CMA考试新考纲(官方)-part one 3 (2)

cma考纲

"CMA" 通常指的是管理会计师(Certified Management Accountant),是由全球管理会计师协会(Institute of Management Accountants,IMA)颁发的专业资格。

以下是CMA考试的主要考纲内容,但请注意,具体的考纲可能有所调整,建议查阅最新的官方信息。

CMA考试分为两个部分:Part 1和Part 2。

每个部分包含了多个主题,涵盖了管理会计的各个方面。

### Part 1: Financial Planning, Performance, and Analytics1. **External Financial Reporting Decisions (15%)**- Financial statements- Recognition, measurement, valuation, and disclosure2. **Planning, Budgeting, and Forecasting (20%)**- Strategic planning- Budgeting concepts- Forecasting techniques3. **Performance Management (20%)**- Cost and variance measures- Responsibility centers and reporting segments- Performance measures4. **Cost Management (15%)**- Costing systems- Overhead costs- Supply chain management5. **Internal Controls (15%)**- Governance, risk, and compliance- Internal auditing- Systems controls and security measures6. **Technology and Analytics (15%)**- Information systems- Data governance- Data analytics### Part 2: Strategic Financial Management1. **Financial Statement Analysis (20%)**- Financial statement ratios- Profitability analysis- Analytical issues in financial accounting2. **Corporate Finance (20%)**- Risk and return- Long-term financial management- Raising capital3. **Decision Analysis (25%)**- Cost-volume-profit analysis- Marginal analysis- Pricing4. **Risk Management (10%)**- Enterprise risk- Hedging5. **Investment Decisions (15%)**- Capital budgeting process- Discounted cash flow analysis- Valuation methods6. **Professional Ethics (10%)**- Ethical considerations for management accounting and financial management professionals每个主题都包含了具体的知识点,而考试中的问题通常要求考生在实际场景中应用相关概念和技能。

CMA考试大纲及考试内容(2019详细版)

CMA考试大纲及考试内容(2019详细版)近日,IMA官方协会已经公布了2019年4月13日CMA报名时间,其中CMA考试注册的截止时间:IMA英文/中文网站2019年2月20日;考位预约及取消的截止时间:普尔文网站2019年2月27日,另外本次考试在全国共开设24个考点(新增三个):北京、上海、苏州、成都、西安、青岛、武汉、广州、大连、南京、昆明、济南、深圳、郑州、杭州、天津、合肥、重庆、长沙、南昌、兰州、太原、沈阳和厦门,大家可以准备起来了。

在备考之前,各位考生先要了解2019年CMA考试大纲,主要考哪些内容?跟着中博小编一起来看看吧。

【文字说明】Part1——财务计划、绩效与控制外部财务报告决策(15%)财务报告;确认、计量、评估与披露。

规划、预算与预测(30%)计划流程;预算概念;年度利润计划及附表;预算类型,包括作业基础预算,项目预算,弹性预算;高层计划及分析;财务预测,包括定量法如回归分析法及学习曲线分析。

绩效管理(20%)内部控制及业绩考评的财务指标,包括收入,成本,利润及资产投资;基于弹性预算和标准成本的各种差别分析;收益,成本,贡献和利润中心的会计责任;平衡记分卡。

成本管理(20%)成本概念,流程和术语;替换成本目标;成本衡量概念;成本积累系统包括分批成本法、分步成本法和作业成本法;间接成本分摊;营效率和业务流程绩效主题如JIT,MRP等生产规范,约束理论,价值链分析,基准分析,ABM以及持续改进。

内部控制(15%)风险评估;内部控制环境,程序及标准;内部审计的责任与权力;审计类型;会计信息系统控制充分性评估。

Part2——财务决策财务报告分析(25%)主要财务报表及其目的;财务报表信息局限性;财务报表解释和分析,包括比率分析和比较分析;市场价值与账面价值对比;公允价值会计;国际问题;国际财务报告准则(IFRS)与美国公认会计准则(GAAP)主要区别;资产负债表外融资;现金流量表的编制、分析和调节;收益质量。

