企业会计准则--具体准则第11号

企业会计准则第11号--股份支付-财会[2006]3号

![企业会计准则第11号--股份支付-财会[2006]3号](https://img.taocdn.com/s3/m/9162ce6526284b73f242336c1eb91a37f1113235.png)

企业会计准则第11号--股份支付正文:---------------------------------------------------------------------------------------------------------------------------------------------------- 企业会计准则第11号--股份支付(财会[2006]3号二○○六年二月十五日)第一章总则第一条为了规范股份支付的确认、计量和相关信息的披露,根据《企业会计准则——基本准则》,制定本准则。

第二条股份支付,是指企业为获取职工和其他方提供服务而授予权益工具或者承担以权益工具为基础确定的负债的交易。

股份支付分为以权益结算的股份支付和以现金结算的股份支付。

以权益结算的股份支付,是指企业为获取服务以股份或其他权益工具作为对价进行结算的交易。

以现金结算的股份支付,是指企业为获取服务承担以股份或其他权益工具为基础计算确定的交付现金或其他资产义务的交易。

本准则所指的权益工具是企业自身权益工具。

第三条下列各项适用其他相关会计准则:(一)企业合并中发行权益工具取得其他企业净资产的交易,适用《企业会计准则第20号——企业合并》。

(二)以权益工具作为对价取得其他金融工具等交易,适用《企业会计准则第22号——金融工具确认和计量》。

第二章以权益结算的股份支付第四条以权益结算的股份支付换取职工提供服务的,应当以授予职工权益工具的公允价值计量。

权益工具的公允价值,应当按照《企业会计准则第22号——金融工具确认和计量》确定。

第五条授予后立即可行权的换取职工服务的以权益结算的股份支付,应当在授予日按照权益工具的公允价值计入相关成本或费用,相应增加资本公积。

授予日,是指股份支付协议获得批准的日期。

第六条完成等待期内的服务或达到规定业绩条件才可行权的换取职工服务的以权益结算的股份支付,在等待期内的每个资产负债表日,应当以对可行权权益工具数量的最佳估计为基础,按照权益工具授予日的公允价值,将当期取得的服务计入相关成本或费用和资本公积。

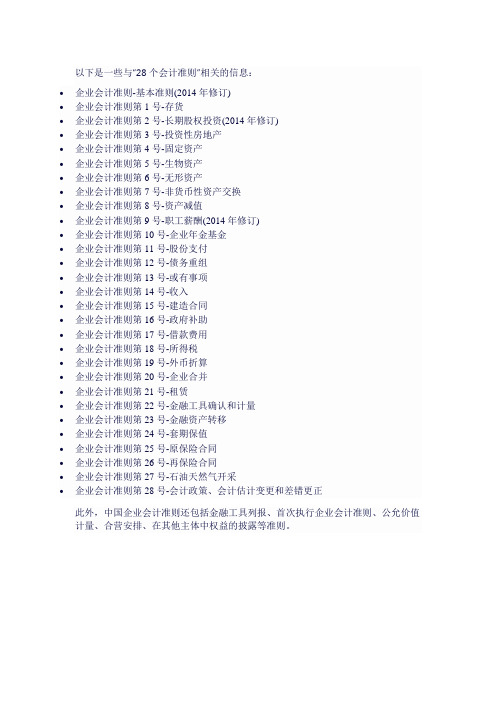

28个会计准则

以下是一些与“28个会计准则”相关的信息:

•企业会计准则-基本准则(2014年修订)

•企业会计准则第1号-存货

•企业会计准则第2号-长期股权投资(2014年修订)

•企业会计准则第3号-投资性房地产

•企业会计准则第4号-固定资产

•企业会计准则第5号-生物资产

•企业会计准则第6号-无形资产

•企业会计准则第7号-非货币性资产交换

•企业会计准则第8号-资产减值

•企业会计准则第9号-职工薪酬(2014年修订)

