中兴新云 财务共享中心的评价体系

财务共享服务中心能力评价体系的构建与应用

财务共享服务中心能力评价体系的构建与应用财务共享服务中心的建立使企业的战略规划、信息技术等内部环境发生了很大的变化,但针对财务共享服务中心本身的能力进行评估的模型和体系较为鲜见。

依据相关的标准对财务共享服务中心的能力进行评估,并据此优化、提升其运作效率的研究尤显重要。

本文借用成熟度模型(CMM)的思想,以发展质量、发展能力、成本以及适宜度四个维度对战略规划、流程管理、信息技术、员工管理四个层面进行了细分,构建了财务共享服务中心能力评价体系。

该体系由三个层级指标构成,其中包含四个基本的一级评估指标,十六个二级评估指标,三十八个三级评估指标,通过层次分析法确定各个指标的权重。

本文以S公司为例,用构建的指标体系对其财务共享服务中心进行能力评估,利用模糊综合评价法将定性指标转化成定量指标,最终得出S公司财务共享中心的成熟度值为3.6755,所处的成熟度等级为"已定义级",针对该公司财务共享中

心能力所处级别提出了能力提高建议。

财务共享服务中心的绩效管理及评估

然而,建立和运营一个成功的FSSC并非易事,需要企业在流程设计、技术应 用、人员管理等多个方面进行全面的规划和实施。此外,随着企业环境和业务需 求的变化,FSSC也需要不断优化和调整以适应新的挑战和机遇。

总的来说,财务共享服务中心对于提高企业绩效具有积极的影响。在日益激 烈的市场竞争中,企业应充分认识到FSSC的重要性并将其纳入战略规划中,以实 现持续的竞争优势和价值最大化。

2、员工满意度:员工的工作状态、福利待遇以及培训和发展机会等方面的 评估。

3、质量管理:对财务共享服务中心输出的质量进行评估,如数据的准确性、 完整性等。

参考内容

基本内容

随着全球化和信息化的发展,财务共享服务中心(FSSC)逐渐成为企业运营 的重要部分。FSSC通过集中处理和标准化企业的财务流程,帮助企业提高效率、 降低成本,并最终影响企业的整体绩效。本次演示将探讨财务共享服务中心对企 业绩效的影响。

二、财务共享服务中心对企业绩 效的影响

1、提高效率:通过集中处理和标准化财务流程,FSSC能够显著提高企业的 财务处理效率。这不仅降低了财务错误和舞弊的风险,还为企业提供了更多时间 和资源来专注于核心业务。

2、降低成本:FSSC通过减少人力成本和简化财务流程,能够帮助企业降低 运营成本。这为企业提供了更多的机会去投资创新和市场拓展,从而扩大企业的 业务范围和市场份额。

参考内容二

基本内容

随着企业规模的扩大和业务范围的拓展,财务共享服务中心作为一种新型的 财务管理模式,逐渐受到越来越多企业的和应用。其中,Z公司作为一家全球知 名的企业,很早就建立了财务共享服务中心,并对其进行了不断的优化和完善。 本次演示旨在探讨Z公司财务共享服务中心绩效评价相关问题,以期为企业优化 财务管理提供参考。

财务共享服务中心财务能力成熟度评价体系研究

财务共享服务中心财务能力成熟度评价体系研究摘要:本文旨在通过对财务共享服务中心(以下简称“共享服务中心”)的财务能力成熟度评价体系进行研究,为企业提升共享服务中心的财务水平提供理论基础和实践经验。

