财务预算管理英文版

财务管理制度英文范文

财务管理制度英文范文Financial Management SystemIntroductionA robust financial management system is crucial for the success and sustainability of any organization. It sets guidelines and procedures for effective resource allocation, budgeting, auditing, and financial reporting. This document provides an overview of our organization's financial management system, focusing on key areas such as budgeting, financial reporting, internal controls, and auditing.Budgeting1. Purpose:The budgeting process aims to allocate financial resources efficiently and effectively to support the organization's goals and objectives.2. Process:a. The Finance Department prepares a budget proposal based on inputs from different departments and stakeholders.b. The budget proposal is reviewed by the management team and adjusted as necessary.c. The final budget is approved and communicated to all relevant stakeholders.d. Throughout the year, the Finance Department monitors actual expenses against the budget, providing regular reports to management.3. Responsibilities:a. The Finance Department is responsible for preparing and monitoring the budget.b. Department heads are responsible for proposing and justifying budget requests for their respective areas.c. The management team is responsible for reviewing and approving the final budget.Financial Reporting1. Purpose:Accurate and timely financial reporting provides transparency and helps stakeholders make informed decisions.2. Frequency:a. Monthly financial reports are prepared within ten days of the end of each month.b. Quarterly financial reports are prepared and reviewed by the management team within fifteen days of the end of each quarter.c. Annual financial reports, including audited financial statements, are prepared within sixty days of the end of the fiscal year.3. Contents:a. Balance sheet: Provides information about the organization's assets, liabilities, and equity.b. Income statement: Presents the organization's revenues, expenses, and net income.c. Cash flow statement: Shows the sources and uses of cash during a specific period.d. Notes to financial statements: Provides additional information and explanations related to the financial statements.Internal Controls1. Purpose:Internal controls aim to safeguard assets, prevent fraud and errors, and ensure compliance with laws and regulations.2. Segregation of Duties:a. The Finance Department ensures that no single individual has control over all financial functions, such as handling cash, recording transactions, and approving payments.b. Regular rotation of roles within the Finance Department is encouraged to mitigate risks and prevent collusion.3. Authorization and Approval:a. All financial transactions, including expenditures, must be authorized by the appropriate level of management.b. Approval documentation must be maintained for auditing purposes.Auditing1. External Audit:a. An external auditing firm is engaged annually to conduct an independent audit of the organization's financial statements.b. The audit firm examines the organization's financial records, internal controls, and adherence to accounting standards.c. The external audit report is presented to the management teamand Board of Directors.2. Internal Audit:a. An internal audit department is established to conduct periodic audits of the organization's financial activities.b. The internal audit team assesses the effectiveness of internal controls, identifies weaknesses, and provides recommendations for improvement.c. Internal audit reports are shared with the management team and appropriate departments to ensure corrective actions are taken. ConclusionA well-defined and well-implemented financial management system is instrumental in achieving an organization's financial goals. This document provides a framework for effective budgeting, financial reporting, internal controls, and auditing. Regular review and updates to this system are necessary to adapt to changing business environments and ensure continuous improvement. By adhering to this financial management system, we can ensure transparency, accountability, and sustainability in our organization's financial activities.。

2023年度公司财务管理制度全文中英文对照

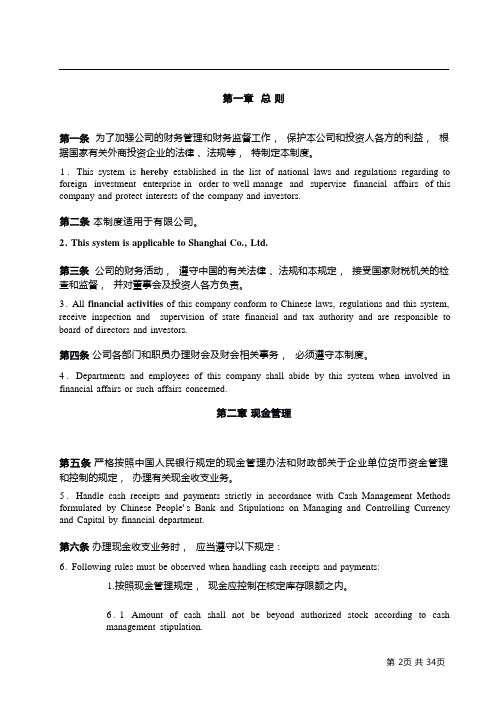

为了加强公司的财务管理和财务监督工作,保护本公司和投资人各方的利益,根据国家有关外商投资企业的法律、法规等,特制定本制度。

1.This system is hereby established in the list of national laws and regulations regarding to foreign investment enterprise in order to well manage and supervise financial affairs of this company and protect interests of the company and investors.本制度适用于有限公司。

