西方财务会计 chapter1

西方会计学第一章

Relevant Information

Affects the decision of its users.

Reliable Information

Is trusted by users.

Comparable Information

McGraw-Hill/Irwin

Is helpful in contrasting organizations.

Accountants and their staff who provide services on a fee basis are said to be employed in public accounting.

McGraw-Hill/Irwin

Slide 11

C4

ETHICS - A KEY CONCEPT

© 2009 The McGraw-Hill Companies, Inc., All Rights Reserved

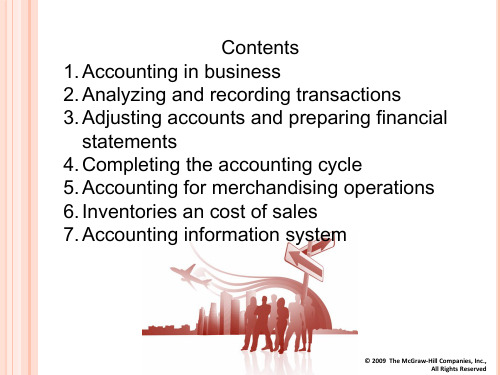

ACCOUNTING IN BUSINESS

Chapter 1

© 2009 The McGraw-Hill Companies, Inc., All Rights Reserved

plus cash value of items received.

Cost Principle

Accounting information is based on actual cost. Actual cost is considered objective.

Matching Principle

•Underwriters

•Human services

•Planners

•Litigation support

西方财务会计PPT课件

二、在不同条件下商品购入和商品销售的帐务处理 (1)购货与销货的记录:购货方须运用“购货”帐户,销货方需运用

“销货”帐户; (2)退货及折让货款的记录:购货方须运用“购货退还及折让”,销

货方需运用“销货退回及折让”帐户; (3)运费的记录:不同条件下,有这不同的帐务处理方法; (4)付款和收款的记录:应用“应付帐款”、“应收帐款”、“现金”

第五章 商业帐款与商业票据 要求:

熟练地掌握应收与应付帐款、应收与应付 票据的帐务处理。 重点: 1、应收帐款坏帐损失的计提; 2、应收、应付票据及其贴现的帐务处理。

一、商业帐款的帐务处理

在第三章论述商品购销业务的帐务处理程序时,已同时说明了应收、应 付帐款的帐务处理程序,因此,在本章中,只是对应收帐款帐务处 理中的特殊问题加以论述,包括坏帐损失、分期收款销货。

第六章 存货 要求:

熟练地掌握存货发出的计价方法和期末存 货计价中成本与市价孰低规则的应用。 重点: 1、各种存货发出计价方法及其适用性; 2、成本与市价孰低规则的应用。

一、存货帐务处理的基本程序 1、存货的定义及范围。 2、存货成本的构成。 3、存货内部控制的基本原则。 4、定期盘存制与永续盘存制下存货的帐务处理: 定期盘存制和永续盘存制含义;定期盘存制与永续盘存制下购货和销货

2、资产负债表的会计恒等式 资产=负债+业主权益 收益表的关系式:收益—费用=净收益

因为业主权益的变动时有以下两个所引起的: (1)投资与派得;(2)企业的净收益, 所以,对会计恒等式中业主权益这一要素也可以表达成:

业主权益=业主出资+净收益-业主派得

四、财务报表的基本形式

资产负债表、收益表、业主权益表三个报表实际上都是上述三个关系 式的展开。

西方财务会计1-PPT文档资料29页

Page 14

Types of Accounting Information

1Financial Accounting

- Provides data for external users

- Is required by SEC/FASB - Is subject to GAAP - Must generate accurate

and timely data - Emphasizes the past - Look at the business as a

whole - Primarily stands by itself

2Management Accounting

- Provides data for internal users - Is not mandated by SEC/FASB - Is not subject to GAAP - Emphasizes relevance and

Eyeing the man in the balloon the passer by says: "You are in a downed balloon in a farmer's field.”

"You must be an accountant, sir," replied the balloon's unhappy resident.

