kpmg36题答案解析

KPMG笔试题(中文解释版+2篇全真verbal)

KPMG笔试题(中文解释版+2篇全真verbal)KPMG笔试题(中文解释版+2篇全真verbal)1.阅读阅读共12篇英文短文,32题选择〔true, false, not given〕,18分钟,KPMG笔试题(中文解释版+2篇全真verbal)。

其中前8篇每篇三题,后4篇每篇2题。

先讲一下其中的疑难词汇congruent全等的 coronal heart disease冠心病unequivocal清楚的,明白的 fructose果糖equilibrium平衡 emergence出现 radium镭undetermination决心、果断其中8篇阅读的大致内容表达如下,不过原文是英文的哦:1、关于工作环境能否为员工提供好的平安用品以及工作环境对人们是否认为它是一个好雇主是很有影响的。

一个有义务购置防火以及其他平安设备,培训员工正确地使用机器,设备等。

2、关于人口与环境人口与环境的平衡并不代表人口是不变的。

疾病与环境,特别是物理环境,的变化都会改变人口的数量。

人口随极地冰盖的变化而变化。

问题:1〕人口随极地冰盖的增加而减少。

2〕物理环境的变化是人口变化的unequivocal的因素。

3、糖和饮食人们的食物中白糖占的比例越来越小,但是食物中的糖份摄入量却越来越多。

根据统计,食品标签上得糖(包括果糖,乳糖,葡萄糖〕的数量在不断增加。

虽然没有调查说明糖与冠心病有必然联络,糖本身也不直接导致肥胖。

问题:糖导致肥胖4原子原子裂解〔disintegrate〕速率是确定的,以镭原子为例,我们只知道镭原子是以确定的速率进展裂变,而不可以知道详细会在何时裂变。

问题:原子分裂的速率与我们观察原子的时间无关。

这题我确定应该是true 组织构造传统的工厂由经理一人解决几乎所有的事情,但是随着企业的不断开展,在公共关系,经营等三方面的事情不断增加,traditional manager 就管不过来了,需要建立一个团队来进展专门管理,资料共享平台《KPMG笔试题(中文解释版+2篇全真verbal)》(s://..)。

KPMG(毕马威)笔试经典24题,36题详解(最终版本)

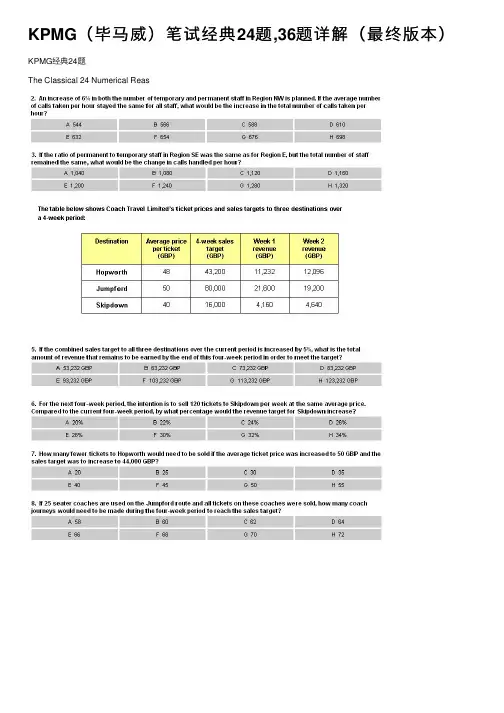

KPMG(毕马威)笔试经典24题,36题详解(最终版本)KPMG经典24题The Classical 24 Numerical Reas"The big economic difference between nuclear and fossil-fuelled powerstations is that nuclear reactors are more expensive to build and decommission, but cheaper to sun. So disputes答案详解1. E(28x200+25x100)/(100%-10%)=90002. C(20x250+16x300) x6%=5883. BRegion E (permanent: temporary)=3:2Region SE Total: 400 Permanent: 150 Temporary: 250(New) Permanent: 400x3/5=240Temporary: 400x2/5=160所以我们可以得出P增加了90⼈,T减少了90⼈90x(30-18)=1080(我们可以⽤其他⽅法算,但是却不是最节约时间的算法)4.E⽬测,(SE和SW的P每⼩时接的电话数是最⾼的,⽽且SW的P的⼈数多,所以总数上SW可定⽐SE要⾼。

虽然E的每⼩时接电话数不⾼,但是他⼈数最多,所以总数也很⾼)5. C(43200+80000+16000) x105%-11232-12096-21600-19200-4160-4640=732326. A(40x120x4-1600)/16000=20%7. A43200/48-44000/50=208. D80000/50/25=649. E(2.50-2.40)/2.40x2.50+2.50=2.604(1.10-1.08)/1.08x1.10+1.10=1.1202.604-1.120=1.4810. A1.70-(3.20-1.70)=0.211. C(1.70-0.3)x(1-15%)=1.1912. E1.08x(1-20%)/2.40=36%13.G(70-50)x4x40x3=960014. B50x40x4x6+50x4x4x10=5600015. E3/2.4x40-40=1016. C(40-38)x4x3x(55+40)=228017. C8000/61.8-100/1.62=67.72不管在Yr 1,⽤了多少英镑买泰铢,我们要知道的是在Yr 2,8000泰铢可换多少英镑,所以⽤第⼆年的汇率,⽽不是第⼀年的。

