会计学原理 快速测试(英文版)

会计学原理 英文版 答案2

!

#74P&'4(%;(CQ&4%5;74(

! ! ( RK! ! ( )K! ! ( SK! ! ( TK! ! ( UK! ! ! ! ( VK! ! ! ! ! ! ! ! ( WK! ! ! ! ! ! ! XK! ! ! ! ! YK! ! ! ! ! ! ! RZK! ! ! ! !

!

!"#$%&'()(

! ! !

%*+('+,-./012($.-,+33(

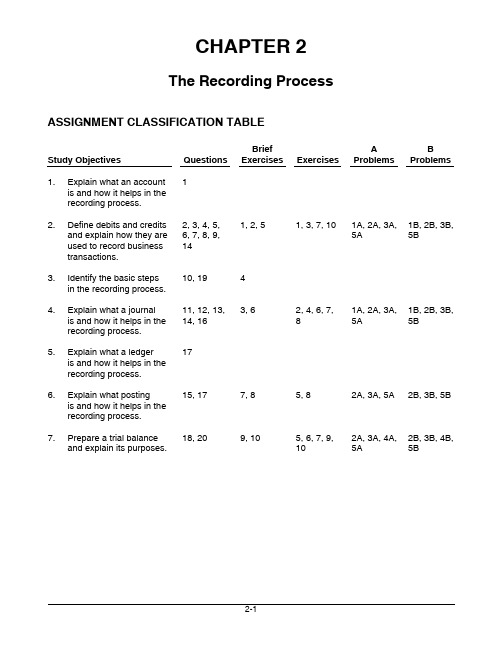

#445678&7%(!9#445:5!#%5;7(%#<9&(

! ! ( 4=>/?(;@A+,=0B+3( ! ! $%! &'()*+,!-.*/!*,!*0012,/! ! +3!*,4!.1-!+/!.5)(3!+,!/.5! 650164+,7!(610533%! ! ! "%! 859+,5!45:+/3!*,4!0654+/3! ! *,4!5'()*+,!.1-!/.5;!*65! 2354!/1!650164!:23+,533! /6*,3*0/+1,3%! ! ! =%! G45,/+9;!/.5!:*3+0!3/5(3! ! +,!/.5!650164+,7!(610533%! ! ! >%! &'()*+,!-.*/!*!H126,*)! ! +3!*,4!.1-!+/!.5)(3!+,!/.5! 650164+,7!(610533%! ! ! ?%! &'()*+,!-.*/!*!)54756! ! +3!*,4!.1-!+/!.5)(3!+,!/.5! 650164+,7!(610533%! ! ! @%! &'()*+,!-.*/!(13/+,7! ! +3!*,4!.1-!+/!.5)(3!+,!/.5! 650164+,7!(610533%! ! ! A%! I65(*65!*!/6+*)!:*)*,05! ! *,4!5'()*+,!+/3!(26(1353%! ! ! ! ! ( <.0+D( ! ( #( <( C>+3=0-13( &E+.,03+3( &E+.,03+3( $.-@F+G3( $.-@F+G3( ! ! ! ! ! ! ! ! ! $! ! ! ! ! ! ! ! ! ! ! ! "<!=<!><!?<! ! $<!"<!?! @<!A<!B<!C<! $>! ! $D<!$C! ! ! ! >! ! ! ! ! ! ! ! $<!=<!A<!$D! ! $E<!"E<!=E<!! $F<!"F<!=F<! ?E! ?F! ! ! ! ! ! ! ! ! ! ! ! !