本文分别从共享服务中心的角度和企业的角度来分析财务能力成熟度,并对共享服务中心的财务能力成熟度评价体系进行构建和优化。

首先,本文通过对共享服务中心的角度来分析财务能力成熟度。

在这些角度中,本文选定了共享服务中心的财务目标、财务流程、财务人员和财务系统等四个角度。

通过对这些角度的深入研究,本文得出了“共享服务中心的财务能力成熟度评价体系”的架构和指标,为企业提升共享服务中心的财务水平提供了理论基础。

其次,本文通过对企业的角度来分析财务能力成熟度。

在这些角度中,本文选定了企业的战略目标、财务战略、组织结构和财务技术等四个角度。

通过对这些角度的深入研究,本文得出了“共享服务中心财务能力提升的策略与方法”的实践经验,为企业提升共享服务中心的财务水平提供了实践指导。

最后,本文重点针对共享服务中心的财务流程和财务人员等两个方面,进行了实践案例分析。

通过具体案例分析,本文进一步验证了“共享服务中心的财务能力成熟度评价体系”的指标合理性,并为企业提升共享服务中心的财务水平提供了具体实践案例。

关键词:财务共享服务中心;财务能力成熟度;评价体系;财务流程;财务人员;实践案例。

Abstract:This paper aims to study the financial capability maturity evaluation system of the financial shared service center (hereinafter referred to as "shared service center"), and provide theoretical basis and practical experience for enterprises to improve the financial level of the shared service center. This paper analyzes the financial capability maturity from both the perspective of the shared service center and the enterprise, and constructs and optimizes the financial capability maturity evaluation system of the shared service center.Firstly, this paper analyzes the financial capability maturity from the perspective of the shared service center. Among these perspectives, this paper selects the financial targets, financial processes, financial personnel, and financial systems of the shared service center. Through in-depth research on theseperspectives, this paper draws the framework and indicators of the "financial capability maturity evaluation system of the shared service center", providing a theoretical basis for enterprises to improve the financial level of the shared service center.Secondly, this paper analyzes the financial capability maturity from the perspective of the enterprise. Among these perspectives, this paper selects the strategic objectives, financial strategy, organizational structure and financial technology of the enterprise. Through in-depth research on these perspectives, this paper draws the practical experience of the "strategies and methods for improving the financial capability of the shared service center", providing practical guidance for enterprises to improve the financial level of the shared service center.Finally, this paper focuses on the financial processes and financial personnel of the shared service center, and conducts a practical case analysis. Through specific case analysis, this paper further verifies the rationality of the indicators of the "financial capability maturity evaluation system of the shared service center", and provides concrete practical cases for enterprises to improve the financial level of theshared service center.Keywords: financial shared service center; financial capability maturity; evaluation system; financial processes; financial personnel; practical casesCase Analysis of Improving Financial Capability Maturity of Shared Service CenterIntroductionThe establishment of a shared service center is a strategic move for enterprises to improve operational efficiency and reduce costs. The financial shared service center is an important part of the shared service center, which undertakes financial management functions of various departments within an enterprise. The financial capability maturity of the shared service center directly affects the quality of financial management within the enterprise. Therefore, it is necessary to evaluate and improve the financial capability maturity of the shared service center.The Financial Capability Maturity Evaluation System of the Shared Service CenterThe financial capability maturity evaluation system ofthe shared service center includes four dimensions of financial processes, financial personnel, financial systems, and financial governance. Each dimension has five levels of maturity, from the initial phase to the optimized phase. The maturity level of each dimension of the shared service center can be determined based on indicators.1. Financial processes dimension: The financial processes dimension includes the finance and accounting processes of the shared service center. The indicators for evaluating the maturity level of this dimension are the standardized degree of financial processes, the degree of automation of financial processes, the efficiency of financial processes, the accuracy of financial processes, and the compliance of financial processes.2. Financial personnel dimension: The financial personnel dimension includes the number, quality, and allocation of financial personnel in the shared service center. The indicators for evaluating the maturity level of this dimension are the number of financial personnel, the professional competence of financial personnel, the allocation of financial personnel, the training and development of financial personnel, and the sharing of knowledge and skills.3. Financial systems dimension: The financial systems dimension includes the financial management system and financial reporting system of the shared service center. The indicators for evaluating the maturitylevel of this dimension are the integration offinancial systems, the standardization of financial systems, the continuity of financial systems, the security of financial systems, and the compatibilityof financial systems.4. Financial governance dimension: The financial governance dimension includes the financial governance structure, policies, and procedures of the shared service center. The indicators for evaluating the maturity level of this dimension are the effectiveness of financial governance, the compliance of financial governance, the transparency of financial governance, the risk management capability of financial governance, and the innovation capability of financial governance.Case AnalysisA company established a financial shared servicecenter to centralize financial management, reduce costs, and improve financial efficiency. However,after the shared service center was established, itwas found that the financial management level was not improved as expected, and there were still many problems in financial management. Therefore, the company decided to evaluate the maturity level of its financial shared service center and improve it basedon the results of evaluation.1. Evaluation of the maturity level of the financial processes dimension: The evaluation results showedthat the financial processes of the shared service center were still in the initial phase, and the degree of standardization and automation was low, the efficiency was low, and the accuracy and compliance were not up to standard. Therefore, the