企业会计准则第号——合并财务报表-中英对照

新会计准则 中英文会计科目对照表

新会计准则中英文会计科目对照表新会计准则中英文会计科目对照表中英文会计科目对照表如下:会计科目中英对照表会计科目 accounting subject顺序号serial number编号code number会计科目名称accounting subject会计科目适用范围accounting subject range of application一、资产类 1 1001库存现金 cash on hand2 1002 银行存款 bank deposit5 1015 其他货币资金 other monetary capital9 1101 交易性金融资产 transaction monetary assets11 1121 应收票据 notes receivable12 1122 应收账款 Account receivable13 1123 预付账款 account prepaid14 1131 应收股利 dividend receivable15 1132 应收利息 accrued interest receivable21 1231 其他应收款 accounts receivable-others22 1241 坏账准备 had debts reserve28 1401 材料采购 procurement of materials29 1402 在途物资 materials in transit30 1403 原材料 raw materials32 1406 库存商品 commodity stocks33 1407 发出商品 goods in transit36 1412 包装物及低值易耗品 wrappage and low value and easily wornout articles42 1461 存货跌价准备 reserve against stock price declining43 1501 待摊费用 fees to be apportioned45 1521 持有至到期投资 hold investment due46 1522 持有至到期投资减值准备 hold investment due reduction reserve47 1523 可供出售金融资产 financial assets available for sale48 1524 长期股权投资 long-term stock ownership investment49 1525 长期股权投资减值准备 long-term stock ownership investmentreduction reserve50 1526 投资性房地产 investment real eastate51 1531 长期应收款 long-term account receivable52 1541 未实现融资收益 unrealized financing income54 1601 固定资产 permanent assets55 1602 累计折旧 accumulated depreciation56 1603 固定资产减值准备permanent assets reduction reserve57 1604 在建工程 construction in process58 1605 工程物资 engineer material59 1606 固定资产清理 disposal of fixed assets60 1611 融资租赁资产租赁专用 financial leasing assets exclusively for leasing61 1612 未担保余值租赁专用 unguaranteed residual value exclusively for leasing62 1621 生产性生物资产农业专用 productive living assets exclusively for agriculture63 1622 生产性生物资产累计折旧农业专用 productive living assets accumulated depreciation exclusively for agriculture64 1623 公益性生物资产农业专用 non-profit living assets exclusively for agriculture65 1631 油气资产石油天然气开采专用 oil and gas assets exclusively for oil and gas exploitation66 1632 累计折耗石油天然气开采专用 accumulated depletion exclusively for oil and gas exploitation67 1701 无形资产 intangible assets68 1702 累计摊销 accumulated amortization69 1703 无形资产减值准备 intangible assets reduction reserve70 1711 商誉 business reputation71 1801 长期待摊费用 long-term deferred expenses72 1811 递延所得税资产 deferred income tax assets73 1901 待处理财产损溢 waiting assets profit and loss二、负债类 debt group74 2001 短期借款 short-term loan81 2101 交易性金融负债 transaction financial liabilities83 2201 应付票据 notes payable84 2202 应付账款 account payable85 2205 预收账款 item received in advance86 2211 应付职工薪酬 employee pay payable87 2221 应交税费 tax payable88 2231 应付股利 dividend payable89 2232 应付利息 interest payable90 2241 其他应付款 other account payable97 2401 预提费用 withholding expenses98 2411 预计负债 estimated liabilities99 2501 递延收益 deferred income100 2601 长期借款 money borrowed for long term101 2602 长期债券 long-term bond106 2801 长期应付款 long-term account payable107 2802 未确认融资费用 unacknowledged financial charges108 2811 专项应付款 special accounts payable109 2901 递延所得税负债 deferred income tax liabilities三、共同类112 3101 衍生工具 derivative tool113 3201 套期工具 arbitrage tool114 3202 被套期项目 arbitrage project四、所有者权益类115 4001 实收资本 paid-up capital116 4002 资本公积 contributed surplus117 4101 盈余公积 earned surplus119 4103 本年利润 profit for the current year120 4104 利润分配 allocation of profits121 4201 库存股 treasury stock五、成本类122 5001 生产成本 production cost123 5101 制造费用 cost of production124 5201 劳务成本 service cost125 5301 研发支出 research and development expenditures126 5401 工程施工建造承包商专用 engineering construction exclusively for construction contractor127 5402 工程结算建造承包商专用 engineering settlement exclusively for construction contractor128 5403 机械作业建造承包商专用 mechanical operation exclusively for construction contractor六、损益类129 6001 主营业务收入main business income130 6011 利息收入金融共用 interest income