- Provides data for external users

- Is required by SEC/FASB - Is subject to GAAP - Must generate accurate

and timely data - Emphasizes the past - Look at the business as a

斯科特财务会计理论PPT课件第一章

– Lack of transparency of asset-backed securities – Excessive risk encouraged by off-balance-sheet activities – Excessive risk encouraged by manager compensation

Copyright © 2012 Pearson Canada Inc

1 - 15

1.10 The Fundamental Problem Of Financial Accounting Theory

• The best measure of net income to control adverse selection not the same as the best measure to motivate manager performance

– Fair value accounting for financial instruments

• Complicated by liquidity pricing

– High leverage of financial institutions

• Off-balance sheet financing liabilities • Use of expected loss notes to avoid consolidation of

• Response of standard setters

– Stopgap measures in response to government pressure

• Fair value accounting guidance during liquidity pricing • Increased use of internal estimates (value-in-use) • Increased use of cost-based valuation

西方财务会计复习资料全

《西方财务会计》复习资料一般期末考试题型:一、判断题二、单项选择题三、多项选择题四、论述题五、业务题各章要求重点掌握的容:第一章:概论1.财务会计与管理会计的区别2.会计信息的质量特征3.各会计假设与会计原则(理解并能应用,不要求背诵)第二章:会计循环1.资产及其特征2.会计等式3.借贷记账法、日记账与分类账的应用4.试算表5.第三节应计制与账项调整6.会计循环的各个步骤第三章:商品购销业务1.购销业务的处理,(1)退货与折让货款(2)商业折扣与现金折扣(总价法与净价法)(3)运费2.销货成本的确定第四章:现金收支业务1.现金的围2.现金部控制的方法3.零用现金的会计处理4.银行余额的调节第五章:应收账款与应收票据1.第二节:应收账款坏账的处理2.第四节:应收票据第六章:存货1.第一节存货的种类和围2.第二节存货数量的确定3.第三节存货成本的确定(不包括成本与市价孰低法)第七章:对外投资1.投资的分类与计价2.债务性证券投资的会计处理(交易性和可供出售证券)3.权益性证券投资的会计处理(交易性和可供出售证券)4.成本法与权益法(看课件容)第八章:厂场资产、自然资源和无形资产1.厂场资产的特点2.长期资产的计价3.第二节厂场资产取得的会计处理(不包括非货币性交易)4.第三节厂场资产折旧及折旧的计算5.厂场资产的处置6.无形资产及其特征第九章:流动负债1.负债及其特点2.第三节金额确定的流动负债3.第六节或有负债第十章:长期负债1.第一节长期负债的特点2.公司债券的计价及其帐务处理(涉及债券发行、折价和溢价摊销、赎回等,以直线摊销法为主)第十一章:股东权益全章容重要(涉及股票发行、库藏股、股利等)第十二章:合伙企业业主权益(不要求)第十三章:财务报表1.财务报表的种类2.收益表及其作用3.资产负债表及其作用4.股东权益表及其作用5.第四节现金流量表(要求理解,掌握方法,不考具体编表)第十四章:财务报表分析1.第一节财务报表分析的目的和方法2.如何进行横向分析和纵向分析3.第三节比率分析法4.财务报表分析的局限性★考核知识点:会计的概念附1.1(考核知识点解释)会计的主要目的在于向决策者提供财务信息,以帮助他们做出有关财务事项的最有利的决策。

