21,000 rent expense shown in the studio’s trial balance includes a $2,000 rent expense for November, which means that total rent expense for January through October was $19,000 ($21,000 - $2,000). The monthly rent expense in these months must have been $1,900($19,000 ÷ 10 months). Thus, it appears that the studio’s monthly rent increased by $100 (from $1,900 to $2,000) in November and December.15 Minutes, Medium PROBLEM 4–6KOYNE CORPORATION。

EXCEL第4章投资决策模型课件例题

1 2 3 4 5 6 7 8 910111213141516171819202122232425262728293031323334353637383940A B C D E F G H I面值发行价格期限计息方式第1年利率第2年利率第3年利率国债A1001005年固定利率 4.15% 4.15% 4.15%国债B100825年贴现利率国债C1001005年变动利率8.00% 6.00% 4.00%国债A国债B国债C初始投资金额100000100000100000每百元面值的单价可购买的面值第0年第1年第2年第3年第4年第5年净现值内部报酬率贴现率最大净现值实现该净现值最大值的项目【例4-11】某投资者现有10万元进行国债投资,若假定现有三个国债品种可供投资。

国债A面值100元,发行价格100元,期限5年,按固定利率计息,每年利率为4.15%每年付息一次,最后按面值还本;国债B面值100元,发行价格82元,期限5年,按贴现利率计息,最后按面值还本付息;国债C面值100元,发行价格100元,期限5年,按变动利率计息,各年的利率分别是:8%、6%、4%、2%、0%,最后按面值还本;试建立一个决策模型,当投资者使用的贴现率等于1%-5%范围内,模型能给出这三个国债品种中最优的投资品种。

1 2 3 4 5 6 7 8 910111213141516171819202122232425262728293031323334353637383940J K L M N O P Q第4年利率第5年利率还本付息方式4.15% 4.15%一年付息一次最后还本到期按面值支付2.00%0.00%一年付息一次最后还本R 12345678910111213141516171819202122232425262728293031323334353637383940。

智慧树知到《Excel经管应用》章节测试【完整答案】

智慧树知到《Excel经管应用》章节测试【完整答案】智慧树知到《Excel经管应用》章节测试【完整答案】智慧树知到《Excel经管应用》章节测试答案第一章1、下列不属于EXCEL主要功能的是 ( )A:排序与筛选B:数据图表C:分析数据D:文字处理正确答案:文字处理2、用Excel创建一个学生成绩表,要按照班级统计出某门课程的平均分,需要使用的方式是( )A:分类汇总B:排序C:合并计算D:数据筛选正确答案:分类汇总3、根据特定数据源生成的,可以动态改变其版面布局的交互式汇总表格是( )A:数据透视表B:数据的筛选C:数据的排序D:数据的分类汇总正确答案:数据透视表4、用Excel可以创建各类图表,如条形图、柱形图等。

为了显示数据系列中每一项占该系列数值总和的比例关系,应该选择( )图表。

A:条形图B:柱形图C:饼图D:折线图正确答案:饼图5、下列有关Excel排序错误的是( )A:可按日期排序B:可按行排序C:最多可设置32个排序条件D:可按笔画数排序正确答案:最多可设置32个排序条件第二章1、微观经济学的中心问题是国民收入决定理论。

A:对B:错正确答案:错2、降低价格一定会使供给量下降。

A:对B:错正确答案:错3、卖者提高价格肯定会增加单位产品的收益。

A:对B:错正确答案:错4、市场经济的协调机制是价格。

A:对B:错正确答案:对5、Excel中的需求曲线生成前提是输入给定的需求函数。

A:对B:错正确答案:对6、市场出清在Excel中的表现是需求和供给两条曲线相交。

A:对B:错正确答案:对7、微观经济学的中心理论是( )。

A:国民收入理论B:国民收入决定理论C:价值理论D:价格理论正确答案:价格理论8、经济学理论或模型是( )A:对经济发展的预测B:基于一系列假设以及由这些假设推导出来的结论C:凭空产生的D:一些数学等式正确答案:基于一系列假设以及由这些假设推导出来的结论9、需求函数Qd=800-100P在Excel中表现为( )。

excel在财务管理中的运用第4章常用财务函数

4.3.3 年金中的利息函数IPMT() IPMT(rate,nper,pv, fv,type) rate——各期利率 nper——付款期总数 pv——现值, fv——终值,缺省为0 Type_0为期末,可缺省;1为期初。

