中国对外直接投资影响研究的文献综述

中国对外直接投资影响研究的文献综述

中国对外直接投资影响研究的文献综述中国对外直接投资(FDI)是指中国企业在境外投资并持有对外实体企业的股权或投资。

自改革开放以来,中国对外直接投资规模不断扩大,对外投资方式和领域也日益多元化。

中国对外直接投资的增长不仅为中国企业拓展国际市场提供了机会,也对全球经济和国际贸易产生了深远影响。

本文旨在通过文献综述的方式,探讨中国对外直接投资的影响及其相关研究成果。

一、中国对外直接投资的发展历程自1979年实行对外开放以来,中国对外直接投资规模不断扩大。

起初,中国企业主要通过政府引导和支持的方式进行对外投资,主要集中在资源开采和基础设施建设领域。

随着中国经济的快速增长和企业国际化进程的加快,中国对外直接投资呈现出快速增长的态势,投资领域也逐渐扩展到制造业、金融业、科技创新等领域。

2014年,中国对外直接投资流出规模首次超过外商直接投资流入规模,成为全球最大的海外投资国之一。

1. 对中国经济的影响中国对外直接投资为中国企业提供了更广阔的市场空间和资源获取途径,有利于提高中国企业的国际竞争力。

中国对外直接投资也为中国企业带来了更多的技术和管理经验,促进中国产业结构升级和经济转型。

中国对外直接投资还有助于推动中国与沿线国家的经济合作,促进区域经济一体化进程。

2. 对全球经济的影响中国对外直接投资不仅推动了中国经济的发展,也对全球经济产生了重要影响。

中国的对外投资活动促进了沿线国家的基础设施建设和产业发展,为当地创造了就业机会和经济增长点。

中国对外直接投资也有助于促进全球经济的复苏和增长,为全球投资提供了新的机遇和动力。

在中国对外直接投资研究领域,国内外学者们进行了大量深入的研究,形成了丰富的研究成果。

主要研究内容包括中国对外直接投资的发展模式、动因和效果、中国对外直接投资与宏观经济的关系、中国对外直接投资与区域经济一体化等方面。

1. 发展模式、动因和效果关于中国对外直接投资的发展模式、动因和效果的研究较为广泛。

外商直接投资(FDI)在我国区位选择的文献综述

位 选 择 的 主要 因素 。

2 城 市之 间 F 1分 . D

布 的 影 响 因素

外商直接投资在城 市之 间分 布的实证研究 外 , 还有一批 国外学者利用计 量 经 济模 型和方法 , 对我 国省 区和 区域 的

FI D 区位 选 择 进行 了分 析 。 C e (9 6 应 用 条 件 逻 辑 模 型 , h n 19 ) 对 18 — 9 1 我 国 3 97 19 年 0个 省 区 的 数 据 进

实证研 究

目前 用 于 区 位 选 择 实 证 研 究 的 主

西藏除外 ) 。研 究 结 果 表 明 ,市 场 化 程

过对统计数据 和公 司访 问调查 发现 , 香 港企业在 中 国直 接投资 的省 际差别 很

大 。魏后 凯 、 灿 飞 、 新 (0 1利 用 问 贺 王 20 )

要方法有横截面数据计量分析 、 面板数

资企业数据为样本 , 应用企业地理定位 选择 的计 量模 型 , 对外 资聚集 的 国( 地

区 0 应进 行 深 入 的 实证 研 究 。 中选 效 文

分析 。 根据 因子分析’ 商在华投资动机 夕 可以归纳为生产投入 与市场动 机 、 生产 服务动 机 、 文化联 系和感情 动机 、 争 竞

外 商直接投资( F I D ) 在我 国区位选择 的文献综述

■ 王 芳

摘要 : 阶段 ,D 现 F I已成为经济学界 的热 f话题 , 1 外商直接投 资给所在地带来 了各种直接 、 间接 的经济效益, 果吸 引外 如 资是 目前学术界讨论的热点之一 , 目前 国内外 学术界对外 商直接投 资的区位选择进行 了大量的研 究, 文就这些研 究 本

考虑的区位因素通常具有较大差异。因

外商直接投资对我国产业结构影响的研究【文献综述】

毕业论文文献综述国际经济与贸易外商直接投资对我国产业结构影响的研究一、前言改革开放以来,随着外商直接投资的不断进入,我国三次产业结构也不断的变化。

外商直接投资从整体上促进了我国产业结构的调整与升级、产业技术的进步和产业组织结构的优化。

但外商直接投资对三次产业的贡献度不同,使得产业间的发展水平差距扩大,不利于经济的长远发展。

特别是外商直接投资在我国投资中所占比重很大,对我国产业结构的改善有着很大的影响。

二、正文外商直接投资的理论回顾哈佛大学教授Vernon在1966年提出“国际产品周期理论”。

Vernon认为国际直接投资的产生是产品生命周期三个阶段(创新、成熟、标准化)更迭的必然结果,外资公司顺应产品生命周期的变化,在成熟产业向低成本国家转移的同时引起各自所在国的产业结构升级。

伴随着国际投资所产生的一个重要现象就是国际产业转移。

赤松要(Kaname Akamatsu)在20世纪30年代提出了“雁行模式”(Flying-Geee Paradigm)。

按照该模式,一国产业成长经历了引进产品、进口替代、出口增长、成熟、返进口五个阶段,而产业结构升级依次分为劳动和资源密集、技术密集和资本密集三个阶梯。

随着外资的进入及一国工业化的发展,某一产业坐逐渐衰落,并将转移到低一个梯级的国家和地区,通过产业替代,推动产业升级。

我国外商直接投资与产业结构的情况改革开放以来,中国吸引外商直接投资的规模不断的扩大,质量也不断提高。

尤其是中国加入WTO以后,我国吸引外商直接投资的规模呈现出进一步扩大的趋势。

我国利用外商直接投资大体上可以分为四个阶段,第一阶段:1979~1986年即萌芽起步阶段;第二阶段:1987~1991年即稳步发展阶段;第三阶段:1992~ 1995年即高速发展阶段;第四阶段:1996年至今即平稳发展阶段(李义福,2009)。

