外文翻译-- 欧盟成员国的增值税

vat欧洲也要交吗

vat欧洲也要交吗

如果欧盟外的公司将欧盟外的商品运送储存在某一欧盟国家,则卖家必须在该国进行VAT增值税的注册、申报和缴纳。

如果卖家将货物从欧盟某国运送到欧盟别国(消费国)的商品销售额超出了该消费国的远程销售起征点,则卖家必须在消费国进行VAT增值税的注册、申报和缴纳。

VAT (Value Added Tax)简单来说是欧盟国家普遍采用的对纳税人生产经营活动的增值额征收的税。

跨境卖家只要在欧盟范围内进行销售,不管是使用亚马逊FBA服务,还是欧盟本地仓储进行发货,都属于欧盟VAT增值税应交范畴,需要注册VAT税号并申报和缴纳税款,以免影响产品的正常销售。

如果您没有按时申报和缴纳应付税款,欧洲相关国家税局会采取惩罚措施,例如征收应缴税额之外的罚金、滞纳金、利息等。

如果卖家不遵守增值税法规相关要求,该国税局还会将该问题反映给您交易所在的平台,并要求该平台采取限制措施。

平台会在法律允许的范围内配合政府相关部门对于可能存在增值税不合规的卖家和账号进行调查;并且会在收到税局的通知后,对被认定为不合规的卖家和账号采取限制措施,包括下架货物、限制刊登和禁止销售等。

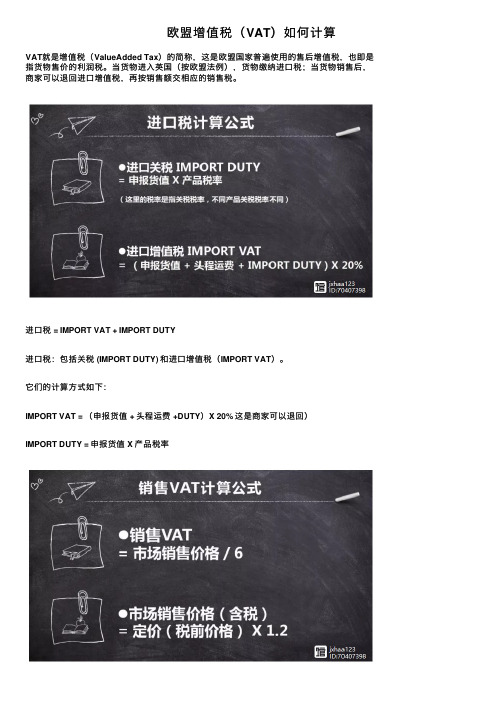

欧盟增值税(VAT)如何计算

欧盟增值税(VAT)如何计算

这是欧盟国家普遍使⽤的售后增值税,也即是

)的简称,这是欧盟国家普遍使⽤的售后增值税,也即是VAT就是增值税(ValueAdded Tax)的简称,

指货物售价的利润税。

当货物进⼊英国(按欧盟法例),货物缴纳进⼝税;当货物销售后,商家可以退回进⼝增值税,再按销售额交相应的销售税。

进⼝税 = IMPORT VAT + IMPORT DUTY

进⼝税:包括关税 (IMPORT DUTY) 和进⼝增值税(IMPORT VAT)。

它们的计算⽅式如下:

IMPORT VAT = (申报货值 + 头程运费 +DUTY)X 20% 这是商家可以退回)

IMPORT DUTY = 申报货值 X 产品税率

销售税VAT= 市场销售价格 / 6 (上缴的VAT,实为市场售价的1/6)

假如设产品申报的货值为:4000欧元

头程运费为:500欧元

关税假定为:400欧元

进⼝增值税=(申报货值+头程运费+关税)*20%=(4,000+500+400)*20%=980欧元若全部销售额为20,000欧元

销售增值税为20,000/6=3,333.3欧元

当期应缴的VAT为3,333.3-980=2,353.3欧元

注意进⼝关税不可抵扣

(⽂中部分素材来源于⽹络,如有侵权联系客服)。

VAT

简介

VAT即 Value Added Tax/ AD VALOREM tax,附加税,欧盟的一种税制,即购物时要另加税,是根据商品 的价格而征收的。如定价是 inc vat,即已含税, excl vat是未包税,Zero vat是税率为0。各国税率不相同, 如意大利是 22%税率(2013年10月开始实行),(英国是17.5%,2011年1月4日调高至20%),即要多给20%款项, 阿根廷为21%(部分商品实行50%减免,即为10.5%)。