4.4 期数函数NPER( )

NPER(rate,pmt,pv,fv,type)

4.2.1 PV函数

◦ 1) 整收整付款项的复利现值 ◦ 2) 年金现值

4.2.2 NPV函数

1.净现值= 项目价值–投资现值 = 产出–投入

= 未来现金净流量现值–原始投资额现值

——将未来现金流入一一折现,同当前的现金流出作比较

若净现值为正数,则投资项目可行

0 1 2 3 若净现值为负数,则投资项目不可行 8%

而且支付及收入的时间都发生在期末。

4.3 年金、本金和利息函数

4.3.1年金函数PMT( ) PMT(rate,nper,pv, fv,type) rate——各期利率 nper——付款期总数 pv——现值, fv——终值,缺省为0 Type_0为期末,可缺省;1为期初。

某企业借入长期借款100000元,期限为5年,借款 利率为固定利率,年利率为6%:

A/(1+i)n-1

2

n-1

n

...

A

A

A: 每年现金流

PA=A+A/(1+i)+A/(1+i)2+…+A/(1+i)n-1

[ ] 1-(1+i)-(n-1)

=A

+1

i

2024/6/19

预付年金现值系数和普通 年金现值系数的关系:

期数-1,系数+1 11

例:若某企业年初准备改进工艺引入一台新设备,公司有2种选择:直接购 买和融资租赁,直接购买需要马上支付现金13000元,租赁则需要每年年 初支付2000元,连续租赁10年,企业应如何选择?假设社会平均回报率为 8%

excel统计分析与决策课后答案

excel 统计分析与决策课后答案【篇一:excel 统计分析与决策课程论文】目对校园两岸超市经营现状的分析姓名xxx 学号30901115092 专业班级国贸092 指导教师樊丽淑分院经济与贸易分院完成日期2011 年 5 月31 日课题组成员孙宝家张晓斌汪立力分工情况:问卷发放:孙宝家张晓斌汪立力数据整理:孙宝家张晓斌汪立力调研报告的填写:孙宝家张晓斌汪立力第一部分(问卷设计及问卷收集):孙宝家第二部分():第三部分(第四部分():调研报告的汇总:孙宝家张晓斌调研报告的审核:汪立力对宁波理工学院两岸超市经营现状的满意度分析一、问卷设计及问卷收集(一)问卷设计1. 问卷设计思路本次问卷是面向在校的的全体学生,本调查问卷对象针对07 届、08 届、09 届10届的学生。

设计问卷前,我们主要从两个方面做问卷设计的准备工作。

第一,我们仔细分析了学院两岸超市的经营现状,以及其员工对该超市的归属感。

第二,同时动员小组各成员向各届学生询问其购物时所遇到的问题。

对于问卷调查对象的人数的选择,我们限定在全体学生之间,问卷采用随机发放的方式,通过回收汇总调查问卷,得到的汇总结果见下表 1.1 :表 1.1 问卷对象的分布课为使设计的问卷具有合理性和有效性,在问卷正式发放之前,征询一些老师和同学的建议,对问卷的部分研究内容进行了一些修正;修改问卷中的一些表达和提问方式,删除和补充一些内容,修改后的调查问卷可见附录。

2.问卷设计结构本次问卷由 4 部分组成,大致内容如下:第一部分是被调查者的基本信息,涉及被调查者的性别、年级、和对主题的了解程度。

第二部分第三部分是对两岸超市的促销方式与被关注度的分析,第四部分是对两岸超市的服务质量及效率的分析,以及不满意的原因的选择,后面还有选做题写出被调查者的自己的看法和建议。

