会计学原理的英文

大学课程英文名

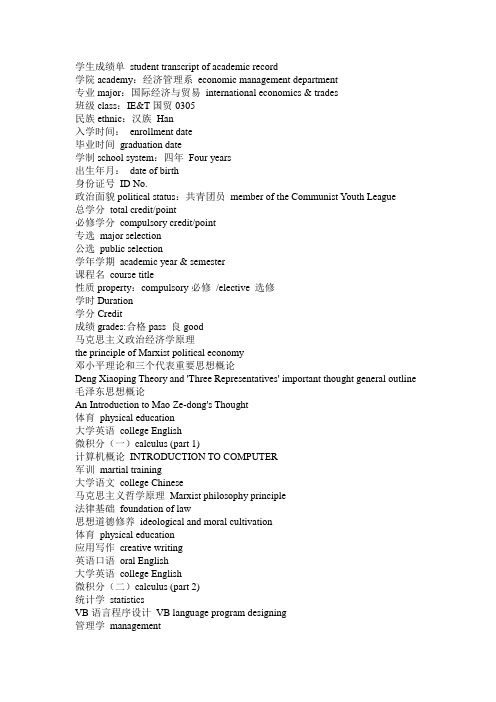

学生成绩单student transcript of academic record学院academy:经济管理系economic management department专业major:国际经济与贸易international economics & trades班级class:IE&T国贸0305民族ethnic:汉族Han入学时间:enrollment date毕业时间graduation date学制school system:四年Four years出生年月:date of birth身份证号ID No.政治面貌political status:共青团员member of the Communist Y outh League总学分total credit/point必修学分compulsory credit/point专选major selection公选public selection学年学期academic year & semester课程名course title性质property:compulsory必修/elective 选修学时Duration学分Credit成绩grades:合格pass 良good马克思主义政治经济学原理the principle of Marxist political economy邓小平理论和三个代表重要思想概论Deng Xiaoping Theory and 'Three Representatives' important thought general outline 毛泽东思想概论An Introduction to Mao Ze-dong's Thought体育physical education大学英语college English微积分(一)calculus (part 1)计算机概论INTRODUCTION TO COMPUTER军训martial training大学语文college Chinese马克思主义哲学原理Marxist philosophy principle法律基础foundation of law思想道德修养ideological and moral cultivation体育physical education应用写作creative writing英语口语oral English大学英语college English微积分(二)calculus (part 2)统计学statisticsVB语言程序设计VB language program designing管理学management市场营销marketing微观经济学microeconomics经济法economic law体育physical education英语口语oral English大学英语college English概率论与数理统计probability theory and mathematical statistics 线性代数linear algebra数据库及其应用database and application(VFP)会计学原理principles of accounting宏观经济学macroeconomics国际贸易international trade财政学finance金融学treasury税法taxation law当代世界经济与政治contemporary world economy and politics 体育physical education英语口语oral English大学英语college English管理信息系统management information system国际贸易实务international trade affairs海关实务customs affairs世界经济地理world economic geography国际金融international finance国际商贸英语会话international business English session英语精读English intensive reading财务管理financial management国际市场营销international marketing电子商务e-commerce影视作品欣赏films appreciation国际经济学international economics国际技术贸易international technology trade国际结算international settlement国际市场调研international market research国际投资international investment国际商法international commercial law国际商贸英语会话international business English session外贸函电foreign trade correspondence英语精读English intensive reading市场预测与决策market forecast & decision网络营销network marketing国际服务贸易international service trade中国对外经贸专题China foreign trades thematic银行业务与管理banking and management高级经贸英语文选读译advanced trade English reading & translation 商务谈判business negotiation学年论文academic year thesis毕业论文graduation thesis。