financial sharing135 6051 其他业务收入 other business income136 6061 汇兑损益金融专用 exchange gain or loss exclusively for finance137 6101 公允价值变动损益 sound value flexible loss and profit138 6111 投资收益 income on investment142 6301 营业外收入 nonrevenue receipt143 6401 主营业务成本 main business cost144 6402 其他业务支出 other business expense145 6405 营业税金及附加 business tariff and annex146 6411 利息支出金融共用 interest expense financial sharing155 6601 销售费用 marketing cost 156 6602 管理费用 managing cost157 6603 财务费用 financial cost 158 6604 勘探费用 exploration expense 159 6701 资产减值损失 loss from asset devaluation160 6711 营业外支出 nonoperating expense 161 6801 所得税 income tax 162 6901 以前年度损益调整prior year profit and loss adjustmentAccounting StandardsAuthoritative & interpretive literature. FASB, AICPA, SEC &more 新会计准则英汉对照目录Effective 2007 for Listed Companies1. 企业会计准则————————-基本准则(Accounting Standard for Business Enterprises - Basic Standard)2. 企业会计准则第1 号————————-存货(Accounting Standard for Business Enterprises No. 1 - Inventories)3. 企业会计准则第2 号————————-长期股权投资(Accounting Standard for Business Enterprises No. 2 - Long-term equity investments)4. 企业会计准则第3 号————————-投资性房地产(Accounting Standard for Business Enterprises No. 3 - Investment properties)5. 企业会计准则第4 号————————-固定资产(Accounting Standard for Business Enterprises No. 4 - Fixed assets)6. 企业会计准则第5 号————————-生物资产(Accounting Standard for Business Enterprises No. 5 - Biological assets)7. 企业会计准则第6 号————————-无形资产(Accounting Standard for Business Enterprises No. 6 - Intangible assets)8. 企业会计准则第7 号————————-非货币性资产:)(Accounting Standard for Business Enterprises No. 7 - Exchange of non-monetary assets)9. 企业会计准则第8 号————————-资产减值(Accounting Standard for Business Enterprises No. 8 - Impairment of assets)10. 企业会计准则第9 号————————-职工薪酬(Accounting Standard for Business Enterprises No. 9 –Employee compensation )11. 企业会计准则第10 号————————企业年金基金(Accounting Standard for Business Enterprises No. 10 - Enterprise annuity fund)12. 企业会计准则第11 号————————股份支付(Accounting Standard for Business Enterprises No. 11 - Share-based payment)13. 企业会计准则第12 号————————债务重组(Accounting Standard for Business Enterprises No. 12 - Debt restructurings)14. 企业会计准则第13 号————————或有事项(Accounting Standard for Business Enterprises No. 13 - Contingencies)15. 企业会计准则第14 号————————收入(Accounting Standard for Business Enterprises No. 14 - Revenue)16. 企业会计准则第15 号————————建造合同(Accounting Standard for Business Enterprises No. 15 - Construction contracts)17. 企业会计准则第16 号————————政府补助(Accounting Standard for Business Enterprises No. 16 - Government grants)18. 企业会计准则第17 号————————借款费用(Accounting Standard for Business Enterprises No. 17 - Borrowing costs)19. 企业会计准则第18 号————————所得税(Accounting Standard for Business Enterprises No. 18 - Income taxes)20. 企业会计准则第19 号————————外币折算(Accounting Standard for Business Enterprises No. 19 - Foreign currency translation)21. 企业会计准则第20 号————————企业合并(Accounting Standard for Business Enterprises No. 20 - Business Combinations)22. 企业会计准则第21 号————————租赁(Accounting Standard for Business Enterprises No. 21 - Leases)23. 企业会计准则第22 号————————金融工具确认和计量(Accounting Standard for Business Enterprises No. 22 - Recognition and measurement of financial instruments)24. 企业会计准则第23 号————————金融资产转移(Accounting Standard for Business Enterprises No. 23 - Transfer of financial assets)25. 企业会计准则第24 号————————套期保值(Accounting Standard for Business Enterprises No. 24 - Hedging)26. 企业会计准则第25 号————————原保险合同(Accounting Standard for Business Enterprises No. 25 - Direct insurance contracts)27. 企业会计准则第26 号————————再保险合同(Accounting Standard for Business Enterprises No. 26 -Re-insurance contracts)28. 企业会计准则第27 号————————石油天然气开采(Accounting Standard for Business Enterprises No. 27 - Extraction of petroleum and natural gas)29. 