公司金融课后习题罗斯

【公司理财】罗斯,中文第六版课后习题详细解答05

第三部分未来现金流量估价第5章估价导论:货币的时间价值财务管理中最重要的问题之一是:未来将收到的现金流量,它在今天的价值是多少?答案取决于货币的时间价值,这也是该章的主题。

第6章贴现现金流量估价本章拓展第5章的基本结论,讨论多期现金流量的估价。

我们考虑了许多相关的问题,包括贷款估价、贷款偿付额的计算以及报酬率的决定。

第7章利率债券是一种非常重要的金融工具。

该章示范如何利用第6章的估价技术来决定债券的价格,我们讲述债券的基本特点,以及财经报章如何报道债券的价格。

我们还将考察利率对债券价格的影响。

第8章股票估价第三部分的最后一章考察股票价格的确定,讨论普通股和优先股的重要特点,例如股东的权利,该章还考察了股票价格的报价。

第5 章估价导论:货币的时间价值◆本章复习与自测题5.1 计算终值假定今天你在一个利率为6%的账户存了10 000美元。

5年后,你将有多少钱?5.2 计算现值假定你刚庆祝完19岁生日。

你富有的叔叔为你设立了一项基金,将在你30岁时付给你150 000美元。

如果贴现率是9%,那么今天这个基金的价值是多少?5.3 计算报酬率某项投资可以使你的钱在10年后翻一番。

这项投资的报酬率是多少?利用72法则来检验你的答案是否正确。

5.4 计算期数某项投资将每年付给你9%的报酬。

如果你现在投资15 000美元,多长时间以后你就会有30 000美元?多长时间以后你就会有45 000美元?◆本章复习与自测题解答5.1 我们需要计算在6%的利率下,10 000美元在5年后的终值。

终值系数为:1.065= 1.3382终值为:10 000美元×1.3382 = 13 382.26美元。

5.2 我们要算出在9%的利率下,11年后支付的150 000美元的现值。

贴现系数为:1/(1.09)11= 1/2.5804 = 0.3875这样,现值大约是58 130美元。

5.3 假定你现在投资1 000美元,10年后,你将拥有2 000美元。

罗斯《公司理财》(第9版)课后习题(第1~3章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第1章公司理财导论一、概念题1.资本预算(capital budgeting)答:资本预算是指综合反映投资资金来源与运用的预算,是为了获得未来产生现金流量的长期资产而现在投资支出的预算。

资本预算决策也称为长期投资决策,它是公司创造价值的主要方法。

资本预算决策一般指固定资产投资决策,耗资大,周期长,长期影响公司的产销能力和财务状况,决策正确与否影响公司的生存与发展。

完整的资本预算过程包括:寻找增长机会,制定长期投资战略,预测投资项目的现金流,分析评估投资项目,控制投资项目的执行情况。

资本预算可通过不同的资本预算方法来解决,如回收期法、净现值法和内部收益率法等。

2.货币市场(money markets)答:货币市场指期限不超过一年的资金借贷和短期有价证券交易的金融市场,亦称“短期金融市场”或“短期资金市场”,包括同业拆借市场、银行短期存贷市场、票据市场、短期证券市场、大额可转让存单市场、回购协议市场等。

其参加者为各种政府机构、各种银行和非银行金融机构及公司等。

货币市场具有四个基本特征:①融资期限短,一般在一年以内,最短的只有半天,主要用于满足短期资金周转的需要;②流动性强,金融工具可以在市场上随时兑现,交易对象主要是期限短、流动性强、风险小的信用工具,如票据、存单等,这些工具变现能力强,近似于货币,可称为“准货币”,故称货币市场;③安全性高,由于货币市场上的交易大多采用即期交易,即成交后马上结清,通常不存在因成交与结算日之间时间相对过长而引起价格巨大波动的现象,对投资者来说,收益具有较大保障;④政策性明显,货币市场由货币当局直接参加,是中央银行同商业银行及其他金融机构的资金连接的主渠道,是国家利用货币政策工具调节全国金融活动的杠杆支点。

货币市场的交易主体是短期资金的供需者。

需求者是为了获得现实的支付手段,调节资金的流动性并保持必要的支付能力,供应者提供的资金也大多是短期临时闲置性的资金。

公司理财第九版罗斯课后案例答案 Case Solutions Corporate Finance

公司理财第九版罗斯课后案例答案 Case Solutions CorporateFinance1. 案例一:公司资金需求分析问题:一家公司需要资金支持其新项目。

通过分析现金流量,推断该公司是否需要向外部借款或筹集其他资金。

解答:为了确定公司是否需要外部资金,我们需要分析公司的现金流量状况。

首先,我们需要计算公司的净现金流量(净收入加上非现金项目)。

然后,我们需要将净现金流量与项目的投资现金流量进行对比。

假设公司预计在项目开始时投资100万美元,并在项目运营期为5年。

预计该项目每年将产生50万美元的净现金流量。

现在,我们需要进行以下计算:净现金流量 = 年度现金流量 - 年度投资现金流量年度投资现金流量 = 100万美元年度现金流量 = 50万美元净现金流量 = 50万美元 - 100万美元 = -50万美元根据计算结果,公司的净现金流量为负数(即净现金流出),意味着公司每年都会亏损50万美元。

因此,公司需要从外部筹集资金以支持项目的运营。

2. 案例二:公司股权融资问题:一家公司正在考虑通过股权融资来筹集资金。

根据公司的财务数据和资本结构分析,我们需要确定公司最佳的股权融资方案。

解答:为了确定最佳的股权融资方案,我们需要参考公司的财务数据和资本结构分析。

首先,我们需要计算公司的资本结构比例,即股本占总资本的比例。

然后,我们将不同的股权融资方案与资本结构比例进行对比,选择最佳的方案。

假设公司当前的资本结构比例为60%的股本和40%的债务,在当前的资本结构下,公司的加权平均资本成本(WACC)为10%。

现在,我们需要进行以下计算:•方案一:以新股发行筹集1000万美元,并将其用于项目投资。

在这种方案下,公司的资本结构比例将发生变化。

假设公司的股本增加至80%,债务比例减少至20%。

根据资本结构比例的变化,WACC也将发生变化。

新的WACC可以通过以下公式计算得出:新的WACC = (股本比例 * 股本成本) + (债务比例 * 债务成本)假设公司的股本成本为12%,债务成本为8%:新的WACC = (0.8 * 12%) + (0.2 * 8%) = 9.6%•方案二:以新股发行筹集5000万美元,并将其用于项目投资。