新考试大纲安排

• • • 每部分考试时间为4个小时:选择题3小时,问答题1小时 新考纲两门考试的先后顺序可由考生自行决定 (根据考生意愿,两门考试可在同一天进行) 所有考题的最高难度为C难度 (综合及推荐能力) 单选题部分的得分至少为50%的考生才有资格进入问答题部分的 考试。 考生无法立即知道考试结果;考试结果将在此考试窗口结束后几 周后邮寄给考生。

7

CMA考试要求

• • • • 考生需拥有国家认可的大学专科学历(专业不限)。GMAT考试分 数将不再作为考生学历背景的资格认证。 2年以上相关工作经验。 考生需具备一定的财务知识:经济,统计学原理,财务会计。 参加过会计和财务方面的课程(强烈建议)。

8

免试/其他相关财务认证资格

• 新考纲无免试政策 • 其他相关财务认证的互免将视具体情况来决定(中国目前还没有相关认 证的互免)

新考纲-两部分考试

• Part 1 – 财务计划,业绩及控制 – 财务计划,预算及财务预测 (30%) – 绩效考核 (25%) – 成本管理 (25%) – 内部控制 (15%) – 职业道德 (5%) • Part 2 – 财务决策 – 财务报告分析 (25%) – 公司理财 (25%) – 风险管理及决策分析 (25%) – 投资决策 (20%) – 职业道德 (5%)

cma 考试大纲

cma 考试大纲一、考试简介CMA(Certified Management Accountant)即注册管理会计师,是全球公认的管理会计领域权威认证。

为了帮助考生更好地准备CMA 考试,我们特此制定了《CMA考试大纲》,为考生提供全面的考试指导。

二、考试科目与内容CMA考试包含两个科目,每个科目涵盖了管理会计和财务规划与报告两个方面的内容。

具体如下:科目一:财务规划与报告1. 财务报表分析:包括财务指标的计算、意义和运用。

2. 预算与预测:包括预算的编制、预测的方法和运用。

3. 财务规划流程:包括财务计划的制定、执行和控制。

4. 财务报告:包括财务信息的收集、整合和解读。

科目二:战略财务管理1. 投资决策:包括资本预算的方法、决策标准和运用。

2. 风险管理:包括风险识别、评估和应对策略。

3. 财务策划:包括个人和企业的财务规划。

4. 财务战略与决策分析:包括企业战略的制定、实施和控制。

三、重点知识点与技能要求1. 掌握财务报表分析的基本原理和方法,能够进行财务指标的分析和评价。

2. 熟悉预算编制、预测和财务规划流程的方法和运用,能够独立完成财务规划工作。

3. 掌握财务报告的编制和解读方法,能够提供有效的信息支持决策。

4. 了解资本预算的基本原理和方法,能够进行投资项目的评估和选择。

5. 熟悉风险管理的基本原理和方法,能够设计和实施有效的风险管理策略。

6. 掌握财务战略制定的方法和运用,能够为企业战略的制定、实施和控制提供有效的支持。

7. 了解并掌握一些常用的财务策划方法,能够为企业和个人制定合理的财务规划。

四、备考建议1. 制定合理的学习计划,分配足够的时间和精力进行学习和复习。

在制定计划时,要考虑到自己的学习能力和时间,合理安排各科目的学习时间和顺序。

2. 多做模拟题和真题,熟悉考试题型和难度,提高解题速度和准确性。

同时,通过模拟考试,可以了解自己的优势和不足,从而调整学习策略。

3. 注重知识点的理解和运用,不要死记硬背。

CMA2024年考纲变动分析

CMA2024年考纲变动分析

一、考纲变化总体分析

1.没有主要变化,但部分章节有一些重要的内容更新(详见下表),每科变动比例大约在10%左右;

2.考试形式、题型、各章的考核占比都保持不变;

3.新增一项对考生的要求——参加道德在线课程;

4.新考纲计划于2024年9月份生效。

二、考纲变化具体内容

三、考纲变化问题解答

Q1.适用当前考纲的最后一次考试窗口是什么时候?

A:中文考试——2024年7月27日

英文考试——2024年5-6月

Q2.新考纲的考试时间什么时候开始?

A:中文考试——2024年11月9日

英文考试——2024年9月

Q3.当前考生已经通过的考试部分依然有效吗?

