(财务会计)国际会计复习资料中英结合版

国际会计期末复习资料

国际会计期末复习资料复习资料一、名词汉译英(本大题共5道小题,每小题1分,共5分)1、融资活动2、投资活动3、公认会计原则4、证券交易委员会5、国际财务报告准则6、国际会计准则理事会7、公允反映8、法律遵循9、资产负债表10、经济合作与发展组织二、英译汉(本大题共3道小题,每小题10分,共30分)1.Accounting entails several broad processes : measurement , disclosure and auditing . Measurement is the process of identifying , categorizing , and quantifying economic activities or transactions . These measurements provide insights into the profitability of a firm's operations and the strength of its financial position . Disclosure is the process by which accounting measurements are communicated to their intended users . This area focuses on such issues as what is to be reported , when , by what means , and to whom . Auditing is the process by which specialized accounting professionals(auditors) attest to the reliability of the measurement and communication process . Whereas internal auditors are company employees who answer to management , external auditors are nonemployees who are responsible for attesting that the company's financial statements are prepared in accordance with generally accepted standards .2. Accounting in common law countries is characterized as oriented toward "fair presentation" , transparency and full disclosure and a separation between financial and tax accounting . Stock markets dominate as a source of finance , and financial reporting is aimed at the information needs of outside investors . Setting accounting standards tends to be a private sector activity , and the accounting profession plays an important role .3、Accounting in code law countries is characterized as legalistic in orientation , opaque with low disclosure , and an alignment between financial and tax accounting . Banks or governments ("insiders") dominate as a source of finance , and financial reporting is aimed at creditor protection . Setting accounting standards tends to be a public sector activity , with relatively less influence by the accounting profession .4、Accounting standards setting normally involves a combination of private- and public-sector groups . The private sector includes the accounting profession and other groups affected by the financial reporting process , such as users and preparers of financial statements and employees . The public sector includes such agencies as tax authorities , government agencies responsible for commercial law , and securities commissions . Stock exchanges may influence the process and may be in either the private or public sector , depending on the country . The roles and influence of these groups in setting accounting standard differ from country to country . These differences help explain why standards vary around the world .5.The Sarbanes-Oxley Act was passed in the wake of numerous corporate and accounting scandals, such as Enron and WorldCom. The act limits the services that audit firms can offerclients and prohibits auditors from offering certain nonaudit services to audit clients. It also requires that lead audit partners rotate off audits every five years. Section 302 of the act requires a company’s chief executive officer and chief financial officer to certify each quarterly and annual report. Section 404 requires manage ment’s assessment of internal control over financial reporting, along with a related report by the independent auditor.6、Briefly, individualism is a preference for a loosely knit social fabric over an interdependent, tightly knit fabric. Power distance is the extent to which hierarchy and an unequal distribution of power in institutions and organizations are accepted. Uncertainty avoidance is the degree to which society is uncomfortable with ambiguity and an uncertain future. Masculinity is the extent to which gender roles are differentiated and performance and visible achievement are emphasized over relationships and caring.三、简答题(本大题共3道小题,每小题15分,共45分)1、对会计体系进行分类的目的是什么?2、为什么说国家层面上的许多会计差别已经越来越模糊不清?3、简述处理会计、披露和审计准则国际差异的方法有哪些,并分别进行简要评价。

国际会计期末复习资料

9 .英国的会计职业团体产生时间最早的是(B)。

A英格兰和威尔士特许会计师协会B苏格兰特许会计师协会

C管理会计师协会D特许注册会计师公会

10.法国会计的重要特征是实行统一的会计制度,对系统表述统一会计制度的文件称为(C)。

A会计准则B会计原则C会计方案D会计法

11 .在法院设立“企业合议庭”的是(B)。

日本会计发展缓慢的原因: 1.日本是一个有着强烈文化和宗教根基的传统社会,存在着传统与外来影响的矛盾,外来影响只能逐步地被接受 2. 日本个人和企业关系中的群体意识和互相依赖性,与西方国家个人和团体之间互相独立、疏远的关系截然相反 3.日本的中央政府也会严格控制企业的活动,这意味着对企

