财务管理Chap006

财务管理ppt英文课件Chapter 6

the firm is to experience problems meeting short-term obligations. Liquid assets frequently have lower rates of return than fixed assets.

➢ In the long run, all inputs of production (and hence costs) are variable.

➢ Financial accountants do not distinguish between variable costs and fixed costs. Instead, accounting costs usually fit into a classification that distinguishes product costs from period costs.

Copyright 2019 Prentice-Hall, Inc.

9

Debt versus Equity

Generally, when a firm borrows it gives the bondholders first claim on the firm’s cash flow.

Thus shareholder’s equity is the residual difference between assets and liabilities.

财务管理第六章ppt课件

30000

2

35000

3

60000

4

50000

5

40000

可编辑课件PPT

17

✓ 检验:贴现投资回收期是一个好的决策方法吗? ✓ 是否考虑了资金的时间价值? ✓ 是否考虑了未来现金流量的风险? ✓ 是否提供了关于价值创造方面的信息?

应将贴现投资回收期法作为 主要决策标准吗?

可编辑课件PPT

18

贴现投资回收期法的优势与不足

可编辑课件PPT

5

NPV 63120 70800 91080 165000 (112%)1 (112%)2 (112%)3

NPV=12,627.42

可编辑课件PPT

6

✓ 检验:NPV是一个好的决策标准吗?

✓ NPV是否考虑到了资金的时间价值? ✓ NPV是否考虑到了项目的投资风险? ✓ NPV是否提供了关于价值创造方面的信息?

23

内部报酬率的计算过程

✓ (1)如果每年的NCF相等 ✓ 计算年金现值系数

✓ 查年金现值系数表

✓ 采用插值法计算内部报酬率

✓ 例3:某投资项目在建设起点一次性投资的 254580元,当完工并投产,经营期为15年,每年 可获净现金流量50000元。按简单方法计算该项 目的内部收益率

可编辑课件PPT

✓ 计算前例中的IRR

NPV

70,000 60,000 50,000 40,000 30,000 20,000 10,000

0 -10,000 0 -20,000

0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2 0.22

可编辑D课件isPPcTount Rate

i 10.99%

财务管理课件4—6章

是公司发行的代表着股东享有平等的权利、义务,不加特 别限制,股利不固定的股票。

优先股:

是公司发行的授予持股者某些优先权利(主要是优先分配 股利权和优先索偿股本权)的股票。

(二)按票面有无记名分:记名股票和不记名股票

记名股票:

是票面上记载股东的姓名或者名称的股票。

不记名股票:

是股票票面上不记载股东的姓名或者名称的股票。

股票是股份公司为筹集权益资本而发行的有价证券, 是股份公司发给股东用来证明其在公司投资入股并借以 获得股利的书面凭证,它代表对公司的所有权。

股票就其性质而言是一种资本证券,是一种虚拟资 本,其主要特点有:

(1) 不返还性; (2)风险性 ; (3)流通性。Fra bibliotek二、股票的种类

(一)按股东的权利和义务分:普通股和优先股

在实务上,股票发行价格的计算,通常采用市盈率 法,具体计算公式为:

发行价格=每股净盈利×发行市盈率

但这还不是最终使用的发行价格。发行价格的最后 确定可以通过两种方式实现:竞价和协商。

▪四、股票发行的推销方式

股票推销 委托承销方式 自销方式 包销 代销

包销与代销方式对发行公司的风险

有利

不利

包销 可以促进股票顺利出 将股票以略低的价格

售,免于承担发行风 售给承销商,实际发

险;

行费用高;

代销 以略高的价格售给承 发行风险由发行公司 销商,实际发行费用 自己承担。 低;

▪ 五、股票上市 股票上市即公司股票在证券交易所挂牌交易。 将公司股票在证券交易所上市交易,是许多股份

公司梦寐以求的事情。但一家非上市公司要转化为上 市公司必须具备特别的条件,并办理相关的手续。这 些特别的条件就是上市标准,符合标准的允许上市, 不符合标准的则不能上市,已上市但条件恶化不能满 足标准要求的,还可终止上市。

财务管理课件4—6章

2.信托抵押债券,即以金融资产作为抵押品。 3.设备抵押债券,即以特定设备作为抵押品。

(二)无担保债券。即没有特定资产作担保,完全 凭借企业信用发行的一类债券,它代表的是一种对企 业收益而非资产的债权。尽管这种债券没有担保,但 债权人仍受到债券契约中各种限制性条款的保护,其 中最主要的是负抵押条款。

2.债券的偿还 根据债券契约,债券的偿还方式一般有以下几种:

(1)债券还本,包括到期一次还本和分期还本; (2)提前赎回; (3)偿债基金; (4)债券调换或换债,即发行新债券,收回旧债券; (5)债券转换,即通过投资者行使转换权来收回债 券。

第三节 可转换债券筹资

标普:AAA、 AA、 A; BBB、 BB、 B; CCC、 CC、 C 和 D;

穆迪: Aaa、 Aa、 A; Baa、 Ba、 B; Caa、 Ca、 C 。

其中,评级在BBB或Baa以上者属投资级债券,评 级在BB或Ba以下者属高风险债券或垃圾债券。

债券评级主要靠主观判断力,但也并非无的放矢。 一般来说,评定债券等级时,应综合考虑以下因素:

第四章 权益资本筹集

▪ 筹资是企业生存与发展的前提条件,也是企业财务

管理的重要课题之一。筹资决策的好与坏,直接影响着 企业的各项决策,甚至是企业的成与败。

▪ 按性质,企业筹资一般分为权益资本筹集和债务资 本筹集,两者在融资方式、决策方法等方面都大不相同, 故分别予以介绍。

第一节 融(或筹)资概述

▪ 一、融资的基本要求

但在我国,上市公司配股比例受到政府法规的严格 限定,即配股比例最多为10股配3股。这是导致我国众 多上市公司配股前往往实施送红股的派息方案的重要原 因。

财务管理学课件——第6章35页PPT文档

23.12.2019

8

营运资金概论

在确定性条件下,将企业的未来净现金流量时间表与 企业的债资务支付时间表进行精确的配比短是期适融当资的 相通产每对过通项应短过资,期长产与融资产即负期将债负到与融债期一资或日种,权配跟永益比它久性法的性资:到的本短期流融期日动资或大资。季致产节相长和性同期所的的融有流融资固动资定资工资产具

营运资金的分类(两类标准)

组成要素:如现金、有价证券、应收账款和存货 时间:永久性的和临时性的 A. 永久性营运资金(permanent working capital)是指满足

企业对流动资产的长期最低需要的那部分流动资产 B. 临时性营运资金(temporary working capital)是指随季节

营运资金管理的重要性

流动资产在企业总资产中的比重较高 过高的流动资产容易使企业只能获得较低的报酬率,过 低的流动资产又会使企业难以维持经营的稳定性 营运资金管理最终影响到企业的风险和收益

23.12.2019

3

营运资金概论

两个基本问题(这两个问题是相互依存的)

流动资产的最佳投资水平 为维持这一流动资产水平所需的短期融资和长期融资的 组合

红利

利息

债务本金 股票回购

流出

发行债券 发行普通股 发行优先股

流入

现金余额

购买

购买

出售 有价证券 Securities

折旧

固定资产

出售

存货

赊销

应收账款

现金销售

收账

现金和有价证券管理

加速现金回收

注:企业用来提高现金管理效率的各种收款和付款方法 构成一个整体,它们对企业现金管理的总体效率产生综 合影响。通常认为,企业将通过加速现金回收和推迟现 金支付而获益

(完整版)财务管理CHAPTER6(20201018150641)