西方财务会计课后习题答案

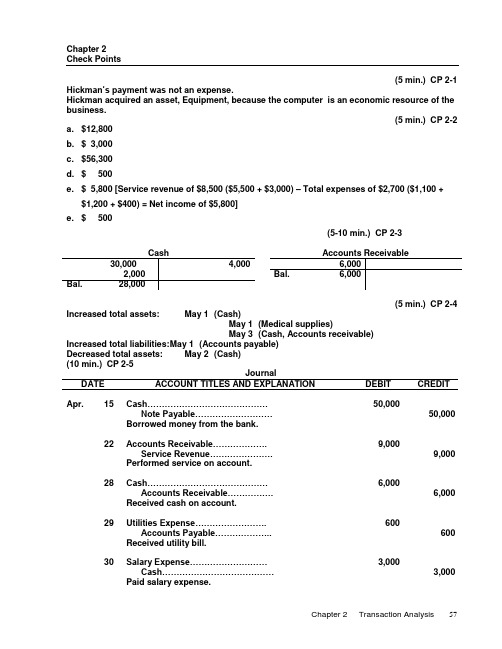

Chapter 2Check Points(5 min.) CP 2-1 Hickman’s payment was not an expense.Hickman acquired an asset, Equipment, because the computer is an economic resource of the business.(5 min.) CP 2-2a. $12,800b. $ 3,000c. $56,300d. $ 500e. $ 5,800 [Service revenue of $8,500 ($5,500 + $3,000) – Total expenses of $2,700 ($1,100 +$1,200 + $400) = Net income of $5,800]e. $ 500(5-10 min.) CP 2-3Cash Accounts Receivable 30,000 4,000 6,0002,000 Bal. 6,000Bal. 28,000(5 min.) CP 2-4 Increased total assets: May 1 (Cash)May 1 (Medical supplies)May 3 (Cash, Accounts receivable)Increased total liabilities: M ay 1 (Accounts payable)Decreased total assets: May 2 (Cash)(10 min.) CP 2-5JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Apr. 15 Cash……………………………………50,000Note Payable………………………50,000 Borrowed money from the bank.22 Accounts Receivable……………….9,000Service Revenue………………….9,000 Performed service on account.28 Cash……………………………………6,000Accounts Receivable…………….6,000 Received cash on account.29 Utilitie s Expense (600)Accounts Payable (600)Received utility bill.30 Salary Expense………………………3,000Cash…………………………………3,000 Paid salary expense.Chapter 2 Transaction Analysis 5730 Interest Expense (300)Cash (300)Paid interest expense.(10-15 min.) CP 2-6Req. 1JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Supplies………………………………..2,000Accounts Payable…………………2,000 Purchased supplies on account.Accounts Payable (500)Cash (500)Paid cash on account.Req. 2Accounts Payable500 2,000Bal. 1,500Req. 3Biaggi’s business owes $1,500, as shown in the Accounts Payable account.(10-15 min.) CP 2-7Req. 1JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Accounts Receivable………………..1,200Service Revenue…………………..1,200 Performed service on account.Cash (500)Accounts Receivable (500)Received cash on account.Req. 2Cash Accounts Receivable Service Revenue500 1,200 500 1,200 Bal. 500 Bal. 700 Bal. 1,200 Req. 3a. The Center earned $1,200: S ervice Revenueb. Total assets $1,200: C ash………………….. $ 500Accounts receivable. 700Total assets…………. $1,20058Financial Accounting 6/e Solutions Manual(10 min.) CP 2-8Old NavyTrial BalanceDecember 31, 20X8ACCOUNT DEBIT CREDITMillionsCash……………………….…...$ 2Other assets (9)Accounts payable……………$ 1Other liabilities (2)Stockholders’ equity (2)Revenues (30)Expenses……………………... 24 ___Total……………………….……$35 $35Old Navy’s net income:$6 million ($30 – $24)(10 min.) CP 2-9 1. Total assets = $53,800 ($33,300 + $2,000 + $500 +$18,000)2. Total liabilities = $1003. Total stockholders’ equity = $53,700 ($53,800 – $100)4. Net income = $5,800 ($8,500 – $1,100 – $1,200 – $400)(10 min.) CP 2-101. Total debits = $121,600 ($58,600 + $81,000 – $18,000)Total credits = $ 58,600Difference = $ 63,000 ($121,600 – $58,600)$63,000 / 9 = $7,000 (an integer), which suggests either atransposition or a slide2. Total debits = $76,600 ($58,600 + $20,000 – $2,000)Total credits = $58,600Difference = $18,000 ($76,600 – $58,600)$18,000 / 9 = $2,000 (original amount of accountsreceivable)3. Total debits = $56,600 ($58,600 – $ 2,000)Total credits = $60,600 ($58,600 + $ 2,000)Difference = $ 4,000 ($60,600 – $56,600)$4,000 / 2 = $2,000 (original amount of accounts receivable)Chapter 2 Transaction Analysis 59(5 min.) CP 2-12Cash Computer Equipment250,000 100,000Accounts Payable Common Stock100,000 250,000Total debits = $350,000 ($250,000 + $100,000)Total credits = $350,000 ($100,000 + $250,000)Exercises(10-15 min.) E 2-1 TO: Home OfficeFROM: Store ManagerDuring the first week, I borrowed $320,000 on a note payable. I used the store’s beginning cash plus the borrowed money to purchase land, a building, copy equipment, and supplies. After all these transactions, the store’s balance sheet appears as follows:Kinko’sOklahoma City StoreBalance SheetDateASSETS LIABILITIESCash $ 80,000* Note payable $320,000 Supplies 10,000Copy equipment 60,000 STOCKHOLDERS’ EQUITYLand 