会计学原理英文版21版答案

会计学原理英文版21版答案【篇一:19版《会计学原理》会计英语双语词汇怀尔德】=txt>会计术语accounting; account; accountant; cpa, cma, cia, cb, cfe; financial accounting; managerial accounting; auditor; internal control; financial management; bookkeeping recordkeeping;会计;账户;会计师;注册会计师,注册管理会计师,注册内部审计师,注册簿记员,注册舞弊检查员;财务会计,管理会计,审计员,内部控制;财务管理;记账;记录;rd, research development; hr human resource; distribution; logistics; marketing; not-for-profit organization; shareholder; stakeholder; lender; creditor; debtors; supplier; customer; regulator; legislator; board of director; broker; mortgage; wholesaler, retailer; merchandiser; manufacturer; services; consignor; consignee; entrepreneur, entrepreneurship; sole proprietorship; partnership; corporation; common stock or ordinary share; preferred stock or preference share; corporate governance system; limited company; soe:state-owned enterprise; sme: small and medium sized enterprise;研发、研发、人力资源;分配;物流;销售;非营利组织;股东;利益相关者;出借人;债权人,债务人;供应商;客户;监管;立法;董事会;代理;抵押贷款;批发商、零售商,推销商,制造商,服务,发货人,收货人,企业家,企业家能力;个人独资,合伙企业;企业;普通股或普通股,优先股或优先股;公司治理系统;有限公司;国有企业,中小企业,financial statement; financial report; footnotes to financial statement; interim financial statement; annual, semiannually, quarterly, monthly financial statement; balance sheet; income statemen t; cash flow statement; statement of owner’s equity; classified financial statement; pro forma financial statements; unadjusted trialbalance; adjusted trial balance; post-closing trial balance; book; journal; ledger; general journal; specific journal; general ledger; subsidiary ledger; chart of accounts; double-entry accounting; working papers; work sheet; 财务报表、财务报告、财务报表附注;中期财务报表,年度,每半年、季度、月度财务报表,资产负债表,损益表,现金流量表,所有者权益表;财务报表分类;形式上的财务报表;调整前试算表,调整后试算表,结帐后试算表;账簿;日记账;分类账;一般日记账;特定日记账,总账、明细分类帐;会计科目表;复式会计;工作底稿;工作表;accounting ethics; accounting fraud, scandal; bogus accounting report; accounting oversight; stringent internal control; accounting principle, assumption, and standard;social responsibility; fasb, gaap, sec, iasb, ifrs; general principle, specific principles; cash basis accounting; accrual basis accounting; cost principle; revenue reorganization principle; matching principle; materiality constraint (cost-to-benefit constraint); full disclosure principle; going-concern assumption; monetary unit assumption; time period assumption (periodicityassumption) ; business entity assumption; consistency concept; conservatism constraint; lower of cost or market; lifo conformity rule;会计道德;会计欺诈,丑闻,虚假的会计报告;会计监督;严格的内部控制,会计原则,假设,和标准;社会责任;财务会计准则委员会,公认会计准则,证券交易委员会,国际会计准则委员会,国际财务报告准则;一般原则,具体原则;收付实现制;权责发生制会计;成本原则;收入确认原则,配比原则;物质性约束(效益成本约束);全面披露原则,持续经营假设;货币计量假设;会计分期假设(周期性假设);会计主体假设;一致性概念;保守主义约束;降低成本或市场;后进先出一致性规则;accounting cycle; operating cycle; accounting documents; source documents; sales tickets; checks; purchase orders; bills; invoice; cash register; money and any medium of exchange; deposit; money orders; promissory note; written promise; asset; tangible asset; intangible asset; liability; owner’s equity; revenue; expense; profit; current asset; non-current asset; fixed asset; plant and equipment; cash discount; cost of goods sold; credit memorandum; credit period; credit terms; debit memorandum; discount period; eom (end of month); fobshipping point; fob destination; general and administrative expenses; gross margin; inventory; list price; multiple-step income statement; periodic inventory system; perpetual inventory system; purchase return and allowance; shrinkage; supplementary records; trade discount; damage and loss intransit; transportation-in, transportation-out; itemized cost; physical count; deterioration;会计循环;营业周期;会计凭证;原始凭证;销售票据,检查,采购订单,账单;发票;收银台;金钱和任何交换的媒介,存款,汇票,本票,书面承诺;资产,有形资产,无形资产,负债,所有者权益,收入,费用,利润,流动资产、非流动资产、固定资产、厂房和设备,现金折扣,销货成本;信用证 ;信贷时期,信贷条件;借项通知单;折扣期间,月末;寄发地交货,目的地交货;一般及行政费用,毛利;存货;定价;多级损益表;定期盘存制;永续盘存制;回购和津贴;损失;补充记录;商业折扣,伤亡和损失在运输过程中,运入运费,运出运费;会计成本;实物盘点;衰退;t-account; contra account; permanent accounts; temporary accounts; transaction and event; what-if or proposed transaction; liquidation; net income or loss; income summary; sale on credit, sale on account; receivables; payables; capital; supplies; notes payable; accumulated depreciation; straight-line depreciation; reduced balance depreciation; withdrawal; deferral; accruals; deferred expenses or revenues; accrued expenses or revenues; working capital; beginning balance; ending balance, end-of-period balance; normal balance; opposite normal balance; short-term, long-term; point of time, period of time; prior period; fiscal year, 12 consecutive months or 52 weeks; calendar year; natural business year; closing entries; prepaid account; premium; journal entry; year-end adjusting entry; posting reference column; unearned revenue;丁字式帐户;抵销帐户;永久账户;临时账户,交易和事件,提出假设或事务;清算;净利润或损失;收益汇总;赊销,赊销;应收,应付款;资本;物料;应付票据,累计折旧;直线折旧,余额递减折旧;撤资;延迟;权责发生额;递延费用或收入;应计费用或收入,营运资本,期初余额,期末余额,期末余额;正常平衡;相反的正常平衡,短期、长期,时点,时期,前期;财政年度,连续12个月或52周,历年;自然年;结帐分录;预付帐户;溢价;日记账分录,年终调整分录;过账备查账,预收收入;business decision; lending