•企业会计准则第10号-企业年金基金

•企业会计准则第11号-股份支付

•企业会计准则第12号-债务重组

•企业会计准则第13号-或有事项

•企业会计准则第14号-收入

•企业会计准则第15号-建造合同

•企业会计准则第16号-政府补助

•企业会计准则第17号-借款费用

•企业会计准则第18号-所得税

•企业会计准则第19号-外币折算

•企业会计准则第20号-企业合并

•企业会计准则第21号-租赁

•企业会计准则第22号-金融工具确认和计量

•企业会计准则第23号-金融资产转移

•企业会计准则第24号-套期保值

•企业会计准则第25号-原保险合同

•企业会计准则第26号-再保险合同

•企业会计准则第27号-石油天然气开采

•企业会计准则第28号-会计政策、会计估计变更和差错更正

此外,中国企业会计准则还包括金融工具列报、首次执行企业会计准则、公允价值计量、合营安排、在其他主体中权益的披露等准则。

企业会计准则解释第11号-关于以使用无形资产产生的收入为基础的摊销方法(财会[2017]18号)

![企业会计准则解释第11号-关于以使用无形资产产生的收入为基础的摊销方法(财会[2017]18号)](https://img.taocdn.com/s3/m/24056eca240c844769eaee7f.png)

关于印发《企业会计准则解释第11号——关于以使用无形资产产生的收入为基础的摊销方法》的通知财会[2017]18号颁布时间:2017-06-12 发文单位:财政部国务院有关部委、有关直属机构,各省、自治区、直辖市、计划单列市财政厅(局),新疆生产建设兵团财务局,财政部驻各省、自治区、直辖市、计划单列市财政监察专员办事处,有关中央管理企业:为了深入贯彻实施企业会计准则,解决执行中出现的问题,同时,实现企业会计准则持续趋同和等效,我部制定了《企业会计准则解释第11号——关于以使用无形资产产生的收入为基础的摊销方法》,现予印发,请遵照执行。

附件:企业会计准则解释第11号——关于以使用无形资产产生的收入为基础的摊销方法财政部2017年6月12日附件:企业会计准则解释第11号——关于以使用无形资产产生的收入为基础的摊销方法一、涉及的主要准则该问题主要涉及《企业会计准则第6号——无形资产》(财会〔2006〕3号,以下简称第6号准则)。

二、涉及的主要问题第6号准则第十七条规定,企业选择的无形资产摊销方法,应当反映与该无形资产有关的经济利益的预期实现方式。

无法可靠确定预期实现方式的,应当采用直线法摊销。

根据上述规定,企业能否以包括使用无形资产在内的经济活动产生的收入为基础进行摊销?三、会计确认、计量和列报要求企业在按照第6号准则的上述规定选择无形资产摊销方法时,应根据与无形资产有关的经济利益的预期消耗方式做出决定。

由于收入可能受到投入、生产过程和销售等因素的影响,这些因素与无形资产有关经济利益的预期消耗方式无关,因此,企业通常不应以包括使用无形资产在内的经济活动所产生的收入为基础进行摊销,但是,下列极其有限的情况除外:1.企业根据合同约定确定无形资产固有的根本性限制条款(如无形资产的使用时间、使用无形资产生产产品的数量或因使用无形资产而应取得固定的收入总额)的,当该条款为因使用无形资产而应取得的固定的收入总额时,取得的收入可以成为摊销的合理基础,如企业获得勘探开采黄金的特许权,且合同明确规定该特许权在销售黄金的收入总额达到某固定的金额时失效。

