企业所得税汇算清缴鉴证报告英文版

企业所得税纳税申报表英译模板

Annual Enterprise Income Tax Return (A) of the People's Republic ofChinaTaxable Period: DD/MM/YY to DD/MM/YYTaxpayer:Monthly(Quarterly)Enterprise Income Tax Return (A) of the People's Republicof ChinaTaxation Period: DD/MM/YY to DD/MM/YYTaxpayer ID:Under the supervision of the State Administration of TaxationThe People’s Republic of ChinaMonthly (Quarterly) Enterprise Income Tax Return (B)Tax Belongs to DD/MM/YY to DD/MM/YYTaxpayer Identification No.:Taxpayer:Unit: RMB Yuan (0.00)I hereby state that this form is true, reliable and complete, filled in accordance with the Law on Enterprise Income Tax of the People’s Republic of China, the Implementation Ordinance of the Law on Enterprise Income Tax of the People’s Republic of China and the State’s related taxation provisions.Legal Representative (signature): Date: Taxpayer’s Official Seal: Agency’s Official Seal:Tax Authority’s Acceptance Seal:Accounting Supervisor: Undertaker:Undertaker: License No.:Date: Date: Date:Under the supervision of the State Administration of TaxationThe People’s Republic of ChinaMonthly (Quarterly) Enterprise Income Tax Return (B)Tax Belongs to DD/MM/YY to DD/MM/YYTaxpayer Identification No.:Taxpayer:Unit: RMB Yuan (0.00)I hereby state that this form is true, reliable and complete, filled in accordance with the Law on Enterprise Income Tax of the People’s Republic of China, the Implementation Ordinance of the Law on Enterprise Income Tax of the People’s Republic of China and the State’s related taxation provisions.Legal Representative (seal): Date: Taxpayer’s Official Seal:Agency’s Official Seal:Tax Authority’s Acceptance Seal:Accounting Supervisor: Undertaker:Undertaker: License No.:Date: Date: Date:Under the supervision of the State Administration of TaxationThe People’s Republic of ChinaMonthly (Quarterly) Enterprise Income Tax Return (B)Tax Belongs to DD/MM/YY to DD/MM/YYTaxpayer Identification No.:Taxpayer:Unit: RMB Yuan (0.00)I hereby state that this form is true, reliable and complete, filled in accordance with the Law on Enterprise Income Tax of the People’s Republic of China, the Implementation Ordinance of the Law on Enterprise Income Tax of the People’s Republic of China and the State’s related taxation provisions.Legal Representative (signature): Date: Taxpayer’s Official Seal: Agency’s Official Seal:Tax Authority’s Acceptance Seal:Accounting Supervisor: Undertaker:Undertaker: License No.:Date: Date: Date:Under the supervision of the State Administration of Taxation。

企业所得税年度纳税申请表中英文

42

以前年度应缴未缴在本年入库所得税额

Prior Year Tax Payable Paid in Current Year

10

二、营业利润(1-2-3-4-5-6-7+8+9)

2. Operation Profit

11

加:营业外收入(填附表一)

Add:

None-operation Income

12

减:营业外支出(填附表二)

Minus: None-operation Expenditures

13

三、利润总额(10+11-12)

17

免税收入

Tax-exempt Income

18

减计收入

Less Accured Income

19

减、免税项目所得

Less Duty-free item of Income

20

加计扣除

Additional deduction

21

抵扣应纳税所得额

Deductible Taxable Income

22

38

合并纳税(母子体制)成员企业就地预缴比例

Allocation ratio for branch

39

合并纳税企业就地预缴的所得税额

Pre-paid Tax in location of branch

40

本年应补(退)的所得税额(33-34)

