芬斯特拉版《国际宏观经济学》课后习题答案第4章

第4章作业题答案,4174

宏观第四章作业答案1题.(a) IS 曲线上的每一点都代表产品市场中的一个均衡。

于是我们可以从商品市场的均衡条件即总收入等于总支出来推导IS 曲线,由给出的第一、二、三、四,四个等式可得: 0.8(10.5)90050800Y C I G Y i =++=×−×+−+⇒0.4170050Y i ×=−(170050)/0.44250125Y i i ⇒=−=−这就是IS 曲线。

(b) IS 曲线表示产品市场均衡时的利率和收入水平的组合。

它描述了利率和收入的反向变动关系,利率下降会导致支出增加,从而厂商的实际产出增加,收入增加。

(c) LM 曲线上的每一点都代表了货币市场的一个均衡。

于是我们可以从货币市场的均衡条件即货币供给等于货币需求来推导LM 曲线,由(P5)(P6)可得:5000.2562.5(50062.5)/0.25ML Y i Y i P=⇒=×−⇒=+ 2000250Y i ⇒=+这就是LM 曲线。

(d) LM 曲线代表了货币市场处于均衡时候的利率与收入水平的组合,即货币供给等于货币需求时候的利率和收入水平的组合。

它描述了利率和收入水平的同向变动关系,收入增加会引起实际货币余额的需求增加,在货币供给不变的情况下,会导致利率的提高,利率的提高又会减少实际货币余额的需求,并使之重新回到原来的需求水平,与货币供给相等。

(e) IS 曲线和LM 曲线的交点代表了收入和利率的均衡水平。

在这个例子中,有:4250125200025037522506IS LM i i i i ∗=⇒−=+⇒=⇒= 4250125425012563500Y i ∗∗=−=−×=即均衡收入水平是3500,均衡利率是6。

(f) 在IS 曲线和LM 曲线的交点处产品市场和货币市场同时处于均衡,在产品市场,自主支出等与实际产出等于总收入,在货币市场,货币供给等于货币需求。

利率和收入都没有进一步改变的倾向。

宏观经济学-第4章习题答案

第四章生产论南方医科大学2010级经济学(医药贸易与管理方向)W洋1. 下面(表4—1)是一张一种可变生产要素的短期生产函数的产量表:表4—1(2)该生产函数是否表现出边际报酬递减?如果是,是从第几单位的可变要素投入量开始的?解答:(1)利用短期生产的总产量(TP)、平均产量(AP)和边际产量(MP)之间的关系,可以完成对该表的填空,其结果如表4—2所示:表4—2开始逐步下降的这样一种普遍的生产现象。

本题的生产函数表现出边际报酬递减的现象,具体地说,由表4—2可见,当可变要素的投入量从第4单位增加到第5单位时,该要素的边际产量由原来的24下降为12。

2. 用图说明短期生产函数Q=f(L, eq \o(K,\s\up6(-)) )的TP L曲线、AP L曲线和MP L曲线的特征及其相互之间的关系。

解答:短期生产函数的TP L曲线、AP L曲线和MP L曲线的综合图如图4—1所示。

图4—1由图4—1可见,在短期生产的边际报酬递减规律的作用下,MP L曲线呈现出先上升达到最高点A以后又下降的趋势。

从边际报酬递减规律决定的MP L曲线出发,可以方便地推导出TP L曲线和AP L曲线,并掌握它们各自的特征及相互之间的关系。

关于TP L曲线。

由于MP L= eq \f(d TP L,d L) ,所以,当MP L>0时,TP L曲线是上升的;当MP L<0时,TP L曲线是下降的;而当MP L=0时,TP L曲线达最高点。

换言之,在L =L3时,MP L曲线达到零值的B点与TP L曲线达到最大值的B′点是相互对应的。

此外,在L<L3即MP L>0的范围内,当MP′L>0时,TP L曲线的斜率递增,即TP L曲线以递增的速率上升;当MP′L<0时,TP L曲线的斜率递减,即TP L曲线以递减的速率上升;而当MP′=0时,TP L曲线存在一个拐点,换言之,在L=L1时,MP L曲线斜率为零的A点与TP L曲线的拐点A′是相互对应的。

宏观经济学习题参考答案(部分)