A先进先出法B后进先出法C加权平均法D移动平均法

28、德国的会计惯例对流动负债和长期负债的划分描述正确的是(B)。

A凡在资产负债表日期 1 年以后到期的负债项目,应归入长期负债

B凡在资产负债表日期 4 年以后到期的负债项目才归入长期负债

C采用了“一年或一个营业周期孰长”的规定

D2 年以后到期的负债项目才归入长期负债

A英格兰和威尔士特许会计师协会B苏格兰特许会计师协会

C管理会计师协会D特许注册会计师公会

23、日本的《商法》以保护(C)的利益为指导思想。

A投资者B雇员C债权人D企业管理层

24、以下哪项不是会计职业国际化的阻力(D)。

A取得执业资格的学历条件B后续教育C执业资格考试D执业资格费用

25、IASB是以下哪个组织的简称(A)。

29、跨国公司兴起导致的独特的会计问题是(B)。

A国际物价变动影响的调整B国际财务报表的合并

C外币报表的折算D国际税务会计

30、国际双重征税发生的根源是(A)。

中英合作会计学复习资料

商务管理会计学复习资料会计学第一章会计概述学习目标1.了解会计信息的内部和外部使用;2.了解经济环境对会计的影响;3.理解会计目标的层次和内容;4.理解管理会计和财务会计的区别和联系;5.理解为什么内部和外部使用者都需要会计信息;6.理解会计信息的局限性。

1.1会计目标(P1)会计目标:一是从个人的角度,二是从企业的角度。

会计有三个功能:计划、控制和决策支持。

在个人层次上,会计有三个功能:计划、控制和决策支持。

在企业的层次上,会计用于控制组织的活动、计划未来的活动、帮助筹资以及向有关利益各方报告企业的活动和业绩。

1.2管理会计与财务会计的关系(P2)管理会计(对内)会计财务会计(对外)管理会计与财务会计之间既有区别,又有联系。

他们是相互联系、相互补充、相互配合的关系。

区别:1、在服务对象方面;2、在主要依据方面;3、在信息的类型方面;4、在时间范围方面;5、在报告范围方面;6、在计算方法方面。

联系:1、在服务对象方面;2、在取得资料方面;3、在职能、作用方面。

1.3会计信息使用者及其需要(P6)会计信息使用者分为两大类:(1)企业内部使用者——经理或小企业的所有者以及企业的雇员。

经理需要会计信息是为了管理、计划、决策和控制;雇员会对长期盈利性、流动性、与其他企业的比较及用于工资谈判的信息感兴趣(2)企业外部使用者——包括股东、银行、财务分析师、政府、税务当局等。

股东需要知道盈利能力管理绩效、股票业绩和未来展望;债权人对盈利能力、流动性、安全性和负债感兴趣;财务分析师对业绩和盈利能力、企业前景感兴趣;贸易伙伴(债权人、债务人、竞争者)对效率、流动性和企业前景感兴趣。

1.4会计信息的局限性(P12)会计信息局限:(1)提供的是定量的信息,对定性信息提供的少,限制了使用范围;(2)技术的变化革新,通货膨胀等因素,不能很好的预测未来;(3)难于精确计量,造成数据过于主观;(4)许多环境因素也会影响会计信息。

中英合作国际财务管理复习笔记(全

中英合作《国际财务管理》复习笔记第一章总论1、国际财务管理是现代财务管理的一个新领域。

把其作为一个专题加以研究始于20世纪50年代。

2、国际财务管理的目标、内容、方法体系尚不成熟。

3、国际财务管理定义的不同观点:(1)视国际财务管理为世界财务管理:(最普遍适用的原理和方法)远离现实,只能作为方向;(2)视国际财务管理为比较财务管理:缺乏实质性内容;(3)视国际财务管理为跨国公司财务管理:不能完全概括国际财务管理的内容。