90,000 Common stock 40,000 Building 120,000 Total liabilities and ________ Total assets $360,000 stockholders’ equity $360,000 _____*$40,000 + $320,000 – $90,000 – $120,000 – $60,000 – $10,000 = $80,000(5-10 min.) E 2-2 a. Issuance of stockRevenue transactionb. Purchase of asset on accountBorrow moneyc. Purchase of asset for cashSale of asset for cashCollection of an account receivabled. Payment of dividends to ownersExpense transactione. Pay a liability60Financial Accounting 6/e Solutions Manual(10-20 min.) E 2-4 Req. 1Analysis of TransactionsASSETS = LIABILITIES + STO CKHOLDERS’ EQUITYDate Cash + AccountsReceivable +MedicalSupplies + Land =AccountsPayable +NotePayable +CommonStock +RetainedEarningsType of Stockholders’Equity TransactionOct. 6 40,000 40,000 Issued stock9 (30,000) 30,00012 2,000 2,00015 Not a transaction of the business.15-31 4,000 4,000 8,000 Service revenue 15-31 (1,400) (1,400) Salary expense (1,000) (1,000) Rent expense(300) (300) Utilities expense31 500 (500)31 10,000 10,00031 (1,500) (1,500)Bal. 20,300 4,000 1,500 30,000 500 10,000 40,000 5,30055,800 55,800Chapter 2 Transaction Analysis 61(continued) E 2-4 Req. 2a. $55,800b. $4,000c. $10,500 ($500 + $10,000)d. $45,300 ($55,800 – $10,500, or $40,000 + $5,300)e. $5,300 (Revenue, $8,000 minus total expenses of $2,700, equals net income, $5,300.)62Financial Accounting 6/e Solutions Manual(10-15 min.) E 2-5JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Oct. 6 Cash………………………………………..40,000Common Stock……………………….40,000 Issued stock to owner.9 Land………………………………………...30,000Cash…………………………………….30,000 Purchased land.12 Medical Supplies…………………………2,000Accounts Payable……………………2,000 Purchased supplies on account.15 Not a transaction of the business.15-31 Cash………………………………………..4,000Accounts Receivable……………………4,000Servi ce Revenue……………………..8,000 Performed service for cash and on account.15-31 Salary Expense…………………………..1,400Rent Expense……………………………..1,000Utilities Expense (300)Cash…………………………………….2,700 Paid expenses.31 Cash (500)Medical Supplies (500)Sold supplies.31 Cash………………………………………..10,000Note Payable…………………………..10,000 Borrowed money.31 Accounts Payable……………………….1,500Cash…………………………………….1,500 Paid on account.(10-15 min.) E 2-6 Req. 1Total assets = $145 million ($100 + $60 – $55 + $35 + $26 – $21)Req. 2Company owes $41 million [$60 – $55 + $35 + $22 – $21]Req. 3Net income = $4 million ($26 – $22)Chapter 2 Transaction Analysis 63(10-20 min.) E 2-7 Req. 1 (journal entries)JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Aug. 1 Cash……………………………………………19,500Common Stock…………………………...19,500 Issued common stock to owner.2 Office Supplies (800)Accounts Payable (800)Purchased office supplies on account.4 Land……………………………………………14,000Cash………………………………………..14,000 Paid cash for land.6 Cash……………………………………………2,000Service Revenue…………………………2,000 Performed services for cash.9 Accounts Payable (100)Cash (100)Paid cash on account.17 Accounts Receivable……………………….1,200Service Revenue…………………………1,200 Performed service on account.23 Cash (900)Accounts Receivable (900)Received cash on account.31 Salary Expense………………………………1,000Rent Expense (500)Cash………………………………………..1,500 Paid cash expenses.(continued) E 2-7Req. 2Ending cash = $6,800($19,500 – $14,000 + $2,000 – $100 + $900 – $1,500)Expects to collect on account = $300 ($1,200 – $900)Total liabilities = $700 ($800 – $100)Net income (profit) = $1,700 ($2,000 + $1,200 – $1,000 – $500)64Financial Accounting 6/e Solutions Manual(20-30 min.) E 2-8 Req. 1Cash Accounts ReceivableAug. 1 19,500 Aug. 4 14,000 Aug. 17 1,200 Aug. 23 9006 23 2,0009009311001,500Aug. 31 300Aug. 31 6,800Office Supplies LandAug. 2 800 Aug. 4 14,000Aug. 31 800 Aug. 31 14,000Accounts Payable Common StockAug. 9 100 Aug. 2 800 Aug. 1 19,500 Aug. 31 700 Aug. 31 19,500 Service Revenue Salary ExpenseAug. 6 2,000 Aug. 31 1,00017 1,200 Aug. 31 1,000Aug. 31 3,200Rent ExpenseAug. 