会计英语UnitTwo

会计英语-东北财经大学出版社 孙坤编著

会计英语复习范围一、翻译(英译汉,汉译英各10个,每个1分)Accounting 会计,会计学 accountant 会计师,会计人员 governmental and institutional accounting 政府和事业单位会计 public utilities 公共事业 assurance services 鉴证服务stakeholder 利益相关者deferrals 递延项目replacement cost 重置成本matching principle 配比原则 income statement 损益表、利润表 accounting equation 会计等式或会计平衡式 retained earnings 留存收益 net income 净收益 source document 原始凭证 general ledger 总分类账 subsidiary ledger 明细分类账 trial balance 余额试算表 work sheet 工作底稿或工作底表 cash receipts 现金收入 cash payment 现金支出 prepaid expenses 预付费用unearned revenues 预收收入accrued expenses 应计费用accrued revenues 应计收入dividend 股利 economic performance 经济成果,经营成果 gross profit 销售毛利 raw material 原材料 treasury stock 库存股、库藏股 stock options 股票认购权 plant and equipment 厂场设备,固定资产 principal 本金 operating cash flows 经营活动资金流量disclosure notes 报表附注accounting policies 会计政策 savings accounts 储蓄账户owners’ equity 所有者权益 original investment 初始投资 stock split 股票分割 cost accounting 成本会计 cost centre 成本中心 job costing 订单成本计算法 contract costing 合同成本计算法activity based costing 作业成本法management accounting 管理会计standard costing 标准成本法 cost behavior 成本习性、成本形态 International Accounting Standards committee(IASC)国际会计准则委员会 transnational financial reporting 跨国企业财务会计 auditing 审计 analytical procedures 分析性程序 standard audit report 标准审计报告 unqualified opinion 无保留意见 adverse opinion 否定意见 disclaimer of opinion 拒绝表示意见 qualified opinion 保留意见 internal control 内部控制 Risk Management 风险管理 Corporate government 公司治理 Capital Budget 资本预算 GAAP(Generally Accepted Accounting Principles)一般公认会计原则二、多选(10个,每个2分)1. Accounting assumptions. 会计假设⑴Separate entity assumption.会计主体假设⑵Going concern assumption.持续经营假设⑶Accounting-period assumption.会计分期假设⑷Monetary unit assumption.货币计量假设2. Accounting recognition and measurement principles 会计确认和计量原则⑴Cost principle. 历史成本原则⑵Matching principle. 配比原则⑶Conservatism. 谨慎性原则⑷Materiality.重要性原则⑸Differentiate capital and revenue.划分资本性支出和收益性支出⑹Substance over form. 实质重于形式3. External users of accounting information are not directly involved in running the organization. Almost all of us are users of accounting information. They include shareholders, lenders, directors, customers, suppliers, regulators, lawyers, brokers, and the press. 会计信息外部使用者不直接参与组织与组织的经营管理,我们所有的人几乎都使用会计信息。

会计英语课件 Unit 2 The Journals

Debit 24,000

Credit 24,000

1,000

1,000

Unit Two The Journals

4 General Journal

Preview question: 1 What is the definition general journal?

Details in the Journal

Unit Two The Journals

22 Details in the Journal

Preview question: 1 What does general journal and special journal have in common?

Definition of Journals

Definition of Journals

An accounting journal may be one of a group of special journals or it may be a general journal. The general journal is a relatively simple record in which any type of business transaction can be recorded. A special journal is used to group similar types of transactions, such as all sales of merchandise on account, or all cash receipts, etc. the types of special journals used depend largely on the types of transaction that occur frequently in a business enterprise. In an accounting system, it is inefficient to record all transactions in the general journal, so we use special journal. .

chapter 2 journals and ledgers 会计英语 第二章 日记账与分类账

Example of a Dividend Voucher Shareholder Name: Shareholders Name Shareholder Address: Town Postcode Number of Ordinary Shares Dividend Payment ? Dividend Tax Credit? XX xxxx xxxx Directors Name Director

2.2 -2.3

EXAMPLES --I

1. In June 2007, Dogwood Limited pays $400 for a one-year fire insurance policy that becomes effective 1 July 2007. The insurance premium provides coverage during one year, and should be recognized as a 2008 expense. Expense recognition is deferred until 2008. 2. At the start of the year the company receives subscriptions of 240 000 and has promised to send out magazines for twelve months. 3. A lawyer receives an advance of $2500 from a client for future services. The revenue will not be earned until a later date when services are performed. Recognition of revenue is deferred until the service has been performed.