企业会计准则第11号----股份支付

3. 股份支付的3个关键点

三 个 关 键 点

行权条件 支付基础: 支付基础:以股份为基础 结算方式 权益结算 现金结算 服务期限 业绩标准 规定期限内的业绩标准

4. 权益工具的公允价值的确定

股份支付交易中权益工具的公允价值应按照《企业会计准 则第22 号——金融工具确认和计量》确定。 1. 对于授予的股份期权等权益工具的公允价值,应当按照 其市场价格计量; 2. 没有市场价格的,应当参照具有相同交易条款的期权的 市场价格; 3. 以上两者均无法获取的,应采用期权定价模型估计,选 用的期权定价模型至少应当考虑以下因素: (1)期权的行权价格; (2)期权的有效期; (3)标的股份的现行价格; (4)股价预计波动率; (5)股份的预计股利; (6)期权有效期内的无风险利率。

股份支付交易会计处理核心

等待期的有关规定:

1. 处理原则 在等待期内的每个资产负债表日,将取得 职工或其他方提供的服务计入成本费用, 同时确认所有者权益或负债。 计入资产成本或费用,适用存货、固定资 产、无形资产等相关会计准则。

等待期的有关规定(续):

2. 对职工股份支付的价值确定 (1)权益结算股份支付,应按授予日权益 工具的公允价值计量,不确认其后续公允 价值变动。 (2)现金结算股份支付,应按资产负债表 日当日权益工具的公允价值重新计量,确 认成本费用和相应的应付职工薪酬,每期 权益工具公允价值变动计入当期损益。

B公司估计,该股票增值权在负债结算之前 每一个资产负债表日以及结算日的公允价值 和可行权后的每份股票增值权现金支出额如 下:

第一年有20 名管理人员离开A 公司,B 公司 估计三年中还将有15 名管理人员离开;第二 年又有10 名管理人员离开公司,公司估计还 将有10 名管理人员离开;第三年又有15 名管 理人员离开。第三年末,假定有70 人行使股 份增值权取得了现金。