KPMGPWC2017校招最新笔试真题解析(文末有福利)

KPMGPWC2017校招最新笔试真题解析(文末有福利)KPMG PWC 2017校招最新笔试真题解析,文章我们以聊天讲解的形式为大家放出,如果大家还不懂的话。

文末有福利哦。

•08-28 21:02•今年KPMG的题整体难度不是很大,主要难度体现在大题量上,题型有两类,数字题和图表题。

首先先来看一下图表题:•••08-28 21:04•上面这个题选错误。

•题目不难,但题目给我们的启示是出题人可能会在关键词上用类似的字来混淆。

比如是应付账款还是应收账款。

•08-28 21:07•因为资产负债表里一共有4个成分,已经占了100%,所以应付账款就不可能有比例了•所以这个题不选无法判断,而是选错误•如果是应收账款就是48%•08-28 21:09•这个题答案是错误,这个题和上面也是一样,要注意题目的细节,这个题需要注意的是题目所用到的单位。

•这个题选错误而不是无法判断的原因是每年的变化都是在10亿元的量级,只能说有可能FY+2大于FY-1 100亿,而不能说很有可能•今天发的题就是考试的真题•注意,题目中FY和FY+2变化只有15亿,注意单位•08-28 21:13•接下来几个题,题目都问到了一些图表中没有的信息,因此都要选择无法判断,例如这个题,表中没有第2年的信息,就无法判断正确与否了。

•咕叽咕叽:意思-1年再大不太可能到100亿?因为根据下两年也就10,15?回复:对••08-28 21:15•这个题也是无法判断,应收账款中回购协议与证券借贷的百分比也未给出。

•咕叽咕叽:上一题因为是欧陆,图表只有欧洲是吗?回复:不是,这个银行叫欧陆银行•小百科.Rar:如果可以根据图中信息能推算出来的就选正确或错误,如果没有牵扯到任何的信息也无法推算的就选无法判断。

对吗?回复:对的•08-28 21:18•这个题答案选错误,这是需要推理的一个题,注意题目问的是收入的趋势,虽然FY+3没有给出,但题目中FY,FY+1,FY+2整体趋势是上涨的,所以FY+3的值是应该大于215亿的。

毕马威测试题

毕马威测试题近年来,随着全球经济的快速发展和企业规模的不断扩大,对于企业财务和业务流程管理的需求也日益增加。

作为一家全球领先的专业服务公司,毕马威(KPMG)致力于提供创新的解决方案和专业的咨询服务,以帮助企业实现财务和业务流程的高效管理和精益运营。

在这篇文章中,将介绍毕马威的测试题,以展示其对于员工选拔和培养的严谨与创新。

我们知道,毕马威对于员工素质和能力的要求非常高。

作为一名申请者,你需要通过一系列的测试来展示自己在逻辑思维、问题解决以及团队合作等方面的能力。

下面是一个示例的毕马威测试题,让我们一起来看看吧。

题目一:逻辑思维请根据以下信息,回答问题。

某电子产品公司计划推出一款新型手机,预计每月销售数量10000部。

已知销售价格为800美元/部,单位产品的固定成本为200美元/部,而可变成本为400美元/部。

根据市场调研,当销售价格为600美元时,每月销售数量将增加到15000部。

问题:1.1 根据以上信息,计算每月销售额和总成本(包括固定成本和可变成本)。

1.2 根据以上信息,计算每月销售的总利润。

1.3 如果该公司希望通过每月销售数量的增加来达到每月总利润为60万美元的目标,需要将销售价格定为多少?解答:1.1 每月销售额 = 销售数量 ×销售价格 = 10000 × 800 = 8000000美元总成本 = 固定成本 + 可变成本 = 200 × 10000 + 400 × 10000 = 6000000美元1.2 每月销售的总利润 = 每月销售额 - 总成本 = 8000000 - 6000000 = 2000000美元1.3 设销售数量为x,则销售数量的增加带来的额外销售额为 (x - 10000) × 600美元。

根据题目中的信息,额外销售额应为60万美元。

因此,(x - 10000) × 600 = 600000。

解方程可得,x = 15000。

SHL测评KPMG-ClassicalVerbalTest(经典36题)

