会计学英文案例1revised

Income and Changes in Retained Earnings英文版会计学

Chapter 12

Income and Changes in Retained Earnings

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

Slide 12-2

Reporting the Results of Operations

Discontinued Operations

Income/Loss from operating the segment prior to disposal.

Income/Loss on disposal of the segment.

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

Information about net income is used by investors, creditors, and other financial statement users.

Normal, recurring revenue and expense transactions.

Unusual, nonrecurring events that affect net income.

$ 350,000

(105,000) (70,000) $ 175,000

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

Slide 12-11

Extraordinary Items

Material in amount. Gains or losses that

会计学原理23版 英文版教学书册Wild FAP 23e Ch24 IRM

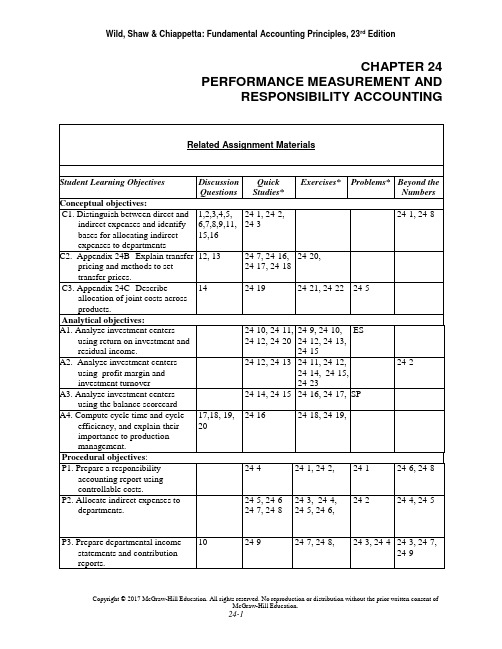

CHAPTER 24 PERFORMANCE MEASUREMENT AND RESPONSIBILITY ACCOUNTING*See additional information on next page that pertains to these quick studies, exercises and problems. SP refers to the Serial ProblemES refers to Excel SimulationsAdditional Information on Related Assignment MaterialConnectA vailable on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.Connect InsightThe first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed by an intuitive question and provide at-a-glance information regarding how an instructor’s class is performing. Connect Insight is available through Connect titles.The Serial Problem (SP) for Success Systems continues in this chapter.General LedgerAssignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post from the general journal all the way through the financial statements. Critical thinking and analysis components are added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide instant feedback to the student.Excel SimulationsAssignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student. Synopsis of Chapter RevisionsNEW opener—Ministry of Supply and entrepreneurial assignment.Reorganized chapter.Revised discussion of performance evaluation and decentralization.Revised discussion of Kraft Heinz responsibility centers.Revised exhibit on responsibility accounting.Revised discussion of responsibility accounting reports.Added NTKs on responsibility accounting, cost allocations, and balanced scorecard.Revised discussion of indirect expense allocations.New exhibit and discussion of general model of expense allocation.New exhibit on common allocation bases for indirect expenses.Revised discussion of preparing departmental income.New exhibit and formula for computing departmental income.Added short section on transfer pricing to the chapter.New Sustainability section with discussion of General Mills, Target and performance reporting, and Ministry of Supply example.Chapter OutlineNotes I.Responsibility AccountingA. Performance Evaluationrge companies are easier to manage if divided into smallerunits called divisions, segments, or departments.2.In decentralized organizations, decisions are made by unitmanagers rather than top management.3.In responsibility accounting, unit managers are evaluated onlyon what they are responsible for.4.The methods of performance evaluation vary for cost centers,profit centers and investment centers.a.Cost center−incurs cost or expenses without directlygenerating revenues (e.g. manufacturing department andservice department).b.Profit center−incurs costs and generates revenues (e.g.product centers).c.Investment center−incurs costs, generates revenues and isresponsible for effectively using center assets.5.Basis for evaluating performance:a.Cost center managers are evaluated on their success incontrolling costs compared to budgeted costs. Profit center:ability to generate more revenue than expenses.b.Profit center managers are evaluated on their success ingenerating income.c.Investment center managers are evaluated on their use ofinvestment-center assets to generate income.II.Controllable versus Uncontrollable CostsA.Controllable Costs -1.Those which a manager has the power to determine or at leastsignificantly affect the amount incurred.B. Uncontrollable costs –1.Are not within the manager’s control.2. A manager’s performance is evaluated using responsibilityreports that describe the department’s activities in terms ofcontrollable costs3.Distinguishing between controllable and uncontrollable costsdepends on the particular manager and the time period underanalysis.4.All costs are controllable at some level of management if the timeperiod is sufficiently long;5.Good judgment is required when identifying controllable costs.Chapter OutlineNotesC.Responsibility Accounting Performance Report1.Reports actual expenses that a manager is responsible for andtheir budgeted amounts.a.Management’s analysis of differences between actual andbudget often results in corrective actions.ed by upper management to evaluate effectiveness oflower-level managers in controlling costs.c.Recognizes that control over costs and expenses belongs toseveral layers of management.2.Responsibility Accounting Reporta.Provide relevant information for each management level.b.At lower levels, managers have limited responsibilities andtherefore fewer controllable costs.c.Responsibility and control broaden for higher-levelmanagers.III.Profit CentersA.The responsibility report focuses on how well each departmentcontrolled costs and generated revenues.B.The departmental income statement is a common way to reportprofit center performance.C.When computing department profits, two key accounting challengesinvolve allocating expenses:1.How to allocate indirect expenses, such as rent and utilities whichbenefit several departments.2.How to allocate service department expenses, such as payroll orpurchasing, that perform services that benefit severaldepartments.D.Direct and Indirect Expenses1.Direct Expenses are readily traced to a department.a.Incurred for sole benefit of that one department; no allocationrequired.b.Often, but not always, controllable costs.2.Indirect Expenses are incurred for joint benefit of more than onedepartment; can’t be readily traced to just one department.a.Allocated across departments benefiting from them.b.Ideally allocated using a cause-effect relation or, if cause-effect relation cannot be identified, allocated on a basisapproximating the benefit received by each department.c.Typically considered uncontrollable costs.Chapter OutlineNotesE.General Model – indirect and service department expenses areallocated across departments benefiting from them. Allocated using acause-effect relation. Sometimes hard to identify.1.Allocated Cost = Total Cost to Allocate x Percentage ofAllocation Base Used.F.Allocating Indirect Expenses – allocation bases vary acrossdepartments and organizations. Managers must use careful judgmentin developing allocation bases. Commonly used allocation bases:1.Wages and salaries –allocated using relative amount of hoursworked in each department.2.Rent and Utilities allocated based on portion of floor spaceoccupied. More valuable location may charge department higherrate.3.Advertising – allocated using a percentage of total sales.4.Depreciation – allocated using hours of depreciable asset used.G.Service Department expenses –provide support to an organization’soperating departments. Common allocation bases:1.Office, personnel, and payroll expenses – allocated based onnumber of employees in each department.2.Purchasing costs – allocated based on dollar amount of purchasesor number of purchase orders processed.3.Maintenance expenses – allocated based on square footage.H.Departmental Income Statements1.Departmental income is computed using the following formula:Departmental income = Dept. sales – Dept. direct expenses –Allocated indirect expenses – Allocated service dept. expenses.2.Four Steps for allocating costs and preparing departmentalincome statements:a.Step one – accumulate revenues and direct and indirectexpenses by department. Involves collecting the necessarydata from general company and departmental accounts.i.Direct and indirect expenses include salaries, depreciationand supplies expenses.b.Step two – allocate indirect expenses across both service andoperating departments.i. Uses a departmental expense allocation spreadsheetshown in Exhibit 24.10.ii.After