2.This system is applicable to Shanghai Co.,Ltd.公司的财务活动,遵守中国的有关法律、法规和本规定,接受国家财税机关的检查和监督,并对董事会及投资人各方负责。

3. All financial activities of this company conform to Chinese laws, regulations and this system, receive inspection and supervision of state financial and tax authority and are responsible to board of directors and investors.公司各部门和职员办理财会及财会相关事务,必须遵守本制度。

4.Departments and employees of this company shall abide by this system when involved in financial affairs or such affairs concerned.严格按照中国人民银行规定的现金管理办法和财政部关于企业单位货币资金管理和控制的规定,办理有关现金收支业务。

财务管理英文第十三版

Corporate Capital Gains / Losses

Currently, capital gains are taxed at ordinary income tax rates for corporations, or a maximum 35%.

The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate after-tax incremental operating cash flows for the investment projects.

c) - (+) Taxes (tax savings) due to asset sale or disposal of “new” assets

d) + (-) Decreased (increased) level of “net” working capital

e) = Terminal year incremental net cash flow

Depreciation and the MACRS Method

Everything else equal, the greater the depreciation charges, the lower the taxes paid by the firm.

预算法 英文版

预算法英文版Budgeting is a fundamental aspect of financial management that allows individuals and organizations to plan and control their spending. In this article, we will explore the concept of budgeting and discuss its importance in both personal and business finance.Budgeting, also known as the budgetary process, involves the estimation of future income and expenses and the allocation of resources to achieve specific financial goals.By creating a budget, individuals and organizations can track their income and expenses, identify areas of overspending, and make informed decisions about how to best allocate their resources.In personal finance, budgeting is crucial for achieving financial stability and long-term goals. By creating a budget, individuals can track their income, expenses, and savings, and identify areas where they can cut costs or increase savings. A budget canalso help individuals plan for major expenses, such as buying a home or paying for education, and ensure that they are living within their means.In business finance, budgeting plays a critical role in ensuring the financial healthand success of an organization. By creating a budget, businesses can plan for future expenses, allocate resources to different departments or projects, and monitor their financial performance. A well-planned budget can help businesses identify areas of inefficiency, make strategic decisions about resource allocation, and achieve their financial goals.There are several different budgeting methods that individuals and organizations can use to create a budget. One common method is zero-based budgeting, where all expenses must be justified for each budgeting period. This method can help individuals and organizations identify unnecessary expenses and prioritize spending based on their financial goals.Another popular budgeting method is the 50/30/20 rule, which suggests allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This methodcan help individuals strike a balance between meeting their basic needs, enjoying discretionary spending, and saving for the future.In conclusion, budgeting is a critical aspect of financial management that allows individuals and organizations to plan and control their spending. By creating a budget, individuals and businesses can track their income and expenses, identify areas of overspending, and make informed decisions about resource allocation. Ultimately, budgeting is essential for achieving financial stability, meeting financial goals, and ensuring long-term financial success.。

