会计档案保管清册模板

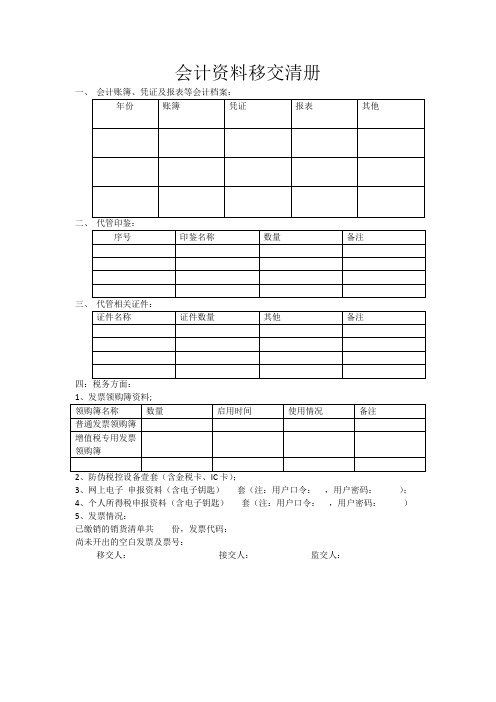

会计资料移交清册模板

一、会计账簿、凭证及报表等会计Байду номын сангаас案:

年份

账簿

凭证

报表

其他

二、代管印鉴:

序号

印鉴名称

数量

备注

三、代管相关证件:

证件名称

证件数量

其他

备注

四:税务方面:

1、发票领购簿资料;

领购簿名称

数量

启用时间

使用情况

备注

普通发票领购簿

增值税专用发票领购簿

2、防伪税控设备壹套(含金税卡、IC卡);

3、网上电子申报资料(含电子钥匙)套(注:用户口令:,用户密码:);

4、个人所得税申报资料(含电子钥匙)套(注:用户口令:,用户密码:)

5、发票情况:

已缴销的销货清单共份,发票代码:

尚未开出的空白发票及票号:

移交人:接交人:监交人:

会计档案清册模板 -回复

会计档案清册模板-回复会计档案清册模板是记录和管理会计档案的工具,它可以帮助会计人员整理、分类和归档会计信息,提高会计工作的效率和准确性。

下面我将一步一步回答关于会计档案清册模板的问题。

第一步:什么是会计档案清册模板?会计档案清册模板是一个表格或电子文档,用于记录会计档案的相关信息。

通常包括档案编号、档案名称、档案类型、所属部门、归档日期等信息。

第二步:为什么需要会计档案清册模板?使用会计档案清册模板可以帮助会计人员清晰地记录和管理会计档案,避免遗漏或混淆。

档案清册模板还可以提供查找和检索会计档案的便利,节省时间和精力。

第三步:如何创建会计档案清册模板?创建会计档案清册模板可以使用电子表格软件,如Microsoft Excel或Google Sheets。

根据需要,可以自定义表头和内容,使其适应具体的会计档案管理需求。

第四步:如何填写会计档案清册模板?在填写会计档案清册模板时,根据每份档案的具体信息,逐项填写相应的字段。

档案编号可以按照一定规则编排,以便于档案的唯一标识和查找。

档案名称和档案类型应准确且清晰地描述档案的内容和性质。

所属部门可根据具体情况填写,以方便定位和管理档案。

归档日期应记录最新归档的日期,以便跟踪档案的存档时间。

第五步:如何使用会计档案清册模板?使用会计档案清册模板时,可以根据需要进行查询和筛选,以便快速定位和检索档案。

可以按照档案编号、档案名称、档案类型等字段进行排序,以方便查找和管理。

此外,可以根据业务需要,将档案清册模板与其他会计软件或档案管理系统进行集成,以进一步提高管理效率。

第六步:如何保管和维护会计档案清册模板?为了确保会计档案清册模板的完整性和准确性,应定期进行备份,并严格控制访问权限。

同时,应对档案清册模板进行定期审查和更新,以反映最新的档案变动情况。

如果需要,可以使用电子签名或时间戳等技术手段对档案清册进行安全认证。

总结:会计档案清册模板是一种有助于记录和管理会计档案的工具,可以提高会计工作的效率和准确性。

深圳南山会计档案销毁清册模板

深圳南山会计档案销毁清册模板

(一)档案销毁清册模板。

序号:。

档案名称:。

档案类型:。

存放单位:。

卷内资料简介:。

起止年月:。

销毁时间:。

保管期限:。

销毁方式:。

销毁人:

(二)深圳南山会计档案销毁清册。

序号档案名称档案类型存放单位卷内资料简介起止年月销毁时间保管期限销毁方式销毁人。

1 深圳南山会计档案财务档案深圳市南山区会计办公室包括例如付款单、收入单、发票等金钱财务类文件2018/06-2019/06 2019/09/10 7年焚烧深圳市南山区会计档案室管理员。

2 深圳南山公司财务档案财务档案深圳市南山区公司包括例如付款单、收入单、发票等金钱财务类文件2015/04-2017/07 2019/09/12 7年焚烧深圳市南山区公司工作人员。

企业和其他组织会计档案保管期限表格模板

10年

11

银行对账单

10年

12

纳税申报表

10年

13

会计档案移交清册

30年

14

会计档案保管清册

永久

15

会计档案销毁清册

永久16Βιβλιοθήκη 会计档案鉴定意见书永久

附表2

财政总预算、行政单位、事业单位和税收会计档案保管期限表

序号

档案名称

保管期限

备注

财政

总预算

行政单位

事业单位

税收

会计

一

会计凭证

1

国家金库编送的各种报表及缴库退库凭证

10年

10年

2

各收入机关编送的报表

10年

3

行政单位和事业单位的各种会计凭证

30年

包括:原始凭证、记账凭证和传票汇总表

4

财政总预算拨款凭证和其他会计凭证

30年

包括:拨款凭证和其他会计凭证

二

会计账簿

5

日记账

30年

30年

6

总账

30年

30年

30年

7

税收日记账(总账)