宏观经济学习题参考答案(部分)宏观经济学习题参考答案(部分)本人精心整理的文档,文档来自网络本人仅收藏整理如有错误还请自己查证!宏观经济学习题参考答案(部分)第一章国民收入的核算一、选择题1、D2、C3、A4、C5、B6、B7、A8、E9、C 10、B11、A 12、B 13、E 14、B 15、C16、C 17、A 18、C 19、E 20、C21、C 22、B 23、D 24、D 25、A26、B 27、A二、填空题1. 国民生产总值2. 资本消耗折旧3. 居民厂商政府国际市场4. 用物品和劳务来满足自己需要的行为5. 投资6. 储存不是用于目前消费的收入的行为7. 更新投资净投资8.居民的储蓄厂商的储蓄折旧费不分配的利润9. 增加值10.支出法三、名词解释1.实际国民生产总值是以具有不变购买力的货币单位衡量的国民生产总值国民生产总值通常是以现行货币单位来表现一国在一定时期(通常为一年)内的全部社会最终产品和劳务的总和但由于通货膨胀和通货紧缩会抬高或降低物价因为会使货币的购买力随物价的波动而发生变化为了消除价格变动的影响一般是以某一年为基期以该年的价格为不变价格然后用物价支书来矫正按当年价格计算的国民生产总值而计算出实际国民生产总值2、当前收入中不用于消费的部分即收入减去消费如寸入银行的存款、购买的有价证券、保存在手中的货币等都称为储蓄储蓄包括政府机构储蓄、企业储蓄和个人及家庭储蓄三种国民生产总值(GNP)是以国民原则来核算的国民收入它被定义为经济社会在一定时期(通常是一年)内运用生产要素所生产的全部最终产品的市场价值GNP是一个市场价值概念它测度的是最终产品而不是中间产品的价值是一定时期内所生产而不是所售卖的最终产品价值是流量而不是存量四、计算题(1)按收入法计算GNP得GNP=工资+利息+租金+利润=100+10+30+30=170(2)按支出法计算GNP得GNP=消费+投资+政府支出+(出口-进口)=90+60+30+(60-70)=170(亿元)(3)所得税-转移支付=30-5=25(亿元)所以政府预算赤字=政府支出-政府收入=30-25=5(亿元)(4)家庭将收入分配为消费、储蓄或税收因此收入=消费+储蓄+(税收-转移支付)所以储蓄=收入-消费-(税收-转移支付)=170-90-25=55(亿元)或者由等式(投资-储蓄)+(政府支出-政府收入)+(出口-进口)=0得储蓄=(政府支出-政府收入)+(出口-进口)+投资=5+(60-70)+60=55(亿元)(5)净出口=出口-进口=60-70=-10(亿元)第二章国民收宏观经济学习题参考答案(部分)入的均衡一、选择题1、D2、D3、B4、A5、A6、B7、D二、填空题1. 消费支出可支配收入2. 越大右上方3. 消费支出可支配收入4. 边际消费倾向5. 储蓄可支配收入6. 越多右上方7. 平均储蓄倾向8. 储蓄增量与可支配收入增量之比9. 同反10.自发投资三、名词解释1、消费函数现代西方经济学所谓的消费函数是指消费与决定消费的各种因素之间的依存关系但凯恩斯理论假定在影响消费的各种因素中收入是消费的唯一的决定因素收入的变化决定消费的变化随着收入的增加消费也会增加但是消费的增加不及收入的增加多收入和消费两个经济变量之间的这种关系叫做消费函数或消费倾向2、储蓄函数储蓄与决定储蓄的各种因素之间的依存关系是现代西方经济学的基本分析工具之一由于在研究国民收入决定时假定储蓄只受收入的影响故储蓄函数又可定义为储蓄与收入之间的依存关系四、计算题(1)在C=120+0.75y中令C=1120得y=1333(2)从消费函数知MPC=0.75从而MPS=0.25(3)在C=120+0.75y中令y=3000得C=2370第三章国民收入的变化一、单项选择题1、B2、B3、C4、D5、A6、C7、D8、B9、B二、多项选择题1.AC三、填空题1. 消费支出投资政府支出出口2. 储蓄政府税收进口3. 投资的增加所引起的国民收入增加的倍数1/(1-MPC)4. 具有5. 越大6. 增加支出减少税收增加同量的支出和税收7. 1(1-MPC)MPC/(1-MPC)8. 平衡预算9. 为了达到充分就业的国民收入总支出曲线向上移动的距离10. 为了消除通货膨胀总支出曲线向下移动的距离四、计算题1、(1)由Y=C+I0得Y=8000(亿元)从而C=6500(亿元)S=1500(亿元)I=1500(亿元)(2)因为△I=250(亿元)K=1/(1-MPC)=1/(1-0.75)=4所以△Y=K*△I=4*250=1000(亿元)于是在新的均衡下收入为8000+1000=9000(亿元)相应地C=7250(亿元)S=1750(亿元)(3)若消费函数斜率增大即MPC增大则乘数亦增大反之相反2、(1)可支配收入:Yd=Y-Tn=Y-50消费C=30+0.8(Y-50)=30+0.8Y-40=0.8Y-10均衡收入:Y=C+I+G=0.8Y-10+60+50+50-0.05Y=0.75Y+150得Y=150/0.25 =600......均衡收入(2)净出口余额:NX=50-0.05Y =50-0.05×600=20(3)KI=1/(1-0.8+0.05)宏观经济学习题参考答案(部分)=4(4)投资从60增加到70时Y=C+I+G+NX=0.8Y-10+70+50+50-0.05Y=0.75Y+160 160得Y =150/0.25 =640......均衡收入净出口余额:NX=50-0.05Y=50-0.05×640=50-32=18(5)当净出口函数从NX=50-0.05Y变为X=40-0.05Y时的均衡收入:Y=C+I+G+X=0.8Y-10+60+50+40-0.05Y=0.75Y+140得Y=140/0.25 =560......均衡收入净出口余额NX=40-0.05Y=40-0.05×560=40-28=12(6)自发投资增加10使均衡收入增加40(640-600=40)自发净出口减少10(从NX=50-0.05Y变为NX=40-0.05Y)使均衡收入减少额也是40(600-560=40)然而自发净出口变化对净出口余额的影响更大一些自发投资增加10时净出口余额只减少2(20-18=2)而自发净出口减少10时净出口余额减少8(20-12=8)五、论述题乘数也叫倍数宏观经济学中所运用的乘数是指国民收入函数中由于某个自变量的变化而引起的国民收入的变化投资乘数是指投资量变化数与国民收入变化数的比率它表明投资的变动将会引起国民收入若干倍的变动投资之所以具有乘数作用是因为各经济部门是相互关联的某一部门的一笔投资不仅会增加本部门的收入而且会在国民经济各部门引起连锁反应从而增加其他部门的投资与收入最终使国民收入成倍增长发挥投资乘数作用有三个前提条件:(1)在消费函数或储蓄函数为即定的条件下一定的投资可以引起收入的某种程度的增加即投资的乘数作用可以相当顺利地发挥出来(2)要有一定数量的劳动力可以被利用(3)要有一定数量的存货可以被利用第四章宏观财政政策一、单项选择题1、A2、D3、C4、A5、B6、B7、A8、A9、B 10、A二、填空题1. 通货紧缩通货膨胀2. 财政支出财政收入3. 政府通过改变支出来影响国民收入水平4. 财政收入政策5. 累进的税收制度福利社会支出制度厂商和居民的储蓄6. 增加抑制减少阻碍7. 增加扩张减少收缩8. 直接税间接税公司收入税9. 赤字10. 当政府用增税的方法来偿还债务时人们为了逃避高税率而减少工作时间第五章货币的需求和供给一、填空题1. 人们普遍接受的交换媒介2. 交换媒介计算单位价值储蓄延期支付的手段3. 把货币留在手中的偏好4. 交易预防投机交易余额预防余额投机宏观经济学习题参考答案(部分)余额5. 国民收入利息率6. 作为货币单位的基础的商品7. 货币供给量8. 纸币硬币9. 商业银行的活期存款10. 通货活期存款M1-A 可转让的提款单ATS第六章货币对经济的影响一、填空题1. 货币需求货币供给2. 货币需求量利息率右下方3. 垂直4. 利息率5. 向右下降6. 投资支出利息率右下方7. 货币需求量对利息率变化反映的敏感程度8. 