decision; investment; return; financing; cost of capital; dividend; bonus; principal amount; interest rate; book value; historical value; residual value; salvage value; amount; pro rata basis; gift card; gift certificate; coupon; premium; salary; wage; pension; welfare; interest; vacation, vocation; carton, cartoon; patent; trademarks; copyrights; franchise; goodwill; licensing agreement; inflation;deflation; goods in transit; goods on consignment; goods damaged or obsolete (deteriorate) ; goods work-in-progress; incidental cost; inventory costing method; physical flow of goods and cost flow of inventory; cost in or out of inventory; specific identification; first-in, first-out; last-in, first-out; weighted average;商业决策;贷款决策;投资;回报;融资;资本成本;股息,红利,本金;利率;账面价值;历史价值;残值;残值;数量;按比例;礼品卡;礼券,礼券,奖金;工资,工资,养老金;福利;利息;假期,假期,纸箱,卡通,专利,商标,版权,特许经营;商誉;许可协议;通货膨胀,通货紧缩,货物在运输途中,货物托运;货物损坏或过时(恶化),货物在制品;杂项费用,存货成本核算方法;商品实质流程和存货成本流;成本或库存,具体识别;先进,先进先出,后进先出,加权平均,,identify; record; classify; communicate; analyze; interpret; prepare financial statement (trial balance); present; manipulate; disclose; withdraw; own; owe; yield; prescribe; summarize; journalize; post; credit; debit;understate; overstate; adjust; defer; subtract; add; multiply; divide; transfer; update; come due; smooth out changes in cost; match cost with revenue;识别、记录、分类;沟通;分析;解释;准备财务报表(试);现在,操纵;披露;撤资;自己所有的;欠;产量;规定;总结;记日记账;宣布;贷方;借方;低估;高估;调整;推迟;减少;增加;乘;分化;转移;更新;到期;平滑变化成本;成本与收入匹配;financial management terms财务管理方面part a-chapter 1 部分一章1financial accounting, managerial accounting, and financial management财务会计、管理会计和财务管理investment decision, financing decision, and dividenddecision投资决策、融资决策和股利决策enterprise, company, firm, business, proprietorship, partnership, corporation企业、公司、公司、企业,独资企业,合伙企业,公司listed company or quoted company上市公司或上市公司stock exchange listing regulation证券交易所上市的监管voluntary and not-for-profit organization, economy, effectiveness and efficiency自愿和非营利性组织、经济、有效性和效率corporate strategy and financial strategy公司战略和财务战略accounting principle, rules, standards, and assumptions会计原则、规则、标准和假设going-concern basis, accounting period, accounting entity, and stable monetary unit assumption持续经营基础上,会计期间、会计主体和稳定货币单位的假设monetary and non-monetary measures货币和非货币性的措施financial statement and financial report财务报表和财务报告balance sheet or statement of financial position资产负债表或财务状况的声明income statement, cash flow statement, and statement of owner’s equity损益表、现金流量表和所有者权益的声明financial objectives or targets财务目标或目标identification and formulation of objectives识别和制定目标the welfare of employee, of management, of society员工的福利,社会的管理the fulfillment of responsibility towards customers and suppliers实现对客户和供应商的责任shareholders’ wealth maximization股东财富最大化profitability, growth, customer satisfaction盈利能力、增长、客户满意度financial achievement财务成果actual performance and forecast performance实际性能和预测性能disproportionate to true worth不成比例的真实价值drawback, advantage, disadvantage, shortcoming缺点,优点,缺点,缺点agency relationship, goal congruence代理关系,目标一致corporate governance, internal control, and risk management公司治理、内部控制和风险管理reward scheme, performance-related pay, extrinsic andintrinsic rewards奖励计划,绩效工资,外在和内在的回报accountability, good supervision,问责,监督好,remuneration committee, nomination committee, independent non-executive director薪酬委员会、提名委员会、独立非执行董事accountant and auditor会计和审计shareholder or stockholder, and stakeholder, creditor anddebt holder股东或股东和利益相关者,债权人和债务持有人employees, directors; managers, pensioners, shareholders, debt holders, investors, customers, bankers, suppliers, competitors, government, pressure groups, local and national communities, professional and regulatory bodies雇员、董事、管理人员、退休人员、股东、债权人、投资者、客户、银行家、供应商、竞争对手、政府、压力团体,地方和全国社区、专业和监管机构securities, bond, stock, loan, bank overdraft, saving, debenture, treasury, accounts receivable,证券,债券,股票,贷款,银行透支,储蓄、债券、财政部、应收帐款、working capital, shareholders’ fund or equity营运资本,股东的基金或股票input, output, yield, product, production, productivity,输入、输出、产量、产品、生产、生产力、asset, liabilities, owners’ equity, revenue, expense profit资产、负债、所有者权益、收入、费用利润current asset, accounts receivable, inventory流动资产、应收帐款、库存non-current asset, plant and equipment, fixed asset非流动资产,厂房和设备,固定资产volume of investment, risk and return of investment的投资,投资的风险和回报short-term, medium-term, long-term funds, shortfall in fund 短期、中期、长期的基金,基金缺口net present value, book value, market value, added value, nominal value and real value 净现值、账面价值、市场价值,附加价值,名义价值和实际价值benefit, gain, interest, dividend, earnings, retained earnings, profit retention利益,收益,利息、股息、获利、留存收益、利润保留ordinary share, preference share普通股、优先股business risk and financial risk商业风险和金融风险accounting profit and economic profit会计利润和经济利润manipulation of profit操纵利润capitalization资本化ratio, index, indicator, variables比率指标,指标变量bad debt, depreciation坏账、折旧cost of goods sold销货成本provision for depreciation or anticipated losses折旧准备或预期的损失overhead cost, development cost, and various expenses间接成本、开发成本和各种费用administration or selling and distribution expenses【篇二:会计学原理试题及答案(很全)】>一、判断题(对的写t,错的写f。