A:是的,只要您的考试准入费在有效期内,您只需要按照新考纲准备另外一科的考试即可。

CMA要考哪些内容

CMA要考哪些内容?考CMA的考生都知道CMA相较于国内传统的财务认证,CMA考试科目不仅不多,而且还很有优势,那么具体都考些什么小编接下来给您说一说。

CMA考试科目总共只有两门课程,分别为P1-财务规划、绩效与控制(主要是对内,优化企业经营管理);P2-财务决策(主要是对外,负责企业战略扩张参与对外经营决策),考试涉及会计、管理、战略、市场、金融等多方面的知识体系,具体如下:Part 1 财务报告、规划、绩效与控制P1主要是针对企业内部运营,提升内部竞争力和整体绩效,帮企业降低成本,提升利润,从而提高绩效。

也就是说P1主要是向内求,提升企业的运营能力。

主要包括:A. 对外财务报告决策(15%)B. 规划、预算编制与预测(30%)C. 绩效管理(20%)D. 成本管理(20%)E. 内部控制(15%)Part 2 财务决策P2主要是针对企业在资本市场怎么样获得利润最大化,向外部要利润:公司理财(投资、融资、控股)、风险管理、决策分析。

就是公司挣钱以后,怎么样把这些钱,再生钱。

也就是说P2主要是向外求来谋求更大的发展。

主要包括:A. 财务报表分析(25%)B. 公司财务(20%)C. 决策分析(20%)D. 风险管理(10%)E. 投资决策(15%)F. 职业道德(10%)此外,CMA分值分布:CMA选择题是375分,简答题是125分,CMA简答题部分的阅卷采取人工阅卷的方式,由ima组成的专家组阅卷,根据采集知识点打分,一道题,你有答对的部分都会酌情给分,不是全盘否定。