投资的利息弹性9. 货币数量的增加已不能降低利息率10. 价格水平货币数量二、单项选择题1、B2、C3、A4、D5、B6、D7、A8、D9、C第七章宏观货币政策一、单项选择题1、D2、B3、D4、C5、D6、A7、A8、C二、多项选择题1、ABC2、AC三、简答题1、中央银行的主要货币政策工具是:公开市场活动准备金要求以及贴现率2、中央银行的两种主要负债是:中央银行发行的、在流通中的通币以及商业银行在中央银行的存款3、持有货币的三种主要动机是:交易动机预防动机以及投机动机4、有许多货币的组成部分并不支付利息例如通货和活期存款利率是持有货币的机会成本持有货币没有支付利息但放弃了用于其他金融资产时所能得到的利息收入当利息上升时持有货币的成本就增加了因此人们就要减少自己的货币持有量并用货币去购买其它金融资产以便获得更高的利率四、计算题(1)货币乘数时货币供给量(M)与货币基础(MB)的比率:mm=M/MB=5000亿/2022年亿=2.5(2)可以计算a=C/D,b=R/D并用第一题的公式计算货币乘数:a=C/D=1000亿/5000亿=0.2b=R/D=500亿/5000亿=0.1mm= 1+a/a+b = 1+0.2/0.2+0.1 = 1.2/0.3 = 4(3)题中已经给出b=R/D=0.1,但仍需计算a=C/D.从题中可以知道C的值但不知道D的值我们可以根据已知的b和R计算出D=R/b因此D=R/b=500亿/0.1=5000亿a=C/D=1500/5000=0.3mm=1+a/a+b=1+0.3/0.3+0.1=1.3/0.4=3第八章国民收入和货币的均衡一、单项选择题1、A2、A3、B4、C5、A6、A7、C8、D9、C二、多项选择题1、ABD三、名词解释:1、IS曲线--在产品市场达到均衡时收入和利率的各种组合的点的轨迹在两部门经济中IS曲线的数学表达式为I(r)=S(Y)它的斜率为负这表明IS曲线一般是一条向右下方倾斜的曲线一般来说在产品市场上位于IS曲线右方的收入宏观经济学习题参考答案(部分)和利率的组合都是投资小于储蓄的非均衡组合;位于IS曲线左方的收入和利率的组合都是投资大于储蓄的非均衡组合只位于IS曲线上的收入和利率的组合才是投资等于储蓄的均衡组合2、LM曲线--表示货币市场中货币供给等于货币需求时收入与利率的各种组合的点的轨迹LM曲线的数学表达式为M/P=ky-hr 它的斜率为正这表明LM曲线一般是向右上方倾斜的曲线一般说来在货币市场上位于LM曲线右方的收入和利率的组合都是货币需求大于货币供给的非均衡组合位于LM曲线左方的收入和利率的组合都是货币需求小于货币供给的非均衡组合只有位于LM曲线上的收入和利率的组合才是货币需求等于货币供给的均衡组合3、凯恩斯陷阱--又称流动偏好陷阱或流动性陷阱指由于流动偏好的作用利息不再随货币供给量的增加而降低的情况西方经济学认为利息是人们在一定时期内放弃流动偏好的报酬利息率的高低取决于货币的供求流动偏好代表了货币的需求货币数量代表了货币的供给货币数量的多少由中央银行的政策决定货币数量的增加在一定程度上可以降低利息率但是由于流动偏好的作用低于这一点人们就不肯储蓄宁肯把货币保留在手中四、简答题1、计划的总支出是包括自发支出与引致支出在IS-LM模型分析中自发支出取决于利率引致支出取决于实际国民生产总值所以只有当利率与实际国民生产总值为某一特定值的结合时所决定的计划的总支出才能与实际国民生产总值相等从而实现物品市场的均衡2、极端的凯恩斯主义者认为当存在流动性陷阱时人们在即定的利率时愿意持有任何数量的货币所以LM曲线为一条水平线自发支出的增加使IS曲线向右方移动实际国民生产总值增加而利率不变由于财政政策所引起的自发支出增加不会引起利率上升所以也就没有挤出效应财政政策的作用最大而且流动陷阱的情况在现实中是存在的第九章国民收入和价格水平的均衡一、单项选择题1、B2、A3、A4、B5、B6、C7、C8、A9、D第十章失业和通货膨胀一、单项选择题1、A2、B3、B4、B5、B6、D7、B二、多项选择题1、ACE2、ABC3、AC4、AB三、简答题:滞胀(或译停止膨胀)就是实际国民生产总值增长率停滞(不增长甚至下降)与通货膨胀率加剧并存的状况第十一章经济周期一、单项选择题1、C2、B3、B4、B5、A6、A7、C8、A9、A第十二、十三章经济的增长和发展一、单项选择宏观经济学习题参考答案(部分)题1、B2、A3、C4、C5、B6、B7、A8、C9、C 10、A11、D 12、C 13、D 14、A 15、B16、A 17、B 18、D二、简答题1、人均生产函数表明了在技术为既定的情况下人均产量如何随人均存量增加而增加如果资本积累率提高那么人均资本存量也就更迅速地提高这就意味着人均产量迅速增长即更高的增长率可以用沿着人均生产函数的变动来说明这一点2、有几种方法可以克服经济增长的障碍其中已被证明最成功的一种是较为自由的国际贸易的扩大香港、新加坡等国家或地区通过生产自己具有比较优势的产品迅速地增加了人均收入获得国际贸易的好处3、在哈罗德- 多马模型G= S/V 中V=4G=7%从而S=G?V=7%×4=28%三、论述题1、英国经济学家哈罗德、美国经济学家多马把凯恩斯理论的短期比较静态分析扩展为长期动态分析在凯恩斯就业理论的基础上分别建立了自己的增长模型由于二者基本内容大致相同通称为哈罗德-多马模型(1)哈罗德模型哈罗德指出凯恩斯收入均衡论的局限性认为要保证经济长期均衡增长必须要求投资保持一定的增长率为分析实现经济稳定增长的均衡条件哈罗德建立了经济增长模型假设条件有:①全社会只生产一种产品不用于消费部分都用于投资②储蓄倾向不变储蓄由收入水平决定③社会生产中只有劳动和资本两种生产要素两种要素的比例不变而且每单位产品消耗的生产要素也不变④技术水平不变边际资本系数等于平均资本系数即资本产量比率不变⑤资本和劳动的边际生产率递减(2)多马模型投资两重性:一方面投资增加有效需求和国民收入即扩大了需求另一方面投资还增加了资本存量和生产能力即扩大了供给多马认为:通过增加投资解决失业问题就必须在下一时期增加更多的支出(需求)才能保证新增加的资本存量及其潜在的生产能力得到充分利用(3)哈罗德-多马模型的理论观点把哈罗德-模型和多马模型合在一起从哈罗德-多马模型出发可得出以下三个观点①经济稳定增长的条件当一定得合意储蓄率与合意得资本-产量比率决定的经济增长率是有保障的增长率时社会经济就能够实现稳定增长②短期经济波动的原因如果实际增长率与有保障的增长率不相等就会引起经济波动实际增长率和有保证的增长率一致是很少见的、偶然的所以社会经济必然要出现波动在收缩和扩张的交替中发展③经济长期波动的原因有保证的增长率和自然增长率之间的关系变化成为经济社会长期波动的原因宏观经济学习题参考答案(部分)(4)哈罗德-多马模型的理论基础是凯恩斯主义理论它不仅在理论上是投资等于储蓄这一公式的长期化与动态化而且在分析中也沿用了凯恩斯主义的某些脱离现实的抽象心理概念例如对经济增长具有重要作用的有保证的增长率是资本家感到满意并准备继续下去的增长率这里所强调的仍然是资本家的心理预测即凯恩斯所说的资本边际效率这样就和凯恩斯同样把资本家的乐观或悲观的情绪扩大为决定经济发展的因素哈罗德-多马模型关于短期与长期经济波动的分析和其他经济周期理论一样否认了波动的根本原因--资本主义社会的基本矛盾用一些抽象的技术经济关系来说明经济波动的产生哈罗德虽然也承认资本主义社会经济波动的必然性但他仍然相信资本主义是可以实现稳定的长期增长的他的整个分析正是为实现这种稳定增长而出谋划策当然对哈罗德-多马模型如果加以改造或使用不同的解释也可以为我们所借鉴例如把哈罗德-多马模型的储蓄率(s)解释为积累率把产量-资本之比(1/c)解释为投资的经济效果即每单位增加的可以造成的产量的增加那么该模型的公式即可变为国民收入增长率=积累率×投资的经济效果或G= s 1/c式中:投资的经济效果为资本-产出之比的倒数至少在理论上它的数值式可能被事先估算出来的在已知投资经济效果的情况下哈罗德-多马模型可以被认为是表明国民收入增长率和积累率之间的数量关系的公式。