会计英语——用英语了解会计的定义和运用

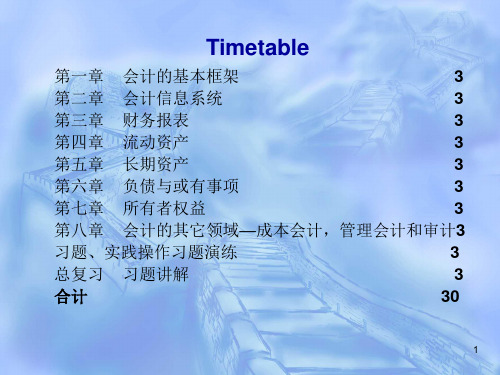

第一章 会计的基本框架

3

第二章 会计信息系统

3

第三章 财务报表

3

第四章 流动资产

3

第五章 长期资产

3

第六章 负债与或有事项

3

第七章 所有者权益

3

第八章 会计的其它领域—成本会计,管理会计和审计3

习题、实践操作习题演练

3

总复习 习题讲解

3

合计

30

1

Chapter 1

I. New words: 1. Account n. statement of money paid or owed for goods or services --The accounts show a profit of $9000. Open/close an account、account payable, account receivable, On account (1) pay part of the money (2)on credit --I will give you$30 on account. --buy things on account.

bank account -- Credit $8 to a customer / an account. Credit n. (1)permission to delay payment for goods and

services --No ~ is given at this shop. Payment must be in

prediction. --There is a lack of ~ between his promises

and his actions. ~ college, ~ column, ~course, ~school Corresponding a. more or less the same ~ fingerprints, the ~ period last year

会计英语备课教案

会计英语备课教案《会计英语》备课教案Unit OneI. Preview Q:What is accounting?Is it different with bookkeeping?II. Language Points:1. Accounting: 会计,会计学 Accountancy: 英国⽤词,与accounting词义相同Accountant: 会计员,会计师 Account: 账户,会计科⽬Oxford Dictionary of Accounting: The process of identifying, measuring, recording, and communicating economic transactions. Measurement is normally made in monetary terms.Textbook: Accounting is an information system necessitated by the great complexity of modern business.会计是由于现代企业的巨⼤复杂性⽽成为必要的信息系统Textbook: Accounting is often described as an information system. It isthe system that measures business activities, processesinformation into reports and communicates these findings todecision makersDong Cai Textbook: Accounting is a process of recording, classifying, summarizing, and interpreting of those business activities that can be expressed in monetary terms. 2.Specialize: 专门研究 n. Specialist: 专家3.Qualified: adj.1) Having the appropriate qualifications for an office, a position, or a task. 有资格的Are you qualified to doctor? 你有资格当医⽣吗?2) Limited, restricted, or modified 有限的,受限制的,有条件的She gave qualified agreement. 她表⽰有条件的同意。

会计英语复式记账法

Answer:

b.Increase an asset and increase owner’s equity

• Why do accountants record transactions in the journal?( )

a.To ensure that all transactions are posted to the ledger b.To ensure that total debits equal total credits c.To have a chronological record of all transactions d.To help prepare the financial statemens

• The accounting equation shows the relationship among assets, liabilities, and owner’s equity.(23-2) • The double-entry system is based on the principle of duality, which means that all events of economic importance have two aspects-effort and reward, sacrifice and benefit, source and use-that offset or balance each other.(25-1) • In actual practice, accountant records transactions first in a book called the Journal.(29-1)

Answer:

c.To have a chronological record of al equation The accounting equation shows the relationship among assets, liabilities, and owner’s equity. Assets appear on the left-hand side of the equation. The legal and economic claims against the assets-the liabilities and owner’s equity appear on the right-hand side of the equation: Assets=Liabilities + Owner’s Equity

会计英语课件1

Unit 2 accounting cycle会计英语Accounting Equation and Double Entry会计等式与复式记账法The financial condition or position of a business enterprise is represented by the relationshipof assets to liabilities and capital.一个企业的财务是由资产对负债和资本的关系来表示的。

Assets are properties that are owned and have monetary value; for instance, cash, inventory, buildings, equipments.资产是指企业所拥有的、具有货币价值的财产,如现金、存货、建筑物、设备。

Liabilities are amounts owned to outsiders, such as notes payable, accounts payable, bonds payable. Liabilities may also include certain deferred items, such as income taxes to be allocated.负债是欠外部的数额,如应付票据、应付账款、应付债券。

负债还可以包括某些递延的项目,如待分配的所得税。

Capital is the interest of the owner in an enterprise. Also known as owner’s equity.资本是企业所有者的利益,也称之为业主权益。