selecting allocation bases, indirect expenses arerecorded in company accounts and allocated to bothoperating and service departments.Chapter OutlineNotesc.Step three – allocate service department expenses tooperating departments using a departmental expenseallocation spreadsheet. After service department costs areallocated, no expenses remain in the service departments.d.Step four – prepare departmental income statements using thedepartmental expense allocation spreadsheet.i. Actual service department expenses are compared withbudgeted amounts to help assess cost center performance.ii.Amounts in the operating department columns are used toprepare departmental income statements. (Exhibit 24.15)I.Departmental Contribution to Overhead (see Exhibit 24.12)1.Departmental income statements not always best for evaluatingeach profit center’s performance especially when indirectexpenses are a large portion of total expenses.2.Evaluate using departmental contributions to overhead a reportof the amount of sales less direct expenses.3.Behavioral Aspects of Departmental Performance Reports –a.Indirect expenses are typically uncontrollable, so a better wayto evaluate is using departmental contribution to overhead.b.Including indirect expenses in department manager’sperformance evaluation can lead to the manager being morecareful in using service departments.c.Some companies allocate budgeted service department costsso operating departments are not held responsible forexcessive costs from service departments.IV.Investment CenterA.Financial Performance Evaluation Measures include:1.Return on investment, return on assets, computed as investmentcenter income / by investment center average invested assets.2.Residual income – Expressed in dollars. Encourages divisionmanagers to accept all opportunities that return more than targetincome. Computed as investment center income – targetinvestment center income.3.Profit margin and investment turnover – split return oninvestment into two measures – profit margin and investmentturnover.a.Profit margin measures income earned per dollar of salescomputed as investment center income divided by investmentcenter sales. Usually use income before tax. Expressed as apercent.b.Investment turnover measures how efficiently an investmentcenter generates sales from its invested assets. Calculated asinvestment center sales divided by investment center averageassets. Expressed as the number of times assets wereconverted into sales.Chapter OutlineNotes4.Nonfinancial Performance Evaluation Measures –using solelyfinancial measures has limitations. Companies can considernonfinancial measures to help in evaluating division manager’sperformance.5.Balanced Scorecard: system of performance measures,including nonfinancial measures used to assess company anddivision manager performance. Requires managers to think oftheir company from four perspectives.a.Customer: what do they think of us?b.Internal process: which of our operations are critical?c.Innovation and learning: how can we improve?d.Financial: what do our owners think of us?V.Decision Analysis Cycle Time and Cycle EfficiencyA.As lean manufacturing practices help companies move toward justin time manufacturing it is important for companies to reduce thetime it takes to manufacture its products and improve efficiency.1.Cycle time measures the time element which describes the timeit takes to produce a product or service.Cycle time = Process + Inspection + Move + WaitTime Time Time Timea.Process time is considered value-added time – it is the onlyactivity in cycle time that adds value to the product from thecustomer’s perspective. The other three activities areconsidered non-value-added time: they add no value to thecustomer.2.Cycle Efficiency measures production efficiency. It is the ratioof value added time to total cycle time.Cycle Efficiency = Value added timecycle timea.If the cycle efficiency is low, the company should evaluatethe production process to see if it can identify ways toreduce the non-value added activities.VI.Appendix 24A – Cost Allocations uses the general model of costallocation to show how the cost allocations in Exhibits 24.10 and 24.11for A-1 Hardware. Rent expense, utilities expense, advertising expenseand insurance expense are allocated first. Then, the two servicedepartment’s expenses are allocated to the three operating departments.Chapter OutlineNotes VII.Appendix 24B – Transfer PricingThe price used to record transfers between divisions in the samecompany is called a transfer price. Can be used in cost, profit andinvestment centers.A.If there is no excess capacity, the internal supplier will not accept atransfer price less than the market price. This is called market basedtransfer pricing.B.If there is excess capacity, the internal supplier should accept a pricebetween the costs to manufacturer the part and the market price.This is called cost based transfer pricing.C.Other issues to consider in determining transfer prices include:1.Market price may not exist2.Cost controls3.Division managers’ negotiation4.Nonfinancial factors to consider include: quality control,reduced lead times and impact on employee morale.III.Appendix 24C – Joint CostsA.Joint Costs−the costs incurred to produce or purchase two or moreproducts at the same time; similar to indirect expense in that it’sshared across more than one cost object.1.Ignored when deciding to sell product as is or process further.2.Allocated to different products produced from it when total costof each product must be estimated (e.g., preparation of GAAPfinancial statements).3.Allocation basesa.Physical basis−allocates joint costs using physicalcharacteristics such as ratio of pounds, cubic feet or gallonsof each joint product to the total pounds, cubic feet orgallons of all joint products flowing from the cost; does notreflect the extra value flowing into some products or theinferior value flowing into others. Not the preferred method.b.Value basis−allocates joint cost in proportion to the salesvalue of the output produced by the process at the “split-offpoint”.Chapter 24 Alternate Demo ProblemJack and Susan Roberts own a farm that produces potatoes. Based on a review of the income statement shown below, Jack remarked that they should have fed the No. 3 potatoes to the pigs; then they would have avoided the loss from the sale of the those potatoes.JACK AND SUSAN ROBERTSIncome from the Production and Sale of PotatoesFor Year Ended December 31, 20xxResults by GradeSales by grades:No. 1, 300,000 lbs. $0.045 per lb.No. 2, 500,000 lbs. $0.04 per lb.No. 3, 200,000 lbs. $0.03 per lb.CombinedCosts:Land preparation, seed,planting,cultivating @ $0.01422 per lb.Harvesting, sorting, grading@ $0.01185 per lb.Marketing @ $0.00415 per lb.Total costsNet income (or loss)Jack and Susan divided their costs among the grades on a per pound basis, because their records do not show cost per grade. However, their records did show that $4,020 of the $4,150 of marketing costs represented the cost of placing the No. 1 and No. 2 potatoes in bags and hauling them to the warehouse of the produce buyer. Bagging and hauling costs were the same for both grades. The remaining $130 represented the cost of loading the No.3 potatoes into the trucks of the potato starch factory that bought these potatoes in bulk and picked them up at the farm.Required:Prepare an income statement that will better show the results of producing and marketing the each of the grades of potatoes.Chapter 24 Alternate Demo Problem: SolutionJACK AND SUSAN ROBERTSIncome from the Production and Sale of PotatoesFor Year Ended December 31, 20xxRevenue from sales:Costs:Land preparation, seed,planting, cultivatingHarvesting, sorting, gradingMarketingTotal costsNet incomeCOST ALLOCATIONSLand preparation, seed, planting, andcultivating:No. 1: $13,500 / $39,500 x $14,220 = No. 2: $20,000 / $39,500 x $14,220 = No. 3: $ 6,000 / $39,500 x $14,220 = $ 4,8607,2002,160 $14,220Harvesting, sorting, and grading:No. 1: $13,500 / $39,500 x $11,850 = No. 2: $20,000 / $39,500 x $11,850 = No. 3: $ 6,000 / $39,500 x $11,850 = $ 4,0506,0001,800 $11,850Marketing:No. 1: $13,500 / $33,500 x $4,020 = No. 2: $20,000 / $33,500 x $4,020 = $1,620 2,400Subtotal bagging and hauling costs 4,020 No. 3: Loading costs 130$4,150。