公司理财-罗斯课后习题答案.doc

第一章1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

高比重的机构所有权导致高学历的股东和管理层讨论决策风险项目。

此外,机构投资者比私人投资者可以根据自己的资源和经验更好地对管理层实施有效的监督机制。

Cha08罗斯公司理财第九版原版书课后习题

Cha08罗斯公司理财第九版原版书课后习题Earlier in the chapter, we saw how bonds were rated based on their credit risk. What you will find if you start looking at bonds of different ratings is that lower-rated bonds have higher yields.We stated earlier in this chapter that a bond’s yield is calculated assuming that all the promised payments will be made. As a result, it is really a promised yield, and it may or may not be what you will earn. In particular, if the issuer defaults, your actual yield will be lower, probably much lower. This fact is particularly important when it comes to junk bonds. Thanks to a clever bit of marketing, such bonds are now commonly called high-yield bonds, which has a much nicer ring to it; but now you recognize that these are really high promised yield bonds.Next, recall that we discussed earlier how municipal bonds are free from most taxes and, as a result, have much lower yields than taxable bonds. Investors demand the extra yield on a taxable bond as compensation for the unfavorable tax treatment. This extra compensation is the taxability premium.Finally, bonds have varying degrees of liquidity. As we discussed earlier, there are an enormous number of bond issues, most of which do not trade on a regular basis. As a result, if you wanted to sell quickly, you would probably not get as good a price as you could otherwise. Investors prefer liquid assets to illiquid ones, so they demand a liquidity premium on top of all the other premiums we have discussed. As a result, all else being the same, less liquid bonds will have higher yields than more liquid bonds.ConclusionIf we combine everything we have discussed, we find that bond yields represent the combined effect of no fewer than six factors. The first is the real rate of interest. On top of the real rate are five premiums representing compensation for (1) expected future inflation, (2) interest rate risk, (3) default risk, (4) taxability, and (5) lack of liquidity. As a result, determining the appropriate yield on a bond requires careful analysis of each of these factors.Summary and ConclusionsThis chapter has explored bonds, bond yields, and interest rates. We saw that:1. Determining bond prices and yields is an application of basic discounted cash flow principles.2. Bond values move in the direction opposite that of interest rates, leading to potential gains orlosses for bond investors.3. Bonds are rated based on their default risk. Some bonds, such as Treasury bonds, have no riskof default, whereas so-called junk bonds have substantial default risk.4. Almost all bond trading is OTC, with little or no market transparency in many cases. As a result,bond price and volume information can be difficult to find for some types of bonds.5. Bond yields and interest rates reflect six different factors: the real interest rate and fivepremiums that investors demand as compensation for inflation, interest rate risk, default risk, taxability, and lack of liquidity.In closing, we note that bonds are a vital source of financing to governments and corporations of all types. Bond prices andyields are a rich subject, and our one chapter, necessarily, touches on only the most important concepts and ideas. There is a great deal more we could say, but, instead, we will move on to stocks in our next chapter.Concept Questions1. Treasury Bonds Is it true that a U.S. Treasury security is risk-free?2. Interest Rate Risk Which has greater interest rate risk, a 30-year Treasury bond or a 30-year21. Using Bond Quotes Suppose the following bond quote for IOU Corporation appears in thefinancial page of today’s newspaper. Assume the bond has a face value of $1,000 and the current date is April 15, 2010. What is the yield to maturity of the bond? What is the current yield?22. Finding the Maturity You’ve just found a 10 percent coupon bond on the market that sells forpar value. What is the maturity on this bond?CHALLENGE (Questions 23–30)23. Components of Bond Returns Bond P is a premium bond with a 9 percent coupon. Bond D isa 5 percent coupon bond currently selling at a discount. Both bonds make annual payments, havea YTM of 7 percent, and have five years to maturity. What is the current yield for Bond P? For BondD? If interest rates remain unchanged, what is the expected capital gains yield over the next year for Bond P? For Bond D? Explain your answers and the interrelationship among the various types of yields.24. Holding Period Yield The YTM on a bond is the interest rate you earn on your investment ifinterest rates don’t change. If you actually sell the bond before it matures, your realized return is known as the holding period yield (HPY).1. Suppose that today you buy a 9 percent annual coupon bond for $1,140. The bond has 10years to maturity. What rate of return do you expect to earn on your investment?2. Two years from now, the YTM on your bond has declined by 1 percent, and you decide tosell. What price will your bond sell for? What is the HPY on your investment? Compare this yield to the YTM when you first bought the bond. Why are they different?25. Valuing Bonds The Morgan Corporation has two different bonds currently outstanding. Bond Mhas a face value of $20,000 and matures in 20 years. The bond makes no payments for the first six years, then pays $800 every six months over the subsequent eight years, and finally pays $1,000 every six months over the last six years. Bond N also has a face value of $20,000 and a maturity of20 years; it makes no coupon payments over the life of the bond. If the required return on boththese bonds is 8 percent compounded semiannually, what is the current price of Bond M? Of Bond N?26. R eal Cash Flows When Marilyn Monroe died, ex-husband Joe DiMaggio vowed to place freshflowers on her grave every Sunday as long as he lived. The week after she died in 1962, a bunch of fresh flowers that the former baseball player thought appropriate for the star cost about $8.Based on actuarial tables, “Joltin’ Joe” could expect to live for 30 years after the actress died.Assume that the EAR is 10.7 percent. Also, assume that the price of the flowers will increase at 3.5 percent per year, when expressed as an EAR. Assuming that each year has exactly 52 weeks, what is the present value of this commitment? Joe began purchasing flowers the week after Marilyn died.27. Real Cash Flows You are planning to save for retirement over the next 30 years. To save forretirement, you will invest $800 a month in a stock account in real dollars and $400 a month in a bond account in real dollars. The effective annual return of the stock account is expected to be 12 percent, and the bond account will earn 7 percent. Whenyou retire, you will combine your money into an account with an 8 percent effective return. The inflation rate over this period is expected to be 4 percent. How much can you withdraw each month from your account in real terms assuminga 25-year withdrawal period? What is the nominal dollar amount of your last withdrawal?28. Real Cash Flows Paul Adams owns a health club in downtown Los Angeles. He charges hiscustomers an annual fee of $500 and has an existing customer base of 500. Paul plans to raise the annual fee by 6 percent every year and expects the club membership to grow ata constant rate of3 percent for the next five years. The overall expenses of running the health club are $75,000 ayear and are expected to grow at the inflation rate of 2 percent annually. After five years, Paul2. How many of the coupon bonds must East Coast Yachts issue to raise the $40 million? Howmany of the zeroes must it issue?3. In 20 years, what will be the principal repayment due if East Coast Yachts issues the couponbonds? What if it issues the zeroes?4. What are the company’s considerations in iss uing a coupon bond compared to a zero couponbond?5. Suppose East Coast Yachts issues the coupon bonds witha make-whole call provision. Themake-whole call rate is the Treasury rate plus .40 percent. If East Coast calls the bonds in 7 years when the Treasury rate is 5.6 percent, what is the call price of the bond? What if it is 9.1 percent?6. Are investors really made whole with a make-whole call provision?7. After considering all the relevant factors, would you recommend a zero coupon issue or aregular coupon issue? Why? Would you recommend an ordinary call feature or a make-whole call feature? Why?。