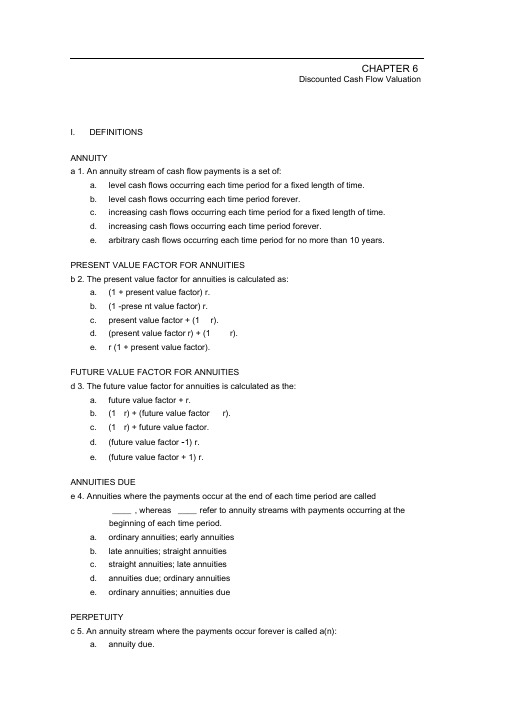

CHAPTER 6Discounted Cash Flow ValuationI. DEFINITIONSANNUITYa 1. An annuity stream of cash flow payments is a set of:a. level cash flows occurring each time period for a fixed length of time.b. level cash flows occurring each time period forever.c. increasing cash flows occurring each time period for a fixed length of time.d. increasing cash flows occurring each time period forever.e. arbitrary cash flows occurring each time period for no more than 10 years.PRESENT VALUE FACTOR FOR ANNUITIESb 2. The present value factor for annuities is calculated as:a. (1 + present value factor) r.b. (1 -prese nt value factor) r.c. present value factor + (1 r).d. (present value factor r) + (1 r).e. r (1 + present value factor).FUTURE VALUE FACTOR FOR ANNUITIESd 3. The future value factor for annuities is calculated as the:a. future value factor + r.b. (1 r) + (future value factor r).c. (1 r) + future value factor.d. (future value factor -1) r.e. (future value factor + 1) r.ANNUITIES DUEe 4. Annuities where the payments occur at the end of each time period are called____ , whereas ____ refer to annuity streams with payments occurring at thebeginning of each time period.a. ordinary annuities; early annuitiesb. late annuities; straight annuitiesc. straight annuities; late annuitiesd. annuities due; ordinary annuitiese. ordinary annuities; annuities duePERPETUITYc 5. An annuity stream where the payments occur forever is called a(n):a. annuity due.b. indemnity.c. perpetuity.d. amortized cash flow stream.e. amortization table.STATED INTEREST RATESa 6. The interest rate expressed in terms of the interest payment made each period is calledthe _________ rate.a. stated interestb. compound interestc. effective annuald. periodic intereste. daily interestEFFECTIVE ANNUALRATEc 7. The interest rate expressed as if it were compounded once per year is called the rate.a. stated interestb. compound interestc. effective annuald. periodic intereste. daily interestANNUAL PERCENTAGE RATEb 8. The interest rate charged per period multiplied by the number of periods per year is calledthe _________ rate.a. effective annualb. annual percentagec. periodic interestd. compound intereste. daily interestPURE DISCOUNT LOANd 9. A loan where the borrower receives money today and repays a single lump sum at sometime in the future is called a(n) _________ loan.a. amortizedb. continuousc. balloond. pure discounte. interest-onlyINTEREST-ONLY LOANe 10. A loan where the borrower pays interest each period and repays the entire principal ofthe loan at some point in the future is called a(n) _____ loan.a. amortizedb. continuousc. balloond. pure discounte. interest-onlyAMORTIZED LOANa 11. A loan where the borrower pays interest each period, and repays some or all of theprincipal of the loan over time is called a(n) ____ loan.a. amortizedb. continuousc. balloond. pure discounte. interest-onlyBALLOON LOANc 12. A loan where the borrower pays interest each period, repays part of the principal of theloan over time, and repays the remainder of the principal at the end of the loan, iscalled a(n) ______ loan.a. amortizedb. continuousc. balloond. pure discounte. interest-onlyII. CONCEPTSORDINARY ANNUITY VERSUS ANNUITY DUEc 13. You are comparing two annuities which offer monthly payments for ten years. Both annuities are identical with the exception of the payment dates. Annuity A pays on the first of each month while annuity B pays on the last day of each month. Which one ofthe following statements is correct concerning these two annuities?a. Both annuities are of equal value today.b. Annuity B is an annuity due.c. Annuity A has a higher future value than annuity B.d. Annuity B has a higher present value than annuity A.e. Both annuities have the same future value as of ten years from today.UNEVENCASH FLOWS ANDPRESENT VALUEb 14. You are comparing two investment options. The cost to invest in either option is thesame today. Both options will provide you with $20,000 of income. Option A pays fiveannual payments starting with $8,000 the first year followed by four annual payments of $3,000 each. Option B pays five annual payments of $4,000 each. Which one of thefollowing statements is correct given these two investment options?a. Both options are of equal value given that they both provide $20,000 of income.b. Option A is the better choice of the two given any positive rate of return.c. Option B has a higher present value than option A given a positive rate of return.d. Option B has a lower future value at year 5 than option A given a zero rate of return.e. Option A is preferable because it is an annuity due.UNEVENCASH FLOWS ANDFUTURE VALUEa 15. You are considering two projects with the following cash flows:Project A Project BYear 1 $2,500 $4,000Year 2 3,000 3,500Year 3 3,500 3,000Year 4 4,000 2,500Which of the follow ing stateme nts are true concerning these two projects?I. Both projects have the same future value at the end of year 4, give n a positive rateof return.II. Both projects have the same future value give n a zero rate of retur n.III. Both projects have the same future value at any point in time, given a positive rate of return.IV. Project A has a higher future value tha n project B, give n a positive rate of return.a. II on lyb. IV onlyc. I and III onlyd. II a nd IV onlye. I, II, and III o nlyPERPETUITY VERSUS ANNUITYd 16. A perpetuity differs from an annuity because:a. perpetuity payme nts vary with the rate of in flati on.b. perpetuity payme nts vary with the market rate of in terest.c. perpetuity payme nts are variable while ann uity payme nts are con sta nt.d. perpetuity payme nts n ever cease.e. ann uity payme nts n ever cease.ANNUAL PERCENTAGE RATEe 17. Which one of the following statements concerning the annual percentage rate is correct?a. The annual perce ntage rate con siders in terest on in terest.b. The rate of in terest you actually pay on a loa n is called the annual perce ntage rate.c. The effective annual rate is lower tha n the annual perce ntage rate whe n an in terest rateis compo un ded quarterly.d. When firms advertise the annual percentage rate they are violating U.S. truth-inlending laws.e. The annual perce ntage rate equals the effective annual rate whe n the rate on an account is desig nated as simple in terest.INTEREST RATESb 18. Which one of the following statements concerning interest