怀尔德会计学原理21版英语题库答案

怀尔德会计学原理21版英语题库答案怀尔德会计学原理21版英语题库答案Chapter 1Accounting in BusinessQUESTIONS1. The purpose of accounting is to provide decision makers with relevant and reliableinformation to help them make better decisions. Examples include information forpeople making investments, loans, and business plans.2. Technology reduces the time, effort, and cost of recordkeeping. There is still ademand for people who can design accounting systems, supervise their operation,analyze complex transactions, and interpret reports. Demand also exists for peoplewho can effectively use computers to prepare and analyze accounting reports.Technology will never substitute for qualified people with abilities to prepare, use,analyze, and interpret accounting information.3. External users and their uses of accounting information include:(a) lenders, tomeasure the risk and return of loans; (b) shareholders, to assess whether to buy,sell, or hold their shares; (c) directors, to oversee theirinterests in the organization;(d) employees and labor unions, to judge the fairness of wages and assess futureemployment opportunities; and (e) regulators, to determine whetherthe organizationis complying with regulations. Other users are voters, legislators, governmentofficials, contributors to nonprofits, suppliers and customers.4. Business owners and managers use accounting information to help answerquestions such as: What resources does an organization own? Whatdebts are owed?How much income is earned? Are expenses reasonable for the level of sales? Arecustomers‘ accounts being promptly collected?5. Service businesses include: Standard and Poor‘s, Dun & Bradstreet, Merrill Lynch,Southwest Airlines, CitiCorp, Humana, Charles Schwab, and Prudential. Businessesoffering products include Nike, Reebok, Gap, Apple Computer, Ford Motor Co.,Philip Morris, Coca-Cola, Best Buy, and Circuit City.6. The internal role of accounting is to serve the organization‘s internal ope ratingfunctions. It does this by providing useful information for internal users incompleting their tasks more effectively and efficiently. By providing this information,accounting helps the organization reach its overall goals.7. Accounting professionals offer many services including auditing, managementadvice, tax planning, business valuation, and money management.8. Marketing managers are likely interested in information such as sales volume,advertising costs, promotion costs, salaries of sales personnel, and salescommissions.9. Accounting is described as a service activity because it serves decision makers byproviding information to help them make better business decisions.10. Some accounting-related professions include consultant,financial analyst,underwriter, financial planner, appraiser, FBI investigator, market researcher, andsystem designer.11. Ethics rules require that auditors avoid auditing clients in which they have a directinvestment, or if the auditor‘s fee is dependent on the figures in the client‘s reports.This will prev ent others from doubting the quality of the auditor‘s report.12. In addition to preparing tax returns, tax accountants help companies and individualsplan future transactions to minimize the amount of tax to be paid. They are alsoactively involved in estate planning and in helping set up organizations. Some taxaccountants work for regulatory agencies such as the IRS or the various statedepartments of revenue. These tax accountants help to enforce tax laws. 13. The objectivity concept means that financial statement information is supported byindependent, unbiased evidence other than someone‘s opinion or imagination. Thisconcept increases the reliability and verifiability of financial statement information. 14. This treatment is justified by both the cost principle and the going-concernassumption.15. The revenue recognition principle provides guidance for managers and auditors sothey know when to recognize revenue. If revenue is recognized too early, thebusiness looks more profitable than it is. On the other hand, if revenue isrecognized too late the business looks less profitable than it is. This principledemands that revenue be recognized when it is both earned and can be measuredreliably. The amount of revenue should equal the value of the assets received orexpected to be received from the business‘s operating activities covering a specifictime period.16. Business organizations can be organized in one of three basic forms: soleproprietorship, partnership, or corporation. These forms have implications for legalliability, taxation, continuity, number of owners, and legal status as follows:Proprietorship Partnership CorporationBusiness entity yes yes yesLegal entity no no yesLimited liability no* no* yesUnlimited life no no yesBusiness taxed no no yesOne owner allowed yes no yes*Proprietorships and partnerships that are set up as LLCs provide limited liability.17. (a) Assets are resources owned or controlled by a company that are expected toyield future benef its. (b) Liabilities are creditors‘ claims on assets that reflectobligations to provide assets, products or services to others.(c) Equity is theowner‘s claim on assets and is equal to assets minus liabilities.(d) Net assets referto equity.18. Equity is increased by investments from the owner and by net income. It isdecreased by withdrawals by the owner and by a net loss (which is the excess ofexpenses over revenues).19. Accounting principles consist of (a) general and (b) specific principles. Generalprinciples are the basic assumptions, concepts, and guidelines for preparingfinancial statements. They stem from long-used accounting practices. Specificprinciples are detailed rules used in reporting on business transactions and events.They usually arise from the rulings of authoritative and regulatory groups such asthe Financial Accounting Standards Board or the Securities and ExchangeCommission.20. Revenue (or sales) is the amount received from selling products and services. 21. Net income (also called income, profit or earnings) equals revenues minus expenses(if revenues exceed expenses). Net income increases equity. If expenses exceedrevenues, the company has a Net Loss. Net loss decreases equity.22. The four basic financial statements are: income statement, statement of owner‘sequity, balance sheet, and statement of cash flows.23. An income statement reports a company‘s revenues and expenses along with theresulting net income or loss over a period of time.24. Rent expense, utilities expense, administrative expenses, advertising and promotionexpenses, maintenance expense, and salaries and wages expenses are someexamples of business expenses.25. The statement of owner‘s equity explains the changes in equity from net income orloss, and from any owner contributions and withdrawals over a period of time. 26. The balance sheet describes a company‘s financial position (types and amounts ofassets, liabilities, and equity) at a point in time.27. The statement of cash flows reports on the cash inflows and outflows from acompany‘s operating, investing, and financing activities.28. Return on assets, also called return on investment, is a profitability measure that isuseful in evaluating management, analyzing and forecasting profits, and planningactivities. It is computed as net income divided by the averagetotal assets. Forexample, if we have an average annual balance of $100 in a bank account and itearns interest of $5 for the year, then our return on assets is $5 / $100 or 5%. Thereturn on assets is a popular measure for analysis because it allows us to comparecompanies of different sizes and in different industries.A 29. Return refers to income, and risk is the uncertainty about the return we expect tomake. The lower the risk of an investment, the lower the expected return. Forexample, savings accounts pay a low return because of the low riskof a bank notreturning the principal with interest. Higher risk implies higher,but riskier, expectedreturns.B30. Organizations carry out three major activities: financing,investing, and operating.Financing provides the means used to pay for resources. Investing refers to theacquisition and disposing of resources necessary to carry out the organizat ion‘splans. Operating activities are the actual carrying out of these plans. (Planning is theglue that connects these activities, including the organization’s ideas, goals andstrategies.)B31. An organization‘s financing activities (liabilities and equity) pay for investingactivities (assets). An organization cannot have more or less assets than itsliabilities and equity combined and, similarly, it cannot have more or less liabilitiesand equity than its total assets. This means: assets = liabilities + equity. Thisrelation is called the accounting equation (also called the balance sheet equation),and it applies to organizations at all times.32. The dollar amounts in Best Buy‘s financial statements are rounded to the nearest$1,000,000. Bes t Buy‘s consolidated st atement of earnings (or income statement)covers the fiscal year (consisting of 53 weeks) ended March 3, 2007. Best Buy alsoreports comparative income statements for the previous two years (consisting of 52weeks).33. In thousa nds, Circuit City‘s accoun ting equation is:Assets = Liabilities + Equity$4,007,283 = $2,216,039 + $1,791,24434. At December 31, 2006, RadioShack had (in millions) assets of $2,070.0, liabilities of$1,416.2, and equity of $653.8.35. The independent auditor for Apple, Inc., is KPMG LLP. The auditor expressly statesthat ―our responsibility is to express an opinion on these consolidated financialstatements based on our audits.