财务管理案例分析

财务管理案例分析论文(5篇)

财务管理案例分析论文(5篇)财务管理案例分析论文(5篇)财务管理案例分析论文范文第1篇【关键词】网络环境财务管理案例教学教学模式案例教学法是一种启发式、争论式、互动式的教学方法,以典型案例为载体,引导同学阅读、思索、争论案例,在互动争论中关心同学把握和运用理论学问,并培育同学分析、推断、表达以及运用所学学问处理问题的力量。

传统的案例教学采纳在课堂中集中争论的教学形式,由于受课堂教学时间和条件的限制,同学难以在短时间内对案例绽开全面分析。

尤其是财务管理教学中的一些案例,案例内容包括公司背景状况、经营状况说明以及许多报表数据,同学很难在短时间内把其中的财务问题分析清晰,更难以提出有效的对策建议,大大降低了案例教学的效果。

网络科技的进展,多媒体教学平台的广泛应用,为财务管理教学模式的创新和改革供应了有力的技术支持。

网络环境下建设网络案例教学平台,给同学供应自主探究、协作学习的环境,使得教学活动突破时间和空间的限制,同学能够实现更具弹性的自主学习。

利用网络教学平台,可以供应参考资料、案例答疑以及争论区,增加同学与老师间、同学与同学间的教学沟通,可以提高同学的参加度,增加教学效果。

本文结合教学实践,构建了网络环境下财务管理案例教学模式。

一、网络环境下财务管理案例教学的理论依据建构主义理论、情境学习理论是构建网络环境下财务管理案例教学模式的重要理论依据。

建构主义关于教学的基本观点:同学是认知的主体,是意义的主动建构者,老师是意义建构的指导者、促进者,而不是学问的灌输者;情境对意义建构具有重要作用,要尽量创设能够促进同学乐观主动地建构学问的情景;注意协作学习,通过同学与老师之间、同学与同学之间沟通争论建构自己的学问结构;学习环境的设计具有重要意义,要细心设计教学环境,让同学能够利用各种工具和资源来达到学习目标。

建构主义理论的启示是:利用网络平台创建“学习社区”,在老师指导下,同学对案例情景绽开自主探究、协作学习,最终提高同学分析问题、解决问题的力量。

财务管理案例分析论文

摘要:随着市场经济的快速发展,企业面临着越来越多的财务管理问题。

本文通过对某企业的财务状况进行分析,探讨其财务管理中存在的问题,并提出相应的改进措施,以期为我国企业财务管理提供参考。

一、引言财务管理是企业经营管理的重要组成部分,直接关系到企业的生存和发展。

良好的财务管理能够提高企业的经济效益,降低经营风险。

本文以某企业为例,对其财务状况进行分析,旨在找出其财务管理中存在的问题,并提出相应的改进措施。

二、案例分析1. 企业概况某企业成立于2000年,主要从事某行业产品的研发、生产和销售。

经过多年的发展,企业规模不断扩大,市场份额逐年提高。

然而,在快速发展的同时,企业也面临着诸多财务管理问题。

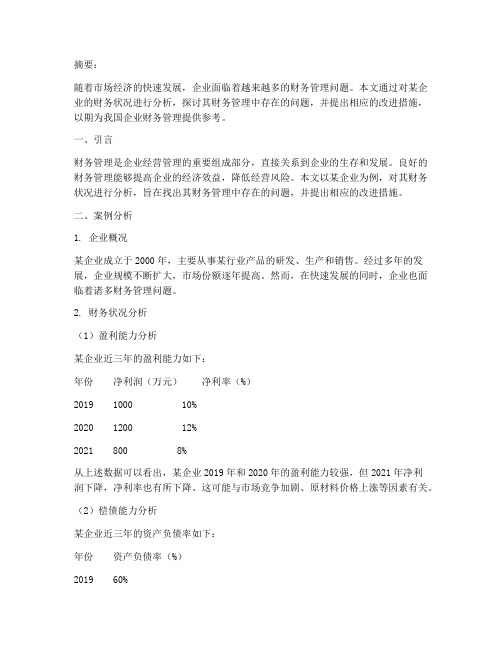

2. 财务状况分析(1)盈利能力分析某企业近三年的盈利能力如下:年份净利润(万元)净利率(%)2019 1000 10%2020 1200 12%2021 800 8%从上述数据可以看出,某企业2019年和2020年的盈利能力较强,但2021年净利润下降,净利率也有所下降。