宏观经济学课后习题答案

宏观经济学课后习题答案!!第一章导论1.(1)宏观经济学研究的问题是一个国家整体经济的运行情况以及政府如何运用经济政策来影响国家整体经济的运作。

其核心是国民收入决定理论和就业理论。

(2)宏观经济学研究的是总体经济问题,它涉及经济中商品与劳务的总产出及其增长速度、通货膨胀与失业的程度、经济衰退及其原因、国际收支状况及汇率的变动等。

2.(1)宏观经济学与微观经济学的区别:①研究对象不同。

微观经济学的研究对象是单个经济单位,如家庭、厂商等。

宏观的研究对象则是整个经济,研究整个经济的运行方式与规律,从总量上分析经济问题。

②解决的问题不同。

微观解决的是资源配置问题,即生产什么、如何生产和为谁生产的问题,以实现个体效益的最大化。

宏观则把资源配置作为既定的前提,研究社会范围内的资源利用问题,以实现社会福利的最大化。

③研究方法不同。

微观的研究方法是个量分析,即研究经济变量的单项数值如何决定。

宏观则是总量分析,即对能够反映整个经济运行情况的经济变量的决定、变动及其相互关系进行分析。

④基本假设不同。

微观的基本假设是市场出清(在给定的价格P之下,市场上的意愿供给等于意愿需求,达到均衡状态)、完全理性、充分信息,认为“看不见的手”能自由调节实现资源的优化配置。

宏观则是既定市场机制是不完善的,政府有能力调节经济,通过“看得见的手”纠正市场机制的缺陷。

⑤中心理论不同。

微观的中心理论是价格理论,还包括消费者行为理论、生产理论、分配理论、一般均衡理论、市场理论、产权理论、福利经济学、管理理论等。

宏观的中心理论则是国民收入决定理论,还包括失业与通货膨胀理论、经济周期理论与经济增长理论、开放经济理论等。

(2)宏观经济学与微观经济学的联系:①微观经济分析是宏观经济分析的基础,离开了微观分析这一基础,宏观分析将成为空中楼阁。

②从根本目标上看,宏观经济分析与微观经济分析也是一致的。

③宏观经济学与微观经济学虽然分析的侧重点不同,但二者是不能分开的。

宏观经济学第四章习题及答案

第四单元财政政策与货币政策本单元所涉及到的主要知识点:1.宏观经济政策目标及其种类;2.财政制度及其自动稳定器;3.财政政策与“挤出效应”;4.平衡预算、功能财政与赤字对经济的影响;5.货币乘数;6.货币政策工具与货币政策;7.财政政策与货币政策的组合及其效果比较。