《corporate finance》罗斯版英文版 Chapter 06书本课后习题及答案

Chapter 061.The changes in a firm's future cash flows that are a direct consequence of accepting a project arecalled _____ cash flows.A. i ncrementalB. s tand-aloneC. o pportunityD. n et present valueE. e rosion2.The annual annuity stream of payments with the same present value as a project's costs is calledthe project's _____ cost.A. i ncrementalB. s unkC. o pportunityD. e rosionE. e quivalent annual3. A cost that has already been paid, or the liability to pay has already been incurred, is a(n):A. s alvage value expense.B. n et working capital expense.C. s unk cost.D. o pportunity cost.E. e rosion cost.4.The most valuable investment given up if an alternative investment is chosen is a(n):A. s alvage value expense.B. n et working capital expense.C. s unk cost.D. o pportunity cost.E. e rosion cost.5. A decrease in a firm’s current cash flows resulting from the implementation of a new project isreferred to as:A. s alvage value expenses.B. n et working capital expenses.C. s unk costs.D. o pportunity costs.E. e rosion costs.6.The depreciation method currently allowed under U.S. tax law governing the accelerated write-offof property under various lifetime classifications is called _____ depreciation.A. F IFOB. M ACRSC. s traight-lineD. s um-of-years digitsE. c urvilinear7.The cash flow tax savings generated as a result of a firm's tax-deductible depreciation expense iscalled the:A. a ftertax depreciation savings.B. d epreciable basis.C. d epreciation tax shield.D. o perating cash flow.E. a ftertax salvage value.8.The cash flow from a project is computed as the:A. n et operating cash flow generated by the project, less any sunk costs and erosion costs.B. s um of the incremental operating cash flow and aftertax salvage value of the project.C. n et income generated by the project, plus the annual depreciation expense.D. s um of the incremental operating cash flow, capital spending, and net working capital cashflows incurred by the project.E. s um of the sunk costs, opportunity costs, and erosion costs of the project.9.Interest rates or rates of return on investments that have been adjusted for the effects of inflationare called _____ rates.A. r ealB. n ominalC. e ffectiveD. s trippedE. c oupon10.The increase you realize in buying power as a result of owning an investment is referred to as the_____ rate of return.A. i nflatedB. r ealizedC. n ominalD. r ealE. r isk-free11.The pro forma income statement for a cost reduction project:A. w ill reflect a reduction in the sales of the firm.B. w ill generally reflect no incremental sales.C. h as to be prepared reflecting the total sales and expenses of the entire firm.D. c annot be prepared due to the lack of any project related sales.E. w ill always reflect a negative project operating cash flow.12.One purpose of identifying all of the incremental cash flows related to a proposed project is to:A. i solate the total sunk costs so they can be evaluated to determine if the project will add valueto the firm.B. e liminate any cost which has previously been incurred so that it can be omitted from theanalysis of the project.C. m ake each project appear as profitable as possible for the firm.D. i nclude both the proposed and the current operations of a firm in the analysis of the project.E. i dentify any and all changes in the cash flows of the firm for the past year so they can beincluded in the analysis.13.Sunk costs include any cost that:A. w ill change if a project is undertaken.B. w ill be incurred if a project is accepted.C. h as previously been incurred and cannot be changed.D. w ill be paid to a third party and cannot be refunded for any reason whatsoever.E. w ill occur if a project is accepted and once incurred, cannot be recouped.14.You spent $500 last week fixing the transmission in your car. Now, the brakes are acting up andyou are trying to decide whether to fix them or trade the car in for a newer model. In analyzing the brake situation, the $500 you spent fixing the transmission is a(n) _____ cost.A. o pportunityB. f ixedC. i ncrementalD. s unkE. r elevant15.Erosion can be explained as the:A. a dditional income generated from the sales of a newly added product.B. l oss of current sales due to a new project being implemented.C. l oss of revenue due to employee theft.D. l oss of revenue due to customer theft.E. l oss of cash due to the expenses required to fix a parking lot after a heavy rain storm.16.Which one of these is an example of erosion that should be included in project analysis?A. T he anticipated loss of current sales when a new product is launched.B. T he expected decline in sales as a new product ages.C. T he reduction in your sales that occurs when a competitor introduces a new product.D. T he sudden loss of sales due to a major employer in your community implementing massivelayoffs.E. T he reduction in sales price that will most likely be required to sell inventory that has aged.17.Which one of the following should be excluded from the analysis of a project?A. e rosion costsB. i ncremental fixed costsC. i ncremental variable costsD. s unk costsE. o pportunity costs18.All of the following are anticipated effects of a proposed project. Which of these should be considered when computing the cash flow for the final year of a project?A. o perating cash flow and salvage valuesB. s alvage values and net working capital recoveryC.operating cash flow, net working capital recovery, salvage valuesD. n et working capital recovery and operating cash flowE.operating cash flow only19.Changes in the net working capital:A. c an affect the cash flows of a project every year of the project's life.B. o nly affect the initial cash flows of a project.C. a re included in project analysis only if they represent cash outflows.D. a re generally excluded from project analysis due to their irrelevance to the total project.E. a ffect the initial and the final cash flows of a project but not the cash flows of the middle years.20.The net working capital of a firm will decrease if there is:A. a decrease in accounts payable.B. a n increase in inventory.C. a decrease in accounts receivable.D. a n increase in the firm's checking account balance.E. a decrease in fixed assets. working capital:A. c an be ignored in project analysis because any expenditure is normally recouped by the end ofthe project.B. r equirements generally, but not always, create a cash inflow at the beginning of a project.C. e xpenditures commonly occur at the end of a project.D. i s frequently affected by the additional sales generated by a new project.E. i s the only expenditure where at least a partial recovery can be made at the end of a project.22.A company which uses the MACRS system of depreciation:A. w ill have equal depreciation costs each year of an asset's life.B. w ill expense the largest percentage of the cost during an asset’s first year of life.C. c an depreciate the cost of land, if it so desires.D. w ill write off the entire cost of an asset over the asset's class life.E. c annot expense any of the cost of a new asset during the first year of the asset's life.23.Champion Toys just purchased some MACRS 5-year property at a cost of $230,000. TheMACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively. The book value of the asset as of the end of Year 2 can be calculated as:A. $230,000 × (1 −.20 −.32).B. $230,000 × ([1 - (.20 × .32)].B. $230,000 × (1 - .20) × (1 - .32).C. $230,000 / (1 - .20 - .32).D. $230,000 - ($230,000 × .20 × .32).24.Pete’s Garage just purchased some equipment at a cost of $650,000. What is the propermethodology for computing the depreciation expense for Year 3 if the equipment is classified as 5-year property for MACRS? The MACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively.A. $650,000 ×(1 − .20) ×(1 −.32) ×(1 −.192)B. $650,000 ×(1 − .20) ×(1 −.32)C. $650,000 ×(1 − .20) ×(1 − .32) × .192)D. $650,000 ×(1 −.192)E. $650,000 ×.19225.The book value of an asset is primarily used to compute the:A. a nnual depreciation tax shield.B. a mount of cash received from the sale of an asset.C. a mount of tax saved annually due to the depreciation expense.D. a mount of tax due on the sale of an asset.E. c hange in depreciation needed to reflect the market value of the asset.26.The salvage value of an asset creates an aftertax cash flow in an amount equal to the:A. s ales price of the asset.B. s ales price minus the book value.C. s ales price minus the tax due based on the sales price minus the book value.D. s ales price plus the tax due based on the sales price minus the book value.E. s ales price plus the tax due based on the book value minus the sales price.27.The pretax salvage value of an asset is equal to the:A. b ook value if straight-line depreciation is used.B. b ook value if MACRS depreciation is used.C. m arket value minus the book value.D. b ook value minus the market value.E. m arket value.28.A project's operating cash flow will increase when the:A. d epreciation expense increases.B. s ales projections are lowered.C. i nterest expense is lowered.D. n et working capital requirement increases.E. e arnings before interest and taxes decreases.29.The cash flows of a project should:A. b e computed on a pretax basis.B. i nclude all sunk costs and opportunity costs.C. i nclude all incremental and opportunity costs.D. b e applied to the year when the related expense or income is recognized by GAAP.E. i nclude all financing costs related to new debt acquired to finance the project.30.Assume a firm has no interest expense or extraordinary items. Given this, the operating cash flow can be computed as:A. E BIT - Taxes.B. E BIT × (1 - Tax rate) + Depreciation × Tax rate.C. (Sales - Costs) × (1 - Tax rate).D. E BIT - Depreciation + Taxes.E.Net income + Depreciation.31.The bottom-up approach to computing the operating cash flow applies only when:A. b oth the depreciation expense and the interest expense are equal to zero.B. t he interest expense is equal to zero.C. t he project is a cost-cutting project.D. n o fixed assets are required for the project.E. t axes are ignored and the interest expense is equal to zero.32.The top-down approach to computing the operating cash flow:A. i gnores all noncash items.B. a pplies only if a project produces sales.C. c an only be used if the entire cash flows of a firm are included.D. i s equal to Sales −Costs −Taxes + Depreciation.E. i ncludes the interest expense related to a project.33.For a profitable firm, an increase in which one of the following will increase the operating cashflow?A. e mployee salariesB. o ffice rentC. b uilding maintenanceD. d epreciationE. e quipment rental34.Tax shield refers to a reduction in taxes created by:A. a reduction in sales.B. a n increase in interest expense.C. n oncash expenses.D. a project's incremental expenses.E. o pportunity costs.35.A project which is designed to improve the manufacturing efficiency of a firm but will generate noadditional sales revenue is referred to as a(n) _____ project.A. s unk costB. o pportunityC. c ost-cuttingD. r evenue-cuttingE. r evenue-generating36.Toni's Tools is comparing machines to determine which one to purchase. The machines sell fordiffering prices, have differing operating costs, differing machine lives, and will be replaced when worn out. These machines should be compared using:A. n et present value only.B. b oth net present value and the internal rate of return.C. t heir equivalent annual costs.D. t he depreciation tax shield approach.E. t he replacement parts approach.37.The equivalent annual cost method is useful in determining:A. t he annual operating cost of a machine if the annual maintenance is performed versus whenthe maintenance is not performed as recommended.B. t he tax shield benefits of depreciation given the purchase of new assets for a project.C. o perating cash flows for cost-cutting projects of equal duration.D. w hich one of two machines to acquire given equal machine lives but unequal machine costs.E. w hich one of two machines to purchase when the machines are mutually exclusive, havedifferent machine lives, and will be replaced once they are worn out.38.Marshall's purchased a corner lot five years ago at a cost of $498,000 and then spent $63,500 ongrading and drainage so the lot could be used for storing outdoor inventory. The lot was recently appraised at $610,000. The company now wants to build a new retail store on the site. Thebuilding cost is estimated at $1.1 million. What amount should be used as the initial cash flow for this building project?A. $1,661,500B. $1,100,000C. $1,208,635D. $1,710,000E. $1,498,00039.Samson's purchased a lot four years ago at a cost of $398,000. At that time, the firm spent$289,000 to build a small retail outlet on the