‖ The auditor also states that ―these consolidatedfinancial statements are the responsibility of the Com pany‘s management.‖Chapter 21EXERCISESExercise 21-1 (25 minutes)1. Allocation of Indirect Expenses to Four Operating DepartmentsSupervision expensesDepartment Employees % of Total CostMaterials ................................ 40 20% $16,000Personnel .............................. 22 11 8,800Manufacturing ....................... 104 52 41,600Packaging .............................. 34 17 13,600Totals ..................................... 200 100% $80,000 Utilities expensesDepartment Square Feet % of Total CostMaterials ................................ 27,000 27% $16,470 Personnel .............................. 5,000 5 3,050Manufacturing ....................... 45,000 45 27,450Packaging .............................. 23,000 23 14,030Totals ..................................... 100,000 100% $61,000 Insurance expensesDepartment Asset Value % of T otal CostMaterials ................................ $ 60,000 50% $ 8,350 Personnel .............................. 1,200 1 167Manufacturing ....................... 42,000 35 5,845Packaging .............................. 16,800 14 2,338Totals .....................................$120,000 100% $16,7002. Report of Indirect Expenses Assigned to Four Operating DepartmentsSupervision Utilities Insurance TotalMaterials ................................$16,000 $16,470 $ 8,350 $ 40,820 Personnel ..............................8,800 3,050 167 $ 12,017 Manufacturing .......................41,600 27,450 5,845 $ 74,895 Packaging .............................. 13,600 14,030 2,338 $ 29,968 Totals ................................$80,000..... $61,000 $16,700 $157,700 Exercise 21-2 (30 minutes)Calculation of predetermined overhead rates to apply ABC Overhead Cost TotalCategory (Activity Total Amount ofCost Pool) Cost Cost Driver Predetermined Overhead Rate Supervision ........................$ 5,400 $36,000 15% of direct labor costDepreciation .......................56,600 2,000 MH $28.30 per machine hourLine preparation ................46,000 250 setups $184.00 per setup1. Assignment of overhead costs to the two products usingABCRounded edgeCost Cost per AssignedDriver Driver Unit CostSupervision ........................... $12,200 15% $ 1,830Machinery depreciation ........ 500 hours $ 28.30 14,150Line preparation.................... 40 setups $184.00 7,360Total overhead assigned ...... $23,340Squared edgeCost Cost per AssignedDriver Driver Unit CostSupervision ........................... $23,800 15% $ 3,570Machinery depreciation ........ 1,500 hour$ 28.30 42,450sLine preparation....................210 setups $184.00 38,640Total overhead assigned ...... $84,6602. Average cost per foot of the two productsRounded edge Squared edgeDirect materials .......................... $19,000 $ 43,200Direct labor ................................. 12,200 23,800Overhead (using ABC) ............... 23,340 84,660Total cost ................................... $54,540 $151,660Quantity produced ..................... 10,500 ft. 14,100 ft.Average cost per foot (ABC) ...... $5.19 $10.763. The average cost of rounded edge shelves declines and the average cost of squared edge shelves increases. Under the current allocation method, the rounded edge shelving was allocated 34% of all of the overhead cost ($12,200 direct labor/$36,000 total direct labor). However, it does not use 34% of all of the overhead resources. Specifically, it uses only 25% ofmachine hours (500 MH/2,000 MH), and 16% of the setups (40/250). Activity based costing allocated the individual overhead components in proportion to the resources used.Exercise 21-7 (15 minutes)(1) Items included in performance reportThe following items definitely should be included in the performance report for the auto service department manager because they arecontrolled or strongly influenced by the manager‘s decisions and activities:, Sales of parts, Sales of services, Cost of parts sold, Supplies, Wages (hourly)(2) Items excluded from performance reportThe following items definitely should be excluded from the performance report because the department manager cannot control or strongly influence them:, Building depreciation, Income taxes allocated to the department, Interest on long-term debt, Manager‘s salary(3) Items that may or may not be included in performance report The following items cannot be definitely included or definitely excluded from the performance report because they may or may not be completely under the manager‘s control or strong influence:, Payroll taxes Some portion of this expense relates to themanager‘s salary and is not controllable by themanager. The portion that relates to hourly wagesshould be treated as a controllable expense., Utilities Whether this expense is controllable depends on the design of the auto dealership. If the auto servicedepartment is in a separate building or has separateutility meters, these expenses are subject to themanager‘s control. Otherwise, th e expense probablyis not controllable by the manager of the auto servicedepartment.Exercise 21-9 (20 minutes)(1)Investment Center Net Income Average Assets Return on AssetsElectronics ................... $750,000 $3,750,000 20%Sporting Goods ............ 800,000 5,000,000 16%Comment: Its Electronics division is the superior investment center on the basis of the investment center return on assets.Exercise 21-9 (continued)(2)Investment Center Electronics Sporting GoodsNet income ................... $750,000 $800,000Target net income$3,750,000 x 12% ....... (450,000)5,000,000 x 12% ........ (600,000)Residual income……. $300,000 $200,000Comment: Its Electronics division is the superior investment center on the basis of investment center residual income.(3) The Electronics division should accept the new opportunity, since it will generate residual income of 3% (15% - 12%) of the investment‘s investedassets.Exercise 21-10 (15 minutes)Investment Center Net Income Sales Profit MarginElectronics ................... $750,000 $10,000,000 7.50%Sporting Goods ............ 800,000 8,000,000 10.0%InvestmentInvestment Center Sales Average Assets TurnoverElectronics ...................$10,000,000 $3,750,000 2.67Sporting Goods ............ 8,000,000 5,000,000 1.6Comments: Its Sporting goods division generates the most net income per dollar of sales, as shown by its higher profit margin. The Electronics division however is more efficient at generating sales from invested assets, based on its higher investment turnover.PROBLEM SET AProblem 21-1A (60 minutes)Part 1Average occupancy cost = $111,800 / 10,000 sq. ft. = $11.18 per sq. ft.Occupancy costs are assigned to the two departments as follows Department Square Footage Rate TotalLanya‘s Dept. ............... 1,000 $11.18 $11,180Jimez‘s Dept. ................ 1,700 $11.18 $19,006**A total of $30,186 ($11,180 + $19,006) in occupancy costs is charged to these departments. The company would follow a similar approach in allocating the remaining occupancy costs ($81,614, computed as $111,800 - $30,186) to its other departments (not shown in this problem).Part 2Market rates are used to allocate occupancy costs fordepreciation, interest, and taxes. Heating, lighting, and maintenance costs are allocated to the departments on both floors at the average rate per square foot. These costs are separately assigned to each class as follows:Total Value-Based Usage-BasedCosts Costs CostsDepreciation—Building...................$ 31,500 $31,500Interest—Building mortgage .......... 47,000 47,000Taxes—Building and land............... 14,000 14,000Gas (heating) expense .................... 4,425 $ 4,425Lighting expense ............................ 5,250 5,250Maintenance expense ..................... 9,625 ______ 9,625Total .................................................$111,800 $92,500 $19,300Problem 21-1A (Continued)Value-based costs are allocated to departments in two steps(i) Compute market value of each floorSquare Value perFloor Footage Sq. Ft. TotalFirst floor ...............................5,000 $40 $200,000Second floor ..........................5,000 10 50,000Total market value................. $250,000(ii) Allocate $92,500 to each floor based on its percent of market valueMarket % of Allocated Cost perFloor Value T otal Cost Sq. Ft.First floor ...............................$200,000 80% $74,000$14.80Second floor .......................... 50,000 20 18,500 3.70Totals ................................$250,000..... 100% $92,500 Usage-based costs allocation rate = $19,300 / 10,000 sq. ft.= $1.93 per sq. ft.We can then compute total allocation rates for the floors FloorValue Usage TotalFirst floor ............................... $14.80 $1.93 $16.73Second floor .......................... 3.70 1.93 $ 5.63These rates are applied to allocate occupancy costs to departments SquareDepartment Footage Rate TotalLanya‘s Department ........................ 1,000 $16.73 $16,730Jim ez‘s Department ........................ 1,700 5.63 $ 9,571Part 3A second-floor manager would prefer allocation based on market value. This is a reasonable and logical approach to allocation of occupancy costs. The current method assumes all square footage has equal value. This is not logical for this type of occupancy. It also means the。