3 .问卷的收集(1)问卷收集方法本次所有调查问卷是通过有小组队员每人负责15 张问卷以直接发放的方式进行。

财务管理能力训练与测试单元四项目投资决策答案

财务管理能力训练与测试单元四项目投资决策答案单元四项目投资决策模块一认识现金流量三、基本知识训练(一)单项选择题:①B ②D ③A ④D ⑤A ⑥B ⑦C ⑧A ⑨D ⑩A(二)多项选择题:①ABD ②AB ③AB ④ABC ⑤ABD ⑥ABC(三)判断及改错题:①错②错③错④错⑤对⑥对四、基本能力训练能力训练一:年折旧=200÷5=40净利润=(80-30-40)×(1-25%)=7.5项目投产后第一年的现金净流量=净利润+折旧=7.5+40=47.5(万元)能力训练二:年折旧=(320-20)÷10=30净利润=(350-180-30)×(1-25%)=105经营期净现金流量=净利润+折旧=105+30=135则项目各年的净现金流量为:NCF0=-320万元,NCF1=0,NCF102=135万元,NCF11=155万元五、综合能力训练年折旧=(110-10)÷10=10无形资产年摊销=20÷5=4经营期前5年每年的净利润=(40-38)×(1-25%)=1.5经营期前5年每年的净现金流量=净利润+折旧+摊销=1.5+10+4=15.5(万元)经营期后5年每年的净利润=(60-40-10)×(1-25%)=7.5经营期后5年每年的净现金流量=净利润+折旧=7.5+10=17.5(万元)则项目各年的净现金流量为:NCF0=-75万元, NCF1=-55万元, NCF2=-20万元NCF7-3=15.5万元, NCF11-8=17.5万元, NCF12=47.5万元模块二学会项目投资的评价与决策三、基本知识训练(一)单项选择题:B ?C ?A ?D ?B ?B ?A ?C ?B ?B ⑴C ⑵B ⑶C(二)多项选择题ABC ?CD ?ABCD ?ACD ?ABCABD ?ABCD ?ABCD ?AD ?BC(三)判断及改错题错 ?错 ?对 ?错 ?对对 ?错 ?对 ?错 ?对四、基本能力训练能力训练一:(1)甲方案的静态投资回收期=50÷16=3.125年乙方案的静态投资回收期=4-1÷16=3.9375年因企业要求的投资回收期为2年,而两个方案的投资回收期均大于此标准,所以,两个方案均不可行。