企业会计准则第11号—股份支付

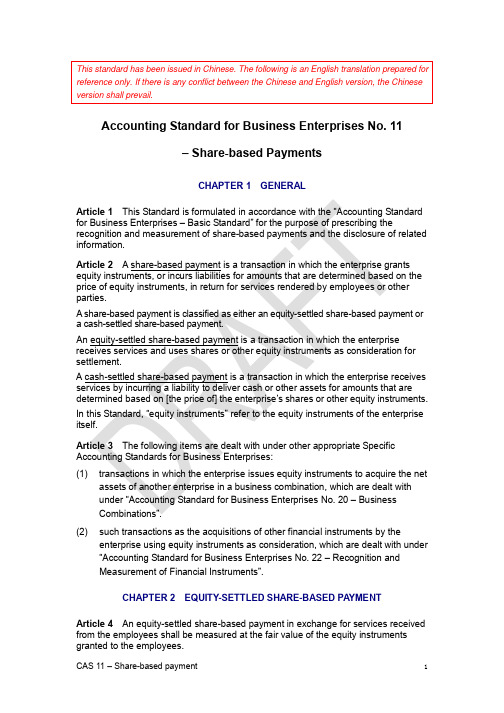

This standard has been issued in Chinese. The following is an English translation prepared for reference only. If there is any conflict between the Chinese and English version, the Chinese version shall prevail.Accounting Standard for Business Enterprises No. 11– Share-based PaymentsCHAPTER 1 GENERALArticle 1This Standard is formulated in accordance with the “Accounting Standard for Business Enterprises – Basic Standard” for the purpose of prescribing the recognition and measurement of share-based payments and the disclosure of related information.Article 2 A share-based payment is a transaction in which the enterprise grants equity instruments, or incurs liabilities for amounts that are determined based on the price of equity instruments, in return for services rendered by employees or other parties.A share-based payment is classified as either an equity-settled share-based payment or a cash-settled share-based payment.An equity-settled share-based payment is a transaction in which the enterprise receives services and uses shares or other equity instruments as consideration for settlement.A cash-settled share-based payment is a transaction in which the enterprise receives services by incurring a liability to deliver cash or other assets for amounts that are determined based on [the price of] the enterprise’s shares or other equity instruments. In this Standard, “equity instruments” refer to the equity instruments of the enterprise itself.Article 3The following items are dealt with under other appropriate Specific Accounting Standards for Business Enterprises:(1) transactions in which the enterprise issues equity instruments to acquire the netassets of another enterprise in a business combination, which are dealt withunder “Accounting Standard for Business Enterprises No. 20 – BusinessCombinations”.(2) such transactions as the acquisitions of other financial instruments by theenterprise using equity instruments as consideration, which are dealt with under “Accounting Standard for Business Enterprises No. 22 – Recognition andMeasurement of Financial Instruments”.CHAPTER 2 EQUITY-SETTLED SHARE-BASED PA YMENTArticle 4An equity-settled share-based payment in exchange for services received from the employees shall be measured at the fair value of the equity instruments granted to the employees.Fair value of equity instruments shall be determined in accordance with “Accounting Standard for Business Enterprises No. 22 – Recognition and Measurement of Financial Instruments”.Article 5If the equity instruments granted under an equity-settled share-based payment for services received from employees vest immediately, the enterprise shall, on grant date, recognise related costs or expenses at an amount equal to the fair value of the equity instruments, with a corresponding increase in capital reserve.Grant date is the date on which the share-based payment agreement is approved.Article 6If the equity instruments granted under an equity-settled share-based payment for services received from employees do not vest until the completion of services for a vesting period, or until the achievement of a specified performance condition, the enterprise shall, at each balance sheet date during the vesting period, recognise the services received for the current period as related costs or expenses, with a corresponding increase in capital reserve, at an amount equal to the fair value of the equity instruments at the grant date, based on the best estimate of the number of equity instruments expected to vest.On the balance sheet date, the estimate shall be revised if subsequent information indicates that the number of equity instruments expected to vest differs from its previous estimate. On vesting date, the enterprise shall revise the estimate to be equal to the number of equity instruments that ultimately vest.Vesting period is the period during which vesting conditions are to be satisfied.If the vesting condition of a share-based payment is a specified period of services, vesting period is from the grant date to the vesting date. If the vesting condition of a share-based payment is the achievement of a specified performance condition, the length of the vesting period shall be estimated, on the grant date, based on the most likely outcome of the performance condition.Vesting date is the date that vesting conditions are satisfied, and the employees or other parties have the rights to receive equity instruments or cash from the enterprise.Article 7After vesting date, the enterprise shall make no subsequent adjustment to related costs or expenses recognised and total owners’ equity.Article 8An equity-settled share-based payment in exchange for services from other parties shall be accounted for as follows:(1) if the fair value of services received from other parties can be measured reliably,that fair value on the date on which services are received from other parties shall be recognised as related costs or expenses, with a corresponding increase in owners’ equity.(2) if the fair value of services received from other parties cannot be measuredreliably but the fair value of the equity instruments can be measured reliably, the fair value of the equity instruments on the date on which services are received shall be recognised as related costs or expenses, with a corresponding increasein owners’ equity.Article 9On the exercise date, the enterprise shall determine the amount to be transferred to paid-in capital or share capital based on the number of equity instruments granted as a result of the rights being actually exercised, and transfer the amount to paid-in capital or share capital.Exercise date is the date on which employees or other parties exercise the rights to CHAPTER 3 CASH-SETTLED SHARE-BASED PAYMENTArticle 10 A cash-settled share-based payment shall be measured at the fair value of the liability incurred, being a liability which is determined based on the price of the enterprise’s shares or other equity instruments.Article 11If the rights under a cash-settled share-based payment vest immediately, the enterprise shall, on grant date, recognise related costs or expenses at an amount equal to the fair value of the liability incurred, with a corresponding increase in liability.Article 12 If the rights under a cash-settled share-based payment do not vest until the completion of services for a vesting period, or until the achievement of a specified performance condition, the enterprise shall, at each balance sheet date during the vesting period, recognise the services received for the current period as related costs or expenses, with a corresponding increase in liability, at an amount equal to the fair value of the liability based on the best estimate of the outcome of vesting.On the balance sheet date, the amount of the liability shall be revised if subsequent information indicates that the current fair value of the liability differs from its previous estimate. On vesting date, the enterprise shall revise the amount of the liability to the actual liability (based on the rights that ultimately vest).Article 13Until the liability is settled, the enterprise shall remeasure the fair value of the liability at each balance sheet date and at the date of settlement, with changes recognised in profit or loss for the period.CHAPTER 4 DISCLOSUREArticle 14An enterprise shall disclose the following information related toshare-based payments in the notes:(1) total amount of each type of equity instruments granted, exercised and lapsedduring the period.(2) the range of exercise prices and remaining contractual life of share options orother equity instruments outstanding at the end of the period.(3) the weighted average share price at the date of exercise for share options orother equity instruments exercised during the period.(4) the method of determining the fair value of equity instruments.For share-based payments of similar nature, the enterprise may aggregate the information for disclosure.Article 15An enterprise shall disclose in the notes the effect of share-based payment transactions on the enterprise’s financial position and operating results for the period, including at least the following information:(1) total expense recognised for the period arising from equity-settled share-basedpayments.(2) total expense recognised for the period arising from cash-settled share-basedpayments.(3) total amount of services received from employees and total amount of servicesreceived from other parties for the period in exchange for share-basedpayments.。