SHL测评SH是全球权威人才测评内容提供商。

现在一些外资企业和大型企业在招聘时已开始使用SHL的测评工具。

SHL题型SHL测评分为两部分:数字能力测试,是与商业活动相关的数学计算。

文字能力测试,就是阅读理解。

题目本身并不难,关键是理解英文题目,以及以0.5-1分钟一题的速度完成测试。

有机考和卷考二种方式。

1、Numerical TestIn this test, you have to use facts and figures presented in statistical tables to answer the questions. In each question, you are given five options from which to choose. One, and only one, of the options is correct in each case.You may use a calculator for the following questions. In addition, you can use rough paper for your working out.2、Verbal TestIn this test, you are given several passages, each of which is followed by several statements. Your task is to evaluate the statements in the light of the information or opinions contained in the passage and to select your answer according to the rules given below.样题KPMG-Classical Numerical Test (经典24题)KPMG-Classical Verbal Test (经典36题)KPMG-Classical Verbal Test (36 Questions) 答案在后Read the passage carefully and then, using only the information given in the passage, for each statement choose whether it is True, False, or Cannot say. The test has 36 questions and you will have 18 minutes to do them.Individuals who are responsible for databases that hold information about people are now bound by the Data Protection Act (PDA). This Act covers any information stored on a computer that identifies a living individual. Companies holding such information must, under the Terms of the Act, make sure that they take ‘adequate care’ of the data, both technica lly and in terms of the behavior of the organization. The personal data stored has to be protected from loss, destruction or damage.Example 1. Any information stored about a named individual currently working for an organization is subject to the Data Protection Act. TrueExample 2. As long as any data about a named individual is managed in a technically adequate way, there are no other restrictions as to how it can be used or handled. FalseExample 3. Damage to data held about named individuals represents the biggest threat to its proper management. Can’t sayExample 4. Data about named individuals who have left a company is not subject to the Act. False Section ACompetitor analysis involves the examination of competitors in order that the planner can develop and sustain superior competitive performance for the organization. This statement belies the fact that in order to do this one must first establish from where the competition currently stems and from where it might stem in the future. One also has to consider and appraise comp etitors’ present and likely future objectives and strategies, and their likely reactions to the competitive moves that an organization might make.1. Planners can only sustain superior performance for their organization by doing competitor analysis.2. Effective competitor analysis involves looking into the future.3. It is easier to establish where competition currently stems from, rather than where it might stem from in the future.4. It is not always apparent to organizations who their competitors are.Section BThe model of consumer behavior on which neo-classical demand theory is based implies that consumers are perfectly informed about the price and quality characteristics of the products on offer, and are constantly altering their expenditure patterns in response to price and quality changes, so as to maximiz e their total ‘utility’ (satisfaction). This model is unrealistic, as the range of products on offer in modern markets is immense, and no consumer has the knowledge or inclination to acquire the information that would be needed to make choices in this way.5. Being up to date with product information plays little part in neo-classical demand theory.6. Neo-classical demand theory is only one of a number of models of consumer behavior.7. There are some consumers who are perfectly informed about the price and quality characteristics of products on offer.8. Maximizing the total utility of a product purchase implies consideration of both price and quality characteristicsThe business of the Company shall be managed by the directors who, subject to the law, the memorandum and articles of association, and any direction given by special resolution, may exercise all the powers of the company. The minimum number of directors is two; there is no maximum number. The directors, or the company by special resolution, may appoint as a director any person who is willing to act as a director, provided he or she is not a bankrupt or disqualified from acting as a director under the Insolvency Act. Directors need not hold shares in the company, but normally they will be required to hold at least a specific minimum shareholding.9. New directors tend to be appointed by existing directors rather than by special resolution.10. The Company cannot operate with only one director.11. Individual bankruptcy is governed by the Insolvency Act.12. There is no upper limit to the number of shares any director can hold.Section DIn most organizations, conflict between groups is quite common. Organizations usually develop differences between functional groups, such as sales and manufacturing, as a means of responding to diversity and uncertainty in their particular environment. Manufacturing must organize for stability and efficiency while sales must organize to relate to and service customers. To accomplish these diverse tasks, sales must hire different people from manufacturing, and each must manage its people in accordance with their unique expectations and the functions’ task requirements. If such differenc es did not exist, neither group could get its job done effectively.13. Functional groups within a single organization are not subject to different forms of uncertainty.14. Conflict between groups is the inevitable result of functional groups having to respond to their own unique environments.15. Manufacturing and sales are unlikely to have the same goals and expectations.16. The reality of functional differences does mean that different groups cannot operate effectively.Section EUnless companies have some knowledge of buyer behavior, they would be unaware of and unfamiliar with the complex range of behavioral factors that impinge upon purchasing behavior. The truth is that, like much of human behavior, purchase behavior is complex and multi-faceted. Even the ‘simplest’ of purchasing dec isions is an amalgam of behavioral forces and factors of which even the purchaser may not be aware. However, even though consumer behavior is a complex subject marketing planners should at least have some understanding of it. Marketers are specifically interested in the behavior associated with groups or segments of consumers as it would be impossible to serve the exact needs and wants of specific individuals in a market and remain profitable.17. The purchasing behavior of consumers is unpredictable.18. Even if one could predict the behavior of an individual buyer, it would not be profitable for marketers to try to do so.19. Some consumer groups exhibit more complex behavior than