会计学原理英文12PPT课件

Type of Investment

Trading Securities

Securities Available for

Sale

Definition

Actively traded for potential profit. Not actively

traded, held for investment returns.

recorded at cost.

Investment carrying amount is adjusted to current market value.

Unrealized holding gains and losses are

recorded.

12-7

Classifying Passive Stock Investments

12-4

Investments in Stock for Control

Investments made with the intent to exert control over another corporation.

The investing company has the ability to determine the operating and financial policies of another corporation.

The ability of the investing company to

have an important impact on the operating and

financial policies of another company.

Significant Influence 20% - 50% outstanding shares

会计学原理英文课件 (1)

1-7

C4

Generally Accepted Accounting Principles (GAAP)

Financial accounting is governed by concepts and rules known as generally accepted accounting principles (GAAP). GAAP aims to make information relevant, reliable, and comparable.

1-8

C3

Fraud Triangle

Three factors must exist for a person to commit fraud: opportunity, pressure, and rationalization.

Envision a way to commit fraud with a low perceived risk of getting caught

1-6

C3

Ethics – A Key Concept

The goal of accounting is to provide useful information for decisions. For information to be useful, it must be trusted. This demands ethics in accounting. Ethics are beliefs that distinguish right from wrong. They are accepted standards of good and bad behavior.

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

会计学原理英文课件 (11)

11-3

LO 1

What Is a Current Liability?

Question

To be classified as a current liability, a debt must be expected to be paid within: a. one year. b. the operating cycle. c. 2 years.

Cash Sales Revenue Sales Tax Payable

10,600 10,000 600

11-10

LO 1

Sales Taxes Payable

Sometimes companies do not enter sales taxes separately in the cash register. Illustration: Cooley Grocery enters total receipts of $10,600. Because the amount received from the sale is equal to the sales price 100% plus 6% of sales, (sales tax rate of 6%), the journal entry is:

11-1

11

1 2 3

Current Liabilities and Payroll Accounting

Learning Objectives

Explain how to account for current liabilities. Discuss how current liabilities are reported and analyzed. Explain how to account for payroll.

会计学原理23版 英文版课件Wild_FAP23e_Ch12_PPT_091117

800 800

11 Learning Objective P1: Prepare entries for partnership formation.

Learning Objective P2:

Allocate and record income and loss among partners.

Accounting for Partnerships

Chapter 12

Wild, Shaw, and Chiappetta Fundamental Accounting Principles 23rd Edition

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

H. Perez, Capital 10,000

• Protects innocent partners from malpractice or negligence claims.

• Most states hold all partners personally liable for partnership debts.

Learning Objective C1: Identify characteristics of partnerships and similar organizations.

their shares of net income (or net loss) when closing the accounts at the end of the period. 3. Each partner’s withdrawal account is closed to that partner’s capital account. Separate capital and withdrawals accounts are kept for each partner.

会计学原理英文课件 (13)

13 - 8

C1

Basics of Capital Stock

Total amount of stock that a corporation’s charter authorizes it to sell.

Stockholders' Equity Common Stock, par value $.01; authorized 250,000,000 shares; issued and outstanding 92,556,295 shares

13 - 1

Accounting for Corporations

Chapter 13

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CP., CPA

Issued 100,000 shares of common stock.

Dr 2,500,000

Cr 200,000 2,300,000

13 - 11

P1

Issuing Par Value Stock

Stockholders' Equity with Common Stock

Stockholders' Equity Common Stock - $2 par value; 500,000 shares authorized; 100,000 shares issued and outstanding $ 200,000 Paid-In Capital in Excess of Par 2,300,000 Retained earnings 650,000 Total stockholders' equity $ 3,150,000

会计学原理英文课件 (23)

23-5

LO 1

The Benefits of Budgeting

Question

Which of the following is not a benefit of budgeting? a. b. c. d. Management can plan ahead. An early warning system is provided for potential problems. It enables disciplinary action to be taken at every level of responsibility. The coordination of activities is facilitated.

u

Primary method of communicating agreed-upon objectives throughout the organization. Promotes efficiency. Control device - important basis for performance evaluation once adopted.

u

Long enough to provide an attainable goal and minimize seasonal or cyclical fluctuations. Short enough for reliable estimates.

u

23-8

LO 1

Businesses Often Feel Too Busy to Plan for the Future A study by Willard & Shullman Group Ltd. Found that fewer than 14% of businesses with less than 500 employees do an annual budget or have a written business plan. For many small businesses, the basic assumption is that, “As long as I sell as much as I can, and keep my employees paid, I’m doing OK.” A few small business owners even say that they see no need for budgeting and planning. Most small business owners, though, say that they understand that budgeting and planning are critical for survival and growth. But given the long hours that they already work addressing day-to-day challenges, they also say that they are “just too busy to plan for the future.”