4、跨国公司的主要内容:(1)由在两个或两个以上国家营业的一组企业组成;(2)是根据资本所有权合同或其它安排建立的共同控制下营业的;(3)各实体退行全球战略时,共享资源和分担责任。

5、国际财务管理研究:一切国际企业在组织财务活动、处理财务关系时所遇到的特殊问题。

6、国际企业指一切超越国境从事生产经营的企业,包括跨国公司、外贸公司、合资公司。

(多选)7、一个国际企业可能不是跨国公司,但任何跨国公司都属于国际企业。

(判断)8、国际财务管理是按国际惯例和国际经济法的有关条款,根据国际企业财务收支的特点,组织国际企业的财务活动,处理国际财务关系的一项经济管理活动。

9、国际财务管理的基本特点:(多选)(1)理财环境的复杂性;(2)资金筹集的可选择性;(3)资金投资的高风险性。

10、国际企业理财环境的复杂性体现在:(1)汇率的变化;(2)外汇的管制程度;(3)通货膨胀和利率的高低;(4)税负的轻重;(5)资本抽回的限制程度;(6)资本市场的完善程度;(7)政治上的稳定程度。

11、筹资选择的方式:(多选)①母公司地主国资金;②子公司东道国资金;③向国际金融机构筹资;④向国际金融市场筹资。

12、国际企业资金投资的风险性分为两大类:(一)经济与经营方面的风险:①汇率变动风险;②利率变动风险;③通货膨胀风险;④经营管理风险;⑤其他经营风险。

(二)上层建筑与政治风险:①政府变动的风险;②政策变动的风险;③战争因素的风险;④法律方面的风险;⑤其他风险。

国际会计(双语)

国际会计(双语)最牛英语口语培训模式:躺在家里练口语,全程外教一对一,三个月畅谈无阻!太平洋英语,免费体验全部外教一对一课程:第七章练习题(第七章全球环境下财务报告与信息披露)第一节全球企业合并、商誉和无形资产会计处理第二节全球分部报告信息披露第三节国际信息披露准则第四节公司财务报告信息披露与发展趋势习题1.名词解释1.1企业合并1.2吸收合并1.3创立合并1.4所有权(业主观)理论1.5实体(主体观)理论1.6购买法1.7权益结合法1.8商誉1.9无形资产1.10分部报告1.11分部收入1.12分部费用1.13分部资产1.14分部负债1.15知识经济2.单项选择题2.1赞成将商誉不进行摊销,而将其保留在资产负债表中的观点认为()。

A 所有的成本都应该成为费用B 商誉是一项资产,它不给企业带来为来的经济利益。

C 对商誉进行摊销会给企业带来压力。

D 商誉的未来价值体现在企业的持续经营中。

E这中做法会使利润虚增。

2.2赞成将品牌作为一项资产而不进行摊销的观点认为()。

A 品牌在持续经营中很容易增值B 这是一中倾向于保守思想C 这是一种好的市场工具D品牌的价值是保持并通过定期的广告获得的。

E它有助于平滑公司的收益。

2.3国际会计准则对品牌的会计处理要是()。

A定期进行重估其价值B作为当期发生的费用C根据国际惯例进行计价D不包括以上各项2.4研究与开发费用属于()。

A在美国是资本化B当企业的研究与开发费用下跌时,其在全球范围内行业中所处的地位也随之下跌。

C 在全球范围内一致要求将研究与开发成本费用化D根据经修订的国际会计准则第9号,分成各部分进行处理。

E 作为一项不能够减免所得税的费用2.5从经济理由考虑,作为投资者其要求的地理分部资料是()。

A它有助于了解公司对各产品线的所依赖程度B 它有助于了解不同国家劳动力成本C 它有助于了解公司在不同国家和地区进行投资的机会和风险D它有助于公司将利润从高税率国家向低税率国家转移。