others do.20. Purchase behavior is not subject to the same whims as other aspects of human behavior.When any company moves from a sales to a marketing approach, it is not just a case of re-titling the Sales Director as Marketing Director and doubling the advertising budget. It requires a complete reorientation in thinking and a revolution in how a company organizes and practices its business activities. Whereas selling focuses on the needs of the seller, marketing focuses on the needs of the buyer. Whereas selling is preoccu pied with the seller’s need to convert his or her product into cash, marketing is preoccupied with the idea of identifying and hence satisfying the needs of the customer. However, subscribing to a philosophy of marketing, even though an important first step, is not the same as putting that philosophy into practice.21. Advertising budgets are normally doubled when a company moves over to a marketing approach.Section GThe corporate mission statement needs detailed consideration by top management to establish the business the company is really in and to relate this consideration to future business intentions. It is a general statement that provides an integrating function for the business, from which a clear sense of business definition and direction can be achieved. By formulating a clear business statement, boundaries for the ‘corporate entity’ can be conceived in the context of wider environmental trends that influence the business. This stage is often overlooked in marketing planning, and yet without it the marketing plan will lack a sense of contribution to the development of the total business.22.The boundaries of a corporate entity can only be assessed in the context of wider environment trends.23.A corporate mission statement enables top management to define the future direction of a business.24.Marketing planning does not often take account of the corporate mission statement.25. Different functions within a business are likely to interpret the mission statement in different ways.Section HThe adoption and application of performance management methods requires many different changes in behavior and attitudes up and down the organization. These methods are not merely techniques; they are ways of life and a philosophy of management. Thus the introduction of performance management systems must come as part of an organiz ation’s commitment to change its culture. Only top management commitment to a new way of managing, often triggered by a crisis, can support such a massive undertaking.29. The support of top managers is essential in changing organizational culture.31. Using performance management systems for the first time requires minimal adaptations on the part of the organization concerned.32. The adoption of performance management methods of itself will create changes in behavior and attitudes.Section IThe ‘prudence rule’, which is sometimes known as conservatism, arises out of the need to make a number of estimates in preparing periodic accounts. Managers and owners are often naturallybe undue optimism over the credit-worthiness of new customers. Insufficient allowance may therefore be made for the possibility of bad debt. In turn, this might have the effect of overstating profit.33. Accountants should avoid making estimates when preparing periodic accounts.34. Most new customers are credit-worthy.35. Managers or owners are not often good judges of their customers’ willingness or ability to pay.36. The ‘prudence rule’ prevents bad debt from arising.Section JA partnership is presumed to exist when two or more people get together in business with the objective of making a profit. The law limits the total number of people who may get together to form a partnership. Apart from a few exceptions, such as firms of accountants and solicitors, a partnership may not consist of more Than 20 partners. The partnership will be managed by general agreement among the partners, but if there is no apparent agreement either formal or informal, then it is presumed that the partnership will operate in accordance with the Partnership Act, 1890. This Act lays down arrangements for dealing with such matters as the amount of capital to be contributed, the management of the business, and the division of the profits or losses among the partners.37. Some agreement must exist between partners as to the way they manage the partnership.Section EThe amount of accounting information that could be supplied to any interested party is practically unlimited. The information needs to be designed in such a way that it meets the objectives of the specific user group. If too much information is given, the user might think that it is an attempt to mislead them, and as a result all of the information may be totally rejected. In this context, accountants try to present accounts in such a way that they represent ‘a true and fair view’. The Companies Act, 1985, for example, requires company accounts to reflect this particular criterion, and it is advisable to apply it to all organizational entities. Unfortunately the Act does not define what is meant by ‘true and fair’, b ut it is assumed that accounts will be so if an entity has followed the rules laid down in appropriate accounting and financial reporting standards.19. It is a positive feature of the Companies Act, 1985, that it does not define what is meant by ‘true an d fair’.20. In practice, the proper application of accounting and financial reporting standards ensures that accounts meet the criteria of being ‘true and fair’.Section FThe style that individual managers choose to adopt depends in no small part on how they regard their subordinates. At one extreme, some will assume that the average employee has an inherent dislike of work and will avoid it if they can. They believe employees need to be controlled, directed, offered rewards or threatened with punishments to get them to make adequate efforts towards the achievement of organizational goals. On the other hand, some will take the view that, according to the conditions, work can be a source of satisfaction or dissatisfaction. Employees are not seen as naturally passive, or resistant to organizational objectives, but have been made so by experience. The most significant reward that can be offered employees is the satisfaction of their need for perso nal21. Using rewards and punishments is a necessary part of organizational life.经典36题答案A:1 C2 T 原文第二句3 C 比较级,原文未提及4 C 未提及B:5 F 与原文意思相反6 C 未提及7 F No Consumer全否定8 T 原文C:9 C 原文未表达比较意思10 T 原文11 C12 CD:13 F 与原文意思相反not14 T15 C16 FE:17 C18 T 原文19 C20 F 相反F:21 C 未提及是哪个的两倍G:22 F 缺少修饰语23 T 第一句24 T 原文25 C 未提及H:29 T31 C未提及32 F 一个是require 一个是create 意思相反I:33 C未提及34 C未提及35 T36 F 相反J: 37 FOther:E: 19 F Positive不对20 F 一个是assume,一个是in practiceF: 21 F18题,根据Marketers are specifically interested in the behaviour associated with groups or segments of consumers as it would be impossible to serve the exact needs and wants of specific individuals in a market and remain profitable.而18题的意思,大概为Marketer即使能预测具体消费者的行为,也不能保持盈利。