企业会计准则第28 号————————会计政策、会计估计变更和差错更正(Accounting Standard for Business Enterprises No. 28 - Changes in accounting policie and estimates, and correction of errors)30. 企业会计准则第29 号————————资产负债表日后事项(Accounting Standard for Business Enterprises No. 29 - Events occurring after the balance sheet date)31. 企业会计准则第30 号————————财务报表列报(Accounting Standard for Business Enterprises No. 30 - Presentation of financial statements)32. 企业会计准则第31 号————————现金流量表(Accounting Standard for Business Enterprises No. 31 - Cashflow statements)33. 企业会计准则第32 号————————中期财务报告(Accounting Standard for Business Enterprises No. 32 - Interim financial reporting)34. 企业会计准则第33 号————————合并财务报表(Accounting Standard for Business Enterprises No. 33 - Consolidated financial statements)35. 企业会计准则第34 号————————每股收益(Accounting Standard for Business Enterprises No. 34 - Earnings per share)36. 企业会计准则第35 号————————分部报告(Accounting Standard for Business Enterprises No. 35 - Segment reporting)37. 企业会计准则第36 号————————关联方披露(Accounting Standard for Business Enterprises No. 36 - Related party disclosure)38. 企业会计准则第37 号————————金融工具列报(Accounting Standard for Business Enterprises No. 37 - Presentation of financial instruments)39. 企业会计准则第38 号————————首次执行企业会计准则(Accounting Standard for Business Enterprises No.38 - First time adoption of Accounting Standards for Business Enterprises)审计法Audit Law, Audit Act审计法实施条例the Implementary Rules of the Audit law审计标准audit criteria,audit standard审计准则auditing standard审计原则auditing principles审计手册audit manual公认审计准则Generally Accepted Auditing Standards审计法律规范audit laws and regulations审计体制audit system审计权限audit purview;audit jurisdiction;audit mandate 审计职责audit responsibility审计监督audit supervision;supervision through auditing 审计管辖权audit jurisdiction审计执法implementation of audit laws and regulations审计处理audit sanction审计处罚audit penalty依法审计conduct auditing in accordance with laws审计意见audit opinion审计决定audit decision审计建议audit suggestion, audit recommendation复核意见conclusion of audit review审计复议audit appeal审计听证audit hearing审计复核audit review审计战略audit strategy审计计划audit plan审计方案auditing program 审计目标auditing objective 审计范围audit scope审计内容audit coverage审计结论audit conclusion审计任务audit assignments 审计结果audit finding审计报告audit report审计方法audit method审计过程auditing process审计证据audit evidence审计测试audit test审计风险audit risk审计抽样audit sampling审计软件audit software审计程序auditing procedures 审计调查audit investigation 审计小组audit team审计线索audit trail工作底稿working paper绕过计算机审计auditing around the computer通过计算机审计auditing through the computer计算机辅助审计computer-assited audit信息技术审计IT audit合法性审计compliance audit, regularity audit合规性审计compliance audit综合审计comprehensive audit效益审计value for money audit (VFM audit)绩效审计performance audit财务审计financial audit财务报表审计financial statement audit财务收支审计audit of financial revenues and expenditures 决算审计final account audit经济责任审计accountability audit任中经济责任审计middle term accountability audit离任经济责任审计term-end accountability audit管理审计management audit项目审计project audit外部审计external audit内部审计internal audit政府审计government audit联合审计joint audit实地审计field audit期末审计final audit期中审计interim audit定期审计periodic audit初次审计initial audit初步审计preliminary audit事后审计post-audit事前审计pre-audit事中审计concurrent audit专项审计special audit法定审计statutory audit后续审计successive audit跟踪审计follow up audit全过程审计whole process auditing 突击审计surprise audit审计报告audit report标准报告standard report长式报告long-form report短式报告short-form report审计工作报告audit working report审计结果公告Announcement of Audit Findings审计长Auditor General副审计长Deputy Auditor General审计主任chief auditor资深审计师senior auditor审计师(员)auditor注册内部审计师certified internal auditor(CIA)注册信息系统审计师certified information systems auditor(CISA)注册公共会计师certified public accountant(CPA)特许会计师chartered accountant(CA)审计经费audit funds审计业务费audit operating expense审计专项经费special funds for auditing无保留意见:unqualified opinion保留意见qualified opinion无法表示意见: disclaimer of opinion否定意见:adverse opinion。