30年

8

明细分类、分户账或登记簿

30年

30年

22

会计档案保管清册

永久

永久

永久

23

会计档案销毁清册

永久

永久

永久

24

会计档案鉴定意见书

永久

永久

永久

注:税务机关的税务经费会计档案保管期限,按行政单位会计档案保管期限规定办理。

30年

9

行政单位和事业单位固定资产卡片

固定资产报废清理后保管5年

三

会计档案清册模板 -回复

会计档案清册模板-回复[Mentioning] the importance of maintaining an accurate and organized accounting record, this article aims to provide a comprehensive guide on creating a well-structured accounting archive inventory. By following the step-by-step instructions detailed below, businesses can effectively manage and track their financial records.Step 1: Understand the Importance of Organized Accounting RecordsMaintaining proper accounting records is crucial for several reasons. Firstly, it ensures compliance with legal and regulatory requirements. Accurate records enable businesses to fulfill their tax obligations promptly and accurately. Additionally, well-maintained accounting records provide an essential foundation for making informed financial decisions. These records help in understanding the financial health of the organization, identifying areas of improvement, and preparing accurate financial statements.Step 2: Determine the Scope of the Accounting ArchiveBefore creating a clearance inventory, it is essential to define thescope of the accounting archive accurately. This involves deciding which financial documents should be included. A general list may include journal entries, general ledgers, trial balances, financial statements, tax returns, invoices, receipts, bank statements, and any other relevant document. Determining the time frame for inclusion is also crucial, such as whether to include records from the current fiscal year or multiple prior years.Step 3: Create a Well-Structured Inventory ListTo create a comprehensive accounting archive inventory, develop a structured list of all the accounting documents that need to be maintained. This list should include details such as the document type, date range, document reference, and location. By organizing the records in a systematic manner, it becomes easier to locate and access any specific document when required.Step 4: Implement Proper Document Management SystemTo efficiently maintain the accounting records, consider implementing a document management system. Such systems enable digitization of documents, making it easier to store, retrieve, and search for specific records. Choose a reliable and secure software solution that offers features like version control,secure access, and document encryption. Utilizing technology for managing accounting documents not only saves space but also enhances data security and accessibility.Step 5: Set Up Regular Archiving ProcessesEstablishing regular archiving processes is crucial for maintaining accurate and up-to-date accounting records. Define a strict schedule for archiving documents, ensuring that it aligns with the business's record retention policy and legal requirements. Assign responsibilities to designated personnel who are responsible for documenting, archiving, labeling, and verifying the accuracy of the records. Conduct regular audits to ensure compliance with established procedures.Step 6: Periodically Review and Update the Inventory ListAs the business grows and evolves, accounting documents will accumulate, making it essential to periodically review, update, and reassess the inventory list. Remove any outdated or irrelevant documents to ensure the list remains current and accurate. This process guarantees that the accounting archive is continuously aligned with the organization's evolving needs.Step 7: Protect and Secure the Accounting Archive Safeguarding the accounting archive is crucial to maintain the integrity and confidentiality of the financial records. Implement strict security measures, such as restricted access, password protection, encryption, and regular data backups. Train employees on proper handling and storage procedures to avoid accidental losses or breaches in the security of sensitive financial data.Step 8: Continuously Monitor and ImproveRegularly monitor the performance of the accounting archive inventory system. Solicit feedback from employees to identify any challenges or areas for improvement. Maintain open communication channels to address any concerns promptly. This continuous improvement process ensures that the accounting archive remains accurate, accessible, and secure.In conclusion, maintaining a well-structured accounting archive is vital for any business. By following the step-by-step instructions outlined above, organizations can efficiently manage their financial records, ensure compliance, make informed decisions, and protect sensitive information. Investing time and effort in thecreation and maintenance of accurate and organized accounting records is a crucial step towards achieving long-term financial success.。

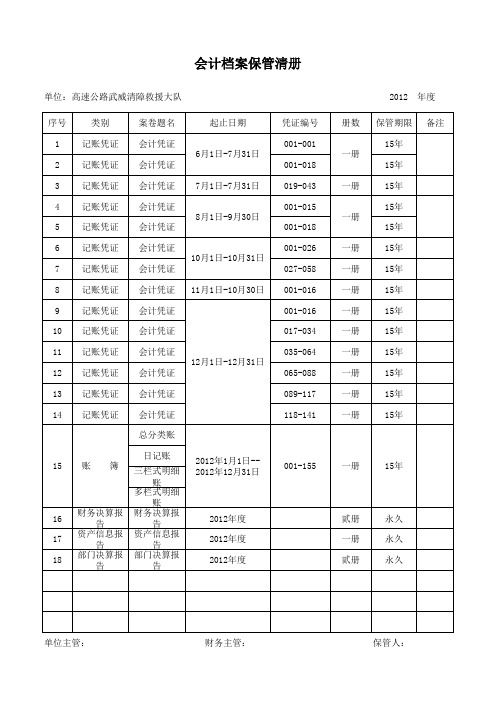

会计档案保管清册

单位:高速公路武威清障救援大队 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 类别 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 记账凭证 案卷题名 会计凭证 6月1日-7月31日 会计凭证 会计凭证 会计凭证 8月1日-9月30日 会计凭证 会计凭证 10月1日-10月31日 会计凭证 会计凭证 会计凭证 会计凭证 会计凭证 12月1日-12月31日 会计凭证 会计凭证 会计凭证 总分类账 日记账 15 账 簿 三栏式明细账 多栏式明细账 16 17 18 财务决算报告 财务决算报告 资产信息报告 资产信息报告 部门决算报告 部门决算报告 2012年度 2012年度 2012年度 贰册 一册 贰册 永久 永久 永久 2012年1月1日-2012年12月31日 001-155 一册 15年 065-088 089-117 118-141 一册 一册 一册 15年 15年 15年 11月1日-10月30日 027-058 001-016 001-016 017-034 035-064 一册 一册 一册 一册 一册 15年 15年 15年 15年 15年 001-018 001-026 一册 7月1日-7月31日 001-018 019-043 001-015 一册 15年 15年 一册 起止日期 凭证编号 001-001 一册 15年 15年 15年 册数 2012 年度 保管期限 15年