Final Tax Payable

附列资料

41

以前年度多缴的所得税额在本年抵减额

Actual Tax Payable

34

企业所得税汇算清缴申报表A类 英文版

Calculation on total profit

Calculation on taxable income

Calculation on the tax payable

Attchment

Tax Return Form for the Yearly Prepayment of Enterprise Income Tax of the People's Republic of China (Type A) Items I. Operating income(attached formA101010\101020\103000) Less:Operating cost (attached formA102010\102020\103000) Business tax and surcharges Sales expenses (attached formA104000) Adminisstrative expenses (attached formA104000) Financial expenses (attached formA104000) Loss from asset devaluation Plus:Gains on the changes in the fair value Income from investment II.Operating profit(1-2-3-4-5-6-7+8+9) Plus:Non-operating income (attached formA101010\101020\103000) Less:Non-operating expenses (attached formA102010\102020\103000) III. Total profit(10+11-12) Less:Oversea income(attached formA108010) Plus:Tax Adjustment Increasing(attached formA105000) Less:Tax Adjusment Decreasing(attached formA105000) Less:Adjustment for tax exemption/reduction of income/collectively deductions(attached formA107010) Plus:Foreign Taxable Income to Cover the Territory of Loss(attached formA108000) IV. Income after tax adjustment(13-14+15-16-17+18) Less:Tax-exempt income(attached formA107020) Less:Deduction of taxable income(attached formA107030) Less:Prior year deficiency(attached formA106000) V. Taxable income(19-20-21-22) Tax rate(25%) VI. Tax payable(23×24) Less:Tax-free Tax Payable(attached formA107040) Less:Deductable Tax Payable(attached formA107050) VII. Tax Payable after adjustment(25-26-27) Plus:Oversea Tax Payable(attached formA108000) Less:Deductable Oversea Tax Payable(attached formA108000) VIII. Actual Tax Payable(28+29-30) Less:Prepaid income tax in current year IX. Final Tax Payable(31-32) Including:Income tax allocation by head institution(attached formA109000) Collective allocation of income tax by financial department (attached formA109000) Independent operation department of head institution should share income tax(attached formA109000) Prior Year Overpaid Tax Deducted in Current Year Prior Year Tax Payable Paid in Current Year

英文模板-企业所得税月(季)度预缴纳税申报表-A类-33行

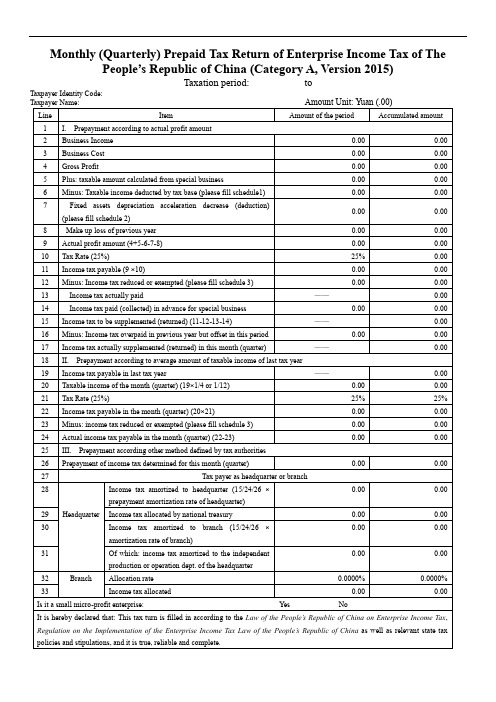

Special Seal for Acceptance of Competent Tax Authority:

Accepted by:

Date of Acceptance:

0.00

3

Business Cost

0.00

0.00

4

Gross Profit

0.00

0.00

5

Plus: taxable amount calculated from special business

0.00

0.00

6

Minus: Taxable income deducted by tax base (please fill schedule1)

0.00

0.00

32

Branch

Allocation rate

0.0000%

0.0000%

33

Income tax allocated

0.00

0.00

Is it a small micro-profit enterprise:YesNo

It is hereby declared that: This tax turn is filled in according to theLaw of the People’s Republic of China on Enterprise Income Tax,Regulation on the Implementation of the Enterprise Income Tax Law of the People’s Republic of Chinaas well as relevantstatetax policies and stipulations, and it is true, reliable and complete.