2021年《企业会计准则第33号——合并财务报表》【-发布】

企业会计准则第33号——合并财务报表第一章总则第一条为了规范合并财务报表的编制和列报,根据《企业会计准则——基本准则》,制定本准则。

第二条合并财务报表,是指反映母公司和其全部子公司形成的企业集团整体财务状况、经营成果和现金流量的财务报表。

母公司,是指控制一个或一个以上主体(含企业、被投资单位中可分割的部分,以及企业所控制的结构化主体等,下同)的主体。

子公司,是指被母公司控制的主体。

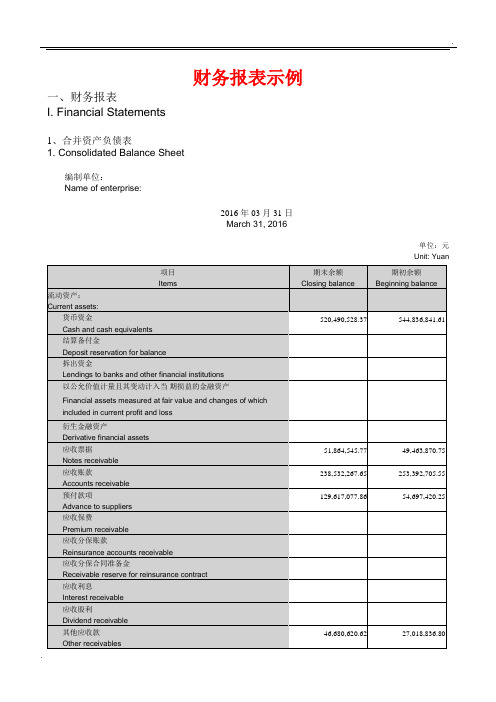

第三条合并财务报表至少应当包括下列组成部分:(一)合并资产负债表;(二)合并利润表;(三)合并现金流量表;(四)合并所有者权益(或股东权益,下同)变动表;(五)附注。

企业集团中期期末编制合并财务报表的,至少应当包括合并资产负债表、合并利润表、合并现金流量表和附注。

第四条母公司应当编制合并财务报表。

如果母公司是投资性主体,且不存在为其投资活动提供相关服务的子公司,则不应当编制合并财务报表,该母公司按照本准则第二十一条规定以公允价值计量其对所有子公司的投资,且公允价值变动计入当期损益。

第五条外币财务报表折算,适用《企业会计准则第19号——外币折算》和《企业会计准则第31号——现金流量表》。

第六条关于在子公司权益的披露,适用《企业会计准则第41号——在其他主体中权益的披露》第二章合并范围第七条合并财务报表的合并范围应当以控制为基础予以确定。

控制,是指投资方拥有对被投资方的权力,通过参与被投资方的相关活动而享有可变回报,并且有能力运用对被投资方的权力影响其回报金额。

本准则所称相关活动,是指对被投资方的回报产生重大影响的活动。

被投资方的相关活动应当根据具体情况进行判断,通常包括商品或劳务的销售和购买、金融资产的管理、资产的购买和处臵、研究与开发活动以及融资活动等。

第八条投资方应当在综合考虑所有相关事实和情况的基础上对是否控制被投资方进行判断。

一旦相关事实和情况的变化导致对控制定义所涉及的相关要素发生变化的,投资方应当进行重新评估。

企业会计准则中英对照

企业会计准则——基本准则Accounting Standard for Business Enterprises:Basic Standard第一章总则Chapter 1 General Provisions第一条为了规范企业会计确认、计量和报告行为,保证会计信息质量,根据《中华人民共和国会计法》和其他有关法律、行政法规,制定本准则。

Article 1 In accordance with The Accounting Law of the People’ s Republichinaof andC other relevant laws and regulations, this Standard is formulated to prescribe the recognition, measurement and reporting activities of enterprises for accounting purposesand to ensure the quality of accounting information.第二条本准则适用于在中华人民共和国境内设立的企业(包括公司,下同)。

Article 2 This Standard shall apply to enterprises (including companies) established within the People’s Republic of China.第三条企业会计准则包括基本准则和具体准则,具体准则的制定应当遵循本准则。