主要税率

欧盟大部分国家主要税率有:标准税率、减免税率、零税率三种。以下为欧盟部分国家常见VAT税率分类: 英国:20%,5%、0%; 德国:19%、7%、0%; 法国:20%、 5.5%、10%、0%; 意大利:22%、5%、10%、0%; 西班牙:21%、 10%、4%

例子

举个例子,如果商家A给一个东西定价2元,增值税是17%,那他就得卖2.34元,这0.34元就是给政府的,商 家还是只收2元,但这个产品的原材料需要1元,原料供应商同样要上缴17%的增值税0.17元并提供买家增值税发 票,商家A可以用发票抵扣联去抵扣这0.17元的应缴增值税,也就是说商家A实际缴纳的增值税为其商品的增值部 分(2元-1元=1元)缴纳17%的增值税0.17元。

谢谢观看

VAT

欧盟的一种税制

01 简介

03 主要税率

目录

02 征收范围 04 例子

vat:单词vat, [væ t],n. (酿造或染色用的)大桶、大缸,vt.把……装入大桶。

VAT:单词缩写,Value-added Tax,最早起源于法国,是在欧盟应用的一种税制。等同于中国地区的增值 税。而在部分地区如澳大利亚地区又称为GST(Goods and Services Tax)。

欧盟的税收政策与税收合作

欧盟的税收政策与税收合作税收是国家经济发展的重要支柱之一,在全球范围内,各国都在积极探索和制定相应的税收政策。

欧盟作为一个经济和政治联盟,也有着自己独特的税收政策和税收合作机制。

本文将重点探讨欧盟的税收政策及其与成员国之间的税收合作方式。

一、欧盟的税收政策欧盟的税收政策主要由欧洲委员会负责制定和执行。

欧洲委员会根据欧洲联盟的宗旨和目标,致力于促进成员国之间的税收合作,协调税收政策,提升税收制度的透明度和效率,以及打击跨国税收逃避行为。

以下是欧盟的一些主要税收政策措施:1.增值税(VAT)欧盟统一增值税制度是欧盟税收政策的核心之一。

增值税是一种消费税,按照货物和服务的增值额计征,逐级追加。

欧洲委员会主导了欧盟内增值税制度的统一与协调,包括税率、纳税义务、税收申报等方面的规定。

这有助于促进欧洲内部市场的一体化和公平竞争。

2.企业所得税(CIT)欧盟的企业所得税政策旨在减少欧洲范围内的税收竞争和负面影响。

欧洲委员会提出了公平合理的企业所得税政策,通过合理的税基设定、防止利润转移和避税等手段,减少成员国之间的税收不平等,并推动成员国之间的税收合作。

3.金融交易税(FTT)金融交易税是欧盟致力于减少金融部门风险和增加稳定性的一项措施。

欧洲委员会计划推行欧洲范围内的金融交易税,以征收金融交易的一定比例。

这将有助于增加金融行业的稳定性,并为欧洲产业和公共财政提供更多的资金来源。

二、欧盟成员国间的税收合作为了加强成员国之间的税收合作,欧盟采取了一系列措施,以确保税收政策的协调和税收制度的高效运作。

以下是欧盟在税收合作方面的主要机制和举措:1.共同税收基础(CCCTB)共同税收基础是欧盟推动税收协调的一项重要举措。

该制度旨在为跨境企业提供简化的纳税义务,通过采用统一的税基计算方法,减少企业在不同国家纳税制度之间的差异,降低企业成本,促进欧洲内部市场的发展。

2.信息交换与透明度欧盟各成员国之间通过信息交换和合作促进税收透明度。

欧盟征税流程的流程和注意事项

欧盟征税流程的流程和注意事项一、欧盟征税流程。

1. 确定应税交易。

- 首先要明确交易是否属于欧盟增值税(VAT)的应税范围。

这包括商品的销售、服务的提供等。

例如,在欧盟境内销售货物,如果货物的供应地在欧盟境内,通常是应税交易。

对于服务,根据服务的类型和接受服务的对象所在地等因素来确定是否应税。

- 企业需要对自身的业务活动进行详细梳理,判断每一项交易是否涉及应税行为。