companydecided to improve the standardization of financial processes, increase the degree of automation, optimize the efficiency of financial processes, and enhance the accuracy and compliance of financial processes.2. Evaluation of the maturity level of the financial personnel dimension: The evaluation results showedthat the number of financial personnel wasinsufficient, the professional competence was not high, the allocation was not reasonable, and the trainingand development was not sufficient. Therefore, the company decided to increase the number of financial personnel, improve the professional competence offinancial personnel through training and assessment, optimize the allocation of financial personnel, and enhance the sharing of knowledge and skills among financial personnel.3. Evaluation of the maturity level of the financial systems dimension: The evaluation results showed that the financial management system and financialreporting system of the shared service center were not fully integrated, standardized, or continuous, and the security and compatibility were not high. Therefore, the company decided to optimize the integration and standardization of financial systems, ensure the continuity, security, and compatibility of financial systems, and enhance the scalability and flexibilityof financial systems.4. Evaluation of the maturity level of the financial governance dimension: The evaluation results showedthat the financial governance structure, policies, and procedures of the shared service center were not effective, compliant, transparent, or capable of risk management and innovation. Therefore, the company decided to optimize the financial governance structure, establish effective and compliant policies and procedures, enhance the transparency of financial governance, strengthen the risk management capability,and encourage innovation in financial governance. ConclusionThe financial capability maturity evaluation system of the shared service center is an effective tool for evaluating and improving the financial managementlevel of an enterprise. The practical case analysis shows that the indicators of the evaluation system are rational and applicable, and can provide specific guidance for enterprises to improve the financial capability maturity of their shared service centers. Improving the financial capability maturity of the shared service center is not only beneficial to the internal financial management of the enterprise, but also conducive to the long-term development of the enterpriseIn addition to the financial capability maturity evaluation system for shared service centers, there are other factors that enterprises should consider to maximize the effectiveness of their shared service centers. One important factor is the selection of appropriate technology systems and platforms to support their shared services. Implementing advanced technology systems such as robotic process automation (RPA) and artificial intelligence () can help automaterepetitive tasks and improve overall efficiency within shared service centers.Furthermore, establishing strong communication channels and effective collaboration across departments is critical for the success of shared service centers. This can be achieved through regular meetings, shared performance metrics, and establishing clear roles and responsibilities for each department.Lastly, companies must also consider the potential impact of cultural differences and ensure that their shared service centers align with the overall company culture. Providing regular training and development opportunities for shared service center employees can also help improve staff morale and retention.In conclusion, the implementation of a well-designed financial capability maturity evaluation system can greatly benefit shared service centers and their parent companies. However, the full potential of shared service centers can only be realized through the integration of appropriate technology systems, effective communication and collaboration, and consideration of cultural differences. By considering these factors, enterprises can continue to improve the effectiveness and efficiency of their shared servicecenters, ultimately leading to increased profitability and successIn addition to the factors mentioned above, there are several other key considerations that can impact the success of shared service centers. These include:1. Standardization: Standardizing processes and procedures across all business units can help to ensure consistency and reduce duplication of effort. This can be achieved through the use of standard operating procedures (SOPs), process maps, and other tools.2. Governance: Shared service centers must have clear governance structures in place to ensure accountability, transparency, and effective decision-making. This includes defining roles and responsibilities, establishing performance metrics, and setting up reporting mechanisms.3. Talent management: Shared service centers rely heavily on skilled and trained staff to operate effectively. As such, it is important to have robust talent management practices in place, including recruitment, training and development, performance management, and succession planning.4. Flexibility: Shared service centers need to be able to adapt to changing business needs, technological advancements, and market conditions. This requires a culture of continuous improvement, along with theability to quickly implement changes to processes, systems, and staffing.By taking a holistic approach to the design and management of shared service centers, enterprises can realize significant benefits, including cost savings, improved efficiency, and enhanced customer service. However, this requires a long-term commitment to ongoing improvement and a willingness to invest in the necessary resources and technologies. With the right strategies in place, shared service centers can become a key driver of an enterprise's successIn conclusion, shared service centers offer apromising solution for enterprises seeking to streamline their administrative processes and reduce costs. However, to maximize the benefits of these centers, companies must adopt a holistic approach that focuses on optimizing processes, systems, and staffing. This requires a long-term commitment to ongoing improvement and investment in the necessary resources and technologies. By following these strategies,shared service centers can become a vital component of an enterprise's success。