一.单项选择1.扩张性财政政策的本质是(D )。

a.货币供给扩张; b.政府规模扩大;c.物价更稳定; d.增加GDP。

2.紧缩性财政政策的本质是(D )。

a.货币供给紧缩; b.政府规模缩小;c.实现物价稳定; d.减少GDP。

3.以下( D)不能视为自动稳定器。

a.失业救济; b.累进税;c.社会保障; d.国防开支。

4.财政盈余与( B)对均衡GDP水平的影响效果相同。

a.储蓄减少; b.储蓄增加;c.消费增加; d.投资增加。

5.投资支出急剧减少的情况下,为保证经济维持在充分就业状态政府应(C )。

a.使税收和政府支出相等; b.使税收超过政府支出;c.使政府支出超过税收; d.提高税率。

6.如果社会总需求的构成是消费1000亿元,投资400亿元,净出口100亿元,政府购买支出200亿元;充分就业的GDP为1200亿元。

为使价格水平保持稳定政府应( A )。

a.提高税率,并减少政府支出;b.通过降低政府债券的利息率来减少私人储蓄;c.增加政府支出;d.通过降低公司所得税率来鼓励私人投资。

7.经济处于严重衰退时,适当的经济政策应当是( B )。

a.减少政府支出; b.降低利息率;c.使本国货币升值; d.提高利息率。

8.下列叙述中(A )是正确的。

a.内在稳定器能部分地抵消经济波动;b.内在稳定器无法缓解失业;c.内在稳定器可以完全抵消任何经济波动;d.以上都不对。

9.拉弗曲线表明( D )。

a.税率越高,总税收额越高; b.税率越高,总税收额越低;c.税率与总税收额之间不相关; d.某一税率水平上税收总额最大。

10.以下( A )的财政政策是彻底反周期波动的。

宏观经济学课后答案第四章

第四章一、名词解说一般均衡:经过生产因素市场和商品市场以及这两种市场互相之间的供应和需求力量的互相作用,每种商品和生产因素的供应量与需求量在某一价钱下同时趋于相等,社会经济将达到全面均衡状态。

交易动机:指个人和公司为了进行正常的交易活动而需要足够的钱币,现金来支付开发。

慎重动机:为预防不测支出而拥有部分钱币的动机。

投灵活机:人们为了抓住有益的购置有价证券的机遇而拥有一部分钱币。

流动偏好:是指因现金存在流动性,令人们更希望拥有更多的现金。

资本边沿效率:是一种使一项资本物件的使用期内各样预期利润的现值之和等于这项资本品的供应价钱或许重置成本的贴现率。

二、单项选择题1、一般来说,A 、为正ISB曲线的斜率(、为负 CB)、为零D、等于 12、在其余条件不变的状况下,政府购置增添会使IS 曲线( B)A 、向左挪动B 、向右挪动 C、保持不变 D、发生转动3、依据凯恩斯的看法,人们拥有钱币事因为(D)A、交易动机 B 、慎重动机 C 、投灵活机 D、以上都正确4、投资需求增添会惹起 IS 曲线( B)A、向右挪动投资需求曲线的挪动量B、向右挪动投资需求曲线的挪动量乘以乘数C、向左挪动投资需求曲线的挪动量D、向左挪动投资需求曲线的挪动量乘以乘数5、IS 曲线上的每一点表示(A)A、产品市场投资等于积蓄时收入与利率的组合B、使投资等于积蓄时的均衡钱币额C、钱币市场钱币需求等于钱币供应时的均衡钱币额D、产品市场与钱币市场都均衡时的收入与利率组合6、以下惹起 IS 曲线左移的因素是( C)A、投资需求增添 B 、政府购置减少 C 、政府税收增添 D 、政府税收减少7、LM曲线的斜率取决于( D)A、边沿花费偏向B、投资需求对利率改动的反响程度C、钱币需求对收入改动的反响程度D、钱币需求对利率改动的反响程度8、当民众预期( B)时,会拥有更多的钱币。

A 、债券价钱上升B 、债券利率降落C 、债券利率降落D 、估算盈利增添9、钱币的谋利型需求主要取决于( A)A 、利率高低B 、将来收入的水平C 、预防动机D 、利率降落10、在其余条件不变的状况下,钱币供应增添会惹起(A)A 、收入增添B 、收入降落C 、利率上升D 、利率降落三、简答题1、为何说资本边沿效率曲线不可以正确代表公司的投资需求曲线资本边沿效率曲线基本上反应了投资需求与利率之间的反方向改动关系。

