债券市场分析与策略第版答案完整版

债券投资理论与实务复习题目与答案(附有重点知识整理)

第三章债券投资理论与实务复习题目与答案(一)单项选择题1.现代大多数公司的债券都具有“赎回”的特性,或者说它们的债券契约中包含赎回条款。

那么债券的发行公司常常在(A)的情况下,在债券未到期以前赎回一部分在外流通的债券。

债券被赎回的原因很明确,当利率下降或者信用品质上升时,新债券可以以更低的利率发行。

A.发行在外的债券的票面利率较高,当前市场利率较低B.发行在外的债券的票面利率较低,当前市场利率较高C.发行在外的债券的票面利率较高,当前市场利率较高D.发行在外的债券的票面利率较低,当前市场利率较低2.根据债券定价原理,债券的价格与债券的收益率具有( B )的关系。

A.当债券价格上升时,债券的收益率上升B.当债券价格上升时,债券的收益率下降C.当债券价格上升时,债券的收益率不变D.二者没有相关关系3.中期债券的偿还期在( B)。

A.1年以上、5年以下B.1年以上、10年以下C.半年以上、1年以下D.1年以上、1年半以下证券组合的价值与应得现值之差叫做( C )。

A.安全净收益B.最小目标值C.现金安全边际D.最小净收益安全边际(margin of safety),也可译作安全幅度,是指盈亏临界点以上的销售量,也就是现有销售量超过盈亏临界点销售量的差额。

5.两种换值的债券价格已经调整的时期叫做( B )时期。

4.债券组合管理是管理债券的一种综合方式,一般由消极管理、积极管理两部分组成。

消极管理策略是债券组合管理者不再积极寻求交易的可能性而企图战胜市场的一种策略,其基本假设是:债券市场是半强型有效市场。

主要包括如下策略:1、免疫策略:管理者选择久期等于他们负债(现金外流)的到期期限的证券组合,利用价格风险和再投资率风险互相抵消的特点,保证管理者不受损失。

2、现金流搭配策略:是一种特殊类型的免疫策略。

债券组合的管理者需要建立一个现金流用于支付每一个到期的负债现金流的专用证券组合。

3、指数化策略:管理者选定一个债券指数做依据,然后追踪指数构造证券组合。

债券市场分析与策略课后答案

债券市场分析与策略课后答案债券市场分析与策略课后答案第一部分:债券市场概述1. 什么是债券?答:债券是一种固定收益证券,指的是发行人向投资者发行债务证券,承诺在一定期间里按照约定的利率向投资者支付利息,并在到期日向投资者支付本金和最后一期利息。

投资者购买债券即为给发行人借款,债券的利率也称为债券收益率。

2. 债券市场的类型有哪些?答:债券市场的类型可以分为一级市场和二级市场。

一级市场也称为新股发行市场,是指债券发行时通过证券公司向广大投资者公开发行的场所。

二级市场也称为交易市场,是指投资者之间在证券交易所进行交易的场所。

3. 债券市场的功能有哪些?答:债券市场的主要功能包括为企业融资、为投资者提供固定收益投资机会、为政府调控经济提供手段等。

第二部分:债券风险与收益1. 债券风险可以分为哪些?答:债券风险可以分为违约风险、利率风险、市场风险和通胀风险。

2. 债券收益有哪些?答:债券收益可以分为票面利率收益和资本利得收益。

票面利率收益即为债券的利率收益,资本利得收益是指在债券购买时市场利率高于债券的票面利率,到期时债券价格上涨后所获得的溢价收益。

第三部分:债券分析与投资1. 什么是债券评级?答:债券评级是一种专业机构对债券信用风险的评估,并对债券进行等级标记,以提供投资者参考。

目前国内主要的债券评级机构有中诚信国际、联合信用评估等。

2. 债券分析的方法有哪些?答:常见的债券分析方法包括基本面分析、技术分析和宏观经济分析。

基本面分析着重考虑发行人的财务状况、经营状况和行业发展等情况。

技术分析主要从股票、期货市场的技术分析方法引入,对债券市场的交易趋势和价格进行分析。

宏观经济分析是从宏观环境中的经济因素对债券市场的影响进行分析。

3. 债券投资的策略有哪些?答:债券投资的策略可以从投资期限、风险偏好等方面进行考虑,包括买入看涨期权、减少风险并提高收益、购买高评级债券等策略。

常用的策略包括买入长期低风险债券、多元化配置固定收益投资品种等。

《债券市场:分析与策略》记录

《债券市场:分析与策略》阅读记录1. 内容概述在阅读《债券市场:分析与策略》这本书的过程中,我对债券市场有了更深入的了解。

该书首先介绍了债券市场的基本概念、运作机制和主要参与者。

详细分析了全球债券市场的历史演变、当前发展趋势以及影响市场变化的各种因素。

书中还深入探讨了债券市场的投资策略、风险管理以及相关的金融工具和衍生产品。

本书内容丰富,涵盖了债券市场的多个方面,有助于读者全面了解并深化对债券市场的认识。

通过阅读本书,我了解到了债券市场的复杂性以及其作为一个重要金融市场的地位。

书中分析了市场内的多种因素和相互之间的关系,如经济状况、政策利率、通胀情况等,这些因素都会对债券市场产生影响。

书中还对不同类型的债券(如政府债券、公司债券、高收益债券等)进行了详细的介绍和分析,使读者能够了解不同类型债券的风险和收益特点。

书中还特别强调了投资策略和风险管理的重要性,作者详细介绍了如何根据市场状况和个人投资目标制定合适的投资策略,以及如何有效地管理投资风险。

书中还介绍了相关的金融工具和衍生产品,如债券期货、债券期权等,这些工具和产品在债券市场中的作用以及如何进行交易。

这些内容让我对债券市场有了更加全面和深入的了解。

《债券市场:分析与策略》是一本非常有价值的书籍,为我提供了宝贵的知识和见解。

1.1 背景介绍债券市场是金融市场的重要组成部分,为企业、政府和个人提供融资渠道。

债券市场的稳定与发展对于整个经济的运行具有重要意义,本章节将对债券市场的背景进行简要介绍,包括债券的定义、类型以及债券市场的发展历程等。

债券是一种金融工具,代表发行者(债务人)向持有者(债权人)借款的书面承诺。

债券的发行人可以是企业、政府、金融机构等,而持有者则是投资者、金融机构等。

债券的发行价格与面值之间的差额即为债券的利息,债券持有人在债券到期时有权收回本金并获得利息收益。

根据发行主体的不同,债券可以分为政府债券、企业债券和金融债券等。

政府债券通常由国家政府发行,具有最高的信用等级,被称为“金边债券”。

证劵投资习题+参考答案

证劵投资习题+参考答案一、单选题(共52题,每题1分,共52分)1.场外交易市场的功能不包括()。

A、逐步向场内市场功能靠拢B、为不能在证券交易所上市的证券提供流通转让的场所C、提供风险分层的金融资产管理渠道D、拓展融资渠道,改善中小企业融资环境正确答案:A2.按照发行流通性质,可以将金融市场划分为()和()。

A、债权市场权益市场B、一级市场二级市场C、货币市场资本市场D、证券市场非证券金融市场正确答案:B3.下列关于债券的特征说法正确的是( )。

A、债务人必须按期向债权人支付利息和偿还本金B、永续债的存在说明偿还性不是债券的一般特性C、债券的收益随发行者经营收益的变动而变动D、具有高度流动性的债券反而不安全正确答案:A答案解析:考查债券的特征。

债券的特征有:偿还性、流动性、安全性、收益性。

偿还性是指债券有规定的偿还期限,债务人必须按期向债权人支付利息和偿还本金。

永续债券只是债券中极少的部分,不能因此否定债券具有偿还性的一般特征。

债券的安全性是指债券持有人的收益相对稳定,不随发行者经营收益的变动而变动,并可按期收回本金。

一般来说,具有高度流动性的债券同时也是较安全的,因为它不仅可以迅速地转换为货币,而且可以按一个较稳定的价格转换。

4.如果发行的证券化产品属于债券,发行前必须经过()进行信用评级。

A、投资人B、信用增级机构C、信用评级机构D、承销人正确答案:C5.引起股票价格变动的直接原因是( ) 。

A、流动性挤压B、政治因素C、公司经营状况的变化D、买卖双方力量强弱的转换正确答案:D答案解析:考查引起股票价格变动的直接原因。

6.根据《证券投资基金法》的规定,我国基金资产估值的责任人是( )。

A、基金持有人B、基金管理人C、基金托管人D、基金投资者正确答案:B答案解析:考查基金资产估值的责任人,基金托管人对基金管理人的估值负有复核义务责任。

7.( )是指依据基金合同设立的一类基金,在我国,是依据基金管理人、基金托管人之间所签署的基金合同设立,基金投资者购买基金份额后成为基金持有人,依法享受权利并承担义务。

债券市场分析与策略第7版答案3.