会计学原理英文版一单元习题

1. Accounting is an information and measurement system that identifies, records, and communicates relevant, reliable, and comparable information about an organization's business activities.2. Bookkeeping is the recording of transactions and events and is only part of accounting.3. An accounting information system communicates data to help businesses make better decisions.4. Managerial accounting is the area of accounting that provides internal reports to assist the decision making needs of internal users.5. Internal operating activities include research and development, distribution, and human resources.6. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze and interpret an organization's activities.7. External auditors examine financial statements to verify that they are prepared according to generally accepted accounting principles.8. External users include lenders, shareholders, customers, and regulators.9. Regulators often have legal authority over certain activities of organizations.10. Internal users include lenders, shareholders, brokers and managers.11. Opportunities in accounting include auditing, consulting, market research, and tax planning.12. Identifying the proper ethical path is easy.13. The Sarbanes-Oxley Act (SOX) requires each issuer of securities to disclose whether is has adopted a code of ethics for its senior financial officers and the contents of that code.14. The fraud triangle asserts that there are three factors that must exist for a person to commit fraud; these factors are opportunity, pressure, and rationalization.15. The Sarbanes-Oxley Act (SOX) does not require public companies to apply both accounting oversight and stringent internal controls.16. A partnership is a business owned by two or more people.17. Owners of a corporation are called shareholders or stockholders.18. In the partnership form of business, the owners are called stockholders.19. The balance sheet shows a company’s net income or loss due to earnings activities over a period of time.20. The Financial Accounting Standards Board is the private group that sets both broad and specific accounting principles.21. The business entity principle means that a business will continue operating for an indefinite period of time.22. Generally accepted accounting principles are the basic assumptions, concepts, and guidelines for preparing financial statements.23. The business entity assumption means that a business is accounted for separately from other business entities, including its owner or owners.24. As a general rule, revenues should not be recognized in the accounting records until it is received in cash.25. Specific accounting principles are basic assumptions, concepts, and guidelines for preparing financial statements and arise out of long-used accounting practice.26. General accounting principles arise from long-used accounting practices.27. A sole proprietorship is a business owned by one or more persons.28. Unlimited liability is an advantage of a sole proprietorship.29. Understanding generally accepted accounting principles is not necessary to use and interpret financial statements.30. The International Accounting Standards board (IASB) has the authority to impose its standards on companies around the world.31. Objectivity means that financial information is supported by independent unbiased evidence.32. The idea that a business will continue to operate instead of being closed or sold underlies the going-concern assumption.33. According to the cost principle, it is preferable for managers to report an estimate of an asset's value.34. The monetary unit assumption means that all international transactions must be expressed in dollars.35. The International Accounting Standards Board (IASB) is the government group that establishes reporting requirements for companies that issue stock to the public. 36. A limited liability company offers the limited liability of a partnership or proprietorship and the tax treatment of a corporation.37. The Securities and Exchange Commission (SEC) is a government agency that has legal authority to establish GAAP.38. The three common forms of business ownership include sole proprietorship, partnership, and non-profit.39. The three major types of business activities are operating, financing, and investing.40. Planning is defining an organization's ideas, goals, and actions.41. Strategic management is the process of determining the right mix of operating activities for the type of organization, its plans, and its markets.42. Planning activities are the means an organization uses to pay for resources like land, buildings, and equipment to carry out its plans.43. Investing activities are the acquiring and disposing of resources that an organization uses to acquire and sell its products or services.44. Owner financing refers to resources contributed by creditors or lenders.45. Revenues are increases in equity from a company's earning activities.46. A net loss occurs when revenues exceed expenses.47. Net income occurs when revenues exceed expenses.48. Liabilities are the owner's claim on assets.49. Assets are the resources of a company and are expected to yield future benefits.50. Owner’s withdrawals are expenses.51. The accounting equation can be restated as: Assets - Equity = Liabilities.52. The accounting equation implies that: Assets + Liabilities = Equity.53. Owner's investments are increases in equity from a company's earnings activities.54. Every business transaction leaves the accounting equation in balance.55. An external transaction is an exchange of value within an organization.56. From an accounting perspective, an event is a happening that affects the accounting equation, but cannot be measured.57. Owner's equity is increased when cash is received from customers in payment of previously recorded accounts receivable.58. An owner's investment in a business always creates an asset (cash), a liability (note payable), and owner's equity (investment.)59. Return on assets is often stated in ratio form as the amount of average total assets divided by income.60. Return on assets is also known as return on investment.61. Return on assets is useful to decision makers for evaluating management, analyzing and forecasting profits, and in planning activities.62.Arrow’s net income of $117 million and average assets of $1,400 million results in a return on assets of 8.36%.63. Return on assets reflects the effectiveness of a company’s ability to generate profit through productive use of its assets.64. Risk is the uncertainty about the return we expect to earn.65. Generally the lower the risk, the lower the return that can be expected.66. U. S. Government Treasury bonds provide high return and low risk to investors.67. The four basic financial statements include the balance sheet, income statement, statement of owner's equity, and statement of cash flows.68. An income statement reports on investing and financing activities.69. A balance sheet covers a period of time such as a month or year.70. The income statement displays revenues earned and expenses incurred over a specified period of time due to earnings activities.71. The statement of cash flows shows the net effect of revenues and expenses for a reporting period.72. The income statement shows the financial position of a business on a specific date.73. The first section of the income statement reports cash flows from operating activities.74. The balance sheet is based on the accounting equation.75. Investing activities involve the buying and selling of assets such as land and equipment that are held for long-term use in the business.76. Operating activities include long-term borrowing and repaying cash from lenders, and cash investments or withdrawals by the owner.77. The purchase of supplies appears on the statement of cash flows as an investing activity because it involves the purchase of assets.78. The income statement reports on operating activities at a point in time.79. The statement of cash flows identifies cash flows separated into operating, investing, and financing activities over a period of time.80. Ending capital reported on the statement of owner’s equity is calculated by adding owner investments and net losses and subtracting net incomes and withdrawals. Multiple Choice Questions81. Accounting is an information and measurement system that does all of the following except:A. Identifies business activities.B. Records business activities.C. Communicates business activities.D. Does not use technology