site. The most recent appraisal on the propertyplaced a value of $629,000 on the property and building. Samson’s now wants to tear down the original structure and build a new strip mall on the site at an estimated cost of $2.3 million. What amount should be used as the initial cash flow for new project?A. $2,987,000B. $2,242,000C. $2,058,000D. $2,300,000E. $2,929,00040.Jamestown Ltd. currently produces boat sails and is considering expanding its operations toinclude awnings. The expansion would require the use of land the firm purchased three years ago at a cost of $142,000 that is currently valued at $137,500. The expansion could use someequipment that is currently sitting idle if $6,700 of modifications were made to it. The equipment originally cost $139,500 six years ago, has a current book value of $24,700, and a current market value of $39,000. Other capital purchases costing $780,000 will also be required. What is the amount of the initial cash flow for this expansion project?A. $953,400B. $962,300C. $948,900D. $927,800E. $963,20041.The Boat Works currently produces boat sails and is considering expanding its operations toinclude awnings. The expansion would require the use of land the firm purchased three years ago at a cost of $197,000 that is currently valued at $209,500. The expansion could use someequipment that is currently sitting idle if $7,500 of modifications were made to it. The equipment originally cost $387,500 five years ago, has a current book value of $132,700, and a current market value of $139,000. Other capital purchases costing $520,000 will also be required. What is the value of the opportunity costs that should be included in the initial cash flow for theexpansion project?A. $425,000B. $485,000C. $329,700D. $348,500E. $537,20042.Walks Softly sells customized shoes. Currently, it sells 14,800 pairs of shoes annually at anaverage price of $59 a pair. It is considering adding a lower-priced line of shoes that will be priced at $39 a pair. Walks Softly estimates it can sell 6,000 pairs of the lower-priced shoes but will sell 3,500 less pairs of the higher-priced shoes by doing so. What annual sales revenue should be used when evaluating the addition of the lower-priced shoes?A. $27,500B. $24,000C. $31,300D. $789,100E. $900,70043.Foamsoft sells customized boat shoes. Currently, it sells 16,850 pairs of shoes annually at anaverage price of $79 a pair. It is considering adding a lower-priced line of shoes which sell for $49a pair. Foamsoft estimates it can sell 5,000 pairs of the lower-priced shoes but will sell 1,250 lesspairs of the higher-priced shoes by doing so. What is the estimated value of the erosion cost that should be charged to the lower-priced shoe project?A. $138,750B. $146,250C. $98,750D. $52,000E. $123,24044.Sue purchased a house for $89,000, spent $56,000 upgrading it, and currently had it appraised at$212,900. The house is being rented to a family for $1,200 a month, the maintenance expenses average $200 a month, and the property taxes are $4,800 a year. If she sells the house she will incur $20,000 in expenses. She is considering converting the house into professional officespace. What opportunity cost, if any, should she assign to this property if she has been renting it for the past two years? A. $178,500A. $120,000B. $185,000C. A NSD. $192,900D. $232,90045.Jamie's Motor Home Sales currently sells 1,100 Class A motor homes, 2,200 Class C motorhomes, and 2,800 pop-up trailers each year. Jamie is considering adding a mid-range camper and expects that if she does so she can sell 1,500 of them. However, if the new camper is added, Jamie expects that her Class A sales will decline to 850 units while the Class C camper sales decline to 2,000. The sales of pop-ups will not be affected. Class A motor homes sell for anaverage of $140,000 each. Class C homes are priced at $59,500 and the pop-ups sell for $5,000 each. The new mid-range camper will sell for $42,900. What is the erosion cost of adding the mid-range camper?A. $54,250,000B. $46,900,000C. $53,750,000D. $63,150,000E. $78,750,00046.Ernie's Electrical is evaluating a project which will increase sales by $50,000 and costs by$30,000. The project will cost $150,000 and will be depreciated straight-line to a zero book value over the 10-year life of the project. The applicable tax rate is 34 percent. What is the operating cash flow for this project?A. $19,200B. $15,000C. $21,300D. $17,900E. $18,30047.Kurt's Cabinets is looking at a project that will require $80,000 in fixed assets and another$20,000 in net working capital. The project is expected to produce sales of $110,000 withassociated costs of $70,000. The project has a 4-year life. The company uses straight-line depreciation to a zero book value over the life of the project. The tax rate is 35 percent. What is the operating cash flow for this project?A. $7,000B. $13,000C. $27,000D. $33,000E. $40,00048.Peter's Boats has sales of $760,000 and a profit margin of 5 percent. The annual depreciationexpense is $80,000. What is the amount of the operating cash flow if the company has no long-term debt?A. $34,000B. $86,400C. $118,000D. $120,400E. $123,90049.Samoa's Tools has sales of $760,000 and a profit margin of 8 percent. The annual depreciationexpense is $50,000. What is the amount of the operating cash flow if the company has no long-term debt?A. $50,000B. $60,800C. $110,800D. $810,000E. $930,00050.Le Place has sales of $439,000, depreciation of $32,000, and net working capital of $56,000. Thefirm has a tax rate of 34 percent and a profit margin of 6 percent. The firm has no interestexpense. What is the amount of the operating cash flow?A. $49,384B. $52,616C. $54,980D. $58,340E. $114,34051.The By-Way has sales of $435,000, costs of $254,000, depreciation of $35,000, interest expenseof $22,000, and taxes of $43,400. What is the amount of the operating cash flow?A. $115,600B. $157,900C. $137,600D. $322,100E. $114,34052.Ben's Border Café is considering a project that will produce sales of $16,000 and increase cashexpenses by $10,000. If the project is implemented, taxes will increase from $23,000 to $24,500 and depreciation will increase from $4,000 to $5,500. What is the amount of the operating cash flow using the top-down approach?A. $4,000B. $4,500C. $6,000D. $7,500E. $8,50053.Camille's Café is considering a project that will not produce any sales but will decrease cashexpenses by $12,000. If the project is implemented, taxes will increase from $23,000 to $24,500 and depreciation will increase from $4,000 to $5,500. What is the amount of the operating cash flow using the top-down approach?A. $15,000B. $10,500C. $5,500D. $17,500E. $13,50054.Ronnie's Coffee House is considering a project which will produce sales of $6,000 and increasecash expenses by $2,500. If the project is implemented, taxes will increase by $1,300. The additional depreciation expense will be $1,000. An initial cash outlay of $2,000 is required for net working capital. What is the amount of the operating cash flow using the top-down approach?A. $200B. $1,500C. $2,200D. $3,500E. $4,20055.A project will increase sales by $60,000 and cash expenses by $51,000. The project will cost$40,000 and will be depreciated using straight-line depreciation to a zero book value over the 4-year life of the project. The company has a marginal tax rate of 35 percent. What is the operating cash flow of the project using the tax shield approach?A. $5,850B. $8,650C. $9,350D. $9,700E. $10,35056.A project will increase sales by $140,000 and cash expenses by $95,000. The project will cost$100,000 and will be depreciated using the straight-line method to a zero book value over the 4-year life of the project. The company has a marginal tax rate of 34 percent. What is the value of the depreciation tax shield?A. $8,500B. $17,000C. $22,500D. $25,000E. $37,75057.Lee's Furniture just purchased $24,000 of fixed assets that are classified as 5-year MACRSproperty. The MACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively. What is the amount of the depreciation expense for the third year?A. $2,304B. $2,507C. $2,765D. $4,608E. $4,80058.Lew just purchased $67,600 of equipment that is classified as 5-year MACRS property. TheMACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively. What will the book value of this equipment be at the end of four years should he decide to resell the equipment at that point in time?A. $11,681.28B. $18,280.20C. $17,040.00D. $19,468.80E. $22,672.0059.Northern Enterprises just purchased $1,900 of fixed assets that are classified as 3-year MACRSproperty. The MACRS rates are 33.33 percent, 44.44 percent, 14.82 percent, and 7.41 percent for Years 1 to 4, respectively. What is the amount of the depreciation expense for Year 2?A. $562.93B. $633.27C. $719.67D. $844.36E. $1,477.6360.The Galley purchased some 3-year MACRS property two years ago at a cost of $19,800. TheMACRS rates are 33.33 percent, 44.44 percent, 14.82 percent, and 7.41 percent. The firm no longer uses this property so is selling it today at a price of $13,500. What is the amount of the pretax profit on the sale?A. $11,140.48B. $9,098.46C. $10,500.00D. $8,016.67E. $10,702.4061.Three years ago, you purchased some 5-year MACRS equipment at a cost of $135,000. TheMACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively. You sold the equipment today for $82,500. Which of these statements is correct if your tax rate is 34 percent?A. T he tax due on the sale is $14,830.80.B. T he book value today is $40,478.C. T he book value today is $37,320.D. T he taxable amount on the sale is $47,380.E. T he tax refund from the sale is $13,219.20.62.Custom Cars purchased some $39,000 of fixed assets two years ago that are classified as 5-yearMACRS property. The MACRS rates are 20 percent, 32 percent, 19.2 percent, 11.52 percent,11.52 percent, and 5.76 percent for Years 1 to 6, respectively. The tax rate is 34 percent. If theassets are sold today for $19,000, what will be the aftertax cash flow from the sale?A. $16,358.88B. $17,909.09C. $18,720.00D. $18,904.80E. $19,000.0063.Winslow Motors purchased $225,000 of MACRS 5-year property. The MACRS rates are 20percent, 32 percent, 19.2 percent, 11.52 percent, 11.52 percent, and 5.76 percent for Years 1 to 6, respectively. The tax rate is 34 percent. If the firm sells the asset after five years for $10,000, what will be the aftertax cash flow from the sale?A. $8,993.60B. $8,880.20C. $11,006.40D. $7,770.40E. $12,892.0064.A project is expected to create operating cash flows of $26,500 a year for four years. The initialcost of the fixed assets is $62,000. These assets will be worthless at the end of the project. An additional $3,000 of net working capital will be required throughout the life of the project. What is the project's net present value if the required rate of return is 12 percent?A. $19,208.11B. $14,028.18C. $15,306.09D. $17,396.31E. $21,954.1765.A project will produce operating cash flows of $45,000 a year for four years. During the life of theproject, inventory will be lowered by $30,000 and accounts receivable will increase by $15,000.Accounts payable will decrease by $10,000. The project requires the purchase of equipment at an initial cost of $120,000. The equipment will be depreciated straight-line to a zero book value over the life of the project. The equipment will be salvaged at the end of the project creating a $25,000 aftertax cash inflow. At the end of the project, net working capital will return to its normal level. What is the net present value of this project given a required return of 15 percent?A. $23,483.48B. $16,117.05C. $24,909.09D. $22,037.86E. $19,876.0266.A project will produce an operating cash flow of $7,300 a year for three years. The initialinvestment for fixed assets will be $11,600, which will be depreciated straight-line to zero over the asset’s 4-year life. The project will require an initial $500 in net working capital plus an additional $500 every year with all net working capital levels restored to their original levels when the project ends. The fixed assets can be sold for an estimated $2,500 at the end of the project, the tax rate is 34 percent, and the required rate of return is 12 percent. What is the net present value of the project?A. $7,532.27B. $9,896.87C. $7,072.72D. $6,353.41E. $8,398.2967.Matty's Place is considering the installation of a new computer system that will cut annualoperating costs by $12,000. The system will cost $42,000 to purchase and install. This system is expected to have a 5-year life and will be depreciated to zero using straight-line depreciation.What is the amount of the earnings before interest and taxes for each year of this project?A. −$20,400B. $5,400C. $3,600D. $12,000E. $8,400。