(财务会计)国际会计复习资料中英结合版

国际会计复习资料A.Basic Knowledge1.we view accounting as consisting of three broad areas: measurement、[‘meʒəmənt](计量)disclosure[dis’kləuʒə](披露) and auditing[‘ɔ:ditiŋ](审计).2.The three international organization of accounting profession are(International Federation of Accountants;IFAC)(国际会计师联合会)(International Accounting Standards Committee; IASC)(国际会计准则委员会)(International Auditing practice Committee;IAPC) (国际审计实务委员会)3.Hofstede’s four cultural dimensions are(霍夫斯泰德的四个文化层面):(1)individualism(个人主义)(2)power distance(权力距离)(3)uncertainty avoidance(风险规避)(4)masculinity(阳刚之气)4. The four culture dimensions that affect a nation’s financial reporting practices by Gray refer to?影响一个国家的财务报告的做法的四个层面系指:(1)Professionalism (职业主义维度)(2)Uniformity (统一性维度)(3)conservatism (保守主义维度)(4)Secrecy (保密性维度)5.Accounting standard setting normally involves a combination of private and public sector groups.(会计准则的制定通常涉及结合私营和公共部门的群体。

会计复习资料(中英文对照)

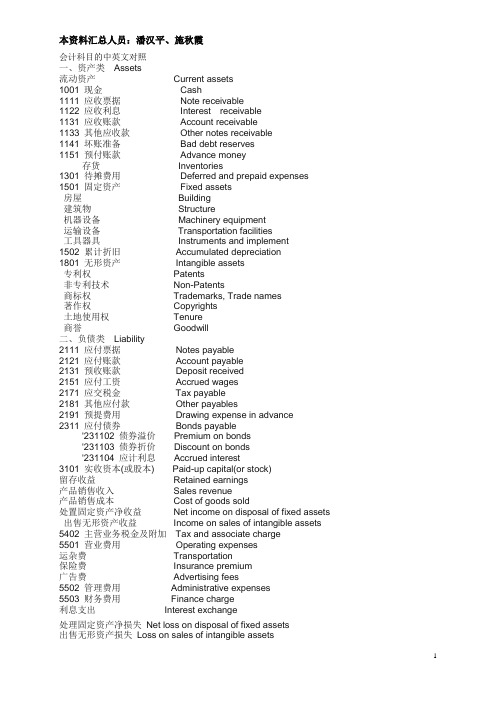

本资料汇总人员:潘汉平、施秋霞会计科目的中英文对照一、资产类Assets流动资产Current assets1001 现金Cash1111 应收票据Note receivable1122 应收利息Interest receivable1131 应收账款Account receivable1133 其他应收款Other notes receivable1141 坏账准备Bad debt reserves1151 预付账款Advance money存货Inventories1301 待摊费用Deferred and prepaid expenses 1501 固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement1502 累计折旧Accumulated depreciation1801 无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill二、负债类Liability2111 应付票据Notes payable2121 应付账款Account payable2131 预收账款Deposit received2151 应付工资Accrued wages2171 应交税金Tax payable2181 其他应付款Other payables2191 预提费用Drawing expense in advance2311 应付债券Bonds payable'231102 债券溢价Premium on bonds'231103 债券折价Discount on bonds'231104 应计利息Accrued interest3101 实收资本(或股本) Paid-up capital(or stock)留存收益Retained earnings产品销售收入Sales revenue产品销售成本Cost of goods sold处置固定资产净收益Net income on disposal of fixed assets 出售无形资产收益Income on sales of intangible assets 5402 主营业务税金及附加Tax and associate charge5501 营业费用Operating expenses运杂费Transportation保险费Insurance premium广告费Advertising fees5502 管理费用Administrative expenses5503 财务费用Finance charge利息支出Interest exchange处理固定资产净损失Net loss on disposal of fixed assets出售无形资产损失Loss on sales of intangible assetsQuiz #1The balance sheet of V erbeek Company as of December 31,2002, is presented below.V erbeek公司2003年12月31日的资产负债表如下Verbeek companyBalance SheetAs of December 31,2002Assets Liabilities and Stockholders’ Equity Cash $3900 Accounts payable $2985Accounts receivable 4985 Notes payable 4000Inventory 3300 Total liabilities 6985Office equipment 4800Accum.depr. (1440) Common stock $10000Furniture and fixtures 6600 Retained earnings 2960 12960Accum.depr. (2200) Total liabilities andzTotal assets 19945 stockholders’ Equity $19945The following transactions occur during the month of January 2003.以下是发生在2003年1月的业务Jan. 2 Receives payment of $1230 on accounts receivable. 收回应收账款3Purchases merchandise on account from Weight Co. $2184,2/30,n/60 f.o.b. shipping point(record at gross amount). 从Weight公司赊购商品4Receives an invoice from Ranger, a trade magazine, for advertising, $75.收到贸易杂志公司Ranger发来的广告费发票4 Sells merchandise on account to Sandstrom Co. for $1534,2/10,n/30 f.o.b. shipping point.赊销商品给Sandstrom公司4 Makes a cash sale to Kariya Inc., for $1786.