企业所得税汇算清缴纳税申报鉴证报告

一、企业所得税汇算清缴纳税申报的审核过程及主要实施情况

(一)企业所得税有关的内部控制及其有效性。

贵公司按照会计制度和税收法规要求设立总账和明细账,对业务收入、支出、货物进出、费用报销、投资、固定资产管理、薪酬等日常业务制定各项相关核算制度,审核中未发现重大未遵守情况。

(三)审核、验证、计算和进行职业推断的情况。

我们对贵公司提供的会计报表、年度企业纳税申报表和其他纳税资料进行了审核和验证,并根据国家有关企业所得税的法律法规规定,在专业判断的基础上对纳税事项的完整性和准确性进行了验算。

二、审核年度利润情况

贵公司20**年度的会计报表已经***会计师事务所有限公司审计,审计报告文号为***审[20**]****号,审定贵公司20**年度的利润总额为******元。

5、纳税调整后所得为******元;

6、弥补以前年度亏损为0.00元;

7、经上述纳税调整,贵公司2011年度应纳税所得额:******元;

8、适用税率:25%;

9、应纳所得税额=******×25%=******(元)

10、减免所得税额为0.00元;

11、抵免所得税额0.00元;

12、实际应纳税额=******×25%-0.00=******(元)

(8)未取得合法凭证的支出******元。

贵公司本年度实际发生的未取得合法凭证的支出账载金额******元,税收规定不允许税前扣除,纳税调整增加额******元。(《中华人民共和国发票管理办法》第二十二条)

(9)代垫税费******元。

汇算清缴英文版指南

汇算清缴英文版指南As a foreign individual or business operating in China, the process of "汇算清缴" (huì suàn qīng jiǎo) or "final settlement and clearance" of taxes can be a complex and daunting task. This guide aims to provide a comprehensive overview of the 汇算清缴 process in English, to help you navigate through the intricacies and ensure compliance with Chinese tax regulations.作为在中国经营的外国个人或企业,“汇算清缴”(huì suàn qīng jiǎo)即“最终结算和清算”税款的过程可能是一个复杂而艰巨的任务。

这份指南旨在全面介绍汇算清缴程序的英文版,帮助您在复杂的税收法规中航行,并确保您遵守中国的税收法规。

The first step in the "final settlement and clearance" process is to gather all relevant financial and tax documents from the previous year. This includes income statements, expense records, tax receipts, and any other documentation related to your financial activities in China.“最终结算和清算”过程的第一步是收集去年所有相关的财务和税务文件。

汇算清缴英文版指南

汇算清缴英文版指南English Response:Reconciliation and Clear Settlement.Reconciliation and clear settlement (RCS) is a process of reconciling and clearing transactions between two or more parties. It is typically used in financial transactions, such as banking, investments, and trade. The purpose of RCS is to ensure that both parties have a complete and accurate record of all transactions, and that all outstanding payments have been settled.The RCS process typically involves the following steps:1. The parties involved agree on the terms of the RCS, including the scope of the reconciliation, the frequency of reconciliation, and the method of settlement.2. The parties exchange data on all transactions thathave occurred during the reconciliation period.3. The data is reconciled to identify any discrepancies or errors.4. The discrepancies or errors are corrected and the data is re-reconciled.5. The parties agree on the final reconciled data and settle any outstanding payments.RCS can be a complex and time-consuming process, but it is essential for ensuring that both parties have a complete and accurate record of all transactions. It can also help to reduce errors and fraud, and improve the efficiency of financial transactions.Here are some of the benefits of RCS:Ensures that both parties have a complete and accurate record of all transactions.Reduces errors and fraud.Improves the efficiency of financial transactions.Helps to resolve disputes.Reconciliation and Clear Settlement in Different Industries.RCS is used in a variety of industries, including:Banking: RCS is used to reconcile and cleartransactions between banks and their customers. This includes transactions such as deposits, withdrawals, checks, and electronic payments.Investments: RCS is used to reconcile and clear transactions between investors and brokers. This includes transactions such as buying and selling stocks, bonds, and mutual funds.Trade: RCS is used to reconcile and clear transactionsbetween buyers and sellers of goods and services. This includes transactions such as purchase orders, invoices,and payments.The specific RCS process used in each industry may vary, but the overall goal is the same: to ensure that bothparties have a complete and accurate record of all transactions, and that all outstanding payments have been settled.中文回答:汇算清缴。

企业所得税申报表-英文版(中华人民共和国企业所得税年度纳税申报表(A类,2014年版)》)