会计专业英语作文

会计专业英语作文As an accounting major, I have always been fascinatedby numbers and financial statements. Crunching numbers and analyzing data excites me, and I find joy in solving complex accounting problems.One of the most important skills I have learned in my accounting studies is attention to detail. In this field, even the smallest mistake can have significant consequences. That's why I always double-check my work and ensure that everything is accurate before submitting any reports.Another key aspect of accounting is ethics. As accountants, we have a responsibility to maintain the highest level of integrity and honesty in our work. This means following ethical guidelines and upholdingprofessional standards at all times.In addition to technical skills, communication is also crucial in accounting. Whether it's explaining financialinformation to clients or collaborating with colleagues, effective communication is essential for success in this field. Being able to clearly convey complex financial concepts is a valuable skill that I have honed through my accounting studies.Overall, studying accounting has equipped me with the knowledge and skills necessary to excel in this field. I am confident in my abilities and excited to embark on a career that allows me to utilize my passion for numbers and problem-solving.。

会计英语案例

会计英语案例(1)On August 1, the company A sold 200,000 of inventory goods to B company, value added tax amounted to 34000, payment has not been received. Meanwhile carrying-over inventory goods sales cost 180000Dr: Account Receivable --B company 234000Cr: Basic Operating Revenue 200,000VAT Payable (output tax) 34000Dr: Basic Dperating Cost 180000Cr: Merchandise Inventory 180000(2) On August 2, A company will value 30,000 yuan ofinventory goods sold to B company, VAT totaling $5,100, payment received. Meanwhile carrying-over inventorygoods sales cost 27000 yuan.Dr: Cash In Bank 35100Cr: Basic Operating Revenue 30,000VAT payable (output tax) 5,100Dr: Basic Dperating Cost 27,000Cr: Merchandise Inventory 27,000(3) On August 3, A company purchases raw material production from D company with 15 tons, unit price 5000 yuan, VAT 12750 yuan, payment paid. Confirm the material in warehouse.Dr: Raw Materials 75000VAT payable (VAT on purchase) 12750Cr:Cash In Bank 87750(4) On August 4, production workshop for A productionfor 50000, workshop consumed for 500, the generalmanager's office of recipients for 500.Dr: Cost Of Production 50000Manufacturing Cost 500Administrative Cost 500Cr: Raw Materials 51000(5) On August 5, received B company forwarded transfer cheque, amount 234000 yuan, owed sales payment for goods.Dr: Cash In Bank 234000Cr: Account Receivable -- B company 234000 (6) On August 5, this provision should be borne by the wage 500,000 yuan. General manager office management personnel salary 100000 yuan, the finance department personnel salary 50000 yuan, production personnel250,000 yuan,Dr : Manufacturing Cost 250,000Administrative Cost 150,000Selling Expenses 100,000Cr: Wages Payable 500,000(7) 6, subject to bank borrowing three-year borrowing $200,000.Dr:Cash In Bank 200,000Cr: Long-term Loans Payable 200,000(8) 6 to B company sellgoods, the price 1200000 ,value-added tax 204000, but not yet received cash,corresponding inventory goods in the sales cost800,000.Dr:Account Receivable -- B company 1404000Cr: Basic Operating Revenue 1200000VAT Payable (output tax) 204000Dr: Basic Dperating Cost 800,000Cr: Merchandise Inventory 800,000(9) 7, marketing material batch, cost 3000, price 4000 yuan, VAT 680 yuan, receive cash a cheque, payment in the bank.Dr:Cash In Bank 4680Cr: Other Operating Revennue 4000VAT Payable (output tax) 680Dr:Other Operating Cost 3000Raw Materials 3000(10) 8 sales to B company materials, materials price 165,000, value-added tax 28050, at the same time receive transfer cheque, the materials cost 100000.Dr:Cash In Bank 193050Cr: Other Revenue 165000VAT Payable (output tax) 28050Dr: Other Operating cost 100,000Cr: Raw Material 100,000(11) 8, prescribing transfer cheque, pay fee 80 000 .Dr:Selling Expenses 80,000Cr:Cash In Bank 80,000(12) 10, A will cash cheque 500,000 yuan, issuing this month salary.Dr: Wages Payable 500,000Cr:Cash In Bank 500,000(13) 15, prescribing transfer cheque, pay housing for repairs to 8 000 yuan, including workshop 3 000 yuan,the factory department 5 000 yuan.Dr: Manufacturing Cost 3000Administrative Cost 5000Cr:Cash In Bank 8,000(14) 18, receive a bank requisition, pay bank settlement poundage 8 600 yuan.Dr: Finance Expenses 8600Cr: Cash In Bank 8600(15) 20, last month from the bank borrow a month of borrowing $100,000 expired, month interest rates, open transfer cheque 4%, return principal and interest.Dr: Short-term Loans Payable 100,000Finance Expenses 4000Cr:Cash In Bank 104000(16) 20, prescribing transfer cheque, payment 10,000 yuan, including bill workshop 1500 yuan, office of general manager, sales department 3500 5000 yuan.Dr: Manufacturing Costs 1,500Administrative Cost 3,500Selling Expenses 5000Cr:Cash In Bank 10000(17), 26 provision for fixed assets depreciation cost, including this month, workshop 29 20,000 yuan, general manager office 8 000 yuan, sales department 2 000 yuan.Dr: Manufacturing Cost 29,000Administrative Cost 8,000Selling Expenses 2000Cr: Accumulated depreciation 39000(18) 31, The cost of the project finishs 50% includedin the cost of inventory goods.Dr: Cost Of Production 34000Cr: Manufacturing Expenses 34000Dr: Merchandise Inventory 17,000Cr: Cost Of Production17,000(19) 31, profit and loss of this month each account balance into "profit of the current year" account, and calculates the total profit.Dr: Basic Operating Revenue 1430000Other Operating Revenue 169000Cr: Current Year Profit 1599000Dr: Current Year Profit 1476600Cr: Basic Operating Cost 1007000Other Operating Cost 103000Administrative Cost 167000Selling Expenses187000Finance Expenses 12600Profit total = 1599000-1476600= 122400(20) 31, according to 25% of total profits payable income tax calculated, and takes "income taxes" account value into "profit of the current year," netcalculating profit.Dr: Income Tax Expenses 30600Cr: Income Tax Payable 30600Dr: Current Year Profit 30600Cr: Income Tax Expenses 30600Dr: Current Year Profit 91800Cr: Undistributed Profit 91800Net profit 122400-30600= 91800(21) 31, according to the net profit of 15% and 50% respectively surplus reserve and provision to investors profits.Dr: Profit Distribution -- the Statutory Reserve7717.5Any Surplus Reserve 3858.75Dividends Payable 38587.5. -Cr: Legal Surplus Reserve 7717.5Any Surplus Reserve 3858.75Dividends Payable 38587.5(22) carryover from the profit of the current year and profit distribution other account balances into profit distribution - undistributed profit general ledger.Dr: Profit Distribution - Undistributed Profit50163.75Cr:Profit Distribution -- the Statutory Reserve 7717.5Any Surplus Reserve 3858.75Dividends Payable 38587.5.PostingAccount Receivable Basic Operating Revenue234000 234000 143000 2000001404000 300001404000 1200000 0Tax Payable Finance Expenses12750 34000 8600 126005100 4000204000680 02805030600289680Accumulation Depreciation Current Year Profit 39000 1476600 159900039000 3060091800Short-term Loans Payable Basic Dperating Cost 100000 180000 100700027000100000 8000000 Merchandise Inventory Cash In Bank17000 180000 35100 8775027000 234000 80000800000 200000 500000990000 4680 800019305 860010400010000131520Income Tax Raw Material30600 30600 75000 5100030000 10000079000Manufacturing Cost Administrative Cost500 34000 500 1670003000 1500001500 500029000 35000 8000Inappropriate Profit Wages Payable59670 91800 500000 500000Blance Sheet August 31,2010AssetsQM QC Liabilities and Owners'Equity QM Cash788,480920,000Short-term Loans Payable 400,000500,000AccountsReceivoble200,400600,000Tax Payable 509,680220,000Inventory548,0001,300,000Dividends Payable 45900Fix Assets600,000600,000Long-term Loans Payable 800,000600,000Less;AccumlationDeprecation39,000 Total Liabilities 1,755,5801,320,000Owners'EquityCapital Stock 2,000,0002,000,000Surplus Reserve 11,370100,000Undistributed Profit 32,130Total Fix Assets 561,000600,000Total Owners'Equity214,5902,100,00032130 0Long-term Loans Payable Other Operating Cost 200000 3000 103000100000200000 0Other Operating RevenueSelling Expenses169000 4000 100000 187000165000 8000050000 2000Dividends Payable Surplus Reserue45900 918045904590013770Cost Of Production 50000 11050150000 59501000002210011900317000Total Assets3,901,4803,420,000Total Liabilitiesand Owners'Equity3,901,4803,420,000A CompanyIncome StatementAugust 31,2010Operating Revenue1,599,000 Cost of Good Sold111,000 Administrative Cost167,000 Selling Expenses187,000 Financed Expenses126,000 Total Profit122,400 Income Tax Expense30,600 Net Income91,800。