现金销售给Kariya6 Sends a letter to Weight Co., regarding a slight defect in one item of merchandise received.发出信函给Weight公司,告诉对方说收到的商品有缺陷9 purchases merchandise on account from Fleury’s Novelty Company,$651.从Fleury’s Novelty公司赊购商品11 Pays freight on merchandise received from Weight Co., $76.支付从weight公司采购货物的运费11 Receives a credit memo form Weight Co. granting an allowance of $34 on defectivemerchandise(see transaction of January 6 ).收到weight公司同意给予$34折扣的函件15 Receives $600 on account to from Sandstrom Co.收回Sandstrom公司的应收账款19 Sells merchandise on account to Brett Huill,$812,2/10,n/30.赊销商品给Brett Huill公司21 Pays display clerk’s salary of $552.支付员工工资25 Sells merchandise for cash, $2350.现金销售商品27 Purchases office equipment on account,$879(begin depreciating in February ).购买办公设备(2月份开始计算折旧)29 Pays Weight Co. in full of account.全额支付weight公司货款30 Receives a note from Brett Huill in full of account.收到Brett Huill的票据31 A count of the inventory on hand reveals $2640 salable merchandise.月末盘点商品库存余额为$2640Instructions要求(a)Open ledger accounts at January 1,2003. 开2003年1月的账目并编制分录(b)Enter the transactions into ledger accounts. 记账(编制T字帐)(c)Prepare a trial balance after adjusting for depreciation; use 8-year life, straight-line method, and nosalvage for all long-term assets. Interest at 12% on the note payable is due every December 31. 编制调整分录,计提折旧(使用期限8年,直线计提折旧,无残值),应付票据的年利率为12%,编制试算平衡表(d)Prepare a balance sheet and income statement (Ignore income taxes).编制资产负债表和利润表(不考虑所得税)(e)Close the ledger. 结账(f)Take a post-closing trial balance. 编制结账后的试算平衡表Answers to Quiz #1(a) (b) (d)1-2 Cash 1230Accounts Receivable 1230 1-3 Purchases 2184Accounts Payable 2184 1-4 Advertising Expense 75Accounts Payable 75 1-4 Accounts Receivable 1534Sales 1534 1-4 Cash 1786Sales 1786 1-6 No entry1-9 Purchases 651Accounts Payable 651 1-11 Transportation-In 76Cash 76 1-11 Accounts Payable 34Purchases Allowances 34 1-15 Cash 600Accounts Receivable 600 1-19 Accounts Receivable 812Sales 812 1-21 Salary Expense 552Cash 552 1-25 Cash 2350Sales 2350 1-27 Office equipment 879Accounts Payable 879 1-29 Accounts Payable 2150Cash 2107Purchases Discounts 43 1-30 Notes Receivable 812Accounts Receivable 812 1-31-1Cost of Goods Sold 6134Purchase Allowance 34Purchase Discounts 43Purchase 2835Inventory 3300Transportation-In 76 1-31-2Inventory 2640Cost of Goods Sold 2640 1-31-3Income Summary 3494Cost of Goods Sold 3494 1-31Interest Expense 40Interest Payable 40 1-31Sales 6482Income Summary 6842 Income Summary 75Advertising Expense 75 Income Summary 552Salary Expense 552 Income Summary 119Accum.Depr.-Furn.&Fixt. 69Accum.Depr.-Off.Equip. 50 Income Summary 40Interest Expense 40 Income Summary 2202Retained Earnings 2202Notes Receivable1-30 812Furniture and Fixtures Bal. 6600Office EquipmentBal. 4800 1-27 879 Bal. 5679 2-1 5679 Common StockBal. 10000Notes PayableBal. 4000 Interest Payable Advertising Expense1-31 40 1-4 75 1-31- 75Expanations:January 29 2%*($2184-$34)=$43 Purchase DiscountsJanuary 31 Depreciation:Office Equipment $4800Furniture and Fixtures 6600Total $11400($11400/8)*1/12= $119January 31 Interest $4000*12%*1/12=$40V erbeek CompanyAdjusted Trial BalanceJanuary 31,2003Debit Credit Cash 7131Accounts Receivable 4689Notes Receivable 812Inventory 3300Office Equipment 5679Accumulated Depreciation—Office Equip. 