公司金融——罗斯版7

本章复习与自测题解答

8.1 上一笔股利D0为2美元,预期股利将稳定地以8%的比率增长,而且必要报酬率为16%。根据股利增长模型,目前 的价格为: P0 = D1/(R-g) = D0×(1 + g)/(R-g) = 2美元×(1.08)/(0.16 -0.08) = 2.16 美元/0.08 = 27 美元 我们可以计算 5 年后的股利,然后再利用股利增长模型求出 5 年后的股票价格。我们还可以根据股价每年增长 8% ,直 接计算5年后的股价。我们两种方法都做。首先,5年后的股利为: D5 = D0×(1 + g)5 = 2美元×1.085 = 2.938 7美元 因此,5年后的股价为: P5 = D5×(1 + g)/(R-g) = 2.938 7美元×(1.08)/0.08 = 3.173 8美元/0.08 = 39.67 美元 然而,一旦我们了解股利模型,更简单的方法是注意到: P5 = P0×(1 + g)5 = 27美元×1.085 = 27美元×1.469 3 = 39.67美元 注意,这两种方法所得出的5年后价格是相同的。 8.2 在这种情形下,前3年有超常报酬。这3年的股利为: D1 = 2.00美元×1.20 = 2.400美元 D2 = 2.40美元×1.20 = 2.880美元 D3 = 2.88美元×1.20 = 3.456美元 3年后,增长率无限期地降为8%。因此,当时的股价P3为: P3 = D3×(1 + g)/(R-g) = 3.456美元×1.08/(0.16-0.08) = 3.7325/0.08 = 46.656美元 为了计算股票的当前价值,我们必须确定这3期股利和未来价格的现值: P0 = D1 (1 + R)1 2.40美元 1.16 + + D2 (1 + R)2 2.88美元 1.16

