ACCA教材

ACCA(BPP、KPLAN、FTC)教材及习题册优点

参加ACCA考试需要用的教材主要包含ACCA课本及ACCA练习册。

ACCA推荐的课本及练习册有:BPP,Kaplan 及Becker。

各个ACCA教材供应商教材特点:

1.BPP以详细见称,BPP教材是全球ACCA使用最多的版本,通俗易懂,比较适合新老学员自学,ACCA学员以看BPP课本及精简版讲义为主。

同时但国内基本上所有的高校ACCA专业也是使用的BPP版教材,因为审计署买下了BPP教材在中国的版权,并且比之FTC版教材价格也有优势,每个点都讲解得很细。

2.FTC版是ACCA官方版本教材,在全球使用也比较多。

这套教材的优点是简洁,基本上每门课教材都比BPP版薄,但是FTC对F4阶段的ACCA备考并不是那么适用,其难度较之BPP版有所加大,所用单词也要复杂一些。

3.Kaplan Publishing(开普兰,又称:卡普兰)Kaplan以精简为主,主次分明,概括性较强。

每个版本的教材内容完全不同,但都是根据ACCA官方的大纲(syllabus)编写,都覆盖了所有内容,可以使用任一版本教材准备考试。

可以根据自己的学习习惯选择适合自己的教材。

第 1 页。

acca教材-ACCA F1 知识课程

ACCAspace 中国ACCA特许公认会计师教育平台

Copyright ©

12

The impact of technology on organisations

Homeworking and supervision

IT技术还使得部分工作得以在家里迚行,员工不用去上班。但这也带来了监管上的一 些问题。 -------------------------------------------------------------------------------------------------------------Outsourcing(外包)把一些非核心业务交给别人来做。

where the employee was employed.(公司全部关闭戒部分关闭导致的人员 冗余。) 2. The requirements of the business for employees to carry out work of a particular kind have ceased or diminished or are expected to.(流程改迚, 技术迚步导致的人员冗余。)

由内到外: 组织本身 经营环境(产业层面上的环境) 宏观环境(经济政治文化技术层 面的环境) 物理环境(整个以物质形态存在 的环境 )

ACCAspace 中国ACCA特许公认会计师教育平台

Copyright ©

3

The political and legal environment

9

Social and demographic trends

• Population and the labour market(人口数量,人口结构的变化,对劳劢力市场有 深刻长进的影响)

会计考证买什么书看

会计考证买什么书看关于会计考证买什么书看会计考证是让个人在会计领域取得有权威认证的证书,是提升个人职业发展的重要方式。

在备考过程中,书籍的选择及阅读方法都至关重要。

本文将从专业会计师的角度分析会计考证买什么书看。

选择适合自己的教材在备考过程中选择合适的教材十分重要。

在选择教材时,需要根据自己的基础及考试的要求选取。

如CMA考试可以选择IMA出版的Wiley教材,ACCA考试可以选择BPP或Kaplan等出版的教材。

此外,在选择教材时,还可以参考教材的特点。

如速读的教材适合对知识基础掌握较好的考生,而深入讲解的教材适合对知识掌握度较低的考生。

阅读方法需要多维度虽然选择了合适的教材,但阅读方法仍然需要好好考虑。

在阅读时需要从多维度进行思考,不可漫不经心地阅读。

首先,可以从题目着手,明确自己需要掌握哪些知识点。

其次,在阅读中应当注重理解,一定要弄懂每一章节,这对于后期复习和应试都十分有帮助。

最后,在阅读中可进行笔记,做好重点知识点的记录。

如何阅读财经报纸在备考过程中,阅读财经报纸可以帮助考生做到及时掌握最新的财经动态,加深对于财经知识的理解及掌握。

在阅读财经报纸时,需要注意以下几点。

首先,针对自己考试的要求,选择合适的报纸。

其次,在阅读时需要注重对于节日、季节等时事的了解,这样可以更好地掌握最新的财经动态。

最后,在阅读后应当进行总结,将阅读获得的知识点进行记录及整理。

案例:1、小明本身学习能力很强,觉得自己的基础较好,选择深入讲解的教材,并注重理解,收效显著。

2、小张基础较差,选择了速读的教材,但在阅读时没有重视理解,导致效果欠佳。

3、小李在阅读财经报纸时,没有根据自己考试的要求选择合适的报纸,导致掌握的财经知识与考试没有直接关联。

4、小赵在阅读财经报纸时,只关注了新闻,忽略了对于各类涉财企业的了解,这使得其掌握的信息不够全面。

5、小伍在阅读教材时,虽然进行了笔记,但笔记内容不够清晰详细,在后期复习时反而使其困惑不解。

一文看懂ACCA各科目内容、特点、题型、分值、通过率、难度、彼此关系·····

ACCA考试共有15个考试科目,其中AB(F1)、MA(F2)、FA(F3)、LW(F4)、PM(F5)、TX(F6)、FR(F7)、AA(F8)、FM(F9)为F阶段课程,共9个科目,SBL、SBR、AFM(P4)、APM(P5)、ATX(P6)、AAA(P7)为P阶段课程,共6个科目。