英语版财务管理制度

1. IntroductionThis Financial Management Policy (the "Policy") is designed to establish the framework for the financial management of [Company Name] (the "Company"). It outlines the principles, procedures, and controls that govern the Company's financial activities, ensuring compliance with applicable laws, regulations, and internal policies. The Policy is intended to promote transparency, accountability, and efficiency in the Company's financial operations.2. ScopeThis Policy applies to all employees, officers, and directors of the Company, as well as any other individuals or entities acting on behalf of the Company. It also applies to all financial transactions, assets, and liabilities of the Company.3. ObjectivesThe objectives of this Policy are as follows:- To ensure the integrity and reliability of the Company's financial records and reports.- To promote effective financial planning and decision-making.- To protect the Company's assets and resources.- To ensure compliance with all applicable laws, regulations, and internal policies.- To maintain a high standard of ethical conduct in all financial matters.4. Financial ControlsTo achieve the objectives outlined above, the following financial controls are established:4.1 Budgeting and ForecastingThe Company shall develop and maintain a comprehensive budget and forecast for each fiscal year. This budget shall be based on realistic assumptions and approved by the appropriate management level. Regular reviews and adjustments to the budget and forecast will be conducted as necessary.4.2 Record KeepingAll financial transactions shall be recorded in the Company's accounting system in a timely and accurate manner. The accounting system shall be designed to ensure the integrity and reliability of the financial records.4.3 Internal ControlsInternal controls shall be established and maintained to safeguard the Company's assets, ensure the accuracy and completeness of financial records, and comply with applicable laws and regulations. These controls may include segregation of duties, approval procedures, and regular internal and external audits.4.4 Approval of Financial TransactionsAll financial transactions exceeding a certain threshold shall require prior approval from the appropriate level of management. This includes, but is not limited to, expenditures, disbursements, and commitments of the Company's resources.5. Compliance and ReportingThe Company shall comply with all applicable laws, regulations, and internal policies in its financial activities. This includes, but is not limited to, tax laws, financial reporting standards, and anti-corruption laws.The Company shall prepare and distribute financial reports on a regular basis, including quarterly and annual reports. These reports shall provide a true and fair view of the Company's financial position, performance, and cash flows.6. Ethics and IntegrityAll employees, officers, and directors of the Company are expected to act with integrity and honesty in all financial matters. They shall avoid conflicts of interest and shall disclose any potential conflicts to the appropriate management level.7. Training and CommunicationThe Company shall provide appropriate training to employees on the financial management policies and procedures. Regular communication regarding the Policy shall be maintained to ensure that all employees are aware of their responsibilities and obligations.8. Review and UpdatesThis Policy shall be reviewed and updated periodically to ensure its relevance and effectiveness. Any significant changes to the Policy shall be communicated to all affected parties.9. EnforcementAny violation of this Policy shall be taken seriously. The Company reserves the right to take appropriate disciplinary action, up to and including termination of employment, against any individual found to be in violation of this Policy.10. ConclusionThe Financial Management Policy is a vital tool for ensuring the financial health and sustainability of the Company. By adhering to this Policy, the Company can maintain the trust and confidence of its stakeholders and continue to operate effectively in a competitive and regulatory environment.[Company Name][Date]。