会计学课件(英文版)1

How Much Cash Should a Business Have?

Financial Assets

Cash

Receivables

Short-term Investments

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

All reconciling items on the book side require an adjusting entry to the cash account.

Irwin/McGraw-Hill

Balance per Depositor

+ Deposits by Bank (credit memos) - Service Charge - NSF Checks

Cash Over and Short is debited for shortages and credited for overages.

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

Bank Statements

Shows the beginning bank balance, deposits made, checks paid, other debits and credits in the month, and the ending bank balance.

Estimated collectible amount

Irwin/McGraw-Hill

?The McGraw-Hill Companies, Inc., 1999

会计学英文案例1-revised-推荐下载

Photographic Equipment, which worth $25,000 and 50,000, respectively.Philip received $97,500 of capital.

1

Received $6,000 to provide Photographic service in the next 12

0 Expenses

5010 0

5020 0

Salary Expense Rent Expense

5030 Utilities Expense 0

5040 Photographic Supplies Expense 0

5050 Office Supplies Expense 0

对全部高中资料试卷电气设备,在安装过程中以及安装结束后进行高中资料试卷调整试验;通电检查所有设备高中资料电试力卷保相护互装作置用调与试相技互术通关,1系电过,力管根保线据护敷生高设产中技工资术0艺料不高试仅中卷可资配以料置解试技决卷术吊要是顶求指层,机配对组置电在不气进规设行范备继高进电中行保资空护料载高试与中卷带资问负料题荷试22下卷,高总而中体且资配可料置保试时障卷,各调需类控要管试在路验最习;大题对限到设度位备内。进来在行确管调保路整机敷使组设其高过在中程正资1常料中工试,况卷要下安加与全强过,看2度并22工且22作尽22下可22都能2可地护1以缩关正小于常故管工障路作高高;中中对资资于料料继试试电卷卷保破连护坏接进范管行围口整,处核或理对者高定对中值某资,些料审异试核常卷与高弯校中扁对资度图料固纸试定,卷盒编工位写况置复进.杂行保设自护备动层与处防装理腐置,跨高尤接中其地资要线料避弯试免曲卷错半调误径试高标方中高案资等,料,编5试要写、卷求重电保技要气护术设设装交备备4置底高调、动。中试电作管资高气,线料中课并3敷试资件且、设卷料中拒管技试试调绝路术验卷试动敷中方技作设包案术,技含以来术线及避槽系免、统不管启必架动要等方高多案中项;资方对料式整试,套卷为启突解动然决过停高程机中中。语高因文中此电资,气料电课试力件卷高中电中管气资壁设料薄备试、进卷接行保口调护不试装严工置等作调问并试题且技,进术合行,理过要利关求用运电管行力线高保敷中护设资装技料置术试做。卷到线技准缆术确敷指灵设导活原。。则对对:于于在调差分试动线过保盒程护处中装,高置当中高不资中同料资电试料压卷试回技卷路术调交问试叉题技时,术,作是应为指采调发用试电金人机属员一隔,变板需压进要器行在组隔事在开前发处掌生理握内;图部同纸故一资障线料时槽、,内设需,备要强制进电造行回厂外路家部须出电同具源时高高切中中断资资习料料题试试电卷卷源试切,验除线报从缆告而敷与采设相用完关高毕技中,术资要资料进料试行,卷检并主查且要和了保检解护测现装处场置理设。备高中资料试卷布置情况与有关高中资料试卷电气系统接线等情况,然后根据规范与规程规定,制定设备调试高中资料试卷方案。