ACCA课程中,F阶段科目全部为必修课,P阶段科目中SBL、SBR为必修课,其他为选修课(4选2参加考试),ACCA考试一共考过13科即可变成ACCA准会员。

考试之前一定要对ACCA有全面的了解,知己知彼方能百战不殆。

AB (F1)1英文名:Accountant in Business2中文名:会计师与企业3课程内容:主要是帮助无任何商业背景知识的学员初步建立人力资源、企业组织、商业环境及相互之间影响关系的相关知识内容。

内容涵盖:企业组织,公司管理,会计和报告体系,内部财务控制,人力资源管理,会计职业道徳。

4科目联系:AB(F1)是SBL课程中《公司治理,风险管理与职业道德》和《商务分析》的基础。

5考试时间:2小时(机考)6考试分值:A部分一一30道单选题(每题2分,共计60分)一一16道单选题(每题1分,共计16分)B部分一一情景为基础的6道多任务题(由单选、多选、判断题构成,每题4分,共计24分)7课程难度:☆☆8时间花费:☆☆☆2019年全球平均通过率:82.50%MA (F2)1英文名:Management Accounting2中文名:管理会计3课程内容:主要向学员介绍了管理会计体系的主要元素以及管理会计如何发挥支持企业决策, 制定企业决策的作用。

内容涵盖:管理会计,管理信息,成本会计,预算和标准成本,业绩衡量,短期决策方法。

4科目联系:MA(F2)《管理会计》是PM(F5)《业绩管理》和APM(P5)《高级业绩管理》的基础。

5考试时间:2小时(机考)6考试分值:A部分一一35道单选题(每题2分,共计70分)B部分一一3道多任务题(由计算、简单、论述题构成,每题10分,共计30分)7课程难度:☆☆8时间花费:☆☆☆2019年全球平均通过率:65.00%FA (F3)1英文名:Financial Accounting2中文名:财务会计3课程内容:主要向学员介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

acca课件

公司法基本原则及案例分析

公司法的基本原则

公司法规定了公司的设立、组织、行为和终止等方面的内容。它强调了公司的法 定性、独立性和责任性。公司必须依法设立,具有独立的法人地位,并能够独立 承担责任。

案例分析

以阿里巴巴集团为例,探讨公司法的实际应用。阿里巴巴集团作为一家大型互联 网公司,其股权结构、治理结构、业务模式等方面都涉及到公司法的相关规定。 通过对这个案例的分析,可以深入了解公司法在实际中的应用和作用。

财务报表分析

资产负债表分析

现金流量表分析

通过分析资产负债表,了解企业的资 产、负债和所有者权益的结构和质量 ,评估企业的偿债能力和资产质量。

通过分析现金流量表,了解企业的现 金流入和流出情况,评估企业的现金 产生和运用能力。

利润表分析

通过分析利润表,了解企业的收入、 成本和利润情况,评估企业的盈利能 力和经营效率。

ACCA课件

目 录

• 引言 • 财务报告与审计 • 税务与公司法 • 财务管理与决策分析 • 战略管理与领导力发展 • 职业道德与职业发展

01

引言

ACCA简介

特许公认会计师公会(ACCA )是全球领先的专业会计师组 织,提供全面的、高质量的会 计资格认证。

ACCA认证被广泛认可,作为 国际会计准则和国际财务报告 准则的重要推动者。

03

税务与公司法

税务概述

税务的基本概念

税务是指国家依据其税收法律和法规 ,对纳税人或纳税人的应税行为进行 征收和管理的活动。税务涵盖了税收 的各个方面,包括税种、税率、税收 优惠政策等。

税务的作用

税务在国家治理中具有重要的作用。 它为国家提供了稳定的财政收入,支 持了国家的发展和建设。同时,税务 还调节了经济,引导了社会资源的合 理配置。

acca的课程体系

acca的课程体系【实用版】目录1.ACCA 课程体系简介2.ACCA 课程体系的级别和课时3.ACCA 课程体系的核心课程和休息安排4.ACCA 课程体系的优势和特点正文一、ACCA 课程体系简介ACCA(Association of Chartered Certified Accountants,特许公认会计师公会)成立于 1904 年,是全球最具影响力的专业会计组织之一。