{财务管理预算编制}财政预算报告范本英文版

{财务管理预算编制}财政预算报告范本英文版⏹IntroductionTricolplcapanywhomakesarangeoffurnitureandkitchenware.Andoneofitsmostpopularpro ductsisthe‘Zupper’expandabletable.Thepurposeofwritingthisreportistodothevarianceanalysis,projectevaluationandtoparethebudgetandactualdatabyusingthetechnique.FindingsPartAPossibleReasonforVariances1.MaterialDirectMaterial–Total-£2,400Fmadeup:DirectMaterialUsage–£20000F(Levelofsignificance–usage/totalbudgetedMaterialcosts=8,000/64,000=12.5%>3%,shouldbereview ed)2000kglessmaterialsareusedthanbudgetedfortheactuallevelofproduction.Possiblerea sonmaybeusingthehigher-gradematerialwithlesswastage.Orthenewmachineryuselessmat erialsandincurslesswstage.DirectMaterialPrice–£5,600A(5,600/64,000=8.75%>3%)Itis£1perkgmoreexpensivethanplanned Possiblereason: Newmaterialsupplierdoesnotgivediscountsformaterials.Hither-gradematerialshavebeenusedwhichismoreexpensive.bourDirectLabourTotal-£6,400ADirectLabourRate–£3,520A(3,520/28,800=12.2%>3%)Onaverage,theactuallabourrateis£1/hourhigherthanbudgetedPossiblereason:Thewagesettlementishigherthanexpected Thenewmachinerequirestrainingssothatovertimerequiredmorethanexpected. DirectlabourEfficiency-£2000A>3%)4.16%Actually,morethan200labourhourshavebeenusedthanbudgeted.Possiblereaso n:Newmachineryrequiresmorehoursfortraining..Humanresourceissues–theskilledoperativesisnotenough. 3.TotalOverhead-£600FRateis4.70% UnpredictedincreaseininsuranceandAdministrationcosts Possiblereason:Newmachinerybringsmoreexpensiveinsurance,highermaintenanceandaddition aladministrativecosts.PartB1.Keyassumptionsmade:a)Thereisnotaxationandinflation.b)Assumedthatthereisnovarygivenreturnmarketrate.c)Thetotalcostoftheprojectwillbepayableatthestartd)Theexpectedrevenuefromtheinvestment–thisistheexpectedNetCashFlowafterdeductionofallrelevantcosts2.PaybackPaybackinthiscaseis4.125years(totalinvestment-returnperiodisfiveyears ).Sothepanycangetbacktheinvestment.TheNetPresentValueis£-64,800.Itindicatesthattheprojectdoesnotappeartobefinanciallyviable. ConclusionPartBThisprojectisavailablebecausethepaybackis4.125years. ButtheNetPresentValue(NPV)isnegative.Sotheprojectisnotavailable. However,weshouldusetheconclusionoftheNetPresentValuebecausetheNetPres entValue(NPV)consideredthetimevalueofmoney.RemendationsPartARemendationsformanagementaction:1.Allthevariancesshouldbeanalysisbecauseallofthemareabove3%,thelevelofsignificance.2.Particularly,thedirectlabourvariancesneedfurtherinvestigation–whyisthepanypayingahigherwageratebutthelabourproductivityislowerth anplanned.PartB1.Toconsidertheeffectofthenewfacilitiesonpany’sownstaff–intermsofemploymentandredeploymentopportunities.2.Toconsideranychangesinanyotherareas,likesocial,political,economic,legalandtechnologicalfactors.3.Whetheritispossibleforthepanytoraisethesufficientfunds–toconsiderifthecurrentcashflowpositioncansupportsuchaninvestment. AppendixPartA1.Table1TricolplcFlexedBudgetforJune2.FurtherVarianceAnalysisThecalculationofthevariancesa)Directmaterialtotal:(BudgetedQuantity*BudgetedPrice)–(ActualQuantity*ActualPrice)=(4kg*1,600*£10perkg)-(5,600kg*£11perkg)=£64,000-£61,600=£2,400F b)Directmaterialusage:Budgetedprice*(BudgetedQuantity–ActualQuantity)=£10perkg*(4kg*1,600-5,600kg)=£8,000Fc)Directmaterialprice:ActualQuantity*(Budgetedprice–Actualprice)=5,600kg*(£10perkg-£11perkg)=£5,600Ad)Directlabortotal:BudgetedHours*BudgetedRate–Actualhours*ActualRate=(2hours*1600*£9)-£35200=£6,400Ae)Directlaborrate:ActualHours*(BudgetedRate–ActualRate)=3,520hours*(£9-£10)=£3,520Af)Directlaborefficiency:BudgetedRate*(BudgetedHours–ActualHours)=£9-(2hours*1600-3520hours)=£2,880Ag)Totaloverhead:(BudgetVariableOverhead+BudgetFixedOverhead)-(ActualVariableOverhead+ ActualFixedOverhead)=(£4000+£8200)-(£3200+£8600)=£400FPartB1.PaybackperiodmethodPayback=4+40,000/320,000=4.125years2.Discountcashflowtechnique(netpresentvalue) CalculationofNetPresentValue (NPV)at10%感谢阅读多年企业管理咨询经验,专注为企业和个人提供精品管理方案,企业诊断方案,制度参考模板等欢迎您下载,均可自由编辑。