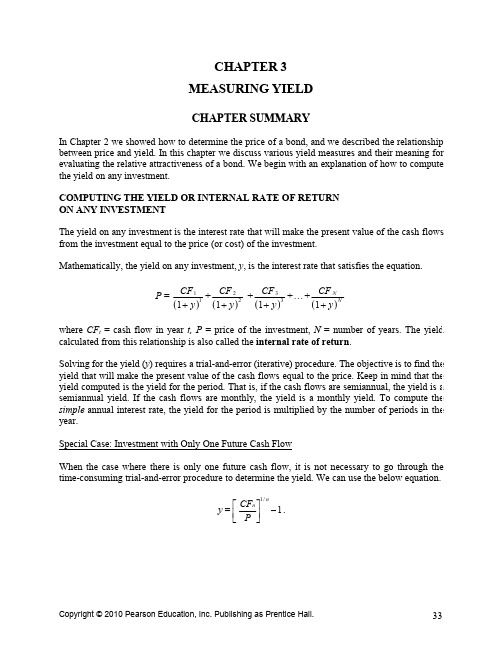

CHAPTER 3MEASURING YIELD CHAPTER SUMMARYIn Chapter 2we showed how to determine the price of a bond,and we described the relationship between price and yield.In this chapter we discuss various yield measures and their meaning for evaluating the relative attractiveness of a bond.We begin with an explanation of how to compute the yield on any PUTING THE YIELD OR INTERNAL RATE OF RETURN ON ANY INVESTMENT The yield on any investment is the interest rate that will make the present value of the cash flows from the investment equal to the price (or cost)of the investment.Mathematically,the yield on any investment,y ,is the interest rate that satisfies the equation.P =()()()()1231231111++++N N CF CF CF CF + + + . . .+ y y y y where CF t =cash flow in year t,P =price of the investment,N =number of years.The yield calculated from this relationship is also called the internal rate of return .Solving for the yield (y )requires a trial-and-error (iterative)procedure.The objective is to find the yield that will make the present value of the cash flows equal to the price.Keep in mind that the yield computed is the yield for the period.That is,if the cash flows are semiannual,the yield is a semiannual yield.If the cash flows are monthly,the yield is a monthly yield.To compute the simple annual interest rate,the yield for the period is multiplied by the number of periods in the year.Special Case:Investment with Only One Future Cash Flow When the case where there is only one future cash flow,it is not necessary to go through the time-consuming trial-and-error procedure to determine the yield.We can use the below equation.1 = /1-⎥⎦⎤⎢⎣⎡P CF y n n.Annualizing Yields To obtain an effective annual yield associated with a periodic interest rate,the following formula is used:effective annual yield =(1+periodic interest rate)m –1where m is the frequency of payments per year.To illustrate,if interest is paid quarterly and the periodic interest rate is 8%/4=2%),then we have:the effective annual yield =(1.02)4–1=1.0824–1=0.0824or 8.24%.We can also determine the periodic interest rate that will produce a given annual interest rate by solving the effective annual yield equation for the periodic interest rate.Solving,we find that:periodic interest rate =(1+effective annual yield)1/m –1.To illustrate,if the periodic quarterly interest rate that would produce an effective annual yield of 12%,then we have:periodic interest rate =(1.12)1/4–1=1.0287–1=0.0287or 2.87%.CONVENTIONAL YIELD MEASURESThere are several bond yield measures commonly quoted by dealers and used by portfolio managers.These are described below.Current YieldCurrent yield relates the annual coupon interest to the market price.The formula for the current yield is:current yield =annual dollar coupon interest /price.The current yield calculation takes into account only the coupon interest and no other source of return that will affect an investor’s yield.The time value of money is also ignored.Yield to Maturity The yield to maturity is the interest rate that will make the present value of the cash flows equal to the price (or initial investment).For a semiannual pay bond,the yield to maturity is found by first computing the periodic interest rate,y ,which satisfies the relationship:P =()()()()()12311111+++++n n C CC CM + + + . . .+ + y y y y y where P =price of the bond,C =semiannual coupon interest (in dollars),M =maturity value (in dollars),and n =number of periods (number of years x 2).For a semiannual pay bond,doubling the periodic interest rate or discount rate (y )gives the yield to maturity,which understates the effective annual yield.The yield to maturity computed on the basis of this market convention is called the bond-equivalent yield .It is much easier to compute the yield to maturity for a zero-coupon bond because we can use:1 = /1-⎥⎦⎤⎢⎣⎡P M y n .The yield-to-maturity calculation takes into account not only the current coupon income but also any capital gain or loss that the investor will realize by holding the bond to maturity.In addition,the yield to maturity considers the timing of the cash flows.Yield To Call The price at which the bond may be called is referred to as the call price .For some issues,the call price is the same regardless of when the issue is called.For other callable issues,the call price depends on when the issue is called.That is,there is a call schedule that specifies a call price for each call date.For callable issues,the practice has been to calculate a yield to call as well as a yield to maturity.The yield to call assumes that the issuer will call the bond at some assumed call date and the call price is then the call price specified in the call schedule.Typically,investors calculate a yield to first call or yield to next call,a yield to first par call,and yield to refunding.Mathematically,the yield to call can be expressed as follows:P =()()()()()123*11111+++++n*n*C C C CM + + + . . .+ + y y y y y where M *=call price (in dollars)and n *=number of periods until the assumed call date (number of years times 2).For a semiannual pay bond,doubling the periodic interest rate (y )gives the yield to call on a bond-equivalent basis.Yield To Put If an issue is putable,it means that the bondholder can force the issuer to buy the issue at a specified price.As with a callable issue,a putable issue can have a put schedule.The schedule specifies when the issue can be put and the price,called the put price.When an issue is putable,a yield to put is calculated.The yield to put is the interest rate that makes the present value of the cash flows to the assumed put date plus the put price on that date as set forth in the put schedule equal to the bond’s price.The formula is the same as for the yield to call,but M *is now defined as the put price and n *is the number of periods until the assumed put date.The procedure is the same as calculating yield to maturity and yield to call.Yield To WorstA practice in the industry is for an investor to calculate the yield to maturity,the yield to every possible call date,and the yield to every possible put date.The minimum of all of these yields is called the yield to worst.Cash Flow YieldSome fixed income securities involve cash flows that include interest plus principal repayment. Such securities are called amortizing securities.For amortizing securities,the cash flow each period consists of three components:(i)coupon interest,(ii)scheduled principal repayment,and (iii)prepayments.For amortizing securities,market participants calculate a cash flow yield.It is the interest rate that will make the present value of the projected cash flows equal to the market price.Yield(Internal Rate of Return)for a PortfolioThe yield for a portfolio of bonds is not simply the average or weighted average of the yield to maturity of the individual bond issues in the portfolio.It is computed by determining the cash flows for the portfolio and determining the interest rate that will make the present value of the cash flows equal to the market value of the portfolio.Yield Spread Measures for Floating-Rate SecuritiesThe coupon rate for a floating-rate security changes periodically based on the coupon reset formula.This formula consists of the reference rate and the quoted margin.Since the future value for the reference rate is unknown,it is not possible to determine the cash flows.This means that a yield to maturity cannot be calculated.Instead,there are several conventional measures used as margin or spread measures cited by market participants for floaters.These include spread for life (or simple margin),adjusted simple margin,adjusted total margin,and discount margin.The most popular of these measures is discount margin.This measure estimates the average margin over the reference rate that the investor can expect to earn over the life of the security. POTENTIAL SOURCES OF A BOND’S DOLLAR RETURNAn investor who purchases a bond can expect to receive a dollar return from one or more of these sources:(i)the periodic coupon interest payments made by the issuer,(ii)any capital gain(or capital loss—negative dollar return)when the bond matures,is called,or is sold,and(iii)interest income generated from reinvestment of the periodic cash flowsAny measure of a bond’s potential yield should take into consideration each of these three potential sources of return.The current yield considers only the coupon interest payments.No consideration is given to any capital gain(or loss)or interest on interest.The yield to maturity takes into account coupon interest and any capital gain(or loss).It also considers the interest-on-interest component.Implicit in the yield-to-maturity computation is the assumptionthat the coupon payments can be reinvested at the computed yield to maturity.The yield to call also takes into account all three potential sources of return.In this case,the assumption is that the coupon payments can be reinvested at the yield to call.Therefore,the yield-to-call measure suffers from the same drawback as the yield to maturity in that it assumes coupon interest payments are reinvested at the computed yield to call.Also,it presupposes that the issuer will call the bond on some assumed call date.The cash flow yield also takes into consideration all three sources as is the case with yield to maturity,but it makes two additional assumptions.First,it assumes that the periodic principal repayments are reinvested at the computed cash flow yield.Second,it assumes that the prepayments projected to obtain the cash flows are actually realized.Determining the Interest-On-Interest Dollar Return The interest-on-interest component can represent a substantial portion of a bond’s potential return.The coupon interest plus interest on interest can be found by using the following equation:()11n r C r ⎡⎤+-⎢⎥⎣⎦where r denote the semiannual reinvestment rate.The total dollar amount of coupon interest is found by multiplying the semiannual coupon interest by the number of periods:total coupon interest =nC The interest-on-interest component is then the difference between the coupon interest plus interest on interest and the total dollar coupon interest,as expressed by the formula interest on interest =()11n r C nC r ⎡⎤+--⎢⎥⎣⎦.Yield To Maturity and Reinvestment Risk The investor will realize the yield to maturity at the time of purchase only if the bond is held to maturity and the coupon payments can be reinvested at the computed yield to maturity.The risk that the investor faces is that future reinvestment rates will be less than the yield to maturity at the time the bond is purchased.This risk is referred to as reinvestment risk.There are two characteristics of a bond that determine the importance of the interest-on-interest component and therefore the degree of reinvestment risk:maturity and coupon.For a given yield to maturity and a given coupon rate,the longer the maturity,the more dependent the bond’s total dollar return is on the interest-on-interest component in order to realize the yield to maturity at the time of purchase.In other words,the longer the maturity,the greater the reinvestment risk.For a given maturity and a given yield to maturity,higher coupon rates will make the bond’s total dollar return more dependent on the reinvestment of the coupon payments in order to produce the yield to maturity anticipated at the time of purchase.Cash Flow Yield and Reinvestment RiskFor amortizing securities,reinvestment risk is even greater than for nonamortizing securities.The reason is that the investor must now reinvest the periodic principal repayments in addition to the periodic coupon interest payments.TOTAL RETURNIn the preceding section we explain that the yield to maturity is a promised yield.At the time of purchase an investor is promised a yield,as measured by the yield to maturity,if both of the following conditions are satisfied:(i)the bond is held to maturity and(ii)all coupon interest payments are reinvested at the yield to maturity.The total return is a measure of yield that incorporates an explicit assumption about the reinvestment rate.The yield-to-call measure is subject to the same problems as the yield to maturity.First,it assumes that the bond will be held until the first call date.Second,it assumes that the coupon interest payments will be reinvested at the yield to call.Computing the Total Return for a BondThe idea underlying total return is simple.The objective is first to compute the total future dollars that will result from investing in a bond assuming a particular reinvestment rate.The total return is then computed as the interest rate that will make the initial investment in the bond grow to the computed total future dollars.APPLICATIONS OF THE TOTAL RETURN(HORIZON ANALYSIS)Using total return to assess performance over some investment horizon is called horizon analysis. When a total return is calculated over an investment horizon,it is referred to as a horizon return. An often-cited objection to the total return measure is that it requires the portfolio manager to formulate assumptions about reinvestment rates and future yields as well as to think in terms of an investment horizon.CALCULATING YIELD CHANGESThe absolute yield change(or absolute rate change)is measured in basis points and is the absolute value of the difference between the two yields as given byabsolute yield change=│initial yield–new yield│X100.The percentage change is computed as the natural logarithm of the ratio of the change in yield as shown bypercentage change yield=100X ln(new yield/initial yield).ANSWERS TO QUESTIONS FOR CHAPTER 3(Questions are in bold print followed by answers.)1.A debt obligation offers the following payments:Years from Now Cash Flow to Investor 1$2,0002$2,0003$2,5004$4,000Suppose that the price of this debt obligation is $7,704.What is the yield or internal rate of return offered by this debt obligation?The yield on any investment is the interest rate that will make the present value of the cash flows from the investment equal to the price (or cost)of the investment.Mathematically,the yield on any investment,y ,is the interest rate that satisfies the equation:P =()()()()1231231111N N CF CF CF CF + + + . . .