罗斯公司理财第九版第八章课后答案对应版(英汉)金融专硕复习

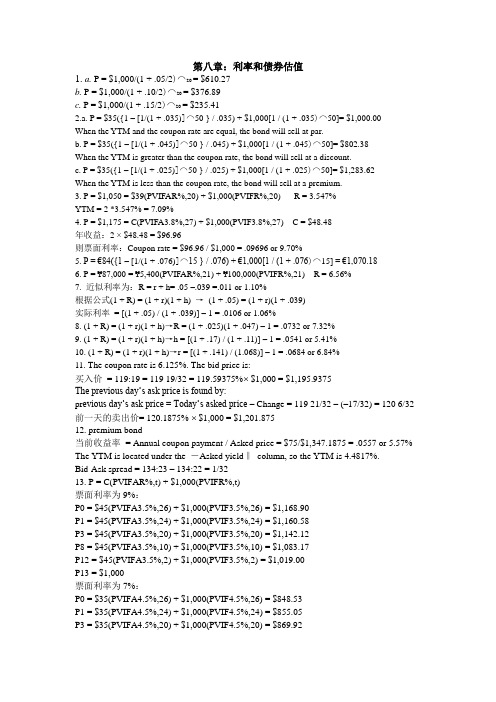

第八章:利率和债券估值1. a. P = $1,000/(1 + .05/2)⌒20 = $610.27b. P = $1,000/(1 + .10/2)⌒20 = $376.89c. P = $1,000/(1 + .15/2)⌒20 = $235.412.a. P = $35({1 – [1/(1 + .035)]⌒50 } / .035) + $1,000[1 / (1 + .035)⌒50]= $1,000.00When the YTM and the coupon rate are equal, the bond will sell at par.b. P = $35({1 – [1/(1 + .045)]⌒50 } / .045) + $1,000[1 / (1 + .045)⌒50]= $802.38When the YTM is greater than the coupon rate, the bond will sell at a discount.c. P = $35({1 – [1/(1 + .025)]⌒50 } / .025) + $1,000[1 / (1 + .025)⌒50]= $1,283.62When the YTM is less than the coupon rate, the bond will sell at a premium.3. P = $1,050 = $39(PVIFAR%,20) + $1,000(PVIFR%,20) R = 3.547%YTM = 2 *3.547% = 7.09%4. P = $1,175 = C(PVIFA3.8%,27) + $1,000(PVIF3.8%,27) C = $48.48年收益:2 × $48.48 = $96.96则票面利率:Coupon rate = $96.96 / $1,000 = .09696 or 9.70%5. P = €84({1 – [1/(1 + .076)]⌒15 } / .076) + €1,000[1 / (1 + .076)⌒15] = €1,070.186. P = ¥87,000 = ¥5,400(PVIFAR%,21) + ¥100,000(PVIFR%,21) R = 6.56%7. 近似利率为:R = r + h= .05 –.039 =.011 or 1.10%根据公式(1 + R) = (1 + r)(1 + h)→(1 + .05) = (1 + r)(1 + .039)实际利率= [(1 + .05) / (1 + .039)] – 1 = .0106 or 1.06%8. (1 + R) = (1 + r)(1 + h)→R = (1 + .025)(1 + .047) – 1 = .0732 or 7.32%9. (1 + R) = (1 + r)(1 + h)→h = [(1 + .17) / (1 + .11)] – 1 = .0541 or 5.41%10. (1 + R) = (1 + r)(1 + h)→r = [(1 + .141) / (1.068)] – 1 = .0684 or 6.84%11. The coupon rate is 6.125%. The bid price is:买入价= 119:19 = 119 19/32 = 119.59375%⨯ $1,000 = $1,195.9375The previous day‘s ask price is found by:pr evious day‘s ask price = Today‘s asked price – Change = 119 21/32 – (–17/32) = 120 6/32 前一天的卖出价= 120.1875% ⨯ $1,000 = $1,201.87512.premium bond当前收益率= Annual coupon payment / Asked price = $75/$1,347.1875 = .0557 or 5.57% The YTM is located under the ―Asked yield‖column, so the YTM is 4.4817%.Bid-Ask spread = 134:23 – 134:22 = 1/3213.P = C(PVIFAR%,t) + $1,000(PVIFR%,t)票面利率为9%:P0 = $45(PVIFA3.5%,26) + $1,000(PVIF3.5%,26) = $1,168.90P1 = $45(PVIFA3.5%,24) + $1,000(PVIF3.5%,24) = $1,160.58P3 = $45(PVIFA3.5%,20) + $1,000(PVIF3.5%,20) = $1,142.12P8 = $45(PVIFA3.5%,10) + $1,000(PVIF3.5%,10) = $1,083.17P12 = $45(PVIFA3.5%,2) + $1,000(PVIF3.5%,2) = $1,019.00P13 = $1,000票面利率为7%:P0 = $35(PVIFA4.5%,26) + $1,000(PVIF4.5%,26) = $848.53P1 = $35(PVIFA4.5%,24) + $1,000(PVIF4.5%,24) = $855.05P3 = $35(PVIFA4.5%,20) + $1,000(PVIF4.5%,20) = $869.92P8 = $35(PVIFA4.5%,10) + $1,000(PVIF4.5%,10) = $920.87P12 = $35(PVIFA4.5%,2) + $1,000(PVIF4.5%,2) = $981.27P13 = $1,00014.PLaurel = $40(PVIFA5%,4) + $1,000(PVIF5%,4) = $964.54PHardy = $40(PVIFA5%,30) + $1,000(PVIF5%,30) = $846.28Percentage change in price = (New price -Original price) / Original price△PLaurel% = ($964.54 -1,000) / $1,000 = -0.0355 or -3.55%△PHardy% = ($846.28 -1,000) / $1,000 = -0.1537 or -15.37%If the YTM suddenly falls to 6 percentPLaurel = $40(PVIFA3%,4) + $1,000(PVIF3%,4) = $1,037.17PHardy = $40(PVIFA3%,30) + $1,000(PVIF3%,30) = $1,196.00△PLaurel% = ($1,037.17 -1,000) / $1,000 = +0.0372 or 3.72%△PHardy% = ($1,196.002 -1,000) / $1,000 = +0.1960 or 19.60%15. Initially, at a YTM of 10 percent, the prices of the two bonds are:P Faulk = $30(PVIFA5%,16) + $1,000(PVIF5%,16) = $783.24P Gonas = $70(PVIFA5%,16) + $1,000(PVIF5%,16) = $1,216.76If the YTM rises from 10 percent to 12 percent:P Faulk = $30(PVIFA6%,16) + $1,000(PVIF6%,16) = $696.82P Gonas = $70(PVIFA6%,16) + $1,000(PVIF6%,16) = $1,101.06Percentage change in price = (New price – Original price) / Original price△PFaulk% = ($696.82 -783.24) / $783.24 = -0.1103 or -11.03%△PGonas% = ($1,101.06 -1,216.76) / $1,216.76 = -0.0951 or -9.51%If the YTM declines from 10 percent to 8 percent:PFaulk = $30(PVIFA4%,16) + $1,000(PVIF4%,16) = $883.48PGonas = $70(PVIFA4%,16) + $1,000(PVIF4%,16) = $1,349.57△PFaulk% = ($883.48 -783.24) / $783.24 = +0.1280 or 12.80%△PGonas% = ($1,349.57 -1,216.76) / $1,216.76 = +0.1092 or 10.92%16.P0 = $960 = $37(PVIFAR%,18) + $1,000(PVIFR%,18) R = 4.016% YTM = 2 *4.016% = 8.03%Current yield = Annual coupon payment / Price = $74 / $960 = .0771 or 7.71% Effective annual yield = (1 + 0.04016)⌒2 – 1 = .0819 or 8.19%17.P = $1,063 = $50(PVIFA R%,40) + $1,000(PVIF R%,40) R = 4.650% YTM = 2 *4.650% = 9.30%18.Accrued interest = $84/2 × 4/6 = $28Clean price = Dirty price – Accrued interest = $1,090 – 28 = $1,06219.Accrued interest = $72/2 × 2/6 = $12.00Dirty price = Clean price + Accrued interest = $904 + 12 = $916.0020.Current yield = .0842 = $90/P0→P0 = $90/.0842 = $1,068.88P = $1,068.88 = $90{[(1 – (1/1.0781)⌒t ] / .0781} + $1,000/1.0781⌒t $1,068.88 (1.0781)⌒t = $1,152.37 (1.0781)⌒t – 1,152.37 + 1,000t = log 1.8251 / log 1.0781 = 8.0004 ≈8 years21.P = $871.55 = $41.25(PVIFA R%,20) + $1,000(PVIF R%,20) R = 5.171% YTM = 2 *5.171% = 10.34%Current yield = $82.50 / $871.55 = .0947 or 9.47%22.略23.P: P0 = $90(PVIFA7%,5) + $1,000(PVIF7%,5) = $1,082.00P1 = $90(PVIFA7%,4) + $1,000(PVIF7%,4) = $1,067.74Current yield = $90 / $1,082.00 = .0832 or 8.32%Capital gains yield = (New price – Original price) / Original priceCapital gains yield = ($1,067.74 – 1,082.00) / $1,082.00 = –0.0132 or –1.32%D: P0 = $50(PVIFA7%,5) + $1,000(PVIF7%,5) = $918.00P1 = $50(PVIFA7%,4) + $1,000(PVIF7%,4) = $932.26Current yield = $50 / $918.00 = 0.0545 or 5.45%Capital gains yield = ($932.26 – 918.00) / $918.00 = 0.0155 or 1.55%24. a.P0 = $1,140 = $90(PVIFA R%,10) + $1,000(PVIF R%,10) R = YTM = 7.01%b.P2 = $90(PVIFA6.01%,8) + $1,000(PVIF6.01%,8) = $1,185.87P0 = $1,140 = $90(PVIFA R%,2) + $1,185.87(PVIF R%,2)R = HPY = 9.81%The realized HPY is greater than the expected YTM when the bond was bought because interest rates dropped by 1 percent; bond prices rise when yields fall.25.PM = $800(PVIFA4%,16)(PVIF4%,12)+$1,000(PVIFA4%,12)(PVIF4%,28)+ $20,000(PVIF4%,40) PM = $13,117.88Notice that for the coupon payments of $800, we found the PV A for the coupon payments, and then discounted the lump sum back to todayBond N is a zero coupon bond with a $20,000 par value; therefore, the price of the bond is the PV of the par, or:PN = $20,000(PVIF4%,40) = $4,165.7826.(1 + R) = (1 + r)(1 + h)1 + .107 = (1 + r)(1 + .035)→r = .0696 or 6.96%EAR = {[1 + (APR / m)]⌒m }– 1APR = m[(1 + EAR)⌒1/m – 1] = 52[(1 + .0696)⌒1/52 – 1] = .0673 or 6.73%Weekly rate = APR / 52= .0673 / 52= .0013 or 0.13%PVA = C({1 – [1/(1 + r)]⌒t } / r)= $8({1 – [1/(1 + .0013)]30(52)} / .0013)= $5,359.6427.Stock account:(1 + R) = (1 + r)(1 + h) →1 + .12 = (1 + r)(1 + .04) →r = .0769 or 7.69%APR = m[(1 + EAR)1/⌒1/m– 1]= 12[(1 + .0769)⌒1/12– 1]= .0743 or 7.43%Monthly rate = APR / 12= .0743 / 12= .0062 or 0.62%Bond account:(1 + R) = (1 + r)(1 + h)→1 + .07 = (1 + r)(1 + .04)→r = .0288 or 2.88%APR = m[(1 + EAR)⌒1/m– 1]= 12[(1 + .0288)⌒1/12– 1]= .0285 or 2.85%Monthly rate = APR / 12= .0285 / 12= .0024 or 0.24%Stock account:FVA = C {(1 + r )⌒t– 1] / r}= $800{[(1 + .0062)360 – 1] / .0062]}= $1,063,761.75Bond account:FVA = C {(1 + r )⌒t– 1] / r}= $400{[(1 + .0024)360 – 1] / .0024]}= $227,089.04Account value = $1,063,761.75 + 227,089.04= $1,290,850.79(1 + R) = (1 + r)(1 + h)→1 + .08 = (1 + r)(1 + .04) →r = .0385 or 3.85%APR = m[(1 + EAR)1/m– 1]= 12[(1 + .0385)1/12– 1]= .0378 or 3.78%Monthly rate = APR / 12= .0378 / 12= .0031 or 0.31%PVA = C({1 – [1/(1 + r)]t } / r )$1,290,850.79 = C({1 – [1/(1 + .0031)]⌒300 } / .0031)C = $6,657.74FV = PV(1 + r)⌒t= $6,657.74(1 + .04)(30 + 25)= $57,565.30。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第一章Corporate finance(公司财务)是金融学的分支学科,用于考察公司如何有效地利用各种融资渠道,获得最低成本的资金来源,并形成合适的资本结构(capital structure);还包括企业投资、利润分配、运营资金管理及财务分析等方面。