N公司财务共享服务中心绩效评价体系优化

N公司财务共享服务中心绩效评价体系优化为了优化N公司财务共享服务中心的绩效评价体系,我们需要制定一个科学合理的评价指标体系,建立有效的绩效管理机制,以确保评价结果准确客观,激发员工积极性和创造力,推动企业发展。

一、绩效评价指标体系的构建1.岗位职责:根据岗位职责制定相关优化指标,确保职业发展路径清晰,并建立任务书、工作计划和绩效考核方案。

2.工作效率:涉及工作量、工作时间、准确性、及时性等,可以通过考核工作质量与效率的比例来考评员工的工作效率。

3.服务质量:衡量服务质量主要从客户满意度、服务速度和服务格局等方面来评估。

4.团队合作:团队合作是公司成功的重要因素之一,建立一套量化的评价体系可以使得团队合作更加高效,包括考核每个员工对团队目标的贡献、建立良好的内部信任和沟通等。

5.个人素质:考评员工的个人素质主要包括专业水平、沟通能力、人际关系等方面。

二、绩效管理机制建立1.设立绩效评价委员会:由高管、部门经理和员工代表等组成,负责制定评价标准、审核评估结果,并根据结果提出奖励或改进意见。

2.设立奖惩机制:推行绩效奖励机制,给予高绩效员工相应的荣誉或奖金;同时,对绩效表现不佳的员工予以制定培训计划和改进建议。

3.定期绩效评估:定期开展全员绩效评估,对员工的贡献和表现进行综合评估。

在评价过程中,要确保评价对话质量到位、互动强度高,从而实现绩效评价的客观性。

4.工作目标分解:将公司战略目标和部门目标分解为每个员工的工作任务,确保员工能够清晰了解自己的工作职责,进而推动企业实现目标。

5.员工反馈机制:建立员工反馈机制,可以收集到员工对绩效评价的反馈和建议,及时处理员工提出的问题和解决员工的潜在不满和矛盾。

三、总结。

中兴通信集团财务共享服务中心建设问题

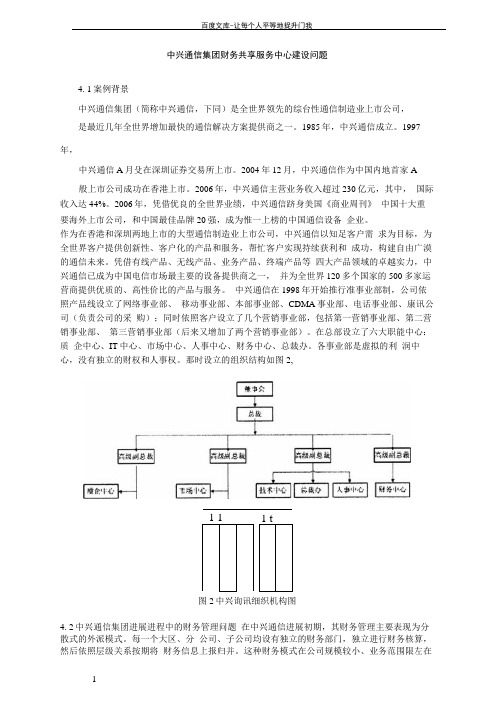

中兴通信集团财务共享服务中心建设问题4. 1案例背景中兴通信集团(简称中兴通信,下同)是全世界领先的综台性通信制造业上市公司,是最近几年全世界增加最快的通信解决方案提供商之一。

1985年,中兴通信成立。

1997年,中兴通信A月殳在深圳证券交易所上市。

2004年12月,中兴通信作为中国内地首家A 般上市公司成功在香港上市。

2006年,中兴通信主营业务收入超过230亿元,其中,国际收入达44%。

2006年,凭借优良的全世界业绩,中兴通信跻身美国《商业周刊》中国十大重要海外上市公司,和中国最佳品牌20强,成为惟一上榜的中国通信设备企业。

作为在香港和深圳两地上市的大型通信制造业上市公司,中兴通信以知足客户需求为目标,为全世界客户提供创新性、客户化的产品和服务,帮忙客户实现持续获利和成功,构建自由广漠的通信未来。

凭借有线产品、无线产品、业务产品、终端产品等四大产品领域的卓越实力,中兴通信已成为中国电信市场最主要的设备提供商之一,并为全世界120多个国家的500多家运营商提供优质的、高性价比的产品与服务。