外商直接投资在我国产业结构分布的现状是,主要集中在第二产业,对第三产业投资比重偏低,对第一产业投资比重很低。

关于出口影响对外直接投资的文献综述

二 ,出 口贸易影响对外投资的理论研究

R f i ( 9 4 曾在 其 对 国 际 贸 易 与 国 际 投 资 的 研 究 中 发 u fn 18 ) 现 ,基 于 经 过 修 正 的 H O S 易 模 型 , 当放 松 要 素 不 能 流 动 的 —-贸 假 定 时 ,对 外 直 接 投 资 可 能 和 出 口贸 易 有 负相 关 关 系 。B c l y uke

出 E贸 易 与 … 国对 外 直 接 投 资之 前 有 密 切 的联 系 , 一 般 来 而 S l a e e(0 2 认 为 对 外 直 接 投 资 与 资本 和 管 理 相 关 ,其 l a vt r 20 ) 说 , 山 1贸 易 的 发 展 会 促 进 该 国 对 外 直 接 投 资 的进 行 ,但 也 有 实 质 是投 资 丁东 道 国 的 资本 、 工 地 、 房 等 生 产 要 素 , 同 时 投 7 1 学 者 对 此 持 相 反 的 观 点 。本 文 将 从 理 论 和 实 证 两个 方 面 对 出 口 影 响 对 外 直 接 投 资 的 理论 进 行 梳 理 。 资者 保 留 其对 所 投 资 资 本 的控 制 权 力 。 国 内学 者 关 于对 外 直 接 投 资 的 定 义 则 主 要 强 调 资本 的 流 动 以及 相 应 的控 制 权 。钟 新 昌 (0 9 提 出对 外 直 接投 资 的 核 心 是 投 资者 对 本 国 或 本 地 区 以外 20)

向不 足 通 常 意 义 上 所 说 的 包 括 技 术 、 资本 和 管 理 等 综 合 要 素 在 5C s o ( 9 1  ̄ a s n 1 8 )提 出 贸易 因素 与对 外 直 接 投 资 行 为 的潜 在 动 D 国 际 间 的 转 移 。进 入 2 世 纪 6 年 代 以 后 ,在 经 济 学 领 域 内也 逐 机 有 非 常 紧 密 的联 系 , 比如 对 东 道 国 出 口的 替 代 ,通 常 被 解 释 O 0 渐 有 学 者 开 始 了对 于 对 外 直 接 投 资 理 论 的 正 式 研 究 , H m r U 为对 外 直接 投 资 的动 机 之 一 。B c l y C s o 的 模 型 给 出 了这 y e  ̄ u k e 和 a sn V r o 的研 究 是 当 时 比较 有 代 表 性 的 , 他 们 的研 究 认 为对 外 直 样 的 理 论 ,可 以认 为 出 口贸 易 是 一 种 固 定 成 本 比较 低 ,而 运 输 enn 接 投 资 是 寡 头 垄 断企 业 的 发 展 与 行 动 扩 大 的 必 然 结 果 , 从 而 在 和 贸 易 壁 垒 等 可变 成 本 比较 高 的活 动 ,通 过 对 外 直 接 投 资 的 形 理 论 上为 美 国对 外 直 接 投 资提 供 了根 据 ,说 明 了它 的合 理 性 。 式 在 国外 建 立 分 公 司 , 来 为 原 来 的 出 口 市 场 提 供 销 售 产 品 的 服 H前 关 于 对 外 直 接 投 资 比 较 权 威 的定 义 主 要 来 自国 际 货 币 务 ,可 以 明显 的 降 低 可 变 成 本 ,但 这 个 过 程 可 能 比 出 口贸 易 产 荩 金 组 织 ( M ) 和 经 济 合 作 与 发 展 组 织 ( E D 对 其 给 出 的 生 更 高 的 固 定 成 本 。只 要 国外 市 场 对 跨 国 公 司 产 品 的 需 求 模 IF OC) 定 。 IF 埘 外 直 接投 资 定 义 为 某种 国 际投 资 ,该 投 资 反 映 了 M把 达 到 一 定 程 度 , 从 出 口 贸易 到对 外 直 接 投 资 的 转 换 将 是 一 个 很 某 绎 济 体 直 接 投 资 者 获 得 其 他 经 济 体 企业 持久 权 益 的 目标 。 O C 在 IF 国 际投 资 定 义 的 基础 上 ,把 对 外 直 接 投 资 阐述 为 : ED M 对 某 自然 的 过 程 , 即 出 口与 投 资 会 表 现 出 一 种此 消彼 长 的关 系 。 但 大 部 分 的 学 者 的 研 究 还 是 支 持 出 F促 进 对 外 直接 投 资 的 1