会计专业教案模板范文英语

Introduction:This course plan is designed for students majoring in accounting. The purpose of this course is to provide students with a comprehensive understanding of accounting principles, practices, and skills required in the field. The course will cover various topics, including financial accounting, management accounting, auditing, taxation, and corporate finance. Through this course, students will develop critical thinking, problem-solving, and analytical skills necessary for a successful career in accounting.Course Overview:1. Course Duration: 16 weeks2. Course Hours: 2 hours per week3. Total Hours: 32 hoursCourse Objectives:1. To understand the fundamental concepts and principles of accounting.2. To learn the process of financial accounting, management accounting, auditing, taxation, and corporate finance.3. To develop practical skills in accounting software and financial analysis.4. To enhance critical thinking, problem-solving, and analytical skills.5. To build a strong foundation for further studies and a career in accounting.Course Outline:Week 1: Introduction to Accounting- Definition and importance of accounting- Types of accounting- Accounting ethics and professional standardsWeek 2: Financial Accounting- Accounting equation and basic accounting principles- Double-entry bookkeeping system- Recording and summarizing transactionsWeek 3: Financial Statements- Income statement- Balance sheet- Statement of cash flows- Statement of retained earningsWeek 4: Adjusting Entries and Financial Statements- Adjusting entries for accruals, deferrals, and estimates - Adjusted trial balance- Financial statement analysisWeek 5: Management Accounting- Cost concepts and cost behavior- Cost-volume-profit analysis- Budgeting and variance analysisWeek 6: Financial Management- Time value of money- Capital budgeting- Financial statement analysis for investment decisions Week 7: Auditing- Introduction to auditing- Audit objectives and procedures- Internal control and risk assessmentWeek 8: Taxation- Introduction to taxation- Taxation of individuals and corporations- Tax planning and complianceWeek 9: Accounting Software and Technology- Introduction to accounting software- Data entry and financial reporting- Financial analysis toolsWeek 10: Case Studies in Accounting- Analyzing real-world accounting situations- Ethical dilemmas and professional judgmentWeek 11: Group Project- Students will work in groups to analyze a real company's financial statements and provide recommendations for improvementWeek 12: Exam Preparation- Review of course material and preparation for the final examWeek 13: Final Exam- Comprehensive examination covering the entire courseWeek 14: Project Presentation- Groups will present their findings from the group projectWeek 15: Review and Feedback- Review of course material and feedback from studentsWeek 16: Course Completion- Course evaluation and feedback from studentsAssessment:1. Quizzes (10%)2. Homework assignments (20%)3. Group project (20%)4. Midterm exam (20%)5. Final exam (30%)Conclusion:This accounting professional course plan aims to provide students with a comprehensive understanding of accounting principles and practices. By the end of the course, students will be well-prepared for further studies and a career in accounting. The course emphasizes practical skills, critical thinking, and ethical considerations to ensure students are ready to excel in the field.。

会计学英文实验

Less:Sales discount

Sales return and allowance

Net Sales

Less: COGS

Gross Profit

Less:expense

Net income

Carl Haupt Consulting

Balance Sheet

December 31, 2010

Dec1

Prepaid office rent, $2000 for 4 month

Dec 1

Borrowed $10,000 from bank, signing a six-month,8% note payable for that amount.

Dec 1

Haupt believes the company will need $500,000 and plans to raise the capital by issuing 6%, 10 year bonds on January. The bonds pay interest semiannually on January 1 and July 1.

Dec1

Paid cash for an equipment--computer, $2,000. This equipment is expected to remain in service for five years

Dec1

Purchase office equipment on account, $3,600. The equipment should last for five years

2.Calculate the ending balance for each account, and prepare adjusted trial balance on December 31

