货物运讲义输保险

货物运输保险培训讲义课件

•31

•货物运输保险培训讲义

•32

•货物运输保险培训讲义

•33

•货物运输保险培训讲义

•34

•11

•货物运输保险培训讲义

•12

•货物运输保险培训讲义

•13

•货物运输保险培训讲义

•14

•货物运输保险培训讲义

•15

•货物运输保险培训讲义•16•Fra bibliotek物运输保险培训讲义

•17

•货物运输保险培训讲义

•18

•货物运输保险培训讲义

•19

•货物运输保险培训讲义

•20

•货物运输保险培训讲义

•货物运输保险培训讲义

•1

•货物运输保险培训讲义

•2

•货物运输保险培训讲义

•3

•货物运输保险培训讲义

•4

•货物运输保险培训讲义

•5

•货物运输保险培训讲义

•6

•货物运输保险培训讲义

•7

•货物运输保险培训讲义

•8

•货物运输保险培训讲义

•9

•货物运输保险培训讲义

•10

•货物运输保险培训讲义

•21

•货物运输保险培训讲义

•22

•货物运输保险培训讲义

•23

•货物运输保险培训讲义

•24

•货物运输保险培训讲义

•25

•货物运输保险培训讲义

•26

•货物运输保险培训讲义

•27

•货物运输保险培训讲义

•28

•货物运输保险培训讲义

•29

•货物运输保险培训讲义

•30

•货物运输保险培训讲义

运输管理讲义ppt课件

• • • • • •

运输质量事故的赔偿 1、提出赔偿 2、赔偿规定 3、赔偿支付 货运质量监督管理办法 1、督促经营者建立健全货运质量管理的 规章制度; • 2、监督货运业者建立和完善质量保证体 系; • 3、加强货运质量的监督检查

运输结点

• 在运输系统网络中,连接运输线路的结 节之处称为结点或节点。 • 主要功能: • 1、衔接功能 • 2、信息功能 • 3、管理功能 • 运输结点主要有:铁路车站、汽车站、 港口、航空港和管道站等。

运输服务与创新—运输质量管理

• 运输质量监督是指运输行政管理机构对运输质量进行检查 监督等活动。目的是为了促使货物运输经营提供安全、及时、 经济,方便的货物运输服务最大限度地满足用户的运输需要。 • 运输质量事故:是指货物承运责任期内发丢失、短少、变 质、污染、损坏、误期、错运,以及由于工作失职、借故刁难、 敲诈勒索等,造成的不良影响和经济损失等现象。 • 汽车运输质量事故分类: • 1、重大事故,3000元上损失,或经省级有关部门鉴定为珍 贵、尖端、保密物品的货物发生灭失、损坏的; • 2、大事故,3000—500元损失; • 3、一般事故,500—50元损失; • 4、小事故,50—20元损失。

运输服务与创新—服务特征和服务方式

• 服务的定义:为满足顾客需要,在同顾客的接触中,供方 的活动和供方活动的结果。 • 服务特征: • 1、服务产品具有无形性; • 2、服务的生产和消费不可分离; • 3、服务具有不可存储性; • 4、服务是不包括所有权转让的特殊形式的交易活动。 • 服务方式: • 1、服务人员与顾客面对面的接触服务; • 2、服务人员与顾客的设备之间的接触服务; • 3、服务提供的设备与顾客之间的接触的服务; • 4、服务提供方的设备与顾客的设备之间的接触服务。 • 运输服务是属于第四种服务。