1490 Furniture and Fixtures 6600Accumulated Depreciation-Furn.&Fixt. 2269 Accounts Payable 4590 Notes Payable 4000 Interest Payable 40 Common Stock 10000 Retained Earnings 2960 Sales 6482 Purchases 2835Advertising Expense 75Transportation-In 76Salary Expense 552Depreciation Expense 119Interest Expense 40Purchase Allowances 34 Purchase Discounts 4331908 31908 (e)V erbeek CompanyBalance SheetJ a n u a r y31,2003Assets Liabilities and Stockholder’s Equity Cash $7131 Notes payable $4000 Accounts receivable 4689 Accounts payable 4590 Notes receivable 812 Interest payable 40 Inventory 2640 Total liabilities 8630 Office equipment $5679 Common stock 10000Less: Acc.depr. Retained earnings 5162 15162 Off.equip. 1490 4189Furniture & fixtures 6600 Total liabilities andLess: Acc.depr. stockholder’s equity $23792Furn.&fixt. 2269 4331Total assets $23792Beginning balance $2960Net income 2220Ending balance $5162V erbeek CompanyIncome StatementF o r t h e M o n t h E n d e d J a n u a r y31,2003Revenue from sales $6482 Cost of Goods Sold:Inventory, January 1 $3300Purchases $2850Less: Allowances $34Discounts 43 77Net purchases 2758Transportation-In 76Net cost of purchasesCost of goods available for sale 6134Inventory, January 31 2640Cost of goods sold 3494 Gross profit 2988 Expresses:Salary expense 552Advertising expense 75Depreciation expense 119Interest expense 40 786 Net income $2202(f)V erbeek CompanyPost-Closing Trial BalanceJ a n u a r y31,2003Debit Credit Cash 7131Accounts Receivable 4689Notes Receivable 812Inventory 2640Office Equipment 5679Accumulated Depreciation—Office Equip. 1490 Furniture and Fixtures 6600Accumulated Depreciation-Furn.&Fixt. 2269 Accounts Payable 4590 Notes Payable 4000 Interest Payable 40 Common Stock 10000 Retained Earnings 5162 Totals 27551 27551Quiz #2(Adjusting Entries) The accounts listed below appeared in the December 31 trial balance of the Jane Alexander Theater.Jane Alexander电影院在12月31日的科目试算平衡表如下Debit CreditEquipment $192000Accumulated Depreciation of Equipment $60000Notes Payable 90000Admissions Revenue 380000Concessions Revenue 36000Advertising Expense 13680Salaries Expense 57600Interest Expense 1400Instructions要求(a)From the account balances listed above and the information given below prepare the annual adjusting entries necessary on December 31.根据上面给出的试算平衡表和下面的资料,在12月31日编制必要的年度调整分录1.The equipment has an estimated life of 16 years and a trade-in value of $40000 at the end of thattime.(Use straight line method.)设备预计使用年限16年,预计残值40000元,(直线折旧)2.The notes payable is a 90-day note given to the bank October 20 and bearing interest at 10%.(Use 360days for denominator.)10月20日开出90天应付票据给银行,利率为10%(按一年360天计)3.In December 2000 coupon admission books were sold at $25 each; they could be used for admissionany time after January 1. 12月销售2000份预售门票,按每份25元卖出,该门票可以在1月1日后使用4.The concession stand is operated by a concessionaire who pays 10% of gross receipts for the privilegeof selling popcorn, candy, and soft drinks in the lobby. Sales for December were $3470,and the 10% due for December has not yet been received or entered.在大堂卖爆米花,糖果和软饮料的店铺需要支付总收入的10%作为特许权的收费。