KPMG 13年笔试题目总结

A,Numerical集合根据收集的所有帖子,本人把出现的题型归类:第一题,经济类犯罪率的图表.04年和08年的各种犯罪。

有犯罪总数,各分类比例。

问题是比较,和求增长率在推算其他年份的一些数据。

2005年和2008年,我还算得很认真,做完才发现年份有问题白算了,所以在这里提醒大家注意一下这个题目,今年的选项设置也进步了05年给了总数没给比例,08年给了总数和各项比例;08年那个总数要常用到第二题,汇率图表。

和经典题基本一样。

基本货币还是英镑,其他的美元,欧元,日元,还有一些这个那个第纳尔(汗)。

每一年的油价和港币与泰铢的汇率1.问不同年份可以买的油的数量有多少不同2.问如果油价的变化的趋势在1月到2月也适用,那XX钱可以在1月买多少桶油。

3.某种货币两年之间价值变动(贬值or 升值)、哪些货币变动量最小(网上好像是问最大的两种,注意陷阱)、4.“哪两种货币兑换比率变换最大”5.大概就是说几年前买了多少泰铢,之后今年后要换成澳大利元,之后问损失多少之类的;还有关于汇率增长的,第三题,健身房图表……某天的午间健身班的题目。

分为空手道、瑜伽等等等等,第一列为班级总人数,第二例为首次参加人数比,第三列为5次以上。

问题有两个班级特定人数比较的,有某一个班级除第一次与5次以上剩余的人数,还有根据增长率求第二天某班特定人数的。

好像是问空手道上课1次以上4次以下的一共占总人数的多少。

第三张,4个健身房,每家都有三总顾客,去过一次的,去过4次以上的,还有剩下的,这题不难,举例:一共50人,第一次去的20%,去过5次以上的10个人,你说剩下的多少人第四张,电脑销售额,单价,税率题。

电脑缴税.条形图。

分别为各年的销售量和价内含税销售额(好像是这样的吧= =),然后旁边给的信息是各年的税率。

第五张,东南亚一些国家某几年的销售额之类的. 东南亚各国5年(也许是6年= =)销售额,条形图。

很变态的是没有告诉各年的总销售额,需要自己加合,浪费了不少时间。

KPMG(毕马威)笔试经典24题,36题详解(最终版本)

KPMG经典24题The Classical 24 Numerical Reas"The big economic difference between nuclear and fossil-fuelled powerstations is that nuclear reactors are more expensive to build and decommission, but cheaper to sun. So disputes答案详解1. E(28x200+25x100)/(100%-10%)=90002. C(20x250+16x300) x6%=5883. BRegion E (permanent: temporary)=3:2Region SE Total: 400 Permanent: 150 Temporary: 250(New) Permanent: 400x3/5=240Temporary: 400x2/5=160所以我们可以得出P增加了90人,T减少了90人90x(30-18)=1080(我们可以用其他方法算,但是却不是最节约时间的算法)4.E目测,(SE和SW的P每小时接的电话数是最高的,而且SW的P的人数多,所以总数上SW可定比SE要高。

虽然E的每小时接电话数不高,但是他人数最多,所以总数也很高)5. C(43200+80000+16000) x105%-11232-12096-21600-19200-4160-4640=732326. A(40x120x4-1600)/16000=20%7. A43200/48-44000/50=208. D80000/50/25=649. E(2.50-2.40)/2.40x2.50+2.50=2.604(1.10-1.08)/1.08x1.10+1.10=1.1202.604-1.120=1.4810. A1.70-(3.20-1.70)=0.211. C(1.70-0.3)x(1-15%)=1.1912. E1.08x(1-20%)/2.40=36%13.G(70-50)x4x40x3=960014. B50x40x4x6+50x4x4x10=5600015. E3/2.4x40-40=1016. C(40-38)x4x3x(55+40)=228017. C8000/61.8-100/1.62=67.72不管在Yr 1,用了多少英镑买泰铢,我们要知道的是在Yr 2,8000泰铢可换多少英镑,所以用第二年的汇率,而不是第一年的。

毕马威笔试题目全集

2007 KPMG实习生笔试数字题&笔试题图表1:ABCDE五个店铺的日销售额图标横轴分别是5个店铺;纵轴是男性,女性消费者的数量,另有每个店铺男性和女性的平均消费金额(单位澳元)题目是:E店铺的销售金额比目标金额少20%,问你E店铺一天的目标金额是多少;如果C店铺的男女比例跟E一样而总数保持不变,那它的销售额变化多少;哪两家店铺男性的消费额较高;图表2:机票价格目标销售额,4个星期为一周期图表横向是去三个目的地(暂定为ABC吧,具体地方英文名不记得了)的机票单价、4星期的目标销售额、第一星期的收入、第二星期的收入;纵向是三个目的地题目是:如果4周目标销售额增长5%的话,那么还需要完成多少销售额;如果去C地单价提高为55$(原价是50$),那么如果完成销售额可以少卖多少张机票;如果一个公车16座的,票已经卖完,那么要完成去A地的销售任务,需要派多少辆公车;图表3:计算投票人数图表横向是90,91,92,94,96,98,06等;纵向是可投票人数、实际投票人数、邮寄投票比例(单位百万)题目是:如果2006年到2014年的可投票人数和实际投票人数增长幅度等同于98年到06年,问你2014年没投票的人数;94年如果邮寄投票比例是*%,问你亲自到现场投票人数将是多少;某年实际投票人数与没投票人数的差额;某年邮寄投票比例变化为*%,问你,亲自现场投票变化多少人;图表4:关于计算工人工资和咨询电话量,4周为1个周期图表横向是ABCDE5个公司;纵向是每个公司员工数量;另还有每个员工每个小时可接销售电话量为9个,每周正常工作时间35小时,工人的基本工资是每小时5元,加班工资是没小时8元题目是:如果E公司每周工作时间由35小时改为32小时,为了保证工作量,需增加多少员工;D公司员工在一个周期内每人每周加班3小时,问总共需要付多少工资;哪两家公司接的电话量最大;图表5:关于各国货币两年的汇率,以1英镑为基础图表横向是05年和06年两年的汇率;纵向是8个国家(大概是8个)题目是:如果第一年买进8000泰铢,第二年先换100欧,剩下的钱还可以换多少英镑;如果第一年买进100美元,第二年可以换多少日元;哪两个国家两年的汇率变动较小;图表6:关于采矿数量和某种稀有金属的销售图表横向是采矿的数量(单位是千吨),矿产中X的含量(单位是克/吨,具体什么稀有金属不记得了),这种金属的单价(第尔纳元/克,不知道是什么国家的货币);纵向是不同年份题目是:如果--年要达到销售额多少,需采多少的矿产;哪两年采矿的财务回报最高;阅读第一篇讲到business statement第二篇关于corporation culture第三篇是business structure第四篇是comsumer behavior其余的忘了,但都与经济有关,阅读我只做了6篇,图表有两张没做,血的教训啊.做题不能太纠结,无论是阅读还是数字题,必须快刀斩乱麻,我就是太容易停留在一道题上了! 数字题第一小题算了n遍也算不出正确结果,明明是超easy的题目:"E店铺的销售金额比目标金额少20%,问你E店铺一天的目标金额是多少;"不知大家算得怎么样,我甚至怀疑题目出错了!先是25分钟的阅读,12篇小短文回答48个问题。

