个人所得税法(英文版)

个人所得税

个人所得税个人所得税(personal income tax)是调整征税机关与自然人(居民、非居民人)之间在个人所得税的征纳与管理过程中所发生的社会关系的法律规范的总称。

凡在中国境内有住所,或者无住所而在中国境内居住满一年的个人,从中国境内和境外取得所得的,以及在中国境内无住所又不居住或者无住所而在境内居住不满一年的个人,从中国境内取得所得的,均为个人所得税的纳税人。

从世界范围看,个人所得税制存在着不同的类型,当前我国个人所得税制采用的是混合所得税制。

发展历程国家对本国公民、居住在本国境内的个人的所得和境外个人来源于本国的所得征收的一种所得税。

在有些国家,个人所得税是主体税种,在财政收入中占较大比重,对经济亦有较大影响。

中国在中华民国时期,曾开征薪给报酬所得税、证券存款利息所得税。

1950年7月,政务院公布的《税政实施要则》中,就曾列举有对个人所得课税的税种,当时定名为“薪给报酬所得税”。

但由于我国生产力和人均收入水平低,实行低工资制,虽然设立了税种,却一直没有开征。

1980年9月10日由第五届全国人民代表大会第三次会议通过《中华人民共和国个人所得税法》。

(直至1980年以后,为了适应我国对内搞活、对外开放的政策,我国才相继制定了《中华人民共和国个人所得税法》。

《中华人民共和国城乡个体工商业户所得税暂行条例》以及《中华人民共和国个人收入调节税暂行条例》。

上述三个税收法规发布实施以后,对于调节个人收入水平、增加国家财政收入、促进对外经济技术合作与交流起到了积极作用,但也暴露出一些问题,主要是按内外个人分设两套税制、税政不统一、税负不够合理。

)为了统一税政、公平税负、规范税制,1993年10月31日,八届全国人大常委会四次会议通过了《全国人大常委会关于修改<中华人民共和国个人所得税法>的决定》,同日发布了新修改的《中华人民共和国个人所得税法》(简称税法),1994年1月28日国务院配套发布了《中华人民共和国个人所得税法实施条例》。

法律英语11税法111 税法简介

2020/9/2

tax law

8

Two specific limitations

Direct taxes Capitation taxes

1. 直接税与人头税必须在各州间按人 口的比例合理分配;

2. 美国境内的所有关税和货物税必须 统一。

Custom duties

2020/9/2

tax law

广泛的 Exert a controlling impact upon the

nation’s economy 对全国经济产生支配性影响

2020/9/2

tax law

5

Federal Fiscal Powers

Among the most important of the powers granted to the federal government

2020/9/2

tax law

14

The Graves case effectively overruled the Pollock decision

The courts continually have held that a tax on income was an excise tax.

indirect taxes ultimately proved to be a stumbling block in the development of our present federal tax structure. ……,直接税与间接税之间的差异已 成为美国现行联邦税制发展的障碍。

2020/9/2

对经营和职业所得的征税不是直接税, 不必以人口为基础分配。

2020/9/2

tax law

22ቤተ መጻሕፍቲ ባይዱ

个人所得税(英文版精品)The Personal Income Tax

Excludable Forms of Income: Interest on State and Local Bonds

• Interest earned on bond issued by state or locality is untaxed (while interest earned on the bond of a private company is taxed).

• Step 1: Compute Adjusted Gross Income (AGI)

• Step 2: Convert AGI into taxable income by subtracting exemptions and deductions

• Step 3: Compute tax due by applying a rate schedule, and subtracting tax credits.

14

Excludable Forms of Income: Interest on State and Local Bonds

• Illustration

– Assume each group has some amount of capital that can be invested in either a private bond or state bond (each with equal riskiness).

4

Defining Income

• Which forms of income could be taxed?

– Wages and salaries, rents, dividends, and so on …

• Haig-Simons definition of income: Income is the money value of the net increase in an individual’s power to consumer during a period.