rates is correct?a. The stated rate is the same as the effective annual rate.b. An effective annual rate is the rate that applies if interest were charged annually.c. The annual percentage rate increases as the number of compounding periods per yearincreases.d. Banks prefer more frequent compounding on their savings accounts.e. For any positive rate of interest, the effective annual rate will always exceed the annualpercentage rate.EFFECTIVE ANNUAL RATEc 19. Which of the following statements concerning the effective annual rate are correct?I. When making financial decisions, you should compare effective annual rates rather thanannual percentage rates.II. The more frequently interest is compounded, the higher the effective annual rate.III. A quoted rate of 6 percent compounded continuously has a higher effective annual rate than if the rate were compounded daily.IV. When choosing which loan to accept, you should select the offer with the highest effective annual rate.a. I and II onlyb. I and IV onlyc. I, II, and III onlyd. II, III, and IV onlye. I, II, III,and IVCONTINUOUS COMPOUNDINGd 20. The highest effective annual rate that can be derived from an annual percentage rate of9 percent is computed as:a. .09e -1. .09b. e q.c. e (1 + .09).d. e.09-1.e. (1 + .09)q.PURE DISCOUNT LOAN a 21. A pure discount loan is a(n):a. example of a present value problem.b. loan that is interest-free.c. loan that gives you a discount if you pay your payments on time.d. loan that requires all interest to be paid at the time the loan is made.e. loan that discounts the payments if you pay them in advance.INTEREST-ONLY LOANc 22. The principle amount of an interest-only loan is:a. never repaid.b. repaid in equal increments and included in each loan payment.c. repaid in full at the end of the loan period.d. repaid in equal annual payments even when the loan interest is repaid monthly.e. repaid in increasing increments and included in each loan payment.AMORTIZED LOANb 23. An amortized loan:a. requires the principle amount to be repaid in even increments over the life of the loan.b. may have equal or increasing amounts applied to the principle from each loan payment.c. requires that all interest be repaid on a monthly basis while the principle is repaid at theend of the loan term.d. requires that all payments be equal in amount and include both principle and interest.e. is the type of loan that describes most corporate bonds.III. PROBLEMSORDINARY ANNUITY AND PRESENT VALUEd 24. Your parents are giving you $100 a month for four years while you are in college. At a6 percent discount rate, what are these payments worth to you when you first startcollege?a. $3,797.40b. $4,167.09c. $4,198.79d. $4,258.03e. $4,279.32ORDINARY ANNUITYAND PRESENT VALUEb 25. You just won the lottery! As your prize you will receive $1,200 a month for 100 months. If youcan earn 8 percent on your money, what is this prize worth to you today?a. $87,003.69b. $87,380.23c. $87,962.77d. $88,104.26e. $90,723.76ORDINARY ANNUITYAND PRESENT VALUE b 26. Todd is able to pay $160 a month for five years for a car. If the interest rate is 4.9 percent, how much can Todd afford to borrow to buy a car?a. $6,961.36b. $8,499.13c. $8,533.84d. $8,686.82e. $9,588.05ORDINARY ANNUITYAND PRESENT VALUEa 27. You are the beneficiary of a life insurance policy. The insurance company informs you thatyou have two options for receiving the insurance proceeds. You can receive a lump sumof $50,000 today or receive payments of $641 a month for ten years. You can earn 6.5percent on your money. Which option should you take and why?a. You should accept the payments because they are worth $56,451.91 today.b. You should accept the payments because they are worth $56,523.74 today.c. You should accept the payments because they are worth $56,737.08 today.d. You should accept the $50,000 because the payments are only worth $47,757.69 today.e. You should accept the $50,000 because the payments are only worth $47,808.17 today.ORDINARY ANNUITYAND PRESENT VALUEc 28.Your employer contributes $25 a week to your retirement plan. Assume that you work foryour employer for another twenty years and that the applicable discount rate is 5 percent.Given these assumptions, what is this employee benefit worth to you today?a. b. $13,144.43 $15,920.55c. d. $16,430.54 $16,446.34e. $16,519.02ORDINARY ANNUITYAND PRESENT VALUEa 29. You have a sub-contracting job with a local manufacturing firm. Your agreement calls forannual payments of $50,000 for the next five years. At a discount rate of 12 percent, what is this job worth to you today?a. b. $180,238.81 $201,867.47c. d. $210,618.19 $223,162.58e. $224,267.10ANNUITY DUE AND PRESENT VALUEb 30. The Ajax Co. just decided to save $1,500 a month for the next five years as a safety netfor recessionary periods. The money will be set aside in a separate savings accountwhich pays 3.25 percent interest compounded monthly. They deposit the first $1,500today. If the company had wanted to deposit an equivalent lump sum today, how muchwould they have had to deposit?a. b. $82,964.59 $83,189.29c.d.e. $83,428.87 $83,687.23 $84,998.01ANNUITY DUE AND PRESENT VALUEb 31. You need some money today and the only friend you have that has any is your‘ miserly ' friend. He agrees to loan you the money you need, if you make payments of $20 a month for the next six month. In keeping with his reputation, he requires that thefirst payment be paid today. He also charges you 1.5 percent interest per month. Howmuch money are you borrowing?a. b.c. d.e. $113.94 $115.65 $119.34 $119.63 $119.96ANNUITY DUE AND PRESENT VALUEc 32. You buy an annuity which will pay you $12,000 a year for ten years. The paymentsare paid on the first day of each year. What is the value of this annuity today at a 7percent discount rate?a. b.c. d.e. $84,282.98 $87,138.04 $90,182.79 $96,191.91 $116,916.21ORDINARY ANNUITY VERSUS ANNUITY DUEa 33. You are scheduled to receive annual payments of $10,000 for each of the next 25years. Your discount rate is 8.5 percent. What is the difference in the present value if you receive these payments at the beginning of each year rather than at the end ofeach year?a. b. $8,699 $9,217c. d. $9,706 $10,000e. $10,850ORDINARY ANNUITY VERSUS ANNUITY DUEd 34. You are comparing two annuities with equal present values. The applicable discountrate is 7.5 percent. One annuity pays $5,000 on the first day of each