管理会计全面预算英文版

写在前面:这是我们小组写的一篇关于编制一个全面预算的作业。

因为课程原因此文为英文版,并有一定的不足。

考虑到与其将之放在U盘里暗无天日,不如拿出来给大家分享并借鉴。

此文仅供参考请勿用于抄袭等。

谢谢!●Contents● Introduction (2)Background (2)Main business competitors (2)Target customer base (2)● Master budget (2)The financial data (2)The master budgets (5)a. Sales budget (5)b. Cash collections from customers (5)c. Purchase and cost of goods sold budget (6)d. Cash Disbursements for purchases (6)e. Operating expense budget (7)f. Capital budget (7)g. Budget Income Statement (8)h. Cash budget (9)i. Budget Balance Sheet (9)● Conclusion (11)● Reference (11)●IntroductionBackgroundWe use 100,000 yuan to open a MAYMAY cake house.It nears the Chongqing University of Technology.And the cake house makes cupcakes and sellsit.Main business competitorsNow,we are under a high pressure,we might face many competitors,such as Hua Sheng Yuan,Holiland and others.We chose here to open the cake house because there are little competitor,and a great deal of people.Target customer baseTeachers,students and the nearby residents, factory workers are our target customers. They have a great demand for convenient, nutritional and benefit breakfast or fast food.●Master budgetThe financial data.MAY MAY company’s balance sheet as 31 Mar.2014 is as follow:Assets 31Mar.2014Current assetsCash 8,600Accounts receivable 9,400Merchandise inventory 12,0001,800Unexpiredinsurance(july-Dec)Unexpired rent 15,000 45,200Plant assetsEquipment and other 74,00017,600 60,800AccumulateddepreciationTotal assets 100,000Liabilities and owner’s equityCurrent liabilitiesAccount payable 8,400Owner’s equity91,600Total liabilities and100,000owner’s equity1.We illustrate the budgeting process using the MAY MAY patisserie company.Although master budgets cover a full year,for the sake of brevity this illustration shows only the first 3 months of MAY MAY’s fiscal year.April-June.Sale budgetMarch April May June JulyTotal sales $40,000 $30,000 $35,000 $40,000 $50,000 2. Our initial investment for 100,000 dollars, and the renovation cost is 30,000 dollars,in addition, the cost of equipment and decoration is one-time payment.3.The following are the cost of fixed assets:Oven 10,000Proofing boxes 10,000Electric mixer 2,000Operation table 2,000Window displays 10,000Implements 5,0004.On average,60% of sales are cash sales and remaining 40% are credit sales.And sales in March were 40,000.5.Gross profit margin is 60% of sales.30% of the purchases are paid in the month of purchase and the remainder in the following month. In addition,we have to maintain a monthly inventory of 50% of next month’s cost of goods sol d.6.The following are the monthly expected expense:(1).We will pay total $6,500 to two salesclerks for wages.(2).Insurance:200(3).Rent:5,000(4).Depreciation on existing assets:200(5).Miscellaneous expense 5% of current month’s sales.7. The fixed assets useful life are 20 years.We use Straight Line Method to computing depreciation every year.8.The cost of insurance is a one-time payment at the beginning of the year.9. The rent expense is paid each quarter.The first month of each quarter is time topay this quarter’s rent expense.10.We will only borrow money if there are insufficient funds.The interest rate on loanis 10% per annum.11.The business tax rate is 5%.The master budgetsa. Sales budgetMarch April May June July April—June Total40,000 30,000 35,000 40,000 50,000 115,000 Totalsalesb. Cash collections from customersApril May JuneCash sales (60% of18,000 21,000 24,000current monthsales)16,000 12,000 14,000 Collections of lastmonth’s creditsales (40%ofprevious monthsales)Total collections 34,000 33,000 38,000c. Purchase and cost of goods sold budgetApril May June April ---JuneTotal12,000 14,000 16,000 42,000 Budget cost ofgoods soldPlus : Desired7,000 8,000 10,000 25,000endinginventory19,000 22,000 26,000 67,000TotalmerchandiseneededLess :6,000 7,000 8,000 21,000 BeginninginventoryPurchases 13,000 15,000 18,000 46,000d. Cash Disbursements for purchasesApril May June8,400 9,100 10,50070% of last month’spurchasesPlus 30% of this9,000 4,500 5,400month’s purchasesDisbursements of17,400 13,600 15,900purchasese. Operating expense budgetApril May June April ---JuneTotalWages (Fixed) 6,500 6,500 6,500 19,500200 200 200 600 Insurance(Fixed)Rent (Fixed) 5,000 5,000 5,000 15,000200 200 200 600 Depreciationon existingassets(Fixed)1,500 1,750 2,000 5,250 Miscellaneousexpense (5%of sales)Total expense 13,400 13,650 13,700 40,750f. Capital budgetAssets CostOven 10,000Proofing boxes 10,000Electric mixer 2,000Operation table 2,000Window displays 10,000 Implements 5,000Total 39,000g. Budget Income StatementApril ---June Total Sales 115,000Cost of goods sold 42,000Gross margin 73,000 Operating expense:Wages 19,500Rent 15,000 Miscellaneous 5,250Insurance 600 Depreciation 600Income from operation 32,050Tax expense 1,602.5Net income 30,447.5h. Cash budgetApril May June8,600 11,800 15,900 Beginning cashbalanceCash receipts and disbursements34,000 33,000 38,000 Collections fromcustomersPayments for(17,400) (13,600) (15,900) merchandise(13,400) (13,650) (13,700) Payment foroperating expenseNet cash receipts3,200 5,750 8,400 and disbursement3,200 5,750 8,400 Total cash increasefrom financingEnding cash11,800 17,550 25,950 balancei. Budget Balance SheetAssets 30.Jun.2014Current assetsCash 25,950 Accounts receivable 16,000 Inventory 1,000 Unexpired insurance 1,20044,150 Plant assetsEquipment and other 74,000 Accumulated depreciation 18,20055,800 Total assets99,950Liabilities and owners’ equityCurrent liabilitiesAccounts payable 32,20032,200 Owner’s equity67,750 Current liabilities and owner’s equity99,950●ConclusionAccording to the preparation of budget table, we know that our net profit is about 30,447,50.However, because of the high fixed costs, we should try our best to improve sales. That means we should improve sales by increasing our customers. So, the next thing we should do immedinatly is to increase the marketing managements like advertising.●Reference[01] PSB Academy. Preparing the Master Budget(p297-p302). Introduction to Management Accounting.2014.[02] PSB Academy. Making Managerial Decisions(p291-p296). Introduction to Management Accounting.2014.。