个人所得税缴纳说明(中英文版)

关于缴纳所得税的说明**同志2011年的年薪总收入为*****元,月平均收入****.**元。

2011年住房公积金和社保共****元允许税前扣除。

按照《中华人民共和国个人所得税法》2007年第五次修正版之规定,人员月平均收入2000元以内的不缴纳个人所得税,月平均收入超过额度的按照累进税率计缴个人所得税。

因此2011年已缴个人所得税****元,年薪净总收入*******元左右。

其计算公式如下:应缴纳个人所得税=([(年薪总收入-个税起征点×12个月-全年缴纳社保及住房公积金)/12个月]×税率-速算扣除数)×12个月。

2011年应缴个税为:*******(元)******公司2011年1月1日Explanation of Individual Income Tax CalculationIn 2011, the annual income of **** is RMB*****; then his average income isRMB***** per month. Meanwhile, social insurance and house fund is RMB****. According to Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China in 2007, tax threshold is RMB2000 per month and those amounts exceeding this will be tax payable. In 2011, ****’s total amount of tax payment was RMB****, and annual net income was RMB****.The calculation formula is as following:annual tax payable = {[(annual income –tax threshold × 12 months – annual social insurance and house fund ) / 12 months] ×tax rate - quick calculation deduction } × 12 months.tax payable in 2010:RMB************* Co., Ltd.1st , Jan. 2011When you are old and grey and full of sleep,And nodding by the fire, take down this book,And slowly read, and dream of the soft lookYour eyes had once, and of their shadows deep;How many loved your moments of glad grace,And loved your beauty with love false or true,But one man loved the pilgrim soul in you,And loved the sorrows of your changing face; And bending down beside the glowing bars, Murmur, a little sadly, how love fledAnd paced upon the mountains overheadAnd hid his face amid a crowd of stars.The furthest distance in the worldIs not between life and deathBut when I stand in front of youYet you don't know thatI love you.The furthest distance in the worldIs not when I stand in front of youYet you can't see my loveBut when undoubtedly knowing the love from both Yet cannot be together.The furthest distance in the worldIs not being apart while being in loveBut when I plainly cannot resist the yearningYet pretending you have never been in my heart.The furthest distance in the worldIs not struggling against the tidesBut using one's indifferent heartTo dig an uncrossable riverFor the one who loves you.倚窗远眺,目光目光尽处必有一座山,那影影绰绰的黛绿色的影,是春天的颜色。

个人所得税英语表达

个人所得税英语表达Personal Income Tax: English ExpressionsPersonal Income Tax is a significant aspect of any country's tax system, and it plays a crucial role in the fiscal well-being of a nation. In this article, we will explore various English expressions related to Personal Income Tax and provide a comprehensive understanding of this topic.1. What is Personal Income Tax?Personal Income Tax refers to the tax levied on the income of individuals by the government. It is typically calculated based on the taxpayer's total earnings, including salaries, wages, tips, and any additional forms of income. The tax rates are usually progressive, meaning they increase as the income level rises.2. Taxable IncomeTaxable income is the portion of an individual's earnings that is subject to taxation. It is calculated by deducting allowed exemptions, deductions, and credits from the total income. In simpler terms, it is the income on which the individual's tax liability is determined.3. Tax BracketTax brackets are specific income ranges in which individuals fall, based on their taxable income. Each bracket corresponds to a different tax rate. For example, someone with a higher taxable income will be in a higher tax bracket and will be subject to a greater tax percentage.4. Filing StatusFiling status refers to the classification of an individual, determining how they are taxed. Common filing statuses include single, married filing jointly, married filingseparately, head of household, etc. The filing status affects the tax brackets, deductions, and credits available to the individual.5. DeductionsDeductions are specific expenses that individuals can subtract from their taxable income, thereby reducing their overall tax liability. Common deductions include mortgage interest, student loan interest, medical expenses, charitable contributions, etc.6. Tax CreditsTax credits are similar to deductions, but they provide a dollar-for-dollar reduction in the tax liability. Unlike deductions, which reduce taxable income, tax credits reduce the amount of tax owed directly. Examples of tax credits include child tax credit, earned income tax credit, education credits, etc.7. WithholdingWithholding refers to the amount of income tax that employers deduct from their employees' paychecks and remit to the government on their behalf. The withholding amount is based on the individual's filing status and the information provided on their Form W-4. This system helps individuals to fulfill their tax obligations throughout the year.8. Tax ReturnA tax return is a form filed by individuals with the tax authorities that reports their income, deductions, tax credits, and other relevant information. The tax return helps determine the individual's tax liability for a given year. The filing deadline for tax returns is typically April 15th.9. Tax RefundA tax refund is an amount of money returned to the taxpayer when their total tax payments, through withholding and estimated payments, exceed their actual tax liability.Tax refunds are often received by individuals who have overpaid their taxes throughout the year.10. Tax AuditA tax audit is a detailed examination of an individual's tax return by the tax authorities to ensure accuracy and compliance with tax laws. Audits can be conducted randomly or triggered by certain red flags, such as excessive deductions or unreported income. It is essential to maintain accurate records and transparent financial documents to minimize the risk of an audit.In conclusion, Personal Income Tax is a crucial aspect of any country's tax system. Understanding the various English expressions related to personal income tax helps individuals navigate their tax obligations and make informed financial decisions. It is important to consult with tax professionals or refer to reputable sources for up-to-date information on tax laws and regulations.。