中兴通信在1998年开始推行准事业部制,公司依照产品线设立了网络事业部、移动事业部、本部事业部、CDMA事业部、电话事业部、康讯公司(负责公司的采购);同时依照客户设立了几个营销事业部,包括第一营销事业部、第二营销事业部、第三营销事业部(后来又增加了两个营销事业部)。

在总部设立了六大职能中心:质企中心、IT中心、市场中心、人事中心、财务中心、总裁办。

各事业部是虚拟的利润中心,没有独立的财权和人事权。

那时设立的组织结构如图2,图2中兴询讯细织机构图4. 2中兴通信集团进展进程中的财务管理问题在中兴通信进展初期,其财务管理主要表现为分散式的外派模式。

每一个大区、分公司、子公司均设有独立的财务部门,独立进行财务核算,然后依照层级关系按期将财务信息上报归并。

这种财务模式在公司规模较小、业务范围限左在国内时期发挥了专门大作用。

N公司财务共享服务中心绩效评价体系优化

N公司财务共享服务中心绩效评价体系优化N公司财务共享服务中心是为了提高公司财务流程效率和降低成本而设立的,对于该中心的绩效评价体系的优化、完善和有效运营对于公司的发展至关重要。

为了实现这一目标,我们提出了以下优化方案:一、明确绩效评价指标:绩效评价指标应该明确、具体且与中心的职能和目标相符。

我们建议将绩效评价指标分为以下几个方面:1. 工作质量和效率:评估员工完成工作的质量和时间效率,包括准确性、及时性和规范性等方面。

2. 服务质量:评估员工的客户服务能力和满意度,包括沟通技巧、响应时间和解决问题的能力等方面。

3. 团队合作能力:评估员工在团队合作中的贡献和表现,包括与他人的合作和协调能力以及分工合作的能力等方面。

4. 自我发展能力:评估员工的学习能力和自我成长的能力,包括自我学习、专业知识更新和职业目标规划等方面。

5. 创新和改进能力:评估员工对工作流程的创新和改进能力,包括提出新的解决方案、流程改进和质量提升等方面。

二、设立绩效评价周期和频率:绩效评价周期和频率的合理安排对于绩效评价的有效性和员工的工作动力有着重要的影响。

我们建议将绩效评价周期设置为一年,并且在每个季度进行绩效进展的跟踪和沟通。

这样可以保证评价结果的全面性和准确性,同时也可以及时调整和指导员工的工作方向。

三、建立绩效评价管理制度:建立绩效评价管理制度是绩效评价体系的保障。

该制度应包括绩效评价流程、评价标准、评价材料和评价权责等方面的规定。

应明确评价结果的权威性和公正性,建立有效的沟通渠道和反馈机制,确保员工对评价结果有较好的理解和接受,同时可以提供改进和提升的机会。

四、定期进行绩效评价结果的跟踪和分析:绩效评价结果的跟踪和分析可以帮助中心管理层了解员工绩效的整体情况和趋势,及时发现问题并采取相应的措施进行改进。

还可以为人力资源管理提供数据支持,帮助制定有针对性的培训和激励计划。

五、积极利用绩效评价结果:绩效评价结果不仅仅是对员工工作的评估,更是对中心管理的反馈和指导。

财务共享服务中心的内部控制研究——以中兴通讯FSSC为例

财务共享服务中心的内部控制研究——以中兴通讯FSSC为例财务共享服务中心的内部控制研究——以中兴通讯FSSC为例近年来,随着财务共享服务中心(Financial Shared Service Center,FSSC)在企业中的应用越来越广泛,其在提高财务管理效率、降低成本、优化内部控制等方面的优势逐渐被认可。

本文将以中国通信设备制造巨头中兴通讯的FSSC为例,探讨FSSC内部控制的实践与研究。

一、中兴通讯FSSC概述中兴通讯于1997年成立,自成立以来,其持续致力于通信技术的研发与创新,成为全球领先的通信设备供应商之一。

为了应对公司不断扩大的业务规模和快速增长的财务需求,中兴通讯于2011年成立了FSSC,旨在集中公司内部多个子系统的财务职能,通过标准化与自动化流程来提高财务管理与服务效率。