财务管理英文版166页PPT文档

Basket Wonders Statement of Earnings (in thousands) for Year Ending December 31, 2019a

Ⅰ.Primary Types of Financial Statements

Balance Sheet

A summary of a firm’s financial position on a given date that shows total assets = total liabilities + owners’ equity.

Examples of External Uses of Statement Analysis

Trade Creditors -- Focus on the liquidity of the firm. Bondholders -- Focus on the long-term cash flow of

Basket Wonders Balance Sheet (thousands) Dec. 31, 2019a

Cash and C.E.

$

a. How the firm stands on

90 Acct. Rec.c

a specific date.

394 Inventories

b. What BW owned.

16

Other Accrued Liab. d 100

Current Liab. e $ 500

Long-Term Debt f

530

Shareholders’ Equity

Com. Stock ($1 par) g

200

Add Pd in Capital g

财务管理制度英文版

IntroductionThe Financial Management System is a comprehensive framework designed to ensure the effective and efficient management of financial resources within an organization. This system encompasses a set of policies, procedures, and guidelines that are implemented to safeguard assets, optimize financial performance, and comply with legal and regulatory requirements. The following document outlines the key components of our Financial Management System.1. ObjectiveThe primary objective of our Financial Management System is to:- Ensure the accuracy, completeness, and reliability of financial information.- Maximize the value of the organization through sound financial planning and decision-making.- Comply with all applicable laws, regulations, and accounting standards.- Promote transparency and accountability in financial operations.2. Organizational StructureThe Financial Management System is managed by the Finance Department, which is responsible for:- Establishing and implementing financial policies and procedures.- Overseeing the preparation of financial reports and statements.- Managing the organization's cash flow and liquidity.- Ensuring compliance with internal controls and external regulations.3. Financial Policies and ProceduresOur Financial Management System includes the following key policies and procedures:- Budgeting: A comprehensive budgeting process is in place to ensurethat financial resources are allocated effectively and efficiently.- Accounts Payable: A robust accounts payable process is implemented to ensure timely payment of invoices and maintain vendor relationships.- Accounts Receivable: A systematic accounts receivable process is followed to ensure timely collection of receivables and minimize bad debt.- Cash Management: A cash management policy is in place to ensure adequate liquidity and minimize the cost of capital.- Investment Management: A well-defined investment policy is followed to manage the organization's investments and maximize returns.- Internal Controls: A strong internal control framework is established to safeguard assets, ensure compliance, and prevent fraud.- Compliance: Regular audits and reviews are conducted to ensure compliance with all applicable laws, regulations, and accounting standards.4. Financial ReportingThe Financial Management System requires the preparation of accurate and timely financial reports, including:- Balance Sheets: Provide a snapshot of the organization's financial position at a specific point in time.- Income Statements: Summarize the organization's revenues, expenses, and net income over a specific period.- Cash Flow Statements: Provide information about the organization's cash inflows and outflows during a specific period.- Statement of Changes in Equity: Detail the changes in theorganization's equity during a specific period.5. Training and CommunicationOur Financial Management System includes training programs for all employees to ensure they understand their roles and responsibilities in managing financial resources. Regular communication is maintained between the Finance Department and other departments to ensure a cohesive and effective financial management process.ConclusionThe Financial Management System is a crucial component of our organization's success. By following this system, we ensure theefficient and effective management of financial resources, promote transparency and accountability, and ultimately contribute to the organization's overall success.。