会计学原理23版 英文练习WildFAP23eCh07EPPT

General Journal

May 2 May 5 May 7 May 8 May 12 May 16 May 19 May 25

Sold merchandise costing $300 to B. Facer for $450 cash, invoice no. 5703. Purchased $2,400 of merchandise on credit from Marchant Corp. Sold merchandise costing $800 to J. Dryer for $1,250, terms 3/10, n/30, invoice no. 5704. Borrowed $9,000 cash by signing a note payable to the bank. Sold merchandise costing $200 to R. Lamb for $340, terms n/30, invoice no. 5705. Received $1,225 cash from J. Dryer to pay for the purchase of May 7. Sold used store equipment for $900 cash to Golf, Inc. Sold merchandise costing $500 to T. Taylor for $750, terms n/30, invoice no. 5706.

May 2 Sold merchandise costing $410 to B. Facer for $615 cash, invoice no. 5703. May 5 Purchased $2,550 of merchandise on credit from Marchant Corp. May 7 Sold merchandise costing $1,107 to J. Dryer for $1,605, terms 3/10, n/30, invoice no. 5704. May 8 Borrowed $8,000 cash by signing a note payable to the bank. May 12 Sold merchandise costing $277 to R. Lamb for $443, terms n/30, invoice no. 5705. May 16 Received $1,557 cash from J. Dryer to pay for the purchase of May 7. May 19 Sold used store equipment for $900 cash to Golf, Inc. May 25 Sold merchandise costing $460 to T. Taylor for $722, terms n/30, invoice no. 5706. Journalize the May transactions that should be recorded in the sales journal assuming the perpetual inventory system is used.

会计学原理 1—6章 英文练习

Chap 11.Mostly the objective of a business is not to make a profit.错2. A corporation is a business that is legally separate and distinct from its owners.对3. Accounting is a service that provides many different users with financial information to make economic decisions.对4. Primary users of accounting information are accountants.错5. "Managerial accounting is primarily concerned with the recording and reporting of economic data and activities of an entity for use by owners, creditors, governmental agencies, and the public." 错6. The financial statements of a proprietorship should include the owner's personal assets and liabilities.错7. The unit of measurement concept requires that economic data be recorded in a common unit of measurement 对8. "If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000." 错9.An entity that is organized according to state or federal statutes and in which ownership is divided into shares of stock is a答案BA. proprietorshipB. corporationC. partnershipD. governmental unit10.Which of the following best describes accounting? BA. records economic data but does not communicate the data to users according to any specific rulesB. is an information system that provides reports to stakeholdersC. is of no use by individuals outside of the businessD. is used only for filling out tax returns and for financial statements for various type of governmental reporting requirements11. The two most common specialized fields of accounting in practice are BA. forensic accounting and financial accountingB. managerial accounting and financial accountingC. managerial accounting and environmental accountingD. financial accounting and tax accounting systems12.Which of the following is not a characteristic of financial accounting ______ CA. external reportingB. general-purpose informationC. future orientationD. standard and uniform reporting13.The business entity concept means that DA. the owner is part of the business entityB. an entity is organized according to state or federal statutesC. an entity is organized according to the rules set by the FASBD. "the entity is an individual economic unit for which data are recorded, analyzed, and reported"14."For accounting purposes, the business entity should be considered separate from its owners if the entity is" DA. a corporationB. a proprietorshipC. a partnershipD. all of the above15."Tom Smith is the owner of a small bookstore. He mainly does business through the internet so that the store has no physical office room and the ordersare dealt with at home. As a result, such bills as electricity, heating, telephone, and housecleaning are all recorded as expenses of the bookstore. This is not correct from the viewpoint of _______" AA. the separate entity conceptB. the going concern assumptionC. the accounting period conceptD. the monetary measurement assumption16.Which of the followings assures the accounting information users of timely decision___________ CA. the separate entity conceptB. the going concern assumptionC. the accounting period conceptD. the monetary measurement assumption17."Smith Company purchased $105,000 of computer equipment from Brown Company. Smith Company paid for the equipment using cash that had been obtained from the initial investment by Connie Smith. The transaction involving the computer equipment should be recorded on the accounting records of which of the following entities?" DA. Smith Company and Connie Smith's personal recordsB. Brown Company and Connie Smith's personal recordsC. Brown CompanyD. Smith Company and Brown Company18."The Reynolds Company estimated that the value of its land had increased from $10,000 to $16,000 and therefore wrote up the land account to $16,000. Which accounting concept(s) was (were) violated?" CA. separate entity conceptB. money measurement conceptC. historical cost conceptD. accounting period concept19.“Equipment with an estimated m arket value of $45,000 is offered for sale at $65,000. The equipment is acquired for $10,000 in cash and a note payable of $40,000 due in 30 days. The amount used in the buyer's accounting records to record this acquisition is" AA.50000B.65000C.10000D.4500020."(mark out all correct answers) Which of the followings should not be included in the financial records of Delicious Sam, a bakery at the corner of the street ____________" A C DA. "Sweetie Alice, another bakery located opposite to Delicious Sam, lowered its price for brown bread from 50 cents to 30 cents "B. Delicious Sam purchased 100kg of flour for $50C. "Sweetie Alice sold cookie of $10 to Sam, the owner of Delicious Sam."D. Delicious Sam promised free delivery to bulk buying customers in order to compete with Sweetie Alice.E. Sam withdrew $200 from his personal bank account to pay the bill from the miller who supplied flour to Delicious SamChap 2 –a3.An asset must have a physical substance and can be touched. 错9. Match each of the following items to: a. assets; b. liabilities; c. owners' equity;d. none of above items. 1.ending inventory ; 2.accounts payable to the suppliers;3.salaries due but unpaid;4.accounts receivable;5.retained earnings;6.capital stock;7.prepaid insurance答案:a b b a c c a13.How does the collection of cash from a customer who was previously put on account affect the accounting equation?答案CA.assets decrease; owner's equity decreases B.assets increase; owner's equity increasesC. assets increase; assets decreaseD. assets increase; liabilities increase25.(mark out all correct answers) The owner’s equity accounts of a partnership might be答案 B D EA. capital stockB. "Tom Smith, capital"C. retained earningsD. "Alice Butler, capital"E. "Pauline Jones, capital"Chap 2 –b3.Indicate for each of following transactions should related accounts be debited or credited. 1.Purchased inventory on account. The inventory account should be____; 2.Borrowed money from a bank. The notes payable account should be___; 3.Issued stock for cash. The capital stock should be____ 答案D C C6.Owner's equity is increased by 答案BA. cashB. revenueC. accounts receivableD. all of the above8."For a corporation, temporary proprietorship accounts are supposed to replace the ____________________ account temporarily."答案 retained earnings12.Consuming goods and services in the process of generating revenues results in expenses. 对17. Net profit reported in the Income statement will not be reduced when the corporation declares and pays cash dividends to the stockholders 对21. A credit signifies a decrease in 答案AA. drawingsB. liabilitiesC. capitalD. revenue27."Land, originally purchased for $20,000, is sold for $75,000 in cash. What is the effect of the sale on the accounting equation?" 答案BA. "assets increase $75,000; owner's equity increases $75,000"B. "assets increase $55,000; owner's equity increases $55,000"C. "assets increase $75,000; liabilities decrease $20,000; owner's equity increases $55,000"D. "assets increase $20,000; no change for liabilities; owner's equity increases $75,000"29.Which of the following entries records the payment of an account payable? 答案 DA. debit Cash; credit Accounts PayableB. debit Accounts Receivable; credit CashC. debit Cash; credit Supplies ExpenseD. debit Accounts Payable; credit CashChap 3 –a2.Which one of the following is a purpose of the ledger rather than a purpose of the journal?答案 AA. to show increases and decreases in accountsB. to show a chronological order for transactionsC. to show a complete transaction in one placeD. to help locate errors10.The accounting entry to record the purchase of office supplies for cash will not involve an expense account. 对14.The process of transferring the data from the journal to the ledger accounts is posting. 对20.Posting a transaction twice will not cause the trial balance totals to be unequal.对21.Journalizing a transaction with both the debit and the credit for $69 instead of $96 will cause the trial balance to be out of balance. 错23."The total number at the bottom of the trial balance should equal to the total number at the bottom of the balance sheet, because they both show the equality of the accounting equation." 错24.(mark out all correct answers) The credit column of a T/B might include _______ accounts。