+ + y + y + y + y where CF t =cash flow in year t ,P =price of the investment,and N =number of years.The yield calculated from this relationship is also called the internal rate of return.To solve for the yield (y )without the use of an advanced financial tool,we can use a trial-and-error (iterative)procedure.The objective is to find the interest rate that will make the present value of the cash flows equal to the price.To compute the yield for our problem,different interest rates must be tried until the present value of the cash flows is equal to $7,704(the price of the financial instrument).Trying an annual interest rate of 10%gives the following present value:Years from Now Promised Annual Payments (Cash Flow to Investor)Present Value of Cash Flow at 10%1$2,000$1,818.182$2,000$1,652.893$2,500$1,878.294$4,000$2,732.05Present value =$8,081.41Because the present value of $8,081.41computed using a 10%interest rate exceeds the price of $7,704,a higher interest rate must be used,to reduce the present value.Trying an annual interest rate of 13%gives the following present value:Years from Now Promised Annual Payments (Cash Flow to Investor)Present Value of Cash Flow at 13%1$2,000$1,769.912$2,000$1,566.293$2,500$1,732.634$4,000$2,453.27Present value =$7,522.10Because the present value of $7,522.10computed using a 13%interest rate is below the price of $7,704,a lower interest rate must be used,to reduce the present value.Thus,to increase the present value,a lower interest rate must be tried.Trying an annual interest rate of 12%gives the following present value:Years from NowPromised Annual Payments (Cash Flow to Investor)Present Value of Cash Flow at 12%1$2,000$1,785.712$2,000$1,594.393$2,500$1,779.454$4,000$2,542.07Present value =$7,701.62Using 12%,the present value of the cash flow is $7,701.62,which is almost equal to the price of the financial instrument of $7,704.Therefore,the yield is close to 12%.The precise yield using Excel or a financial calculator is 11.987%.Although the formula for the yield is based on annual cash flows,it can be generalized to any number of periodic payments in a year.The generalized formula for determining the yield is ) + (1=t t1=t y CF P N where CF t =cash flow in period t ,and n =number of periods.Keep in mind that the yield computed is the yield for the period.That is,if the cash flows are semiannual,the yield is a semiannual yield.If the cash flows are monthly,the yield is a monthly yield.To compute the simple annual interest rate,the yield for the period is multiplied by the number of periods in the year.2.What is the effective annual yield if the semiannual periodic interest rate is 4.3%?To obtain an effective annual yield associated with a periodic interest rate,the following formula is used:effective annual yield =(1+periodic interest rate)m –1where m is the frequency of payments per year.In our problem,the periodic interest rate is a semiannual rate of 4.3%and the frequency of payments is twice per year.Inserting these numbers,we have:effective annual yield =(1.043)2–1=1.087849–1=0.087849or about 8.785%.3.What is the yield to maturity of a bond?The yield to maturity is the interest rate that will make the present value of the cash flows equal to the price (or initial investment).For a semiannual pay bond,the yield to maturity is found by first computing the periodic interest rate,y ,which satisfies the relationship:P =()()()()()2311111+++++n n C C C C M + + + . . .+ + y y y y y where P =price of the bond,C =semiannua l coupon interest (in dollars),M =maturity value (in dollars),and n =number of periods (number of years times 2).It is much easier to compute the yield to maturity for a zero-coupon bond because we can use:1 = /1-⎥⎦⎤⎢⎣⎡P M y n.The yield-to-maturity calculation takes into account not only the current coupon income but also any capital gain or loss that the investor will realize by holding the bond to maturity.In addition,the yield to maturity considers the timing of the cash flows.4.What is the yield to maturity calculated on a bond-equivalent basis?For a semiannual pay bond,doubling the periodic interest rate or discount rate (y )gives the yield to maturity,which understates the effective annual yield.The yield to maturity computed on the basis of this market convention is called the bond-equivalent yield.5.Answer the below questions.(a)Show the cash flows for the following four bonds,each of which has a par value of$1,000 and pays interest semiannually.Bond Coupon Rate(%)Number of Years to Maturity PriceW75$884.20X87$948.90Y94$967.70Z010$456.39Bond W has cash flows of0.07($1,000)/2=$35for semiannual periods from periods1to10.At the end of period10,Bond W also pays back the par of$1,000for a total payment of$1,000+$35 =$1,035.Bond X has cash flows of0.08($1,000)/2=$40for semiannual periods from periods1to14.At the end of period14,Bond X also pays back the par of$1,000for a total payment of$1,000+$40 =$1,040.Bond Y has cash flows of0.09($1,000)/2=$45for semiannual periods from periods1to8.At the end of period8,Bond Y also pays back the par of$1,000for a total payment of$1,000+$45= $1,045.Bond Z has cash flows of0($1,000)/2=$0for semiannual periods from periods1to20.At the end of period20,Bond Z also pays back the$1,000for a total payment of$1,000+$0=$1,000.Below we show these cash flows in table format.PeriodCash Flow for Bond W Cash Flow for Bond X Cash Flow for Bond Y Cash Flow for Bond Z 1$35$40$45$02$35$40$45$03$35$40$45$04$35$40$45$05$35$40$45$06$35$40$45$07$35$40$45$08$35$40$1,045$09$35$40$010$1,035$40$011$40$012$40$013$40$014$1,040$015$016$017$018$019$020$1,000(b)Calculate the yield to maturity for the four bonds.The yield to maturity is computed in the same way as the internal rate of return;the cash flows are those that the investor would realize by holding the bond to maturity.For a semiannual pay bond,the yield to maturity is found by first computing the periodic interest rate,y ,which satisfies the relationship P =()()()()()2311111+++++n n C C C C M + + + . . .+ + y y y y y where P =price of the bond,C =semiannual coupon interest (in dollars),M =maturity value (in dollars),and n =number of periods (number of years times 2).For a semiannual pay bond,doubling the periodic interest rate or discount rate (y )gives the yield to maturity.However,annualizing the yield by doubling the periodic interest rate understates the effective annual yield.Despite this,the market convention is to compute the yield to maturity by doubling the periodic interest rate,y that satisfies our equation.The yield to maturity computed on the basis of this market convention is called the bond-equivalent yield.The computation of the yield to maturity requires a trial-and-error procedure.To illustrate the computation,we first look at bond W.The cash flows for this bond are ten coupon payments of$35every six months and the principal of$1,000to be paid in ten six-month periods from now.To get y using our equation given above,different interest rates must be tried until the present value of the cash flows is equal to the price.In doing this,we get the following yield to maturities for the four bonds.For bond W,we get a periodic interest rate real close to5%.This is seen below.Years fromNow Promised Annual Payments(Cash Flow to Investor)Present Valueof Cash Flow at5%1$35$33.332$35$31.753$35$30.234$35$28.795$35$27.426$35$26.127$35$24.878$35$23.689$35$22.5610$1,035$635.40Present value=$884.17Using5%,the present value of the cash flow is$884.17,which is almost equal to the price of the financial instrument of$884.20.Therefore,the periodic interest rate is close to5%.The precise yield using Excel or a financial calculator is4.99964%.Doubling the periodic interest rate of5% gives a yield to maturity of10%(doubling4.99964%gives9.99928%).For bond X,we get an interest rate real close to4.50%.Using this rate,the value of the cash flow is $951.59,which is almost equal to the price of the financial instrument of$948.90.Therefore,the yield is close to4.5%.The precise periodic interest rate using Excel or a financial calculator is 4.5271%.Doubling the periodic interest rate of4.5%gives a yield to maturity of9%(doubling 4.5271%gives9.0542%).For bond Y,we get an interest rate close to5%.Using this rate,the value of the cash flow is $967.68,which is almost equal to the price of the financial instrument of$967.70.Therefore,the yield is close to5%.The precise periodic interest rate using Excel or a financial calculator is 5.11078%.Doubling the periodic interest rate of5%gives a yield to maturity of10%(doubling 5.11083%gives10.2215%).For bond Z,we get an interest rate close to4%.Using this rate,the value of the cash flow is $456.39,which is equal to the price of the financial instrument of$456.39.Therefore,the yield is virtually4%.The precise periodic interest rate using Excel or a financial calculator is3.99965%. Doubling the periodic interest rate of4%gives a yield to maturity of8%(doubling3.99965% gives7.9993%).6.A portfolio manager is considering buying two bonds.Bond A matures in three years and has a coupon rate of10%payable semiannually.Bond B,of the same credit quality,matures in10years and has a coupon rate of12%payable semiannually.Both bonds are priced at par.(a)Suppose that the portfolio manager plans to hold the bond that is purchased for three years.Which would be the best bond for the portfolio manager to purchase?The shorter term bond will pay a lower coupon rate but it will likely cost less for a given market rate.Since the bonds are of equal risk in terms of credit quality(the maturity premium for the longer term bond should be greater),the question when comparing the two bond investments is: What investment will be expected to give the highest cash flow per dollar invested?In other words, which investment will be expected to give the highest effective annual rate of return?In general, holding the longer term bond should compensate the investor in the form of a maturity premium and a higher expected return.However,as seen in the discussion below,the actual realized return for either investment is not known with certainty.To begin with,an investor who purchases a bond can expect to receive a dollar return from(i)the periodic coupon interest payments made by the issuer;(ii)any capital gain(or capital loss—negative dollar return)when the bond matures,is called,or is sold;and,(iii)interest income generated from reinvestment of the periodic cash flows.The last component of the potential dollar return is referred to as reinvestment income.For a standard bond(our situation)that makes only coupon payments and no periodic principal payments prior to the maturity date,the interim cash flows are simply the coupon payments.Consequently,for such bonds the reinvestment income is simply interest earned from reinvesting the coupon interest payments.For these bonds,the third component of the potential source of dollar return is referred to as the interest-on-interest component.If we are going to compute a potential yield to make a decision,we should be aware of the fact that any measure of a bond’s potential yield should take into consideration each of the three components described above.The current yield considers only the coupon interest payments.No consideration is given to any capital gain(or loss)or interest on interest.The yield to maturity takes into account coupon interest and any capital gain(or loss).It also considers the interest-on-interest component.Additionally,implicit in the yield-to-maturity computation is the assumption that the coupon payments can be reinvested at the computed yield to maturity.The yield to maturity is a promised yield and will be realized only if the bond is held to maturity and the coupon interest payments are reinvested at the yield to maturity.If the bond is not held to maturity and the coupon payments are reinvested at the yield to maturity,then the actual yield realized by an investor can be greater than or less than the yield to maturity.Given the facts that(i)one bond,if bought,will not be held to maturity,and(ii)the coupon interest payments will be reinvested at an unknown rate,we cannot determine which bond might give the highest actual realized rate.Thus,we cannot compare them based upon this criterion.However,if the portfolio manager is risk inverse in the sense that she or he doesn’t want to buy a longer term bond,which will likely have more variability in its return,then the manager might prefer the shorter term bond(bond A)of three years.This bond also matures when the manager wants to cashin the bond.Thus,the manager would not have to worry about any potential capital loss in selling the longer term bond(bond B).The manager would know with certainty what the cash flows are.If these cash flows are spent when received,the manager would know exactly how much money could be spent at certain points in time.Finally,a manger can try to project the total return performance of a bond on the basis of the planned investment horizon and expectations concerning reinvestment rates and future market yields.This permits the portfolio manager to evaluate which of several potential bonds considered for acquisition will perform best over the planned investment horizon.As we just argued,this cannot be done using the yield to maturity as a measure of relative ing total return to assess performance over some investment horizon is called horizon analysis.When a total return is calculated over an investment horizon,it is referred to as a horizon return.The horizon analysis framework enables the portfolio manager to analyze the performance of a bond under different interest-rate scenarios for reinvestment rates and future market yields.Only by investigating multiple scenarios can the portfolio manager see how sensitive the bond’s performance will be to each scenario.This can help the manager choose between the two bond choices.(b)Suppose that the portfolio manager plans to hold the bond that is purchased for six years instead of three years.In this case,which would be the best bond for the portfolio manager to purchase?Similar to our discussion in part(a),we do not know which investment would give the highest actual realized return in six years when we consider reinvesting all cash flows.If the manager buys a three year bond,then there would be the additional uncertainty of now knowing what three-year bond rates would be in three years.The purchase of the ten-year bond would be held longer than previously(six years to three years)and render coupon payments for a six period that are known.If these cash flows are spent when received,the manager will know exactly how much money could be spent at certain points in time.Not knowing which bond investment would give the highest realized return,the portfolio manager would choose the bond that fits the firm’s goals in terms of maturity.(c)Suppose that the portfolio manager is managing the assets of a life insurance company that has issued a five-year guaranteed investment contract(GIC).The interest rate that the life insurance company has agreed to pay is9%on a semiannual basis.Which of the two bonds should the portfolio manager purchase to ensure that the GIC payments will be satisfied and that a profit will be generated by the life insurance company?The portfolio manager needs to generate a semiannual cash flow of9%semiannual basis for five years.Bond A will only lock in a10%cash flow per dollar invested for three years.However,bond B will lock in a12%cash flow per dollar invested for ten years.Thus,the portfolio manager would choose bond B and hopefully be able buy as many of these bonds as are needed to generate the cash flows required to meet the five-year guaranteed investment contract.。