ACCA 课程体系是该组织为培养国际财务会计人才所设立的一套完善、系统的培训课程。

二、ACCA 课程体系的级别和课时ACCA 课程体系分为四个级别,分别是 S1、S2、S3 和 S4。

每个级别包含 48 个课时,每周一次课,每次课时为 2 小时,其中核心课程时间为 30 分钟,接着休息 10 分钟,然后再进行 30 分钟的核心课程学习。

三、ACCA 课程体系的核心课程和休息安排在 ACCA 课程体系中,核心课程是指那些涵盖了会计、财务管理、审计、税务和企业战略等关键领域的课程。

这些核心课程旨在帮助学员掌握国际财务会计领域的专业知识和技能。

课程安排中的休息时间,可以让学员在紧张的学习中得到适当的休息和调整,从而更好地吸收和消化所学知识。

四、ACCA 课程体系的优势和特点1.国际化:ACCA 课程体系遵循国际财务会计准则和实务,有助于学员提升国际视野,成为具有国际竞争力的财务会计人才。

2.系统性:ACCA 课程体系分为四个级别,由浅入深,逐步提升学员的专业知识和能力。

3.实用性:ACCA 课程体系注重实际操作能力和应用能力的培养,使学员能够更好地将所学知识应用于实际工作中。

4.专业性:ACCA 课程体系中的核心课程,都是由具有丰富实践经验和专业背景的专家编写,保证了课程内容的专业性和权威性。

5.灵活性:ACCA 课程体系允许学员根据自己的时间和进度进行学习,为学员提供了很大的学习自主性和灵活性。

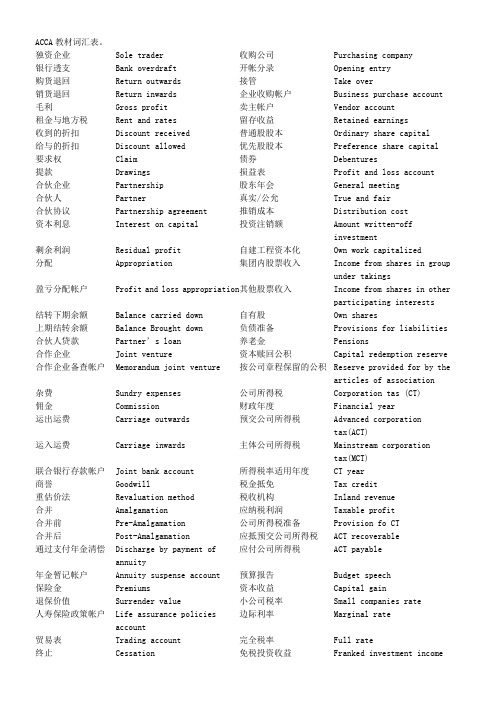

ACCA教材词汇表

ACCA教材词汇表。

独资企业Sole trader 收购公司Purchasing company银行透支Bank overdraft 开帐分录Opening entry购货退回Return outwards 接管Take over销货退回Return inwards 企业收购帐户Business purchase account 毛利Gross profit 卖主帐户Vendor account租金与地方税Rent and rates 留存收益Retained earnings收到的折扣Discount received 普通股股本Ordinary share capital给与的折扣Discount allowed 优先股股本Preference share capital要求权Claim 债券Debentures提款Drawings 损益表Profit and loss account合伙企业Partnership 股东年会General meeting合伙人Partner 真实/公允True and fair合伙协议Partnership agreement 推销成本Distribution cost资本利息Interest on capital 投资注销额Amount written-offinvestment剩余利润Residual profit 自建工程资本化Own work capitalized分配Appropriation 集团内股票收入Income from shares in groupunder takings盈亏分配帐户Profit and loss appropriation 其他股票收入Income from shares in otherparticipating interests结转下期余额Balance carried down 自有股Own shares上期结转余额Balance Brought down 负债准备Provisions for liabilities 合伙人贷款Partner’s loan养老金Pensions合作企业Joint venture 资本赎回公积Capital redemption reserve 合作企业备查帐户Memorandum joint venture 按公司章程保留的公积Reserve provided for by thearticles of association杂费Sundry expenses 公司所得税Corporation tas (CT)佣金Commission 财政年度Financial year运出运费Carriage outwards 预交公司所得税Advanced corporationtax(ACT)运入运费Carriage inwards 主体公司所得税Mainstream corporationtax(MCT)联合银行存款帐户Joint bank account 所得税率适用年度CT year商誉Goodwill 税金抵免Tax credit重估价法Revaluation method 税收机构Inland revenue合并Amalgamation 应纳税利润Taxable profit合并前Pre-Amalgamation 公司所得税准备Provision fo CT合并后Post-Amalgamation 应抵预交公司所得税ACT recoverable通过支付年金清偿Discharge by payment of应付公司所得税ACT payableannuity年金暂记帐户Annuity suspense account 预算报告Budget speech保险金Premiums 资本收益Capital gain退保价值Surrender value 小公司税率Small companies rate人寿保险政策帐户Life assurance policies边际利率Marginal rateaccount贸易表Trading account 完全税率Full rate终止Cessation 免税投资收益Franked investment income变卖资产帐户Realization account 资本减免Capital allowances合伙企业的解体Dissolution of partnership 剩余预交公司所得税Surplus ACT最后约定的资本Last agreed capital 寄售业务Consignment trading 逐步解体Piecemeal dissolution 汇票Bills of exchange变卖资产费用准备Provision for realizationexpense分支机构Branch变卖资产损失Loss on realization 代理商Agent股票帐户Shares account 交易商Trader英国境内公司UK resident company 受托人Consignee非免税收入Un-franked receipts 委托人,寄售人Consigner公司所得税费用CT charge 保障,赔偿Indemnity代扣所得税的交纳Payment under deduction of IT 销售帐单Account sales磨损Wear and tear 寄售利润Profit on consignment 拥有法定所有权的土地Freehold land 进口税Import duties过时Obsolescence 运费Delivery to customers开采或消耗Extraction of consumptionover time 途中保险费Carriage