会计学原理 快速测试(英文版)

TEST FOR CHAPTER 1-4注:判断题红色标记句为错句,选择题加下划线选项为正确答案PART I TRUE OR FALSE1)Accounting is an information and measurement system that identifies, records, and communicatesrelevant, reliable, and comparable formation about an organization's business activities.2)Managerial accounting is the area of accounting that provides internal reports to assist the decisionmaking needs of internal users.3)The primary objective of financial accounting is to provide general purpose financial statementsto help external users analyze and interpret an organization's activities.4)Internal users include lenders, shareholders, brokers and managers.5)In the partnership form of business, the owners are called stockholders.6)The business entity principle means that a business will continue operating for an indefinite periodof time.7)As a general rule, revenues should not be recognized in the accounting records until it is receivedin cash.8)Accrued expenses at the end of one accounting period are expected to result in cash payments in afuture period.9)The idea that a business will continue to operate until it can sell its assets to pay its creditorsunderlies the going-concern assumption.10)The monetary unit assumption means that all international transactions must be expressed indollars.11)The International Accounting Standards Board (IASB) is the government group that establishesreporting requirements for companies that issue stock to the public.12)Expenses decrease equity and are the costs of assets or services used to earn revenues.13)A company might provide a service or product on credit. "On credit" implies that the cash paymentwill occur on a later date.14)Each adjusting entry affects only one or more income statement account and never cash.15)The legitimate claims of a business's creditors take precedence over the claims of the businessowner.16)Under the cash basis of accounting, no adjustments are made for prepaid, unearned, and accrueditems.17)From an accounting perspective, an event is a happening that affects an entity's accounting equation,but cannot be measured.18)The income statement is a financial statement that shows revenues earned and expenses incurred duringa specified period of time.19)Chuck Taylor withdrew $6,000 in cash from FastForward. This amount should be included as an expenseon the income statement.20)Source documents provide evidence of business transactions and are the basis for accountingentries.21)Items such as sales tickets, bank statements, checks, and purchase orders are source documents.22)It is not necessary to keep separate accounts for all items of importance for business decisions.23)Closing entries are necessary so that owner's capital will begin each period with a zero balance.24)Cash withdrawn by the owner of a proprietorship should be treated as an expense of the business.25)When a company provides services for which cash will not be received until some future date, thecompany should record the amount received as unearned revenue for the amount charged to the customer.26)Double entry accounting requires that each transaction affect, and be recorded in, at least twoaccounts.27)Asset accounts normally have credit balances and revenue accounts normally have debit balances.28)A transaction that decreases an asset account and increases a liability account must also affectone or more other accounts.29)Adjusting entries are used to bring asset or liability accounts to their proper amount and updatethe related expense or revenue account.30)When a company bills a customer for $600 for services rendered, the journal entry to record thistransaction will include a $600 debit to Services Revenue.31)The journal is known as the book of final entry because financial statements are prepared from it.32)The closing process takes place after financial statements have been prepared.33)A trial balance that balances is not proof of complete accuracy in recording transactions.34)Closing entries are designed to transfer the end-of-period balances in the revenue accounts, theexpense accounts, and the withdrawals account to owner's capital.35)If cash was incorrectly debited for $100 instead of correctly credited for $100, the cash accountis out of balance by $100.36)Adjusting entries result in a better matching of revenues and expenses for the period.37)The matching principle requires that expenses get recorded in the same accounting period as therevenues that are earned as a result of the expenses, not when cash is paid.38)On October 15, a company received $15,000 cash as a down payment on a consulting contract. The amountwas credited to Unearned Consulting Revenue. By October 31, 10% of the services required by the contract were completed. The company will record consulting revenue of $1,500 from this contract for October.39)Closing revenue and expense accounts at the end of the accounting period serves to make the revenueand expense accounts ready for use in the next period.40)Accrued expenses reflect transactions where cash is paid before a related expense is recognized.41)Before an adjusting entry is made to recognize the cost of expired insurance for the period, PrepaidInsurance and Insurance Expense are both overstated.42)A company purchased $6,000 worth of supplies in August and recorded the purchase in the Suppliesaccount. On August 31, the fiscal year-end, the supplies count equaled $3,200. The adjusting entry would include a $2,800 debit to Supplies.43)In preparing statements from the adjusted trial balance, the balance sheet must be prepared first.44)A company performs 20 days work on a 30-day contract before the end of the year. The total contractis valued at $6,000 and payment is not due until the contract is fully completed. The adjusting entry includes a $4,000 credit to unearned revenue.45)An unadjusted trial balance is a list of accounts and balances prepared before adjustments arerecorded and posted.46)Financial statements can be prepared directly from the information in the adjusted trial balance.47)Income Summary is a temporary account only used for the closing process.48)Revenue accounts should begin each accounting period with zero balances.49)The last four steps in the accounting cycle include preparing the adjusted trial balance, preparingfinancial statements and recording closing and adjusting entries.50)When expenses exceed revenues, there is a net loss and the Income Summary account would have a creditbalance.51)A post-closing trial balance is a list of permanent accounts and their balances from the ledger afterall closing entries are journalized and posted.PART II MULTIPLE-CHOICE1. The primary objective of financial accounting is:A.To serve the decision-making needs of internal users.B.To provide financial statements to help external users analyze an organization's activities.C.To monitor and control company activities.D.To provide information on both the costs and benefits of looking after products and services.E.To know what, when, and how much to produce.2. Internal users of accounting information include:A.Shareholders.B.Managers.C.Lenders.D.Suppliers.E.Customers.3. A corporation:A.Is a business legally separate from its owners.B.Is controlled by the FASB.C.Has shareholders who have unlimited liability for the acts of the corporation.D.Is the same as a limited liability partnership.E.All of these.4. The accounting assumption that requires every business to be accounted for separately from other business entities, including its owner or owners is known as the:A.Objectivity principle.B.Business entity assumption.C.Going-concern assumption.D.Revenue recognition principle.E.Cost principle.5. The rule that requires financial statements to reflect the assumption that the business will continue operating instead of being closed or sold, unless evidence shows that it will not continue, is the: A.Going-concern principle. B.Business entity principle. C.Objectivity principle.D.Cost Principle.E.Monetary unit principle.6. If a parcel of land that was originally acquired for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land should be recorded in the purchaser's books at:A.$95,000.B.$137,000.C.$138,500.D.$140,000.E.