最主要的是你要知道题目考察的是哪部分的知识点,否则一错全错。

对于CMA英文考试来说,简答题的正确率只有达到50%方能进入简答题界面,否则考试提前结束。

CMA及格线为360分,只要你选择题+简答题能达到360即可,不必在乎每一部分得多少分。

新cma考试大纲-推荐下载

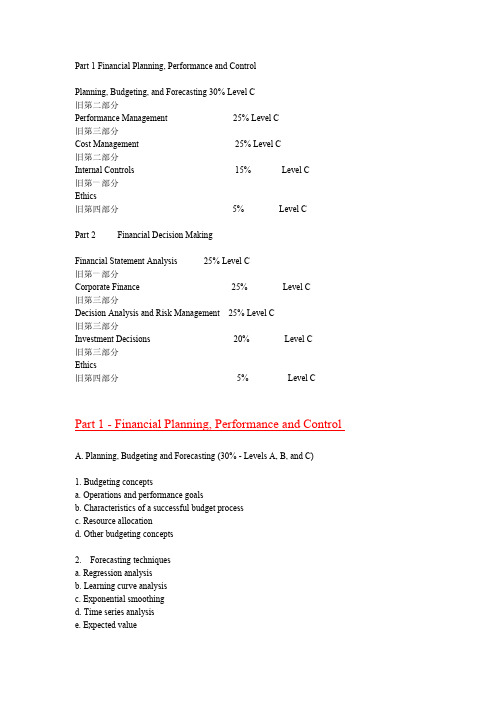

Part 1 Financial Planning, Performance and ControlPlanning, Budgeting, and Forecasting 30% Level C 旧第二部分Performance Management 25% Level C 旧第三部分Cost Management 25% Level C 旧第二部分Internal Controls 15% Level C 旧第一部分 Ethics旧第四部分 5% Level CPart 2 Financial Decision MakingFinancial Statement Analysis 25% Level C 旧第一部分Corporate Finance 25% Level C 旧第三部分Decision Analysis and Risk Management 25% Level C 旧第三部分Investment Decisions 20% Level C 旧第三部分 Ethics旧第四部分 5% Level CPart 1 - Financial Planning, Performance and ControlA. Planning, Budgeting and Forecasting (30% - Levels A, B, and C)1. Budgeting conceptsa. Operations and performance goalsb. Characteristics of a successful budget processc. Resource allocationd. Other budgeting concepts2. Forecasting techniques a. Regression analysis b. Learning curve analysis c. Exponential smoothing d. Time series analysis e. Expected value题,带负荷中资料3. Budgeting methodologiesa. Annual business plans (master budgb. Project budgetingc. Activity-based budgetingd. Zero-based budgetinge. Continuous (rolling) budgetsf. Flexible budgeting4. Annual profit plan and supporting schedulesa. Operational budgetsb. Financial budgetsc. Capital budgets5. Top-level planning and analysisa. Pro forma incomeb. Financial statement projectionsc. Cash flow projectionsB. Performance Management (25% - Levels A, B, and C)1. Cost and variance measuresa. Comparison of actual to planned resultsb. Use of flexible budgets to analyze performancec. Management by exceptiond. Use of standard cost systemse. Analysis of variation from standard cost expectations2. Responsibility centers and reporting segmentsa. Types of responsibility centersb. Transfer pricing modelsc. Reporting of organizational segments3. Performance measuresa. Product profitability analysisb. Business unit profitability analysisc. Customer profitability analysisd. Return on investmente. Residual incomef. Investment base issuesg. Effect of international operationsh. Critical success factorsi. Balanced scorecardC. Cost Management (25% - Levels A, B, and C)1. Measurement conceptsa. Cost behavior and cost objectsb. Actual and normal costsc. Standard costsd. Absorption (full) costinge Variable (direct) costingf. Joint and by-product costing2. Costing systemsa. Job order costingb. Process costingc. Activity-based costingd. Life-cycle costing3. Overhead costsa. Fixed and variable overhead expensesb. Plant-wide versus departmental overheadc. Determination of allocation based. Allocation of service department costs4. Operational Efficiencya. Just-in time manufacturingb. Material requirements planning (MRP)c. Theory of constraints and throughput costingd. Capacity management and analysis5. Business process performancea. Value chain analysisb. Value-added conceptsc. Process analysisd. Benchmarkinge. Activity-based managementf. Continuous improvement conceptsg. Best practice analysish. Cost of quality analysisD. Internal Controls (15% - Levels A, B, and C)1. Risk assessment, controls, and risk managementa. Internal control structure and management philosophyb. Internal control policies for safeguarding and assurancec. Internal control riskd. Implications of the Sarbanes-Oxley Act of 2002e. U.S. Foreign Corrupt Practices Act internal control requirementsf. COSO Internal Control Framework2. Internal auditinga. Responsibility and authority of the internal audit functionb. Types of audits conducted by internal auditors3. Systems controls and security measuresa. General accounting system controlsb. Application and transaction controlsc. Network controlsd. Flowcharting to assess controlse. Backup controlsf. Disaster recovery proceduresE. Professional Ethics (5% - Levels A, B, and C)1. Ethical considerations for management accounting and financial management professionalsa. Provisions of IMA’s “Statement of Ethical Professional Practice”b. Evaluation and resolution of ethical issues such as:ƒ Fraudulent reportingƒ Manipulation of analyses and resultsƒ Unethical behavior in developing budgets and standardsƒ Manipulation of decision factorsPart 2- Financial Decision MakingA. Financial Statement Analysis (25% - Levels A, B, and C)1. Basic Financial Statement Analysisa. Common size financial statementsb. Common base year financial statementsc. Growth analysis2. Financial Performance Metrics – Financial Ratiosa. Liquidityb. Leveragec. Activityd. Profitabilitye. Market3. Profitability analysisa. DuPont analysisb. Income measurement analysisc. Revenue analysisd. Cost of sales analysise. Expense analysisf. Variation analysis4. Analytical Issues in Financial Accountinga. Impact of foreign operationsb. Effects of changing prices and inflationc. Off-balance sheet financingd. Cash Flow Statement reconciliation to Income Statemente. Impact of changes in accounting treatmentf. International Financial Reporting Standards (IFRS)g. Fair value accountingh. Differences in accounting and economic concepts of value and incomei. Earnings qualityB. Corporate Finance (25% - Levels A, B, and C)1. Risk and returna. Calculating returnb. Types of riskc. Relationship between risk and returnd. Risk and return in a portfolio contexte. Diversificationf. Asset pricing models2. Managing financial riska. Portfolio managementb. Hedgingc. Financial risk management3. Financial instrumentsa. Term structure of interest ratesb. Bondsc. Debt managementd. Common stocke. Preferred stockf. Options and other derivativesg. Valuation of financial instruments4. Cost of capitala. Weighted average cost of capitalb. Cost of individual capital componentsc. Calculating the cost of capitald. Marginal cost of capital5. Managing current assetsa. Working capital terminologyb. Cash managementc. Marketable securities managementd. Accounts receivable managemente. Inventory managementf. Types of short-term creditg. Minimizing the cost of short-term credit6. Raising capitala. Financial markets and regulationb. Market efficiencyc. Financial institutionsd. Initial public offeringse. Secondary offeringsf. Dividend policy and share repurchasesg. Private placementsh. Lease financing7. Corporate restructuringa. Mergers and acquisitionsb. Divestituresc. Bankruptcy8. International financea. Fixed, flexible and floating exchange ratesb. Managing transaction exposurec. Financing international traded. Transfer pricing tax implicationse. Political riskC. Decision Analysis and Risk Management (25% - Levels A, B, and C)1. Cost/volume/profit analysisa. Breakeven analysisb. Profit performance and alternative operating levelsc. Analysis of multiple products2. Marginal analysisa. Sunk costs, opportunity costs and other related conceptsb. Marginal costs and marginal revenuec. Special orders and pricingd. Make versus buye. Sell or process furtherf. Add or drop a segmentg. Capacity considerations3. Pricinga. Market comparablesb. Setting pricesc. Target costingd. Elasticitye. Product life cycle considerationsf. Market structure considerations4. Risk assessmenta. Risk identification and exposureb. Definition and scope of operational risk, hazard risk, financial risk and strategic riskc. Risk mitigation strategiesd. Enterprise Risk ManagementD. Investment Decisions (20% - Levels A, B, and C)1. Capital budgeting processa. Stages of capital budgetingb. Incremental cash flowsc. Income tax considerations2. Discounted cash flow analysisa. Net present valueb. Internal rate of returnc. Comparison of NPV and IRR3. Payback and discounted paybacka. Uses of payback methodb. Limitations of payback methodc. Discounted payback4. Ranking investment projectsa. Ranking methodsb. Capital rationingc. Mutually exclusive projects5. Risk analysis in capital investmenta. Sensitivity analysisb. Certainty equivalentsc. Real options6. Valuationa. Discounted cash flow modelsb. Multiples modelsc. Valuation for acquisitions and divestituresd. Discount ratesE. Professional Ethics (5% - Levels A, B, and C)2. Ethical considerations for the organizationa. Anti-bribery provisions of the U.S. Foreign Corrupt Practices Actb. Provisions of IMA’s Statement on Management Accounting, “Values and Ethics: From Inception to Practice”c. Corporate responsibility for ethical conduct。