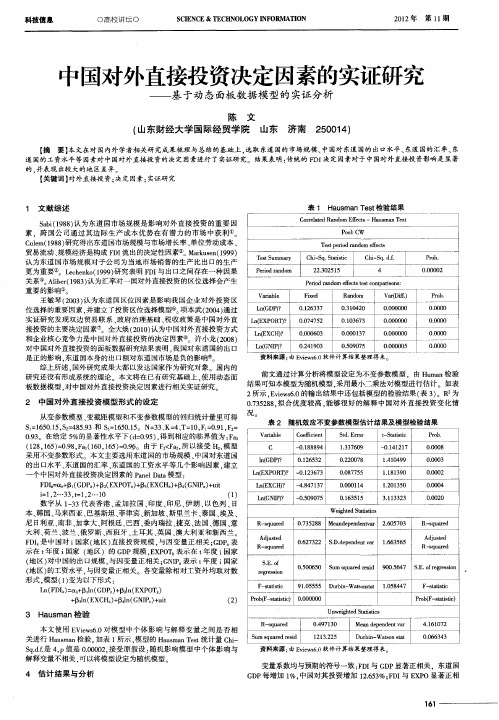

中国对外直接投资决定因素的实证研究——基于动态面板数据模型的实证分析

【 要】 摘 本文在 对国 内外学者相 关研 究成果梳 理与总结的基础上 , 选取 东道 国的市场规模 、 中国对 东道 国的出口水平 、 东道 国的汇率、 东 道 国的工资水平等因素对中国对外直接投资的决定因素进行 了实证研究。结果表明: 传统 的 F I D 决定 因素对于中国对 外直接投资影响是显著 的, 并表现 出较大的地区差异。 【 关键词 】 对外直接投 资; 决定因素 ; 实证研究

重 要 的影 响 ⑤ 。

表 1 Ha s nT s 检验结果 u ma e t

C reae n o E e t — Ha s n T s o rltdRa d m f cs t ma b t l

P o: W olC T s p r d rn o e e t et e o d m cs i a f T s S mmay et u r C i S . tt t h- q S a s c ii C iS . - h - q d£ Po . rb

S = 6 0 1 , 2 4 59 1 5 . S = 8 .3和 S = 6 0 1 。 N= 3 K= 、 1 , 1O9 , 2 5 3 1 5 .5 3 、 4 T= 0 F = .1 F =

况。

表 2 随机效应不变参数模型估计结果及模型检验结果 源自Vaibe r l aC

P ro n o ei r d m d a

2 .0 51 23 2 5

【

4

0O o 2 .0 o

P r d rn o e e t ts mp r o s e o a d m cs e t o ai n : i f c s Va a l f be Fx d ie Ra d m no V rDf. a『i 1 Po . rb

中国主权财富基金对外直接投资战略文献综述

【 摘 要 】美 国次贷危机 引起国际投资市场剧烈波动,中国主权财富基金也深受其害 ,本文首先梳理 了中国主权财 富基金战略定位,然后从战略效应、区位 战

略、行 业战略及投资模式四个方面,对 中国主权财 富基金对外直接投资战略研究现状进行归纳分祈,并对现有研 究做出评述。 1 . 引言

期 的积 极 影 响 ,但 是 这 一 一 影 响并 未 持 续 。 F o t a k 、B o r t o 1 o t t i 和

M e g g i n s o n( 2 0 0 8) 基 于 主 权 财 富 基 金 的 7 5 项 投 资行 为研 究发 现 , 主权 财 富基 金 能够 获 得平 均 1 % 的异 常收 益 ,但 两 年后 却 获得 了4 1 %

的 负 收 益 。 此 后 ,B o r t o l o t t i 、F o t a k 和M e g g i n s o n( 2 0 0 9 ) ̄ J 2 3 5