31 500Aug. 31 500(continued) E 2-8Req. 2Coaxial Electronic Systems, Inc.Trial BalanceAugust 31, 20X6ACCOUNT DEBIT CREDITCash…………………………...$ 6,800Accounts receivable (300)Office supplie s (800)Land…………………………...14,000Accounts payable…………..$ 700Common stock………………19,500Service revenue……………..3,200Salary expense………………1,000Rent expense (500)Total…………………………...$23,400 $23,400Req. 3Total a ssets ($6,800 + $300 + 800 + $14,000)……..$21,900Total liabilities (700)Total stockholders’ equity ($21,900 –$700)………$21,200Chapter 2 Transaction Analysis 65(10-15 min.) E 2-9JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT1. Cash…………………………………..10,000Common Stock…………………..10,000 Issued common stock.2. Cash…………………………………..7,000Note Payable……………………..7,000 Borrowed money; signed note payable.3. Land…………………………………..31,000Cash………………………………..8,000Note Payable……………………..23,000 Purchased land by paying cashand signing a note payable.4. Supplies (600)Accounts Payable (600)Purchased supplies on account.5. Cash (100)Su pplies (100)Sold supplies for cash.6. Equipment……………………………6,000Cash………………………………..6,000 Paid cash for equipment.7. Accounts Payable (300)Cash (300)Paid cash on account.Cash balance = $2,800 ($10,000 + $7,000 – $8,000 + $100 – $6,000 – $300)Company owes $30,300 ($7,000 + $23,000 + $600 – $300)(10-20 min.) E 2-10Req. 1Whirlpool Appliance ServiceTrial BalanceJune 30, 20X6ACCOUNT DEBIT CREDIT Cash…………………………...$ 9,000Accounts receivable………..15,500Building……………………….40,250Land…………………………...29,000Accounts payable………….. $ 4,300Note payable………………… 13,000Common stock……………… 48,800Retained earnings………….. 21,350*Dividends……………………..6,000Service revenue…………….. 22,00066Financial Accounting 6/e Solutions ManualSalary expense………………8,000Utilities expense…………….1,400Delivery expense (300)Total…………………………...$109,450 $109,450 *Total debits…………………………………………$109,450 Total credits, ex cluding retained earnings…… (88,100) Retained earnings…………………………………$ 21,350 (continued) E 2-10Req. 2Whirlpool Appliance ServiceIncome StatementMonth Ended June 30, 20X6Service revenue………………...$22,000Salary expense…………………$8,000Ut ilities expense………………..1,400Delivery expense (300)Total expenses…………………. 9,700Net income………………………$12,300 (15-25 min.) E 2-11Car Connection, Inc.Trial BalanceDecember 31, 20X3ACCOUNT DEBIT CREDIT Cash…………………………...$ 4,600*Accounts receivable……….. 12,600*Inventory……………………... 17,000Supplies (600)Land…………………………... 55,000Accounts payable…………..$13,100*Common stock………………48,300*Sales revenue……………….. 35,700Cost of goods sold…………. 3,900Salary expense……………… 1,700Rent expense (800)Utilities expense……………. 900* _______Total…………………………...$97,100 $97,100_____*Explanations:Cash: $4,200 + $400 = $4,600Accounts Receivable: $13,000 – $400 = $12,600Accounts Payable: $12,000 + $1,000 – $100 + $200 = $13,100Common Stock: $47,900 + $400 = $48,300Utilities Expense: $700 + $200 = $900(5-15 min.) E 2-12 Cash Accounts Receivable(a) 12,500 (b) 1,500 (f) 8,300(d) 1,800 Bal. 8,300(e) 400(g) 2,000Bal. 6,800Office Supplies Office Furniture(c) 800 (a) 9,000Bal. 800 Bal. 9,000Accounts Payable Common Stock(e) 400 (c) 800 (a) 21,500Bal. 400 Bal. 21,500 Dividends Service Revenue(g) 2,000 (f) 8,300 Bal. 2,000 Bal. 8,300 Salary Expense Rent Expense(d) 1,800 (b) 1,500Bal. 1,800 Bal. 1,500(10-20 min.) E 2-13Req. 1LaVell Oxford, AttorneyTrial BalanceJuly 31, 20X8ACCOUNT DEBIT CREDITCash…………………………...$ 6,800Accounts receivable………..8,300Office supplies (800)Office furniture………………9,000Accounts payable…………..$ 400Common stock………………21,500Dividends……………………..2,000Service revenue……………..8,300Salary expense………………1,800Rent expense……………….. 1,500Total…………………………...$30,200 $30,200Req. 2The business performed well during July. The result of operations was net income of $5,000, as shown by the income statement accounts:Service revenue………………….$ 8,300Salary expense………..$1,800Rent expense…………. 1,500Total expenses……………….. (3,300)Net income……………………….. $ 5,000(20-30 min.) E 2-14Reqs. 1 and 3Cash Accounts ReceivableDec. 