《企业会计准则第11号——股份支付》的应用——以伊利为例

《企业会计准则第11号——股份支付》的应用——以伊利为例作者:许敏敏席秀华来源:《财会学习》2008年第09期早在20世纪90年代初,我国已有企业开始股权激励方面的尝试,武汉、上海、北京等地都推出了国有企业经营者股权激励的具体形式。

之后,各种文件和政策陆续确定股权激励可以作为公司高管的激励方式。

2005年8月证监会和国资委、财政部等五部委联合推出了《关于上市公司股权分置改革的指导意见》指出,完成股权分置改革的上市公司可以实施管理层股权激励,上市公司管理层股权激励的具体实施和考核办法,以及配套的监督制度由证券监管部门会同有关部门制定。

2005年11月中国证监会“关于就《上市公司股权激励规范意见》(试行)公开征求意见的通知”对上市公司实施股权激励进行明确的规范,可见股权激励在我国将会成为一种重要的激励方式。

但直到2006年2月,《企业会计准则第11号——股份支付》的发布,才有了股份支付的会计处理规范,改变了以往企业会计准则在这方面的空白。

伊利作为较早实行股权激励的上市公司,在2008年1月预亏时,引起了社会的极大反响。

因此,我们以伊利为例,来分析在股权激励的不同阶段,如何根据《企业会计准则第11号——股份支付》来进行相应的会计处理。

一、新旧会计制度对股份支付会计处理的差异股份支付,是指企业为获取职工和其他方提供服务而授予权益工具或者承担以权益工具为基础确定的负债的交易。

企业用期权来奖励员工或者作为薪酬的组成部分,是目前具有代表性的股份支付交易。

由于股份支付是以权益工具的公允价值为计量基础,《企业会计准则第9 号——职工薪酬》规定,以股份为基础的薪酬适用《企业会计准则第11号——股份支付》。

在在新会计准则颁布以前,没有专门的会计制度对股份支付进行专门的规范,我国实施股票期权计划的公司只需调整公司的权益结构,整个会计处理过程不会影响现金流量表和利润表,唯一变化的是原有股东的每股收益会被摊薄。

而新准则规定,上市公司通过股权激励所形成的股份支付,应记入股权激励期间的费用。

企业会计准则解释第11号—关于以使用无形资产产生的收入为基础的摊销方法

本文极具参考价值,如若有用可以打赏购买全文!本WORD版下载后可直接修改企业会计准则解释第11号——关于以使用无形资产产生的收入为基础的摊销方法 (【2017至2018最新会计实务】

一、涉及的主要准则

该问题主要涉及《企业会计准则第6号——无形资产》(财会〔2006〕3号,以下简称第6号准则)。

二、涉及的主要问题

第6号准则第十七条规定,企业选择的无形资产摊销方法,应当反映与该无形资产有关的经济利益的预期实现方式。

无法可靠确定预期实现方式的,应当采用直线法摊销。

根据上述规定,企业能否以包括使用无形资产在内的经济活动产生的收入为基础进行摊销?