国际海上货物运输保险-讲义

CHAPTER 3 INTERNATIONAL MARINE INSURANCE第三章国际海上货物运输保险法[Aims and Requirements] This chapter is aimed to help the students to have a basic knowledge concerning the international marine insurance, including the conclusion of contract, principles of insurance, insurance policy, liabilities of the insurer and marine insurance clauses.Section A. Contract of Marine Insurance第一节海上保险合同[Main Content]I. Contract of Marine InsuranceA contract of marine insurance is a contract whereby the insurer undertakes, as agreed, to indemnify the loss to the subject matter insured and the liability of the insured caused by perils covered by the insurance against the payment of an insurance premium by the insured.II. Certain Terminologies1. Insurer (underwriter)2. Insured3. Insurable Interest4. Applicant for Insurance5. Subject-matter insured6. Insurance accident7. Insured amountIII. Basic Principles of Marine Insurance1. Principle of Insurable Interest(1) The meaning of insurable interestAn insurable interest refers to the interest which the applicant has in the subject matter of the insurance and is recognized by laws. The subject matter of the insurance refers to either to the property of the insured and related interests associated therewith, or to the life and body of the insured, which is the object of the insurance.(2) The significance of insurable interest2. Principle of Utmost Good Faith(1) The Meaning of utmost good faithA positive duty to voluntarily disclose, actually and fully, all facts material to the risk being proposed, whether asked for them or notInsurance Law: “any insurance activity shall be in conformity with laws and administrative regulations and shall be conducted voluntarily under the principle of utmost good faith”.(2) Representations and warranties(3) Breach of the doctrine of Utmost Good Faith3. Principle of Indemnity(1) The meaning of Indemnity“Indemnity can be defined as exact financial compens ation. It is sufficient to place the insured in the same financial position after a loss as he can enjoy the benefit before it occurs.”In other words, when claims occur in property insurance, the insurer will pay the claims to the insured if the damage or loss is covered by the policy conditions.(2) Measurement of indemnity(3) Factors limiting the payment of indemnity4. Principle of Proximate Cause(1) The Meaning of proximate cause“Proximate cause is an active and efficient cause that sets a trai n of events in motion and brings about a result. If there are several causes operating simultaneously, the proximate one will be the dominant or the most forceful one operating to bring a result.(2) Occurrence of trains of event(3) How do we determine the efficient cause?IV. The Conclusion of Marine Insurance ContractV. Insurance Policy1. Function of the Policy2. Assignment of the Policy3. Floating Policy & Open Cover[Key Points and Difficult Points]1. Insurable Interest2. Utmost Good Faith3. Open Cover[Questions]1. Describe different types of insurable interests.2. What is utmost good faith?3. What are the functions of Policy?Section B. Obligation of the Insurer and Insured第二节保险人与被保险人的义务[Main Content]I. Obligations of the Insured1. The insured shall pay the premium immediately upon conclusion of the contract.2. The insured shall notify the insurer in writing immediately where the insured has not complied with the warranties under the contract.3. Upon the occurrence of the peril insured against, the insured shall notify the insurer immediately and shall take necessary and reasonable measures to avoid or minimize the loss.II. Liability of the Insurer1. The insurer is responsible for the issue of insurance policy.2. The insurer shall indemnify the insured promptly after the loss from a peril insured against has occurred.3. But the insurer is not liable for the loss or damage rising from any of the following causes:(1) Delay in the voyage or in the delivery of cargo or change of market price;(2) Fair wear and tear, inherent vice or nature of the cargo;(3) Improper packing.III. Perils under Marine Insurance1. Natural calamitiesSuch as weather, thunder and lighting, tidal wave, earthquake, floods, etc.2. Fortuitous accidentsSuch as ship stranded, striking upon the rocks, ship sinking, ship collision, colliding with icebergs, fire, explosion, etc.3. Extraneous risksThis cover theft, rain, shortage, leakage, breakage, dampness, etc. They may include special risks, such as war risks, strikes, non-delivery of cargo, refusal t receive cargo, etc.IV. Losses covered by Marine Insurance1. Total loss(1) Actual total loss(2)Constructive total loss2. Partial loss(1) General Average(2) Particular Average[Key Points and Difficult Points]1. Obligations of the insured2. Liability of the insurer3. Constructive total loss4. General Average5. Abandonment[Questions]1. What is abandonment? Does the insurer have the obligation to accept abandonment?2. What are the differences between actual total loss and constructive total loss?3. What does General Average refer to? Please give an example.Section C Marine Insurance Clauses第三节海上保险合同条款[Main Content]I. Marine Insurance Clauses1. London Institute Cargo Clause (ICC)(1) Institute Cargo Clause A(2) Institute Cargo Clause B(3) Institute Cargo Clause CEXCLUSIONS2. PICC Ocean Marine Cargo ClausesAccording to the stipulat ions of the People’s Insurance Company of China, the following basic insurance covers are available in marine insurance:(1) Free From Particular Average (FPA)Under FPA the insurance company will be resposible to pay claims for total or constructive total losses suffered by the whole lot of cargoes during transportation due to such natural calamities as vile weather, thunder and lighting, tidal wave, earthquakes, and floods, ot for total or partial losses due to the ship or carrier being on fire, stranded, sinking, colliding or meeting other fortuitous accidents.(2) With Particular Average (WA)The cover of this insurance is more extensive. The insurer is liable, in addition to the total or constructive total losses covered by FPA insurance, also for the partial losses of the insured goods due to the risks caused by natural calamities not mentioned under FPA.(3) All RisksUnder an “all risks” policy the goods are insured against all risks, e.g. from natural calamities, fortuitous accidents at sea, or general extraneous risks, irrespective of percentage of loss, total or partial. A natural deterioration of perishable goods, delay, loss or damage caused by inherent vice nature of the subject matter are not covered.EXCLUSIONSPICC Cargo Clauses do not cover:(1) Loss or damage caused by the intentional act or fault of the Insured.(2) Loss or damage falling under the liability of the consignor.(3) Loss or damage arising from the inferior quality or shortage of the insured goods prior to the attachment of this insurance.(4) Loss or damage arising from normal loss, inherent vice or nature of the insured goods, loss of market and/or delay in transit and any expenses arising therefrom.(5) Risks and liabilities covered and excluded by the Ocean Marine Cargo War Risks Clauses and Strike, Riot and Civil Commotion Clauses.3. War Risks Clause & Strike Risks Clause(1)Institute Cargo Clause-War(2) Strike ClauseII. Commencement and Termination of Cover (warehouse to warehouse) seagoing vessel at the final port of discharge before they reach the above mentioned warehouse or place of storage. If prior to the expiry of the above mentioned sixty (60) days, the insured goods are to be forwarded to a destination other than that named in the Policy, this insurance shall terminate at the commencement of such transit.[Key Points and Difficult Points]1. FPA2. WA3. All Risks[Questions]1. When will the Cover be terminated?2. What is Free From Particular Average?。