2 7,000 Dec. 2 500 Dec. 18 1,7009 800 3 3,00012 200Bal. 4,100Supplies EquipmentDec. 5 300 Dec. 3 3,000Furniture Accounts PayableDec. 4 3,600 Dec. 4 3,6005 300Bal. 3,900 Common Stock DividendsDec. 2 7,000Service Revenue Rent ExpenseDec. 9 800 Dec. 2 50018 1,700Bal. 2,500Utilities Expense Salary ExpenseDec. 12 200(continued) E 2-14Req. 2JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Dec. 2 Cash……………………………………..7,000Common Stock……………………..7,0002 Rent Expense (500)Cash (500)3 Equipment……………………………...3,000Cash………………………………….3,0004 Furniture………………………………..3,600Accounts Payable………………….3,6005 Supplies (300)Accounts Payable (300)9 Cash (800)Service Revenue (800)12 Utilities Expense (200)Cash (200)18 Accounts Receivable…………………1,700Service Revenue…………………...1,700 (continued) E 2-14Req. 4Matthew Rogers, Certified Public Accountant, P.C.Trial BalanceDecember 18, 20XXACCOUNT DEBIT CREDIT Cash…………………………...$ 4,100Accounts receivable………..1,700Supplies (300)Equipment……………………3,000Furniture……………………...3,600Accounts payable…………..$ 3,900Common stock………………7,000Dividends……………………..—Service revenue……………..2,500Rent expense (500)Utilities expense (200)Salary expense………………—Total…………………………...$13,400 $13,400(20-40 min.) E 2-15a. Net income for March – Given as follows:Retained EarningsFeb. 28 Bal. 7,000MarchMarch dividends 15,800 net income X = $19,300Mar. 31 Bal. 10,500$7,000 + X – $15,800 = $10,500X = $19,300b. Total cash paid during March:CashFeb. 28 Bal. 11,600March receipts 81,200 March payments X = $87,800Mar. 31 Bal. 5,000$11,600 + $81,200 – X = $ 5,000X = $87,800 (continued) E 2-15c. Cash collections from customers during March:Accounts ReceivableFeb. 28 Bal. 24,300March saleson account 49,400 March collections X = $47,000 Mar. 31 Bal. 26,700$24,300 + $49,400 – X = $26,700X = $47,000d. Cash paid on a note payable during March:Note PayableFeb. 28 Bal. 13,900 March MarchX =17,500 payments on note X new borrowing 25,000Mar. 31 Bal. 21,400 $13,900 + $25,000 – X = $21,400X = $17,500(20-30 min.) E 2-16Req. 1Road Runner, Inc.Trial BalanceDecember 31, 20X5Cash…………………………...$ 4,200Accounts receivable………..7,200Supplies (800)Land…………………………...34,000Accounts payable…………..$ 5,800Note payable…………………5,000Common stock………………20,000Retained earnings…………..7,300Service revenue……………..9,100Salary expense………………3,400Advertising expense………. 900 _______Totals………………………….$50,500 $47,200Out of balanceby $3,300The correct balance of Accounts Receivable is $3,900 ($7,200 – $3,300). After this correction, total debits will be $47,200 ($50,500 – $3,300), the same as total credits.(continued) E 2-16Req. 2Road Runner, Inc.Trial BalanceDecember 31, 20X5Cash ($4,200 –$400)……………………$ 3,800Accounts receivable($7,200 –$3,300 + $7,000)..............10,900 Supplies.. (800)Land ($34,000 + $80,000)………………114,000Accounts payable ($5,800 + $2,000)…$ 7,800 Note payable ($5,000 + $80,000)……...85,000 Common stock…………………………..20,000 Retained earnings………………………7,300 Service revenue ($9,100 + $7,000)……16,100 Salary expense ($3,400 + $400)………3,800Advertising expense ($900 + $2,000). 2,900Tot als……………………………………...$136,200 $136,200Req. 3a. Total assets = $129,500 ($3,800 + $10,900 + $800 + $114,000).b. Road Runner is profitable, as indicated by the excess of revenue ($16,100) over totalexpenses ($6,700 = $3,800 + $2,900).(10-15 min.) E 2-17San Francisco:Income statement June July Medical expense…………..$40,000 $ -0- Balance sheet June 30 July 31 Cash…………………………$55,000 $23,000*Accounts payable…………40,000 8,000** Bay Area:Income statement June July Service revenue…………..$40,000 $ -0- Balance sheet June 30 July 31 Cash………………………… $ -0- $32,000Accounts receivable……..40,000 8,000**Explanation:San Francisco’s expense is Bay Area’s revenue.San Francisco’s cash payment is Bay Area’s cash receipt.San Francisco’s account payable is Bay Area’s account receivable. __________*$55,000 – $32,000 = $23,000**$40,000 – $32,000 = $ 8,000。