$150,000.7. To include the personal assets and transactions of a business's owner in the records and reports of the business would be in conflict with the:A.Objectivity principle.B.Realization principle.C.Business entity principle.D.Going-concern principle.E.Revenue recognition principle.8. The question of when revenue should be recognized on the income statement (according to GAAP) is addressed by the:A.Revenue recognition principle.B.Going-concern principle.C.Objectivity principle.D.Business entity principle.E.Cost principle.9. On December 15, 2007, Myers Legal Services signed a $50,000 contract with a client to provide legal services to the client in 2008. Which accounting principle would require Myers Legal Services to record the legal fees revenue in 2008 and not 2007?A.Monetary unit principleB.Going-concern principleC.Cost principleD.Business entity principleE.Revenue recognition principle10. A partnership:A.Is also called a sole proprietorship.B.Has unlimited liability.C.Has owners called shareholders.D.Has to have a written agreement in order to be legal.E.Is a legal organization separate from its owners.11. According to generally accepted accounting principles, a company's balance sheet should show the company's assets at:A.The cash equivalent value of what was given up or received.B.The current market value of the asset received in all cases.C.The cash paid only, even if something other than cash was given in the exchange.D.The best estimate of a certified internal auditor.E.The objective value to external users.12. Revenue is properly recognized:A.When the customer's order is received.B.Only if the transaction creates an account receivable.C.At the end of the accounting period.D.When cash from a sale is received.E.Upon completion of the sale or when services have been performed and the business obtains the right to collect the sales price.13. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. What is the effect of the sale on the accounting equation for the seller?A.Assets increase $52,000; owner's equity increases $52,000B.Assets increase $85,000; owner's equity increases $85,000C.Assets increase $137,000; owner's equity increases $137,000D.Assets increase $140,000; owner's equity increases $140,000E.None of these14. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, isassessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. At the time of the sale, assume that the seller still owed $30,000 to TrustOne Bank on the land that was purchased for $85,000. Immediately after the sale, the seller paid off the loan to TrustOne Bank. What is the effect of the sale and the payoff of the loan on the accounting equation?A.Assets increase $52,000; owner's equity increases $22,000; liabilities decrease $30,000B.Assets increase $52,000; owner's equity increases $30,000; liabilities decrease $30,000C.Assets increase $22,000; owner's equity increases $52,000; liabilities decrease $30,000D.Assets decrease $30,000; owner's equity decreases $30,000; liabilities decrease $30,000E.Assets decrease $55,000; owner's equity decreases $55,000; liabilities decrease $30,00015. The difference between a company's assets and its liabilities, or net assets is: income.B.Expense.C.Equity.D.Revenue. loss.16. Which of the following statements is true about assets?A.They are economic resources owned or controlled by the business.B.They are expected to provide future benefits to the business.C.They appear on the balance sheet.D.Claims on them can be shared between creditors and owners.E.All of these.17. On June 30 of the current year, the assets and liabilities of Phoenix Phildell are as follows: Cash $20,500; Accounts Receivable, $7,250; Supplies, $650; Equipment, $12,000; Accounts Payable, $9,300. What is the amount of owner's equity as of July 1 of the current year?A.$8,300B.$13,050C.$20,500D.$31,100E.$40,40018. Photometer Company paid off $30,000 of its accounts payable in cash. What would be the effects of this transaction on the accounting equation?A.Assets, $30,000 increase; liabilities, no effect; equity, $30,000 increase.B.Assets, $30,000 decrease; liabilities, $30,000 decrease; equity, no effect.C.Assets, $30,000 decrease; liabilities, $30,000 increase; equity, no effect.D.Assets, no effect; liabilities, $30,000 decrease; equity, $30,000 increase.E.Assets, $30,000 decrease; liabilities, no effect; equity $30,000 decrease.19. How would the accounting equation of Boston Company be affected by the billing of a client for $10,000 of consulting work completed?A.+$10,000 accounts receivable, -$10,000 accounts payable.B.+$10,000 accounts receivable,+$10,000 accounts payable.C.+$10,000 accounts receivable, +$10,000 cash.D.+$10,000 accounts receivable, +$10,000 revenue.E.+$10,000 accounts receivable, -$10,000 revenue.20. Source documents include all of the following except:A.Sales tickets.B.Ledgers.C.Checks.D.Purchase orders.E.Bank statements.21. Which of the following statements is correct?A.When a future expense is paid in advance, the payment is normally recorded in a liability account called Prepaid Expense.B.Promises of future payment are called accounts receivable.C.Increases and decreases in cash are always recorded in the owner's capital account.D.An account called Land is commonly used to record increases and decreases in both the land and buildings owned by a business.E.Accrued liabilities include accounts receivable.22. A written promise to pay a definite sum of money on a specified future date is a(n):A.Unearned revenue.B.Prepaid expense.C.Credit account.D.Note payable.E.Account receivable.23. A collection of all accounts and their balances used by a business is called a:A.Journal.B.Book of original entry.C.General Journal.D.Balance column journal.E.Ledger.24. A list of all accounts and the identification number assigned to each account used by a company is called a:A.Source document.B.Journal.C.Trial balance.D.Chart of accounts.E.General Journal.25. Which of the following statements is incorrect?A.The normal balance of accounts receivable is a debit.B.The normal balance of owner's withdrawals is a debit.C.The normal balance of unearned revenues is a credit.D.The normal balance of an expense account is a credit.E.The normal balance of the owner's capital account is a credit.26. A simple account form widely used in accounting as a tool to understand how debits and credits affect an account balance is called a:A.Withdrawals account.B.Capital account.C.Drawing account.D.T-account.E.Balance column sheet.27. Double-entry accounting is an accounting system:A.That records each transaction twice.B.That records the effects of transactions and other events in at least two accounts with equal debits and credits.C.In which each transaction affects and is recorded in two or more accounts but that could include two debits and no credits.D.That may only be used if T-accounts are used.E.That insures that errors never occur.28. Management Services, Inc. provides services to clients. On May 1, a client prepaid Management Services $60,000 for 6-months services in advance. Management Services' general journal entry to record this transaction will include aA.Debit to Unearned Management Fees for $60,000.B.Credit to Management Fees Earned for $60,000.C.Credit to Cash for $60,000.D.Credit to Unearned Management Fees for $60,000.E.Debit to Management Fees Earned for $60,000.29. On September 30, the Cash account of Value Company had a normal balance of $5,000. During September, the account was debited for a total of $12,200 and credited for a total of $11,500. What was the balance in the Cash account at the beginning of September?A. A $0 balance.B. A $4,300 debit balance.C. A $4,300 credit balance.D. A $5,700 debit balance.E. A $5,700 credit balance.30. On April 30, Holden Company had an Accounts Receivable balance of $18,000. During the month of May, total credits to Accounts Receivable were $52,000 from customer payments. The May 31 Accounts Receivable balance was $13,000. What was the amount of credit sales during May?A.$ 5,000.B.$47,000.C.$52,000.D.$57,000.E.