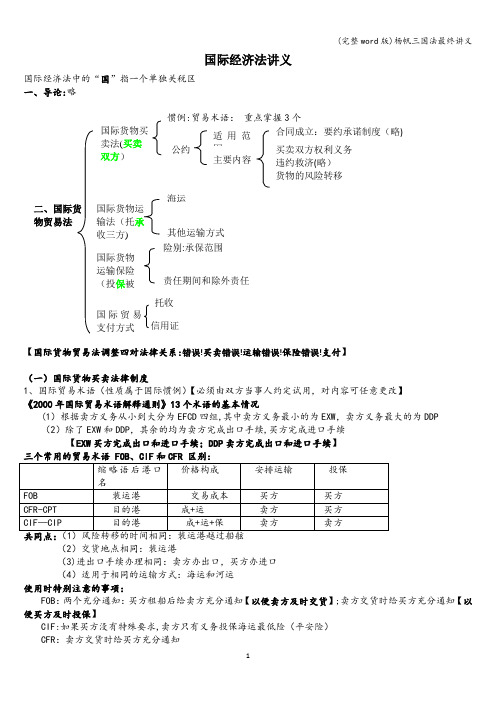

(完整word版)杨帆三国法最终讲义

2、贸易救济措施 (1)反倾销措施 A、条件:进口产品存在倾销、对国内产业造成(实质)损害、因果关系【实质损害:实质损害的威胁或相关

的损

5

失;

(完整 word 版)杨帆三国法最终讲义 信用证欺诈例外原则(最初在美国司法实践中提出):在银行付款或承兑以前,发现确凿证据,买方可以请 求法院向银行颁发止付令 (8) 2005年《最高人民法院关于审理信用证纠纷案件若干问题的规定》: 核心内容:提高了信用证欺诈例外原则适用的门槛

在银行(包括开证行、议付行、保兑行以及其他经授权的银行)付款或承兑以前,发现确凿证据(申请 人应当提供担保),(开证申请人、开证行或其他利害关系人)可以请求法院(必须是有管辖权的法院)向银 行颁发止付令 时间限制:法院接受止付信用证项下款项的申请后,须在48小时内作出裁定 (9)UCP600(2007年7月1日生效)对UCP500的修改: A、取消了可撤销信用证的内容; B、明确议付是对单据和票据的买入行为;兑付是信用证下除议付以外的一切与支付有关的行为; C、明确银行处理单据的时间为不超过收单翌日起第5个工作日; D、明确银行拒付时,可以自行联系开证申请人,如接到开证申请人放弃不符点的通知,银行可以释放单据 【出现单证、单单不符时,决定权在银行】