会计专业英语复习资料10页word文档

会计专业英语复习资料一、短语中英互译1、会计分录2、投资活动3、后进先出法4、客观性原则5、注册会计师6、权责发生制7、累计折旧8、资产负债表9、经营决策10、银行存款11、到期日12、历史成本13、source document14、nominal rate15、credit sale16、sum-of-years-digits method17、economic entity assumption18、financial position19、fixed assets20、public hearing21、income statement22、sales discount23、value added tax24、trade mark25、bank overdraft二、从下列选项中选出最佳答案1、Generally,revenue is recorded by a business enterprise at a pointwhen :( )A、Management decides it is appropriate to do soB、The product is available for sale to consumersC、An exchange has taken place and the earning process isvirtually completeD、An order for merchandise has been received2、Why are certain costs capitalized when incurred and then depreciated or amortized over subsequent accounting periods?( )A、To reduce the income tax liabilityB、To aid management in making business decisionsC、To match the costs of production with revenue as earnedD、To adhere to the accounting concept of conservatism3、What accounting principle or concept justifies the use of accruals and deferrals?( )A、Going concernB、MaterialityC、ConsistencyD、Stable monetary unit4、An accrued expense can best be described as an amount ( )A、Paid and currently matched with revenueB、Paid and not currently matched with revenueC、Not paid and not currently matched with revenueD、Not paid and currently matched with revenue5、Continuation of a business enterprise in the absence of contrary evidence is an example of the principle or concept of ( )A、Business entityB、ConsistencyC、Going concernD、Substance over form6、In preparing a bank reconciliation,the amount of checks outstanding would be:( )A、added to the bank balance according to the bank statement.B、deducted from the bank balance according to the bank statement.C、added to the cash balance according to the depositor’s records.D、deducted from the cash balance according to the depositor’srecords.7、Journal entries based on the bank reconciliation are requiredfor:( )A、additions to the cash balance according to the depositor’srecords.B、deductions from the cash balance according to the depositor’srecords.C、Both A and BD、Neither A nor B8、A petty cash fund is :( )A、used to pay relatively small amounts。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

国际会计复习资料A.Basic Knowledge1.we view accounting as consisting of three broad areas: measurement、[‘meʒəmənt](计量)disclosure[dis’kləuʒə](披露) and auditing[‘ɔ:ditiŋ](审计).2.The three international organization of accounting profession are(International Federation of Accountants;IFAC)(国际会计师联合会)(International Accounting Standards Committee; IASC)(国际会计准则委员会)(International Auditing practice Committee;IAPC) (国际审计实务委员会)3.Hofstede’s four cultural dimensions are(霍夫斯泰德的四个文化层面):(1)individualism(个人主义)(2)power distance(权力距离)(3)uncertainty avoidance(风险规避)(4)masculinity(阳刚之气)4. The four culture dimensions that affect a nation’s financial reporting practices by Gray refer to?影响一个国家的财务报告的做法的四个层面系指:(1)Professionalism (职业主义维度)(2)Uniformity (统一性维度)(3)conservatism (保守主义维度)(4)Secrecy (保密性维度)5.Accounting standard setting normally involves a combination of private and public sector groups.(会计准则的制定通常涉及结合私营和公共部门的群体。