单位主管:

财务主管:

保管人:

8.会计档案管理用表

1.会计档案移交清册

会计档案移交清册

年度:第页,共页序号档号案卷题名起止日期起止凭证号册(页)数应保管期限已保管期限备注

移交部门(单位):移交人:移交部门(单位)负责人:移交时间:

接收部门(单位):接收人:接收部门(单位)负责人:接收时间:

注:册(页)数:会计凭证填写册数,其他材料填写页数。

2.会计档案销毁清册

会计档案销毁清册

序

档号案卷题名起止日期起止凭证号册(页)数应保管期限已保管期限销毁时间备注号

单位负责人:

监察审计分管领导:财务工作分管领导:档案工作分管领导:

监察审计部门负责人:财务管理部门负责人:档案管理部门负责人:

注:册(页)数:会计凭证填写册数,其他材料填写页数。

会计档案移交、销毁清册

会计档案移交清册1、交接双方的单位负责人负责监交。

2、交接完毕后,交接双方经办人和监交人应当在会计档案移交清册上签名或者盖章。

移交单位负责人:接收单位负责人:移交单位经办人:接收单位经办人:移交时间:接收时间:3、会计档案移交清册一式三份,交接双方及单位各存一份。

《会计档案移交清册》填写说明1、顺序号:指会计档案案卷在本册案卷目录中顺次排列的序号。

2、类别:主要指会计档案的种类。

如:会计凭证、会计账簿、财务报告及其他。

3、案卷题名:指会计档案案卷的具体名称。

如:会计账簿类的总账、现金日记账等。

4、起止日期:指案卷卷内最开始启用的时间到最后终止使用的时间。

如:1996.1.1-1996.12.31。

5、凭证编号:填写记账凭证的编号。

6、卷内张数:主要指综合后凭证、账簿、财务报告的页数。

7、保管期限:指案卷封面上注明的保管期限。

会计档案的保管期限一般有:永久、长期、25年、15年、10年、5年等。

8、已保管期限:指会计档案形成至移交时,已保管的期限。

9、备注:指用来说明个别案卷的某些特殊情况的记录。

如:卷内某页文件不清楚、残破、缺页漏张等,以示查阅或鉴定时特别注意。

会计档案销毁清册1、单位负责人意见:2、监销人:(1)档案机构:(2)会计机构:(3)同级财政部门:(4)同级审计部门:(国家机关销毁会计档案时,应当由同级财政部门、审计部门派员参加监销。

财政部门销毁会计档案时,应当由同级审计部门派员参加监销。

)会计档案移交、销毁须知一、各单位每年形成的会计档案,应当由会计机构按照归档要求,负责整理立卷,装订成册,编制会计档案保管清册。

当年形成的会计档案,在会计年度终了后,可暂由会计机构保管一年,期满之后,应当由会计机构编制移交清册,移交本单位档案机构统一保管;未设立档案机构的,应当在会计机构内部指定专人保管。

出纳人员不得兼管会计档案。

移交本单位档案机构保管的会计档案,原则上应当保持原卷册的封装。

个别需要拆封重新整理的,档案机构应当会同会计机构和经办人员共同拆封整理,以分清责任。

财务部档案管理清册(全)