excel上机考试题和答案

excel上机考试题和答案**Excel上机考试题和答案**一、单项选择题(每题2分,共20分)1. 在Excel中,以下哪个函数用于计算一组数据的方差?A. SUMB. AVERAGEC. VARIANCED. COUNT答案:C2. Excel中,哪个功能可以快速对数据进行排序?A. 筛选B. 查找和替换C. 数据透视表D. 排序答案:D3. 在Excel中,如何插入一个图表?A. 点击“插入”选项卡,然后选择“图表”B. 点击“插入”选项卡,然后选择“图片”C. 点击“插入”选项卡,然后选择“形状”D. 点击“插入”选项卡,然后选择“文本框”答案:A4. Excel中,哪个功能可以合并多个单元格?A. 格式刷B. 查找和选择C. 合并并居中D. 清除答案:C5. 在Excel中,如何快速复制一个单元格的格式到另一个单元格?A. 使用格式刷B. 使用查找和替换C. 使用粘贴特殊D. 使用剪切和粘贴答案:A6. Excel中,哪个函数用于计算一组数据的标准差?A. SUMB. AVERAGEC. STDEVD. COUNT答案:C7. 在Excel中,如何快速填充一个序列?A. 使用自动填充手柄B. 使用查找和替换C. 使用数据透视表D. 使用排序答案:A8. Excel中,哪个功能可以进行数据的分类汇总?A. 数据透视表B. 数据透视图C. 筛选D. 排序答案:A9. 在Excel中,如何设置单元格的边框?A. 使用“开始”选项卡中的“边框”按钮B. 使用“插入”选项卡中的“形状”工具C. 使用“页面布局”选项卡中的“打印区域”工具D. 使用“公式”选项卡中的“名称管理器”答案:A10. Excel中,哪个函数用于计算一组数据的平均值?A. SUMB. AVERAGEC. COUNTD. MAX答案:B二、多项选择题(每题3分,共15分)1. 在Excel中,以下哪些操作可以改变单元格的格式?A. 改变字体大小B. 改变单元格颜色C. 改变单元格边框D. 改变单元格的行高答案:A, B, C2. Excel中,哪些函数可以用来计算一组数据的总和?A. SUMB. AVERAGEC. COUNTD. SUMIF答案:A, D3. 在Excel中,以下哪些操作可以插入一个图片?A. 点击“插入”选项卡,然后选择“图片”B. 点击“插入”选项卡,然后选择“图表”C. 点击“插入”选项卡,然后选择“形状”D. 点击“插入”选项卡,然后选择“文本框”答案:A4. Excel中,哪些功能可以对数据进行筛选?A. 数据透视表B. 筛选C. 查找和替换D. 排序答案:A, B5. 在Excel中,以下哪些操作可以插入一个公式?A. 点击“公式”选项卡,然后选择“插入函数”B. 直接在单元格中输入等号“=”C. 点击“插入”选项卡,然后选择“形状”D. 点击“插入”选项卡,然后选择“文本框”答案:A, B三、判断题(每题1分,共10分)1. 在Excel中,可以通过按“Ctrl+C”复制选中的单元格,然后按“Ctrl+V”粘贴到其他位置。

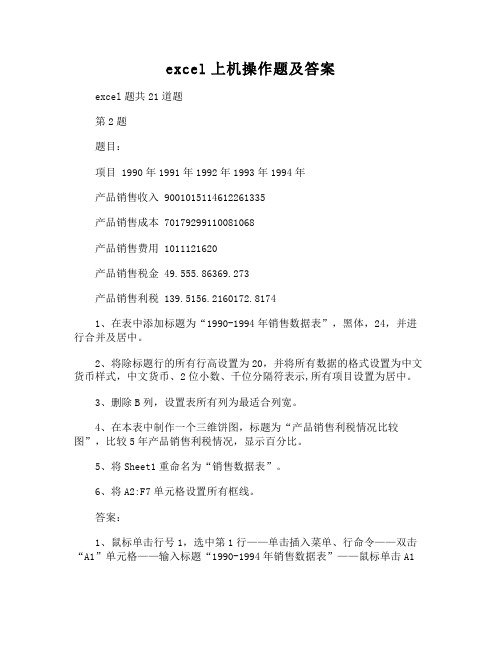

excel上机操作题及答案

excel上机操作题及答案excel题共21道题第2题题目:项目 1990年1991年1992年1993年1994年产品销售收入 9001015114612261335产品销售成本 70179299110081068产品销售费用 1011121620产品销售税金 49.555.86369.273产品销售利税 139.5156.2160172.81741、在表中添加标题为“1990-1994年销售数据表”,黑体,24,并进行合并及居中。