这可能与市场竞争加剧、原材料价格上涨等因素有关。

(2)偿债能力分析某企业近三年的资产负债率如下:年份资产负债率(%)2019 60%2020 65%2021 70%从上述数据可以看出,某企业的资产负债率逐年上升,说明企业负债规模不断扩大,偿债压力加大。

(3)运营能力分析某企业近三年的存货周转率如下:年份存货周转率(次)2019 52020 4.52021 4从上述数据可以看出,某企业的存货周转率逐年下降,说明企业存货管理存在问题,可能导致资金占用过多。

三、问题分析1. 盈利能力下降某企业盈利能力下降的原因主要有以下几点:(1)市场竞争加剧,产品价格下降;(2)原材料价格上涨,导致生产成本增加;(3)销售费用、管理费用等期间费用较高。

2. 偿债能力下降某企业偿债能力下降的原因主要有以下几点:(1)负债规模过大,导致财务风险增加;(2)盈利能力下降,还款能力减弱;(3)融资渠道单一,资金筹集困难。

财务管理案例分析报告

一、案例背景某公司成立于2000年,主要从事电子产品研发、生产和销售。

经过多年的发展,该公司已成为我国电子产品行业的领军企业之一。

然而,在2019年,该公司因财务管理问题导致资金链断裂,面临破产的风险。

为了挽救公司,公司管理层决定对财务管理体系进行改革。

以下是该公司财务管理改革的案例分析。

二、案例分析1. 案例问题描述(1)资金链断裂:由于公司财务管理不善,导致资金链断裂,无法按时偿还债务。

(2)财务风险:公司财务风险较高,资金使用效率低下,财务状况不稳定。

(3)成本控制:公司成本控制不力,导致产品成本过高,影响产品竞争力。

2. 案例原因分析(1)财务管理体制不完善:公司财务管理体制不完善,缺乏有效的内部控制和风险防范机制。

(2)财务人员素质不高:公司财务人员素质参差不齐,缺乏专业知识和技能,无法满足公司财务管理需求。

(3)成本控制意识淡薄:公司管理层对成本控制意识淡薄,导致成本控制不力。

3. 案例解决方案(1)完善财务管理体制:建立健全内部控制制度,加强风险防范和监督,确保财务安全。

(2)提高财务人员素质:加强财务人员培训,提高其专业知识和技能,确保财务工作质量。

(3)加强成本控制:强化成本控制意识,制定合理的成本控制措施,降低产品成本。

4. 案例实施与效果(1)实施过程:公司管理层根据解决方案,对财务管理体系进行改革。

具体措施包括:①调整财务组织架构,设立专门的财务管理部门,负责财务管理、风险防范和内部控制等工作。

②加强财务人员培训,提高其专业素质和业务能力。

③制定成本控制方案,对生产、销售等环节进行成本控制。

(2)实施效果:通过财务管理改革,公司财务状况得到明显改善,具体表现在:①资金链断裂问题得到解决,公司按时偿还债务。

②财务风险得到有效控制,财务状况稳定。

③成本控制取得显著成效,产品成本降低,竞争力提高。

三、案例总结1. 案例启示(1)财务管理是企业发展的关键因素,企业应高度重视财务管理。

财务典型案例分析报告(3篇)