to improve accuracy in reporting.E. Helps people make better decisions.82. Technology:A. Has replaced accounting.B. Has not changed the work that accountants do.C. Has closely linked accounting with consulting, planning, and other financial services.D. In accounting has replaced the need for decision makers.E. In accounting is only available to large corporations.83.The primary objective of financial accounting is:A. To serve the decision-making needs of internal users.B. To provide financial statements to help external users analyze an organization's activities.C. To monitor and control company activities.D. To provide information on both the costs and benefits of looking after products and services.E. To know what, when, and how much to produce.84.The area of accounting aimed at serving the decision making needs of internal users is:A. Financial accounting.B. Managerial accounting.C. External auditing.D. SEC reporting.E. Bookkeeping.85.External users of accounting information include all of the following except:A. Shareholders.B. Customers.C. Purchasing managers.D. Government regulators.E. Creditors.86. All of the following regarding a Certified Public Accountant are true except:A. Must meet education and experience requirements.B. Must pass an examination.C. Must exhibit ethical character.D. May also be a Certified Management Accountant.E. Cannot hold any certificate other than a CPA.87. Ethical behavior requires:A. That auditors' pay not depend on the success of the client's business.B. Auditors to invest in businesses they audit.C. Analysts to report information favorable to their companies.D. Managers to use accounting information to benefit themselves.E. That auditors' pay depend on the success of the client's business.88. Social responsibility:A. Is a concern for the impact of our actions on society.B. Is a code that helps in dealing with confidential information.C. Is required by the SEC.D. Requires that all businesses conduct social audits.E. Is limited to large companies.89. All of the following are true regarding ethics except:A. Ethics are beliefs that separate right from wrong.B. Ethics rules are often set for CPAs.C. Ethics do not affect the operations or outcome of a company.D. Are critical in accounting.E. Ethics can be hard to apply.90. The accounting concept that requires financial statement information to be supported by independent, unbiased evidence other than someone's belief or opinion is:A. Business entity assumption.B. Monetary unit assumption.C. Going-concern assumption.D. Time-period assumption.E. Objectivity91. A corporation:A. Is a business legally separate from its owners.B. Is controlled by the FASB.C. Has shareholders who have unlimited liability for the acts of the corporation.D. Is the same as a limited liability partnership.E. Is not subject to double taxation.92. The group that attempts to create more harmony among the accounting practices of different countries is the:A. AICPA.B. IASB.C. CAP.D. SEC.E. FASB.93. The private group that currently has the authority to establish generally accepted accounting principles in the United States is the:A. APB.B. FASB.C. AAA.D. AICPA.E. SEC.94. The accounting assumption that requires every business to be accounted for separately from other business entities, including its owner or owners is known as the:A. Time-period assumption.B. Business entity assumption.C. Going-concern assumption.D. Revenue recognition principle.E. Cost principle.95. The rule that requires financial statements to reflect the assumption that the business will continue operating instead of being closed or sold, unless evidence shows that it will not continue, is the:A. Going-concern assumption.B. Business entity assumption.C. Objectivity principle.D. Cost Principle.E. Monetary unit assumption.96. If a parcel of land that was originally acquired for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land should be recorded in the purchaser's books at:A. $95,000.B. $137,000.C. $138,500.D. $140,000.E. $150,000.97. To include the personal assets and transactions of a business's owner in the records and reports of the business would be in conflict with the:A. Objectivity principle.B. Monetary unit assumption.C. Business entity assumption.D. Going-concern assumption.E. Revenue recognition principle.98. The accounting principle that requires accounting information to be based on actual cost and requires assets and services to be recorded initially at the cash orcash-equivalent amount given in exchange, is the:A. Accounting equation.B. Cost principle.C. Going-concern assumption.D. Realization principle.E. Business entity assumption.99. The rule that (1) requires revenue to be recognized at the time it is earned, (2) allows the inflow of assets associated with revenue to be in a form other than cash, and (3) measures the amount of revenue as the cash plus the cash equivalent value of any noncash assets received from customers in exchange for goods or services, is called the:A. Going-concern assumption.B. Cost principle.C. Revenue recognition principle.D. Objectivity principle.E. Business entity assumption.100. The question of when revenue should be recognized on the income statement (according to GAAP) is addressed by the:A. Revenue recognition principle.B. Going-concern assumption.C. Objectivity principle.D. Business entity assumption.E. Cost principle.101. The International Accounting Standards Board (IASB):A. Hopes to create harmony among accounting practices of different countries.B. Is the government group that establishes reporting requirements for companies that issue stock to the public.C. Has the authority to impose its standards on companies.D. Is the only source of generally accepted accounting principles (GAAP).E. Only applies to companies that are members of the European Union.102. The Maxim Company acquired a building for $500,000. Maxim had the building appraised, and found that the building was easily worth $575,000. The seller had paid $300,000 for the building 6 years ago. Which accounting principle would require Maxim to record the building on its records at $500,000?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Revenue recognition principle.103. On December 15 of the current year, Myers Legal Services signed a $50,000 contract with a client to provide legal services to the client in the following year. Which accounting principle would require Myers Legal Services to record the legal fees revenue in the following year and not the year the cash was received?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Revenue recognition principle.104. Marian Mosely is the owner of Mosely Accounting Services. Which accounting principle requires Marian to keep her personal financial information separate from the financial information of Mosely Accounting Services?A. Monetary unit assumption.B. Going-concern assumption.C. Cost principle.D. Business entity assumption.E. Matching principle.105. A limited partnership:A. Includes a general partner with unlimited liability.B. Is subject to double taxation.C. Has owners called stockholders.D. Is the same as a corporation.E. May only have two partners.106. A partnership:A. Is also called a sole proprietorship.B. Has unlimited liability for its partners.C. Has to have a written agreement in order to be legal.D. Is a legal organization separate from its owners.E. Has owners called shareholders.107. Which of the following accounting principles would require that all goods and services purchased be recorded at cost?A. Going-concern assumption.B. Matching principle.C. Cost principle.D. Business entity assumption.E. Consideration assumption.108. Which of the following accounting principles prescribes that a company record its expenses incurred to generate the revenue reported?A. Going-concern assumption.B. Matching principle.C. Cost principle.D. Business entity assumption.E. Consideration assumption.109. Revenue is properly recognized:A. When the customer's order is received.B. Only if the transaction creates an account receivable.C. At the end of the accounting period.D. Upon completion of the sale or when services have been performed and the business obtains the right to collect the sales price.E. When cash from a sale is received.110. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land account transaction amount to handle the sale of the land in the seller's books is:A. $85,000 increase.B. $85,000 decrease.C. $137,000 increase.D. $137,000 decrease.E. $140,000 decrease.111. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. What is the effect of the sale on the accounting equation for the seller?A. Assets increase $52,000; owner's equity increases $52,000.B. Assets increase $85,000; owner's equity increases $85,000.C. Assets increase $137,000; owner's equity increases $137,000.D. Assets increase $140,000; owner's equity increases $140,000.E. Assets decrease $85,000; owner's equity decreases $85,000.112. If a parcel of land that was originally purchased for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000. At the time of the sale, assume that the seller still owed $30,000 to TrustOne Bank on the land that was purchased for $85,000. Immediately after the sale, the seller paid off the loan to TrustOne Bank. What is the effect of the sale and the payoff of the loan on the accounting equation?A. Assets increase $52,000; owner's equity increases $22,000; liabilities decrease $30,000B. Assets increase $52,000; owner's equity increases $30,000; liabilities decrease $30,000C. Assets increase $22,000; owner's equity increases $52,000; liabilities decrease $30,000D. Assets decrease $30,000; owner's equity decreases $30,000; liabilities decrease $30,000E. Assets decrease $55,000; owner's equity decreases $55,000; liabilities decrease $30,000113. An example of a financing activity is:A. Buying office supplies.B. Obtaining a long-term loan.C. Buying office equipment.D. Selling inventory.E. Buying land.114. An example of an operating activity is:A. Paying wages.B. Purchasing office equipment.C. Borrowing money from a bank.D. Selling stock.E. Paying off a loan.115. Operating activities:A. Are the means organizations use to pay for resources like land, buildings and equipment.B. Involve using resources to research, develop, purchase, produce, distribute and market products and services.C. Involve acquiring and disposing of resources that a business uses to acquire and sell its products or services.D. Are also called asset management.E. Are also called strategic management.116. An example of an investing activity is:A. Paying wages of employees.B. Withdrawals by the owner.C. Purchase of land.D. Selling inventory.E. Contribution from owner.117. Net Income:A. Decreases equity.B. Represents the amount of assets owners put into a business.C. Equals assets minus liabilities.D. Is the excess of revenues over expenses.E. Represents owners' claims against assets.118. If equity is $300,000 and liabilities are $192,000, then assets equal:A. $108,000.B. $192,000.C. $300,000.D. $492,000.E. $792,000.119. Resources that are expected to yield future benefits are:A. Assets.B. Revenues.C. Liabilities.D. Owner's Equity.E. Expenses.120. Increases in equity from a company's earnings activities are:A. Assets.B. Revenues.C. Liabilities.D. Owner's Equity.E. Expenses.121. The difference between a company's assets and its liabilities, or net assets is:A. Net income.B. Expense.C. Equity.D. Revenue.E. Net loss.122. Creditors' claims on the assets of a company are called:A. Net losses.B. Expenses.C. Revenues.D. Equity.E. Liabilities.123. Decreases in equity that represent costs of assets or services used to earn revenues are called:A. Liabilities.B. Equity.C. Withdrawals.D. Expenses.E. Owner's Investment.124. The description of the relation between a company's assets, liabilities, and equity, which is expressed as Assets = Liabilities + Equity, is known as the:A. Income statement equation.B. Accounting equation.C. Business equation.D. Return on equity ratio.E. Net income.125. Revenues are:A. The same as net income.B. The excess of expenses over assets.C. Resources owned or controlled by a companyD. The increase in equity from a company’s earning activities.E. The costs of assets or services used.126. If assets are $99,000 and liabilities are $32,000, then equity equals:A. $32,000.B. $67,000.C. $99,000.D. $131,000.E. $198,000.127. Another name for equity is:A. Net income.B. Expenses.C. Net assets.D. Revenue.E. Net loss.128. The excess of expenses over revenues for a period is:A. Net assets.B. Equity.C. Net loss.D. Net income.E. A liability.129. A payment to an owner is called a(n):A. Liability.B. Withdrawal.C. Expense.D. Contribution.E. Investment.130. Distributions of assets by a business to its owners are called:A. Withdrawals.B. Expenses.C. Assets.D. Retained earnings.E. Net Income.131. The assets of a company total $700,000; the liabilities, $200,000. What are the claims of the owners?A. $900,000.B. $700,000.C. $500,000.D. $200,000.E. It is impossible to determine unless the amount of this owners' investment is known.132. On June 30 of the current year, the assets and liabilities of Phoenix, Inc. are as follows: Cash $20,500; Accounts Receivable, $7,250; Supplies, $650; Equipment, $12,000; Accounts Payable, $9,300. What is the amount of owner's equity as of June 30 of the current year?A. $8,300B. $13,050C. $20,500D. $31,100E. $40,400133. Assets created by selling goods and services on credit are:A. Accounts payable.B. Accounts receivable.C. Liabilities.D. Expenses.E. Equity.134. An exchange of value between two entities is called:A. The accounting equation.B. Recordkeeping or bookkeeping.C. An external transaction.D. An asset.E. Net Income.135. Photometer Company paid off $30,000 of its accounts payable in cash. What would be the effects of this transaction on the accounting equation?A. Assets, $30,000 increase; liabilities, no effect; equity, $30,000 increase.B. Assets, $30,000 decrease; liabilities, $30,000 decrease; equity, no effect.C. Assets, $30,000 decrease; liabilities, $30,000 increase; equity, no effect.D. Assets, no effect; liabilities, $30,000 decrease; equity, $30,000 increase.E. Assets, $30,000 decrease; liabilities, no effect; equity $30,000 decrease.136. How would the accounting equation of Boston Company be affected by the billing of a client for $10,000 of consulting work completed?A. +$10,000 accounts receivable, -$10,000 accounts payable.B. +$10,000 accounts receivable, +$10,000 accounts payable.C. +$10,000 accounts receivable, +$10,000 cash.D. +$10,000 accounts receivable, +$10,000 revenue.E. +$10,000 accounts receivable, -$10,000 revenue.137. Zion Company has assets of $600,000, liabilities of $250,000, and equity of $350,000. It buys office equipment on credit for $75,000. What would be the effects of this transaction on the accounting equation?A. Assets increase by $75,000 and expenses increase by $75,000.B. Assets increase by $75,000 and expenses decrease by $75,000.C. Liabilities increase by $75,000 and expenses decrease by $75,000.D. Assets decrease by $75,000 and expenses decrease by $75,000.E. Assets increase by $75,000 and liabilities increase by $75,000.138. Viscount Company collected $42,000 cash on its accounts receivable. The effects of this transaction as reflected in the accounting equation are:A. Total assets decrease and equity increases.B. Both total assets and total liabilities decrease.C. Total assets, total liabilities, and equity are unchanged.D. Both total assets and equity are unchanged and liabilities increase.E. Total assets increase and equity decreases.139. If the liabilities of a business increased $75,000 during a period of time and the owner's equity in the business decreased $30,000 during the same period, the assets of the business must have:A. Decreased $105,000.B. Decreased $45,000.C. Increased $30,000.D. Increased $45,000.E. Increased $105,000.140. If the assets of a business increased $89,000 during a period of time and its liabilities increased $67,000 during the same period, equity in the business must have:A. Increased $22,000.B. Decreased $22,000.C. Increased $89,000.D. Decreased $156,000.E. Increased $156,000.141. If the liabilities of a company increased $74,000 during a period of time and equity in the company decreased $19,000 during the same period, what was the effect on the assets?A. Assets would have increased $55,000.B. Assets would have decreased $55,000.C. Assets would have increased $19,000.D. Assets would have decreased $19,000.E. None of these.142. If a company paid $38,000 of its accounts payable in cash, what was the effect on the assets, liabilities, and equity?A. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would decrease $38,000.B. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would increase $38,000.C. Assets would decrease $38,000, liabilities would decrease $38,000, and equity would not change.D. There would be no effect on the accounts because the accounts are affected by the same amount.E. None of these.。