(完整word版)债券市场分析与策略第7版答案2

CHAPTER 2PRICING OF BONDSCHAPTER SUMMARYThis chapter will focus on the time value of money and how to calculate the price of a bond. When pricing a bond it is necessary to estimate the expected cash flows and determine the appropriate yield at which to discount the expected cash flows. Among other aspects of a bond, we will look at the reasons why the price of a bond changesREVIEW OF TIME VALUE OF MONEYMoney has time value because of the opportunity to invest it at some interest rate.Future ValueThe future value of any sum of money invested today is:P n= P0(1+r)nwhere n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars), r = interest rate per period (in decimal form), and the expression (1+r)n represents the future value of $1 invested today for n periods at a compounding rate of r.When interest is paid more than one time per year, both the interest rate and the number of periods used to compute the future value must be adjusted as follows:r = annual interest rate / number of times interest paid per year, andn = number of times interest paid per year times number of years.The higher future value when interest is paid semiannually, as opposed to annually, reflects the greater opportunity for reinvesting the interest paid.Future Value of an Ordinary AnnuityWhen the same amount of money is invested periodically, it is referred to as an annuity. When the first investment occurs one period from now, it is referred to as an ordinary annuity.The equation for the future value of an ordinary annuity is:P n =()11⎡⎤+-⎢⎥⎢⎥⎣⎦nrArwhere A is the amount of the annuity (in dollars).Example of Future Value of an Ordinary Annuity Using Annual Interest:If A = $2,000,000, r = 0.08, and n = 15, then P n = ()11n r A r ⎡⎤+-⎢⎥⎣⎦→ P 15 = 08.01 17217.3 000,000,2$⎥⎦⎤⎢⎣⎡- = $2,000,000[27.152125] = $54,304.250.Because 15($2,000,000) = $30,000,000 of this future value represents the total dollar amount of annual interest payments made by the issuer and invested by the portfolio manager, the balance of $54,304,250 – $30,000,000 = $24,304,250 is the interest earned by reinvesting these annual interest payments.Example of Future Value of an Ordinary Annuity Using Semiannual Interest:Consider the same example, but now we assume semiannual interest payments.If A = $2,000,000 / 2 = $1,000,000, r = 0.08 / 2 = 0.04, n = 2(15) = 30, thenP n = ()11n r A r ⎡⎤+-⎢⎥⎢⎥⎣⎦→ P 30 = 04.01 )04. (1 000,000,1$ 30⎥⎦⎤⎢⎣⎡- = 04.01 2434.3 000,000,1$⎥⎦⎤⎢⎣⎡-=$1,000,000[56.085] = $56,085,000.The opportunity for more frequent reinvestment of interest payments received makes the interest earned of $26,085,000 from reinvesting the interest payments greater than the $24,304,250 interest earned when interest is paid only one time per year.Present ValueThe present value is the future value process in reverse. We have:For a given future value at a specified time in the future, the higher the interest rate (or discount rate), the lower the present value. For a given interest rate (discount rate), the further into the future that the future value will be received, then the lower its present value.Present Value of a Series of Future ValuesTo determine the present value of a series of future values, the present value of each future value must first be computed. Then these present values are added together to obtain the present value of the entire series of future values.Present Value of an Ordinary AnnuityWhen the same dollar amount of money is received each period or paid each year, the series is referred to as an annuity. When the first payment is received one period from now, the annuity is called an ordinary annuity. When the first payment is immediate, the annuity is called an annuity due.The present value of an ordinary annuity is:()111n r PV = A r ⎡⎤-⎢⎥+⎢⎥⎣⎦where A is the amount of the annuity (in dollars).The term in brackets is the present value of an ordinary annuity of $1 for n periods.Example of Present Value of an Ordinary Annuity Using Annual Interest:If A = $100, r = 0.09, and n = 8, then: ()111n r PV = A r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = ()811 1.09$100 0.09⎡⎤-⎢⎥⎢⎥⎣⎦=11 1.99256$100 0.09⎡⎤-⎢⎥⎢⎥⎣⎦ = 10.501867 $100 0.09-⎡⎤⎢⎥⎣⎦= $100[5.534811] = $553.48. Present Value When Payments Occur More Than Once Per YearIf the future value to be received occurs more than once per year, then the present value formula is modified so that (i) the annual interest rate is divided by the frequency per year, and (ii) the number of periods when the future value will be received is adjusted by multiplying the number of years by the frequency per year.PRICING A BONDDetermining the price of any financial instrument requires an estimate of (i) the expected cash flows, and (ii) the appropriate required yield. The required yield reflects the yield for financial instruments with comparable risk, or alternative investments.The cash flows for a bond that the issuer cannot retire prior to its stated maturity date consist of periodic coupon interest payments to the maturity date, and the par (or maturity) value at maturity.Computing the Value of a Bond: An Example:Consider a 20-year 10% coupon bond with a par value of $1,000 and a required yield of 11%. Given C = 0.1($1,000) / 2 = $50, n = 2(20) = 40 and r = 0.11 / 2 = 0.055, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = ()4011 1.055$50 0.055⎡⎤-⎢⎥⎢⎥⎣⎦ = 11 8.51332$50 0.055⎡⎤-⎢⎥⎢⎥⎣⎦ = 10.117463$50 0.055-⎡⎤⎢⎥⎣⎦=[] 046131.16 50$ = $802.31.The present value of the par or maturity value of $1,000 is: ()1n M r + =()40$1,000.055 1 =51331.8000,1$ = $117.46.The price of the bond (P) = present value coupon payments + present value maturity value = $802.31 + $117.46 = $919.77.Pricing Zero-Coupon BondsFor zero-coupon bonds, the investor realizes interest as the difference between the maturity value and the purchase price. The equation is:()1nM P r =+where M is the maturity value. Thus, the price of a zero-coupon bond is simply the present value of the maturity value.Zero-Coupon Bond ExampleConsider the price of a zero-coupon bond that matures 15 years from now, if the maturity value is $1,000 and the required yield is 9.4%. Given M = $1,000, r = 0.094 / 2 = 0.047, and n = 2(15) = 30,we have: ()1n M P r =+ =()30$1,0001.047 = 99644.3000,1$ = $252.12. Price-Yield RelationshipA fundamental property of a bond is that its price changes in the opposite direction from the change in the required yield. The reason is that the price of the bond is the present value of the cash flows.Relationship Between Coupon Rate, Required Yield, and PriceWhen yields in the marketplace rise above the coupon rate at a given point in time , the price of the bond falls so that an investor buying the bond can realizes capital appreciation. The appreciation represents a form of interest to a new investor to compensate for a coupon rate that is lower than the required yield. When a bond sells below its par value, it is said to be selling at a discount. A bond whose price is above its par value is said to be selling at a premium.Relationship Between Bond Price and Time if Interest Rates Are UnchangedFor a bond selling at par value, the coupon rate is equal to the required yield. As the bond moves closer to maturity, the bond will continue to sell at par value. Its price will remain constant as the bond moves toward the maturity date.The price of a bond will not remain constant for a bond selling at a premium or a discount. The discount bond increases in price as it approaches maturity, assuming that the required yield does not change. For a premium bond, the opposite occurs. For both bonds, the price will equal par value at the maturity date.Reasons for the Change in the Price of a BondThe price of a bond can change for three reasons: (i) there is a change in the required yield owing to changes in the credit quality of the issuer; (ii) there is a change in the price of the bond selling at a premium or a discount, without any change in the required yield, simply because the bond is moving toward maturity; or, (iii) there is a change in the required yield owing to a change in the yield on comparable bonds (i.e., a change in the yield required by the market).COMPLICATIONSThe framework for pricing a bond assumes the following: (i) the next coupon payment is exactly six months away; (ii) the cash flows are known; (iii) the appropriate required yield can be determined; and, (iv) one rate is used to discount all cash flows.Next Coupon Payment Due in Less than Six MonthsWhen an investor purchases a bond whose next coupon payment is due in less than six months, the accepted method for computing the price of the bond is as follows:where v = (days between settlement and next coupon) / (days in six-month period).Cash Flows May Not Be KnownFor most bonds, the cash flows are not known with certainty. This is because an issuer may call a bond before the stated maturity date.Determining the Appropriate Required YieldAll required yields are benchmarked off yields offered by Treasury securities. From there, we must still decompose the required yield for a bond into its component parts.One Discount Rate Applicable to All Cash FlowsA bond can be viewed as a package of zero-coupon bonds, in which case a unique discount rate should be used to determine the present value of each cash flow.PRICING FLOATING-RATE AND INVERSE-FLOATING-RATE SECURITIESThe cash flow is not known for either a floating-rate or an inverse-floating-rate security; it will depend on the reference rate in the future.Price of a FloaterThe coupon rate of a floating-rate security (or floater) is equal to a reference rate plus some spread or margin. The price of a floater depends on (i) the spread over the reference rate and (ii) any