第1篇一、引言随着我国经济的快速发展,企业财务管理工作日益重要。

财务典型案例分析报告旨在通过对具体案例的深入剖析,揭示企业财务管理中的常见问题,为企业管理者提供有益的借鉴和启示。

本报告选取了一家企业财务管理的典型案例,对其进行分析,以期为我国企业财务管理提供参考。

二、案例背景(一)企业简介某公司成立于1998年,主要从事房地产开发、物业管理、酒店管理、商业运营等业务。

经过20多年的发展,该公司已成为我国房地产行业的领军企业之一。

截至2020年底,公司总资产达到500亿元,员工人数超过1万人。

(二)案例背景2019年,某公司因财务管理问题被监管部门查处,涉及金额巨大。

经调查,该公司存在以下问题:1.财务报表虚假记载;2.关联交易未披露;3.内部控制不完善。

三、案例分析(一)财务报表虚假记载1.问题表现经调查,某公司2016年至2018年期间,通过虚构销售收入、虚增资产等方式,将财务报表中的利润虚增约20亿元。

具体表现在以下几个方面:(1)虚构销售收入:公司将未实际发生的销售业务计入报表,虚增销售收入。

(2)虚增资产:公司将未实际取得的资产计入报表,虚增资产总额。

2.原因分析(1)公司管理层追求短期利益,忽视财务报表的真实性。

(2)公司内部控制不完善,缺乏有效的监督机制。

(3)公司财务人员职业道德缺失,为达到虚增利润的目的,伪造财务数据。

(二)关联交易未披露1.问题表现某公司在2017年至2018年期间,与关联方进行多笔关联交易,涉及金额巨大。

然而,公司未按规定披露这些关联交易,侵犯了中小股东的利益。

2.原因分析(1)公司管理层为掩盖关联交易的真实情况,规避监管。

(2)公司内部控制不完善,关联交易审批流程不规范。

(3)公司信息披露制度不健全,未及时披露关联交易信息。

(三)内部控制不完善1.问题表现某公司在财务管理过程中,内部控制存在以下问题:(1)财务制度不健全,缺乏统一的财务管理规范。

(2)内部审计机制不完善,无法及时发现和纠正财务问题。

财务管理案例题

财务管理分析案例一(一)案例资料:材料1:A公司是煤炭类上市公司,2008年1-8月,全国煤炭市场火爆,供不应求,焦煤价格一度突破2200元/吨,电煤价格一度突破1600元/吨,在这种市场形势下,煤炭类上市公司2008年年报利润均创新高,其每股收益远远高于其他行业,A公司也不例外。

但是2008年9月份以来,截止2009年初由于美国金融危机的影响,下游钢铁电力等行业出现萎缩,虽然煤价仍然较高,但是煤炭销售量急剧萎缩,秦皇岛港口一度出现大量煤炭积压,A公司为了减少产量被迫停产检修。

材料2:B公司为石油贸易类的上市公司,2008年下半年由于世界油价急剧下跌,由于该公司在高油价期间高价购入大量油料,存货成本太高,影响年终业绩。

因此公司决定到国外期货交易所进行石油期货业务,由于操作得当,该企业在新加坡原油期货交易所获利3亿美元,此项业务导致2008年利润表由亏损转为盈利。

材料3:C上市公司2009年1月预计2008年度盈利增长30%,但经注册会计师审计,C公司2008年年报中,存在重大舞弊行为,该企业采用收入提前入账,成本延后入账,伪造销售合同等手法,使当期利润虚高50%。

(二)问题分析讨论:如果你是一位财务分析师,面对以上情况,请思考:1、财务目标有哪几种提法,请简要加以说明。

答:①利润最大化,利润等于收入减成本和费用。

②资本利润率最大化或每股利润最大化,是利润与普通股股数的对比数。

③企业价值最大化,企业价值并不等于账面资产的总价值。

2、结合ABC三个公司的情况,请说明会计利润存在的缺陷。

答:①利润最大化是一个绝对指标,没有考虑企业的投入和产出之间的关系。

②利润最大化没有考虑利润发生的时间,没有考虑资金的时间价值。

③利润最大化没能有效地考虑风险问题。

这可能使财务人员不顾风险的大小去追求最大的利润。

④利润最大化往往会使企业财务决策行为具有短期行为的倾向,只顾片面追求利润的增加,而不考虑企业长远的发展。

⑤会计利润的主观性导致会计信息失真的缺陷。

财务管理案例报告分析(3篇)