year for twentyyears. How much does the second annuity pay each year for twenty years if it pays at the end of each year?a. b. c.d. e. $4,651 $5,075 $5,000 $5,375 $5,405ORDINARY ANNUITY VERSUS ANNUITY DUEa 35. Martha receives $100 on the first of each month. Stewart receives $100 on the lastday of each month. Both Martha and Stewart will receive payments for five years. Atan 8 percent discount rate, what is the difference in the present value of these twosets of payments?a. b. $32.88 $40.00c.d.e. $99.01 $108.00 $112.50ORDINARY ANNUITYAND FUTURE VALUEWhat is the future value of $1,000 a year for five years at a 6 percent rate of interest? $4,212.36 $5,075.69 $5,637.09 $6,001.38 $6,801.91c 36.a.b.c.d.e.ORDINARY ANNUITYAND FUTURE VALUE d 37. What is the future value of $2,400 a year for three years at an 8 percent rate of interest?a. $6,185.03b. $6,847.26c. $7,134.16d. $7,791.36e. $8,414.67ORDINARY ANNUITYAND FUTURE VALUEc 38. Janet plans on saving $3,000 a year and expects to earn 8.5 percent. How much willJanet have at the end of twenty-five years if she earns what she expects?a. $219,317.82b. $230,702.57c. $236,003.38d. $244,868.92e. $256,063.66ANNUITY DUE VERSUS ORDINARY ANNUITYb 39. Toni adds $3,000 to her savings on the first day of each year. Tim adds $3,000 to hissavings on the last day of each year. They both earn a 9 percent rate of return. Whatis the difference in their savings account balances at the end of thirty years?a. $35,822.73b. $36,803.03c. $38,911.21d. $39,803.04e. $40,115.31ORDINARY ANNUITY PAYMENTSd 40. You borrow $5,600 to buy a car. The terms of the loan call for monthly payments for fouryears at a 5.9 percent rate of interest. What is the amount of each payment?a. $103.22b. $103.73c. $130.62d. $131.26e. $133.04ORDINARY ANNUITY PAYMENTS AND COST OF INTERESTc 41. You borrow $149,000 to buy a house. The mortgage rate is 7.5 percent and the loanperiod is 30 years. Payments are made monthly. If you pay for the house accordingto the loan agreement, how much total interest will you pay?a. $138,086b. $218,161c. $226,059d. $287,086e. $375,059ORDINARY ANNUITY PAYMENTS AND FUTURE VALUEd 42. The Great Giant Corp. has a management contract with their newly hired president. The contract requires a lump sum payment of $25 million be paid to the president upon the completion of her first ten years of service. The company wants to set asideanequal amount of funds each year to cover this anticipated cash outflow. The companycan earn 6.5 percent on these funds. How much must the company set aside each year for this purpose?a. $1,775,042.93b. $1,798,346.17c. $1,801,033.67d. $1,852,617.25e. $1,938,018.22ORDINARY ANNUITY PAYMENTS AND PRESENT VALUEe 43. You retire at age 60 and expect to live another 27 years. On the day you retire, you have$464,900 in your retirement savings account. You are conservative and expect toearn 4.5 percent on your money during your retirement. How much can you withdrawfrom your retirement savings each month if you plan to die on the day you spendyour last penny?a. $2,001.96b. $2,092.05c. $2,398.17d. $2,472.00e. $2,481.27ORDINARY ANNUITY PAYMENTS AND PRESENT VALUEc 44. The McDonald Group purchased a piece of property for $1.2 million. They paid a downpayment of 20 percent in cash and financed the balance. The loan terms requiremonthly payments for 15 years at an annual percentage rate of 7.75 percentcompounded monthly. What is the amount of each mortgage payment?a. $7,440.01b. $8,978.26c. $9,036.25d. $9,399.18e. $9,413.67ORDINARY ANNUITY PAYMENTS AND PRESENT VALUEd 45. You estimate that you will have $24,500 in student loans by the time you graduate. Theinterest rate is 6.5 percent. If you want to have this debt paid in full within five years,how much must you pay each month?a. $471.30b. $473.65$476.79$479.37$480.40c. d. e.ORDINARY ANNUITY PAYMENTS AND PRESENT VALUEb 46. You are buying a previously owned car today at a price of $6,890. You are paying$500 down in cash and financing the balance for 36 months at 7.9 percent. What isthe amount of each loan payment?a. b.c. d.e. $198.64 $199.94 $202.02 $214.78 $215.09ORDINARY ANNUITY PAYMENTS AND PRESENT VALUEb 47. The Good Life Insurance Co. wants to sell you an annuity which will pay you $500per quarter for 25 years. You want to earn a minimum rate of return of 5.5 percent.What is the most you are willing to pay as a lump sum today to buy this annuity?a. b.c. d.e. $26,988.16 $27,082.94 $27,455.33 $28,450.67 $28,806.30ANNUITY DUE PAYMENTSAND PRESENT VALUEc 48. Your car dealer is willing to lease you a new car for $299 a month for 60 months.Payments are due on the first day of each month starting with the day you sign thelease contract. If your cost of money is 4.9 percent, what is the current value of thelease?a. b. $15,882.75 $15,906.14c. d. $15,947.61 $16,235.42e. $16,289.54ANNUITY DUE PAYMENTS AND PRESENT VALUEd 49. Your great-aunt left you an inheritance in the form of a trust. The trust agreementstates that you are to receive $2,500 on the first day of each year, startingimmediately and continuing for fifty years. What is the value of this inheritancetoday if the applicable discount rate is 6.35 percent?a. b. c.d. e. $36,811.30 $37,557.52 $39,204.04 $39,942.42 $40,006.09ANNUITY DUE PAYMENTS AND PRESENT VALUEe 50. You recently filed suit against a company. Today, you received three settlement optionsas follows:Option A: $10,000 on the first day of each year for 25 yearsOption B: $880 on the first day of each month for 25 yearsOption C: $119,830 as a lump sum payment todayYou can earn 7.5 percent on your investments. You do not care if you personallyreceive the funds or if they are paid to your heirs should you die within the next 25years. Which one of the following statements is correct given this information?a. Option C is clearly the best choice since you can earn 7.5 percent on the entirelump sum starting immediately.b. Option B is clearly the best choice since it offers the largest number of payments.c. Option A is clearly the best choice since it has by far the largest future value.d. Option B is clearly the best choice since it has by far the largest present value.e. You are relatively indifferent to the three options as they are all approximately equalin value to you.ANNUITY DUE PAYMENTSAND FUTURE VALUEa 51. Your firm wants to save $250,000 to buy some new equipment three years from now.The plan is to set aside