restrictions that may be imposed on the resetting of the coupon rate.Price of an Inverse FloaterIn general, an inverse floater is created from a fixed-rate security. The security from which the inverse floater is created is called the collateral. From the collateral two bonds are created: a floater and an inverse floater.The price of a floater depends on (i) the spread over the reference rate and (ii) any restrictions that may be imposed on the resetting of the coupon rate. For example, a floater may have a maximum coupon rate called a cap or a minimum coupon rate called a floor. The price of a floater will trade close to its par value as long as the spread above the reference rate that the market requires is unchanged, and neither the cap nor the floor is reached.The price of an inverse floater equals the collateral’s price minus the floater’s price.PRICE QUOTES AND ACCRUED INTERESTPrice QuotesA bond selling at par is quoted as 100, meaning 100% of its par value. A bond selling at a discount will be selling for less than 100; a bond selling at a premium will be selling for more than 100. Accrued InterestWhen an investor purchases a bond between coupon payments, the investor must compensate the seller of the bond for the coupon interest earned from the time of the last coupon payment to the settlement date of the bond. This amount is called accrued interest. For corporate and municipal bonds, accrued interest is based on a 360-day year, with each month having 30 days.The amount that the buyer pays the seller is the agreed-upon price plus accrued interest. This is often referred to as the full price or dirty price. The price of a bond without accrued interest is called the clean price. The exceptions are bonds that are in default. Such bonds are said to be quoted flat, that is, without accrued interest.ANSWERS TO QUESTIONS FOR CHAPTER 2(Questions are in bold print followed by answers.)1. A pension fund manager invests $10 million in a debt obligation that promises to pay 7.3% per year for four years. What is the future value of the $10 million?To determine the future value of any sum of money invested today, we can use the future value equation, which is: P n= P0 (1 + r)n where n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars) and r = interest rate per period (in decimal form). Inserting in our values, we have: P4 = $10,000,000(1.073)4 = $10,000,000(1.325558466) = $13,255,584.66.2. Suppose that a life insurance company has guaranteed a payment of $14 million to a pension fund 4.5 years from now. If the life insurance company receives a premium of $10.4 million from the pension fund and can invest the entire premium for 4.5 years at an annual interest rate of 6.25%, will it have sufficient funds from this investment to meet the $14 million obligation?To determine the future value of any sum of money invested today, we can use the future value equation, which is: P n= P0 (1 + r)n where n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars)and r = interest rate per period (in decimal form). Inserting in our values, we have: P4.5 = $10,400,000(1.0625)4.5 = $10,400,000(1.313651676) = $13,661,977.43. Thus, it will be short $13,661,977.43 – $14,000,000 = $338,022.57.3. Answer the below questions.(a) The portfolio manager of a tax-exempt fund is considering investing $500,000 in a debt instrument that pays an annual interest rate of 5.7% for four years. At the end of four years, the portfolio manager plans to reinvest the proceeds for three more years and expects that for the three-year period, an annual interest rate of 7.2% can be earned. What is the future value of this investment?At the end of year four, the portfolio manager’s amount is given by: P n= P0 (1 + r)n. Inserting in our values, we have P4= $500,000(1.057)4 = $500,000(1.248245382) = $624,122.66. In three more years at the end of year seven, the manager amount is given by: P7= P4(1 + r)3. Inserting in our values, we have: P7= $624,122.66(1.072)3 = $624,122.66(1.231925248) = $768,872.47. (b) Suppose that the portfolio manager in Question 3, part a, has the opportunity to invest the $500,000 for seven years in a debt obligation that promises to pay an annual interest rate of 6.1% compounded semiannually. Is this investment alternative more attractive than the one in Question 3, part a?At the end of year seven, the portfolio manager’s amount is given by the following equation, which adjusts for semiannual compounding. We have: P n= P0(1 + r/2)2(n). Inserting in our values, we have P7= $500,000(1 + 0.061/2)2(7)= $500,000(1.0305)14= $500,000(1.522901960) =$761,450.98. Thus, this investment alternative is not more attractive. It is less by the amount of $761,450.98 – $768,872.47 = -$7,421.49.4. Suppose that a portfolio manager purchases $10 million of par value of an eight-year bond that has a coupon rate of 7% and pays interest once per year. The first annual coupon payment will be made one year from now. How much will the portfolio manager have if she(1) holds the bond until it matures eight years from now, and (2) can reinvest all the annual interest payments at an annual interest rate of 6.2%?At the end of year eight, the portfolio manager’s amount is given by the following equation, which adjusts for annual compounding.We have:()11+ Par Value n n + r P A r ⎡⎤-=⎢⎥⎢⎥⎣⎦where A = coupon rate times par value. Inserting in our values, we have:88(1 + 0.062 1) = 0.07($10,000,000) 0.062P ⎡⎤-⎢⎥⎣⎦+ $10,000,000 = $700,000[9.9688005] + $10,000,000 = $6,978,160.38 + $10,000,000 = $16,978,160.38.5. Answer the below questions.(a) If the discount rate that is used to calculate the present value of a debt obligation’s cash flow is increased, what happens to the price of that debt obligation?A fundamental property of a bond is that its price changes in the opposite direction from the change in the required yield. The reason is that the price of the bond is the present value of the cash flows. As the required yield increases, the present value of the cash flow decreases; hence the price decreases. The opposite is true when the required yield decreases: The present value of the cash flows increases, and therefore the price of the bond increases.(b) Suppose that the discount rate used to calculate the present value of a debt obligation’s cash flow is x %. Suppose also that the only cash flows for this debt obligation are $200,000 four years from now and $200,000 five years from now. For which of these cash flows will the present value be greater?Cash flows that come earlier will have a greater value. As long as x% is positive and the amount is the same, the present value will be greater for the $200,000 four years from now compared to fiveyears from now. This can also be seen by noting that if x > 0 then ()()4511 1x 1x ⎡⎤⎡⎤>⎢⎥⎢⎥++⎣⎦⎣⎦. The latter inequality implies ()()4511$2,000 $2,0001x 1x ⎡⎤⎡⎤>⎢⎥⎢⎥++⎣⎦⎣⎦will hold.6. The pension fund obligation of a corporation is calculated as the present value of the actuarially projected benefits that will have to be paid to beneficiaries. Why is the interest rate used to discount the projected benefits important?The present value increases as the discount rate decreases and decreases as the discount rate increases. Thus, in order to project the benefits accurately, we need an accurate estimate of the discount rate. If we underestimate the discount rate then we will be projecting more available pension funds than we will actually have.7. A pension fund manager knows that the following liabilities must be satisfied:Years from Now Liability (in millions)1 2.02 3.03 5.44 5.8Suppose that the pension fund manager wants to invest a sum of money that will satisfy this liability stream. Assuming that any amount that can be invested today can earn an annual interest rate of 7.6%, how much must be invested today to satisfy this liability stream?To satisfy year one’s liability (n = 1), the pension fund manager must invest an amount today that is equal to the future value of $2.0 million at 7.6%. We have:To satisfy year two’s liability (n = 2), the pension fund manager must invest an amount today that is equal to the future value of $3.0 million at 7.6%. We have:To satisfy year three’s liability (n = 3), the pension fund manager must invest an amount today that is equal to the future value of $5.4 million at 7.6%. We have:To satisfy year four’s liability (n = 4), the pension fund manager must invest an amount today that is equal to the future value of $5.8 million at 7.6%. We have:If we add the four present values, we get $1,858,736.06 + $2,591,174.80 + $4,334,679.04 + $4,326,920.42 = $13,111,510.32, which is the amount the pension fund manager needs to invest today to cover the liability stream for the next four years.8. Calculate for each of the following bonds the price per $1,000 of par value assuming semiannual coupon payments.Bond Coupon Rate (%) Years to Maturity Required Yield (%)A 8 9 7B 9 20 9C 6 15 10D 0 14 8Consider a 9-year 8% coupon bond with a par value of $1,000 and a required yield of 7%. Given C = 0.08($1,000) / 2 = $40, n = 2(40) = 80 and r = 0.07 / 2 = 0.035, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = ()8011 1.035$40 0.035⎡⎤-⎢⎥⎢⎥⎣⎦= 11 15.6757375$400.035⎡⎤-⎢⎥⎢⎥⎣⎦= [] 035.0 20.06379285 1 40$⎥⎦⎤⎢⎣⎡-= [] 26.7487757 40$= $1,069.951.The present value of the par or maturity value of $1,000 is: ()1n M + r = ()80$1,0001.035= $1,00015.6757375= $63.793. Thus, the price of the bond (P) = present value of coupon payments + present value of par value = $1,069.951 + $63.793 = $1,133.74.Consider a 20-year 9% coupon bond with a par value of $1,000 and a required yield of 9%. GivenC = 0.09($1,000) / 2 = $45, n = 2(20) = 40 and r = 0.09 / 2 = 0.045, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = ()4011 