2、将除标题行的所有行高设置为20,并将所有数据的格式设置为中文货币样式,中文货币、2位小数、千位分隔符表示,所有项目设置为居中。

3、删除B列,设置表所有列为最适合列宽。

4、在本表中制作一个三维饼图,标题为“产品销售利税情况比较图”,比较5年产品销售利税情况,显示百分比。

5、将Sheet1重命名为“销售数据表”。

6、将A2:F7单元格设置所有框线。

答案:1、鼠标单击行号1,选中第1行——单击插入菜单、行命令——双击“A1”单元格——输入标题“1990-1994年销售数据表”——鼠标单击A1单元格——格式工具栏,字体列表中选择黑体、字号选24号字——按住鼠标左键拖动选择A1:G1单元格区域——单击格式单元格合并及居中按钮2、按住鼠标拖动选择A2:G7单元格区域——选择“格式”菜单、“行”命令、“行高”——在“行高”对话框中输入20 ——确定——按住鼠标左键拖动选择C3:G7单元格区域——选择格式菜单、单元格命令——选择“数字”选项卡——分类项选“货币”——“小数位数”框中输入2、“货币符号”选择中文货币符号¥——确定——格式工具栏单击居中按钮3、鼠标右击选中B列——选择删除——按住鼠标左键拖动选择A1:F7单元格区域——选择格式菜单、列命令、最适合的列宽4、按住鼠标左键拖动选择A2:F2单元格区域——再按住Ctrl键+鼠标左键拖动选择A7:F7单元格区域——单击常用工具栏上的“图表向导”按钮──在图表向导对话框中,图表类型选“饼图”——“子图表类型”中选“三维饼图” ——单击下一步——在图表数据源,单击“数据区域”项右侧按钮——拖动鼠标选择A2:F2单元格区域——再按住Ctrl键+鼠标左键拖动选择A7:F7单元格区域——再单击右侧按钮——“系列产生在”项选“行” ——单击下一步——“标题”选项卡、“图表标题”项输入“产品销售利税情况比较图”——“数据标志”选项卡、选“显示百分比” ——单击下一步——内容默认即可——单击完成5、鼠标双击工作表名称Sheet1——重命名为“销售数据表” ——回车6、按住鼠标左键拖动选择A2:F7单元格区域——选择格式菜单、单元格命令、单击“边框”选项卡——“预置”中选择“外边框”和“内部” ——确定1第1题题目: A B1 姓名2 张文远3 刘明传4 李敏峰5 陈丽洁6 戴冰寒7 何芬芳8 秦叔敖9 马美丽10 叶长乐11 白清风12 韩如雪13 方似愚14 胡大海15 常遇春16 赵高怀1、添加标题“×××公司销售数据表”,合并及居中A1至C1单元格;2、设置销售额数据为中文货币、2位小数、千位分隔符表示;3、在C2单元格输入“销售比率%”;4、利用公式计算每人销售额占总销售额的百分比(保留一位小数);5、在本表中制作一个簇状柱形图,比较每个人的销售额情况;7、将A2:C17区域的外框设置红色粗线,内部为红色细线。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

102205.64 102205.64 102205.64 102205.64 102205.64 102205.64 102205.64 102205.64 102205.64 102205.64

0 102205.64 10220.56 214631.84 21463.18 338300.66 33830.07 474336.36 47433.64 623975.63 62397.56 788578.83 78857.88 969642.35 96964.24 1168812.22 116881.2 1387899.08 138789.9 1628894.63

当前房价 房价上升率 投资收益率 年限 购买时房价 每年存入金额

1000000 5% 10% 10 1628894.63 102205.64年ຫໍສະໝຸດ 年初存款余额年存入金额

年收益

年末存款余额

1 2 3 4 5 6 7 8 9 10

0 102205.64 214631.84 338300.66 474336.36 623975.63 788578.83 969642.35 1168812.22 1387899.08

额金钱存入(投入)一种收益率为10%的投资项目,准备在10年末将存 款全部取出来支付当时的房价。要求:

(1) 在单元格D7与D8中分别求出10年后购买时的房价与购房人每年

应存入的金额

(2)基于D8中的数据,在H3:N13的动态模拟表的各个单元格中键入正

确公式以求出该人每年向投资项目存入的金额、从该投资项目得到(并 继续投入到该项目中去)的年收益、每年年初与年末的存款余额以及每

年末房价

【习题4-3】某人准备在10年后购买一套必须全额现金支付的住房,该

住房当前房价为1000000元,预计房价每年上涨5%,购房人每年将等

1050000.00 1102500.00 1157625.00 1215506.25 1276281.56 1340095.64 1407100.42 1477455.44 1551328.22 1628894.63

年末的房价(利用这个计算表来确认10年末的存款余额正好可以支付当

时所需的购房款)。