2 0 0 8 年 夏 天 以来 , 由于 美 国次贷 危机 引发 的 金 融风 暴 蔓 延全 球 , 美 国 、 欧 盟 及 日本 等 世 界 主 要 金 融 市 场 都 饱 受 危 机 困 扰 , 而 主 权财 富基 金 对 于 一 些濒 临 破 产 的 著 名金 融 机 构 的 注 资 ,对 于 稳 定 全球 经 济 危 机 做 出 了突 出贡 献 。 与 此 同时 ,全 球 资源 性 商 品如 石 油价 格 的一 路 高 涨 以及 新 兴 市 场 国 家经 济 的高 速 发展 ,都 促 使 主权 财 富基 金 规 模 不 断扩 张 ,成 为 世 界经 济 和 国际 金 融领 域 的重 点 研 究 对 象 。 由 于 主 权 财 富 基 金 投 资 数 据 不 易 获 得 ,对 其 对 外 直 接 投 资 战略 的研 究 大 都 缺 乏系 统 性 和 实 证 数据 支 撑 。本 文主 要 从 主 权 财 富基 金 对 外 直 接投 资 的战 略 定 位 、 战略 效 应 及 战 略选 择 三 个 方面 ,对 国内外 相关 研 究成 果进 行梳 理 并评 述 。 2 . 主权 财 富基 金 战略 定位 O E C D 投 资委 员在 2 0 0 8 年 公布 的‘‘ 份 报 告 中明确 指 出,被 投 资国 有权采 取行动 以保护 本国的 国家安伞 ,需要对 主权 财富基 金的投 资动 机 给予 更 多关 注 ,投资 动机 不仅 来 自商 业利 益 ,也有 可 能受政 治 、 国 防 或 外 交 政 策 因 素 的 驱 动 。B e r n s t e i n ,L e r n e r ,a n d A n t o i n e t t e S c h o a r( 2 0 0 9 )通过对 2 9 支主权 财富基 金在 1 9 8 4  ̄2 0 0 7 年 问共计 2 6 6 2 起 交易 的研 究结果表 明 ,由于主权财 富基金具 有政治背 景 ,尽管 母国 的政治 干预 会 对盈 利状 况造 成 负面 影响 ,但 是 盈利仍 然 不是 主 要 目 的,主权财 富基金主 要投 资于文化相近 的 国家 ,利润最 大化并非 主要 驱 动因 素 。但 也有 部分学 者持相 反观 点 ,S a n t i S O( 2 0 0 9)实 证研究 发 现 , 主 权 财 富 基 金 和 共 同 基 金 一 样 , 其 投 资 行 为 在 于 追 求 商 业 回 报 而 非战略 意图 ,主权 财富基 金投 资偏 向于 多元化资产 , 以实现 国家财 富的保值 增值 ,并 改变过度 依赖美 国国债的 局面 。 我 国主 权 财 富基 金 在 未 来 发展 中成 功 的关 键 , 主 要 是 明确 对 外 投 资 战 略 定 位 ,而 国 内 学 者 对 此 一 直 存 在 争 议 , 主 要 有 三 种 观 点 :一是 战 略型投 资 。王铁 山、郭 根龙 、冯 宗 宪 ( 2 0 0 7 )等 认 为我 国主 权财 富基 金应 通 过诸 如 寻求 战略伙 伴 和人 员管 理 、合 理化 投 资 目标 和 策略选 择 、风 险度 量和 评估 等方 式 ,将 投 资战略 与 国家 经济 发展 战 略相 协调 ,并 配合 国家 重 大政 策和 产业 调整 进 行投 资 ,实施 利用 国 外资源 补 充 国 内资源 的战 略 ,以实 现 国家宏 观 经济 和主 权财 富 基 金 的 共 赢 ; 二 是 财 务 型 投 资 谢 平 , 陈 超 ( 2 0 0 9 )认为 主 权财 富基 金 的行 为与 企业 、 居 民的经 济理 性行 为 一致 , 国家应 被视 为追 求 国家 效用 最大 化 的 “ 经 济 人 ”,其 投 资行 为与 商业 企业 并没 有实 质 性 区 别 ,主 权 财 富 基 金 作 为 国家 投 资 的代 表 ,完 全 是 以追 求利 润 最大 化为 目标 的 商业 投资 主体 ,它 不 应 当也不 可能 承担 国 家政治 目标 。而罗 勇 ( 2 0 0 9 )也指 出 中国在 基金 设立 和 管理 方式 上应 进行 严 格 区 分 ,分 别 设 立 国家 战略 型基 金 和 商 业 型基 金 , 以确 保 商业 目的 基 金 的 正常 投 资 活 动 免 受政 府 干 预 ; 三 是 “国家 资 本 主 义 ” 二 重 性 投 资 。宋 玉 华 ( 2 0 0 9)等认 为 主 权 财 富基 金 在 经 济 利 益驱 动 下 偏 好 于 高风 险高 回报 的 投 资 目标 ,但 在 国 家利 益 层 面 上 ,会 倾 向于 配 合 国家 宏 观 经 济 的 长 期发 展 战 略 目标 ,而 杨 新 臣 , 笪桂 青 ( 2 0 l 0)的 分 析 也 指 出 ,主 权 财 富基 金 在 投 资 发展 过 程 中的 战 略 转 型 不 可 避 免 ,不 能 为 了短 期 目标 放 弃 长 期 目标 ,应 该 是 战 略 性 和 商 业 性 并 重 ,但 在 战 略 高 度仍 需借 鉴 国际 金 融资 本 与 产 业 资 本 合 作 的 模 式 , 为 中 国企 业 的 “ 走 出去 ” 以及 大 宗商 品的 “引进 来 ” 提 供 有 力 的 支 撑 。 中 国 主 权 财 富基 金 采 取 哪 种 战 略 定 位 为 佳 ?或 者 说 中 国 目前 的战 略 定 位 是什 么 ?这 一 困 惑应 该 是 中国 主 权 财 富基 金未 来 发展 中 必须 要解 决 的重 要课 题 。 3 . 主权 财 富基 金战 略效 应 在 战 略 效 应 的研 究 中 ,所 采 用 的定 量 分 析 方 法基 本 都 是 事 件 研究法 ( E v e n t S t u d y ) , 区别 就 在 于 样 本 数量 和 时 间跨 度 的 差 异 ,但 结 论 却存 在 较 大 不 同 。B e c k 和F i d o r a( 2 0 0 8)的研 究表 明 主权 财 富基 金 的投 资 效应 在 短期 内并 不显 著 ,而 R a y m o n d( 2 0 0 8)