芬斯特拉版《国际宏观经济学》课后习题答案第 章

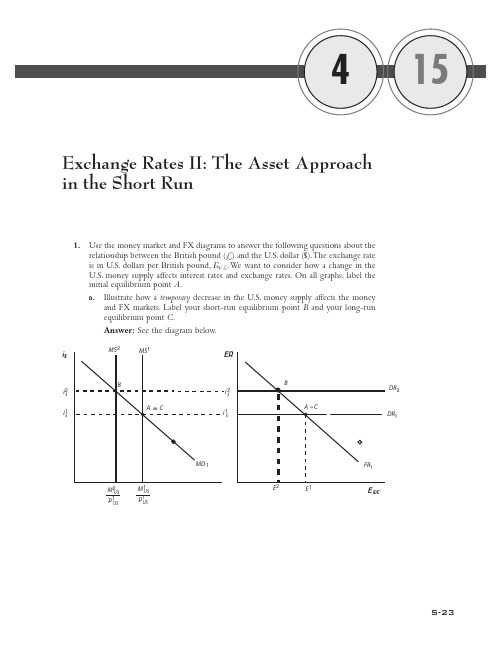

Exchange Rates II: The Asset Approach in the Short Rune the money market and FX diagrams to answer the following questions about therelationship between the British pound (£) and the U.S. dollar ($). The exchange rate is in U.S. dollars per British pound, E $/£. W e want to consider how a change in the U.S. money supply affects interest rates and exchange rates. On all graphs, label the initial equilibrium point A.a.Illustrate how a temporary decrease in the U.S. money supply affects the moneyand FX markets. Label your short-run equilibrium point B and your long-run equilibrium point C .Answer:See the diagram below.S-23i $i 1$i 2$2$DR 1DR2E 1E E $/£M 1US P 1US M 2US P 1USing your diagram from (a), state how each of the following variables changesin the short run (increase/decrease/no change): U.S. interest rate, British interestrate, E $/£, E e $/£, and the U.S. price level.Answer: The U.S. interest rate increases, the British interest rate does notchange, E $/£decreases, E e $/£does not change, and the U.S. price level does notchange.ing your diagram from (a), state how each of the following variables changesin the long run (increase/decrease/no change relative to their initial values atpoint A ): U.S. interest rate, British interest rate, E $/£, E e $/£, and U.S. price level.Answer:All of the variables return to their initial values in the long run. This isbecause the shock is temporary, implying the central bank will increase themoney supply from M 2to M 1in the long run.e the money market and FX diagrams from (a) to answer the following questions.This question considers the relationship between the Indian rupees (Rs) and the U.S.dollar ($). The exchange rate is in rupees per dollar, E Rs /$. On all graphs, label the ini-tial equilibrium point A .a.Illustrate how a permanent increase in India’s money supply affects the money andFX markets. Label your short-run equilibrium point B and your long-run equi-librium point C .Answer:See the following diagram. Thick arrows indicate temporary movementwhile thinner ones indicate the movements in the long run. In the short run,prices are fixed. Therefore the real money supply changes from MS 1to MS 2, thustemporarily lowering the domestic interest rate. In the long run, as prices rise,the real money supply and interest rate return to their original level. In the for-eign exchange market, FR shifts to the right and stays there permanently becauseof an expected depreciation of rupees.S-24Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi Rs i 1Rs i 2Rs1Rs2Rs12E 1E 2E 3M 2INP 2IN E Rs/$M 1IN P 1IN M 2IN P 1IN3.Is overshooting (in theory and in practice) consistent with purchasing power parity?Consider the reasons for the usefulness of PPP in the short run versus the long run and the assumption we’ve used in the asset approach (in the short run versus the long run). How does overshooting help to resolve the empirical behavior of exchange rates in the short run versus the long run?Answer:Y es, overshooting is consistent with PPP. Investors forecast the expected ex-change rate based on the theory of PPP.When there is some change in the market, the investors know the exchange rate will change to equate relative prices in the long run.This is why we observe overshooting in the short run—the investors incorporate this information into their short-run forecasts. Exchange rates are volatile in the short run.The theory’s implication that there is exchange rate overshooting (in response to per-manent shocks) is one explanation for short-run volatility in exchange rates.e the money market and foreign exchange (FX) diagrams to answer the followingquestions. This question considers the relationship between the euro (€) and the U.S.dollar ($). The exchange rate is in U.S. dollars per euro, E$/€. Suppose that with fi-nancial innovation in the United States, real money demand in the United States de-creases. On all graphs, label the initial equilibrium point A.a.Assume this change in U.S. real money demand is temporary. Using the FX andmoney market diagrams, illustrate how this change affects the money and FXmarkets. Label your short-run equilibrium point B and your long-run equilib-rium point C.Answer: See the following diagram. The long-run values are the same as the ini-tial values because the shock is temporary. Also because the shock is temporary,we assume that the reversal of real money demand occurs before the price leveladjusts—that is, MD returns from MD2to MD1before the price level changes. S-26Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Run i$i1$i2 $i1$i2$1E1M1US / P1US E2E$/€b.Assume this change in U.S. real money demand is permanent. Using a new dia-gram, illustrate how this change affects the money and FX markets. Label your short-run equilibrium point B and your long-run equilibrium point C.Answer:See the following diagram. In the long run, the price level will have to increase to adjust for the drop in real money demand (assuming the central bank does not change the money supply, M). That is, the nominal interest rate returns to its initial value in the long run. This requires that the price level increase to reduce real money supply. The drop in real money demand will have to be met one-for-one with a drop in real money supply (generated by an increase in the price level). In this case, the expected exchange rate changes because the shock is permanent. Therefore, FR schedule in the forex market also shifts upward.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-27i 1$i 2$1E 1E 2E 3E $/€i $i 1$i 2$M 1US / P 1US M 1US / P 2US 2c.Illustrate how each of the following variables changes over time in response to apermanent reduction in real money demand: nominal money supply M US , price level P US , real money supply M US /P US , U.S. interest rate i $, and the exchange rate E $/€.Answer:See the following diagrams.M US P US i $T T nE $/⑀M US /P US M US /P US22115.This question considers how the FX market will respond to changes in monetarypolicy. For these questions, define the exchange rate as Korean won per Japanese yen,E WON /¥. Use the FX and money market diagrams to answer the following questions.On all graphs, label the initial equilibrium point A .a.Suppose the Bank of Korea permanently decreases its money supply. Illustrate theshort-run (label the equilibrium point B ) and long-run effects (label the equilib-rium point C ) of this policy.Answer:See the following diagram. In the short run, prices are fixed. Thereforethe real money supply changes from MS 1to MS 2, thus temporarily raising the Ko-rean interest rate. In the long run, as prices fall, the real money supply and interestrate return to their original levels. In the foreign exchange market, FR shifts to theleft and stays there permanently because of an expected appreciation of won.S-28Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi won i 1won i 2won1won2wonM 1K / P 1K M 2K / P 2K M 2K / P 1K 1E 1E 3E 2E won/¥2b.Now , suppose the Bank of Korea announces it plans to permanently decrease itsmoney supply but doesn’t actually implement this policy . How will this affect theFX market in the short run if investors believe the Bank of Korea’s announcement?Answer:See the following diagram. I n this case, interest rates on won-denominated deposits don’t change because the Bank of Korea doesn’t cut themoney supply. However, because investors expected the Bank of Korea to cut themoney supply, they expect the won will appreciate relative to the yen, causing adecrease in the return on yen-denominated deposits in the short run. Notice theresulting change in the exchange rate is relatively small (compared with the dra-matic decrease we see in [a]).i won i 1won M 1K / P 1K DR 1E 1E 2E won/¥c.Finally, suppose the Bank of Korea permanently decreases its money supply butthis change is not anticipated. When the Bank of Korea implements this policy,how will this affect the FX market in the short run?Answer:In this case, the expected exchange rate is unchanged because the in-vestors didn’t expect the decrease in the money supply.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-29i won i 1won i 2won 2won1wonM 1K / P 1K M 2K / P 1K DR 1DR E 1E 2E won/¥ing your previous answers, evaluate the following statements:i.If a country wants to increase the value of its currency, it can do so (tem-porarily) without raising domestic interest rates.ii.The central bank can reduce both the domestic price level and the value ofits currency in the long run.iii.The most effective way to increase the value of a currency is through sur-prising investors.Answer: Though it is theoretically possible, as shown in (b), it is not a good pol-icy because it is bad for the policy makers reputation in the long run.i.True; shown in (b).ii.False; shown in (a) A reduction in price level implies an exchange rate ap-preciation by PPP .iii.False; shown in (b) and (c) compared with (a). The most dramatic appreci-ation in the won occurs when the reduction in M is coupled with investorsanticipating the appreciation in the won. In general, a policy must be cred-ible for it to have an effect in the long run.6.In the late 1990s, several East Asian countries used limited flexibility or currency pegsin managing their exchange rates relative to the U.S. dollar. This question considers how different countries responded to the East Asian Currency Crisis (1997–1998).For the following questions, treat the East Asian country as the home country and the United States as the foreign country. Also, for the diagrams, you may assume these countries maintained a currency peg (fixed rate) relative to the U.S. dollar. Also, for the following questions, you need consider only the short-run effects.a.In July 1997, investors expected that the Thai baht would depreciate. That is, theyexpected that Thailand’s central bank would be unable to maintain the currency peg with the U.S. dollar. Illustrate how this change in investors’ expectations af-fects the Thai money market and the FX market, with the exchange rate defined as baht (B) per U.S. dollar, denoted E B/$. Assume the Thai central bank wants to maintain capital mobility and preserve the level of its interest rate and abandons the currency peg in favor of a floating exchange rate regime.Answer:If Thailand is willing to let its currency float against the dollar, thenThailand’s central bank can maintain monetary policy autonomy and interna-tional capital mobility. See the following diagram:S-30Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi baht i 1bahtM 1T / P 1T ERDR 12E 1E 2E baht/$b.I ndonesia faced the same constraints as Thailand—investors feared I ndonesiawould be forced to abandon its currency peg. Illustrate how this change in in-vestors’ expectations affects the Indonesian money market and the FX market,with the exchange rate defined as rupiahs (Rp) per U.S. dollar, denoted E Rp /$. As-sume the Indonesian central bank wants to maintain capital mobility and the cur-rency peg.Answer: If Indonesia wants to maintain the currency peg against the dollar andmaintain international capital mobility, it will have to give up monetary policyautonomy. In this case, Indonesia has to increase the domestic interest rate to keepinvestors from dumping their rupiah-denominated deposits for U.S. dollars andmove their investments out of Indonesia (this would then cause a depreciation inthe rupiah).i rup i 1rup i 2rup 1rup 2rupM 1I / P 1I M 2I / P 1I 12FR E 1E rupiah/$2c.Malaysia had a similar experience, except that it used capital controls to maintainits currency peg and preserve the level of its interest rate. Illustrate how this change in investors’ expectations affects the Malaysian money market and the FX market,with the exchange rate defined as ringgit (RM) per U.S. dollar, denoted E RM/$. Y ou need show only the short-run effects of this change in investors’ expectations.Answer:See the following diagram. In the absence of capital controls Malaysian interest rate would have to rise. However, by preventing investors from taking ad-vantage of arbitrage, Malaysia creates a disequilibrium. The investors require i 2RM to keep their deposits in Malaysia, but they only receive i 1RM . Because of the cap-ital controls imposed by Malaysia, investors cannot withdraw their ringgit-denominated deposits (selling ringgit in exchange for dollars in the FX market).n effect, the foreign market equilibrium diagram shown below does notwork/exist. This allows Malaysia to maintain monetary policy autonomy and a fixed exchange rate at the same time.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-31i RM i 1RM i 2RM 1RM 2RM M 1M / P 1M 12E 1E RM/$pare and contrast the three approaches just outlined. As a policy maker,which would you favor? Explain.Answer: There is no “correct” answer to this question. The cases above highlight the trilemma because each country can choose a different option depending on their domestic or international priorities. They need to compare the benefits of having any two of (a) fixed exchange rates, (b) monetary autonomy, and (c) in-ternational capital mobility against the cost of not having the third one.7.Several countries have opted to join currency unions. Examples include the Euroarea, the CFA franc union in W est Africa, and the Caribbean currency union. This in-volves sacrificing the domestic currency in favor of using a single currency unit in multiple countries. Assuming that once a country joins a currency union it will not leave, do these countries face the policy trilemma discussed in the text? Explain.Answer: These countries do face the trilemma because they are committed to main-taining the first policy goal of a fixed exchange rate. Joining a currency union effec-tively means a country has a fixed exchange rate without the need for government intervention because the money supply is controlled by a regional central bank for member countries. This effectively reduces the choice to a dilemma between mone-tary policy autonomy versus international capital mobility. T ypically, countries that are parts of a currency union sacrifice monetary policy autonomy; policy decisions are made jointly rather than independently.S-32Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Run8.During the Great Depression, the United States remained on the international goldstandard longer than other countries. This effectively meant that the United States wascommitted to maintaining a fixed exchange rate at the onset of the Great Depression.The U.S. dollar was pegged to the value of gold along with other major currencies,including the British pound, the French franc, and so on. Many researchers haveblamed the severity of the Great Depression on the Federal Reserve and its failure toreact to economic conditions in 1929 and 1930. Discuss how the policy trilemma ap-plies to this situation.Answer: The United States was committed to the fixed exchange rate with gold;consequently, policy makers had to sacrifice either monetary policy autonomy or cap-ital mobility, just as the trilemma suggests. Based on the information given in thequestion, we can assume that the policy did not respond to the U.S. business cycle(policy makers did not exercise monetary policy autonomy). Thus, if we assume in-ternational capital mobility, the United States could not react to the business cyclewith a monetary expansion until it abandoned the gold standard.9.On June 20, 2007, John Authers, investment editor of the Financial Times,wrote thefollowing in his column “The Short View”:The Bank of England published minutes showing that only the narrowest pos-sible margin, 5–4, voted down [an interest] rate hike last month. Nobody fore-saw this. . . . The news took sterling back above $1.99, and to a 15-year highagainst the yen.Can you explain the logic of this statement? Interest rates in the United Kingdomhad remained unchanged in the weeks since the vote and were still unchanged afterthe minutes were released. What news was contained in the minutes that causedtraders to react? Use the asset approach.Answer: The news item indicates that investors did not expect the decision to leaveinterest rates unchanged would be divisive. They thought that any increases in inter-est rates would happen further in the future. Higher interest rates would lead to anappreciation in the pound sterling. When the minutes showed that interest rate in-creases were more likely than previously thought, investors came to expect an appre-ciation sooner rather than later. This caused an appreciation in the current spot ex-change rate.10.W e can use the asset approach to both make predictions about how the market willreact to current events and understand how important these events are to investors.Consider the behavior of the Union/Confederate exchange rate during the CivilW ar. How would each of the following events affect the exchange rate, defined as?Confederate dollars per Union dollar, EC$/$a.The Confederacy increases the money supply by 2,900% between July and De-cember of 1861.Answer: The Confederate money supply increases, the exchange rate increases,and the Confederate dollar depreciates.b.The Union Army suffers a defeat in Battle of Chickamauga in September 1863.Answer: Appreciation in the Confederate dollar is expected because a militaryvictory means a stable economy and monetary policy, implying decreased uncer-tainty and risk, the exchange rate decreases, and the Confederate dollar appreci-ates.c.The Confederate Army suffers a major defeat with Sherman’s March in the au-tumn of 1864.Answer: Just the opposite of (b) above: depreciation in the Confederate dollar isexpected because of military defeat increases economic and monetary uncertaintyand risk; the exchange rate increases, and the Confederate dollar depreciates.。