2024年cma考试新考纲

2024年cma考试新考纲

2024年CMA考试将采用新考纲,具体内容如下:

1. 考试内容将更加注重实际应用和问题解决能力的考察,而不仅仅是理论知识的掌握。

2. 考试形式将更加灵活多样,包括选择题、简答题、案例分析题等多种形式,以全面考察考生的综合素质。

3. 考试难度将有所提高,要求考生具备更深入的理解和更高水平的分析能力。

新考纲的实施将有助于提高CMA考试的水平和质量,确保考试结果更加准确、客观、公正。

同时,新考纲也将为考生提供更加广阔的视野和更加深入的洞察力,帮助他们更好地适应不断变化的市场需求和提升自己的职业发展。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

控制程序

Control Procedures

第四章:内部控制

Section D: Internal Controls

1

第一节:风险评估、控制和风险管理

Topic 1: Risk Assessment, Controls, and Risk Management

2

风险

Risk

风险 – 暴露于某种情况的敞口,增加损失的可能性 风险 – P(t) ×P(f) ×(损失金额) 最小化风险 – 预防威胁发生,增加系统控制和保险 影响风险的因素 – 独立检查的频率,控制方法的足够程度、 沟通的足够程度,执行控制的一贯性,资产的访问限制或 物理控制 Risk – exposure to circumstance, increase likelihood of loss, Risk = P(t) × P(f) ×(Amount of Loss) Minimize risks – preventing threats from occurring, increasing system controls, insuring. Factors affecting risk – frequency of independent check, adequacy of controls methods, adequacy of communication, consistency of enforcement of control, limit access to or physical control of asset