第1篇一、案例背景随着我国经济的快速发展,企业之间的竞争日益激烈,财务管理在企业运营中的地位越来越重要。

本文以某企业为例,分析其财务管理的现状、存在的问题以及改进措施,以期为企业财务管理提供有益的借鉴。

二、案例企业概况某企业成立于2005年,主要从事电子产品研发、生产和销售。

经过多年的发展,企业规模不断扩大,已成为行业内的知名企业。

企业现有员工1000余人,年销售收入超过10亿元。

三、案例企业财务管理现状1. 财务组织架构某企业财务部门设有财务总监、财务经理、会计、出纳等岗位,形成了较为完善的财务组织架构。

财务部门负责企业的财务管理、会计核算、资金管理、税务筹划等工作。

2. 财务管理制度企业制定了完善的财务管理制度,包括预算管理、成本控制、应收账款管理、存货管理、固定资产管理等方面。

这些制度为企业财务管理的规范化提供了保障。

3. 财务核算企业采用权责发生制进行会计核算,按照国家会计准则进行财务报表编制。

财务报表包括资产负债表、利润表、现金流量表等,能够全面反映企业的财务状况。

4. 资金管理企业实行集中资金管理,确保资金安全、高效运转。

企业设立资金管理部门,负责资金筹集、使用和监控。

同时,企业还建立了严格的资金审批制度,确保资金使用的合理性和合规性。

5. 成本控制企业高度重视成本控制,通过制定合理的成本预算、加强成本核算和分析,降低生产成本。

企业还开展了成本效益分析,不断提高企业的盈利能力。

四、案例企业财务管理存在的问题1. 财务风险意识不足企业在财务管理过程中,对财务风险的识别、评估和防范意识不足。

在实际操作中,存在一些不规范的行为,如违规操作、内部控制薄弱等,导致财务风险增大。

2. 财务信息化程度低企业财务信息化程度较低,部分财务数据仍依赖于手工处理,导致工作效率低下,数据准确性难以保证。

3. 财务人员素质参差不齐企业财务人员素质参差不齐,部分人员缺乏专业知识和实践经验,难以满足企业财务管理的要求。

优秀财务案例分析报告(3篇)

第1篇一、案例背景随着市场经济的发展,企业之间的竞争日益激烈,财务管理的地位和作用愈发重要。

为了提升财务管理水平,许多企业开始借鉴优秀财务管理的案例,以期为自身的发展提供有益的借鉴。

本报告以某知名企业为例,对其财务管理的优秀案例进行深入分析,旨在为我国企业财务管理提供有益的启示。

二、案例概述某知名企业成立于20世纪90年代,经过多年的发展,已成为行业内的领军企业。

在企业的发展过程中,其财务管理部门始终秉持着“严谨、务实、创新”的理念,为企业创造了良好的经济效益。

本案例将从以下几个方面对该企业的财务管理优秀案例进行分析。

三、案例分析(一)财务管理组织架构1. 高层领导重视:该企业高层领导高度重视财务管理,将财务管理纳入企业发展战略的重要组成部分。

企业董事长亲自担任财务总监,确保财务管理工作的高效开展。

2. 专业团队建设:企业财务部门拥有一支高素质、专业化的团队,成员均具备丰富的财务管理经验和扎实的理论基础。

3. 分工明确:财务部门内部设置多个岗位,如财务分析、预算管理、资金管理、税务筹划等,确保各项工作有序开展。

(二)财务管理制度1. 健全的财务制度体系:该企业建立了完善的财务制度体系,涵盖了财务预算、成本控制、资金管理、税务筹划等方面。

2. 严格的内部控制:企业财务管理制度强调内部控制,通过建立健全的内部控制体系,有效防范财务风险。

3. 信息化管理:企业积极应用财务信息化管理,实现财务数据的实时监控和分析,提高财务管理效率。

(三)财务分析1. 全面预算管理:企业实施全面预算管理,通过预算编制、执行、分析和考核,确保企业财务目标的实现。

2. 成本控制:企业通过成本核算、成本分析和成本控制,降低成本,提高企业盈利能力。

3. 资金管理:企业建立健全的资金管理制度,确保资金安全、高效运转。

(四)税务筹划1. 合理避税:企业根据国家税法,合理避税,降低企业税负。

2. 税务筹划:企业结合自身业务特点,进行税务筹划,提高企业整体税务效益。

财务管理分析报告案例(3篇)

第1篇一、报告概述本报告以某企业为例,对其财务管理进行分析。

通过对企业财务状况、经营成果和现金流量的分析,评估企业的财务风险和经营状况,为企业决策提供参考。

二、企业概况某企业成立于2000年,主要从事电子产品研发、生产和销售。

经过多年的发展,企业已具备一定的市场份额和品牌知名度。

企业目前拥有员工1000余人,年销售额达到10亿元。

三、财务状况分析1. 资产负债表分析(1)资产结构分析截至2021年底,企业总资产为15亿元,其中流动资产为8亿元,占总资产的比例为53.33%;非流动资产为7亿元,占总资产的比例为46.67%。