【VIP专享】宏观经济学思考题及参考答案

宏观经济学思考题及参考答案(1)第四章基本概念:潜在GDP,总供给,总需求,AS曲线,AD曲线。

思考题1、宏观经济学的主要目标是什么?写出每个主要目标的简短定义。

请详细解释为什么每一个目标都十分重要。

答:宏观经济学目标主要有四个:充分就业、物价稳定、经济增长和国际收支平衡。

(1)充分就业的本义是指所有资源得到充分利用,目前主要用人力资源作为充分就业的标准;充分就业本不是指百分之百的就业,一般地说充分就业允许的失业范畴为4%。

只有经济实现了充分就业,一国经济才能生产出潜在的GDP,从而使一国拥有更多的收入用于提高一国的福利水平。

(2)物价稳定,即把通胀率维持在低而稳定的水平上。

物价稳定是指一般物价水平(即总物价水平)的稳定;物价稳定并不是指通货膨胀率为零的状态,而是维持一种能为社会所接受的低而稳定的通货膨胀率的经济状态,一般指通货膨胀率为百分之十以下。

物价稳定可以防止经济的剧烈波动,防止各种扭曲对经济造成负面影响。

(3)经济增长是指保持合意的经济增长率。

经济增长是指单纯的生产增长,经济增长率并不是越高越好,经济增长的同时必须带来经济发展;经济增长率一般是用实际国民生产总值的年平均增长率来衡量的。

只有经济不断的增长,才能满足人类无限的欲望。

(4)国际收支平衡是指国际收支既无赤字又无盈余的状态。

国际收支平衡是一国对外经济目标,必须注意和国内目标的配合使用;正确处理国内目标与国际目标的矛盾。

在开放经济下,一国与他国来往日益密切,保持国际收支的基本平衡,才能使一国避免受到他国经济波动带来的负面影响。

3,题略答:a.石油价格大幅度上涨,作为一种不利的供给冲击,将会使增加企业的生产成本,从而使总供给减少,总供给曲线AS将向左上方移动。

b.一项削减国防开支的裁军协议,而与此同时,政府没有采取减税或者增加政府支出的政策,则将减少一国的总需求水平,从而使总需求曲线AD向左下方移动。

c.潜在产出水平的增加,将有效提高一国所能生产出的商品和劳务水平,从而使总供给曲线AS向右下方移动。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Exchange Rates II: The Asset Approach in the Short Rune the money market and FX diagrams to answer the following questions about therelationship between the British pound (£) and the U.S. dollar ($). The exchange rate is in U.S. dollars per British pound, E $/£. W e want to consider how a change in the U.S. money supply affects interest rates and exchange rates. On all graphs, label the initial equilibrium point A.a.Illustrate how a temporary decrease in the U.S. money supply affects the moneyand FX markets. Label your short-run equilibrium point B and your long-run equilibrium point C .Answer:See the diagram below.S-23i $i 1$i 2$2$DR 1DR2E 1E E $/£M 1US P 1US M 2US P 1USing your diagram from (a), state how each of the following variables changesin the short run (increase/decrease/no change): U.S. interest rate, British interestrate, E $/£, E e $/£, and the U.S. price level.Answer: The U.S. interest rate increases, the British interest rate does notchange, E $/£decreases, E e $/£does not change, and the U.S. price level does notchange.ing your diagram from (a), state how each of the following variables changesin the long run (increase/decrease/no change relative to their initial values atpoint A ): U.S. interest rate, British interest rate, E $/£, E e $/£, and U.S. price level.Answer:All of the variables return to their initial values in the long run. This isbecause the shock is temporary, implying the central bank will increase themoney supply from M 2to M 1in the long run.e the money market and FX diagrams from (a) to answer the following questions.This question considers the relationship between the Indian rupees (Rs) and the U.S.dollar ($). The exchange rate is in rupees per dollar, E Rs /$. On all graphs, label the ini-tial equilibrium point A .a.Illustrate how a permanent increase in India’s money supply affects the money andFX markets. Label your short-run equilibrium point B and your long-run equi-librium point C .Answer:See the following diagram. Thick arrows indicate temporary movementwhile thinner ones indicate the movements in the long run. In the short run,prices are fixed. Therefore the real money supply changes from MS 1to MS 2, thustemporarily lowering the domestic interest rate. In the long run, as prices rise,the real money supply and interest rate return to their original level. In the for-eign exchange market, FR shifts to the right and stays there permanently becauseof an expected depreciation of rupees.S-24Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi Rs i 1Rs i 2Rs1Rs2Rs12E 1E 2E 3M 2INP 2IN E Rs/$M 1IN P 1IN M 2IN P 1INb. By plotting them on a chart with time on the horizontal axis, illustrate how eachof the following variables changes over time (for India): nominal money supply M IN , price level P IN , real money supply M IN /P IN , India’s interest rate i Rs , and the exchange rate E Rs /$.Answer:See the following diagrams.ing your previous analysis, state how each of the following variables changesin the short run (increase/decrease/no change): India’s interest rate i Rs , E Rs/$E e Rs/$,and India’s price level P IN .Answer: India’s interest rate decreases, the U.S. interest rate remains unchanged,E Rs /$increases, E e Rs /$increases, and India’s price level remains unchanged.ing your previous analysis, state how each of the following variables changesin the long run (increase/decrease/no change relative to their initial values atpoint A ): India’s interest rate i Rs , E Rs/$E e Rs/$, India’s price level P IN .Answer: India’s interest rate remains unchanged, the U.S. interest rate remainsunchanged, E Rs /$increases, E e Rs /$increases (remains unchanged in transition fromshort to long run), India’s price level increases.e.Explain how overshooting applies to this situation.Answer:The short-run exchange rate overshoots its long-run value, E E as in the text Figure 4-13 (15-13). W e can see this in the impulse response diagrams shown previously. The overshooting is caused by the investors’ adjustment of exchange rate expectations coupled with lower domestic interest rates. Since the rupees in-terest rate falls, investors must be compensated by a rupee appreciation for UIP with U.S. interest rate to hold. For a rupee appreciation to be possible, it must depreciate more in the short run than its longer-run value.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Run S-25M IN P IN i RsT T nE Rs/$M IN /P IN M IN /P IN11223.Is overshooting (in theory and in practice) consistent with purchasing power parity?Consider the reasons for the usefulness of PPP in the short run versus the long run and the assumption we’ve used in the asset approach (in the short run versus the long run). How does overshooting help to resolve the empirical behavior of exchange rates in the short run versus the long run?Answer:Y es, overshooting is consistent with PPP. Investors forecast the expected ex-change rate based on the theory of PPP.When there is some change in the market, the investors know the exchange rate will change to equate relative prices in the long run.This is why we observe overshooting in the short run—the investors incorporate this information into their short-run forecasts. Exchange rates are volatile in the short run.The theory’s implication that there is exchange rate overshooting (in response to per-manent shocks) is one explanation for short-run volatility in exchange rates.e the money market and foreign exchange (FX) diagrams to answer the followingquestions. This question considers the relationship between the euro (€) and the U.S.dollar ($). The exchange rate is in U.S. dollars per euro, E$/€. Suppose that with fi-nancial innovation in the United States, real money demand in the United States de-creases. On all graphs, label the initial equilibrium point A.a.Assume this change in U.S. real money demand is temporary. Using the FX andmoney market diagrams, illustrate how this change affects the money and FXmarkets. Label your short-run equilibrium point B and your long-run equilib-rium point C.Answer: See the following diagram. The long-run values are the same as the ini-tial values because the shock is temporary. Also because the shock is temporary,we assume that the reversal of real money demand occurs before the price leveladjusts—that is, MD returns from MD2to MD1before the price level changes. S-26Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Run i$i1$i2 $i1$i2$1E1M1US / P1US E2E$/€b.Assume this change in U.S. real money demand is permanent. Using a new dia-gram, illustrate how this change affects the money and FX markets. Label your short-run equilibrium point B and your long-run equilibrium point C.Answer:See the following diagram. In the long run, the price level will have to increase to adjust for the drop in real money demand (assuming the central bank does not change the money supply, M). That is, the nominal interest rate returns to its initial value in the long run. This requires that the price level increase to reduce real money supply. The drop in real money demand will have to be met one-for-one with a drop in real money supply (generated by an increase in the price level). In this case, the expected exchange rate changes because the shock is permanent. Therefore, FR schedule in the forex market also shifts upward.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-27i 1$i 2$1E 1E 2E 3E $/€i $i 1$i 2$M 1US / P 1US M 1US / P 2US 2c.Illustrate how each of the following variables changes over time in response to apermanent reduction in real money demand: nominal money supply M US , price level P US , real money supply M US /P US , U.S. interest rate i $, and the exchange rate E $/€.Answer:See the following diagrams.M US P US i $T T nE $/⑀M US /P US M US /P US22115.This question considers how the FX market will respond to changes in monetarypolicy. For these questions, define the exchange rate as Korean won per Japanese yen,E WON /¥. Use the FX and money market diagrams to answer the following questions.On all graphs, label the initial equilibrium point A .a.Suppose the Bank of Korea permanently decreases its money supply. Illustrate theshort-run (label the equilibrium point B ) and long-run effects (label the equilib-rium point C ) of this policy.Answer:See the following diagram. In the short run, prices are fixed. Thereforethe real money supply changes from MS 1to MS 2, thus temporarily raising the Ko-rean interest rate. In the long run, as prices fall, the real money supply and interestrate return to their original levels. In the foreign exchange market, FR shifts to theleft and stays there permanently because of an expected appreciation of won.S-28Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi won i 1won i 2won1won2wonM 1K / P 1K M 2K / P 2K M 2K / P 1K 1E 1E 3E 2E won/¥2b.Now , suppose the Bank of Korea announces it plans to permanently decrease itsmoney supply but doesn’t actually implement this policy . How will this affect theFX market in the short run if investors believe the Bank of Korea’s announcement?Answer:See the following diagram. I n this case, interest rates on won-denominated deposits don’t change because the Bank of Korea doesn’t cut themoney supply. However, because investors expected the Bank of Korea to cut themoney supply, they expect the won will appreciate relative to the yen, causing adecrease in the return on yen-denominated deposits in the short run. Notice theresulting change in the exchange rate is relatively small (compared with the dra-matic decrease we see in [a]).i won i 1won M 1K / P 1K DR 1E 1E 2E won/¥c.Finally, suppose the Bank of Korea permanently decreases its money supply butthis change is not anticipated. When the Bank of Korea implements this policy,how will this affect the FX market in the short run?Answer:In this case, the expected exchange rate is unchanged because the in-vestors didn’t expect the decrease in the money supply.