2. 注册增值税号(VAT号)- 如果企业在欧盟境内有应税交易,且达到了注册门槛(不同成员国门槛可能不同),就需要在相关成员国注册增值税号。

- 注册过程中,企业要提供准确的公司信息,包括公司名称、地址、联系方式、业务范围等。

通常需要通过当地的税务机关网站在线注册,有些情况下可能需要提交纸质文件。

- 例如,在英国(仍在一定程度上遵循欧盟增值税相关规定的过渡期内情况),企业可以通过英国税务海关总署(HMRC)的在线平台进行VAT注册。

3. 计算应纳税额。

- 对于商品销售,增值税应纳税额=应税销售额×增值税税率。

不同类型的商品可能适用不同的税率,欧盟有标准税率、低税率和零税率等多种税率结构。

- 以销售电子产品为例,如果适用标准税率20%(假设某成员国的标准税率),销售额为1000欧元,那么应纳税额 = 1000×20% = 200欧元。

- 对于服务,计算方式类似,但要根据服务的性质确定应税基数。

例如,对于咨询服务,应税基数可能是服务收费金额。

4. 开具增值税发票。

- 当发生应税交易时,企业需要按照欧盟的规定开具增值税发票。

发票上应包含必要信息,如供应商和客户的名称和地址、增值税号、发票日期、商品或服务描述、数量、单价、增值税税率和税额等。

- 发票必须清晰、准确,并且要按照规定的格式开具。

在一些成员国,电子发票也是被认可的,但同样要满足相关的电子签名、存储和可访问性等要求。

5. 申报增值税。

- 企业需要按照规定的申报周期向当地税务机关申报增值税。

欧盟财务状况分析报告(3篇)

第1篇一、引言欧盟(European Union,简称EU)是世界上最大的经济体之一,由28个成员国组成,其经济总量和影响力在全球范围内具有重要地位。

随着全球经济的不断发展,欧盟的财务状况备受关注。

本报告将对欧盟的财务状况进行详细分析,包括财政收入、支出、债务等方面,以期为我国相关决策提供参考。

二、欧盟财政收支概况1. 财政收入欧盟的财政收入主要来源于以下几个方面:(1)成员国缴纳的会费:欧盟会费是欧盟财政的主要收入来源,占欧盟财政收入的约80%。

会费缴纳标准根据各成员国的国内生产总值(GDP)和人口等因素确定。

(2)关税和进口税:欧盟对进口商品征收关税和进口税,这部分收入占欧盟财政收入的约10%。

(3)增值税:欧盟内部增值税是欧盟财政的重要收入来源,占欧盟财政收入的约10%。

(4)其他收入:包括罚款、利息收入等,占欧盟财政收入的约10%。

2. 财政支出欧盟的财政支出主要包括以下几个方面:(1)农业补贴:农业补贴是欧盟财政支出的重要组成部分,主要用于支持欧盟农业发展和农民利益。

(2)区域发展基金:区域发展基金用于支持欧盟内部欠发达地区的经济发展,缩小地区发展差距。

(3)社会保障:社会保障支出包括养老保险、失业保险、医疗保险等,占欧盟财政支出的约30%。

(4)其他支出:包括教育、科研、环境保护、外交、安全等领域支出。

三、欧盟债务状况1. 债务规模截至2020年底,欧盟债务总额达到约7.5万亿美元,占欧盟GDP的约80%。

其中,欧元区债务总额约为6.6万亿美元,占欧元区GDP的约88%。

2. 债务结构欧盟债务主要分为以下几类:(1)公共债务:包括政府债务和地方政府债务,占欧盟债务总额的约70%。

(2)私营部门债务:包括银行、企业等私营部门债务,占欧盟债务总额的约30%。

(3)家庭债务:家庭债务占欧盟债务总额的约10%。

3. 债务风险欧盟债务风险主要体现在以下几个方面:(1)债务水平较高:欧盟债务水平较高,容易引发债务危机。

european vat number格式

european vat number格式全文共四篇示例,供读者参考第一篇示例:欧洲增值税号码(European VAT number)是指欧盟成员国企业的增值税登记号码,用于在跨境贸易中进行增值税规范征收。