1.045$45 0.045⎡⎤-⎢⎥⎢⎥⎣⎦ = 11 5.81863645$45 0.045⎡⎤-⎢⎥⎢⎥⎣⎦ = 1 0.1719287 $45 0.045-⎡⎤⎢⎥⎣⎦=$45[18.401584] = $828.071.The present value of the par or maturity value of $1,000 is: ()1n M+ r = ()40$1,0001.045 = $1,0005.81863645= $171.929. Thus, the price of the bond (P) = $828.071+ $171.929= $1,000.00. [NOTE. We already knew the answer would be $1,000 because the coupon rate equals the yield to maturity.]Consider a 15-year 6% coupon bond with a par value of $1,000 and a required yield of 10%. GivenC = 0.06($1,000) / 2 = $30, n = 2(15) = 30 and r = 0.10 / 2 = 0.05, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = ()3011 1.05$30 0.05⎡⎤-⎢⎥⎢⎥⎣⎦ = 11 4.3219424$300.05⎡⎤-⎢⎥⎢⎥⎣⎦ = 10.2313774 $30 0.05-⎡⎤⎢⎥⎣⎦=$30[15.372451] = $461.174.The present value of the par or maturity value of $1,000 is: ()1n M + r = ()30$1,0001.05 =3219424.4000,1$ =$231.377. Thus, the price of the bond (P) = $461.174 + $231.377= $692.55.Consider a 14-year 0% coupon bond with a par value of $1,000 and a required yield of 8%. GivenC = 0($1,000) / 2 = $0, n = 2(14) = 28 and r = 0.08 / 2 = 0.04, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦=2811 (1.04)$0 0.04⎡⎤-⎢⎥⎢⎥⎣⎦=11 2.998703319$0 0.055⎡⎤-⎢⎥⎢⎥⎣⎦= 055.0 0.33477471 1 0$⎥⎦⎤⎢⎣⎡-=$0[16.66306322] = $0. [NOTE. We already knew the answer because the coupon rate is zero.]The present value of the par or maturity value of $1,000 is: ()1n M + r = ()28$1,0001.04 = $1,0002.99870332 = $333.48. Thus, the price of the bond (P) = $0 + $333.48 = $333.48.9. Consider a bond selling at par ($100) with a coupon rate of 6% and 10 years to maturity.(a) What is the price of this bond if the required yield is 15%?We have a 10-year 6% coupon bond with a par value of $1,000 and a required yield of 15%. GivenC = 0.06($1,000) / 2 = $30, n = 2(10) = 20 and r = 0.15 / 2 = 0.075, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = 2011 (1.075)$30 0.075⎡⎤-⎢⎥⎢⎥⎣⎦ = 11 4.2478511$30 0.075⎡⎤-⎢⎥⎢⎥⎣⎦ = 1 0.2354131$30 0.075-⎡⎤⎢⎥⎣⎦=$30[10.1944913] = $305.835.The present value of the par or maturity value of $1,000 is: ()1n M + r = ()20$1,0001.075 = $1,0004.2478511 =$235.413. Thus, the price of the bond (P) = $305.835 + $235.413 = $541.25.(b) What is the price of this bond if the required yield increases from 15% to 16%, and by what percentage did the price of this bond change?If the required yield increases from 15% to 16%, then we have:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦=2011 (1.08)$30 0.08⎡⎤-⎢⎥⎢⎥⎣⎦= [] 9.8181474 30$= $294.544.The present value of the par or maturity value of $1,000 is: ()1n M + r = ()20$1,0001.08= $214.548.Thus, the price of the bond (P) = $294.544 + $214.548= $509.09.The bond price falls with percentage fall is equivalent to $509.09$541.25$541.25- = -0.059409 or about -5.94%.(c) What is the price of this bond if the required yield is 5%?If the required yield is 5%, then we have:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ = 2011 (1.025)$30 0.025⎡⎤-⎢⎥⎢⎥⎣⎦= [] 15.5891623 30$= $467.675.The present value of the par or maturity value of $1,000 is: ()1n M + r = ()20$1,0001.025= $610.271.Thus, the price of the bond (P) = $467.675 + $610.271 = $1,077.95.(d) What is the price of this bond if the required yield increases from 5% to 6%, and by what percentage did the price of this bond change?If the required yield increases from 5% to 6%, then we have:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦ =2011 (1.03)$30 0.03⎡⎤-⎢⎥⎢⎥⎣⎦= [] 614.8774748 30$= $446.324.The present value of the par or maturity value of $1,000 is: ()1n M + r =)03.1(000,1$20 = $553.676.The price of the bond (P) = $446.324 + $553.676 = $1,000.00. [NOTE. We already knew the answer would be $1,000 because the coupon rate equals the yield to maturity.]The bond price falls with the percentage fall equal to ($1,000.00 – $1,077.95) / $1,077.95 = -0.072310 or about -7.23%.(e) From your answers to Question 9, parts b and d, what can you say about the relative price volatility of a bond in a high-interest-rate environment compared to a low-interest-rate environment?We can say that there is more volatility in a low-interest-rate environment because there was a greater fall (-7.23% versus -5.94%).10. Suppose that you purchased a debt obligation three years ago at its par value of $100,000 and nine years remaining to maturity. The market price of this debt obligation today is $90,000. What are some reasons why the price of this debt obligation could have declined from time you purchased it three years ago?The price of a bond will change for one or more of the following three reasons:(i) There is a change in the required yield owing to changes in the credit quality of the issuer.(ii) There is a change in the price of the bond selling at a premium or a discount, without any change in the required yield, simply because the bond is moving toward maturity.(iii) There is a change in the required yield owing to a change in the yield on comparable bonds (i.e., a change in the yield required by the market).The first and third reasons are the likely reasons for the situation where the bond has plummeted from $100,000 to $90,000. The bond has plummeted in value because the credit quality of the issuer has fallen and/or the bond has plummeted because the yield on comparable bonds has increased.11. Suppose that you are reviewing a price sheet for bonds and see the following prices (per $100 par value) reported. You observe what seem to be several errors. Without calculating the price of each bond, indicate which bonds seem to be reported incorrectly, and explain why.Bond Price Coupon Rate (%) Required Yield (%)U 90 6 9V 96 9 8W 110 8 6X 105 0 5Y 107 7 9Z 100 6 6If the required yield is the same as the coupon rate then the price of the bond should sell at its par value. This appears to be the case of bond Z since par values are typical at or near a $100 quote. If the required yield decreases below the coupon rate then the price of a bond should increase. This is the case for bond W. This is not the case for bond V so this bond is not reported correctly. If the required yield increases above the coupon rate then the price of a bond should decrease. This is the case for bond U. This is not the case for bonds X and Y so these bonds are not reported correctly. Thus, bonds V, X, and Y are incorrectly reported because the change in the bond price is not consistent with the difference between the coupon rate and the required yield.12. What is the maximum price of a bond?Consider an extreme case of a 100-year 20% coupon bond with a par value of $1,000 that after one year falls so that the required yield is 1%. Given C = 0.2 ($1,000) / 2 = $100, n = 2(99) = 198 and r = 0.01 / 2 = 0.005, the present value of the coupon payments is:()111n r P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦= 19811 (1.005)$100 0.005⎡⎤-⎢⎥⎢⎥⎣⎦= 11 2.684604$100 0.005⎡⎤-⎢⎥⎢⎥⎣⎦=1 0.3724944 $100 0.005-⎡⎤⎢⎥⎣⎦= $1,000[1,125.51012] = $12,550.112.The present value of the par value of $1,000 is: ()1n M + r =()198$1,0001.005 = $1,0002.684604 = $372.494.Thus, the price of the bond (P) = $12,550.112 + $372.494 = $12,922.61.This is a percent increase of ($12,922.6 – $1,000) / $1,000 = 11.92606 or about 1,192.61%.If the required yield falls to 0.001%, then the bond price would increase to $20,778.33, which would be a percent increase of about 1,977.83%.If the required yield falls to 0.00001%, then the bond price would increase to $20,778.33, which would be a percent increase of about 1,977.83%.If the required yield falls to 0.0000000001%, then the bond price would increase to $20,801.76, which would be a percent increase of about 1,980.18%.Thus, we see that even for these extreme numbers (that are highly unlikely), we find there appears to be a limit on how high a bond price might rise assuming that rates do not reach negative numbers.If the required yield is a negative number then there would be no limit to how high a bond price might rise. For example, if the required yield becomes a negative 1%, then the bond price would increase to $70,468.18. If it becomes a negative 10%, then the bond price becomes $2,296,218.049,925.23.13. What is the “dirty” price of a bond?The “dirty” (or “full”) price is the amount that the buyer agrees to pay the seller, which is the agreed-upon price plus accrued interest. The price of a bond without accrued interest is called the clean price. The exceptions are bonds that are in default. Such bonds are said to be quoted flat, that is, without accrued interest.14. Explain why you agree or disagree with the following statement: “The price of a floater will always trade at its par value.”One would disagree with the statement: “The price of a floater will always trade at its par value.”First, the coupon rate of a floating-rate security (or floater) is equal to a reference rate plus some spread or margin. For example, the coupon rate of a floater can reset at the rate on a three-month Treasury bill (the reference rate) plus 50 basis points (the spread).Next, the price of a floater depends on two factors: (1) the spread over the reference rate and (2) any restrictions that may be imposed on the resetting of the coupon rate. For example, a floater may have a maximum coupon rate called a cap or a minimum coupon rate called a floor. The price of a floater will trade close to its par value as long as (1) the spread above the reference rate that the market requires is unchanged and (2) neither the cap nor the floor is reached.However, if the market requires a larger (smaller) spread, the price of a floater will trade below (above) par. If the coupon rate is restricted from changing to the reference rate plus the spread because of the cap, then the price of a floater will trade below par.。