外商直接投资文献综述资料

本文档包括改专题的:外文文献、文献综述一、外文文献Foreign Direct Investment (FDI) and standard of living in NigeriaAkinmulegun, Sunday Ojo.Journal of Applied Finance and Banking (2012),2(3): 295-309. AbstractThe subject of interrelationship that exists between foreign direct investment (FDI) and standard of living has been an issue of both theoretical and empirical investigations. This study, thus examined the relationship between foreign direct investment and standard of living measured by per capita income (PCI) in Nigeria over 1986 - 2009 period using time series data. The study employed Vector Auto regression (V AR) model because of the fact that the variables are integrated of different orders in their Unit Root Tests.Test involving Impulse Response Analysis and Variance Decomposition reveal that the relationship between FDI and standard of living is insignificant. Thus, the past values of FDI could be used to predict the future behavior of standard of living in Nigeria only to a lesser extent.Thus, the policy implications underscore the need for institutional and macroeconomic policy framework that would redirect steps in making FDI to contribute positively to the standard of living in Nigeria by channeling the available FDI into industrial, productive sector of the economy.JEL classification numbers: F3, I3, D3, C3Keywords: Foreign Direct Investment (FDI), Standard of Living, Per Capital Income, Vector Autoregression Model(ProQuest: ... denotes formulae omitted.)1 IntroductionForeign direct investment (FDI) can be defined as "investment made to acquire lasting interest in enterprises operating outside of the economy of the investor" (Mosima, 2003). Thus, it is not only a transfer of ownership from domestic to foreign residents but also a mechanism that makes it possible for foreign investors to exercisemanagement and control over host country's firms (Hill, 2004; Sandey, 2003). Accordingly,"when a corporation or an individual decides to move from its countrydomain; crossing international border(s) to establish a new production capacity in such a nation, and/or join a domestic enterprise or a host national to form a corporation, whether or not the corporation has formerly being in existence, in the course of a national establishing a new corporation/enterprise not existing in its country-domain; such that the control and management lies in the hands of the foreign national, such an investment is called foreign direct investment (FDI) and hitherto manifests as such" (Akinmulegun, 2011)Among others, Feldstein (2000) opined that profits generated by FDI contribute to corporate tax revenue in the host country. In addition, if the foreign affiliate decides to reinvest the proceeds into the domestic system, it will be an additional advantage to economic growth in the host nation with the attendant impact any structural change exerts on standard of living of individual citizenry. Although, the theoretical literature on this is clear and straightforward (Findlay, 1978; Romer, 1994), however, the evidence in empirical studies is still divided. This gap needs to be filled.This study therefore aims at examining the impact of FDI on the life standards of Nigerian citizens. Thus, the major hypothesis to be tested is; Ho: foreign direct investment in Nigeria has no significant relationship with the people's standard of living.2 Literature Review2.1 Conceptual LiteratureOne of the major dramatic changes in the world economy over the past three decades as evidence in the super flows of institutions is the surge in the FDI across national borders (Mimiko, 2010). This is so to the extent that scholars all over the ages have argued in favour of FDI as a catalyst for economic growth and living standards in the host nation. That, the wide externalities in respect of technology transfer, the development of human capital and enhancement of domestic productive capacities attested to the beneficial effects of FDI cannot be overemphasized (Bende-Nabende,2002; Feldstein, 2000; Chantal and Patrick, 2005; Alfaro and Charlton, 2007; Mottaleb, 2007; Ayanwale, 2007; Maertens and Swinnen, 2008). The growth effects of FDI and subsequent multiplier impact on living standards in the host country in terms of productivity gains, managerial skills and know-how in the domestic market, employee training, international networks and markets account for its preference as evident in the literature (Findlay, 1978; Caves, 1996; UNCTAD, 1999; Carkovic and Levine, 2002).However, it is sometimes feared whether FDI contributes to the broader aspect of growth and the distribution of income in the host economy. For growth potentials of FDI to manifest, the distribution and redistribution of income as a central factor in determining the impact of growth on living standards cannot be overemphasized. This presupposes a linkage between growth and poverty level of an economy. Thus empirical evidence on the relationship between growth and poverty has shown that higher growth is usually associated with reduction in poverty (Ravallion and Chen, 1997; Dollar and Kraay, 2002; Ravallion and Datt, 2002; Besley and Burgess, 2003; Kraay, 2006; Ashley, 2008). This further presupposes equitable living standard.2.2 Empirical LiteratureThat economic theory univocally predicts a positive and directional impact of FDI on standard of living is a subject of intensive examination as empirical evidence is mixed. There seems to be no doubt that there is a strong correlation between FDI and standard of living. This has been argued from the economic growth potentials of FDI (Hayami, 2001; Mottaleb, 2007; Crespo and Fontura, 2007).Measured in terms of domestic productivity, Adams (2004) found from his regression analysis that FDI is not harmful to sub-Saharan African (SSA) countries. Thus, contributing to the living standard of its citizenry. All these predict a greater positive impact of FDI on living standards of the host country.However, empirical evidence casts doubts on the relationship that exist between FDI and standard of living. This spurred the idea behind this research work at investigating the relationship using a dynamic approach as specified below.3 MethodologyThe methodological approach used in this study follows the works of Selvanathan and Selvanathan (2008) as captured in the growth model, which depicts a realistic relationship between two variables of output and capital stock as in Solow (1956) given as;Yit= α0+αi+μ i+βXit+εit (1)In line with the above theoretical framework therefore, this relationship between FDI and standard of living measured by PCI is presented in a simple model as follows: PCI=f(FDI) (2)wherePCI = per capita income (a measure of standard of living)FDI = foreign direct investmentThe apriori expectation is that;...To avoid spurious regression as suggested by Gujarati and Porter (2009), a stationary test (unit root test) will be conducted to determine the time series properties of the variables and to know whether a condition for long-run equilibrium relationship among them is met.Thus, it is required that variables in a model should be integrated of the same order to meet the condition for long-run equilibrium relationship known as cointegration.If this condition is not met, a better option for estimation as suggested by Gujarati and Porter (2009) and Greene (2003) is the Vector Autoregression (V AR). Hence, this study prefers the V AR model which is specified mathematically asYt=AtYt-1+...