财务管理制度(中英文对照)

财务管理制度(中英文对照)Financial Management System一、概述Overview财务管理制度是企业为了规范和管理财务活动而建立的一套制度和规范。

它的目的是确保企业的财务活动得到合理的安排和有效的控制,以最大程度地实现财务目标。

下面是本公司财务管理制度的具体内容。

The financial management system is a set of rules and regulations established by a company to regulate and manage financial activities. Its purpose is to ensure that financial activities are properly organized and effectively controlled to maximize financial goals. The following is the specific content of the financial management system in our company.二、财务核算Financial Accounting1. 制度概述1. System Overview本公司财务核算制度由财务部门负责执行。

所有财务活动必须按照国家法律法规和会计准则进行核算和报告。

The financial accounting system in our company is implemented by the finance department. All financial activities must comply with national laws and regulations as well as accounting standards for accounting and reporting.2. 财务报表2. Financial Statements按照国家相关规定和会计准则,财务部门将每年编制并及时发布财务报表,包括资产负债表、利润表和现金流量表等。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

A)

responsibility accounting.

B)

contribution accounting.

C)

absorption accounting.

D)

operational budgeting.

Choosing the Budget Period

Operating Budget

1999

2000

Fairmont Inc. uses an accounting system that charges costs to the manager who has been delegated the authority to make decisions concerning the costs. For example, if the sales manager accepts a rush order that will result in higher than normal manufacturing costs, these additional costs are charged to the sales manager because the authority to accept or decline the rush order was given to the sales manager. This type of accounting system is known as:

Planning and Control

ቤተ መጻሕፍቲ ባይዱ

❖Planning -involves developing objectives and preparing various budgets to achieve these objectives.

Control -involves the steps taken by management that attempt to ensure the objectives are attained.

This budget is usually a twelve-month budget that rolls forward one month as the current month is completed.

2002

Participative Budget System

Top Management

Advantages of Budgeting

Communicating plans

Define goal and objectives

Think about and plan for the future

Coordinate activities

Advantages

Means of allocating resources

A) operational budgeting. B) zero-based budgeting. C) continuous budgeting. D) responsibility accounting.

Zero-Base Budgeting

Managers are required to justify all budgeted expenditures, not just changes in the budget from the previous year. The baseline is zero rather than last year’s budget.

Middle Management

Middle Management

Supervisor Supervisor Supervisor Supervisor

Flow of Budget Data

The Budget Committee

A standing committee responsible for

2001

The annual operating budget may be divided into quarterly

or monthly budgets.

2002

Choosing the Budget Period

Continuous or Perpetual Budget

1999

2000

2001

overall policy matters relating to the budget coordinating the preparation of the budget

A method of budgeting in which the cost of each program must be justified every year is called:

objectives of the various parts. C. It ensures that accounting records comply with generally accepted accounting

principles. D. It provides benchmarks for evaluating subsequent performance.

Uncover potential bottlenecks

Responsibility Accounting

Managers should be held responsible for those items — and only those items — that

the manager can actually control to a significant extent.

Which of the following is not a benefit of budgeting?

A. It uncovers potential bottlenecks before they occur. B. It coordinates the activities of the entire organization by integrating the plans and