它会涉及到现代公司制度中的一些诸如委托-代理结构的金融安排等深层次的问题。

为什么说公司理财研究的就是如下三个问题:(1) 公司应该投资于什么样的长期资产?涉及资产负债表的左边。

我们使用“资本预算(capital budgeting)”和“资本性支出”这些专业术语描述这些长期固定资产的投资和管理过程。

(2) 公司如何筹集资本性支出所需的资金呢?涉及资产负债表的右边。

回答这一问题又涉及到资本结构(Capital structure),它表示公司短期及长期负债与股东权益的比例。

(3) 公司应该如何管理它在经营中的现金流量?涉及资产负债表的上方。

首先,经营中的现金流入量和现金流出量在时间上不对等。

此外,经营中现金流量的数额和时间都具有不确定性,难于确切掌握。

财务经理必须致力于管理现金流量的缺口。

从资产负债表的角度看,现金流量的短期管理与净营运资本(net working capital)有关。

净营运资本定义为短期资本与短期负债之差。

从财务管理的角度看,短期现金流量问题是由于现金流量和现金流量之间不对等所引起的,属于短期理财问题。

资本结构公司可以事先发行比股权多的债权,筹集所需的资金;可以考虑改变二者的比例,买回它的一些债权。

融资决策在原先投资决策前就可以独立设定。

这些发行债权和股权的决策影响到公司的资本结构。

资金主管负责处理现金流量、投资预算和制定财务计划。

财务主管负责会计工作职能,包括税收、成本核算、财务会计和信息系统。

现金流量的时点公司投资的价值取决于现金流量的时点。

一个最重要的假设是任何人都偏好早一点收到现金流量。

今天收到的一美元比明天收到的一美元更有价值。

这种偏好对股票和债券的价格有一定影响。

负债和所有者权益有何本质区别?关键是:考虑当公司价值发生变化时对负债和所有者权益的报酬所产生的影响。

负债的基本特征是:借债的公司承诺在某一确定的时间支付给债权人一笔固定的金额。

公司制企业所有权和管理权分离有很多好处:(1)产权可以随时转让给新的所有者。

股份转让不受限制。

(2) 公司具有无限存续期。

(3) 股东的责任仅限于其投资于所有权的股份数。

有限责任、易于产权转让和永续经营是优点。

提高了企业筹集资金的能力。

缺点政府按照公司所得征收公司所得税,是双重征税。

Long-lives assets 资本预算:长期资产的投资和管理过程。

Capital structure(资本结构raise cash)公司短期及长期负债与股东权益的比例。

The Net Working Capital Investment Decision (净营运资本short term)流动资产减去流动负债。

Stakeholders(利益相关者) 除股东和债权人以外,对公司的现金流具有要求权的人。

Proxy fight(表决权)表决权是指代表其他股东进行投票的表决权利。

股东因不满意而采取行动更换现有管理层的一个重要机制被称为表决权之争。

财务经理最重要的工作是通过资本预算、融资和净营运资本管理活动为公司创造价值。

How do financial manager create value(财务经理如何创造价值)公司应该做到努力购入创造超过其成本的现金资产,发行债券、股票和其他金融工具,已筹集超过其成本的现金。