欧盟成员国之间的贸易是征收增值税的,而只有具有增值税号码的企业才能参与增值税交易,并享受相关的退税或减免政策。

欧洲增值税号码的格式是由各个欧盟成员国自行制定的,并且格式可能会有所不同。

一般来说,欧洲增值税号码由国家代码加上企业注册号码组成,中间可能会有一些分隔符号,具体格式如下:- 国家代码:欧盟成员国有不同的国家代码,如德国是“DE”、法国是“FR”、意大利是“IT”等等。

- 企业注册号码:根据各个国家的注册制度不同,企业注册号码可能由数字、字母或者组合而成。

举个例子,德国的欧洲增值税号码格式为“DE123456789”,其中“DE”表示德国的国家代码,而“123456789”则是企业的注册号码。

而法国的欧洲增值税号码格式可能是“FR12345678”,具体格式可能有所不同。

在申请欧洲增值税号码时,企业需要根据所在国家的规定向当地税务机关进行注册。

一般来说,欧盟成员国的税务机关会对企业进行严格审核和核实,确保企业具有合法经营资格和真实的营业信息。

一旦注册成功,企业就会获得一个独一无二的欧洲增值税号码,并可以在跨境贸易中合法开展业务。

欧洲增值税号码是欧盟成员国企业在跨境贸易中不可或缺的重要证明,具有合法性和信誉性。

企业需要按照各国的规定合法申请并使用欧洲增值税号码,避免不必要的法律风险和经济损失。

希望以上内容能为您对欧洲增值税号码有更深入的了解。

第二篇示例:欧洲增值税号(VAT number)是指欧洲国家对企业征收增值税(VAT)的一种税号,也称为欧洲税号。

不同国家有不同的VAT号格式和命名规则,但基本上都是由不同国家的地区代码、企业代码和校验码组成。

欧洲VAT号的格式通常是由数字和字母组合而成的,不同国家之间也会有所不同。

增值税暂行条例中英文对照

中华人民共和国增值税暂行条例The Provisional Regulations of the People‘s Republic of China on Value-Added Tax第一条在中华人民共和国境内销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人,为增值税的纳税义务人(以下简称纳税人),应当依照本条例缴纳增值税。

Article 1 All units and individuals engaged in the sales of goods, provision of processing,repairs and replac ement services, and the importation of goods within the territory of the People“s Republic of China are taxpayers of Value-Added Tax (heteinafter referred to as "taxpayers“),and shall pay VAT in acco rdance with these Regulations.第二条增值税税率:Article 2 VAT rates:(一)纳税人销售或者进口货物,除本条第(二)项、第(三)项规定外,税率为17%。

(1)For taxpayers selling or importing goods,other than those stipulated in items (2)and (3)of this Article,the tax rate shall be 17%.(二)纳税人销售或者进口下列货物,税率为13%:(2)For taxpayers selling or importing the following goods,the tax rate shall be 13%:1.粮食、食用植物油;i。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

毕业设计/论文外文文献翻译院系经济管理学院专业班级会计1202班姓名原文出处Bruce. V AT Between EU Member States[J].Int-ernational Tax and Public Finance.2013,(6).评分指导教师2016年3 月1 日欧盟成员国的增值税布鲁斯.欧盟成员国的增值税[J].国际税收与公共财政.2013,(6).本文结合了法律、经济等方面的知识对增值税(V AT)的征收过程中存在的问题进行了分析。

其主要目的是提供全面的教学工具、法律、案例和分析演习,并通过对世界各国的税务专家和学者的研究分析得出的启发,为未来应对的增值税问题提供借鉴意义。

通过本文的比较介绍,提供了一个分析有关税收结构和税收基础的政策问题,以及深入了解为何产生增值税纠纷,从而使增值税纠纷得到解决。

作者扩大了覆盖范围,包括在欧洲,亚洲,非洲和澳大利亚,介绍了这些国家新增值税的相关发展。

最后用一章对生活服务业进行了补充和案例分析。

增值税作为政府收入的主要来源正在被130 多个国家所使用。

增值税是一个具有普遍性和基础性的消费税,它增加了商品和服务的价值评估。

增值税是在生产的每一个阶段普遍征收的附加值,它也是一个让卖方为买方支付己购买的商品和服务的税款(进项税额)的一中税收信贷机制(销项税额)。

一般而言,增值税有以下几层含义:一个普通税适用于所有涉及生产和销售商品以及提供服务的商业活动;消费税最终由消费者承担;是间接征收消费的商品或服务价格的一部分;在每个阶段的生产和分配阶段间接税可见多级税收征收消费的商品或服务价格;一个小幅收税款,已被控在其所有的采购系统,它采用的是由卖方收取了相应的信贷索赔其所有销售的增值税或增值税的部分付款。