insurance on goodsdelivered to Customers直线法Straight line method 佣金Commission余额递减法Reducing balance method 汇付Remittance年数总和法Sum of the digits method 未售存货Unsold stock累计折旧Accumulated depreciations 应收票据Bills receivable 经济使用年限Useful economic lives 保险收入Insurance proceeds 每股净收益Earnings per share 面值Face value例外项目Exceptional items 贴现费用Discount charges 非常项目Extraordinary items 财务费用Financing cost前期调整Prior year adjustment 应付票据Bills payable不能抵销的预交公司税Irrevocable advancedcorporation tax支出Expenditure未抵销的损失Unrelieved losses 即期汇票Sight drafts净值基础Net basis 监管Custody零值基础Nil basis 主损益帐户Main profit and loss account 消耗品Consumable stores 部门化Departmentalization成本与可实现净值孰低The lower of cost and netrealizable value分摊Apportionment平均成本Average cost 共同性费用Common expense先进先出First in first out 包装纸Wrapping paper后进先出Last in first out 评价Assess标准成本Standard cost 独立实体Independent entity重置成本Replacement cost 投资报酬率Return on investment 资产负债表日后日期Event after balance sheet date 减除佣金后利润Post-commission profit 董事会The board of directors 赊销收入Credit sales调整事项Adjusting event 修理费用Repair charges非调整事项Non-adjusting event 一般费用General expense或有事项Contingencies 分支销售机构Selling agency branch 或有收益Contingent gain 正常存货损失Normal stock losses或有损失Contingent loss 交易帐户Trading account资本承诺Capital commitments 非常存货损失Abnormal stock losses现金流量表Cash flow statement 本地购货Local purchase信用交易Credit transaction 退货Returned goods独立分支机构Independent branch现实购买力会计Current purchasing poweraccounting (CPP)现实成本会计Current cost accounting(CCA) 往来帐户Current account零售物价指数Retail price index 复式簿记帐户Double-entry accounts持有收益Holding gains 时间差异Time lag differences业绩评估Assessment of performance 分支机构间转移Inter-branch transfer货币性项目的衡量Measurement of monetary items 结算Settlement货币性资产Monetary assets 分支机构间往来帐户Interbranch current account 货币性负债Monetary liabilities 分支机构存货调整帐户Branch stock adjustmentaccount征求意见稿Exposure draft 未实现利润准备Provision for unrealizedprofit实现原则Realization货币性营运资本调整Monetary working capitaladjustment举债比率调整Gearing adjustment 货币折算Currency translation净营业资产Net operating assets 货币兑换Currency conversion发行和赎回债券Issue and redemption当地货币Local currencydebentures债券Bonds 汇率Exchange rate契约Deed 即期汇率Spot rate无担保债券Naked-debentures(unsecured) 远期合同Forward contract拥有法定所有权的Freehold 贴水Discount偿债基金Sinking fund 升水Premium货币性项目Monetary items债券赎回偿债基金Debenture redemption sinkingfund account风险Risk偿债基金投资帐户Sinking fund investmentaccount可转换债券Convertible debentures 不确定性Uncertainty资本化发行Capitalization issue 套期保值Hedging股权发行Bonus issue 长期货币性资产Long-term monetary assets 含权价Cum-rights prices 长期货币性要求权Long-term monetary claims 除权价Ex-rights prices 汇兑收益/损失Exchange rate gain/loss可分配公积Distributable of reserves 时态法Temporal method历史汇率法Historic method以公积支付股利Paying a dividend out ofreserve已付清红利股Paid-up bonus shares 期末汇率法Closing rate method重估公积Revaluation reserve 场地费用Site expenses减资Capital reductions 管理费用Administrative expenses资本重组Capital reorganizations 装置和设备Furniture and fittings过剩资本Excess capital 房屋Premises资本重建Capital reconstruction 预付费用Payment in advance权益汇总帐户Sundry members account 建造合同Construction contract实现帐户Realization account 工程保留款Retention购买者帐户Purchaser’s account分期付款Progress