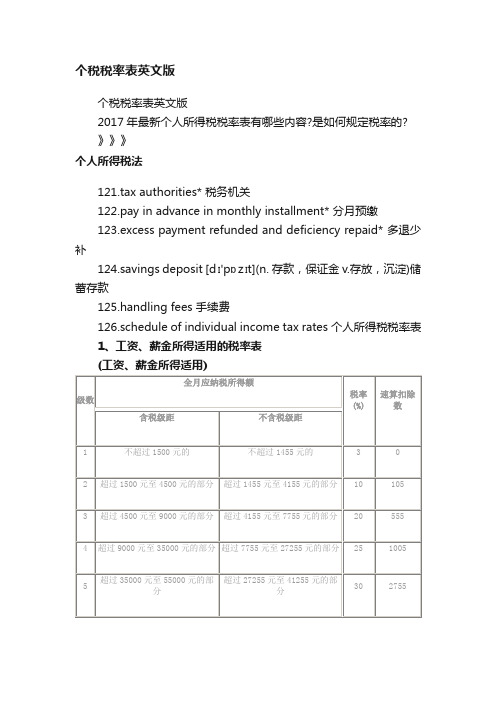

个税税率表英文版

个税税率表英文版

个税税率表英文版

2017年最新个人所得税税率表有哪些内容?是如何规定税率的?

》》》

个人所得税法

121.tax authorities* 税务机关

122.pay in advance in monthly installment* 分月预缴

123.excess payment refunded and deficiency repaid* 多退少补

124.savings deposit [dɪ'pɒzɪt](n. 存款,保证金 v.存放,沉淀)储蓄存款

125.handling fees 手续费

126.schedule of individual income tax rates 个人所得税税率表

1、工资、薪金所得适用的税率表

(工资、薪金所得适用)

有关费用后的所得额;

2。

含税级距适用于由纳税人负担税款的工资、薪金所得;不含税级距适用于由他人(单位)代付税款的工资、薪金所得。

2、个体工商户,企业等适用税率表二

(个体工商户的生产、经营所得和对企事业单位的承包经营、承租经营所得适用)

注:

1。

本表所列含税级距与不含税级距,均为按照税法规定以每一纳税年度的收入总额减除成本、费用以及损失后的所得额;

2。

含税级距适用于个体工商户的生产、经营所得和由纳税人负担税款的对企事业单位的承包经营、承租经营所得;不含税级距适用于由

他人(单位)代付税款的对企事业单位的承包经营、承租经营所得。

〈个人所得税自行纳税申报办法(试行)〉宣传通稿(英文版)