账册封面!A1

保管期限 附件 30年 30年 30年 30年 30年 30年 固定资产 报废清理 后保管5 年 30年 30年 30年

10年 10年 10年 10年 10年 10年 11年

备注 年度为永久保管

纳税申报资料

财务部档案管理清册

类别

辅助类别

各类合同协议

四类(编码04): 文字资料及其他类

其他类

账册封面

责任人

保管期限 附件 10年

备注

10年 10年

30年 永久 Leabharlann 久会计档案借阅申请表!A1 会计档案移交清册!A1 会计档案保管清册!A1 会计档案销毁清册!A1

收据使用登记簿!A1

金税盘系统导出

库存现金盘点表!A1 往来业务对帐函!A1

未认证增值税专用发票登 记表 '!A1

融资台账!A1

是否需要 电子版 电子版 电子版

类别

辅助类别

一类(编码

CW01):会计凭证 会计凭证类

类

二类(编码CW02): 会计账簿类

会计账簿类

财务部档案管理清册

序列 明细 1 原始凭证

责任人

2 记账凭证

3 总账 4 明细账 5 银行存款日记账 6 现金日记账

7 固定资产卡片

财务报表类

三类(编码CW03): 报表报告类

财务报告类

纳税申报资料

8 客户明细账 9 供应商明细账 10 其他会计账簿 11 会计报表 12 附表 13 附注及文字说明 14 所得税汇算清缴报告 15 审计报告(税务) 16 审计报告(银行) 17 审计报告(内部经营业绩) 18 面积测绘报告 19 土地清算报告 20 土地评估报告 21 房产评估报告 22 预算执行报告 23 财务报告(分析说明等) 24 营业收入增值税 25 土地增值税 26 个人所得税 27 企业所得税 28 印花税 29 缴纳凭证(税票复印件) 30 其他税种申报表

会计档案封面及各类清册的表格样

立档单位:阳光保险()凭据名称:

日期:年代本月共册本册是第册

凭据号:第号至第号保存限期:年

全宗号:目录号:模卷号:

会计档案

阳光财富保险股份有限企业

保险业务记账凭据

年代

本月共册,此册为第册

凭据号自第号至第号

阳光财富保险股份有限企业

财务核算记账凭据

年代

本月共册,此册为第册

凭据号自第号至第号

会计档案销毁清册

编制部门:

同意人:

序号

题名

年度

档号

卷内文件

原限期

已保存

年限

件数

页数

会计档案移交登记表

移交时间:移交部门:移交时间:

序号

题名

年度

文号或计档案借阅申请表

借阅部门

借阅人署名

同意人署名

借阅日期

利用方式

借阅内容

借阅目的

经办人署名

送还确认

会计档案借阅登记表

序号

借阅时间

申请单号

档案编号

借阅人

年代日

单位(印章)

年代日

年代日

档案备考表

整理人:检查人:年代日

审查人

送还时间

送还人

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

电子档案移交与接收登记表

交接工作名称

内容描绘

移交电子档案数目

移交数据量

载体起止次序号

移交载体、种类、规格

查验内容

单位名称

移交单位:

接收单位:

正确性查验

完好性查验

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计档案保管清册模板

档案编号:XXXX-XXXX-XXX

档案名称:XXXX年会计档案

保管期限:长期/短期

保管责任人:XXX

档案内容清单:

1.原始凭证

2.记账凭证

3.会计账簿

4.财务报表

5.其他会计资料(如银行对账单、税务申报表等)

档案存放位置:

1.原始凭证:存放于XXXX办公室档案柜中,具体位置为第X层第X

格。

2.记账凭证:存放于XXXX办公室档案柜中,具体位置为第X层第X

格。

3.会计账簿:存放于XXXX办公室档案柜中,具体位置为第X层第X

格。

4.财务报表:存放于XXXX办公室档案柜中,具体位置为第X层第X

格。

5.其他会计资料:存放于XXXX办公室档案柜中,具体位置为第X层

第X格。

档案备份情况:所有会计档案均已进行电子和纸质备份,电子备份存储在XXXX电脑中,纸质备份存放在XXXX办公室档案柜中。

档案查阅和使用规定:

1.查阅和使用会计档案需经财务部门负责人批准。

2.查阅和使用会计档案需进行登记和审批流程。

3.会计档案不得随意带出工作单位或提供给外部人员查阅。

4.使用会计档案需严格遵守保密规定,不得泄露公司财务机密。

5.使用完毕后,需及时归还档案,并确保档案的完整性和安全性。