会计学 实例综合大全

CASE 1 PREPARE THE FINANCIAL ST ATEMENTSThe amounts of (a) the assets and liabilities of Aspen Supply Co. as of December 31, 2004, and (b) the revenues and expenses of the company for the year ended on that date follow. The items are listed in alphabetic al order. Accounts payable 12 000 Notes payable 31 000Accounts receivable 3 000 Property taxexpense2 000Building 56 000 Rent expense 14 000Cash 7 000 Salary expense 38 000Equipment 21 000 Service revenue 108 000Interest expense 4 000 Supplies 7 000Interest payable 1 000 Utilities expense 3 000Land 8 000The owner’s beginning balance , Linda Elkins, Capital, was $43 000, and during the year Elkins withdrew $32 000 for personal use.REQUIRED:1.Prepare the income statement of Aspen Supply Co. for the year ended December 31, 2004.2.Prepare the company’s statement of owner’s equity for the year ended December 31, 2004.3.Prepare the company’s balance sheet at December 31, 2004.4.Answer these questions about the companya.Was the result of operations for the year a profit or a loss? How much?b.Did Elkins drain off all the earnings for the year, or did she build the company’s capital during theperiod? How would her actins affect the company’s ability to borrow in the future?CASE 2 PREPARE THE CONRECT BALANCE SHEETThe bookkeeper of Haynes Editorial Service prepared the balance sheet of the company while the accountant was ill. The balance sheet contains numerous errors. In particular, the bookkeeper knew that the balance sheet should bal ance, so he plugged in the owner’s equity amount to achieve this balance. The owner’s equity amount, however, is not correct. All other amounts are accurate, but some are out of place.HAYNES EDITORIAL SERVESEBalance SheetREQUIRED:1.Prepare the correct balance sheet, and date it correctly. Compute total assets, total liabilities, and owner’sequity.2.Identify the accounts that should not be presented on the balance sheet and state why you excluded themfrom the correct balance sheet you prepared for requirement 1.CASE 3 RECORD TRANSACTIONS AND PREPARE THE FINANCIAL ST ATEMENTAllen Musser started a consulting service and during the first month of operations(June 2003) completed the following selected transactions:a.Musser began the business with an investment of $5,000 cash and a building valued at $60,000. Thebusiness gave Musser’s equity in the business.b.Borrowed $30,000 from the bank; signed a note payable.c.Purchased office supplies on account, $2,100.d.Paid $18,000 for office furniture.e.Paid employee’s salary. $2,200.f.Performed consulting service on account for client, $5,100.g.Paid $800 of the account payable created in transaction(c).h.Received a $600 bill for advertising expense that will be paid in the near future.i.Performed consulting service for customers and received cash,$1,600.j.Received cash on account, $1,200k.Paid the following cash expenses:(1) Rent on land, $700; (2) Utilities, $400l.Withdrew $7,500 for personal use.REQUIED:1.Open the T-accounts.2.Record each transaction directly in the T-account without using a journal, using the letters to identifythe transactions.3.Prepare the trial balance of Musser Consulting Service at June 30, 2003.4.Prepare the income statement, the statement of owner’s equity, and the balance sheet of MusserConsulting Service at the June 30, 2003.CASE 4 MAKE DECISION: TO BUY A COMPANY OR NOT?Benjamin O’henry has owened and operated O’Henry Data Services since its beginning ten years ago. From all appearances, the business has prospered. In the past few years, you have become friends with O’Henry and his wife through your church. Recently , O’Henry mentioned that he h as lost his zest for the business and would consider selling it for the right price. Y ou are interested in buying this business and obtain its most recent monthly unadjusted trial balance, which follows.O’HENRY’S DA TA SERVICESUnadjusted Trial BalanceRevenues and expenses vary from month to month, and November is a typical month. Y our investigation reveals that the unadjusted trial balance does not include the effects of monthly revenues of $2,100 and monthly expenses totaling $2,750. If you were to buy O”Henry’ Data Services. Y ou would hire a manager who would require a monthly salary of $3,000.REQUIRED:1.The most you would pay for the business is 20 times the monthly net income you could expect to earn formit. Compute the possible price.2.The least O”Henry will take for the business is his en ding capital. Compute this amount.3.Under these conditions, how much should you offer O”Henry? Give your reason.CASE 5 Was Maltbee’s summer work successful?Doug Maltbee formed a lawn service business as a summer job. To start t business on May 1, he deposited $1,000 in a new bank account in the name of the proprietorship. The $1,000 consisted of a $600 loan from his father and $400 of his own money. Doug rented lawn equipment, purchased supplies, and hired fellow students to mow and trim his customer’s lawns.At the end of each month, Doug mailed bills to his customers. On August 31, he was ready to dissolve the business and return to Louisiana State University for the fall semester. Because he was so busy, he kept few records other than his checkbook and a list of amounts owed to him by customers.At August 31, Doug’s checkbook shows a balance of $690, and his customers still owe him $500. During the summer, he collected $4,250 from customers. His checkbook lists payments for supplies totaling $400, and he still has gasoline, weedeater cord, and other supplies that cost a total of $50. He paid his employees $1,900, and he still owes them $200 for the final week of the summer.Doug rented some equipment from Scholes Machine Shop. On May 1, he signed a six-month lease on mowers and paid $600 for the full lease period. Scholes will refund the unused portion of the prepayment if the equipment is in good shape. In order to get the refund, Doug has kept the mowers in excellent condition. In fact, he had to pay $300 to repair a mower.To transport employees and equipment to jobs, Doug used trailer tat he bought for $300. He figures that the summer’s work used up one-third of the trailer that he bought for the business. Checkbook lists a payment of $460 for cash withdrawals by Doug during the summer. Doug paid his father back during August. REQUIRED:1.Prepare the income statement of Maltbee Lawn Service for the four months May through August.2.Prepare the classified balance sheet of Maltbee Lawn Service at August 31.3.Was Maltbee’s summer work successful? Give the reason for your answer.CASE 6 TO ADJUST USING THE WORKSHEETFresh Market Grocery’s trial balance pertains to December 31, 2001FRESH MARKET GROCERYTRIAL BALANCEDecember 31, 2001Additional data at December 31,2001:a.Insurance expense for the year, $6,090.b.Store fixtures have an estimated useful life of ten years and are expected to beworthless when they are retired from service.c.Accrued salaries at December 31, $1,260.d.Accrued interest expense at December 31, $870.e.Store supplies on hand at December 31,$760.f.Inventory on hand at December 31, $94,780.REQUIRED:plete Fresh Market’s work sheet for the year ended Decembe r 31,2001.Key adjusting entries by letter.2.What was the net income for the year ended December 31,2001?3.What was the ending balance of the capital account?Case 07 Determining cost of purchaseThe following is an excerpt from a conversation between Joe Hitachi and Kim Kenwood. Joe is debating whether to buy a stereo system from Audio-Tec, a locally owned electronics store, or Powerhouse, a mail-order electronics company.Joe: Kim, I don’t know what to do about buying my new stereo.Kim: So what's the problem?Joe: Well, I can buy it locally at Audio-Tec for $689.95. However, Powerhouse Electronics has the same system listed for $699.99.Kim: So what’s the big deal? Buy it from Audio-Tec.Joe: It’s not quite that simple. Powerhouse said someth ing about not having to pay sales tax, since I was out-of-state.Kim: Y es that’s a good point. If you buy it at Audio-Tec, they’ll charge you 6% sales tax.Joe: But Powerhouse Electronics charges $15 for shipping and handing. If I have them send it next-d ay air, it’ll cost an additional $20 for shipping and handling. Kim: I guess it is a little confusing.Joe: That’s not all. Audio-Tec will give an additional 2% discount if I pay cash. Otherwise, they will let me use my MasterCard, or I can pay it of in three monthly installments (the interest rate for a month is 1.5%).Kim: Anything else???Joe: Well…Powerhouse says I have to charge it on my MasterCard. They don’t accept checks.Kim: I am not surprised. Many mail-order houses don’t accept checks.Joe: I give up. What would you do?Required:1.Assuming that Powerhouse Electronics doesn’t charge sales tax on the sale to Joe, which company is offering the best buy?2.What might be some consideration other than price that might influence Joe’s decision on where to buy the stereo system?Case 08 Sales discountsY our sister operates Escapade V ideo Company, a videotape distributorship that is in its third year of operation. The following income statement was recently prepared for the year ended October 31, 1997:Escapade V ideo CompanyIncome statementFor the Y ear Ended October 31, 1997Y our sister is considering a proposal to increase net income by offering sales discounts of 2/15, n/30, and by shipping all merchandise FOB shipping point. Currently, no sales discounts are allowed and merchandise is shipped FOB destination. It is estimated that these credit terms will increase net sales by 10%. The ratio of the cost of merchandise sold to net sales is expected to be 70%. All selling and administrative expenses are expected to remain unchanged, except for store supplies, miscellaneous selling, office supplies, and miscellaneous administrative expenses, which are expected to increase proportionately with increased net sales. The amounts of these preceding items for the year ended October 31, 1997, were as follows:Store supplies expense 2000Miscellaneous selling expense 1000Office supplies expense 800Miscellaneous administrative expense 1500The other income and other expense items will remain unchanged. The shipment of all merchandise FOB shipping point will eliminate all transportation-out expenses, which for the year ended October 31, 1997, were $18000.Required:Prepare a projected single-step income statement for the year ending October 31,1998, based on the proposal.CASE 09 How much cash did ABC collect in month 4 and 5?ABC Ltd makes all its sales on credit. For customers who pay within ten days of purchase, ABC gives a discount of 5 per cent.(Assume all sales are made evenly over the month and there are 30 working days every month.) ABC knows that, on average, 50 per cent of its customers pay within the discount period, 40 per cent pay within 30 days. And 8 per cent within 60 days. Two per cent are uncollectable.Month 1 1 200 000Month 2 1 300 000Month 3 880 000Month 4 1 000 000Month 5 1 250 000CASE 10 FIFO AND LIFOThe Ramayya Corporation is nearing the end of its first year in business. The following purchasesSales for the year will be 5,000 units for $120,000. Expenses other than cost of goods sold will be $20,000.The president is undecided about whether to adopt FIOF or LIFO for income tax purposes. The company has ample storage space for up to 7,000 units of inventory. Inventory prices are expected to stay at $15 per unit for the next few months.REQUIRED:1.What would be the net income before taxes, the income taxes, and the net income after taxesfor the year under (a) FIFO and (b) LIFO? Income tax rates are 40%.2.If the company sells its year-end inventory in year two @ $24 per unit and goes out ofbusiness, what would be the net income before taxes, the income taxes, and the net income after taxes under (a) FIFO and (b) LIFO? Assume that other expenses in year two are $20,000.3.Repeat requirements 1 and 2, assuming that the 4,000 units @ $ 15 purchased in Decemberwere not purchased until January of the second year. Generalize on the effect on net income of the timing of purchases under FIFO and LIFO.。