Effective Control Principles

Control principle – internal control feature, protect a firm’s assets and ensure data is reliable Compatibility principle – in harmony with organizational and human factors of the business Flexibility principle – flexible enough to allow the volume of transaction to grow and changes to be made Cost-benefit principle - benefits must be greater than the system’s costs, both tangible or intangible 8

会计系统

会计系统 – 财务会计系统和经营信息系统,可靠与完整

Auditor responsibility under SOX – annual report include a report on internal control, follow a risk-based approach, principle-based apprห้องสมุดไป่ตู้ach, top down risk assessment approach, four steps in TDRA, page 328

信息和沟通 – 相关信息必须被识别、捕捉和交流,形式和 时间框架,成功地完成工作 监控 – 持续的管理行为,独立的评估或两者相结合,内部 审计师、审计委员会、披露委员会以及管理层

Information and communication – relevant information must be identified, captured and communicated, form and time frame, to do job successfully Monitoring – ongoing management activities, separate evaluation, internal auditors, audit committee, disclosure committee, as well as management

7

设计内部控制来处理风险 Design Controls to Address Risks 有效控制原则

控制原则 – 内部控制特征,保护公司资产,数据可靠 兼容性原则 – 与组织和人员因素保持一致 灵活性原则 – 允许交易量增长和组织结构变化 成本-利益原则 - 利益必须大于成本,有形与无形

Control Environment

Accounting System

Accounting system – financial accounting system and operation information system, reliable and integrity 11

控制程序

控制活动 - 政策和流程,风险反应被有效执行,六个控制 活动 Control environment – management philosophy and appetite for risk

Risk assessment – determining probability and degree of importance, inherent or residual

内部控制结构和管理理念 Internal Control Structure and Management Philosophy 控制环境

控制环境 – 管理层和董事会设定控制环境 董事会和审计委员会 – 负有最终责任,设定业务的整体目 标,确保股东的最佳利益,审计总监直接向COO和审计委 员会报告,独立董事,至少一位财务专家

Control activities – policies and procedures, risk response are effectively carried out, six control activities, page 323

6

设计内部控制来处理风险 Design Controls to Address Risks

4

风险 可接受审计风险

Risk

可接受审计风险 – 审计失败的可能性,取决于三种风险类 型,代表审计师愿意接受的审计失败的风险 取决于以下三个因素 – 管理层正直,财务报表使用者数量, 被审单位的财务状况 Acceptable audit risk – probability of audit failure, a function of three types of risk, risk the auditor is willing to take that the audit will fail a function of three things – management integrity, number of financial statement users, the auditee’s financial condition

Control Environment

Control environment – management and board set the environment Board of directors and audit of committee – bear final responsibility, sets broad purposes of operation, ensure in the best interest of shareholders, audit director reporting directly to the COO and the audit committee, audit committee consist of independent director, at least one should be financial expert

Control Procedures

一般控制和具体控制,每个一般控制都有至少一个相应的 具体控制 资产的保护 – 物理控制,处理事务的职能分离,访问控制 符合法律法规 – 法律、法规、政策、计划、流程 组织目标和目的的实现 – 效果 General control and specific control, each general control has at least one corresponding specific control Safeguarding of Assets – physical control, segregation of function in processing transaction, access control Compliance with applicable laws and regulations – law, regulation, policies, plans and procedures Accomplishment of organization goals and objectives effectiveness

Control Environment

10

内部控制结构和管理理念 Internal Control Structure and Management Philosophy 控制环境

2002年萨班斯-奥克斯利法案关于审计师的责任 – 年度报 告中包含内部控制报告,风险为基础的方法,原则为基础 的方法,自上而下的风险评估方法,TDRA的四个步骤

3

风险 风险种类

Risk

固有风险 – 当没有内部控制时,财务报表出现重大虚假陈 述的可能性,错误和舞弊,胜任力和正直 控制风险 – 公司的内控措施不能预防或发现超出接受范围 的虚假陈述,控制失效 失侦风险 – 审计证据没有能够发现超出可接受审险的虚假 陈述