期权期货及其衍生产品约翰赫尔官方课件-PPT精选文档

hull (期权 期货及其他衍生品)官方ppt1

Examples of Futures Contracts

Agreement to:

Buy 100 oz. of gold @ US$900/oz. in December (NYMEX) Sell £62,500 @ 2.0500 US$/£ in March (CME) Sell 1,000 bbl. of oil @ US$120/bbl. in April (NYMEX)

Options, Futures, and Other Derivatives, 7th International Edition, Copyright © John C. Hull 2008 7

Profit from a Long Forward Position

Profit

K

Price of Underlying at Maturity, ST

Options, Futures, and Other Derivatives, 7th International Edition, Copyright © John C. Hull 2008 15

1. Oil: An Arbitrage Opportunity?

Suppose that:

- The spot price of oil is US$95 - The quoted 1-year futures price of oil is US$125 The 1-year US$ interest rate is 5% per annum The storage costs of oil are 2% per annum

期权期货及其衍生产品约翰赫尔官方课件97522共21页

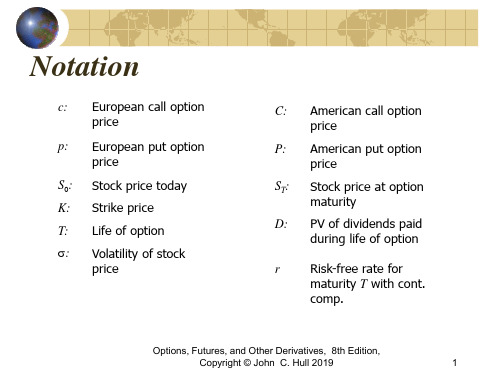

c: European call option price

p: European put option price

S0: Stock price today K: Strike price T: Life of option s: Volatility of stock

price

C: American call option price

ST > K ST − K

K ST 0 ST ST

ST < K 0 K K

K− ST ST K

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

9

The Put-Call Parity Result (Equation

P: American put option price

ST: Stock price at option maturity

D: PV of dividends paid during life of option

r Risk-free rate for maturity T with cont. comp.

(Equation 10.5, page 221)

p Ke -rT–S0

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

7

Put-Call Parity: No Dividends

Cc Pp

Options, Futures, and Other Derivatives, 8th Edition,

期权期货及其衍生产品约翰赫尔官方课件共29页

Copyright © John C. Hull 2019

2

Mechanics of Put Futures Option

When a put futures option is exercised the holder acquires

A short position in the futures A cash amount equal to the excess of the strike price over the futures price at the time of the most recent settlement

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

1

Mechanics of Call Futures Options

When a call futures option is exercised the holder acquires

A long position in the futures A cash amount equal to the excess of the futures price at the time of the most recent settlement over the strike price

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

6

Potential Advantages of Futures Options over Spot Options

期权期货及其衍生产品约翰赫尔官方课件97522PPT精品文档21页

Copyright © John C. Hull 2019

2

Effect of Variables on Option Pricing (Table 10.1, page 215)

Variable

c

p

C

P

S0

+

−

+

−

K

−

+

−

+

T

?

?

+

+

s

+

+

+

+

r

+

−

+

Байду номын сангаас

−

D

−

+

−

+

Options, Futures, and Other Derivatives, 8th Edition,

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

11

Arbitrage Opportunities

Suppose that

c= 3 T = 0.25 K =30

Copyright © John C. Hull 2019

5

Lower Bound for European Call Option Prices; No Dividends (Equation 10.4, page 220)

c S0 –Ke -rT

Options, Futures, and Other Derivatives, 8th Edition,

期货期权及其衍生品配套课件(全34章)Ch03.ppt

Options, Futures, and Other Derivatives, 7th International

Edition, Copyright © John C. Hull 2008

7

Short Hedge

Options, Futures, and Other Derivatives, 7th International

Edition, Copyright © John C. Hull 2008

8

Choice of Contract

Choose a delivery month that is as close as possible to, but later than, the end of the life of the hedge When there is no futures contract on the asset being hedged, choose the contract whose futures price is most highly correlated with the asset price. This is known as cross hedging.