流动资产中,货币资金为2亿元,存货为3亿元,应收账款为3亿元。

非流动资产中,固定资产为4亿元,无形资产为3亿元。

从资产结构来看,企业资产流动性较好,短期偿债能力较强。

但存货占比较高,需关注存货周转率。

(2)负债结构分析截至2021年底,企业总负债为8亿元,其中流动负债为5亿元,占总负债的比例为62.5%;非流动负债为3亿元,占总负债的比例为37.5%。

流动负债中,短期借款为2亿元,应付账款为3亿元。

非流动负债中,长期借款为1亿元。

从负债结构来看,企业负债以流动负债为主,短期偿债压力较大。

企业需关注短期借款和应付账款的偿还情况。

2. 利润表分析(1)营业收入分析2021年,企业营业收入为10亿元,同比增长10%。

其中,主营业务收入为9亿元,其他业务收入为1亿元。

从营业收入来看,企业主营业务收入占比高,市场竞争力较强。

(2)成本费用分析2021年,企业营业成本为7亿元,同比增长8%。

其中,主营业务成本为6.5亿元,其他业务成本为0.5亿元。

期间费用为1亿元,同比增长5%。

从成本费用来看,企业成本控制能力较好,但期间费用增长较快,需关注费用控制。

(3)利润分析2021年,企业实现净利润1亿元,同比增长15%。

其中,主营业务利润为0.8亿元,其他业务利润为0.2亿元。

从利润来看,企业盈利能力较强,但需关注主营业务利润的增长。

财务管理案例分析及答案

财务管理案例分析及答案在企业管理中,财务管理是一个至关重要的部门,它负责监督和控制公司的财务活动。

正确的财务管理对于企业的发展和成功至关重要。

本文将通过一个案例分析来探讨财务管理的实践和答案。

案例:公司A的财务管理挑战公司A是一家刚刚起步的小型企业。

由于业务扩张和市场竞争的压力,公司A面临着一系列的财务管理挑战。

以下是公司A所面临的主要问题:1. 资金管理不善:公司A的现金流问题严重,无法及时支付供应商和员工的薪资,导致供应链断裂和员工流失。

2. 预算编制不准确:公司A没有建立有效的预算制度,导致资金使用不当,支出超过预期,难以做出正确的战略决策。

3. 资产负债管理薄弱:公司A的负债水平相对较高,无法有效管理负债与资产的比例,导致财务风险增加。

4. 缺乏财务规范:公司A没有建立完善的财务制度和流程,导致财务数据的准确性和及时性受到威胁。

面对这些挑战,公司A需要采取适当的财务管理策略来解决问题并实现可持续发展。

答案:1. 资金管理:公司A应该优先解决现金流问题。

首先,建立一个详细的现金流预测模型,并进行定期更新与监控。

其次,与供应商和客户沟通,寻求延迟付款或分期付款的合作机会。

此外,积极寻求外部资金支持,例如与银行合作获得贷款等。

2. 预算编制:公司A应该建立一个科学合理的预算制度。

首先,进行详细的市场和行业调研,制定准确的销售和费用预算。

其次,与各部门和员工合作,制定具体可行的目标和任务,确保各项投资和支出符合预算要求。

最后,定期进行预算执行情况的跟踪和分析,及时调整预算方案。

3. 资产负债管理:公司A应该优化资产负债结构,降低财务风险。

首先,减少短期负债,寻求长期稳定的融资渠道,如发行债券或股票等。

其次,优化资产配置,平衡固定资产和流动资产的比例,提高资产回报率。

另外,加强对负债的监控和管理,及时偿还债务,保持良好的信用记录。

4. 财务规范:公司A应该建立健全的财务制度和流程,确保财务数据的准确性和及时性。

财务管理案例分析实验报告5篇

财务管理案例分析实验报告5篇财务管理案例分析实验报告(精选篇1)实训目的:通过财务管理模拟,使我们能够比较系统地掌握财务管理的基本程序和具体方法,加深对所学专业理论知识的理解,提高实际动手能力。