会计学原理-英文版-第21版--第一章Accounting-in-Bussiness

Time Period Assumption

Presumes that the life of a company can be divided into time periods, such as months and years.

C4 Proprietorship, Partnership, and Corporation

C4

Accounting Assumptions

Now

Future

Going-Concern Assumption

Reflects assumption that the business will continue operating instead of being closed or sold.

Chapter 1

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

C1

Accounting in Business

C1

Importance of Accounting

For example, the sale by Apple of an iPhone.

International Accounting Standards Board (IASB)

An independent group (consisting of individuals from many countries), issues International Financial Reporting Standards (IFRS)

Here are some of the major attributes of proprietorships, partnerships, and corporations:

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计学原理的英文

The Principles of Accounting

Introduction:

Accounting is the process of recording, classifying, summarizing, and interpreting financial transactions and events of an organization. It plays a crucial role in providing relevant and reliable financial information for decision-making purposes. To ensure consistency and accuracy in accounting practices, several fundamental principles have been established. This essay aims to provide an overview of the principles of accounting.

1. The Entity Concept:

The entity concept states that the business entity and its owner(s) should be treated as separate entities. This principle ensures that personal transactions of the owner(s) are not mixed with those of the business. It facilitates accurate measurement and reporting of business transactions, ensuring transparency and accountability.

2. The Going Concern Concept:

The going concern concept assumes that a business will continue its operations indefinitely. This principle allows assets and liabilities to be recorded at their acquisition cost and allows the business to be evaluated for its long-term

viability. It also supports the concept of depreciation, where the cost of fixed assets is allocated over their expected useful lives.

3. The Historical Cost Principle:

According to the historical cost principle, assets should be recorded at their original cost when acquired by the business. This principle provides objectivity and verifiability in financial reporting. However, it does not reflect the current market value of assets and can underestimate their true worth.

4. The Matching Principle:

The matching principle states that expenses should be recorded in the same accounting period as the revenue they help generate. This principle ensures that the financial statements reflect the true profitability of the business. It allows for the matching of expenses against the revenue they contribute to, providing a more accurate representation of the financial performance of the business.

5. The Revenue Recognition Principle:

The revenue recognition principle dictates that revenue should be recognized when it is earned, regardless of when it is collected. This principle ensures that revenue is reported in the same accounting period as the related expenses, leading to a

more accurate measurement of the business's financial performance.

6. The Consistency Principle:

7. The Materiality Principle:

The materiality principle states that financial information should be disclosed or reported if its omission or misstatement would affect the decision-making process of users of the financial statements. This principle allows for the elimination of irrelevant or immaterial information, focusing on providing useful information for decision-making.

8. The Conservatism Principle:

Conclusion:。