Publicity Material For Self-DeclarationRules Concerning IndividualIncome Tax (Provisional)According to the Decision on Amending the Law of the People's Republic of China on Individual Income Tax reviewed and adopted at the 18th Session of the Standing Committee of the 10th National People's Congress on October 27, 2005, the taxpayer “with individual income exceeding the amount stipulated by the State Council” shall declare taxes by himself/herself, widening the scope of self-declaration by taxpayers. Thereafter, the State Council stipulated that "the individual income exceeding the amount stipulated by the State Council" means “annual income of over RMB120,000”by amending the Implementing Rules of the Law on Individual Income Tax and authorized the State Administration of Taxation to Formulate specific management measures. According to the provisions above and the principle of “providing convenience to taxpayers, regulating high incomes, facilitating tax collection and administration, and stressing on key management issues”, the State Administration of Taxation formulated and issued the Self-Declaration Rules Concerning Individual Income Tax (Provisional) (hereinafter referred to as “Rules”) after an in-depth study and repeated demonstration on the basis of the opinions of many taxpayers, withholding agents, experts, scholars and grassroots tax authorities. The Rules consist of eight chapters containing 44 articles, which define the specific operational methods of tax self-declaration from the aspects of the legal basis of the Rules, declarers, declaration content, declaration place, declaration period, way of declaration, declaration management, legal responsibility, and time of enforcement.The Rules specify five Cases in which taxpayers shall declare taxes to the tax authority by themselves: 1. With annual income of overRMB120,000; 2. Receiving salary and remuneration from two or more employers in China; 3. Generating income abroad; 4. Generating taxable income without withholding agent; 5. Other Cases as specified by the State Council. The Rules stipulate that the taxpayer with total taxable income of over RMB120,000 within a tax year in Case 1 shall declare taxes to the tax authority after the end of a year, no matter whether the tax on his/her taxable income in the year has been withheld byhis/her withholding agent or has been declared and paid by the taxpayer to the tax authority on his/her own. The taxpayer in Cases 2-4 shall declare taxes from time to time, that is, when receiving taxable income, the taxpayer shall declare and pay tax to the tax authority within the specified period. Other cases as specified by the State Council in case 5 have not been clarified yet, and tax declaration rules will be formulated otherwise according to the specific conditions. The Rules stipulate that any taxpayer with annual income of over RMB120,000 shall declare his/her annual income of all items, tax payable, paid (withheld) tax, tax credit, tax supplementation (refund) and relevant personal basic information within three months after the end of a tax year. The declared “annual income” contains 11 taxableincome items specified in the Law on Individual Income Tax, i.e. salary and compensation, income from production and operation by individually-owned businesses, income from contract operation and operation under lease of public institutions, compensation For labor services, author’s remuneration, royalty, interest, dividend and bonus, income from lease of property, income from transfer of property,incidental income, and other taxable income specified by finance department under the State Council. The Rules also define that three categories of tax-free income items excluded in the calculation of annual income, i.e. tax-free income specified in Items 1-9 of Article 4 of the Law on Individual Income Tax; income that is generated from China and is allowed to be free of tax as provided in Article 6 of the Implementing Rules of the Law on Individual Income Tax; the basic old-age insurance, medical insurance, unemployment insurance and public housing reserve fund contributed by units for individuals or by individuals in accordance with the provisions of Article 25 of the Implementing Rules of the Law on Individual Income Tax. The Rules also stipulate that the annual income of all items shall be calculated according to the gross income, except “the annual production and operation income of individually-owned businesses”and “the income from transfer of property”calculated on the basis of “taxable income”.For the convenience of self-declaration by taxpayers, the Rules stipulate that taxpayers may declare taxes in various ways, including data telegraph (e.g. online declaration) and mail declaration. They can also go to the tax authority directly to declare taxes, or declare taxes by other ways as provided by the tax authority. At the same time, it is stipulated that the taxpayer may entrust intermediary agencies or other persons qualified for tax agency service with tax declaration. The Rules also specify the requirements concerning the provision of quality service for taxpayers’self-declaration by tax authorities. For example, the tax authority shall have various declaration forms published on its website, or placed in the taxpayer servie office providing tax declaration services, for taxpayers to download or access from time to time free of charge; the tax authority shall remind the taxpayer withannual income