此次的实训为我们在学习财务管理过程中将理论与实际完美地结合起来。

让我能够认真学习财务管理理论,学习相关法律,法规等知识,利用空余时间认真学习一些课本内容以外的相关知识,掌握了一些基本的财务管理技能,从而意识到我以后还应该多学些什么,加剧了紧迫感,为真正跨入社会施展我们的才华,走上工作岗位打下了基础!实训经过:首先,我们进行的是为期四周的财务管理模拟题,通过大量的模拟题的训练,使得我们对财务管理有了一定的了解。

紧接着,我们开始分小组设立公司,模拟我们即将进行一个项目的投资。

通过计算项目与之相关的各种报表以及制作商业计划书,再对其他小组进行我们项目的答辩,完成了整个财务管理的过程。

实训体会:财务管理实训是非常重要的课程,经过对初级财务管理以及中级财务管理的学习,财务管理实训是由理论到实际操作的重要转变。

财务管理这种职业,在理论研究方面,并不需要多少人,需要的是实际操作好、专业技能强的人才。

在没有上财务管理实训这门课程之前,我所懂得的,都只是一些理论知识。

就如同第一次做财务管理实训时一样,只剩下了手忙脚乱。

发现自己真的实际操作起来一塌糊涂,什么都错。

随着时间的推移,以及老师的指导,我才渐渐对财务分析这件事熟悉起来,不再手忙脚乱。

从一开始的做财务管理模拟题,到财务分析,然后商业计划书答辩等一系列繁琐的工作,其中的酸甜苦辣,只有经历过了,才正真的了解到什么是财务管理。

原来财务管理工作并没有想象中的那么简单,那么轻闲。

以前,我总以为自己的财务管理理论知识扎实较强,正如所有工作一样,掌握了规律,照葫芦画瓢准没错,经过这次实践,才发现,财务管理其实更讲究的是它的实际操作性和实践性。

书本上似乎只是纸上谈兵。

倘若将这些理论性极强的东西搬上实际上应用,那我们也会是无从下手。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