These three basic elements are connected by fundamental relationship called balance-sheet equation, sometimes called simply the accounting equation.This equation expresses the equality of the assets on one side with the claims of the creditorsand owners on the other side:Assets = Liability + Capital.这三个基本的要素由一个叫做资产负债表等式、有时称之为会计等式的关系式联系起来。

会计英语词汇

会计英语词汇 Prepared on 22 November 2020C h a p t e r 1 Accounting 会计,会计学Accountant 会计师,会计人员Accounting information 会计信息Financial data 财务数据Business 企业,经营,商业,业务Business transaction 经济业务,经济交易Enterprise 企业Economic information 经济信息Business organization 经济组织Financial activity 财务活动,筹资活动Profitability 获利能力,盈利能力End product 最终产品Creditor 债权人Performance 业绩Favorable 有利的Unfavorable 不利的Accounting system 会计系统,会计制度Financial condition 财务状况Investor 投资人Result of operations 经营成果Financial report 财务报告To make decision 制定决策Accounting principles 会计原则Business activity 经济活动Accounting concepts 会计概念Financial accounting 财务会计Economic unit 经济单位Owner 业主,拥有者Governmental agency 政府机构Generally accepted accounting principles 公认会计原则Employ 采用Prepare 准备,编制Annual report 年度报告Stockholder 股东Audit 审计,审查,查帐Auditing 审计,审计学Accounting records 会计记录Public accountant 公共会计师Fairness 公正性,公允性Reliability 可靠性Periodic audit 定期审计Corporation 股份有限公司Internal auditor 内部审计人员Cost accounting 成本会计Cost data 成本数据Management accounting 管理会计Selling price 销售价格Management advisory service 管理咨询服务Management service 管理服务Tax accounting 税务会计Tax returns 纳税申报单,税单Budgetary accounting 预算会计International accounting 国际会计International trade 国际贸易Not-for-profit accounting 非盈利组织会计Not-for-profit organization 非盈利组织Social accounting 社会会计Measurement 计量Chapter2Accounting practice 会计实务Accounting theory 会计理论Decline 方针,指南Assumption 假设Business entity 经济主体Accounting entity 会计主体Economic activity 经济活动Bookkeeping 簿记Double-entry bookkeeping system 复试记账系统Entry分录,记录Single proprietorship独资Partnership合伙Accounting purpose会计目的Separate entity独立主体Asset资产Going-concern持续经营Historical cost历史成本Current market value 当前市场价值Accounting period会计期间Stable-monetary-unit货币计量单位Objective principle客观性原则Operating result经营成果Cost principle成本原则Actual cost实际成本Book value账面价值Equivalent当量,约当量Depreciation折旧Consistency principle一贯性原则Accounting method会计方法Financial statement 财务报告Comparability可比性Materiality principle重要性原则Conservatism principle谨慎性原则Revenue收入Expense费用Cost of goods商品成本Net income净收入Net loss净损失Accrual-basis 权责发生制Cash-basis 现金收付制Journal 日记账Realization principle 实现原则Matching principle 配比原则Recognize 确认Transfer转让,转帐,过户Income statement收益表,损益表Full-disclosure principle充分揭示原则Chapter3Accounting element会计要素Accounting equation会计等式Liability负债Owner s’ equity业主权益,所有者权益Current asset长期资产Long-term asset长期资产Operating cycle 经营周期Bank deposit 银行存款Short-term investment短期投资Long-term investment长期投资Accounts receivable应收账款Note receivable应收票据Prepayment 预付款项Inventory 存货Fixed asset 固定资产Plant and equipment 厂房和设备Intangible asset 无形资产Store fixtures店面装置Office equipment办公设备Delivery equipment运输设备Creditors’ equity债权人权益Obligation责任,义务Debt债务Current liability流动负债Long-term liability长期负债Short-time loans payable应付短期贷款Long-term loans payable长期应付贷款Notes payable应付票据Accounts payable应付账款Accrued expense应计费用Bonds payable应付债券Long-term accounting payable长期应付账款Interest 股份,利息Claim 要求权Net assets 净资产Capital资本Stockholder’s equity 股东权益Cost of goods sold 商品销售成本Administrative expenses 管理费用Selling expenses销售费用Financial expense 财务费用Occur 发生Dividend payable 应付股利Retained earnings留存收益Chapter4Classification分类,分级Day-to-day 随时Account title 账户名称Ledger 分类帐Debit side 借方Credit side 贷方Charge借记,收取费用Memorandum 摘要,备忘录Insert 插入,嵌入,写入Cash on hand 库存现金subgrouping子目,细目supplies 物料用品prepaid expenses 预付费用face value 面值check 支票bank draft 银行汇票money order 汇款单debtor 债务人bearer 持票人salaries payable 应付工资taxes payable 应付税费interest payable 应付利息long-term notes payable 长期应付票据mortgage payable 应付抵押借款bonds payable 应付公司债券drawing提款income summary收益汇总professions fees职业服务费commissions revenues 佣金收入interest income利息收入chart of accounts账户一览表executive salaries主管人员薪金office salaries办公人员薪金sales salaries销售人员薪金prepaid rent预付租金accumulated depreciation累计折旧depreciation expense折旧费用sales销售收入sales returns and allowance销售退回与折让purchases returns and allowance购买退回与折让Chapter5Accounting cycle会计循环Accounting procedures会计程序,会计方法Trial balance试算平衡表Post-closing trial balance结算后试算平衡表Journalize 做分录,记账Post to the ledger过入分类帐Assemble汇集Work sheet工作底表Adjusting entry调整分录close结账,结清,关闭ledger accounts分类账户general ledger总分类帐two-column account两栏式账户source document原始凭证check stub支票存根journal日记帐journal entry日记帐分录records(book) of original entry原始记录簿transcribe抄录post过账,誊帐manually手工的chronological按时间顺序的enter登记,计入general journal普通日记账special journal特殊日记帐sales journal销售日记帐purchases journal购买日记帐cash receipts journal现金收入日记帐cash disbursements journal现金支出日记帐division of labor分工Chapter6Adjusting procedures调整程序Accrual(basis) accounting权责发生制Align调整,使成一线,(转做)使一致Apportion(按比例)分配,摊配Accrue自然积累(如利息等),计提Outlay支出Expire期满,耗尽,失效Insurance expense保险费用Prepaid insurance 预付保险费Supplies expense物料用品费Supplies on hand在用物料Subscription预订Deferred credit递延贷项Accrued salaries payable应计应付工薪Accrued revenue应计收入Closing entry结账分录Closing procedure结账程序Temporary account临时性账户,名义账户,虚账户Permanent account 永久性账户,实账户Withdrawals提款Statement of cash flow现金流量表Financial position财务状况Portray描绘Dispose处理Inflows流入Outflows流出Chapter7Working paper工作底稿Adjusted trial balance调整后试算平衡表Cross-reference交叉参考Occasion需要,机会,工作场合Salaries accrued应计薪金Combine结合,联合Extend(会计)将数字转入。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