Article 3Accounting Standards for Business Enterprises include the Basic Standard andSpecific Standards. Specific Standards shall be formulated in accordance with this Standard.第四条企业应当编制财务会计报告(又称财务报告,下同)。

新发布企业会计准则目录(中英文对照版)

新发布企业会计准则目录(中英文对照版)企业会计准则目录Index for Accounting Standards for Business EnterprisesAnnounced February 2006Effective 2007 for Listed Companies1. 企业会计准则---------基本准则(Accounting Standard for Business Enterprises - Basic Standard)2. 企业会计准则第1 号---------存货(Accounting Standard for Business Enterprises No. 1 - Inventories)3. 企业会计准则第2 号---------长期股权投资(Accounting Standard for Business Enterprises No. 2 - Long-term equity investments) 4. 企业会计准则第3 号---------投资性房地产(Accounting Standard for Business Enterprises No. 3 - Investment properties)5. 企业会计准则第4 号---------固定资产(Accounting Standard for Business Enterprises No. 4 - Fixed assets)6. 企业会计准则第5 号---------生物资产(Accounting Standard for Business Enterprises No. 5 - Biological assets)7. 企业会计准则第6 号---------无形资产(Accounting Standard for Business Enterprises No. 6 - Intangible assets)8. 企业会计准则第7 号---------非货币性资产交换(Accounting Standard for Business Enterprises No. 7 - Exchange of non-monetary asset s)9. 企业会计准则第8 号---------资产减值(Accounting Standard for Business Enterprises No. 8 - Impairment of assets)10. 企业会计准则第9 号---------职工薪酬(Accounting Standard for Business Enterprises No. 9 – Employee compensation )11. 企业会计准则第10 号--------企业年金基金(Accounting Standard for Business Enterprises No. 10 - Enterprise annuity fund)12. 企业会计准则第11 号--------股份支付(Accounting Standard for Business Enterprises No. 11 - Share-based payment)13. 企业会计准则第12 号--------债务重组(Accounting Standard for Business Enterprises No. 12 - Debt restructurings)14. 企业会计准则第13 号--------或有事项(Accounting Standard for Business Enterprises No. 13 - Contingencies)15. 企业会计准则第14 号--------收入(Accounting Standard for Business Enterprises No. 14 - Revenue)16. 企业会计准则第15 号--------建造合同(Accounting Standard for Business Enterprises No. 15 - Construction contracts)17. 企业会计准则第16 号--------政府补助(Accounting Standard for Business Enterprises No. 16 - Government grants)18. 企业会计准则第17 号--------借款费用(Accounting Standard for Business Enterprises No. 17 - Borrowing costs)19. 企业会计准则第18 号--------所得税(Accounting Standard for Business Enterprises No. 18 - Income taxes)20. 企业会计准则第19 号--------外币折算(Accounting Standard for Business Enterprises No. 19 - Foreign currency translation) 21. 企业会计准则第20 号--------企业合并(Accounting Standard for Business Enterprises No. 20 - Business Combinations)22. 企业会计准则第21 号--------租赁(Accounting Standard for Business Enterprises No. 21 - Leases)23. 企业会计准则第22 号--------金融工具确认和计量(Accounting Standard for Business Enterprises No. 22 - Recognition and measurement offinancial instruments)24. 企业会计准则第23 号--------金融资产转移(Accounting Standard for Business Enterprises No. 23 - Transfer of financial assets)25. 企业会计准则第24 号--------套期保值(Accounting Standard for Business Enterprises No. 24 - Hedging)26. 企业会计准则第25 号--------原保险合同(Accounting Standard for Business Enterprises No. 25 - Direct insurance contracts)27. 企业会计准则第26 号--------再保险合同(Accounting Standard for Business Enterprises No. 26 - Re-insurance contracts)28. 企业会计准则第27 号--------石油天然气开采(Accounting Standard for Business Enterprises No. 27 - Extraction of petroleum and natural gas)29. 企业会计准则第28 号--------会计政策、会计估计变更和差错更正(Accounting Standard for Business Enterprises No. 28 - Changes in accounting policies and estimates, and correction of errors)30. 企业会计准则第29 号--------资产负债表日后事项(Accounting Standard for Business Enterprises No. 29 - Events occurring after thebalance sheet date)31. 企业会计准则第30 号--------财务报表列报(Accounting Standard for Business Enterprises No. 30 - Presentation of financialstatements)32. 企业会计准则第31 号--------现金流量表(Accounting Standard for Business Enterprises No. 31 - Cash flow statements)33. 企业会计准则第32 号--------中期财务报告(Accounting Standard for Business Enterprises No. 32 - Interim financial reporting)34. 企业会计准则第33 号--------合并财务报表(Accounting Standard for Business Enterprises No. 33 - Consolidated financialstatements)35. 企业会计准则第34 号--------每股收益(Accounting Standard for Business Enterprises No. 34 - Earnings per share)36. 企业会计准则第35 号--------分部报告(Accounting Standard for Business Enterprises No. 35 - Segment reporting)37. 企业会计准则第36 号--------关联方披露(Accounting Standard for Business Enterprises No. 36 - Related party disclosure)38. 企业会计准则第37 号--------金融工具列报(Accounting Standard for Business Enterprises No. 37 - Presentation of financialinstruments)39. 企业会计准则第38 号--------首次执行企业会计准则(Accounting Standard for Business Enterprises No. 38 - First time adoption ofAccounting Standards for Business Enterprises)。