+ApTt-p+βtXtεt (3)where t Y is a k vector of endogenous variables (PCI and FDI), t X is a vector of exogenous variables. At ,....Ap and β are matrices of coefficient to be estimated and εt is a vector of innovation.The V AR is commonly used for forecasting system of interrelated time series and for analyzing the dynamic impact of random disturbances on the system of variables. It sidesteps the need for structural modeling by modeling every endogenous variable in the system as a function of the lagged values of all the endogenous variables in theThe V AR form of the model above is given as (4) (5)where β1j and β2j are matrices of coefficient to be estimated and β1t is a vector of innovation, j=1,2,...,k . This is the lag length of each variable. The choice of lag length for this study is made using Akaike Information Criterion (AIC).Once the V AR is estimated, a further analysis in terms of Variance Decomposition and Impulse Response will be conducted. Impulse Response Analysis traces the effects of a shock to an endogenous variable on the variables in the V AR. By contrast, variance decomposition decomposes variation in an endogenous variable into the component shocks to the endogenous variable in the V AR. This gives information about the relative importance of each random innovation to the variables in the V AR.The study thus uses time series data on per capita income (PCI) and foreign direct investment (FDI) collected for 1986 ¡V 2009 period. Data were gathered notably through secondary sources. Results of both Impulse Response functions and Variance Decomposition are presented in the next section.4 Data Analysis4.1 Stationary Test of VariablesTable 1 above presents the results of the Philip Peron Unit root test. The table enables us to determine the time series properties of each variable, and know whether a condition for long-run equilibrium relationship among the variables is met.Note: The Null hypothesis is that the series is non-stationary or contains a unit root. Test statistics for PP are compared with stimulated critical values from Mckinnon, testing the hypothesis at both 5% and 10% significance levels.The lag length in PP test known as test bandwidth selection is based on Newey-West. All results are obtained from E-view 7.1 econometric package.The variables are made stationary at their first difference thereby integrated of order one, denoted as I(1). Hence, the result is a clear indication that the model does not meet the condition for cointegration since all variables are integrated of differentAs suggested by Gujarati and Porter (2009) and Greene (2003); a better alternative when variables in a model are not integrated of the same order is to resort to the V AR technique and all its attached system dynamics. Hence, the use of V AR by this study is justified.4.2 Vector Autoregression ResultsTo know how much endogenous the variables are, the summary regression statistics are presented in Table 2 below.Table 2 above shows the summary of regression statistics. The table presents the level of endogeneity of the variables in the model.The degree of endogeneity of each variable is found to be very high with the high R2 and adjusted R2 of the variables. This implies that the variables are affected by each other to a larger extent.As stated earlier, the main uses of the V AR are the impulse response analysis and the variance decomposition, which show the nature and direction of the relationship among the variables.The impulse response function and the variance decomposition tables are presented in Tables 3 and 4 below.Table 3 below represents the impulse response function. The impulse response function table traces the effect of a one standard deviation shock to one of the innovations on current and future values of the endogenous variables in the V AR model.Table 4 below presents the results of the variance decomposition. The result as presented decomposes variations in an endogenous variable into the component shocks to the endogenous variables in the V AR model.The result in Tables 3 and 4 represents the impulse response function results and the variance decomposition results. The interpretation of the results is straight forward. The question is that, what happened to PCI (a proxy for standard of living) if there is one standard deviation shock to FDI. The impulse response results in Table 3 show that a one standard deviation shock to FDI impacts significantly on living standard,measured by PCI. However, the impact is positively unstable. On the other hand, a better analysis of the magnitude and direction of impact between FDI and living standard is revealed by the results of the variance decomposition in Table 4 below. The table shows that initially 73.25 percent of variations in PCI were feedback effect, but reduces drastically to 8.44 percent and 9.41 percent in the 5th and 10th periods respectively.The impact of FDI on PCI was insignificant. Less than 1 percent in the first instance. However, in the variance decomposition of FDI, the results revealed that the contribution of FDI to variations in PCI (a measure of standard of living) was about 33.12 in the first period and diminishingly reduces to a low figure of 3.39 percent in the 10th period. This highly contradicts the apriori expectation of this studyThus, the major inference that can be drawn from the findings is that FDI impacts insignificantly on living standard in Nigeria.While the feedback effect on PCI (a measure of standard of living) reduces, the impact from other exogenous variables takes over except for the FDI. These other exogenous variables according to Akinmulegun (2011) include, Current Account Balance (CAB) and Index of openness (both proxies of globalization).5 Discussions, Conclusions and Policy RecommendationsThis study adopts a country specific-data in the analysis to allow for an indepth and elaborate investigation into the impact of FDI on standard of living as it relates to an individual nation-state. The variables are affected by each other from the results of the regression statistics tests, thus; they stand to explain changes in each other. Deduced from the findings is that FDI has insignificant impact on living standard in Nigeria with FDI accounting for less than 2 percent in the variations in PCI in the first instance, and less than 10 percent in the subsequent impact decomposition of FDI. This might not be unconnected with the small proportionate share by Nigeria from the slow proportion of FDI flows to sub- Saharan Africa and the appropriation of the little flows that accrued to Nigeria. When the investment of FDI into the domestic economy is majorly on white elephant projects that have no direct impact on what goes to the pockets of individual citizenry, one would not expect anything other than the resultsabove. Chantal and Patrick (2005) argued that the sector in which a country receives FDI affects the extent to which the country could realize its potential benefits. Furthermore, the results juxtapose the findings of Adams (2009); as the political environment in Nigeria over the years and the dilapidated infrastructural facilities serve as a bane to FDI growth-potential in the nation. Where over 80 percent of the FDI flows to Nigeria goes to oil sector alone, one will not expect the effect to be on the per capita income as the majority of the benefits are channel towards unproductive service sector, thus neglecting the industrial productive sectors.The findings of this study therefore leads us to accepting our Null hypothesis that FDI in Nigeria has no significant relationship with living standard. Thus, with the bi-directional relationship between FDI and PCI, the finding is consistent with theory and empirical literature. FDI is expected to have causal influence on standard of living, such that the past values of FDI should be able to help predict future values of PCI. This is in line with the previous findings (Adams, 2004; Fosu and Magnus, 2006) and therefore satisfies the objective of examining relationship between FDI and PCI of this study, however, the relationship is insignificant. This insignificant impact of FDI on PCI corroborates Ayadi (2009).The policy implication of this is that the past values of FDI can only predict the future values of PCI to a lesser extent.It is thus recommended that;i. Government should embark on policies that would attract more FDI to the dynamic products and sectors with high-income elasticities of demand.ii. FDI should be channeled to the production of secondary products, such that FDI be made to contribute positively to the living standard of Nigeria.iii. Government should redirect steps at making FDI (more importantly, Oil FDI) to contribute positively to the PCI through a well articulated policies that will develop non-oil sectors of the economy.Acknowledgements: I wish to acknowledge the contribution of the entire academic staffof Banking and Finance Department, Adekunle Ajasin University for the successful completion of this work. In addition, the comment of Professor J.A.Oloyede and Dr. T.M. Obamuyi is appreciated.二、文献综述作为技术溢出的外商直接投资文献综述摘要目前国内外学者主要是从外商直接投资和进口贸易两个方面研究技术溢出的效应。