►2 Attention: ►material means important enough to

influence the decisions of statement users. ► Large/ small/ differ significantly/ nature

十二 Substance over form

►

Assets: lowest

► Liabilities: highest

十一 Materiality convention

►1 Definition: record and report separately only those transactions which are material.

五 Objectivity convention

the accounting records and reports be base upon objectivity evidence.

六 Relevance

► if accounting information is to be of any use, it must be relevant for its intended use.

transactions from its own viewpoint. ►3 In other words, the business is viewed as

an entity separate from its owners, creditors, or other stakeholders.

a particular type of transaction are the same from one period to the next. ►2 Uniformity ► requires that companies in the same industry use the same accounting policies and procedures.

十三 Cost convention

►1 Definition: enter the exchange price into the accounting records.

►2 The cost principle provides guidance primarily at the initial acquisition date.

十 Conservatism convention

► accountants act conservatively or prudently in the measurement of profit.

► (reasonable pessimism)

► Revenue: ceble

二 Going-concern convention (continuity convention)

►1 Definition: the entity will remain in operation for the foreseeable future.

►2 the assumption of continuity is made in the absence of evidence to the contrary.

三 Monetary convention

►1 Definition: an entity’s transactions are recorded in the monetary unit of the country in which it is operating. (economic data be recorded in dollars)

七 Reliability

►1 Truthfulness (validity) ►2 Verifiability ►3 Neutrality

八 Understandability 九 Comparability

►1 Consistency: ► implies that the accounting procedures for

►2 Financial statements are presented in the currency of the country where the reports are published

四 Accounting period convention (Time-period)

measure the result of an entity’s operation over a relatively short period and to present a Balance Sheet at frequent intervals.

一 Accounting Entity convention

►1 Definition: ► the smallest unit of activity with a self-

contained accounting system. ►2 Characteristic: ► each accounting entity interprets

Unit Two

GAAP

Generally Accepted Accounting Principle

(FASB develop it)

Learning Objectives

►Understand the definition, terms, characteristic, difficulties of each accounting conventions.( if they have)