The characteristics of Sole proprietorship(独资企业特点)1是费用最低的一种企业组织形式,不需要正式的章程,对大多数行业而言需要遵守的政府法规很少2无需缴纳公司所得税,企业所有的利润都安个人所得税税率缴纳3独资企业业主对企业债务负债有无限责任,个人资产和企业之间没有差别。

4独资企业的企业存缓期受限于业主本人寿命5由于投资与企业的资金仅仅是业主的资金,因此企业主筹集的权益资本受限于业主的个人财富状况。

The characteristics of partnership(合伙制的特征)1费用通常较低,易于成立,无论是一般合伙制企业还是有限合伙制企业,在进行复杂安排时,都应采用书面形式。

2一般合伙人对企业的负所有债务负有无限责任,有限合伙人通常以其出资额为有限承担责任。

3如果一个一般合伙人退出或死亡,一般合伙制企业将随之终结(有限合伙人不是这样,可以出手他们呢在企业中的权益)4筹集大量资金难度很大。

5合伙制企业的收入按合伙人的个人收入征收个人所得税。

6管理控制权属于一般合伙人。

Faults(缺点)1无限责任2有限的企业寿命3所有权转让困难,以上三点导致融资困难Articles of association(公司制公司章程)1公司名称2供公司计划经营年限(可以永久经营)3经营目的4公司获准发行的股票数量5股东拥有的权利6初创时董事会成员的人数。

Corporation advantages(公司制优点)1由于公司的所有权以股份表示,因此所有权可以随时转让给新的所有者2具有无限存续期3股东的责任以其投资的股份数为限,这些优点大大提高了公司的融资能力。

Financial management goal(财务管理的目标)最大化现有股票的每股当前价值。

更全面的表达为是公司现有的所有者权益的市场价值最大化。

Agency problem(代理问题)委托人和代理人之间可能会存在的利益冲突成为代理问题。

公司的最终控制权在股东手中,他们举行董事会,在由董事会聘用或解雇管理层,可以利用表决权进行表决或者是并购来更换管理层。

代理成本Agency Costs(解决冲突)由管理者与股东之间代理问题而引起的成本。

间接成本指有价值的机会流失,直接成本:(1)使管理层受益,但使股东受损的公司支出。

管理人员的薪酬和在职消费,(2)为监督管理者行为的成本。

,Financial Management Principle(财务管理原则)风险与收益相权衡的原则,货币的时间价值原则,价值的衡量要考虑的是现金而不是利润,增量现金流量原则,纳税影响业务决策,风险分为不同的类别管理者是否依循股东利益行事取决于:管理层和股东的目标是否一致?如果管理层不按股东目标行事,是否会被撤换?管理层的薪酬:(1)管理层的薪酬与公司的财务业绩挂钩,与股票价值挂钩。

(2)管理人员对工作的前景规划,提升机会。

货币市场(money markets)指短期的债务证券市场,需在一年内偿还。

资本市场(capital markers)指长期债务证券和权益股份市场,长期债务证券的期限为一年以上。

经纪人是一些根据其库存的货币市场工具和风险随时准备购买或销售而进行连续报价的公司。

拍卖市场和经纪人市场的区别:一,拍卖市场上交易在交易所的大厅进行。

二,拍卖市场交易的股票,其交易价格几乎立即通过计算机或其他方法公布于众。

1. 公司金融学与财务管理学之间的关系:财务管理是关于资产的购置、融资和管理的科学;从内容上看,财务管理学有四个主要的分支:公共财务管理、私人财务管理、公司财务管理和国际财务管理;由于公司财务管理包含了所有的理财原理和思想在内,在实践中的用途最广,因而狭义的财务管理学就是指公司财务管理即公司金融学。

2. 企业筹集长期资金的方式有哪些?1、折旧—内部筹资;2留存受益——内部筹资;3银行长期贷款——外部间接债务筹资;4发行公司债券——外部直接债务筹资;5发行股票——外部直接权益筹资。

3. 公司财务管理的目标是什么?股东财富最大化,其载体是股票的市场价格;因为股东财富最大化考虑了风险因素,考虑了货币的时间价值,考虑了股东所提供的资金的成本。

4. 为什么公司这种组织形式融资比较便利?有限责任、股份容易转让;永续经营;融资比较便利。

5. 简述影响债券价值的因素。

债券价值与投资者要求的收益率(当前市场利率) 成反向变动关系;当债券的收益率不变时,债券的到期时间与债券价格的波动幅度之间成正比关系;债券的票面利率与债券价格的波动幅度成反比关系(不适用于1年期债券或永久债券);当市场利率变动时,长期债券价格的波动幅度大于短期债券的波动幅度;债券价值对市场利率的敏感性与债券所要产生的预期未来现金流的期限结构有关。

二章Accounting liquidity(会计流动性)各项资产转换成现金的容易程度和快速程度。

Liabilities(负债) 是企业在规定期限内偿付一笔现金承诺。

Stockholders’ equity(股东权益) 是对企业资产的一中剩余的和非固定的请求权。

EBIT(息税前利润)该直白哦总括了在计算所得税和筹资费用之前的收益。

Accounting cost(产品成本) 是在一段时间内发生的总的生产成本(原材料、直接人工及制造费用)在损益表上作为已售产品的成本加以报告。

Average tax rate(品均税率) 敬你的税单处以你的应税总额。

Marginal tax rate (边际税率) 当你每多挣亿美元时所应缴纳的税款。

Change in net working capital(净营运资本的变动额)除了投资于固定资产,一家企业还可以投资于净营运资本。

Debt service(债务清偿)就是利息支付加上本金偿还。

Discustion of cash flow(现金流讨论的重要结果)1好几种现金流都与理解企业的财务状况有关2净利润不是现金流Operating cash flow(经营性现金流)等于息税前利润加上折旧减去所得税,它反映的是经营活动生产的现金,不包括资本性支出和营运资本要求。

A primary difference between the accounting cash flow and the finance cash flow of the firm is interest expense.(会计现金流和企业财务现金流的一个主要不同是利息费用)三章Financial ratios group(财务比率分类)1短期偿债能力(流动性)比率2长期偿债能力(财务杠杆)比率3资产管理(或周转)比率4活力能力比率5市场价值比率ROA衡量每1美元资产产生的利润,ROE衡量股东当年获利的指标。

The du pontidentity tells us that ROE is affected by(杜邦分析说影响roe的因素)1经营效率(有利润衡量)2资产利用率(有总资产周转率衡量)3财务杠杆(由权益乘数衡量)第五章Bonds(债券)一种标准的只还息不还本金的贷款。

Level coupon bond(等额票息债券)票息固定不变并且在每年支付。