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-29i won i 1won i 2won 2won1wonM 1K / P 1K M 2K / P 1K DR 1DR E 1E 2E won/¥ing your previous answers, evaluate the following statements:i.If a country wants to increase the value of its currency, it can do so (tem-porarily) without raising domestic interest rates.ii.The central bank can reduce both the domestic price level and the value ofits currency in the long run.iii.The most effective way to increase the value of a currency is through sur-prising investors.Answer: Though it is theoretically possible, as shown in (b), it is not a good pol-icy because it is bad for the policy makers reputation in the long run.i.True; shown in (b).ii.False; shown in (a) A reduction in price level implies an exchange rate ap-preciation by PPP .iii.False; shown in (b) and (c) compared with (a). The most dramatic appreci-ation in the won occurs when the reduction in M is coupled with investorsanticipating the appreciation in the won. In general, a policy must be cred-ible for it to have an effect in the long run.6.In the late 1990s, several East Asian countries used limited flexibility or currency pegsin managing their exchange rates relative to the U.S. dollar. This question considers how different countries responded to the East Asian Currency Crisis (1997–1998).For the following questions, treat the East Asian country as the home country and the United States as the foreign country. Also, for the diagrams, you may assume these countries maintained a currency peg (fixed rate) relative to the U.S. dollar. Also, for the following questions, you need consider only the short-run effects.a.In July 1997, investors expected that the Thai baht would depreciate. That is, theyexpected that Thailand’s central bank would be unable to maintain the currency peg with the U.S. dollar. Illustrate how this change in investors’ expectations af-fects the Thai money market and the FX market, with the exchange rate defined as baht (B) per U.S. dollar, denoted E B/$. Assume the Thai central bank wants to maintain capital mobility and preserve the level of its interest rate and abandons the currency peg in favor of a floating exchange rate regime.Answer:If Thailand is willing to let its currency float against the dollar, thenThailand’s central bank can maintain monetary policy autonomy and interna-tional capital mobility. See the following diagram:S-30Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Runi baht i 1bahtM 1T / P 1T ERDR 12E 1E 2E baht/$b.I ndonesia faced the same constraints as Thailand—investors feared I ndonesiawould be forced to abandon its currency peg. Illustrate how this change in in-vestors’ expectations affects the Indonesian money market and the FX market,with the exchange rate defined as rupiahs (Rp) per U.S. dollar, denoted E Rp /$. As-sume the Indonesian central bank wants to maintain capital mobility and the cur-rency peg.Answer: If Indonesia wants to maintain the currency peg against the dollar andmaintain international capital mobility, it will have to give up monetary policyautonomy. In this case, Indonesia has to increase the domestic interest rate to keepinvestors from dumping their rupiah-denominated deposits for U.S. dollars andmove their investments out of Indonesia (this would then cause a depreciation inthe rupiah).i rup i 1rup i 2rup 1rup 2rupM 1I / P 1I M 2I / P 1I 12FR E 1E rupiah/$2c.Malaysia had a similar experience, except that it used capital controls to maintainits currency peg and preserve the level of its interest rate. Illustrate how this change in investors’ expectations affects the Malaysian money market and the FX market,with the exchange rate defined as ringgit (RM) per U.S. dollar, denoted E RM/$. Y ou need show only the short-run effects of this change in investors’ expectations.Answer:See the following diagram. In the absence of capital controls Malaysian interest rate would have to rise. However, by preventing investors from taking ad-vantage of arbitrage, Malaysia creates a disequilibrium. The investors require i 2RM to keep their deposits in Malaysia, but they only receive i 1RM . Because of the cap-ital controls imposed by Malaysia, investors cannot withdraw their ringgit-denominated deposits (selling ringgit in exchange for dollars in the FX market).n effect, the foreign market equilibrium diagram shown below does notwork/exist. This allows Malaysia to maintain monetary policy autonomy and a fixed exchange rate at the same time.Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short RunS-31i RM i 1RM i 2RM 1RM 2RM M 1M / P 1M 12E 1E RM/$pare and contrast the three approaches just outlined. As a policy maker,which would you favor? Explain.Answer: There is no “correct” answer to this question. The cases above highlight the trilemma because each country can choose a different option depending on their domestic or international priorities. They need to compare the benefits of having any two of (a) fixed exchange rates, (b) monetary autonomy, and (c) in-ternational capital mobility against the cost of not having the third one.7.Several countries have opted to join currency unions. Examples include the Euroarea, the CFA franc union in W est Africa, and the Caribbean currency union. This in-volves sacrificing the domestic currency in favor of using a single currency unit in multiple countries. Assuming that once a country joins a currency union it will not leave, do these countries face the policy trilemma discussed in the text? Explain.Answer: These countries do face the trilemma because they are committed to main-taining the first policy goal of a fixed exchange rate. Joining a currency union effec-tively means a country has a fixed exchange rate without the need for government intervention because the money supply is controlled by a regional central bank for member countries. This effectively reduces the choice to a dilemma between mone-tary policy autonomy versus international capital mobility. T ypically, countries that are parts of a currency union sacrifice monetary policy autonomy; policy decisions are made jointly rather than independently.S-32Solutions ■Chapter 4(15) Exchange Rates II: The Asset Approach in the Short Run8.During the Great Depression, the United States remained on the international goldstandard longer than other countries. This effectively meant that the United States wascommitted to maintaining a fixed exchange rate at the onset of the Great Depression.The U.S. dollar was pegged to the value of gold along with other major currencies,including the British pound, the French franc, and so on. Many researchers haveblamed the severity of the Great Depression on the Federal Reserve and its failure toreact to economic conditions in 1929 and 1930. Discuss how the policy trilemma ap-plies to this situation.Answer: The United States was committed to the fixed exchange rate with gold;consequently, policy makers had to sacrifice either monetary policy autonomy or cap-ital mobility, just as the trilemma suggests. Based on the information given in thequestion, we can assume that the policy did not respond to the U.S. business cycle(policy makers did not exercise monetary policy autonomy). Thus, if we assume in-ternational capital mobility, the United States could not react to the business cyclewith a monetary expansion until it abandoned the gold standard.9.On June 20, 2007, John Authers, investment editor of the Financial Times,wrote thefollowing in his column “The Short View”:The Bank of England published minutes showing that only the narrowest pos-sible margin, 5–4, voted down [an interest] rate hike last month. Nobody fore-saw this. . . . The news took sterling back above $1.99, and to a 15-year highagainst the yen.Can you explain the logic of this statement? Interest rates in the United Kingdomhad remained unchanged in the weeks since the vote and were still unchanged afterthe minutes were released. What news was contained in the minutes that causedtraders to react? Use the asset approach.Answer: The news item indicates that investors did not expect the decision to leaveinterest rates unchanged would be divisive. They thought that any increases in inter-est rates would happen further in the future. Higher interest rates would lead to anappreciation in the pound sterling. When the minutes showed that interest rate in-creases were more likely than previously thought, investors came to expect an appre-ciation sooner rather than later. This caused an appreciation in the current spot ex-change rate.10.W e can use the asset approach to both make predictions about how the market willreact to current events and understand how important these events are to investors.Consider the behavior of the Union/Confederate exchange rate during the CivilW ar. How would each of the following events affect the exchange rate, defined as?Confederate dollars per Union dollar, EC$/$a.The Confederacy increases the money supply by 2,900% between July and De-cember of 1861.Answer: The Confederate money supply increases, the exchange rate increases,and the Confederate dollar depreciates.b.The Union Army suffers a defeat in Battle of Chickamauga in September 1863.Answer: Appreciation in the Confederate dollar is expected because a militaryvictory means a stable economy and monetary policy, implying decreased uncer-tainty and risk, the exchange rate decreases, and the Confederate dollar appreci-ates.c.The Confederate Army suffers a major defeat with Sherman’s March in the au-tumn of 1864.Answer: Just the opposite of (b) above: depreciation in the Confederate dollar isexpected because of military defeat increases economic and monetary uncertaintyand risk; the exchange rate increases, and the Confederate dollar depreciates.。