of over RMB120,000 to declare tax on his/her own by appropriate ways in the legal declaration period; the tax authority accepting tax declaration shall handle the procedures of collection, supplementation, refund and set-off of tax according to the declaration of taxpayers, and issue duty paid proof according to regulations for taxpayers who have completed tax declaration and submitted tax; the tax authority shall hold the tax declaration information of taxpayers in confidence.Moreover, the Rules also clearly define declaration place, declaration period, way of declaration, declaration management, legal responsibility and time of enforcement.The Formulation and distribution of the Rules is essential to implementing of the decision made at the 18th Session of the Standing Committee of the 10th National People's Congress to widen the scope of individual income tax self-declaration and giving full play to the role of individual income tax in regulating high incomes.First, it will help cultivate taxpayers’consciousness of paying taxes in good faith according to the law, define legal responsibilities, and enhance the compliance with tax law. Since individual income tax is levied mainly by withholding the tax, before the amendment of the Law on Individual Income Tax, people with high income were not legally obligated to declare tax by themselves. Therefore, in Case the withholding agent fails to withhold taxes and the individual fails to declare taxes, it is hard to define the legal responsibility of the individual who failed to declare taxes. To that end, the law only stipulates that withholding agents failing to withhold taxes shall besubject to punishment and individuals shall pay the taxes payable. The tax law revised last year stipulates that taxpayers with annual incomeof over RMB120,000 shall declare taxes by themselves. On the basis ofthe provisions of the law, the Rules clarify such matters as specific methods, requirements and legal responsibilities of tax self-declaration. The implementation of the Rules and the widening of the scope of self-declaration by taxpayers will effectively strengthen taxpayers’ consciousness of paying taxes in good faith according to the law, define their legal responsibilities and further enhance their compliance with tax law.Second, it will help strengthen the regulation of the incomes of high-income people. From the perspective of the practice of individual income tax collection and administration, the incomes of high-income people generally come in diverse and invisible channels and forms. However, tax authorities lack necessary information sources and thus are unable to well manage such people. That easily leads to defects in tax collection and administration. The revised tax law requires for thefirst time that any taxpayer with annual income of over RMB120,000 declare all taxable income obtained in the whole year to the taxa uthority, legally defining the taxpayer’s obligation to declare taxes and legal responsibilities and broadening the channels for taxauthorities to obtain individual income information. That will help tax authorities strengthen administration of tax sources, find out various income items of high-income people, intensify the tax regulation onhigh-income people, and mitigate the contradiction of unfairdistribution of income.Third, it will help further push forward the scientific and refined administration of individual income tax collection. Based on the arrangement and classification of detailed information submitted by withholding agents and information submitted by individuals, tax authorities can find out the key groups of people and key industriesFor the collection and administration of individual income tax, making the aim of individual income tax administration more clear; based on the cross comparison and analysis of detailed information submitted by withholding agents and information submitted by individuals, tax authorities can discover tax-related doubtful points and people not paying taxes in full, and provide Case sources for tax inspectors. Therefore, it will help further push forward the scientific and refined administration of individual income tax collection.Fourth, it will help accelerate the transition to the mixed tax system that combines comprehensive and classified tax systems. In the Decisions of the CPC Central Committee on Some Major Issues Concerning the Building of a Harmonious Socialist Society and the Outline of the11th Five-Year Plan for National Economic and Social Development of the People’s Republic of China adopted at the Sixth Plenary Session of the 16th Central Committee of the Party, it is clarified that China will implement an individual income tax system that combines comprehensive and classified tax systems. Since individual income is diverse and invisible at present and it is difficult for tax authorities to gain and monitor all individual income information, urging high-income people to declare taxes can continuously strengthen residents’consciousness of paying taxes in good faith according to the law and enhance the compliance with tax law; it can also create conditions and accumulateexperience for the transition to a mixed tax system that combines comprehensive and classified tax systems in the future. Besides, obligating taxpayers to declare taxes by themselves on the basis of the withholding of taxes by withholding agents at the source is also in accordance with general international practice.。