二、中兴通讯FSSC的内部控制框架中兴通讯FSSC建立了完善的内部控制框架,确保财务运营的安全性、可靠性和有效性。

其内部控制框架主要包括控制环境、风险评估、控制活动、信息与沟通和监控等五个要素。

1. 控制环境中兴通讯FSSC高层管理层树立了“严格、自律、开放、协作”的内控文化,明确了管理层对内部控制的重视和支持。

该文化鼓励员工自觉遵守财务制度、规章制度,并提供必要的培训和意识提高活动。

2. 风险评估中兴通讯FSSC建立了风险评估制度,对可能影响到财务运营的各类风险进行评估和管理。

该制度通过制定并实施各类风险控制措施,及时应对可能出现的风险,保障财务运营的正常进行。

3. 控制活动中兴通讯FSSC通过建立标准化流程和规范操作手册,明确了财务流程的具体操作和责任,确保了公司内部财务管理的一致性和及时性。

同时,中兴通讯FSSC采用信息化系统对财务流程进行管理,并设置了各类控制点,确保关键环节的合规性和准确性。

4. 信息与沟通中兴通讯FSSC建立了财务信息的收集、分析和报告机制,及时提供准确可靠的财务信息给公司决策层和其他部门。

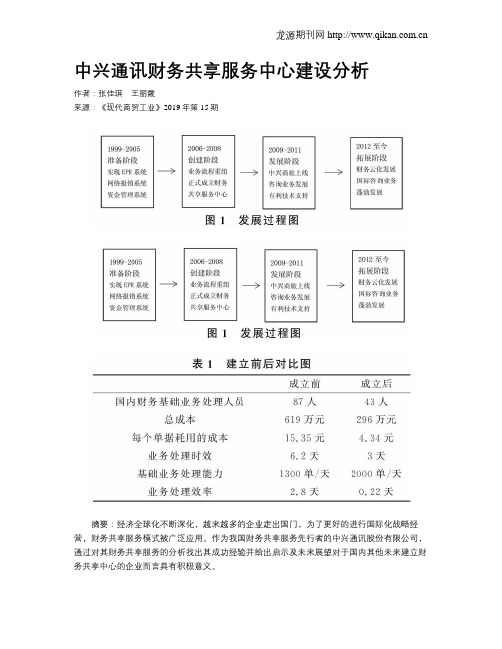

中兴通讯财务共享服务中心建设分析

中兴通讯财务共享服务中心建设分析作者:张佳琪王丽霞来源:《现代商贸工业》2019年第15期摘要:经济全球化不断深化,越来越多的企业走出国门,为了更好的进行国际化战略经营,财务共享服务模式被广泛应用。

作为我国财务共享服务先行者的中兴通讯股份有限公司,通过对其财务共享服务的分析找出其成功经验并给出启示及未来展望对于国内其他未来建立财务共享中心的企业而言具有积极意义。

关键词:财务共享;建设过程;效果;指导中图分类号:F27文献标识码:Adoi:10.19311/ki.1672-3198.2019.15.0200引言2006年,中兴通讯股份有限公司首次进行了集团公司财务共享模式的改革,自行建立了中国本土企业的第一家财务共享服务中心,于2016年成功完成了集团公司的财务共享模式变革,为世界107个分支机构、将近8萬名的企业员工提供了全方位的便捷的财务服务。

中国企业的共享服务中心建设从理论与实践的借鉴上仅仅来自两家企业:IBM,还有中兴通讯。

1财务共享与财务集中的区别财务共享的概念常常与财务集中的概念混淆,两者在初期的表现形式上确实有相似的地方,但经过发展,两者最终会走向不同的方向。

可以从四个方面对其进行区分:(1)本质不同,财务共享的本质是一种商业经营行为,最终会实现高度的市场化,而财务集中是集团内部的一种管理模式。

(2)性质不同,财务共享的信息集中是一种具有流程化的行为,具有严格的要求,而财务集中不具有流程性,仅是一种位移的变动。

(3)地点不同,财务共享可以在任何地点,不一定非要在集团总部或集团中的任一公司内部,而财务集中常常是在集团总部中。

(4)竞争环境差异,财务共享由其商业本质而存在一种竞争环境中,当一个集团的内部共享服务中心要与外部市场中一些外包商提供的服务竞争时,才是真正的共享。

仅仅存在集团内部,以一种职能式的服务存在的没有存在与市场竞争的则趋近于财务集中。

2中兴财务共享服务中心发展过程中兴通讯在1999年实施了EPR系统,完成了独立的网络报销系统,并在集团内部安装了首台ATM机,达到了银行与企业的直接连接。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