三、会计确认、计量和列报要求

企业在按照第6号准则的上述规定选择无形资产摊销方法时,应根据与无形资产有关的经济利益的预期消耗方式做出决定。

由于收入可能受到投入、生产过程和销售等因素的影响,这些因素与无形资产有关经济利益的预期消耗方式无关,因此,企业通常不应以包括使用无形资产在内的经济活动所产生的收入为基础进行摊销,但是,下列极其有限的情况除外:

1.企业根据合同约定确定无形资产固有的根本性限制条款(如无形资产的使用时间、使用无形资产生产产品的数量或因使用无形资产而应取得固定的收入总额)的,当该条款为因使用无形资产而应取得的固定的收入总额时,取得的收入可以成为摊销的合理基础,如企业获得勘探开采黄金的特许权,且合同明确规定该特许权在销售黄金的收入总额达到某固定的金额时失效。

2.有确凿的证据表明收入的金额和无形资产经济利益的消耗是高度相关的。

企业采用车流量法对高速公路经营权进行摊销的,不属于以包括使用无形资产在内的经济活动产生的收入为基础的摊销方法。

《企业会计准则第11号――股份支付》案例分析

《企业会计准则第11号――股份⽀付》案例分析2019-10-20财政部的新准则对股份⽀付有了明确的规范,体现在新增《企业会计准则第11号――股份⽀付》⽂件上,新准则的内容和实际操作中的财税差异值得上市公司关注。

我国现⾏会计准则和制度均未对股份⽀付有明确的规范,只是对股权激励的范围在2005年11⽉中国证监会“关于就《上市公司股权激励规范意见》(试⾏)公开征求意见的通知”(以下简称“旧制度”)等⼀些相关规定中有零星分散的说明,⽽2006年财政部的新准则弥补了这⼀缺陷,新增了《企业会计准则第11号――股份⽀付》(以下简称“新准则”)。

1.计量属性不同旧制度:按实际成本计量。

新准则:以授予的权益⼯具或承担债务性⼯具的公允价值计量。

2.计量范围不同旧制度:企业以各种形式对⾼管⼈员实施的奖励。

新准则:企业为获取职⼯和其他⽅提供服务⽽授予权益⼯具或者承担以权益⼯具为基础确定的负债的交易。

3.会计处理不同旧制度:只是对⾼管层激励⽅⾯做了⼀些粗略的规定。

新准则:股份⽀付分为权益结算⽀付、现⾦结算⽀付两种;核算过程包括了授予⽇、等待⽇、⾏权⽇的处理。

详见表1:财税差异1.从范围分析新准则明确规定,股份⽀付属于职⼯薪酬的内容,是企业为获得职⼯提供的服务⽽给予的报酬。

新《中华⼈民共和国企业所得税法实施条例》第三⼗四条规定:⼯资薪⾦是指企业每⼀纳税年度⽀付给在本企业任职或者受雇的员⼯的所有现⾦形式或者⾮现⾦形式的劳动报酬,包括基本⼯资、奖⾦、津贴、补贴、年终加薪、加班⼯资以及与员⼯任职或者受雇有关的其他⽀出。

即新税法及其实施条例尚未明确规定权益结算和现⾦结算等股份⽀付作为职⼯薪酬的具体内容。

2.从确认时间分析根据《企业所得税法》第⼋条规定,由于企业实际发⽣的与取得收⼊有关的、合理的⽀出,包括成本、费⽤、税⾦、损失和其他⽀出,可以在计算应纳税所得额时扣除。