个人所得税法(英文版)

第15章 个人所得税法Chapter 15 Individual Income Tax• Who are the individuals liable to Individual Income Tax?• What is the income from sources within China?• What is the income from sources outside China?• What income earned by an individual is subject to Individual Income Tax?• How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?• What does wage, salary income include specifically?• How are salaries and wages assessed for Individual Income Tax payable?” regulated for wages and salaries?• How is the “additional deduction for expenses• How to compute the income tax payable on the bonus income on the year-end in one payment?• How to compute the income tax payable on the income of welfare in kind?• How to compute the income tax payable on the income stock options of employees of enterprises?• How is severance pay taxed?• How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?• What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?• How to calculate the taxable income of individual I ndustrial and Commercial Households?• What are the rules concerning deductions for Individual Industrial and Commercial Households?• How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?• How do single proprietorship enterprises compute and pay income tax payable on their production and business income?• How to levy income tax payable by the investors of single p roprietorship and partnership enterprises by mode of administrative assessment?• How do single proprietorship and partnership enterprises compute and pay incomedividend and bonus income as return from their tax payable on their i nterest,investment?• How is income from contracted o r leased o peration o f enterprises or institutions assessed for Individual Income Tax?• How is income from remuneration for personal service a ssessed f or Individual Income Tax payable?• How to treat t he receivables unrecoverable and the business l osses incurred by Individual Industrial and Commercial Households?• What expenses are not allowed for deductions for Individual I ndustrial a nd Commercial Households?• What are the rules c oncerning the depreciation of the fixed a ssets of Individual Industrial and Commercial Households?• How to deduct the expenses concerning intangible a ssets u sed by Individual Industrial and Commercial Households?• How do Individual Industrial and Commercial Households compute their i ncome tax payable?• How additional income tax is levied on remuneration income that is excessively high at one payment?• How is author’s remuneration income assessed for Individual Income Tax payable?• How is income from royalties assessed for Individual Income Tax payable?• How is income from lease of property assessed for Individual Income Tax payable?• How is income from transfer o f property assessed f or Individual I ncome Tax payable?• How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?dividend, b onus, contingent i ncome and/ or other income• What do the interest,include specifically?dividends, bonuses, contingent i ncome and/ or other income• How are interests,assessed for Individual Income Tax payable?• How to compute the income tax payable on income derived by two individuals or more together?• How is donation income assessed for Individual Income Tax payable?• How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?• How is income derived from sources outside China assessed for Individual Income Tax payable?• What are the main exemptions for Individual Income Tax?• What kind of bond interest income and earmarked saving d eposit i nterest income are exempt from Individual Income Tax as ruled by the State?• What are the main reductions for Individual Income Tax?• What are the rules concerning the mode, time and places for Individual Income Tax payment?• How to report and pay income tax on wages and salaries income?• How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?• How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?• How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?• How to report and pay income tax on income earned by taxpayers f rom sources outside China?纳税义务人 判定标准 征税对象范围1.居民纳税人(负无限纳税义务)(1)在中国境内有住所的个人(2)在中国境内无住所,而在中国境内居住满一年的个人。

个人所得税缴纳清单 英文版

个人所得税缴纳清单英文版Here's a draft of an informal and conversational English version of a personal income tax payment statement:First off, let's get the numbers down. For the past year, I've paid quite a bit in taxes. Yeah, it's not fun, but it's a necessary evil, right? The total amount I've shelled out is quite substantial, but it's all for the greater good.You know, sometimes I wonder where all that money goes. But then I remember all the services and benefits we get in return. It's like a trade-off, really. We pay our taxes, and in return, we get a stable government, infrastructure, and social services.This year, I've made sure to keep track of my tax payments. It's important to be aware of what you're paying and why. After all, it's your hard-earned money. So, I've kept all the receipts and documentation organized just so Ican refer back to them anytime I want.Talking about taxes, have you ever tried using a tax calculator? It's super helpful! You can estimate how much you'll owe based on your income and deductions. It's a great way to stay on top of your finances and make sureyou're not paying too much or too little.Lastly, I've learned that it's always a good idea to consult a tax professional if you have any questions or concerns. They can guide you through the complex tax system and help you maximize your deductions and minimize your tax burden. So, don't hesitate to seek help if you need it!。