Options, Futures, and Other Derivatives, 7th International

Edition, Copyright © John C. Hull 2008

6

Long Hedge

We define

F1 : Initial Futures Price F2 : Final Futures Price S2 : Final Asset Price If you hedge the future purchase of an asset by entering into a long futures contract then

(NEW)赫尔《期权、期货及其他衍生产品》教材精讲讲义

(NEW)赫尔《期权、期货及其他衍生产品》教材精讲讲义简介赫尔的《期权、期货及其他衍生产品》是一本经典的金融学教材,被广泛用于大学金融学课程的教学。

本文档将对该教材进行精讲,涵盖主要内容和关键概念,旨在帮助读者深入理解和掌握期权、期货及其他衍生产品领域的知识。

本文档采用Markdown格式,方便阅读和使用。

第一章:期权市场简介1.1 期权的定义和特点期权是一种金融衍生工具,它赋予持有者在未来某个时间以特定价格买入或卖出某一标的资产的权利。

期权的特点包括灵活性、杠杆作用、风险限定和多样性等。

1.2 期权市场的组织和参与者期权市场包括交易所市场和场外市场。

交易所市场由交易所组织和管理,参与者包括期权合约买方、卖方、证券公司和交易所监管机构等。

1.3 期权定价模型期权定价模型是评估期权价格的数学模型,常用的模型包括布莱克-斯科尔斯模型和基于风险中性定价的模型。

第二章:期权定价理论2.1 基本期权定价理论基本期权定价理论包括不含股息的欧式期权定价、含股息的欧式期权定价以及美式期权定价等。

2.2 期权市场交易策略期权市场交易策略包括买入期权、卖出期权、期权组合以及期权套利等。

2.3 隐含波动率与期权定价隐含波动率是指根据期权市场价格反推出的波动率水平,它对期权价格的波动具有重要影响。

第三章:期权交易策略3.1 期权买入策略期权买入策略包括买入认购期权、买入认沽期权和买入期权组合等,旨在获得价差和方向性收益。

3.2 期权卖出策略期权卖出策略包括卖出认购期权、卖出认沽期权和卖出期权组合等,旨在获取权利金收入和时间价值消耗。

3.3 期权组合策略期权组合策略包括多头组合和空头组合,以及各种组合的调整和套利策略。

第四章:期货市场简介4.1 期货合约的基本特点期货合约是一种标准化的合约,约定了在未来某个时间以特定价格交割特定数量的标的资产。

4.2 期货交易所和市场参与者期货交易所是组织和管理期货市场的机构,市场参与者包括期货合约买方、卖方、交易所监管机构和期货经纪人等。

[考研专业课课件]_赫尔《期货、期权及其他衍生产品》_课件_第22章__估计波动率和相关系数

目标是估计当前波动率σn的水平,因此将较大的

权重用在最近的数据更有意义。

模型:

m

2 n

i uni 2

(22-4)

i 1

αi——第i天以前观察值所对应的权重,α

取正值

如果i>j,则αi<αj,将较少的权重给予较

旧的数据。权重之和必须为1,即ARCH(m)模型。

推广式(22-4)

假定存在某一长期平均方差,并且应当给予

σn2——方差率(variance rate)

Si——市场变量在i天末的价格

ui——在第i天连续复利收益率 σn2的无偏估计为

ui

ln

Si Si 1

:

2 n

1 m 1

m i 1

2

uni u

(22-1)

u ——ui的平均值

u

1 m

m

uni

i 1

:

为了监测日方差率的变化:

令w=γVL,可以将式(22-5)写成

m

2 n

i uni 2

(22-6)

i 1

式(22-4)及式(22-5)是后两节中将讨论

的两种测算波动率的重要方法的基础。

22.2 指数加权移动平均模型 指数加权移动平均模型(EWMA)是式(22-4) 的一个特殊形式,其中权重αi随着时间以指数速 度递减,具体地讲,αi+1=λαi,其中λ是介于0 与1之间的某一常数。在以上特殊假设下,更新波 动率公式被简化为

GARCH(1,1)与EWMA模型类似,其不同之处 是除了对过去的u2权重按指数下降的同时,对于 长期平均浮动率赋予了一定的权重。

赫尔《期权期货及其他衍生产品》第1章(第八版)讲述

期权、期货及其他衍生产品(第八版) Copyright © John C. Hull 2012

32

对冲基金( 见业界事例1-2,p8)

• 对冲基金受到的约束与共同基金不同,一般不对外公 布持有的证券组合。

• 共同基金必须

– 披露投资策略 – 在任意时刻允许份额赎回 – 杠杆率受到限制 – 不能持有空头头寸

20

2. 石油:另外一种套利机会?

假定:

- 石油的即期价格为95美元 - 1年期原油期货的标价为80美元 - 1年期的美元利率为 5% - 原油的储存成本为每年2%

是否存在套利机会?