$32,000.31. The following transactions occurred during July:1. Received $900 cash for services provided to a customer during July.2. Received $2,200 cash investment from Barbara Hanson, the owner of the business.3. Received $750 from a customer in partial payment of his account receivable which arose from sales in June.4. Provided services to a customer on credit, $375.5. Borrowed $6,000 from the bank by signing a promissory note.6. Received $1,250 cash from a customer for services to be rendered next year.What was the amount of revenue for July?A. $ 900.B. $ 1,275.C. $ 2,525.D. $ 3,275.E. $11,100.32. During the month of March, Cooley Computer Services made purchases on account totaling $43,500. Also during the month of March, Cooley was paid $8,000 by a customer for services to be provided in the future and paid $36,900 of cash on its accounts payable balance. If the balance in the accounts payable account at the beginning of March was $77,300, what is the balance in accounts payable at the end of March?A.$83,900.B.$91,900.C.$6,600.D.$75,900.E.$4,900.33. On January 1 of the current year, Bob's Lawn Care Service reported owner's capital totaling $122,500. During the current year, total revenues were $96,000 while total expenses were $85,500. Also, during the current year Bob withdrew $20,000 from the company. No other changes in equity occurred during the year. If, on December 31 of the current year, total assets are $196,000, the change in owner's capital during the year was:A. A decrease of $9,500.B.An increase of $9,500.C.An increase of $30,500.D. A decrease of $30,500E.Impossible to determine from the information provided.34. A balance column ledger account is:A.An account entered on the balance sheet.B.An account with debit and credit columns for posting entries and another column for showing the balance of the account after each entry is posted.C.Another name for the withdrawals account.D.An account used to record the transfers of assets from a business to its owner.E. A simple form of account that is widely used in accounting to illustrate the debits and credits required in recording a transaction.35. A general journal is:A. A ledger in which amounts are posted from a balance column account.B.Not required if T-accounts are used.C. A complete record of any transaction and the place from which transaction amounts are posted to the ledger accounts.D.Not necessary in electronic accounting systems.E. A book of final entry because financial statements are prepared from it.36. Which of the following statements is true?A.If the trial balance is in balance, it proves that no errors have been made in recording and posting transactions.B.The trial balance is a book of original entry.C.Another name for the trial balance is the chart of accounts.D.The trial balance is a list of all accounts from the ledger with their balances at a point in time.E.The trial balance is another name for the balance sheet as long as debits balance with credits.37. A trial balance taken at year-end showed total credits exceed total debits by $4,950. This discrepancy could have been caused by:A.An error in the general journal where a $4,950 increase in Accounts Receivable was recorded as an increase in Cash.B. A net income of $4,950.C.The balance of $49,500 in Accounts Payable being entered in the trial balance as $4,950.D.The balance of $5,500 in the Office Equipment account being entered on the trial balance as a debit of $550.E.An error in the general journal where a $4,950 increase in Accounts Payable was recorded as a decrease in Accounts Payable.38. In which of the following situations would the trial balance not balance?A. A $1,000 collection of an account receivable was erroneously posted as a debit to Accounts Receivable and a credit to Cash.B.The purchase of office supplies on account for $3,250 was erroneously recorded in the journal as $2,350 debit to Office Supplies and credit to Accounts Payable.C. A $50 cash receipt for the performance of a service was not recorded at all.D.The purchase of office equipment for $1,200 was posted as a debit to Office Supplies and a credit to Cash for $1,200.E.The cash payment of a $750 account payable was posted as a debit to Accounts Payable and a debit to Cash for $750.39. Interim financial statements refer to financial reports:A.That cover less than one year, usually spanning one, three, or six-month periods.B.That are prepared before any adjustments have been recorded.C.That show the assets above the liabilities and the liabilities above the equity.D.Where revenues are reported on the income statement when cash is received and expenses are reported when cash is paid.E.Where the adjustment process is used to assign revenues to the periods in which they are earned andto match expenses with revenues.40. The length of time covered by a set of periodic financial statements is referred to as the:A.Fiscal cycle.B.Natural business year.C.Accounting period.D.Business cycle.E.Operating cycle.41. Adjusting entries:A.Affect only income statement accounts.B.Affect only balance sheet accounts.C.Affect both income statement and balance sheet accounts.D.Affect only cash flow statement accounts.E.Affect only equity accounts.42. The main purpose of adjusting entries is to:A.Record external transactions and events.B.Record internal transactions and events.C.Recognize assets purchased during the period.D.Recognize debts paid during the period.E.Correct errors.43. Which of the following statements is incorrect?A.Adjustments to prepaid expenses, depreciation, and unearned revenues involve previously recorded assets and liabilities.B.Accrued expenses and accrued revenues involve assets and liabilities that had not previously been recorded.C.Adjusting entries can be used to record both accrued expenses and accrued revenues.D.Prepaid expenses, depreciation, and unearned revenues often require adjusting entries to record the effects of the passage of time.E.Adjusting entries affect the cash account.44. An adjusting entry could be made for each of the following except:A.Prepaid expenses.B.Depreciation.C.Owner withdrawals.D.Unearned revenues.E.Accrued revenues.45. A company made no adjusting entry for accrued and unpaid employee wages of $28,000 on December 31. This oversight would:A.Understate net income by $28,000.B.Overstate net income by $28,000.C.Have no effect on net income.D.Overstate assets by $28,000.E.Understate assets by $28,000.46. If a company mistakenly forgot to record depreciation on office equipment at the end of an accounting period, the financial statements prepared at that time would show:A.Assets overstated and equity understated.B.Assets and equity both understated.C.Assets overstated, net income understated, and equity overstated.D.Assets, net income, and equity understated.E.Assets, net income, and equity overstated.47. If a company failed to make the end-of-period adjustment to remove from the Unearned Management Fees account the amount of management fees that were earned, this omission would cause:A.An overstatement of net income.B.An overstatement of assets.C.An overstatement of liabilities.D.An overstatement of equity.E.An understatement of liabilities.48. When closing entries are made:A.All ledger accounts are closed to start the new accounting period.B.All temporary accounts are closed but not the permanent accounts.C.All real accounts are closed but not the nominal accounts.D.All permanent accounts are closed but not the nominal accounts.E.All balance sheet accounts are closed.49. Which of the following statements is incorrect?A.Permanent accounts is another name for nominal accounts.B.Temporary accounts carry a zero balance at the beginning of each accounting period.C.The Income Summary account is a temporary account.D.Real accounts remain open as long as the asset, liability, or equity items recorded in the accounts continue in existence.E.The closing process applies only to temporary accounts.50. Journal entries recorded at the end of each accounting period to prepare the revenue, expense, and withdrawals accounts for the upcoming period and to update the owner's capital account for the events of the period just finished are referred to as:A.Adjusting entries.B.Closing entries.C.Final entries.D.Work sheet entries.E.Updating entries.51. The recurring steps performed each reporting period, starting with analyzing and recording transactions in the journal and continuing through the post-closing trial balance, is referred to as the:A.Accounting period.B.Operating cycle.C.Accounting cycle.D.Closing cycle.E.Natural business year.52. Which of the following is the usual final step in the accounting cycle?A.Journalizing transactions.B.Preparing an adjusted trial balance.C.Preparing a post-closing trial balance.D.Preparing the financial statements.E.Preparing a work sheet.。