an equal amount of money on the first day of each yearstarting today. The firm can earn a 4.7 percent rate of return. How much does thefirm have to save each year to achieve their goal?a. $75,966.14b. $76,896.16c. $78,004.67d. $81.414.14e. $83,333.33ANNUITY DUE PAYMENTSAND FUTURE VALUEe 52. Today is January 1. Starting today, Sam is going to contribute $140 on the first of eachmonth to his retirement account. His employer contributes an additional 50 percentof the amount contributed by Sam. If both Sam and his employer continue to dothis and Sam can earn a monthly rate of ? of 1 percent, how much will he have inhis retirement account 35 years from now?a. $199,45.944.b. $200,456.74c. $249,981.21d. $299,189.16e. $300,685.11ORDINARY ANNUITY TIME PERIODS AND PRESENT VALUEc 53. You are considering an annuity which costs $100,000 today. The annuity pays $6,000 ayear. The rate of return is 4.5 percent. What is the length of the annuity timeperiod?a. 24.96 yearsb. 29.48 yearsc. 31.49 yearsd. 33.08 yearse. 38.00 yearsORDINARY ANNUITY TIME PERIODS AND PRESENT VALUEd 54. Today, you signed loan papers agreeing to borrow $4,954.85 at 9 percentcompounded monthly. The loan payment is $143.84 a month. How many loanpayments must you make before the loan is paid in full?a. b.c. d.e. 29.89 36.00 38.8840.0041.03ORDINARY ANNUITY TIME PERIODS AND FUTURE VALUEa 55. Winston Enterprises would like to buy some additional land and build a new factory.The anticipated total cost is $136 million. The owner of the firm is quite conservativeand will only do this when the company has sufficient funds to pay cash for the entireexpansion project. Management has decided to save $450,000 a month for thispurpose. The firm earns 6 percent compounded monthly on the funds it saves. Howlong does the company have to wait before expanding its operations?a. b. 184.61 months 199.97 monthsc.d.e. 234.34 months 284.61 months 299.97 monthsANNUITY DUE TIME PERIODS AND PRESENT VALUEb 56. Today, you are retiring. You have a total of $413,926 in your retirement savings andhave the funds invested such that you expect to earn an average of 3 percent,compounded monthly, on this money throughout your retirement years. You want towithdraw $2,500 at the beginning of every month, starting today. How long will it beuntil you run out of money?a. b.c. d.e. 185.00 months 213.29 months 227.08 months 236.84 months 249.69 monthsANNUITY DUE TIME PERIODSc 57. The Bad Guys Co. is notoriously known as a slow-payer. They currently need toborrow $25,000 and only one company will even deal with them. The terms of theloancall for daily payments of $30.76. The first payment is due today. The interest rate is21 percent compounded daily. What is the time period of this loan?a. b. c. 2.88 years2.94 years3.00 yearsd. 3.13 yearse. 3.25 yearsORDINARY ANNUITY INTEREST RATEc 58. The Robertson Firm is considering a project which costs $123,900 to undertake. The project will yieldcash flows of $4,894.35 monthly for 30 months. What is the rate of return on this project?a. 12.53 percentb. 13.44 percentc. 13.59 percentd. 14.02 percente. 14.59 percentORDINARY ANNUITY INTEREST RATEa 59. Your insurance agent is trying to sell you an annuity that costs $100,000 today. By buying this annuity, your agent promises that you will receive payments of $384.40 amonth for the next 40 years. What is the rate of return on this investment?a. 3.45 percentb. 3.47 percentc. 3.50 percentd. 3.52 percente. 3.55 percentORDINARY ANNUITY INTEREST RATEe 60. You have been investing $120 a month for the last 15 years. Today, your investment account is worth$47,341.19. What is your average rate of return on your investments?a. 9.34 percentb. 9.37 percentc. 9.40 percentd. 9.42 percente. 9.46 percentORDINARY ANNUITY INTEREST RATEc 61. Brinker, Inc. has been investing $136,000 a year for the past 4 years into a business venture. Today,Brinker sold that venture for $685,000. What is their rate of return on this venture?a. 9.43 percentb. 11.06 percentc. 15.59 percentd. 16.67 percente. 18.71 percentANNUITY DUE INTEREST RATEb 62. Your mother helped you start saving $25 a month beginning on your 10 th birthday.She always made you make your deposit on the first day of each month just to“ start the month out right ” . Today, you turn 21 and have $4,482.66 in your account. What is your rate of return on your savings?a. b.c. d.e. 5.25 percent 5.29 percent 5.33 percent 5.36 percent 5.50 percentANNUITY DUE INTERESTRATEa 63. Today, you turn 21. Your birthday wish is that you will be a millionaire by your 40th birthday. In anattempt to reach this goal, you decide to save $25 a day, every day until you turn 40. You openan investment account and deposit your first $25 today. What rate of return must you earn toachieve your goal?a. b.c. d. 15.07 percent 15.13 percent 15.17 percent 15.20 percente. 15.24 percentUNEVENCASH FLOWS ANDPRESENT VALUEb 64.Marko, Inc. is considering the purchase of ABC Co. Marko believes that ABC Co. can generatecash flows of $5,000, $9,000, and $15,000 over the next three years, respectively. After that time, they feel the business will be worthless. Marko has determined that a 14 percent rate of return is applicable to this potential purchase. What is Marko willing to pay today to buy ABC Co.?a. b. $19,201.76 $21,435.74c. d. $23,457.96 $27,808.17e. $31,758.00UNEVEN CASH FLOWS ANDPRESENT VALUEa 65.You are considering two savings options. Both options offer a 4 percent rate of return. The firstoption is to save $1,200, $1,500, and $2,000 a year over the next three years, respectively. Theother option is to save one lump sum amount today. If you want to have the same balance in your savings at the end of the three years, regardless of the savings method you select, how much do you need to save today if you select the lump sum option?a. b. c.d. $4,318.67 $4,491.42 $4,551.78 $4,607.23e. $4,857.92UNEVEN CASH FLOWS ANDPRESENT VALUEYou are considering two insurance settlement offers. The first offer includes annual payments of $5,000, $7,500, and $10,000 over the next three years, respectively.The other offer is the payment of one lump sum amount today. You are trying todecide which offer to accept given the fact that your discount rate is 5 percent. Whatis the minimum amount that you will accept today if you are to select the lump sumoffer?$19,877.67$20,203.00$21,213.15$23,387.50$24,556.88b 66.a. b. c. d. e.。