会计学 实例综合大全

CASE 1 PREPARE THE FINANCIAL ST ATEMENTSThe amounts of (a) the assets and liabilities of Aspen Supply Co. as of December 31, 2004, and (b) the revenues and expenses of the company for the year ended on that date follow. The items are listed in alphabetic al order. Accounts payable 12 000 Notes payable 31 000Accounts receivable 3 000 Property taxexpense2 000Building 56 000 Rent expense 14 000Cash 7 000 Salary expense 38 000Equipment 21 000 Service revenue 108 000Interest expense 4 000 Supplies 7 000Interest payable 1 000 Utilities expense 3 000Land 8 000The owner’s beginning balance , Linda Elkins, Capital, was $43 000, and during the year Elkins withdrew $32 000 for personal use.REQUIRED:1.Prepare the income statement of Aspen Supply Co. for the year ended December 31, 2004.2.Prepare the company’s statement of owner’s equity for the year ended December 31, 2004.3.Prepare the company’s balance sheet at December 31, 2004.4.Answer these questions about the companya.Was the result of operations for the year a profit or a loss? How much?b.Did Elkins drain off all the earnings for the year, or did she build the company’s capital during theperiod? How would her actins affect the company’s ability to borrow in the future?CASE 2 PREPARE THE CONRECT BALANCE SHEETThe bookkeeper of Haynes Editorial Service prepared the balance sheet of the company while the accountant was ill. The balance sheet contains numerous errors. In particular, the bookkeeper knew that the balance sheet should bal ance, so he plugged in the owner’s equity amount to achieve this balance. The owner’s equity amount, however, is not correct. All other amounts are accurate, but some are out of place.HAYNES EDITORIAL SERVESEBalance SheetREQUIRED:1.Prepare the correct balance sheet, and date it correctly. Compute total assets, total liabilities, and owner’sequity.2.Identify the accounts that should not be presented on the balance sheet and state why you excluded themfrom the correct balance sheet you prepared for requirement 1.CASE 3 RECORD TRANSACTIONS AND PREPARE THE FINANCIAL ST ATEMENTAllen Musser started a consulting service and during the first month of operations(June 2003) completed the following selected transactions:a.Musser began the business with an investment of $5,000 cash and a building valued at $60,000. Thebusiness gave Musser’s equity in the business.b.Borrowed $30,000 from the bank; signed a note payable.c.Purchased office supplies on account, $2,100.d.Paid $18,000 for office furniture.e.Paid employee’s salary. $2,200.f.Performed consulting service on account for client, $5,100.g.Paid $800 of the account payable created in transaction(c).h.Received a $600 bill for advertising expense that will be paid in the near future.i.Performed consulting service for customers and received cash,$1,600.j.Received cash on account, $1,200k.Paid the following cash expenses:(1) Rent on land, $700; (2) Utilities, $400l.Withdrew $7,500 for personal use.REQUIED:1.Open the T-accounts.2.Record each transaction directly in the T-account without using a journal, using the letters to identifythe transactions.3.Prepare the trial balance of Musser Consulting Service at June 30, 2003.4.Prepare the income statement, the statement of owner’s equity, and the balance sheet of MusserConsulting Service at the June 30, 2003.CASE 4 MAKE DECISION: TO BUY A COMPANY OR NOT?Benjamin O’henry has owened and operated O’Henry Data Services since its beginning ten years ago. From all appearances, the business has prospered. In the past few years, you have become friends with O’Henry and his wife through your church. Recently , O’Henry mentioned that he h as lost his zest for the business and would consider selling it for the right price. Y ou are interested in buying this business and obtain its most recent monthly unadjusted trial balance, which follows.O’HENRY’S DA TA SERVICESUnadjusted Trial BalanceRevenues and expenses vary from month to month, and November is a typical month. Y our investigation reveals that the unadjusted trial balance does not include the effects of monthly revenues of $2,100 and monthly expenses totaling $2,750. If you were to buy O”Henry’ Data Services. Y ou would hire a manager who would require a monthly salary of $3,000.REQUIRED:1.The most you would pay for the business is 20 times the monthly net income you could expect to earn formit. Compute the possible price.2.The least O”Henry will take for the business is his en ding capital. Compute this amount.3.Under these conditions, how much should you offer O”Henry? Give your reason.CASE 5 Was Maltbee’s summer work successful?Doug Maltbee formed a lawn service business as a summer job. To start t business on May 1, he deposited $1,000 in a new bank account in the name of the proprietorship. The $1,000 consisted of a $600 loan from his father and $400 of his own money. Doug rented lawn equipment, purchased supplies, and hired fellow students to mow and trim his customer’s lawns.At the end of each month, Doug mailed bills to his customers. On August 31, he was ready to dissolve the business and return to Louisiana State University for the fall semester. Because he was so busy, he kept few records other than his checkbook and a list of amounts owed to him by customers.At August 31, Doug’s checkbook shows a balance of $690, and his customers still owe him $500. During the summer, he collected $4,250 from customers. His checkbook lists payments for supplies totaling $400, and he still has gasoline, weedeater cord, and other supplies that cost a total of $50. He paid his employees $1,900, and he still owes them $200 for the final week of the summer.Doug rented some equipment from Scholes Machine Shop. On May 1, he signed a six-month lease on mowers and paid $600 for the full lease period. Scholes will refund the unused portion of the prepayment if the equipment is in good shape. In order to get the refund, Doug has kept the mowers in excellent condition. In fact, he had to pay $300 to repair a mower.To transport employees and equipment to jobs, Doug used trailer tat he bought for $300. He figures that the summer’s work used up one-third of the trailer that he bought for the business. Checkbook lists a payment of $460 for cash withdrawals by Doug during the summer. Doug paid his father back during August. REQUIRED:1.Prepare the income statement of Maltbee Lawn Service for the four months May through August.2.Prepare the classified balance sheet of Maltbee Lawn Service at August 31.3.Was Maltbee’s summer work successful? Give the reason for your answer.CASE 6 TO ADJUST USING THE WORKSHEETFresh Market Grocery’s trial balance pertains to December 31, 2001FRESH MARKET GROCERYTRIAL BALANCEDecember 31, 2001Additional data at December 31,2001:a.Insurance expense for the year, $6,090.b.Store fixtures have an estimated useful life of ten years and are expected to beworthless when they are retired from service.c.Accrued salaries at December 31, $1,260.d.Accrued interest expense at December 31, $870.e.Store supplies on hand at December 31,$760.f.Inventory on hand at December 31, $94,780.REQUIRED:plete Fresh Market’s work sheet for the year ended Decembe r 31,2001.Key adjusting entries by letter.2.What was the net income for the year ended December 31,2001?3.What was the ending balance of the capital account?Case 07 Determining cost of purchaseThe following is an excerpt from a conversation between Joe Hitachi and Kim Kenwood. Joe is debating whether to buy a stereo system from Audio-Tec, a locally owned electronics store, or Powerhouse, a mail-order electronics company.Joe: Kim, I don’t know what to do about buying my new stereo.Kim: So what's the problem?Joe: Well, I can buy it locally at Audio-Tec for $689.95. However, Powerhouse Electronics has the same system listed for $699.99.Kim: So what’s the big deal? Buy it from Audio-Tec.Joe: It’s not quite that simple. Powerhouse said someth ing about not having to pay sales tax, since I was out-of-state.Kim: Y es that’s a good point. If you buy it at Audio-Tec, they’ll charge you 6% sales tax.Joe: But Powerhouse Electronics charges $15 for shipping and handing. If I have them send it next-d ay air, it’ll cost an additional $20 for shipping and handling. Kim: I guess it is a little confusing.Joe: That’s not all. Audio-Tec will give an additional 2% discount if I pay cash. Otherwise, they will let me use my MasterCard, or I can pay it of in three monthly installments (the interest rate for a month is 1.5%).Kim: Anything else???Joe: Well…Powerhouse says I have to charge it on my MasterCard. They don’t accept checks.Kim: I am not surprised. Many mail-order houses don’t accept checks.Joe: I give up. What would you do?Required:1.Assuming that Powerhouse Electronics doesn’t charge sales tax on the sale to Joe, which company is offering the best buy?2.What might be some consideration other than price that might influence Joe’s decision on where to buy the stereo system?Case 08 Sales discountsY our sister operates Escapade V ideo Company, a videotape distributorship that is in its third year of operation. The following income statement was recently prepared for the year ended October 31, 1997:Escapade V ideo CompanyIncome statementFor the Y ear Ended October 31, 1997Y our sister is considering a proposal to increase net income by offering sales discounts of 2/15, n/30, and by shipping all merchandise FOB shipping point. Currently, no sales discounts are allowed and merchandise is shipped FOB destination. It is estimated that these credit terms will increase net sales by 10%. The ratio of the cost of merchandise sold to net sales is expected to be 70%. All selling and administrative expenses are expected to remain unchanged, except for store supplies, miscellaneous selling, office supplies, and miscellaneous administrative expenses, which are expected to increase proportionately with increased net sales. The amounts of these preceding items for the year ended October 31, 1997, were as follows:Store supplies expense 2000Miscellaneous selling expense 1000Office supplies expense 800Miscellaneous administrative expense 1500The other income and other expense items will remain unchanged. The shipment of all merchandise FOB shipping point will eliminate all transportation-out expenses, which for the year ended October 31, 1997, were $18000.Required:Prepare a projected single-step income statement for the year ending October 31,1998, based on the proposal.CASE 09 How much cash did ABC collect in month 4 and 5?ABC Ltd makes all its sales on credit. For customers who pay within ten days of purchase, ABC gives a discount of 5 per cent.(Assume all sales are made evenly over the month and there are 30 working days every month.) ABC knows that, on average, 50 per cent of its customers pay within the discount period, 40 per cent pay within 30 days. And 8 per cent within 60 days. Two per cent are uncollectable.Month 1 1 200 000Month 2 1 300 000Month 3 880 000Month 4 1 000 000Month 5 1 250 000CASE 10 FIFO AND LIFOThe Ramayya Corporation is nearing the end of its first year in business. The following purchasesSales for the year will be 5,000 units for $120,000. Expenses other than cost of goods sold will be $20,000.The president is undecided about whether to adopt FIOF or LIFO for income tax purposes. The company has ample storage space for up to 7,000 units of inventory. Inventory prices are expected to stay at $15 per unit for the next few months.REQUIRED:1.What would be the net income before taxes, the income taxes, and the net income after taxesfor the year under (a) FIFO and (b) LIFO? Income tax rates are 40%.2.If the company sells its year-end inventory in year two @ $24 per unit and goes out ofbusiness, what would be the net income before taxes, the income taxes, and the net income after taxes under (a) FIFO and (b) LIFO? Assume that other expenses in year two are $20,000.3.Repeat requirements 1 and 2, assuming that the 4,000 units @ $ 15 purchased in Decemberwere not purchased until January of the second year. Generalize on the effect on net income of the timing of purchases under FIFO and LIFO.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Photographic Equipment, which worth $25,000 and 50,000,