payment自愿清算Voluntary liquidation 交易帐户Trading account特别决议Special resolution 合同收入Contract fee方案\计划Scheme 合同亏损Loss on contract清偿\偿还Discharge 完工百分比Percentage of completion卖方帐户Vendor account 完成合同Completed contract创立合并Amalgamation 预期利润Expected profit高估Over-valuation 承建商Contractor低估Under-valuation 矫正Rectification集团报表Group accounts 已鉴定完工价值Value of work certified纵向联合Vertical integration 总部费用Head office costs横向联合Horizontal integration 合同成本Contract costs不同行业联合Diversification 销售收入Turnover控股公司Holding company 合同损失准备Provision for loss oncontract重大影响Dominant influence 预收款Payment on account直接控制集团Direct group 可预见损失Foreseeable loss垂直控制集团Vertical group 已付款超过收入(部分) Excess progress payment混合控制集团Mixed group 股票/证券Stock ,security盈余公积Revenue reserve 债券Debenture合并公积Consolidation reserve 法定权利Legal rights少数股权Minority interests 报价Quote合并商誉Goodwill on consolidation 证券交易所Stock exchange上市投资Listed investment合并资本公积Capital reserve onconsolidation少数股东Minority share holders 偿还Repayment股本溢价Share premium 累积股息Cum div cd部分收购Partial acquisition 累积利息Cum-int ci在途支票Cheque in the post 股息除外Ex-div xd收买前后Pre( post)-acquisition 利息除外Ex-int xi调整帐户Adjustment accounts 面值Nominal value对子公司投资Investment in subsidiary 市价Market value普通公积General reserve 应计股利Accrued dividend参与股权Participating interest 应计利息Accrued interest集团内部交易Intra-group trading 证券交易所官方清单Stock exchange official list 公司间销售Inter-company sales 二级市场Secondary market溢价Premium 未上市证券市场Unlisted securities market 折价Discount 让与,出售disposal债券利息Debenture interest 加权平均Weighted分次购买Piecemeal acquisition 结帐Close off关联公司Associated company 已分派股份Allocated shares多数股权Majority holding 国库券Treasury stock累计控股Cumulative holding 认股权发行Rights issue孙公司Sub-subsidiary 赊销Credit sale子集团,附属集团Sub-group 租购Hire purchase多公司结构Multi-company structures 信用协议Credit agreement伙伴子公司Fellow subsidiaries 会计处理Accounting treatment有效股权Effective shareholdings 经营性租赁Operating lease控制股权Controlling interest 融资租赁Finance lease资本报酬率Return on capital employed 出租人/承租人Lesser /lessee产权收益率Returen on equity 一期(二期)租赁Primary(secondary)period息税前净利Net Profit before interest andtax不可撤销的付款No-cancelable payment应收帐款帐龄表Aging schedule of debtors 名义租金Peppercorn rent资金来源及运用表Source and application offunds statement报酬Reward通货膨胀Inflation 现值Present value通货紧缩Deflation 最低租赁付款额Minimum lease payment损耗Deplete 定金Deposit每股收益Earnings per share 公允价值Fair value股利保证倍数Dividend cover 财务费用Finance charge股利分配率Dividend payout ratio 实际利率Effective rate of financecharge股利收益率Dividend yield ratio 平均未付资本余额Average balance of capitaloutstanding净收益率Earnings yield 资本偿还Capital repayment市盈率Price/ earnings ratio 精确法Actuarial method公司估价The valuation of components 递延收益Deferred income联营公司Associated companies 分期支付Installment共同比财务报表Common-size financialstatements 未实现利润准备Provision for unrealizedprofit物质资源Physical resources 应收租购款帐户Hire purchase debtorsaccount会计原则Accounting principles 重新获得帐户Repossessions account 会计方法Accounting methods 金融公司Finance house权责发生制Accrual accounting 制造商Manufacturer重置成本Replacement cost 交易商Dealer一般会计原则Generally accepted accountingprinciples(GAAP)总盈余Gross earnings剩余现金Cash surplus 政府补助Government grant净值减免Writing down allowance 租赁期Lease term。