财务管理Chap0ppt课件

Net Working Capital

Current Liabilities

Long-Term Debt

How should short-term assets be managed and financed?

Shareholders’ Equity

精选课件ppt

1-8

The Financial Manager

Corporation

Shares can be easily exchanged

Partnership

Subject to substantial restrictions

Voting Rights

Usually each share gets one vote

Taxation

Double

Reinvestment and dividend payout

3. How should current assets be managed and financed?

精选课件ppt

1-5

The Capital Budgeting Decision

Current Assets

Current Liabilities

Long-Term Debt

Fixed Assets 1 Tangible 2 Intangible

◦Treasurer

Cash flow, capital expenditure, capital structure

◦ Controller

Accounting, information systems, taxes

精选课件ppt

1-9

Hypothetical Organization Chart

财务管理学》第六章

a.可动用的银行贷款指标; b.准备很快变现的长期资产; c.偿债能力的信誉。

B.减少变现能力的因素:

a.未作记录的或有负债;

PPT文档演模板

财务管理学》第六章

思考

• 有哪些方法可以在短期内提高公司的 流动比率?

PPT文档演模板

财务管理学》第六章

2.1.2 长期偿债能力分析

2.4 其他常见比率分析

1. 每股盈余

2. 市盈率

3. 每股股利

PPT文档演模板

财务管理学》第六章

4. 股票获利率 5. 股利支付率 6. 股利保障倍数

PPT文档演模板

财务管理学》第六章

7. 留存盈余比率 8. 每股净资产 9. 净资产倍率

PPT文档演模板

财务管理学》第六章

2.5 现金流量分析

公司适应经济环境变化和利用投资的能力。

PPT文档演模板

财务管理学》第六章

5. 收益质量分析

•经营所得现金=经营净收益+非付现费用

PPT文档演模板

财务管理学》第六章

3. 财务综合分析

1. 纵向比较 2. 横向比较 3. 理想的财务报表 4. 财务综合分析方法

PPT文档演模板

财务管理学》第六章

• 3.4.1 杜邦财务分析模型

结合流动比率指标,我们可以认为该企业 存货管理较差。

PPT文档演模板

财务管理学》第六章

3. 现金比率

假设行业平均值为:0.553。反映公司直 接偿付流动负债的能力较行业平均水平略低

于行业平均水平。但这一比率过高意味着公 司流动负债未进行合理地运用。

PPT文档演模板

财务管理学》第六章

4. 其他影响短期偿债能力的因素

公司财务管理课件第六章

营业杠杆只是对这种不确定性的放大作用. 反映的是企业经营的"潜在风险",这种风险 只有在销售和生产成本的变动性存在的条件 下才会实际地产生作用

财务杠杆

▪ 不论企业营业利润多少,债务的利息和优先 股的股利通常都不是不变的.当息税前利润 增大时,每1元盈余所负担的固定财务费用 就会相对减少,这能给普通股股东带来更多 的盈余;