期权、期货及其他衍生产品(第八版) Copyright © John C. Hull 2012

21

期权

• 看涨期权:其持有者有权在将来某一特定时间 以某一确定价格( 执行价格)买入某种资产。

卖出价 1.4411 1.4413 1.4415 1.4422

期权、期货及其他衍生产品(第八版) Copyright © John C. Hull 2012

8

远期价格

• 合约的远期价格是今天约定的合约支付价 格(使合约价值为零的支付价格);

• 对不同期限的远期合约而言,远期价格也 不同(如表1-1所示) 。

期权、期货及其他衍生产品(第八版) Copyright © John C. Hull 2012

34

期权、期货及其他衍生产品(第八版) Copyright © John C. Hull 2012

23

表1-2 谷歌股票看涨期权在2010年6月15日的价格

(P6)

执行 2010年7月

价格

买入价

2010年7月 卖出价

2010年9月 买入价

期权、期货及其他衍生产品第9版-赫尔】Ch(9)幻灯片PPT

Options, Futures, and Other Derivatives, 9th Edition, Copyright ©

John C. Hull 2014

4

Historical Simulation to Calculate the One-Day VaR

Create a database of the daily movements in all market variables. The first simulation trial assumes that the percentage changes in all market variables are as on the first day The second simulation trial assumes that the percentage changes in all market variables are as on the second day and so on

Let vi be the value of a variable on day i

There are 500 simulation trials

The ith trial assumes that the value of the market

variable tomorrow is

v500

vi vi1

期权、期货及其他衍生产品第9 版-赫尔】Ch(9)幻灯片PPT

本PPT课件仅供大家学习使用 请学习完及时删除处理 谢谢!

Options, Futures, and Other Derivatives, 9th Edition,

Copyright © John C. Hull 2014

期权期货及其衍生产品约翰赫尔官方课件

Options, Futures, and Other Derivatives, 8th Edition, Copyright © John C. Hull 2012

9

First Scenario for the Example:

Table 18.2 page 384

Week 0 Stock price 49.00 Delta 0.522 Shares purchased 52,200 Cost (‘$000) 2,557.8 Cumulative Cost ($000) 2,557.8 Interest 2.5

Relationship Between Delta, Gamma, and Theta (page 393)

For a portfolio of derivatives on a stock paying a continuous dividend yield at rate q it follows from the Black-ScholesMerton differential equation that

Options, Futures, and Other Derivatives, 8th Edition, Copyright © John C. Hull 2012

11

Theta

Theta (Q) of a derivative (or portfolio of derivatives) is the rate of change of the value with respect to the passage of time The theta of a call or put is usually negative. This means that, if time passes with the price of the underlying asset and its volatility remaining the same, the value of a long call or put option declines

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

2

Day Count Conventions in the U.S. (Page 129)

Treasury Bonds: Actual/Actual (in period)

Bond: 8% Actual/ Actual in period.

4% is earned between coupon payment dates. Accruals on an Actual basis. When coupons are paid on March 1 and Sept 1, how much interest is earned between March 1 and April 1?

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

10

Conversion Factor

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

4

Examples continued

T-Bill: 8% Actual/360:

8% is earned in 360 days. Accrual calculated by dividing the actual number of days in the period by 360. How much interest is earned between March 1 and April 1?

Cash price = Quoted price + Accrued Interest

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

8

Treasury Bond Futures

Pages 132-136

P 360 (100 Y ) n

Y is cash price per $100 P is quoted price

Options, Futures, and Other Derivatives, 8th ion,

Copyright © John C. Hull 2019

7

Treasury Bond Price Quotes in the U.S

Chapter 6 Interest Rate Futures

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

1

Day Count Convention

Defines:

the period of time to which the interest rate applies The period of time used to calculate accrued interest (relevant when the instrument is bought of sold

Bond: 8% 30/360

Assumes 30 days per month and 360 days per year. When coupons are paid on March 1 and Sept 1, how much interest is earned between March 1 and April 1?

Corporate Bonds: 30/360

Money Market Instruments:

Actual/360

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

3

Examples

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

5

The February Effect (Business Snapshot 6.1)

How many days of interest are earned between February 28, 2019 and March 1, 2019 when

day count is Actual/Actual in period? day count is 30/360?

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

6

Treasury Bill Prices in the US

Cash price received by party with short position = Most recent settlement price × Conversion factor + Accrued interest

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2019

9

Example

Most recent settlement price = 90.00 Conversion factor of bond delivered = 1.3800 Accrued interest on bond =3.00 Price received for bond is 1.3800×90.00+3.00 = $127.20 per $100 of principal