)6.The private sector includes the accounting profession and other groups affected by the financial reporting process.(私营部门包括会计专业和受财务报告程序影响的其他团体。

)7.The public sector includes such agencies as tax authorities ministries responsible for commercial law,and securities commissions.(公共部门,包括负责商业法的税务机关部委和证券委员会)8.One key distinction in financial reporting is whether accounting is oriented toward (定位于)a fair presentation (公允表述)of financial position and results of operations or toward compliance with legal (符合法律法规)requirements and tax laws.9.The countries who emphasize Fairness and substance over form include United Kingdom, United States, Canada, Mexico and Philippines.Their accounting systems are usuallyassociated with a common law legal system and shareholders as the principal source of finance.(强调公平和实质重于形式的国家包括英国,美国,加拿大,墨西哥和菲律宾。

它们的会计制度通常与普通法法律制度和股东的主要资金来源联系。

10.Countries whose accounting system are oriented toward compliance with legal(符合法律法规)requirements tend to have a code law legal system and rely heavily on banks and the governments as sources of finance.11.Accounting in the United States is regulated by a private sector body the Financial Accounting Standards board, or FASB(财务会计准则委员会),but a governmental agency (the Securities and Exchange Commission, or SEC)(美国证券交易委员会)underpins the authority of its standards. SEC have right to supervise and revise to the standard finally . 在美国会计是受一个私营部门机构(财务会计标准委员会)管制的,但政府机构(美国证券交易委员会)的权威基础是其标准。

美国证券交易委员会最后也有权监督和修订标准。

12.The basic characteristic of United Kingdom Accounting pattern is the requirement to financial accounting and report is from the companies law.(公司法)13.Th e accounting “the true and fair” view appear in United Kingdom companies law (1948) first. (会计的“真实和公正”第一次出现在英国的公司法)13.FASB has Seven full-time members?(财务会计准则委员会有7个全职成员)14 In France , large companies must also prepare documents relating to the prevention of business bankruptcies and a social report .(在法国,大企业也必须准备有关防止企业破产和和社会报告。

的文件)15.The following three exchange rates can be used to translate foreign currency balances to domestic currency.they are the current rate.the historical rate and the average rate(以下三个汇率可以用来转化外币货币为本国货币.它们是现行汇率,历史汇率和平均汇率)16.There are four methods can answer the questions above and be used in foreign currency translation.Concepts:1.current rate method(现行汇率法)2.current-noncurrent method(流动性与非流动性法)3.monetary-nonmonetary method(货币性与非货币性项目法)4.temporal method(时态法)17.In a direct quote(直接标价), the exchange rate specifies the number of domestic currency units (本国货币单位)needed to acquire a unit of foreign currency.(外国货币)18.The majority countries in the world use the direct quote except British and America .19.under deferral(递延)method translation gains and losses (外币折算损益)are listed on the balance sheet (资产负债表). It is regarded as a single item”“Translation gains ( losses)”, list atthe part of “owner’s equity”(所有者权益).20. The government of the hostcountry levy taxes on the benefit from dividend(股息), interest (利息)and royalty payments(特许使用金)that gained by foreign invester is withholding tax (预提所得税) .21.There are three calculation of added-value tax(增值税)additive method(叠加法),subtractive method(减数法)and tax by tax method.( tax-deducting method )(实耗扣税法)But most countries use tax by tax method.22.There are three recognition principles about the revenue(收入)that foreign institutions obtained in foreign countries : principle of territorial(属地管辖), principle of person and world principle.23. There are three major international popular tax administration systems, namely, classical system,tax-split system(税收分割制度)and shift system.(轮班制度)24. the method of avoidance of international double taxation usually consist of tax deductions,tax credit and tax exemption..(避免国际双重征税的方法通常包括减税,课税扣除和免税)25.The important act relate to British accounting regulation is The Companies Act.涉及到英国的会计制度最重要的法例是公司法。