kpmg性格测试题(3篇)

第1篇一、个人倾向1. 你更喜欢独自活动还是与朋友一起?A. 独自活动B. 与朋友一起C. 两者都可以2. 你在解决问题时,更倾向于:A. 依靠直觉B. 逻辑分析C. 情感判断3. 你通常怎样度过周末?A. 安静地在家休息B. 参加社交活动C. 两者兼有4. 你认为自己的性格是:A. 外向型B. 内向型C. 中间型5. 你更喜欢以下哪种活动?A. 观看体育比赛B. 参与体育活动C. 既观看又参与二、工作态度6. 你在工作中更注重:A. 结果B. 过程C. 团队合作7. 你在面对困难时,更倾向于:A. 坚持到底B. 寻求帮助C. 放弃8. 你认为自己的工作风格是:A. 创新型B. 稳定型C. 灵活型9. 你更喜欢以下哪种工作环境?A. 独立工作B. 团队合作C. 管理层10. 你认为自己的职业规划是:A. 短期目标B. 长期目标C. 随机应变三、人际关系11. 你在与人交往时,更注重:A. 实用性B. 情感交流C. 两者兼有12. 你认为自己的沟通方式是:A. 直接表达B. 委婉表达C. 灵活应对13. 你在处理人际关系时,更倾向于:A. 坚持原则B. 灵活应变C. 避免冲突14. 你认为自己的朋友类型是:A. 朋友众多B. 朋友较少,但关系紧密C. 两者兼有15. 你在团队中更喜欢:A. 领导角色B. 成员角色C. 灵活应对请您根据自己的实际情况,选择每个问题的答案。

完成后,您可以对照答案解析,了解自己的性格特点。

祝您测试顺利!第2篇尊敬的参与者:您好!KPMG作为全球领先的专业服务机构,一直致力于为客户提供最优质的服务。

为了更好地了解您的性格特点,挖掘您的职业潜能,我们特为您精心设计了这套KPMG性格测试题。

本测试题旨在帮助您认识自己,为您的职业发展提供有益的参考。

请您根据自己的实际情况认真作答,测试结束后,我们将为您提供个性化的分析报告。

一、测试说明1. 请仔细阅读每一道题,并根据您的实际情况选择最符合您的选项。

KPMG经典24题和36题详细讲解[2016版]