The case study ofSony corporation Members of our group:童士卫财务管理0201 012002019106唐虎财务管理0201 012002019105王小夏财务管理0201 012002019126季春蕾财务管理0202 012002019214张亚茹财务管理0201 012002019131任课老师: 夏新平完成时间: 2005年1月28日一.Background information of Sony1. Sony is founded on May 7, 1946 with the Headquarters Tokyo and Japan.2. Its corporate strategies are becoming a “knowledge-emergent enterprise in the broadband network era”.①Evidenced by recent improvements in network infrastructure,the broadband environment has begun to expand at a rapid pace.②In preparation for the arrival of the full-scale broadband era,Sony is pursuing its vision of creating a Ubiquitous “V alue”Network (UVN).3. Its development aspect expanded from the first magnetic tape recorder in1950, to the first "QUALIA" products in 2003, during these years with representative products in each decade:60th—first tape recorder and transistor70th--video cassette player and headphone stereo Walkman80th--CD player and camcorder90th--high-density disc and DVD playerIn the 21th century-- EL Display and optical disc二. The main operations of the corporation are:①②③④⑤⑥三. The main structure of its sales income1. First is the Electronics:The Electronics segment consists of the following categories: Audio, Video, Televisions, Information and Communications,Semiconductors, Components and Other.The graph shows the information about this: The income is decreasing2. Second is the Game:Game console and software business is conducted by Sony Computer Entertainment Inc.We can see the information from the graph: the income is also decreasing3. Third is the Music:Music business is conducted by Sony Music Entertainment Inc. (SMEI) and Sony Music Entertainment (Japan) Inc. (SMEJ).The graph is showing the basic information: The income is decreasing4. Fourth is the Picture:Motion pictures, television and other businesses are conducted by Sony Pictures Entertainment Inc. (SPE).And also the basic information is from the Graph: The income is increasing5. Fifth is the financial service:The Financial Services segment includes Sony Life Insurance Co. Ltd. Sony Assurance Inc., Sony Bank Inc. and Sony Finance International. Inc.As graph of right show the operating information: The income is increasing6. Sixth is other operating:The Other segment includes an Internet-related business, So-net, which is conducted by Sony Communication Network Corporation, an in-House information system services business, an IC card business and other businesses.With the information in the right graph: The income is increasingThe major Products of Sony①AudioHome audio, portable audio, car audio, and car navigation systems②VideoVideo cameras, digital still cameras, video decks, and DVD-Video players/recorders, and Digital-broadcasting receiving systems③TelevisionsCRT-based televisions, projection televisions, PDP televisions, LCD televisions, projector for computers and display for computers④Information and communicationsPC, printer system, portable information PC, broadcast and professional use audio/video/monitors and other professional-use equipment⑤SemiconductorsLCD, CCD and other semiconductors⑥Electronic componentsOptical pickups, batteries, audio/video/data recording media, and data recording systems四.Sales and Operating Revenue by Geographic Information1. The main market of course is the USA2. It is expand the Europe and other country market ,while decrease theUSA and Japan market ,While seems flat in total market .3. We can conclude Sony is facing a worldwide competition.4. It is changing its business from traditional area to the new area,especially the entertainment market.5. It also need find new market, for example the Asian market, and bringnew product with technology.This is the Segment Information of its sales income6. Developing trend AnalysisFactors which may affect Sony‟s fi nancial performance include the following:①market conditions, including general economic conditions, levels ofconsumer spending, foreign exchange fluctuations②Sony‟s ability to continue to implement personnel reduction and otherbusiness reorganization activities③Sony‟s ability to implement i ts network strategy, and implementsuccessful sales and distribution strategies in the light of the Internet and other technological developments④Sony‟s ability to devote sufficient resources to research anddevelopment⑤Sony‟s ability to prioritize capi tal expenditure s, and the success Sony‟sjoint ventures and alliances.⑥Risks and uncertainties also include the impact of any future events withmaterial unforeseen impacts.7.The basic financial ratios of Sony from year 2002 to 2004From the above analysis and the table, we can see that:①The liquidity ratio and Acid-test ratio are in a year by year up-trend ,butcombining receivable turnover and inventory turnover, the increase is mainly because of the increase of accounts receivable and the decrease of current liability.②The company accounts receivable turnover and inventory turnover are inup-trend ,this shows that Sony do well in accounts receivable and inventory, so its debt-repay ability and profit abilities will be in advantages.③Its debt ratio is decreasing year by year, so we can see that Sony will have a low financial leverage, its financial environment will be good for its operating④Also, from analysis of the table, Sony‟s consolidated sales, operating income, income before taxes, and net income are expected to decrease compared with the fiscal year ended March 31, 2004. While we assume that the yen for the fiscal year ending March 31, 2005 will strengthen against the U.S. dollar andwill weaken against the euro⑤Sony‟s inve stments are comprised of debt and equity securities accounted for under both the cost and equity method of accounting. If it has been determined that an investment has sustained an other-than-temporary decline in its value, the investment is written down to its fair value by a charge to earnings.五.Analysis of Sony’s abilitiesThe ability to meet the obligation1.①. From the current ratio, we see that the situation is not good for Sony corporation. Because the median current ratio for the industry is 2.1, but those of Sony is less than this obviously.