《西方财务会计》PPT课件

CASH AND ITS CONTROL

Introduction(cont.)

• Cash is one of financial assets. • Financial assets include cash,short-term investments and

receivables. • Financial assets are shown in the balance sheet at their

• 1. All receipts should be banked promptly. • 2. Receipts from cash sales should be supported by sales tickets,

cash register tapes, and so on. • 3. Accountability should be established each time when cash is

very stable market value,and mature within 90 days of the date of acquisition.

Cash controlling

• Cash receipts • Cash payments • Cash balance

Controlling Cash Receipts

Why should a business control

cash?(summary of textbook)

• To ensure that sufficient cash is available when needed and that too much cash is not idle, managers must plan and control carefully the cash needs of the business. In addition, because cash is universally desirable, a good business must maintain careful control over its cash to ensure that it is not lost through fraud or embezzlement.

西方财务会计 chapter1

1.2 COMPARISON BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

Financial Accounting ---- The process of developing and reporting financial information for external users who do not have direct access to the information preparing which should be in accordance with General Accepted Accounting Principles (GAAP).

1.2 COMPARISON BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

Management Accounting ---- The process of developing and reporting accounting information for internal users who have direct access to the information preparing.

Generally Accepted Accounting Principles

The Securities and Exchange Commission (SEC) has the authority to determine the financial statements to be provided to stockholders and the measurement rules applied in producing the statements. The Financial Accounting Standards Board (FASB) is currently recognized as the group responsible for establishing GAAP.

财务会计(英)答案

1-10Owners' equity is also called capital (for proprietorships and partnerships) and shareholders' equity or stockholders' equity (for corporations).

1-3Examples of decisions that are likely to be influenced by financial statements include choosing where to expand or reduce operations, lending money, investing ownership capital, and rewarding mangers.

1-17CPA is a Certified Public Accountant. One becomes a CPA by a combination of education, qualifying experience, and the passing of a two-day national examination.

1-16The board of directors is the link between stockholders and the actual managers. It is the board’s duty to ensure that managers act in the interests of shareholders.