对外直接投资对人民币国际化影响分析

对外直接投资对人民币国际化影响分析一、前言(一)研究背景近年来,我国成为世界贸易第一大国、世界对外投资第二大国,人民币开始在国际舞台崭露头角,并逐渐发挥重要的作用。

然而在新的国际形势下,国际间合作逐渐从贸易导向转变为投资导向,传统贸易方式驱动人民币国际化发展已经出现示弱趋势,开始初步探索投资驱动人民币国际化将成为今后一个时期重要发展方向。

“一带一路”发展布局不仅为对外直接投资提供丰富发展思路,也为人民币国际化带来全新发展契机。

(二)研究内容和方法本文主要以对外直接投资对人民币国际化直接和间接两方面促进作用为理论依据。

其中直接作用主要体现在由于对外直接投资是一个长期性质的经济活动,可以在一定时序期间不断增加人民币海外资本存量,并从融资、资金使用、资金回笼过程不断发生的货币兑换加速人民币使用的频率和范围,降低持有人民币的风险和成本,使其在国际资本流通过程中逐渐发挥重要职能。

间接作用主要是对外直接投资提升我国的对外贸易规模、改善我国的对外贸易结构,在这一前提条件下我国的贸易地位得以提升,人民币在贸易过程中逐步得到重视。

VAR模型作为重要的经济分析和预测方法,主要是针对选取的内生变量可能受到自身以及其他内生变量滞后值的影响建立起的模型。

方差分解分析是针对VAR回归分析所做的进一步结构性分析,能详细具体表示出不同结构冲击引起内生变量的变化幅度,并表示出一定时序期间影响程度的变化情况。

二、文献综述对外直接投资与人民币国际化关系的起步研究主要是针对较高的资本项目自由化程度有助于对外直接投资的发展,从而对人民币国际化产生积极影响。

肖丹丹和范爱军(2009)主要从以下角度叙述了对外直接投资对于人民币国际化的促进作用,首先是他们提出了用货币流通量作为货币国际化衡量标准,而对外投资活动是提高本国货币流通的重要方式;其次对外投资可以在一定程度上缓解贸易壁垒对进出口造成的影响,对稳定币值有一定积极影响,为货币国际化营造良好的外部环境。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

中国对外直接投资影响研究的文献综述作者:康珊珊来源:《对外经贸》2019年第03期摘要:中国对外直接投资规模巨大,学者对其影响效果进行了探讨。

通过对现有国内外文献进行梳理发现:我国对外直接投资能够产生反向技术外溢这一观点已在我国学术界达成基本共识;在讨论FDI对东道国影响方面研究结论并不一致,这可能是未考虑投资母国与东道国的差异引起的;而当固定探讨一国OFDI对东道国所产生的影响时,研究结果趋于一致,但东道国的异质性仍不可忽略。

关键词:对外直接投资;反向技术外溢;污染问题Abstract:China’s foreign direct investment is huge, and a large number of scholars have explored its effects. This paper intends to sort out the existing domestic and foreign literatures and finds that China’s foreign direct investment can prod uce reverse technology spillovers has reached a basic consensus in China’s academic circles; the conclusions of the research on the impact of FDI on the host country are not consistent, which may be unconsidered investment. The difference between the home country and the host country is caused; when the influence of a country’s OFDI on the host country is fixedly studied, the research results tend to be consistent, but the heterogeneity of the host country cannot be ignored.Keywords: Foreign Direct Investment; Reverse Technology Spillover; Pollution Paradise一、引言随着经济全球化的纵深发展,以外商直接投资(Foreign Direct Investment,即FDI)推动国家经济发展的观点日趋成熟。

根据《世界投资报告》,2017年中国对外投资额为1250亿美元,位居第三,仅次于美国和日本;在2016年,中国对外直接投资额达1830亿美元,超过日本排名世界第二,位于美国之后。

如此大规模的对外直接投资( Outward Foreign Direct Investment,即OFDI)会如何影响我国经济发展?更重要的是,承接FDI的东道国将会受到怎样的影响?对这些问题的讨论对于中国继续坚持对外开放的基本国策和树立负责任的大国形象十分重要。

近年来,随着全球环境问题的日益严峻以及新制度经济学的不断发展,东道国的环境质量和制度质量成为FDI流入效应的研究重点。

本文旨在从中国对外直接投资对中国的影响和对承接FDI东道国的影响两方面对国内外现有文献进行梳理,为未来研究中国对外直接投资影响提供新思路。

二、中国对外直接投资影响研究文献总结(一)中国对外直接投资对中国的影响研究理论认为随着一国对外投资活动的增多,跨国公司通过对外投资项目能够吸引和学习东道国有关的先进技术,降低生产成本,获得积极的反向外溢。

国内学者对中国FDI反向技术外溢效应的存在进行了大量的研究。

目前,中国对外直接投资可以通过各种传导机制获得东道国的反向技术外溢,从而提高我国企业的自主创新能力,这在我国学术界已达成基本共识(阙大学,2010;沙文兵,2012;孟青兰,2017)[1]-[3]。

毛其淋和许家云(2014)的研究结果表明中国OFDI与企业创新之间的因果效应显著,且OFDI对企业创新的促进作用是逐年递增的[4]。

蔡冬青和刘厚俊(2012)认为我国OFDI显著提高了我国企业的自主创新能力,而东道国优良的制度环境可通过与我国OFDI反向技术外溢的协同作用对我国的技术创新起到促进作用[5]。

张春萍(2012)、王恕立和向姣姣(2014)使用中国对外直接投资与进出口贸易的面板数据进行了实证研究,结果表明中国对外直接投资具有明显的进出口创造效应,但存在国别差异[6][7]。

接下来需要讨论的是哪些因素影响了反向技术外溢效应作用的发挥?技术外溢效应在各种产业之间的效果是否一致?国内学者对这些问题已经做出了尝试性研究,这将是今后中国对外直接投资对母国影响研究的新方向。

(二)中国对外直接投资对东道国的影响研究关于中国对外直接投资对东道国所产生的影响研究起步较晚,类似的研究侧重于讨论FDI 对东道国的影响,而FDI与OFDI之间联系紧密,因此对于FDI對东道国影响研究的文献梳理将有助于进一步理解中国OFDI对东道国的影响研究。