②. But if we look at the quick r atio, we will find it‟s very good: the industry median quick ratio is 1.1, and those of Sony are very near to it.This is because Sony has not as much inventories as other corporations. Then we can see that the ability of Sony to meet short-term obligations is good.For long-term obligations①. The debt ratios are lager than 50%, which indicates that Sony borrows alarge amount of money. Its evidenced by the increasing amount of interest payment.②. Its interest coverage ratios are obviously less than the median of that forthe industry which is 4.0.Then we can see that Sony’s ability to meet the long-term obligations is not good.2. Assets management analysisFirst, the receivable turnovers are obviously less than the median of 8.1for the industry, which tells us that Sony‟s receivables are considerably slower in turning over than is typical for the industry.Second, the inventory turnovers are higher than the median of 3.3 for the industry, which shows Sony has a good inventory management. This is because that inventory is a small portion of assetsThird, the total asset turnovers are obviously less than the median of 1.66 for the industry. So it is clear that Sony generates less sales revenue per dollar of asset investment than does the industry.So Sony’s assets management is not good enough3. Profitability analysis①Sony‟s gross profit margin is above the median of 23.8 percent for theindustry, indicating that it is relatively more effective at producing and selling products above cost.②But comparing to the median ROI value of 7.8% and the median ROEvalue of 14.04%, those of Sony are very poor. And this means that it employs more assets and equity to generate a dollar of profit than does the typical firm in the industry.4. Accounts receivable securitization programIn the United States of America, Sony set up an accounts receivable securitization program whereby Sony can sell interests in up to $900 million of eligible trade accounts receivable, as defined. Through this program, Sony can securitize and sell a percentage of undivided interest in that pool of receivables to several multi-seller commercial paper conduits owned and operated by banks. Sony can sell receivables in which the agreed upon original due dates are no more than 90 days. after the invoice dates. The value assigned to undivided interests retained in securitized trade receivables is based on the relative fair values of the interest retained and sold in the securitization. Sony has assumed that the fair value of the retained interest is equivalent to its carrying value as the receivables are short-term in nature, high quality and have appropriate reserves for bad debt incidence. There was no sale of receivables for the fiscal year endedMarch 31, 2003. Losses from these transactions were insignificant.5. EPS attributable to common stock:Reconciliation of the differences between basic and diluted EPS for the years ended March 31, 2002, 2003 and 2004 is as follows:As discussed in Note 2, the earnings allocated to the subsidiary tracking stock are determined based on the subsidiary tracking stockholders‟economic interest.The statutory retained earnings of SCN (the subsidiary tracking stock entity as discussed in Note 15) available for dividends to the shareholders were ¥209 million as of March 31, 2002, which decreased by ¥374 million during the year ended March 31, 2002 after the date of issuance. The accumulated losses of SCN were ¥779 million and ¥1,764 million ($17 million) as of March 31, 2003and 2004, respectively.For the year ended March 31, 2002, 75,201 thousand shares of potential common stock upon the conversion of convertible bonds were excluded from the computation of diluted EPS due to their anti-dilutive effect. 44,603 thousand shares of potential common stock upon the conversion of ¥250,000 million convertible bond issued dated December 18, 2003 were excluded from the computation of the number of weighted-average shares for diluted EPSPotential common stock upon the exercise of warrants and stock acquisition rights, which were excluded from the computation of diluted EPS since they have an exercise price in excess of the average market value of Sony‟s common stock during the fiscal year, were 2,665 thousandshares, 4,141 thousand shares, and 6,796 thousand shares for the years ended March 31, 2002, 2003 and 2004, respectively.Warrants and stock acquisition rights of subsidiary tracking stock for the years ended March 31, 2002,2003 and 2004, which have a potentially dilutive effect by decreasing net income allocated to common stock, were excluded from the computation of diluted EPS since they did not have a dilutive effectStock options issued by affiliated companies accounted for under the equity method for the years endedMarch 31, 2002, 2003 and 2004, which have a potentially dilutive effect by decreasing net income allocated to common stock, were excluded from the computation of diluted EPS since such stock options did not have a dilutive effect.On October 1, 2002, Sony implemented a share exchange as a result of which Aiwa became a wholly-owned subsidiary. As a result of this share exchange, Sony issued 2,502 thousand shares. The shares were included in the computation of basic and diluted EPS.6. P/E ratioLet‟s see the three year‟s data of P/E RatioWe can see that the P/E ratios are large, and if we invest on it, we will need many years to get back our money. So it‟s not good to invest on it. 六. Do Pont analysis1. Here I‟d like to analysis the effects of all kinds of items, such as …Return oftotal assets‟ and …Equity multiplier‟, to ROE.Then, based on thecontributions of the items, we try to find ways to improve the ROE.At the first glance of the table, you will obverse there is so great difference between the ROE of 2002 and the other two year. ---So I decide to analysis that one for example the decrease of the ROE in year 2002 is primarily because of the decrease of other income, increase of costs and expenses and other expenses.Let us go to the “income statement” to see the details------From the …income statement‟ behind,(1)we can see that the decrease of …other income‟ is primarily because of the decreaseof …foreign exchange gain‟ and decrease of …marketable security and security sales‟.The news behind has shown that the foreign exchange rate has changed so much that the foreign exchange risk is so high ,and the economics in Japanese has fallen down.It is may be one of the reasons of the decrease of …foreign exchange gain‟中新网香港1月23日消息:尽管亚洲国家对日元继续贬值表示关注,但美国财政部长奥尼尔与日本财务大臣盐川正十郎进行会谈后表态,外汇汇率应由市场决定。