ACCAF1StudyText,PDF原版BPP教材

Accountant in Business Paper F1 Course Notes ACF1CN07 l i BPP provides revision courses question days mock days and specific material to assist you in this important phase of your studies. F1 Accountant in Business Study Programme for Standard Taught Course Page Introduction to the paper and the course...............................................................................................................iii 1 Business organisation and structure...........................................................................................................1.1 2 Information technology and systems...........................................................................................................2.1 3 Influences on organisational culture............................................................................................................3.1 4 Ethical considerations........................................................................................................................ ..........4.1 5 Corporate governance and social responsibility..........................................................................................5.1 6 Home study chapter – The macro economic environment..........................................................................6.1 End of Day 1 – refer to Course Companion for Home Study 7 The business environment..........................................................................................................................7.1 8 Home study chapter – The role of accounting.............................................................................................8.1 9 Control security and audit............................................................................................................................9.1 10 Identifying and preventing fraud................................................................................................................10.1 11 Leadership and managing people.............................................................................................................11.1 12 Individuals groups teams.........................................................................................................................12.1 End of Day 2 – refer to Course Companion for Home Study Course exam 1 13 Motivating individuals and groups.............................................................................................................13.1 14 Personal effectiveness and communication..............................................................................................14.1 15 Recruitment and selection.........................................................................................................................15.1 16 Diversity and equal opportunities..............................................................................................................16.1 17 Training and development. (1)7.1 18 Performance appraisal (1)8.1 End of Day 3 – refer to Course Companion for Home Study Course exam 2 19 Answers to Lecture Examples...................................................................................................................19.1 20 Appendix: Pilot Paper questions................................................................................................................20.1 ??Revision of syllabus ?? Testing of knowledge ?? Question practice ?? Exam technique practice INTRODUCTION ii Introduction to Paper F1 Accountant in Business Overall aim of the syllabus To introduce knowledge and understanding of the business and its environment and the influence this has on how organisations are structured on the role of the accounting and other key business functions in contributing to the efficient effective and ethical management and development of an organisation and its people and systems. The syllabus The broad syllabus headings are: A Business organisation structure governance and management B Key environmental influences and constraints on business and accounting C History and role of accounting in business D Specific functions of accounting and internal financial control E Leading and managing individuals and teams F Recruiting and developing effective employees Main capabilities On successful completion of this paper candidates should be able to: ?? Explain how the organisation is structured governed and managed ?? Identify and describe the key environmental influences and constraints ?? Describe the history purpose and position of accounting ?? Identify and explain the functions of accounting systems ?? Recognise the principles of leadership and authority ?? Recruit and develop effective employees Links with other papers This diagram shows where direct solid line arrows and indirect dashed line arrows links exist between this paper and other papers that may follow it. The Accountant in Business is the first paper that students should study as it acts as an introduction to business structure and purpose and to accountancy as a core business function. BA P3 MA F2 and FA F3PA P1 AB F1 INTRODUCTION iii Assessment methods and format of the exam Examiner: Bob Souster The examination is a two hour paper-based or computer-based examination. Questions will assess all parts of the syllabus and will test knowledge and some comprehension of application of this knowledge. The examination will consist of 40 two mark and 10 one mark multiple choice questions. The pass mark is 50 ie. 45 out of 90. INTRODUCTION iv Course Aims Achieving ACCAs Study Guide Outcomes Business organisations structure governance and management A1 The business organisation and its structure Chapter 1A2 The formal and informal business organisation Chapter 3 A3 Organisational culture in business Chapter 3 A4 Stakeholders of business organisations Chapter 3 A5 Information technology and information systems in business Chapter 2 A6 Committees in the business organisation Chapter 1 A7 Business ethics and ethical behaviour Chapter 4 A8 Governance and social responsibility Chapter 5 Key environmental influences and constraints on business and accounting B1 Political and legal factors Chapter 7 B2 Macro-economic factors Chapter 6 B3 Social and demographic factors Chapter 7 B4 Technological factors Chapter 7 B5 Competitive factors Chapter 7 History and role of accounting in business C1 The history and functions of accounting in business Chapter 8 C2 Law and regulations governing accounting Chapter 8 C3 Financial systems procedures and IT applications Chapter 8 C4 The relationship between accounting and other business functions Chapter 1 Specific functions of accounting and internal financial control D1 Accounting and financial functions within business Chapter 1 D2 Internal and external auditing and their functions Chapter 9 D3 Internal financial control and security within business organisations Chapter 9 D4 Fraud and fraudulent behaviour and their prevention in business Chapter 10 INTRODUCTION v Leading and managing individuals and teams E1 Leadership management and supervision Chapter 11 E2 Individual and group behaviour in business organisations Chapter 12 E3 Team formationdevelopment and management Chapter 12 E4 Motivating individuals and groups Chapter 13 Recruiting and developing effective employees F1 Recruitment and selection managing diversity and equal opportunities Chapter 15 16 F2 Techniques for improving personal effectiveness at work and their benefits Chapter 14 F3 Features of effective communication Chapter 14 F4 Training development and learning in the maintenance and improvement of business performance Chapter 17 F5 Review and appraisal of individual performance Chapter 18 INTRODUCTION vi Classroom tuition and Home study Your studies for BPP consist of two elements classroom tuition and home study. Classroom tuition In class we aim to cover