英文版会计学考试题及答案

英文版会计学考试题及答案English Accounting Exam Questions and AnswersQuestion 1: Define the term "Double Entry Bookkeeping" and explain its significance in accounting.Answer 1: Double Entry Bookkeeping is a system of recording financial transactions in which every entry to an account requires a corresponding and opposite entry to a different account. This ensures that the accounting equation (Assets = Liabilities + Owner's Equity) remains in balance. The significance of double entry bookkeeping lies in its ability to provide an accurate and comprehensive picture of a business's financial status, facilitating better decision-making and financial control.Question 2: What is the purpose of a trial balance, and how does it help in the preparation of financial statements?Answer 2: A trial balance is a report that lists the balances of all general ledger accounts at a particular point in time, with debit and credit amounts. It is used to ensure that the debits and credits have been recorded correctly. The trial balance helps in the preparation of financial statements by identifying any discrepancies in the accounting records, which can then be rectified before finalizing the statements.Question 3: Explain the difference between "AccrualAccounting" and "Cash Accounting."Answer 3: Accrual Accounting is a method of accounting where revenues and expenses are recognized when they are earned or incurred, not necessarily when cash is received or paid. This method provides a more accurate representation of a company's financial performance over a period. Cash Accounting, on the other hand, records transactions only when cash is exchanged. It is simpler and is often used by small businesses or those that operate on a cash basis.Question 4: Describe the process of preparing an income statement.Answer 4: Preparing an income statement involves several steps:1. List all the revenues for the period, such as sales and service income.2. Deduct all the expenses incurred to generate those revenues, including cost of goods sold, operating expenses, and taxes.3. Calculate the net income by subtracting total expenses from total revenues.4. The income statement should reflect the company's profitability over a specified period, typically a month, quarter, or year.Question 5: What are the main components of a balance sheet, and how do they relate to each other?Answer 5: The main components of a balance sheet are:1. Assets: What the company owns or controls with future economic benefit, divided into current assets (short-term) and non-current assets (long-term).2. Liabilities: Obligations the company owes to others, classified as current liabilities (due within one year) and long-term liabilities (due after one year).3. Owner's Equity: The residual interest in the assets of the entity after deducting liabilities, also known as shareholders' equity or net assets.These components are related through the fundamental accounting equation: Assets = Liabilities + Owner's Equity.Question 6: How does depreciation affect a company'sfinancial statements?Answer 6: Depreciation is a non-cash accounting method used to allocate the cost of tangible assets over their useful lives. It affects a company's financial statements in the following ways:1. It reduces the book value of the asset on the balance sheet.2. It increases the accumulated depreciation account, whichis a contra-asset account.3. It decreases net income on the income statement, as depreciation is an expense.4. It can lower taxable income, potentially reducing the company's tax liability.Question 7: What is the purpose of the statement of cash flows, and how does it differ from the income statement?Answer 7: The purpose of the statement of cash flows is to provide information about a company's cash receipts and payments during a period, showing how these cash flows affect the company's financial position. It differs from the income statement in that:1. It focuses on cash transactions, not accrual-basis accounting.2. It categorizes cash flows into operating, investing, and financing activities.3. It does not report net income but rather the net change in cash and cash equivalents.Question 8: Explain the concept of "Going Concern" and its importance in financial reporting.Answer 8: The Going Concern concept assumes that a businesswill continue to operate for the foreseeable future, allowing it to realize its assets and discharge its liabilities in the normal course of business. It is important in financial reporting because it underpins the accrual basis of accounting, which assumes that the business will continue to operate and therefore can recognize revenues and expensesover time.Question 9: What are the ethical considerations in accounting, and why are they important?Answer 9: Ethical considerations in accounting include honesty, integrity, objectivity, and confidentiality. Theyare important because they ensure the reliability andcredibility of financial information, which is crucial for stakeholders to make informed decisions. Ethical behavior also helps maintain public trust。

智慧树答案会计学原理(双语)知到课后答案章节测试2022年

第一章1.下列选项中属于近代会计史中的两个里程碑的是()。

Which one of thefollowing items could be considered as the two milestones in the modernaccounting history ?( ).答案:帕乔利复式簿记著作的出版和会计职业的出现The publication of Pacioli’s double-entry bookkeeping and the emergence of the accounting profession2.通过归集一定计算对象上的全部费用,借以确定各该对象的总成本和单位成本的一种专门会计方法是()。

A special accounting method fordetermining the total cost and unit cost of each object by aggregating thetotal expenses of a certain calculation object is ( )答案:成本计算Costcalculation3.会计具有双重属性,即()。

Accounting has double attributes, namely ( ).答案:技术性与社会性Technicality and sociality4.关于会计的产生与发展,下列说法中正确的有()。

The following correctstatements on the origin and development of accounting include ( ).答案:经济越发展,会计越重要The faster economy develops, the more importantaccounting is.;会计是生产活动发展到一定阶段的产物Accounting is theproduct of the development of production activities to a certain stage.;会计是为适应生产活动发展的需要而产生的Accounting is generated to meet theneeds of the development of production activities.;会计从产生到现在经历了一个漫长的发展历程 Accounting has experienced a long journey ofdevelopment since its inception.5.下列关于会计作用的说法正确的有()。

会计学原理23版 英文练习WildFAP23eCh04EPPT

9,000

9,000

Totals

$ 146,000 $ 146,000

58,000

95,000

88,000

51,000

Net Income

37,000

37,000

Totals

$ 95,000 $ 95,000 $

88,000 $

88,000

Exercise 4-2 page 173 Alternate

Exercise 4-3 page 173

Use the following information from the Adjustments columns of a 10-column work sheet to prepare the necessary adjusting journal entries (a) through (e).

Prepaid insurance

To record expired insurance.

(b)

Office supplies expense

Office supplies

To record consumed supplies.

(c)

Depreciation expense - Office equip.

Copyright © by McGraw-Hill Education, Inc. All rights reserved.

Exercise 4-2 page 173

The Adjusted Trial Balance for Planta Company follows. Complete the work sheet by extending the account balances into the appropriate financial statement columns and by entering the amount of net income for the reporting period.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。