一、KPMG经典24题。

The Classical 24 Numerical Reasoning(200*28 + 100*25)*0.9 = 7290 错(200*28+100*25)/0.9 = 9000 EC (250*20+300*16)*0.06 =588400*3/5 = 240 240-150=90 90*(30-18)=1080 B4.which two regions had the highest total number of calls handed per hour by permanent staff?SW 和E (5400,5600)(43200+80000+16000)*1.05 = 139200*1.05 = 146160146160-11232-…-4640 = 73232 C4*120*40 = 19200 (19200-16000)/16000 = 3200/16000 = 20% A44000/50 – 43200/48 = 880-900 = -20 A80000/(50*25) = 64 DCommuter:(远距离)上下班往返的人(2.5-2.4)/2.4 = (x-2.5)/2.5 x=2.6 (1.1-1.08)/1.08=(y-1.1)/1.1 y=1.12 E(3.2-1.7)-1.7=-0.2 A(1.7-0.3)*(1-15%) = 1.19 C1.08*(1-20%)/2.4 = 36% E20*4*40*3 = G50*4*(40*6+4*10) = B40*3 = (40+x)*2.4 E(55+40)*4*(40-38)*3 = C8000/61.8 – 100/1.62 = C1000*1.52/1.62 * 11.1 = 10414.8 F(61.8-65.4)/65.4 = 5.5 这是不对的应该除以后者(1/61.8 –1/65.4)/(1/65.4) 除的是year1的数 DB根据前一题知,比较:差额/yr2E (gm:gram克)(150-110)/110£英镑X*5*8=100000 G10.5 - 9.5*1.1 A"The big economic difference between nuclear and fossil-fuelled powerstations is that nuclear reactors are more expensive to build and decommission, but cheaper to sun. So disputesA经典24题答案详解1. E(28x200+25x100)/(100%-10%)=90002. C(20x250+16x300) x6%=5883. BRegion E (permanent: temporary)=3:2Region SE Total: 400 Permanent: 150 Temporary: 250(New) Permanent: 400x3/5=240Temporary: 400x2/5=160所以我们可以得出P增加了90人,T减少了90人90x(30-18)=1080(我们可以用其他方法算,但是却不是最节约时间的算法)4. E目测,(SE和SW的P每小时接的电话数是最高的,而且SW的P的人数多,所以总数上SW 可定比SE要高。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Classcical 36 Verbal QuestionsExampleIndividuals who are responsible for databases that hold information about people are now bound by the Data Protection Act (PDA). This Act covers any information stored on a computer that identifies a living individual. Companies holding such information must, under the Terms of the Act, make sure that they take ‘adequate care’ of the data, both technically and in terms of the behaviour of the organisation. The personal data stored has to be protected from loss, destruction or damage.Example 1. Any information stored about a named individual currently working for an organisation is subject to the Data Protection Act.Example 2. As long as any data about a named individual is managed in a technically adequate way, there are no other restrictions as to how it can be used or handled.Example 3. Damage to data held about named individuals represents the biggest threat to its proper management.Example 4. Data about named individuals who have left a company is not subject to the Act.Section ACompetitor analysis involves the examination of competitors in order that the planner can develop and sustain superior competitive performance for the organisation. This statement belies the fact that in order to do this one must first establish from where the competition currently stems and from where it might stem in the future. One also has to consider and appraise competitors’ present and likely future objectives and strategies, and their likely reactions to the competitive moves that an organisation might make.1. Planners can only sustain superior performance for their organisation by doing competitor analysis.2. Effective competitor analysis involves looking into the future.3. It is easier to establish where competition currently stems from, rather than where it might stem from in the future4. It is not always apparent to organisations who their competitors are.Section BThe model of consumer behaviour on which neo-classical demand theory is based implies that consumers are perfectly informed about the price and quality characteristics of the products on offer, and are constantly altering their expenditure patterns in response to price and quality changes, so as to maximise their total ‘utility’(satisfaction). This m odel is unrealistic, as the range of products on offer in modern markets is immense, and no consumer has the knowledge or inclination to acquire the information that would beneeded to make choices in this way.5. Being up to date with product information plays little part in neo-classical demand theory.6. Neo-classical demand theory is only one of a number of models of consumer behaviour.7. There are some consumers who are perfectly informed about the price and quality characteristics of products on offer.8. Maximising the total utility of a product purchase implies consideration of both price and quality characteristicsSection CThe business of the Company shall be managed by the directors who, subject to the law, the memorandum and articles of association, and any direction given by special resolution, may exercise all the powers of the company. The minimum number of directors is two; there is no maximum number. The directors, or the company by special resolution, may appoint as a director any person who is willing to act as a director, provided he or she is not a bankrupt or disqualified from acting as a director under the Insolvency Act. Directors need not hold shares in the company, but normally they will be required to hold at least a specific minimum shareholding.9. New directors tend to be appointed by existing directors rather than by special resolution.10. The Company cannot operate with only one director.11. Individual bankruptcy is governed by the Insolvency Act.12. There is no upper limit to the number of shares any director can hold.Section DIn most organisations, conflict between groups is quite common. Organisations usually develop differences between functional groups, such as sales and manufacturing, as a means of responding to diversity and uncertainty in their particular environment. Manufacturing must organise for stability and efficiency while sales must organise to relate to and service customers. To accomplish these diverse tasks, sales must hire different people from manufacturing, and each must manage its people in accordance with their unique expectations and the functions’ task requirements. If such differences did not exist, neither group could get its job done effectively.13. Functional groups within a single organisation are not subject to different forms of uncertainty.14. Conflict between groups is the inevitable result of functional groups having to respond to their own unique environments.15. Manufacturing and sales are unlikely to have the same goals and expectations.16. The reality of functional differences does mean that different groups cannot operate effectively.Section EUnless companies have some knowledge of buyer behaviour, they would be unaware of and unfamiliar with the complex range of behavioural factors that impinge upon purchasing behaviour. The truth is that, like much of human behaviour, purchase behaviour is complex and multi-faceted. Even the ‘simplest’ of purchasing decisions is an amalgam of behavioural forces and factors of which even the purchaser may not be aware. However, even though consumer behaviour is a complex subject marketing planners should at least have some understanding of it. Marketers are specifically interested in the behaviour associated with groups or segments of consumers as it would be impossible to serve the exact needs and wants of specific individuals in a market and remain profitable.17. The purchasing behavior of consumers is unpredictable.18. Even if one could