考研英语翻译天天练:个人所得税法_毙考题

2019考研英语翻译天天练:个人所得税法学好英语翻译一定要加强练习,掌握不同话题的相关词汇短语和专业表达。

小编整理分享不同话题段落和翻译,19考生注意每天练一练,相信日积月累必然提升翻译能力。

2019考研英语翻译天天练:个人所得税法个人所得税法individual income tax law请看例句:A draft amendment to the individual income tax law has been submitted for afirst reading at a bimonthly session of the National People s Congress StandingCommittee. Specific personal income tax changes that aim to reduce taxpayerburdens and boost consumption are expected after the proposed changes receiveregulatory approval.近日,个人所得税法修正案草案提请全国人大常委会初次审议。

此次提交审议的草案通过后,有望出台减轻纳税人负担、刺激消费等个人所得税具体改革措施。

个人所得税法修正案草案的亮点有:起征点提高raise the thresholdThe draft amendment raises the threshold for personal income tax from 3,500yuan to 5,000 yuan per month, or 60,000 yuan per year.草案将个税起征点由之前的3500元上调至5000元/月(6万元/年)。

专项附加扣除special expense deductionsThe draft amendment adds special expense deductions for items likechildren s education, continuing education, treatment for serious diseases, aswell as housing loan interest and rent.草案首次增加子女教育支出、继续教育支出、大病医疗支出、住房贷款利息和住房租金等专项附加扣除。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第15章个人所得税法Chapter 15 Individual Income Tax•Who are the individuals liable to Individual Income Tax?•What is the income from sources within China?•What is the income from sources outside China?•What income earned by an individual is subject to Individual Income Tax? •How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?•What does wage, salary income include specifically?•How are salaries and wages assessed for Individual Income Tax payable? •How is the “additional deduction for expenses” regulated for wages and salaries?•How to compute the income tax payable on the bonus income on the year-end in one payment?•How to compute the income tax payable on the income of welfare in kind? •How to compute the income tax payable on the income stock options of employees of enterprises?•How is severance pay taxed?•How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?•What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?•How to calculate the taxable income of individual Industrial and Commercial Households?•What are the rules concerning deductions for Individual Industrial and Commercial Households?•How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?•How do single proprietorship enterprises compute and pay income tax payable on their production and business income?•How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?•How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return from their investment?•How is income from contracted or leased operation of enterprises or institutions assessed for Individual Income Tax?•How is income from remuneration for personal service assessed for Individual Income Tax payable?•How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?•What expenses are not allowed for deductions for Individual Industrial andCommercial Households?•What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?•How to deduct the expenses concerning intangible assets used by Individual Industrial and Commercial Households?•How do Individual Industrial and Commercial Households compute their income tax payable?•How additional income tax is levied on remuneration income that is excessively high at one payment?•How is author’s remuneration income assessed for Individual Income Tax payable?•How is income from royalties assessed for Individual Income Tax payable? •How is income from lease of property assessed for Individual Income Tax payable?•How is income from transfer of property assessed for Individual Income Tax payable?•How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?•What do the interest, dividend, bonus, contingent income and/ or other income include specifically?•How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?•How to compute the income tax payable on income derived by two individuals or more together?•How is donation income assessed for Individual Income Tax payable? •How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?•How is income derived from sources outside China assessed for Individual Income Tax payable?•What are the main exemptions for Individual Income Tax?•What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State? •What are the main reductions for Individual Income Tax?•What are the rules concerning the mode, time and places for Individual Income Tax payment?•How to report and pay income tax on wages and salaries income?•How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?•How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses? •How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?•How to report and pay income tax on income earned by taxpayers from sourcesoutside China?纳税义务人判定标准征税对象围1.居民纳税人(负无限纳税义务)(1)在中国境有住所的个人(2)在中国境无住所,而在中国境居住满一年的个人。