respectively.Philip received $97,500 of capital.

1

Received $6,000 to provide Photographic service in the next 12

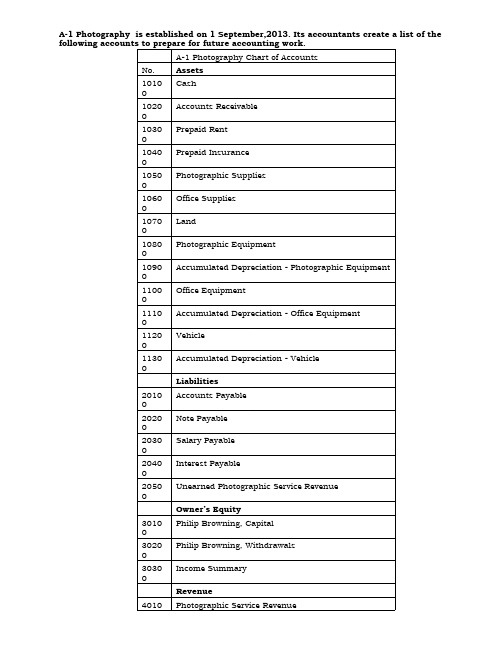

文档来源为:从网络收集整理.word 版本可编辑.欢迎下载支持. A-1 Photography is established on 1 September,2013. Its accountants create a list of the following accounts to prepare for future accounting work.

Sep

1

Philip Browning deposited $10,000 in the business account. Also on

this date, Philip transferred his Vehicle, worth $12,500, to the

business.Besides, he also provided Office Equipment and

11200 Vehicle

11300 Accumulated Depreciation - Vehicle

Liabilities

20100 Accounts Payable

20200 Note Payable

20300 Salary Payable

20400 Interest Payable

20500 Unearned Photographic Service Revenue

50800 DLeabharlann preciation Expense - Office Equipment

50900 Depreciation Expense - Vehicle

51000 Gas and Oil Expense

51100 Janitorial Expense

51200 Advertising Expense

months for another business.

1

Purchased an Auto insurance policy for $2,400 and paid cash

for one year.

1

Wrote a check for $3,600 to rent an office. In the “for” area of the check, it

10

Purchased $4,000 of office equipment on account.

10

Paid $18 for Magazine subscription.

11

Performed Photographic Services for $1,500 to Jerri Wales on

account.

51300 Interest Expense

51400 Miscellaneous Expense

文档来源为:从网络收集整理.word 版本可编辑.欢迎下载支持. A-1photography starts its business in September. All of the first month’s activity for it is as follows.

10700 Land

10800 Photographic Equipment

10900 Accumulated Depreciation - Photographic Equipment

11000 Office Equipment

11100 Accumulated Depreciation - Office Equipment

11

Performed Photographic Services and received $1,288 of cash.

12

Paid $200 to Safeguard Oil Company for gas and oil consumed

12

Borreowed $20,000 from Central National Bank due within 60 days,10%

states “September through December rent”.

5

Purchase $264 of Photographic Supplies on account.

6

Performed Photographic Services and received $1,563 of cash.

interest rate for two month.

15

Paid $350 for advertising in the Charlotte News.

50200 Rent Expense

50300 Utilities Expense

50400 Photographic Supplies Expense

50500 Office Supplies Expense

50600 Insurance Expense

50700 Depreciation Expense - Photographic Equipment

A-1 Photography Chart of Accounts

No.

Assets

10100 Cash

10200 Accounts Receivable

10300 Prepaid Rent

10400 Prepaid Insurance

10500 Photographic Supplies

10600 Office Supplies

Owner’s Equity

30100 Philip Browning, Capital

30200 Philip Browning, Withdrawals

30300 Income Summary

Revenue

40100 Photographic Service Revenue

Expenses

50100 Salary Expense