【在运输关系中,可以提单追究当事人责任,不受合同相对性的限制】 ★ 海运单:适用于短途运输的一种不可流通转让、不具有物权凭证作用的书面海运单据【仍有合同证明, 交货凭证的作用】 提单的种类: (1)根据签发提单的时候货物是否已装船:已装船提单和收货待运提单【船方未收到货先签发提单】 (2)根据提单上有无不良批注:清洁提单和不清洁提单 (3)根据收货人抬头不同:记名提单、不记名提单、指示提单【凭托运人指示】

(4)适用于相同的运输方式:海运和河运

保险结构市场与运作讲义(PPT 43张)

服务体系:保证保险经营的科学性和市场运行 的公正性 成熟的保险市场必须建筑在能够提供各种配套 服务的科学系统之上,为保险展业提供可靠的 基础性服务

监控体系 目的:保证市场正常高效率地运行,规范市场 主体活动、维护有序竞争、保护消费者的利益 四个层次: 政府主管机关的监督管理 行业自律组织相互之间的约束和监督 基础服务机构 社会公共监督

特征: 参加相互保险社的成员之间互相提供保险 相互保险社无股本 相互保险社保险费采取事后分摊制,事先并不确定 相互保险社最高管理机构是社员选举出来的管理委员会

(四) 保险合作社 由一些对某种风险具有同一保障要求的人,自愿集股设 立的保险组织。

特点: 由社员共同出资入股设立的,加入保险合作社的社员必 须交纳一定金额的股本。 只有保险合作社的社员才能作为保险合作社的被保险人, 但是社员也可以不与保险合作社建立保险关系。 业务范围仅局限于社员,只承保合作社社员的风险。 采取固定保险费制,事后不补交。

三、保险供求均衡 指一定时间点上,保险产品的需求量与供应量正好相等 的状态。这种均衡一般包括总量均衡和结构均衡,后者 是指不同种类保险供求量的均衡。

四、保险市场的种类

(一)按照承保的风险性质分类

财产保险市场:可细分为财产损失保险、责任 保险和信用保证保险三个子市场。 人身保险市场:可细分为人寿保险、医疗健康 保险和养老年金保险等若干子市场。

(二)按照风险交易的层次分类 原保险市场:保险人和被保险人之间从事风险交易、实 现风险分散和经济补偿保障的市场,属于风险交易的初 级市场或一级市场 再保险市场:保险人之间实现承保风险再分散、再交易 的市场,是风险交易的二级市场或次级市场 保险证券市场:在承保风险证券化的基础上所形成的各 种保险证券发行和交易的市场,将发展成为现代保险业 不可缺少的“第三级市场”

海上货物运输保险讲义课件(ppt 88页)

• 所作牺牲具有特殊性,支出的费用是额外的, 是为了解除危险,而不是由危险直接造成的;

• 牺牲和费用的支出最终必须是有效的,也就 是说经过采取某种措施后船舶和/或货物全部

或一部分最后安全抵达航程的终点港或目的 港,从而避免了船、货同归于尽的局面。

课件 制作者:张袆

12海上风险

进

单独海损

出 口

单独海损(particular

取了救助措施并获得成功而向其支付

的报酬,保险人对这种费用也负责赔

偿。

课件 制作者:张袆

19

进

外来风险

出

口

一般外来风险是指被保险货物在运输途中实由 于 受偷 潮窃 受、热雨、淋串、味短 、量 生、 锈玷 等污 一、 般渗 外漏来、原破因碎所、造务

成的风险损失。

特殊外来风险是指由于战争、罢工、交货不

到、拒收、政府禁令等特殊外来原因所造成 的风险损失。

达到合同约定年龄、期限承担给予保险责任的

商业保险行为。按保险标的(subject matter

insured)的不同,保险种类可分为:

财产保险:如国际货物运输保险

责任保险:如产品责任保险

信用保险:如出口信用保险 人身保险:如寿险

课件 制作者:张袆

4

进

国际货物运输保险种类 出

口

国际货物运输保险因运输方式不同分为实:

沉。由于在投保时,没有加保战争险,不能

取得保险公司的赔偿。买方为此向卖方提出

索赔,理由是,卖方明知海湾有战事公海上

不平安,而没有投保战争险,致使买方利益

受损。

课件 制作者:张袆

32

保险案例1分析

进 出

口

[案例分析]

实

物流职业经理人运输管理(6-7章)

第六章 运输商务管理

本章知识要点一览表

主要运输单证(各种单证的性质、作用、种类、内容和使用等) 运输合同的含义及特征 运输合同及管理 运输合同的订立和履行 运输合同的变更和解除 运 输 商 务 运输纠纷及其处理 运输合同管理 保险的意义和作用 与运输相关的保险 货物运输保险 海运货物保险保障的范围 我国海运货物保险的险别与保险条款 陆上运输货物保险条款 航空运输货物保险条款 运输代理制

海运货物保险保障的范围#

• 海上风险;(自然灾害承保范围,意外事 (自然灾害承保范围, 故承保范围) 故承保范围) • 海上损失与费用; • 外来原因所引起的风险损失。(一般外来, (一般外来, 特殊外来) 特殊外来)

管 理

货物运输代理

国际货运代理

主要运输单证

• • • • • • 铁路运输单证 道路运输单证 水路运输单证(主要是班轮运输单证) 航空运输单证 集装箱运输单证 多式联运单证

铁路运输单证(#性质 性质P327) 性质 )

• 铁路运单(重点!) 铁路运单(重点!) • 货票:具有财务性质 财务性质的货运单据 财务性质 • 国际铁路货物联运单:国际铁路联运中使 国际铁路联运中使 用 • 承运货物收据:通往港澳地区的铁路运输 通往港澳地区的铁路运输 使用

• 在运输组织中推行合同运输,要抓好以下 几方面工作:

– 建立健全货运合同管理制度,实现货运合同管 理制度化; – 加强合同运输的推广工作; – 运政管理部门应对合同运输进行监督检查; – 运政管理部门应将合同履行情况进行定期检查。

保险的意义和作用#选择题 选择题

• 从社会观点分析:保险是一种经济补偿 经济补偿 制度,它按约定的合同 约定的合同计收保险费。 制度 约定的合同 • 从法律观点分析:保险是一种补偿性 补偿性的 补偿性 契约关系。

零担货物运输讲义

任务一 整车货物运输的组织

一、公路整车货物运输与零担货物运输的主要区别 整车货物运输与零担货物运输相比,虽然主要是货物计费数量上的不同, 然而作业过程却简单得多。在作业流程方面的主要区别是: 1.在接收货物形式方面,整车货物运输是整车(批)货物接收;而零担 货物运输是零星地接收。 2.在是否直达运输方面,整车货物运输多数是直达运输,货物从发货地 直接到收货地仓库,没有入库储存保管环节;而零担货物运输是接收每个客 户的货物后,入库保管,等待一定时间货物凑足整车或到达一定时间后,才 装车运送。 3.在装车环节,整车货物运输是整车整装,而零担运输往往要有分拣、 组配和拣选环节。 4.在是否需要押运方面,整车货物运输的部分货物如活的动植物和贵重 物品的运输等,需要押运;而零担货物运输一般不需要押运。 5.在收付款方式方面,整车货物运输多数是预交部分运杂费(3070%),交付货物前结算清楚;多数零担运输是先交清运杂费后实施货物运 输。

任务一 公路货物运输 任务1 整车货物运输的组织 任务2 零担货物运输的组织

◆知识能力目标 ¤掌握汽车整车货物运输与零担货物运输的主要区别 ¤了解汽车整车货物运输生产过程 ¤学会签订公路货物运输合同 ¤清楚公路整车货物运输的作业流程,学会组织公路整车货物 运输 ¤养成严谨的工作作风,良好的职业操守;具有人际沟通和团 队合作协调能力。

3到达站站务工作 货物在到达站发生的各项货运作业统称为到达站站务 工作。到达站站务工作主要包括货运票据的交接,货 物卸车、保管和交付等内容。车辆装运货物抵达卸车 地点后,收货人或车站货运员应组织卸车。卸车时, 对卸下货物的品名、件数、包装和货物状态等应作必 要的检查。 整车货物一般直接卸在收货人仓库或货场内,并由收 货人自理。收货人确认卸下货物无误并在货票上签收 后,货物交付即完毕。货物在到达地向收货人办完交 付手续后,才告完成该批货物的全部运输过程。