the key areas of the syllabus. To ensure examination success you will need to spend private study time reinforcing your classroom course with question practice and reviewing areas of the Course Notes and Study Text. Home study To support you with your private study BPP provides you with a Course Companion which helps you to work at home and aims to ensure your private study time is effectively used. The Course Companion includes a Home Study section which breaks down your home study by days one to be covered at the end of each day of the course. You will find clear guidance as to the time to spend on various activities and their importance. You are also provided with sample questions and either two course exams which should be submitted for marking as they become due or an I-pass CD which is full of questions. These may include questions on topics covered in class and home study. BPP Learn Online Come and visit the BPP Learn Online free at/acca/learnonline for exam tips FAQs and syllabus health check. ACCA Forum We have thriving ACCA bulletin boards at /accaforum. Register and discuss your studies with tutors and students. Helpline If you have any queries during your private study simply contact your class tutor on the telephone number or e-mail address that they will supply. Alternatively call 44 020 8740 2222 or your local training centre if outside the London area and ask for a tutor for this paper to speak to you or to call you back within 24 hours. Feedback The success of BPP’s courses has been built on what you the students tell us. At the end of the course for each subject you will be given a feedback form to complete and return. If you have any issues or ideas before you are given the form to complete please raise them with the course tutor or relevant head of centre. If this is not possible please email . INTRODUCTION vii Key to icons Question practice from the Study Text This is a question we recommend you attempt for home study. Real world examples These can be found in the Course Companion. Section reference in the Study Text Further reading is needed on this area to consolidate your knowledge. INTRODUCTION viii 1.1 Syllabus Guide Detailed Outcomes Having studied this chapter you will be able to: ?? Ascertain the appropriate organisational structure for different types and sizes of business. ?? Understand the concepts of span of control and scalar chains. ?? Appreciate the differing levels of strategy in an organisation. Exam Context This chapter lays the foundation for an understanding of what organisations are what they do and how they do it. Section 2 Organisational structure represents a higher level of knowledge. You must be able to apply knowledge to exam questions. Qualification Context An understanding of business structures is important with regard to higher level accounting papers as well as P3 Business Analysis. Business Context Appreciating why organisations are structured in different ways will help with an understanding of how they should be managed. Business organisation and structure 1: BUSINESS ORGANISATION AND STRUCTURE 1.2Overview Departments and functions Why does the organisation exist Structural forms Business hierarchy 1: BUSINESS ORGANISATION AND STRUCTURE 1.3 1 Organisations 1.1 Definition – An organisation is a social arrangement which pursues collective goals which controls its own performance and which has a boundary separating it from its environment. Boundaries can be physical or social. 1.2 Key categories: ?? Commercial ?? Not for profit ?? Public sector ?? Charities ?? Trade unions ?? Local authorities ?? Mutual associates Class exercise Required Identify a real-world example of the above categories of organisation. 1.3 Organisations owned or run by the government local or national or government agencies are described as being in the public sector. All other organisations are classified as the private sector. Limited liability 1.4 Limited companies denoted by X Ltd or X plc are set up so as to have a separate legal entity from their owners shareholders. Liability of these owners is thus limited to the amount invested. Private v public 1.5 Private companies are usually owned by a small number of people family members and these shares are not easily transferable. Shares of public companies will be traded on the Stock Exchange. Pg 52-561: BUSINESS ORGANISATION AND STRUCTURE 1.4 2 Organisational structure 2.1 Henry Mintzberg believes that all organisations can be analysed into five components according to how they relate to the work of the organisation and how they prefer to co-ordinate. a Strategic apex Drives the direction of the business through control over decision-making. b Technostructure Drives efficiency through rules and procedures. c Operating core Performs the routine activities of the organisation in a proficient and standardised manner. d Middle line Performs the management functions of control over resources processes and business areas. e Support staff Provide expertise and service to the organisation. Strategic Apex Support Staff Technostructure Middle Line Operating Core 1: BUSINESS ORGANISATION AND STRUCTURE 1.5 Exam standard question Required Match the following staff/rules to Mintzbergs technostructure: a Manager of a retail outlet supervising 40 staff. b A salesman responsible for twenty corporate accounts. c The owner of a start-up internet company employing two staff. d The HR department which provides support to business managers. e The IT department seeking to standardise internal systems. 3 Structural forms for organisations Scalar chain and span of control 3.1 As organisations grow in size and scope different organisational structures may be suitable. 3.2 The Scalar chain and Span of control determine the basic shape. The scalar chain relates to levels in the organisation and the span of control the number of employees managed. 3.3 Tall organisations have a: a Long scalar chain via layers of management b Hierarchy c Narrow span of control. 3.4 Flat organisations have a: a Short scalar chain less layers b Wide span of control. 1: BUSINESS ORGANISATION AND STRUCTURE 1.6 3.5 MD Divisional directors Department managers Section managers MD Supervisors Department managers Charge hands Supervisors Workers Workers Tall Flat Pilot paper Required Identify factors which may contribute to the length of the chain and the span of control. Organisational structures 3.6 Entrepreneurial A fluid structure with little or no formality. Suitable for small start-up companies the activities and decisions are dominated by a key central figure the owner/entrepreneur. 3.7 Functional This structure is created via separate departments or functions. Employees are grouped by specialism and departmental targets will be set. Formal communication systems will be set up to ensure information is shared. 1: BUSINESS ORGANISATION AND STRUCTURE 1.7 3.8 Matrix A matrix organisation crosses a functional with a product/customer/projectstructure. This structure was created to bring flexibility to organisations geared towards project work or customer-specific jobs. Staff may be employed within a hierarchy or within specific functions but will be slotted into different teams or tasks where their skill is most needed. The matrix structure is built upon the principles of flexibility and dual authority. Required Identify two advantages and two disadvantages of each structure. Advantages Disadvantages Entrepreneurial Functional Matrix 3.9 Organisations are rarely composed of only one type of structure especially if the organisation has been in existence for some time and as a consequence a hybrid structure may be established. Hybrid structures involve a mixture of functional divisionalisation and at least one other form of divisionalisation. Area Manager A Area Manager B Area Manager C.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