企业会计准则2024中英对照

企业会计准则2024中英对照Enterprise Accounting Standards 2024Chapter 1: General Principles1.1 Purpose and Basis1.2 Scope of ApplicationThis standard is applicable to all enterprises engaged in production or business activities in the People's Republic of China. The specific accounting treatment shall be determined based on the nature and size of the enterprise.Chapter 2: Accounting Assumptions2.1 Going Concern AssumptionEnterprises are assumed to continue operating in the foreseeable future. Therefore, accounting records and financial statements should be prepared on the basis of this assumption.2.2 Accrual Basis AssumptionTransactions and events are recorded based on their economic substance and are recognized in the accounting records and financial statements when they occur, rather than when cash is received or paid.Chapter 3: Recognition and Measurement of Assets, Liabilities, and Equity3.1 Recognition of AssetsAn asset should be recognized if it is probable that future economic benefits associated with the asset will flow to the enterprise and the cost or value of the asset can be reliably measured.3.2 Recognition of LiabilitiesA liability should be recognized if it is probable that an outflow of economic benefits will be required to settle the obligation and the amount of the obligation can be reliably measured.3.3 Measurement of AssetsAssets should be initially measured at cost. Subsequently, assets should be measured at cost less accumulated depreciation, impairment loss, or fair value if the fair value is reliably measurable.3.4 Measurement of LiabilitiesLiabilities should be measured at the amount of proceeds received or receivable in exchange for the obligation. If the amount received or receivable is not fair value, the present value of the future cash outflows should be used as the measurement basis.4.1 Revenue RecognitionRevenue should be recognized when it is probable that future economic benefits will flow to the enterprise, and the amount of revenue can be reliably measured.4.2 Expense RecognitionExpenses should be recognized when it is probable that an outflow of economic benefits will be required to settle the related obligations and the amount of the expense can bereliably measured.Chapter 5: Presentation and Disclosure of Financial Statements5.1 Balance SheetThe balance sheet should present the financial position of the enterprise at a particular date, presenting assets, liabilities, and equity.5.3 Statement of Cash FlowsThe statement of cash flows should provide information about the cash flows of the enterprise during a particular period, classified into operating activities, investing activities, and financing activities.Chapter 6: Consolidated Financial Statements6.1 Consolidation PrinciplesConsolidated financial statements should be prepared when an enterprise has control over another entity or entities.6.2 Consolidation Procedures7.1 Acquisition Method7.2 Goodwill。