新准则在等待期内的每个资产负债表⽇,⽆论权益结算或者现⾦结算股份⽀付,都依据权责发⽣制原则按公允价值计提了成本和费⽤,但这并未实际⽀付,不得在税前扣除,需作纳税调增处理,⽽实际⾏权时,则视同发放⼯资薪⾦,应据实扣除,作纳税调减处理。

企业会计准则第 11 号股份支付

企业会计准则第11 号股份支付

摘要:

和

正文:

企业会计准则第11 号股份支付详细规定了企业如何处理股份支付的会计问题。

股份支付是企业为了获取职工或其他方提供的服务而授予的权益工具或承担的负债交易。

它包括以权益结算的股份支付和以现金结算的股份支付。

股份支付的会计处理是这个准则的核心内容。

企业需要按照一定的原则确认股份支付,包括确定股份支付的金额、时间和对象等。

同时,企业还需要按照规定的会计方法计量股份支付,确保计量结果准确、真实。

最后,企业需要充分披露股份支付的相关信息,以便用户了解企业的真实财务状况。

股份支付的举例和应用可以帮助我们更好地理解这个准则。

例如,企业可以通过授予职工期权、认股权证等衍生工具来激励职工,提高职工的工作积极性和创造性。

企业也可以通过承担以股份或其他权益工具为基础计算确定的交付现金或其他资产的方式,来获取服务。

最后,股份支付对企业的影响也需要我们关注。

股份支付会对企业的财务报表产生影响,同时也会影响公司的经营决策。

企业会计准则11号

企业会计准则11号

(原创实用版)

目录

1.企业会计准则第 11 号的定义和目的

2.企业会计准则第 11 号的主要内容

3.企业会计准则第 11 号的应用范围和意义

正文

一、企业会计准则第 11 号的定义和目的

企业会计准则第 11 号,简称“股份支付”,是指企业为获取职工和其他方提供服务而授予权益工具或者承担以权益工具为基础确定的负债

的交易。

这一准则主要目的是规范企业的股份支付行为,确保企业准确计算相关成本和费用,如实反映企业的财务状况和经营成果。

二、企业会计准则第 11 号的主要内容

1.股份支付的定义:股份支付包括企业授予职工或其他方的股票、股票期权、限制性股票等权益工具,以及承担以权益工具为基础确定的负债。

2.股份支付的确认和计量:企业在进行股份支付时,应按照权益工具的公允价值确认相关成本和费用,并按照权益工具的公允价值和可行权条件进行计量。

3.股份支付的会计处理:企业应将股份支付的相关成本和费用计入当期损益,同时增加资本公积或负债。

4.股份支付的披露:企业应披露股份支付的相关信息,包括股份支付的种类、数量、公允价值、成本和费用等。

三、企业会计准则第 11 号的应用范围和意义

企业会计准则第 11 号主要适用于企业进行股份支付的相关会计处

理。

这一准则对于规范企业的股份支付行为,确保企业准确计算相关成本和费用,如实反映企业的财务状况和经营成果具有重要意义。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

企业会计准则第11号——股份支付

第一章总则

第一条为了规范股份支付的确认、计量和相关信。

息的披露,根据《企业会计准则—墓本准则》,制定本准则。

第二条股份支付,是指企业为获取职工和其他方提供服务或商品而授予权益工具或者承担以权益工具为签础确定的负债的交易。

股份支付分为以权益结算的股份。

支付和以现金结算的股份支付:

以权益结算的股份支付,是指企业因获取服务或商品。

以股份或其他权益工具作为对价进行结算的交易。

以现金结算的股份支付,是指企业因获取服务或商品。

承担以股份或其他权益工具。

为基础计算确定交付现金或其他资产义务的交易。

第三条下列各项适用其他相关会计准则:

(一)企业合并中发行权益工具取得其他企业净资产的交易,适用《企业会计准则第20号—企业合并》。

(二)通过股份支付换。

入金融工具等交易。

适用《企业会计准22号—金融工具确认和计量》

第二章以权益结算的股份支付

第四条以权益结算的股份支付换取职工提供服务或其他方提供类似服务的,应当以授予职工和其他方权益工具的公允价值计量。

第五条授予后立即可行权的换取职工服务或其他方类似服务的以权益结算的股份支付,应当在授予日按权益工具的公允价值计入相关成本或费用,相应增加资本公积。

授予日,是指股份支付协议获得批准的日期。

第六条完成等待期内的服务或达到规定业绩条件才可行权的换取职工服务或其他方类似服务的以权益结算的股份支付,在等待期内的每个资声负债表日,应当以对可行权权益工具数量的最佳估计为基础,按照权益工具授予日的公允价值,将当期取得的服务计入相关成本或费用和资本公积

在资产负债表日、后续信。

息表明可行权权益工具的数量与以前估计文同的,应当进行调整;在可行权日,调整至实际可行权的权益工具数量。

等待期,是指可行权条件得到满足的期问。

对干可行权条件为规定服务期间的股份支付,等待期为授予日至可行权日的期间;对于可行权条件为规定业绩的股份支付,应当在授予日根据最可能的业绩结果预计等待期的长度。

可行权日,是指可行权条件得到满足、职工和其他方具有从企业取得现金或权益工具权利的日期。

第七条企业在可行权日之后不再对已确认的相关成本或费用和所有者权益总额进行调整。

第八条以权益结算的股份支付换取商品或其他服务的,应当分别下列情况处理:

(一)商品或其他服务的公允价值能够可靠计量的,应当以其取得的公允价值和应支付的相关税费作为商品或其他服务的成本,相应增加所有者权益。

〔二〕商品或其他服务的公允价值不能可靠计量但权益工具公允价值能够可靠计量的,应当以权益工具的公允价值和应支付的相关税费作为换取的商品或其他服务的成本,相应增加所有者权益。

第九条在行权日,企业根据实际行权的权益工具数量,计算确定应转入实收资本或股本的金额,将其转入实收资本或股本。

行权日,是指职工和其他方行使权利、获取现金或权益工具的日期。

第三章以现金结算的股份支付

第十条以现金结算的股份支付,应当以承担负债的公允价值计量。

第十一条授予后立即可行权的以现金结算的股份支付,应当在授子日以承担负债的公允价值计入相关成本或费用,相应增加负债。

第十二条完成等待期内的服务或达到规定业绩条件以后才可行权的以现金结算的股份支付,在等待期内的每个资产负债表日,应当以对可行权情况的最佳估计为墓础,按照承担负债的公允价值金额,将当期取得的服务计入成本或费用和负债。

在资产负债表日,后续信息表明当期承担债务的公允价值与以前估计不同的,应当进行调整;在可行权日,调整至实际可行权水平。

第十三条企业应当在相关负债结算前的每个资产负债表日以及结算日,对负债的公允价值重新计量、其变动计入当期损益。

第四章披露

第十四条企业应当在附注中披露与股份支付的性质和范围有关的下列信息

(一)当期授予、行使和失效的权益工具总额。

(二)期末发行在外的股份期权或其他权益工具行权价格的范围和合同剩余期限的加权平均数。

(三)当期行权的股份期权或类似工具以行权日股票价格计算的加权平数。

(四)权益工具公允价值的确定方法。

企业对性质相似的股份支付信息可以合并披露。

第十五条企业应当在附注中披露股份支付交易对当期财务状况和经重成果的影响,至少包括下列信息

(一)当期因以权益结算的股份支付而确认的费用总额,

(二)当期因以现金结算的股份支付而确认的费用总额。

(三)当期以股份支付换取的商品和其他服务总额。