国际货运代理责任及其责任保险概述(PPT32页)

国际货运代理责任及其责任保险概述( PPT32页)培 训课件 培训讲 义培训ppt教程 管理课 件教程ppt 国际货运代理责任及其责任保险概述( PPT32页)培 训课件 培训讲 义培训ppt教程 管理课 件教程ppt

3) 建立评估机构

4) 制定管理程序

根据实际情况制定一套风险管理程序,并 严格按照这个程序进行操作。同时,不 断地进行风险管理的培训,增强大家的 风险意识,尤其是各级领导的风险管理 观念与知识,以克服风险管理的短期行 为,实现风险管理的标准化、程序化、 规范化。此外,风险管理尚需发挥团队 精神,只有这样才能从根本上提高企业 抵抗风险的能力。

国际货运代理的除外责任

除外责任,又称免责,是指根据国家法律、国际 公约、运输合同的有关规定,责任人免于承担 责任的事由。

1) 一般情况下的除外责任

国际货运代理的除外责任通常规定在国际货运 代理标准交易条件或与客户签订的合同中,归 纳起来包括:客户的过失或疏忽所致;客户或 其代理在搬运、装卸、存储和其他处理中所致; 货物包装不良;货物的自然特性或固有的缺陷; 货物的内容申报不详所致; 货物的标识不良 或地址有误所致;不可抗力所致。

责任保险合同的特点: ① 责任保险合同订立的目的是对第三人实施

救济 ② 责任保险合同的保险标的是法律上的赔偿

责任 ③ 责任保险合同明确约定赔偿的最高限额 ④ 责任保险合同的赔付具有替代性 ⑤ 责任保险合同有特殊的承保基础

职业责任保险合同

各种专业人员在从事职业活动中造成他人人身伤害或财 产损失而依法承担损害赔偿责任,称为职业责任。

人,包括其他的货运代理、货物拼装人、报关人及与事 故或事件有关的保险人,并及时提供法律上所要求的事 故通知书。

国际货运代理责任及其责任保险概述( PPT32页)培 训课件 培训讲 义培训ppt教程 管理课 件教程ppt 国际货运代理责任及其责任保险概述( PPT32页)培 训课件 培训讲 义培训ppt教程 管理课 件教程ppt

《保险法讲义》PPT课件

大致可以分为以下三种: 1.将保险法纳入商法典中,主要有法国、日本、比利时、西班牙等; 2.制定单行保险法律,主要有德国、瑞士、瑞典、丹麦、英国、美国等; 3.将保险法作为民法典的一部分,放在民法债编中,采此体例的国家主要有意

大利、原苏联及东欧一些国家。

26

第二节 保险法的历史流变

• 一、保险法的形成 • 二、大陆法系保险法的历史流变 • (一)法国法系国家的保险法 • (二)德国法系国家的保险法 • 三、英美法系保险法的历史流变 • (一)英国保险法 • (二)美国保险法

保险事故发生时给付保险金的义务。

31

• 二、保险合同的特征 • 保险合同的特征是在保险合同与其他民法上合同

相区别而言所表现出来的不同于其他民法上合同 的属性。 • (一)保险合同是债权合同 • 保险合同不能直接促使权利发生、变动或消灭, 是债权合同非物权合同。 • 保险合同属债法上合同的一种,但因保险合同所 生之债系属特种之债,故民法上有关债的

40

• 式合同,实务中有利于便捷地完成交易,切合效率价值的要求,亦能满足当 事人的实际生活需要。若必须等到签发保险单或其他保险单证后才能成立, 则不利于上述价值的实现。其三,若采要式说,在实务中则必须等到签发保 险单或其他保险单证后合同才能成立。

41

• (六)保险合同是格式合同 • 格式合同是指由当事人一方为与不特定多数人订

35

• (三)保险合同是有偿合同 • 合同以当事人取得权益是否须付出相应代价为标

准,可分为有偿合同与无偿合同两种。若当事人 一方取得合同约定的权益,须向对方当事人偿付 相应代价,则为有偿合同。若当事人取得约定的 权益,无须向对方当事人给付相应代价,则是无 偿合同,。 • 区分的法律意义在于:其一,订立合同主体的要 求不同。其二,当事人的责任轻重不同。