增值税纳税义务的计算方法有三种:信贷发票的计算方法是—加减法,还有另外的两种方法,但是仅仅只有信用发票的计算方法是相对使用广泛的。

信贷发票的方法突出了增值税的定义功能:使用销项税(销售缴纳的税款)和进项税(采购缴纳的税款)一般纳税人收取的增值税应税销售额和采购所支付的应税进项税额之间的差额作为计算其增值税纳税义务。

因此这种方法需要使用发票,分别列出所有应税销售额的增值税部分。

从而销售货物的一方为买方提供购货发票。

销售发票显示的是收取的销项税额,则购货发票显示的就是支付的进项税额。

最后,纳税人通过使用增值税发票抵免的计算方法来计算需汇到税务机关的增值税额。

方法如下:销售发票中的增值税(销项税额)减去购货发票所示的增值税(进项税额),减去进项税额后的余额汇给税务机关;如果进项税大于了销项税一般需退款。

美国是唯一一个作为经济合作与发展组织的成员不征收增值税的国家,然而,增值税已经成为联邦税收改革辩论争议的重要对象。

间接税如增值税产生的税收收入是许多国家的重要税收部分。

在实践中,增值税制度产生全球四分之一的税收收入。

近130个国家现在有一个增值税制度(包括过去10年中已经采用该系统的70个国家)(肯尼和明茨2004年)。

更多专注于国际流动性税基,备受外界关注更多的是税负、间接税、消费税或增值税制度,少缴纳企业所得税,特别是资本所得(戈登和尼尔森1997年)。

在欧盟统一增值税期间,间接税和增值税制度的协调受到重视(费尔等人,1995年)。

一项涵盖所有私人物品和服务的增值税法律都是现行欧盟制度的特点,但仍有许多豁免,这一普遍的指令,在2001年挪威的增值税改革也同样存在。

改革引入了服务增值税一般法,但许多豁免仍然特别存在着。

相比于不完善的、不均匀的系统更多的支持一般的、统一的增值税系统。

这样的系统可以提高经济效率,降低行政成本,寻租和欺诈活动的行业,低利率和零评级大堂(肯尼和史密斯2006)。

一般的、统一的增值税系统相当于一个统一的消费税的所有商品和服务。

这样的系统也意味着,生产者的物质投入净增值税税率为零,不论速度结构。

根据生产效率定理(德蒙和米尔利斯)。

一个增值税制度与豁免是不遵守生产效率定理,因为中间的税收将产业之间的差异,这是最佳的。

在另一方面,它覆盖了增值税制度,但有较低的利率,对他们的销售零的评级行业的青睐,它们可以在全速率撤销支出增值税中间体,只减少销售率或为销售率零。

一个一般的和统一的增值税制度也可能正面影响家庭福利的分配。

如果初始情况的特点是在大部分商品和少数服务征收增值税的税率不同,福利分配就相对较小,因此实行对所有商品和服务的统一税率可能会提高福利,因为服务消费随收入的分配提高福利分配。

热衷缺乏价值利益点(肯尼2007年)从理论的角度出发讨论了这一观点,尽管在实际的税收政策以及增值税的普及增加了税收。

正如上面所提到的,增值税系统一般不统一。

理论分析要求相对简单的模型和简单的税制结构分析的实际政策,经济和税收制度的结构是非常复杂的,需要有一个详细的数值模型,以分析不同增值税的影响系统。

本文主要分析了不完善和不均匀增值税系统的福利效应,通过分析和比较不同的不完善,不均匀增值税系统,做出了一个统一的以增值税体系为基础的动态和可计算的一般小型开放型经济均衡模型(CGE)。

该模型反映了实体经济在许多方面有所不同,从更简单的理论模型,满足规范税收理论的假设,并建议统一商品税,以便减少税务。

在我们的分析中,我们提出了下面的问题。

不完善的增值税制度可以导致经济发展更加糟糕,纳税对象是服务行为的增值税体系还不如纳税对象仅仅只包括商品的增值税体系,这是为什么呢?2001年进行增值税改革的挪威和从1990年底开始增值税改革的欧盟都出现过这种情况。