西方财务会计chapt1

评价:虽然历史成本会计模式受到很多批评,但迄今为止未找到更好 的模式替代它,故其为更为合适的会计计量模式,其他会计计量模式 只是对历史成本进行局部的修正。

第六节

财务报表的基本要素和一般 目的财务报表

• 会计平衡公式 Assets=Liabilities + Owner’s equity 或 : Assets=Equity 财务报表的基本要素 ☆美国FASB的“财务会计概念公告”第六号 《财务会计报表的基本要素》定义了10大会计要 素:资产、负债、所有者权益、收入、费用、利 得、综合收益、所有者向企业投资、企业对所有 者的分派。本教材定义的会计要素为8项,不包 括所有者向企业投资、企业对所有者的分派。

会计的基本原则

原则

历史成本原 则 Historical 基 Cost 本 Principle

含义

经营活动的各项交易以实际发生的成 本入账历史成本容易取得,客观,历 史悠久,易于理解接受,但由于通胀 和币值变动的存在,该模式受到较多 的批评。 确认为某一会计期间的收入应符合2个 条件:已经赚取;现金流入确实可实 现。 在取得收入的同时应确认与收入相关 的费用。

配合使用者 的质量特征 易懂性(Understandability)

决策有用性的 基本质量特征

相关性Relevance(与决策相关,具有 反馈价值Feedback Value和预测价 值Predictive Value,还应是适时的 Timeliness ) 可靠性Reliability (包含可验证性 Verifiability 和如实表述 Representational Faithfulness 两项基本品质要素)

• 财务会计的概念结构

FASB从1973年创立时起,便着手财务会计概念结构的 研究,由8大专题组成。 财务报告目标的研究于1978年11月完成。 FASB所发表 的一系列的《财务会计概念公告》构成了财务会计概念 结构的基本框架,是财务会计的基础和基础理论。 美国财务会计准则委员会(FASB)对于财务会计概念 框架的研究是卓有成效的,对世界一些国家的会计理论 和会计实务的发展及国际会计准则的制定和概念框架产 生了较大影响。 如果没有一套前后一致、系统完整、逻辑严密的基础理 论体系为指导,具体会计准则将缺乏一致和可比,甚至 产生矛盾和冲突。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.2 COMPARISON BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

Management Accounting ---- The process of developing and reporting accounting information for internal users who have direct access to the information preparing.

The Conceptual Framework

The Financial Accounting Standards Board (FASB) issues Statements of Financial Accounting Concepts. These statements constitute the conceptual framework of accounting.

Generally Accepted Accounting Principles

The Securities and Exchange Commission (SEC) has the authority to determine the financial statements to be provided to stockholders and the measurement rules applied in producing the statements. The Financial Accounting Standards Board (FASB) is currently recognized as the group responsible for establishing GAAP.

西方财务会计

WESTERN FINANCIAL ACCOUNTING

Chapter 1

The Financial Accounting Conceptual Framework And The Accounting Equation

1.1 ACCOUNTING

A service activity ---- Provide useful information about economic entities to interested parties

The Framework is to be a reference of basic accounting theory for solving emerging practical problems of reporting.

1.3-2 Overview of the Conceptual Framework ---- Three levels of objectives elements and principles

1.3 THE FASB’S FINANCIAL ACCOUNTING CONCEPTUAL FRAMEWORK

1.3-1 Objectives of the Conceptual Framework

The Framework is to be the foundation for building a set of coherent accounting standards and rules.

The first level consists of objectives.

The second level explains financial elements and characteristics of information.

The third level incorporates recognition and measurement criteria.

1.2 COMPARISON BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

Financial Accounting ---- The process of developing and reporting financial information for external users who do not have direct access to the information preparing which should be in accordance with General Accepted Accounting Principles (GAAP).

GAAP

Generally accepted accounting principles are the measurement rules used to develop the information in financial statement. They are those guidelines which indicate how to report economic events. They consist of a number of concepts,principles and procedures.

And a measurement-communication activity---The usefulness of accounting information depends on effective measurement of the economic activities and effective communication of those measurements to users of that information.

Accounting information and decision makers

Accounting information

Financial accounting

External Decision makers

Management Accounting

Internห้องสมุดไป่ตู้l Decision makers