CFP国际金融理财师投资规划第二章 债券投资与分析综合练习与答案

CFP国际金融理财师投资规划第二章债券投资与分析综合练习与答案一、单选题1、下列关于债券价格的叙述,正确的是()。

A.市场利率越高,债券价格越高B.息票率越高,债券价格也越高C.当市场利率小于息票率时,债券价格越低D.当市场利率大于息票率时,债券价格越高【参考答案】:B【试题解析】:债券价格与市场利率成反比;当市场利率小于息票率时,债券价格越高;当市场利率大于息票率时,债券价格越低。

2、关于债券的到期收益率,下列表述正确的是()。

A.当债券以折价方式卖出时,Y TM低于息票利率;当以溢价方式卖出时,Y TM 高于息票利率B.所支付款项的现值等于债券价格的折现率C.现在的收益率加上平均年资本利得率D.以任何所得的利息支付都是以息票利率再投资这一假定为基础的【参考答案】:B【试题解析】:A项,当债券折价出售时Y TM高于息票率,当债券溢价发行时Y TM低于息票率;C项,年资本平均收益率加上当期收益率不等于到期收益率;D项,Y TM基于的假设是:任何收益的再投资都是以到期收益率而不是当期利率进行的。

3、新股网上定价发行与网上竞价发行的不同之处在于()。

Ⅰ.认购方式不同Ⅱ.发行价格的确定方式不同Ⅲ.认购成功者的确认方式不同Ⅳ.承销方式不同A.Ⅰ、ⅡB.Ⅰ、ⅢC.Ⅱ、ⅢD.Ⅰ、Ⅱ、Ⅲ、Ⅳ【参考答案】:C【试题解析】:新股网上定价发行与网上竞价发行的不同之处主要有两点:①发行价格的确定方式不同,前者事先确定价格,后者事先确定发行底价,由发行时竞价决定发行价;②认购成功者的确认方式不同,前者按抽签决定,后者按价格优先、同等价位时间优先原则决定。

4、同一类型的债券,长期债券利率比短期债券高,这是对()的补偿。

A.信用风险B.利率风险C.政策风险D.购买力风险【参考答案】:B【试题解析】:债券的期限越长,就越容易受到利率风险的影响;期限越短,受到利率风险的损害的可能性就越小。

5、证券发行者为扩充经营,按照一定的法律规定和发行程序,向投资者出售新证券而形成的市场称为()。

《债券市场:分析与策略(第九版)》名词解释索引----考试必备!!!