企业会计准则中英版

企业会计准则中英版企业会计准则是指对于企业会计核算和财务报告所制定的基本规则和规范。

它的主要目的是为了保证企业会计信息的真实性、完整性和透明度,为投资者、债权人、股东和其他相关利益者提供准确的财务信息,以便作出决策和评价企业财务状况的依据。

下面是企业会计准则中英版的主要内容。

第一章:总则这一章主要介绍了企业会计准则的基本原则和适用范围。

企业会计准则的基本原则包括真实性、公允性、连续性、谨慎性和稳定性。

它还规定了企业会计准则适用的范围,包括各类企业和各种经济业务的会计核算和财务报告。

第二章:会计要素和计量这一章主要介绍了企业会计中的基本要素和计量方法。

基本要素包括资产、负债、所有者权益、收入和费用。

计量方法包括历史成本法、公允价值法和现值法等。

这一章还对企业会计中的会计准则和计量方法进行了具体的解释和说明。

第三章:会计准则和政策这一章主要介绍了企业会计中的准则和政策。

准则是指会计核算和财务报告的基本规则和规范,包括会计制度、会计政策和会计方法等。

政策是指企业根据实际情况和需要所采用的会计操作方法和处理方式。

这一章还对企业在会计核算和财务报告中应遵循的规定和要求进行了详细的说明。

第四章:会计核算和财务报告这一章主要介绍了企业在会计核算和财务报告中的具体内容和要求。

它包括会计凭证和原始凭证的管理、会计科目和账簿的设立、会计期间和会计年度的确定、财务报表和报表分析等。

这一章还对企业在会计核算和财务报告中应遵循的原则和规定进行了详细的说明。

第五章:财务预测与决策这一章主要介绍了企业在财务预测和决策中所应遵循的原则和方法。

它包括财务预测和决策的基本概念和过程、预测模型和方法、风险评估和控制等。

这一章还对企业在财务预测和决策中所需要的信息和数据进行了详细的说明。

第六章:监管和合规这一章主要介绍了企业会计中的监管和合规事项。

它包括会计监管的基本原则和机构、会计审计的要求和程序、会计内部控制的建立和运作等。

这一章还对企业在会计监管和合规中所需要履行的责任和义务进行了详细的说明。

财务报表词汇-中英对照

. Total current liabilities 非流动负债: Non-current liabilities: 长期借款 Long-term loans 应付债券 Bonds payable 其中:优先股 Incl.: Preferred stock 永续债 Perpetual capital securities 长期应付款 Long-term payables 长期应付职工薪酬 Long-term payroll payable 专项应付款 Special accounts payable 预计负债 Estimated liabilities 递延收益 Deferred income 递延所得税负债 Deferred income tax liabilities 其他非流动负债 Other non-current liabilities 非流动负债合计 Total non-current liabilities 负债合计 Total liabilities 所有者权益: Owner's equity: 股本 Capital stock 其他权益工具 Other equity instruments 其中:优先股 Incl.: Preferred stock 永续债 Perpetual capital securities 资本公积 Capital reserve 减:库存股 Less: Treasury share 其他综合收益 Other comprehensive income 专项储备 Special reserve 盈余公积 Surplus reserve 一般风险准备 General risk preparation 未分配利润 . 292,465,187.40 254,438,787.61 17,969,331.07 17,969,331.07 1,062,696.58 1,248,514.49 63,391,195.82 63,889,889.82 644,603,890.25 644,603,890.25 499,983,108.00 500,481,802.00 836,879,016.94 765,543,346.68 6,378,937.32 7,319,437.32 6,378,937.32 6,269,437.32 1,050,000.00

新会计准则下中英文对照财务报表

1. 出售、处置部门或被投资单位所得收益 2. 自然灾害发生的损失 3. 会计政策变更增加(或减少)利润总额 4. 会计估计变更增加(或减少)利润总额 5. 债务重组损失 6. 其他

ITEMS Income from sale of invst. units Less from natural disaster Profit from changes in policy Profit from accounting budget Less from liablities rebuilt Others 复核: 制表:

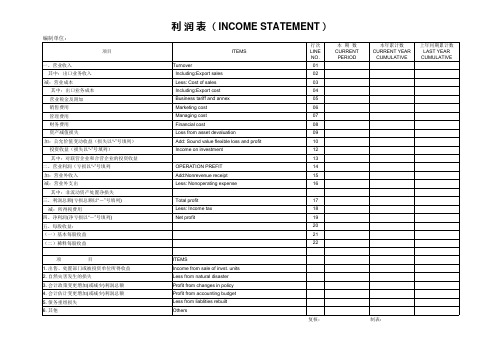

利 润 表 (INCOME STATEMENT)

编制单位:

项目 一、营业收入 其中:出口业务收入 减:营业成本 其中:出口业务成本 营业税金及附加 销售费用 管理费用 财务费用 资产减值损失 加:公允价值变动收益(损失以“-”号填列) 投资收益(损失以“-”号填列) 其中:对联营企业和合营企业的投资收益 二、营业利润(亏损以“-”号填列 加:营业外收入 减:营业外支出 其中:非流动资产处置净损失 三、利润总额(亏损总额以“-”号填列) 减:所得税费用 四、净利润(净亏损以“-”号填列) 五、每股收益: (一)基本每股收益 (二)稀释每股收益 项 目 Total profit Less: Income tax Net profit 17 18 19 20 21 22 OPERATION PREFIT Add:Nonrevenue receipt Less: Nonoperating expense Turnover Including:Export sales Less: Cost of sales Including:Export cost Business tariff and annex Marketing cost Managing cost Financial cost Loss from asset devaluation Add: Sound value flexible loss and profit Income on investment ITEMS 行次 LINE NO. 01 02 03 04 05 06 07 08 09 10 12 13 14 15 16 本 期 数 CURRENT PERIOD 本年累计数E 上年同期累计数 LAST YEAR CUMULATIVE

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

ChapterIGeneralProvisions

第一章 总则

Article1: These Standards areformulatedin accordancewiththeAccountingStandards for Enterprises- Basic Standardsforthe purposeofregulating thepreparationandpresentationof consolidatedfinancial statements.

第三条合并财务报表至少应当包括下列组成部分:

(1)The consolidated balancesheet;

(一)合并资产负债表;

(2)The consolidatedprofitstatement;

(二)合并利润表;

(3) The consolidated cash flow statement;

第一条为了规范合并财务报表的编制和列报,‘consolidatedfinancial statements’ are structuralreports about thefinancial status,businessperformances andcash flowsofthe enterprise groupformulated byparentcompaniesand subsidiarycompanies.

(五)附注。

Article 4: parentcompany should prepare consolidatedfinancial statements.

第四条 母公司应当编制合并财务报表。

Article5: foreigncurrencyfinancial statement translationshallbesubjectto the AccountingStandardforBusinessEnterprises No.19-Foreign Currency Translation andtheAccounting Standardsfor Enterprises No. 31- CashFlowStatements.

Subsidiary companiesmean whicharecontrolled by their parentcompany.

子公司,是指被母公司控制的企业。

Article3: Theconsolidated financial statementsshall at leastcomprisethe following parts:

第二条 合并财务报表,是指反映母公司和其全部子公司形成的企业集团整体财务状况、经营成果和现金流量的财务报表。

Parent companymeans thecompanyhas oneormoresubsidiary companies (ormain body).

母公司,是指有一个或一个以上子公司的企业(或主体,下同)。

企业会计准则第号——合并财务报表-中英对照

———————————————————————————————— 作者:

———————————————————————————————— 日期:

ﻩ

AccountingStandardfor Business EnterprisesNo. 33 - Consolidatedfinancial statements

第五条外币财务报表折算,适用《企业会计准则第19号——外币折算》和《企业会计准则第31号——现金流量表》。

Chapter IIConsolidated Scope

第二章合并范围

Article6:thescope ofconsolidatedfinancialstatementsshall be confirmed baseon the control.

(三)合并现金流量表;

(4)The consolidatedstatement of changesintheowner’sequities(or shareholder’sequities,the same below); and

(四)合并所有者权益(或股东权益,下同)变动表;

(5)Thenotes.

第七条母公司直接或通过子公司间接拥有被投资单位半数以上的表决权,表明母公司能够控制被投资单位,应当将该被投资单位认定为子公司,纳入合并财务报表的合并范围。但是,有证据表明母公司不能控制被投资单位的除外。

Article 8: parent enterprises having less thanhalfof votingrights ofinvested enterprises,which meetone ofthe followingconditions,shallbe deemed thatparententerprisecan control invested enterprises.The investedcompanyshallbedetermined its subsidiarywithintheconsolidatedscope. However, exceptfortheinvestedcompany whichcan’tbe provedtowithoutcontrolled by parent enterprise:

控制,是指一个企业能够决定另一个企业的财务和经营政策,并能据以从另一个企业的经营活动中获取利益的权力。

Article7:parent enterpriseshavemorethan halfof voting rightsof invested enterprises directly orbysubsidiaries.Parententerprisesare able to controltheinvested company, so theinvestedcompany shallbedetermined its subsidiarywithin the consolidated scope.However, except for theinvested company whichcan’t beproved to withoutcontrolledby parent enterprise.

第六条合并财务报表的合并范围应当以控制为基础予以确定。

Controlmeans an enterprise candecide thefinancialandmanage policyofanother enterpriseandhaveauthoritytoearnthe benefitfrom another enterprise.