Actual supplement (refund) of income tax in current month (quarter) 692.26 - II: Prepay on average according to last annual taxable income Last annual taxable income 0 - Taxable income in current month or quarter (line 21× 1/4 or 1/12) 0 0 Tax rate (25%) 0.25 0.25 Assessed income tax in current month or quarter (line 22× line 23) 0 0 Less:reduction or exempt of income tax for qualified small enterprises with low profits 0 0 Actual assessed income tax in current month or quarter (line 24 -line 25) 0 0 III: Other prepayment method issued by taxation authority Identified prepayment of income tax in current month (quarter) 0 0 Taxpayer in head institution and branch Income tax allocation by head institution (line 17 or line 26 or line28 × 30 0 0 prepay allocation percentage of head institution) 31 Collective allocation of income tax by financial department 0 0 Head Income tax allocation by branch institution 32 0 0 (line 17 or line 26 or line 28 × allocation percentage of branch) Including:independent operation department of head institution should 33 0 0 share income tax 34 Allocation percentage 0 0 branch 35 Allocated income tax amount 0 0 Declaration: This tax return form is finished in accordance with the Law of People's Republic China on Enterprise Income Tax,Regulation on Implementation of Enterprise Income Tax Law of the People's Republic of China and relevant tax regulations of state which has authenticity, reliability and integrity. Signature of legal representative: Taxpayer seal: Agent seal: Accountant: Filling date: Operator: Operator's Practice Certificate No.: Filling date of agent:

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

XXX Authentication Report of Income Tax (2011)

jianzi[2012]No.16

XXX:

We examined and verified your settlement and payment of Enterprise Income Tax for the year of 2011 upon your entrustment in accordance with stipulations of Enterprise Income Tax Law of the People's Republic of China and Detailed Rules for implementation of Enterprise Income Tax Law of the People's Republic of China, and conducted necessary inspection proceeding on your vouchers, account books and relevant financial statements in the light of Business Rules of Settlement and Payment of Enterprise Income Tax on a Trial Basis and Business Guidance tor Settlement and Payment of Enterprise Income Tax.

Your company is responsible for the legitimacy, reasonability, and completeness of relevant documents upon which we issue our authentication report independently, objectively and fairly. You shall make use of the authentication report pursuant to the Authentication Engagement. Consequences caused by the principal or any other third party’s misuse of authentication report shall be undertaken by the Certified Tax Agent and Tax Agent Office.

I.Authentication Process and Main Enforcement

ment on the Effectiveness and Reasonability of the Internal Control

There’s no evidence against the reasonability of the certified units shown in our process of Authentication. We trust the internal control system completely.

ment on the Interdependency and Dependability of Both Internal and External

Evidences

1.Interdependency

We examined the internal and external evidences such as relevant accounting material

and tax filling documents in accordance with Business Rules of Settlement and Payment

of Enterprise Income Tax on a Trial Basis, which supports our authentication result

soundly.

2.dependability

After making proper judgment and certification of relevant documents according to

statutory proceeding and certifying standard, we didn’t find illegitimate evidence and

recognize the authentic of annual tax filling prepared by the certified unit.

C.Authentication, V erification, Calculation and Inference on Relevant Accounting

Material and Taxation Documents

Due to the following conditions, we determine to issue this authentication report:

1.All the authenticated items correspond to the statutory criterion, and the

preparation of related accounting material and tax filling documents complies with

relevant regulations.

2.Certified Public Tax Agent conducted necessary authentication procedures without

any challenge from the certified company in accordance with regulations of the

Business Rules of Settlement and Payment of Enterprise Income Tax on a Trial

Basis.

3.Certified Public Tax Agent collected proper and adequate evidence on the

authenticated items, which fully supports our recognition of tax payment.

II.Authentication Conclusion

Audit results on your company’s expenditure for the year of 2011 are as below:

1. Gross Profit: ¥4,718,887.61

2. Adjustment for Additional ax Payment:¥4,955,091.62

3. Adjustment for Tax Payment Deductible:¥2,330,753.46

4. Overseas Taxable Income Offset Assets Loss for Domestic Losses ¥0.00

4. Income after Tax Adjustment:¥7,343,22

5.77

5. Offset Assets Loss for Prior Years ¥0.00

6.Taxable Income: ¥7,343,225.77

7. Tax Rate:25%

8. Tax Payable ¥1,835,806.44

9. Tax Exempted: ¥0.00

10. Tax Paid:¥1,181,002.50

11.Tax in Arrears ¥654,803.94

The above information is dependable for tax filling.。