名词面数承诺收益率47字母承销标准192 alt-A贷款194初始贷款额与抵押品价值之比201 CD等价收益率122初始发行时的高收益债券138 CPR209传统赎回条款和再融资条款136 LIBOR曲线111次级贷款194 MBS205次级抵押贷款支持证券205 MMD尺度167次级留置权193 wi市场120次级债券类别148 A次级债务131按市价调整头寸10次主权政府债券175案件受托人132存续期利率上限195 B D保兑信用证161大型发行机构168保障性186贷款抵押债券147备用信用证161贷款额与抵押品价值之比192本国债券市场174贷款重估198本金4贷款组合补充文件209本金保值票据144担保费208本金剥离国债124担保品管理人148本金价值4担保信托债券131贬值177担保债券184变现再融资219单交易商系统140波动性风险10单一价格拍卖120剥息124单一类别抵押贷款支持证券206不可撤销的信用额度161单月提前偿付率210不可赎回136当期贷款额与抵押品价值之比201不可再融资136当期国债120布雷迪债券185当前可赎回债券136部分偿付199导管企业192部分提前清偿199到期价值4 C到期期限3参考利率195到期日1产业部门131到期收益率37常规抵押贷款199到期收益率预期解释108常规价格136道义责任债券159偿债基金159等值应税收益率91偿债基金条款137抵押贷款191偿债基金要求137抵押贷款发放人192偿债准备基金159抵押债券131抵押转手证券206浮动利率债券27地方性发行机构168浮动利率债券163递延利息债券138负凸性222递延赎回权136覆盖率测试148递延息票结构138G第二留置权193杠杆贷款146第一留置权193杠杆收购153盯市10高级135定期拍卖法183高级次级债务132定期债券135高级担保债务131陡峭收益率曲线105高级无担保债务131斗牛士债券174高级银行贷款146短端久期80高级债券类别148短期债券3高收益债券135对投资组合久期的贡献度67高质量债券135多交易商系统140个性化抵押贷款支持证券205堕落天使138更新和重置基金159 F公共部门借款要求186发行前交易市场120公司175发行人1公司债券2发行说明书补充文件209公用事业部门130反向浮动利率债券5购买力风险9反向浮动利率债券163股票挂钩票据143反向收益率曲线105固定本金证券118非分期偿还债券5固定利率抵押贷款195非合规常规贷款200挂钩债券183非竞争性投标119关键利率久期81非欧元区市场区175滚动发行144非套现再融资194滚动发行风险144非投资级144国际债券市场174非投资级债券135国际组织175非政府机构抵押贷款支持证券205国家机构175分批还本债券135国家认可统计评级机构133分期偿付证券42国家债券市场174分期偿还债券5国库券118分期还款195国内信贷比率186分期还款时间表196国债2风险的风险10H服务费192还款额与收入之比192浮动利率债券4合规常规贷款200合规贷款200交叉匹配系统140合规限额199交易日123合同相对人关系146交易商间经纪人120荷兰式拍卖法183交易商间系统140宏观经济基本面186交易商募集的商业票据145后端比率194结构化债券162互换利率111结构性票据142互换利率收益率曲线111结算日123互换曲线111借款人1回售收益率42金额久期66回售条款6金额凸性值71汇率177金融部门131汇率风险9金融机构175汇率风险177仅付利息产品198混合可调整利率抵押贷款195经营和维持基金159货币风险9净价30货币风险177竞争性投标120货币挂钩票据144久期向量81货币认购权证180久期中性68货币市场等价收益率122局部预期理论108 J巨额贷款199基本价格169巨额潘德布雷夫185基本余额186具有货币选择权的债券180基础利率88绝对利率变动51基础设施债务175绝对收益率变动51基点的价值59绝对优先权规则132基准利差88K基准利率88可变利率通知债券163即期利率95可对冲利率105即期利率曲线95可交换债券6季节性效应219可调整利率抵押贷款195加权平均存续期5可选A级贷款194加权平均贷款期限207可选择偿还债券163加权平均贷款账龄207可延长的调息结构139加权平均票面利率207可转换债券6加权平均期限207客户对交易商系统140加权平均剩余期限207L加速偿债基金条款138垃圾债券135价格波动性59离岸金融中心176简单年利率36离岸债券市场174离岸中心176欧洲中期票据181理论即期曲线95P利差久期66拍卖系统140利率风险7潘德布雷夫债券市场184利率久期81票面利率195利率期限结构93平均存续期5利率期限结构95平均存续期221利率上限27平坦的收益率曲线106利率下限27普通年金14利率与期限再融资194普通年金18利率再融资219普通收益率曲线105利率止跌债券180Q利息的利息7期初年金18利息的利息45期间利率上限195联邦住房管理局提前偿付经验209期限3零息债券4期限结构的流动性理论108零息债券22期限利差93留置权状况193期限偏好理论106流动性风险9期限再融资219流动性理论106气球型期限137伦勃朗债券174前端比率194伦敦银行同业拆借利率4清偿能力186 M清算132美国受托人计划132权益组别148美元价格债券169全价30美元区175全球债券181猛犬债券174R面积覆盖率测试148燃尽效应220面值4认购倍数120面值收益率曲线95认购权证180名义利率4SN商业不动产抵押贷款支持证券2内部收益率34升值177内部债券市场174实际久期77年金14实际天数计算惯例123年金18实物付息债券138 O市场分割理论106欧洲美元债券178市场风险7欧洲区175市场间利差89欧洲债券市场174市场内利差89市政票据163提前还款风险202市政债券2提前赎回赔偿条款137事件风险153提前赎回溢价137适销性风险9提前再融资市政债券162收益率88条件提前偿付率209收益率比率89调息公式4收益率变动百分比52贴现17收益率利差88贴现率17收益率曲线93贴现值17收益率曲线重构久期80停止收益率120收益率相对变动52通货膨胀保值国债118首次按面值赎回收益率40通货膨胀风险9首次赎回日136通货膨胀挂钩债券5首次赎回收益率40通货膨胀调整本金119受让人146头条风险153赎回价格40投资级144赎回价格136投资级贷款146赎回价值4投资级债券135赎回时间表40投资期分析51赎回时间表136投资期收益率51赎回收益率40凸性56赎回条款5凸性偏差110双货币债券180凸性值71双重担保158托管至期满债券162水龙头式拍卖法183W税后收益率91外部债务比率186税收风险166外国债券市场174私人抵押贷款保险商199完全分期还款贷款195速度209完全预期理论106缩期风险222违约风险8锁定期198违约损失率150 T维修准备基金159套现再融资194无限税收一般责任债券158特别拍卖法183武士债券174提前偿付S曲线220X提前偿付额42息票4提前偿付风险222息票剥离国债124提前偿付速度209息票利率4提前还款惩罚抵押贷款200息票利率或息票利率递减债券180提前还款额199现金流瀑布148现金流收益率42有偏预期理论106现金流收益率209有限税收一般责任债券158现金流收益率220与通货膨胀指数挂钩的证券118现值16预期理论106相对收益率利差89远期利率104项目融资176Z新发国债95再融资136新发国债120再融资136信用分析133再融资比率219信用风险8再融资风险186信用挂钩票据143再融资收益率40信用降级9再投资风险7信用降级风险9再投资风险46信用利差8再投资期149信用利差风险8再投资收益45信用评级8暂具占有权的债务人132信用评级转换表152脏价30信用评级转换矩阵152债券等价收益率122信用升级9债券等值收益率38信用债券131债券等值收益率220信用证协议161债券重构125循环信用额度161债务人1 Y债务认购权证180烟草税债券162长端久期80延期风险222长期国债118延期付息债券5长期债券3衍生抵押贷款支持证券产品206长期债券135扬基债券174折价24扬基债券177正式声明168一般赎回价格136正凸性76一般责任债券158正向倾斜收益率曲线105一级票据146证券化192已发国债120证券化204溢价24政府贷款198银行贴现额基础121政府机构抵押贷款支持证券205盈余基金159政府机构债券2应计利息30政治分析187永久性(无期限)债券180直接付款信用证161优级贷款194直接募集票据145优级债券135指数利率195中级债券135转让方法146中期国债118转手息票利率207中期票据141资产支持证券市场2中期债券3资金的总成本141中期债券135子弹式贷款146中上级债券135子弹债券137重组132子市场89逐步升息债券138总收益率47主权债券175组别181住房抵押贷款支持证券2组合前缀206住房抵押贷款支持证券204组合系数207住房周转率218最差收益率42注册的证券本金和利息的分离过程124最低价拍卖法183专项收益债券162最高收益率120。

证劵投资试题库含参考答案

证劵投资试题库含参考答案一、单选题(共52题,每题1分,共52分)1.债券种类很多,依据不同的标准会有不同的分类。

其中,按( )分类,可以将债券分为政府债券、金融债券和公司债券。

A、付息方式B、债券形态C、发行主体D、发行方式正确答案:C答案解析:考查债券的分类。

按发行主体,债券可以分为政府债券、金融债券和公司债券。

2.交易者买入( ),是因为他预期基础金融工具的价格在近期内将会下跌。

A、认沽期权B、认购期权C、欧式期权D、美式期权正确答案:A3.基金合同生效后,投资者申请购买基金份额的行为被称作( )。

A、申购B、认购C、购买D、赎回正确答案:A答案解析:考查基金认购和申购的概念区分。

4.优先股对发行人的意义包括( )。

A、享受利息税前抵扣B、享有较为固定的收益C、避免决策权分散D、为公司筹集短期资金正确答案:C答案解析:优先股对发行人的意义:可以筹集长期稳定的公司股本,股息固定,减轻利润分配负担,优先股股东的管理决策权一般受限,可以避免决策权分散和改变。

5.通常,( )债券以低于面值的价格发行和交易,债券持有人实际上是以买卖(到期赎回)价差的方式取得债券利息。

A、零息B、附息C、政府D、票息累积正确答案:A答案解析:债券按付息方式的分类。

根据债券发行条款中是否规定在约定期限向债券持有人支付利息,债券可分为零息债券、附息债券和息票累积债券。

其中,零息债券以低于面值的价格发行和交易,债券持有人实际上是以买卖(到期赎回)价差的方式取得债券利息。

6.按照发行流通性质,可以将金融市场划分为()和()。

A、货币市场资本市场B、证券市场非证券金融市场C、债权市场权益市场D、一级市场二级市场正确答案:D7.引起股票价格变动的直接原因是( ) 。

A、流动性挤压B、政治因素C、公司经营状况的变化D、买卖双方力量强弱的转换正确答案:D答案解析:考查引起股票价格变动的直接原因。

8.( )是证券监管机构对申报文件的真实性、准确性、完整性和及的性作合规性的形式审查,而将发行人的质量留给证券中介机构来判断和决定的股票发行监管制度。

债券测试题及答案详解

债券测试题及答案详解一、单项选择题(每题2分,共10题)1. 债券的面值通常是多少?A. 100元B. 1000元C. 10000元D. 100000元答案:A2. 债券的票面利率是指?A. 债券发行时的利率B. 债券到期时的利率C. 债券持有期间的利率D. 债券转让时的利率答案:A3. 债券的到期收益率与市场利率的关系是?A. 市场利率上升,到期收益率下降B. 市场利率下降,到期收益率上升C. 市场利率与到期收益率无关D. 市场利率与到期收益率成正比答案:B4. 以下哪项不是债券的基本特征?A. 偿还性B. 收益性C. 流动性D. 风险性答案:D5. 债券的信用评级是由哪个机构提供的?A. 证券交易所B. 评级机构C. 银行D. 保险公司答案:B6. 债券的发行价格高于其面值时,我们称之为?A. 溢价发行B. 折价发行C. 平价发行D. 零价发行答案:A7. 债券的期限是指?A. 债券发行到到期的时间B. 债券发行到偿还的时间C. 债券到期到偿还的时间D. 债券发行到偿还的时间答案:A8. 债券的持有人享有的权利不包括以下哪项?A. 利息收益权B. 债券转让权C. 债券赎回权D. 参与公司经营决策权答案:D9. 债券的付息方式通常有?A. 一次性付息B. 定期付息C. 按需付息D. 以上都是答案:B10. 债券的发行主体可以是?A. 政府B. 企业C. 金融机构D. 以上都是答案:D二、多项选择题(每题3分,共5题)1. 债券的发行方式包括哪些?A. 公募发行B. 私募发行C. 直接发行D. 间接发行答案:A|B|C|D2. 债券的分类依据可以是?A. 发行主体B. 债券期限C. 利息支付方式D. 债券的偿还方式答案:A|B|C|D3. 债券的风险包括?A. 利率风险B. 信用风险C. 流动性风险D. 通货膨胀风险答案:A|B|C|D4. 债券的偿还方式有?A. 到期偿还B. 提前偿还C. 分期偿还D. 延期偿还答案:A|B|C|D5. 债券的交易市场包括?A. 场内市场B. 场外市场C. 银行间市场D. 国际市场答案:A|B|C|D结束语:以上是债券测试题及答案详解,希望能够帮助您更好地理解和掌握债券的相关知识。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。