RMB

200,000 80,000

248,000 64,000

200,000 ––––––––––

1,700,000 15,000

155,790 300,000 ––––––––––

RMB 16,600,000

792,000

(2,170,790) –––––––––– 15,221,120 ––––––––––

i.e. RMB200,000 x 60% = RMB120,000 is deductible. Thus, RMB120,000 is deductible and

RMB80,000 (200,000 – 120,000) is non-deductible. Also any excess amount cannot be carried

RMB200,000) x 2% = RMB36,000. Thus, RMB64,000 (100,000 – 36,000) is non-deductible.

Any excess amount cannot be carried forward.

2

(9) Staff and workers’ education expenses cannot exceed 2·5% of total salaries and wages, i.e.

1

(5) Allowable entertaining expenses cannot exceed 0·5% of the sales/business income of the year, i.e.

RMB60,000,000 x 0·5% = RMB300,000; a maximum of 60% of the entertainment expenses,

Marks

0·5

0·5 0·5 0·5 0·5 0·5

0·5 0·5 0·5 0·5 –––

5 –––

1 1 1 ––– 3 –––

(b) The revenue base used for the calculation of allowable advertising expenses should include the business/sales

(1) The bonus payable is not allowable until it is actually paid.

1

(2) The deemed sales principle is not applied to self-used products for EIT purposes, so no adjustment

1

IIT on the annual bonus:

The applicable IIT rate for the annual bonus is 15% (40,000/12 = 3,333·33)

RMB (40,000 x 15% – 125) = RMB5,875

1

(2) IIT in relation to the income from the provision of technical services:

2

12

(3) IIT in relation to the publication of the novel and its serialisation: RMB [(50,000 + 20,000) x (1 – 20%) x 20% x (1 – 30%) + 3,600 x 3 x (1 – 20%) x 20% x (1 – 30%)] = RMB7,840 + RMB1,210 = RMB9,050

RMB155,790.

3

(12) The writing off of a liability is taxable.

1

(13) Interest income on a national debenture is exempt.

1

–––

20

–––

11

(ii) Enterprise income tax computation for the year 2009

forward.

2

(6) Allowable advertisement expenses cannot exceed 15% of the sales/business income of the year,

i.e. RMB60,000,000 x 15% = RMB9,000,000, so the whole of the current year’s expense is

IIT was paid by the enterprise, therefore if the tax paid equals ‘t’:

(25,000 + t) x (1 – 20%) x 30% – 2,000 = t

Solving the equation the tax payable (t) equals RMB5,263

RMB252,000 is deductible and RMB248,000 (500,000 – 252,000) is non-deductible. Any

excess amount cannot be carried forward.

(8) Union expenses cannot exceed 2% of the total salaries and wages, i.e. (RMB2,000,000 –

Taxable profit before adjustment Add: (1) Bonus payable (5) Entertainment (7) Staff benefit (8) Union expenses (10) Interest capitalised

Less: (6) Advertisement expenses (9) Staff and workers’ education expenses (11) Non-deductible input VAT (13) Interest on national debenture

1

(11) The net loss on the stock, including the non-deductible input VAT should be tax allowable. The

non-deductible input VAT is RMB850,000 x 17% + (RMB150,000/(1 – 7%)) x 7% =

1

–––

4

–––

35 –––

2 Mr Duan

(1) IIT in relation to the monthly salary:

RMB [(22,000 – 2,000) x 25% – 1,375] x 11 = RMB39,875

1

The RMB20,000 of salary donated to an approved charity in September is exempt from IIT.

1,700,000) is carried forward.

2

(7) Staff and workers’ benefits cannot exceed 14% of the total salaries and wages but sponsorship is

not deductible regardless of amount. Thus, (RMB2,000,000 – RMB200,000) x 14% =

1

The sales revenue is RMB500,000/(1·17) = RMB427,350

0·5

The taxable income arising from the sales is RMB427,350 – RMB225,580 = RMB201,770

0·5

So, the EIT payable is (RMB201,770 + RMB234,000) x 25% = RMB108,943.

2

–––

3

–––

(c) Company X

The taxable income arising from the donation is RMB200,000 + RMB34,000 = RMB234,000

1

The cost of the sales is RMB200,000 + RMB20,000 + (RMB6,000 x (1 – 7%)) = RMB225,580

Answers

Fundamentals Level – Skills Module, Paper F6 (CHN) Taxation (China)

June 2010 Answers and Marking Scheme

1 (a) Company K

Marks

(i) Treatment of items

(RMB2,000,000 – RMB200,000) x 2·5% = RMB45,000, so the whole of the current year’s

expense is deductible. Also, any excess amount carried forward is deductible up to the limit. Thus,

RMB30,000 + RMB15,000 from 2008 is deductible and RMB75,000 (90,000 – 15,000) is