750 000 1 000 000 1 000 000

普通股股数〔股〕 20 000

30 000

20 000

发行新股发行价25元,10 000股,普通股股本增加10 000元资本供给增加15 000元

▪

▪

项目

增发股票

▪ 预计息税前利润〔EBIT> 减:利息 税前利润 减:所得税〔50%〕

▪ 净利润 普通股股数

息税前利润―每股利润分析法

▪ 将息税前利润〔EBIT〕和每股利润 〔EPS〕联系起来,分析资金结构与每股 利润之间的关系,进而来确定合理的资金 结构的方法,简写为EBIT—EPS分析法.这 种方法因为要确定每股利润的无差异点, 所以又叫每股利润无差异点法.

▪ 例题:华特公司目前有资金75万元,因生产 需要在筹资25万元,可利用发行股票也可利 用放行债券筹集,具体数据如下.

案例分析

▪ 项目A、B、C、D、E 的投资总额为7200万 元,不超过总预算额; 而且,最低内含报酬率 11.3%大于最高边际资 本成本11.16%,故上述

五个项目可组成最佳 资本预算

▪ 各个项目的风险水平 差异可能会导致资本 预算的调整.还要考虑 股权、控制权稀释等, 而不愿意发行新股

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

年金:等额、定期的系列收支。

如:分期付款、购房按揭、付养老金等 按收付款发生时间的不同分为: •预付年金 •递延年金 •永续年金 •普通年金

McGraw-Hill/Irwin

所以,预付年金的现值=普通年金的现值×(1+r)

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

递延年金的现值 (有两种方法)

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

t

McGraw-Hill/Irwin

A(1+r)2

2

A1 r

2

A1 r

t 1

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

普通年金的终值 (1)

FVAt A A1 r A1 r A1 r

普通年金终值与

复利终值的关系

普通年金终值是 多笔复利终值之和

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

普通年金的终值 0 1 A 2 A 3 A A A(1+r) A(1+r)2

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

实际年利率

Hale Waihona Puke McGraw-Hill/Irwin

所以

r R 1 1 m

m

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

FIGURE 6.5

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

普通年金的现值

0

1

A

2

A

3

A

A(1+r)-1

A(1+r)-2

A(1+r)-3

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

各年利率(不)相等

A0 A1 A2 A3 At-1 At

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

1

等式两边同乘(1+r)

(t 1)

(2)

PVAt r A1 1 r

McGraw-Hill/Irwin

(2)-(1)

t

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

1 (1 r ) t PVAt A r

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

FIGURE 6.6

4.普通年金的现值

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

2

t 1

等式两边同乘(1+r) (2)

FVAt 1 r A1 r A1 r A1 r

2 t

t

(2)-(1)

FVAt r A A1 r

t

1 式中 ( r ) 1 r

( r )t 1 1 即 FVAt A r

PVAt A( r) A( r) A( r) 1 1 1

推广至t期

1 2

1

2

3

PVAt A( r) A( r ) A( r ) (1) 1 1 1

t

PVAt 1 r A A( r) A( r) 1 1

1 (1 r ) t 式中 是 r

普通年金为1元,利率为r,经过t期的年 金现值,可据此编制“年金现值系数表” (见附表A-3)

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

多笔不等额现金流量现值的计算

年金和多笔不等额现金流量混合情况下的 现值 计息期短于1年时间价值的计算

贴现率的计算

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

年金的分类

•普通年金 (后付年金) •预付年金 (先付年金) •递延年金 m期 •永续年金

McGraw-Hill/Irwin

0

1 A 1 A

2 A 2 A n期

3 A 3

0 A

未来

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

FIGURE 6.1

先付年金的终值

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

FIGURE 6.4

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

1.普通年金的终值

A A(1+r)

FVAt A A1 r A1 r

推广(N次): FVA A A 1 r

FIGURE 6.2

普通年金的终值

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

FIGURE 6.3

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

多笔现金流量的现值和终值

A1, A2, A3, A4,

r

t FVA

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

•递延年金 m期

n期

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

永续年金的现值 由普通年金的现值

1 (1 r ) t PVAt A r

当t

1 永续年金的现值 PVAt A r

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

2、预付年金的终值

0 A 1 A 2 A A(1+r) A(1+r)2 A(1+r)3 所以,预付年金的终值=

McGraw-Hill/Irwin

3

普通年金的终值×(1+r)

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Six

Discounted Cash Flow Valuation

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

单笔现金流量的现值和终值

Pv

r

t

Fv

多笔现金流量的现值和终值

A1, A2, A3, A4,r

t FVA

所以,在其他条件相同的情况下,一年 内利息复合计算的次数越多,未来值就越大。

McGraw-Hill/Irwin

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

令n=1,则 1年的利息

I1 FV1 PV0

m r PV0 1 1 m m r PV0 1 1 m I1 r PV0 PV0