predict the behaviour of an individual buyer, it would not be profitable for marketers to try to do so.19. Some consumer groups exhibit more complex behaviour than others do.20. Purchase behaviour is not subject to the same whims as other aspects of human behaviour.Section FWhen any company moves from a sales to a marketing approach, it is not just a case ofre-titling the Sales Director as Marketing Director and doubling the advertising budget. It requires a complete reorientation in thinking and a revolution in how a company organises and practises its business activities. Whereas selling focuses on the needs of the seller, marketing focuses on the needs of the buyer. Whereas selling is preoccupied with the seller’s need to convert his or her product into cash, marketing is preoccupied w ith the idea of identifying and hence satisfying the needs of the customer. However, subscribing to a philosophy of marketing, even though an important first step, is not the same as putting that philosophy into practice.21. Advertising budgets are normally doubled when a company moves over to a marketing approach.Section GThe corporate mission statement needs detailed consideration by top management to establish the business the company is really in and to relate this consideration to future business intentions. It is a general statement that provides an integrating function for the business, from which a clear sense of business definition and direction can be achieved. By formulating a clear business statement, boundaries for the ‘corporate entity’ c an be conceived in the context of wider environmental trends that influence the business. This stage is often overlooked in marketing planning, and yet without it the marketing plan will lack a sense of contribution to the development of the total business.22.The boundaries of a corporate entity can only be assessed in the context of wider environment trends.23.A corporate mission statement enables top management to define the future direction of a business.24.Marketing planning does not often take account of the corporate mission statement.25. Different functions within a business are likely to interpret the mission statement in different ways.Section HThe adoption and application of performance management methods requires many different changes in behaviour and attitudes up and down the organisation. These methods are not merely techniques; they are ways of life and a philosophy of management. Thus the introduction of performance management systems must come as part of an organisation’s commitme nt to change its culture. Only top management commitment to a new way of managing, often triggered by a crisis, can support such a massive undertaking.29. The support of top managers is essential in changing organisational culture.31. Using performance management systems for the first time requires minimaladaptations on the part of the organisation concerned.32. The adoption of performance management methods of itself will create changes in behaviour and attitudes.Section I The ‘prudence rule’, whi ch is sometimes known as conservatism, arises out of the need to make a number of estimates in preparing periodic accounts. Managers and owners are often naturally overoptimistic about future events. As a result, there is a tendency to be too confident about the future, and not to be altogether realistic about the organisation’s prospects. There may, for example, be undue optimism over thecredit-worthiness of new customers. Insufficient allowance may therefore be made for the possibility of bad debt. In turn, this might have the effect of overstating profit.Randall at kpmg33. Accountants should avoid making estimates when preparing periodic accounts.34. Most new customers are credit-worthy.35. Managers or owners are not often good judges of their cu stomers’ willingness or ability to pay.36. The ‘prudence rule’ prevents bad debt from arising.Section JA partnership is presumed to exist when two or more people get together in business with the objective of making a profit. The law limits the total number of people who may get together to form a partnership. Apart from a few exceptions, such as firms of accountants and solicitors, a partnership may not consist of more Than 20 partners. The partnership will be managed by general agreement among the partners, but if there is no apparent agreement either formal or informal, then it is presumed that the partnership will operate in accordance with the Partnership Act, 1890. This Act lays down arrangements for dealing with such matters as the amount of capital to be contributed, the management of the business, and the division of the profits or losses among the partners.37. Some agreement must exist between partners as to the way they manage the partnership.Section EThe amount of accounting information that could be supplied to any interested party is practically unlimited. The information needs to be designed in such a way that it meets the objectives of the specific user group. If too much information is given, the user might think that it is an attempt to mislead them, and as a result all of the information may be totally rejected. In this context, accountants try to present accounts in such a way that they represent ‘a true and fair view’. The Companies Act, 1985, for example, requires company accounts to reflect this particular criterion, and it is advisable to apply it to all organisational entities. Unfortunately the Act does not define what is meant by ‘true and fair’, but it is assumed that accounts will be so if an entity has followed the rules laid down in appropriate accounting and financial reporting standards.19. It is a positive feature of the Companies Act, 1985, that it does not define what is meant by ‘true and fair’.20. In practice, the proper application of accounting and financial reporting standards ensures that accounts meet the criteria of being ‘true and fair’.Section FThe style that individual managers choose to adopt depends in no small part on how they regard their subordinates. At one extreme, some will assume that the average employee has an inherent dislike of work and will avoid it if they can. They believe employees need to be controlled, directed, offered rewards or threatened with punishments to get them tomake adequate efforts towards the achievement of organisational goals. On the other hand, some will take the view that, according to the conditions, work can be a source of satisfaction or dissatisfaction. Employees are not seen as naturally passive, or resistant to organisational objectives, but have been made so by experience. The most significant reward that can be offered employees is the satisfaction of their need for personal growth and self-development21. Using rewards and punishments is a necessary part of organisational life.经典36题答案Example1:T Example2:F Example3:C Example4:FA:1 C2 T 原文第二句3 C 比较级,原文未提及4 C 未提及B:5 F 与原文意思相反6 C 未提及7 F No Consumer全否定8 T 原文C:9 C 原文未表达比较意思10 T 原文11 C12 CD:13 F 与原文意思相反not14 T15 C16 FE:17 C18 T 原文19 C20 F 相反F:21 C 未提及是哪个的两倍G:22 F 缺少修饰语23 T 第一句24 T 原文25 C 未提及H:29 T31 C未提及32 F 一个是require 一个是create 意思相反I:33 C未提及34 C未提及35 T36 F 相反J: 37 FOther:E: 19 F Positive不对20 F 一个是assume,一个是in practice F: 21 F。