将一个不完善的增值税体系扩展成一个统一的和一般的增值税体系,会带来很多福利,那么它的先决条件又是什么呢?美国对其进行了解释,不能纯粹依据理论来建立增值税制度系统,因为这样会存在税收楔子和扭曲市场经济。

基线增值税系统是一个非均匀增值税系统,它的增税对象主要包括商品。

这个基线增值税系统与2001年挪威增值税改革相比较,它的特点是统一了所有商品和服务,包括公共产品和服务的增值税税率。

2001年挪威的增值税改革迈出了一步,它的一般增值税系统包括许多服务,但仍有许多免税、零税率和较低的税率。

特别是增值税税率对食品和不含酒精的饮料的征税,其征税率是一般增值税率的一半。

本文对公开收入的中性政策改革、一次性转移的变化以及系统中特定的增值税率都进行了研究,从中得出系统特定的增值税率对收入没有影响变化,但对其家庭福利有所影响。

综上所述,研究增值税对企业税收影响的影响是一项非常系统的工程。

首先,要对该项工程的必要性与重要性有一个清晰认识;其次,要对该项工程的研究现状有一个全面分析;最后,要对该项工程的加强路径有一个科学把握。

只有这样,才能真正夯实该项工程的基础,增强该项工程的有效性与实效性。

V AT Between EU Member StatesBruce.V AT Between EU Member States[J].International Tax and PublicFinance.2013,(6).This paper integrates legal, economic, and administrative materials about value added tax. Its principal purpose is to provide comprehensive teaching tools-laws, cases, analytical exercises, and questions drawn from the experience of countries and organizations from all areas of the world. It also serves as a resource for tax practitioners and government officials that must grapple with issues under their V AT or their prospective V AT. The comparative presentation of this volume offers an analysis of policy issues relating to tax structure and tax base as well as insights into how cases arising out of V AT disputes have been resolved. The authors have expanded the coverage to include new V AT related developments in Europe, Asia, Africa and Australia. A chapter on life service industry has been added as well as an analysis of significant new cases.More than 130 countries use V AT as a key source of government revenue. V AT is a general, broad-based consumption tax assessed on the value added to goods and services. V AT is generally levied on value added at every stage of production, with a mechanism allowing the sellers a credit for the tax they have paid on their own purchases of goods and services (input tax) against the taxes collected on their sales of goods and service (output tax). Generally, V AT is: A general tax that applies to all commercial activities involving the production and distribution of goods and the provision of services; A consumption tax ultimately borne by the consumer; An indirect tax levied on the consumer as part of the price of goods or services; A multistage tax visibleateach stage of the production and distribution chain; and A fractionally collected tax that uses a system of partial payments whereby a seller charges V AT on all of its sales with a corresponding claim of credit for V AT that it has been charged on all of its purchases.There are three methods of calculating V AT liability: the credit-invoice method, the subtraction method, and the addition method. This column deals with only the credit-invoice method, which is the most widely used. The credit-invoice method highlights the V AT defining feature: the use of output tax (tax collected on sales) and input tax (tax paid on purchases). A taxpayer generally computes its V AT liability as the difference between the V ATcharged on taxable sales and the V AT paid on taxable purchases. This method requires the use of an invoice that separately lists the V AT component of all taxable sales. The sales invoice for the seller becomes the purchase invoice of the buyer. The sales invoice shows the output tax collected and the purchase invoice shows the input tax paid. To summarize, taxpayers use the credit-invoice method to calculate the amount of V AT to be remitted to the taxing authorities in the following manner: Aggregate the V AT shown in the sales invoices (output tax); Aggregate the V AT shown in the purchase invoices (input tax); Subtract the input tax from the output tax and remit any balance to the government; and In the event the input tax is greater than the output tax. The United States is the only member of the Organization of Economic Cooperation and Development that does not levy a V AT on a national level; however, V AT has become widely recognized as an important option in federal tax reform debates.Indirect taxes such as value added taxes generate a substantial part of tax revenue in many countries. In fact, V AT systems generate a quarter of the world’s tax revenue. Nearly 130 countries now have a V AT system (with over 70 countries having adopted the system during the last 10 years) (Keen and Mintz 2004). More focus on internationally mobile tax bases has drawn attention to directing more of the tax burden to indirect taxes such as consumption taxes or V AT systems, and less to income taxes, especially capital income (Gordon and Nielsen 1997). During the harmonization of EU taxes, indirect taxes, and V AT systems received much attention (Fehr etal. 1995). A general V AT law covering all private goods and services characterizes the current EU system, but there are still many exemptions from this general instruction.Such a V AT system also exists in Norway as a