1.FDI 与东道国环境质量的研究综述FDI与东道国环境质量的关系主要有两类观点:第一种是“污染天堂”假说,假说认为那些面对国内严格环境规制的企业会为了节约成本而将高污染产业转移至其他环境标准较低的国家,进而导致了东道国环境质量的降低(Copeland和Taylor,1994)[8]。

Esty和Geradin (1997)还发现在国际竞争环境下,东道国会倾向于通过降低本国的环境标准来吸引更多的FDI,带来“竞次效应”[9]。

Baek(2016)、Lin(2017)、严雅雪和齐绍洲(2017)、张磊等(2018)的研究也从不同视角证明FDI会在某些程度上恶化东道国的环境污染,即承接FDI的东道国会成为“污染避难所”[10]-[13]。

另一种是“污染光环”假说,核心观点是FDI所带来的先进清洁技术和环境友好理念能通过技术外溢来推动东道国本土污染治理水平的提高,从而降低东道国环境污染(Birdsall和Wheeler,1993;刘玉博和汪恒,2016;Liu等,2017)[14]-[16]。

以中国为例,许和连和邓玉萍(2012)基于省际面板数据空间计量的研究表明:总体来说“污染天堂”假说在中国并不成立,FDI在空间地理上的集群是有利于改善中国环境的,其中来自全球离岸金融中心的外商投资更是显著降低了中国的环境污染[17]。

长期以来,国内外学者各持己见,但根据已有文献的回顾与梳理,不难发现研究结论的差异主要来自两方面:一方面是学者们在选取研究方法以及反映一国环境质量水平的核心指标上差异较大,这将极大干扰最终结论。

林季红和刘莹(2013)的研究发现若将环境规制视为严格外生变量,那么实证结果表明“污染天堂”假说在中国不成立,而一旦将其视为内生变量,则结果表明“污染天堂”假说在中国是成立的[18]。

另一方面,部分学者提出不能忽略了FDI来源国的差异,将一国的FDI总量视为一个整体进行研究。

事实上,不同来源国的FDI在投资进入方式(王明益,2014)[19]和投资进入动机(孙早等,2014)[20]等方面有明显不同,对东道国产生影响的能力和路径也并不一致,因此在研究时有必要将投资母国的异质性考虑在内。

基于此思路,刘乃全和戴晋(2017)运用多种估计方法来说明中国OFDI给“一带一路”沿线国家环境带来了“污染光环”效应,且这种效应不存在异质性[21]。

刘玉博和吴万宗(2017)让污染进入生产函数,实证结果表明中国OFDI规模的增长总体上促使东道国污染排放总量增加,但从人均排放的角度,中国OFDI显著降低了污染排放量,提高了东道国能源利用效率,改善了当地环境质量[22]。

显然,当从特定国家角度出发探讨一国OFDI对东道国环境质量所产生的影响时,研究结论的冲突有所降低。

2.FDI与东道国制度质量的研究综述关于FDI与东道国制度质量之间的关系,传统理论认为FDI的进入能够影响东道国的腐败程度与营商环境,从而改变东道国经济社会运行交易成本(Kwok和Tadesse,2006;Long等,2015)[23][24]。

和FDI与东道国环境质量关系的研究类似,学者们对于FDI的流入是对东道国制度质量产生了正向的积极影响还是负向的消极影响存在分歧。

但由于学者们在核心指标的选取上较为统一,采用世界治理指数(WGI)来衡量一个国家制度质量进行研究,因此结论争议主要来自于投资母国与东道国的差异。

使用WGI的研究结果表明FDI的流入能够整体提升东道国国家质量,但在制度质量维度上呈现出异质性(祖煜和李宗明,2018;黄玖立等,2018)[25][26]。

而关于投资母国与东道国差异带来的争议,潘春阳和廖佳(2018)的研究结果表明对于制度质量低于中国的东道国,中国的OFDI显著提高了制度质量,而对于制度质量高于中国的东道国,中国的OFDI则没有显著的制度效应[27]。

此外,Long等(2015)从中国企业微观调查数据出发,研究表明FDI的存在对不同地区税负下降与法制水平上升产生了积极影响[23]。

由上文可知,大多数文献将一国的FDI总量视为一个整体,忽略了FDI来源国差异。

而FDI与东道国之间的关系是复杂多维的,条件不同,得出的结论也不可一概而论,如不加区别地引入外资则有可能阻碍东道国的经济发展(黄建宏和蒲云,2004)[28]。

因此,继续将一国FDI视为一个同质整体进行研究将极大地影响结论的可信度,有必要从特定国家角度出发,探讨一国OFDI对东道国所产生的影响。

除研究OFDI与东道国环境(刘乃全和戴晋,2017;刘玉博和吴万宗,2017)[21][22]和制度之间的关系(潘春阳和廖佳,2018;祖煜和李宗明,2018)[25][27]之外,部分学者将关注点放在了行业出口、结构升级等方面。

郑磊和汪旭晖(2018)通过行业层面的实证检验发现美国OFDI对东道国行业出口强度的影响会因投资动机不同而明显不同。

其中,资源寻求型FDI对东道国出口强度起显著正向作用,出口平台型FDI能降低东道国企业沉没成本以提高其出口业绩[29]。

姜慧和孙玉琴(2018)通过动态面板门限模型发现东道国制度指标在影响东道国经济增长时,都存在显著的“单门槛效应”,只有跨越相应门槛值,中国OFDI才能给其经济增长带来积极的促进作用[30]。

贾妮莎和雷宏振(2019)基于开放经济国家产业结构升级的数理模型发现:中国OFDI整体上通过技术溢出、要素供给及生产率效应推动了“一带一路”沿线东道国国家的产业升级[31]。