中兴新云财务共享中心评价体系

一、背景介绍

中兴通讯是我国领先的通信设备制造商,成立于1985年,总部位于深圳。

作为全球通信设备制造商之一,中兴通讯致力于推动行业创新,

提供高质量、高性能的产品和解决方案。

中兴新云财务共享中心成立

于2016年,旨在为中兴通讯旗下的各个业务单元提供财务共享服务,包括会计、财务分析、风险管理等领域。

在日常运营中,中兴新云财

务共享中心非常重视评价体系的建设和完善,以确保服务质量和业务

效率。

二、评价体系的建设目的

1.标准化服务质量

中兴新云财务共享中心的评价体系旨在建立一套标准化的服务质量评

价方法,通过量化和客观的指标,评估财务共享中心提供的服务质量,确保服务水平达到一定的标准。

2.监督和激励员工表现

评价体系可以用来监督和评估财务共享中心的员工表现,确保员工履

行职责,提升工作效率,同时也是一种激励方式,能够激发员工的工

作动力,提高员工的工作积极性和主动性。

3.指导业务发展

通过对业务数据和指标进行分析,评价体系可以为业务决策和发展提

供指导意见,帮助财务共享中心领导层更好地把握业务发展方向和重点,推动财务共享中心服务的持续改进和提升。

三、评价体系的设计要素

1.明确评价指标

中兴新云财务共享中心的评价体系中,包含了一系列明确的评价指标,涵盖了服务质量、工作效率、员工表现等多个方面,确保全面客观地

评价财务共享中心的服务表现和员工绩效。

2.定期评价制度

评价体系建立了定期的评价制度,每月、每季度甚至每年进行一次全

面的参评,对财务共享中心的服务质量和员工绩效进行全面评估和激励,有利于发现问题和弱点,及时进行改进和提升。

3.客观评价标准

评价体系中的评价标准以客观、量化的形式呈现,如KPI指标、工作

效率指标、服务满意度等,能够客观地量化财务共享中心的服务表现,减少主观因素的干扰,确保评价结果的客观性和准确性。

四、评价体系的实施

1.数据收集和分析

中兴新云财务共享中心通过各种数据收集手段,包括业务系统、员工

绩效数据、客户满意度调查等,对财务共享中心的服务表现和员工绩

效进行数据收集和整理,通过专业工具对数据进行分析和计算,形成

评价结果。

2.评价结果反馈

评价结果已成交予财务共享中心的领导层和员工,目的是及时反馈评

价结果,发现问题,指导员工改进和提升,同时也可以作为员工晋升

和薪酬激励的依据,提高员工的工作积极性和主动性。

3.改进和持续优化

中兴新云财务共享中心将评价结果作为改进和持续优化的重要依据,

通过评价结果发现问题和不足,制定改进措施,推动财务共享中心服

务的不断改进和提升,确保最终达到客户满意度和业务效率的最优化。

五、评价体系的意义与价值

中兴新云财务共享中心的评价体系的建立和实施,不仅是对财务共享

中心服务质量和员工表现的一种把控手段,更是一种对业务发展、员

工激励以及服务持续改进的保障。

评价体系为财务共享中心的领导层

提供了全面客观的数据支持,推动业务决策和发展,对员工的工作表

现进行监督和激励,对财务共享中心的服务质量和效率进行持续优化,确保为中兴通讯各个业务单元提供高质量、高效率的财务共享服务,

为中兴通讯的持续发展和业务创新提供有力的支持。

六、结语

中兴新云财务共享中心的评价体系的建立和实施,是对服务质量和员工绩效的一种全面、客观的监督和管理手段,也是对业务发展和持续优化的一种有力支持。

通过评价体系的建设和实施,财务共享中心能够及时发现问题和不足,开展改进和优化,确保为中兴通讯提供高质量、高效率的财务共享服务,为公司的发展和创新提供有力支持。

评价体系的建设和实施也为财务共享中心的员工提供了一个公平公正的工作环境,能够激发员工的工作积极性和主动性,实现个人价值和公司价值的双赢。

中兴新云财务共享中心的评价体系的建设和实施,将继续为公司的发展和员工的成长提供有力支持。

以上就是中兴新云财务共享中心的评价体系的相关内容,谢谢!。