consequence of the Norwegian V AT reform in 2001. The reform introduced a general V AT law on services, but many exemptions are still specified.There are several arguments in favor of a general and uniform V AT system, compared with imperfect, nonuniform (and nongeneral) systems.Such a system may improve economic efficiency and reduce administration costs, rent-seeking and fraud activities by industries that lobby for lower rates and zero ratings (Keen and Smith 2006). A general and uniform V AT system equals a uniform consumer tax on all goods and services.Such a system also implies that the producers’ net V AT rate on material inputs equals zero, irrespective of the ratestructure. This is optimal according to the production efficiency theorem (Diamond and Mirrlees ).A V AT system with exemptions violates the production efficiency theorem because taxation of intermediates will differ between industries. On the other hand, industries that are covered by the V AT system but have lower rates or zero ratings on their sales are favored because they can withdraw expenditures to V AT on intermediates at full rates and only levy reduced or zero rates on their sales.A general and uniform V AT system may also have positive effects on the distribution of welfare among households. If the initial situation is characterized by a V AT on most goods but only on a few services, the introduction of a uniform rate on all goods and services may improve the distribution of welfare because services shareof consumption increases with income.Keen (2007) points to the lack of interest in value added taxation from the theoretical second-best literature in spite of the V AT’s popularity in practical tax policy. As mentioned above, V AT systems are in general not uniform. Theoretical analyses demand relatively simple models and simple tax structures to be analytically tractable.In practical policies, the structures of the economy and the tax systems are quite complex, and there is a need for detailed numerical models in order to analyze the effects of different V AT systems. This paper contributes to the literature by analyzing the welfare effects of an imperfect extension of a nonuniform V AT system, and comparing different imperfect, nonuniform V AT systems with a uniform and general V AT system within an empirically based dynamic computable general equilibrium (CGE) model for a small open economy. This model mirrors a real economy, Norway, and differs in many respects from the more simple theoretical models that fulfill the assumptions of normative tax theory and recommend uniform commodity taxes, combined with no input taxation.In our analyses, we ask the following questions. Can the introduction of a nonuniform V AT system including only some services make the economy worse off than having a V AT system only covering goods and in that case, why? Such reforms characterize both the Norwegian V AT reform of 2001 and the EU V AT reform from the late 1990-ties. Will an additional extension to a uniform and general V AT system be welfare superior to the nonuniform (and nongeneral) V AT systems and what are important preconditions? As will beexplained below, one cannot on purely theoretical grounds establish the welfare rankings of such V AT systems when there are preexisting distortions as tax wedges and market power in the economy. The baseline V AT system is a nonuniform V AT system mainly covering goods. This baseline V AT system is then compared with the extended nonuniform Norwegian V AT reform of 2001, and a general V AT system characterized by a uniform V AT rate on all goods and services, including public goods and services. The Norwegian V AT reform of 2001 was a step in the direction of a general V AT system by including many services, but there are still many exemptions, zero ratings and lower rates. In particular, the V AT rate on food and nonalcoholic beverages is half the general V AT rate. The policy reforms are made public revenue neutral, and changes in lump sum transfers as well as in the system specific V AT rate are studied. With a revenue-neutral change in the system-specific V AT rate, the V AT systems can be ranked with respect to welfare effects.When comparing the two different nonuniform V AT systems, our analysis shows that an imperfect extension of the V AT system to cover more services is welfare inferior to the baseline nonuniform V AT system only covering goods.In summary, influence of V AT tax on enterprises is a system engineering. First of all, it is necessary to have a clear understanding of the necessity and importance of the project; secondly, it is necessary to have a comprehensive analysis on the present situation of the project. Only in this way can we truly strengthen the foundation of the project, and enhance the effectiveness and effectiveness of the project.。