财政预算 hnd

HND项目专业大三财政预算答案报告参考Outcome3

Preparing Financial Forecasts – Outcome 3Report to ManagementPrepared by: accountantDate: 02/3/2019IntroductionYou asked me to make a budget according to the company's situation, Prepare the calculation about the variance.For example, materials include total, usage and price, labour include total, efficiency and rate and total overhead. Finally, prepare a report for management based on the budget and provide SuggestionsFlexed Budget StatementPossible Reasons for VariancesDirect Material Total Variance: £2,000 F made up of:Direct Material Usage Variance:- £30,000 UDirect Material Price Variance:£ 32,000 FReasons for Direct Material Usage VarianceThe budgeted amount is 13,500 kilograms, while the actual amount is 16,000 kilograms.The possible reason for this change is that the company orders more, so the actual consumption increases.Reasons for Direct Material Price VarianceThe budget price is 12 / kg, but the actual price is 10 / kg. The possible reason for this change is that maybe the material used by the company is not good enough in quality, so the price is lowerDirect Labour Total Variance: -£5,000 U made up of:Direct Labour Efficiency Variance:£10,000 FDirect Labour Rate Variance: -£15,000 UReasons for Direct Labour Efficiency VarianceThe estimated working hours were 11,250 hours, while the actual working hours were 10,000 hours. The possible reason for this change was that the working hours were shortened due to the improvement of employees' working efficiency.The budget price is 8 pounds per hour, while the actual price is 9.5 pounds per hour. This change may be due to the increased demand of employees or the lack of sufficient labor forceReasons for Direct Labour Rate VarianceThe budget price is 8 pounds per hour, while the actual price is 9.5 pounds per hour. This change may be due to the increased demand of employees or the lack of sufficient labor forceTotal Overhead Variance:-£400 UThe direct material,direct labour,variable overhead,administration and insurance have changed.The possible reasons for this change are the improvement in working efficiency and the fact that employees can complete more work in a shorter time, or the company finds an alternative and cheaper product, which makes variable overhead reduced.RecommendationsAs can be seen from the fixed budget statement, labor costs have increased, and variable production costs have far exceeded the budget, possibly due to insufficient labor force. Therefore, I suggest that the company should attract more employees and purchase more raw materials。

HND SQA 财政预算outcome3 答案

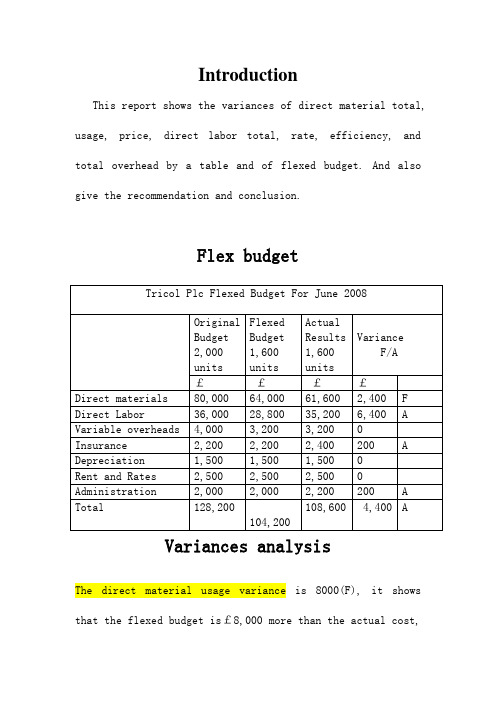

IntroductionThis report shows the variances of direct material total, usage, price, direct labor total, rate, efficiency, and total overhead by a table and of flexed budget. And also give the recommendation and conclusion.Flex budgetVariances analysisThe direct material usage variance is 8000(F), it shows that the flexed budget is£8,000 more than the actual cost, as a result of the using of higher-grade materials and changing of the way of production.The direct material price variance is 5600(A), which means that the actual price is£5600 more than the flexed budget price, because of the Tricol PLC had changed their supplier and purchase the higher-grade material lead to the price raised from £10 per/kg to£11 per/kg.The direct material total = direct material usage – direct material price.As calculated above, 8000-5600=2400, the direct material total variance is£2400.The direct labor rate variance is 3520(A), which means that the actual labor rate is£3520 more than the flexed budget, caused by the company supplied a higher-than-expected wage, the labor cost raised fro m£9 per hour to£10 per hour, and may because Some employees still apprentices, with poor efficiency.The direct labor efficiency variance is 2880(A), as to say, the actual labor efficiency is£2880 more than flexed budget efficiency.It may be because the machine on the production line equipment getting old and it influence the efficiency of employees at the time of production, or maybe the culture of the company is not so well at current time, which result in reduced efficiency.The direct labor total variance is 6400(A) caused by the labor rate variance and efficiency variance. It shows that the actual total labor is £6400 more than the flexed budget total labor.The total overhead variance is 400(A) that means the actual total overhead is £400 more than flexed budget, which caused by the changing of administration overhead and insurance cost both. These two things may change by the company change the salary of the management, and they may add extra insurances for the employees or the machinery.ConclusionThere is a policy of the company in which the company applies a rate of significance of 3% for any Variance analysis. According to the data above, we can clearly see that all the actual variances are higher than 3%, it may caused by the actual production for June was 80% of the target amount, and there are some respects had been changed in the factory.RecommendationI’d give some advices to Tricol Plc for improving their business.●To improve the efficiency not only by increase the salary but alsochange the way of production.●The company may discuss with the new supplier to lower rawmaterial prices.●Training a group of experienced staff.Appendix1. Direct material total variance(Standard units of actual production *standard price) - (actual quantity* actual price)10*4*1600- 61600=2,400(F) 2400/64000=3.75%2. Direct material usage varianceStandard price*(standard units of actual production –actual units)10*(4*1600-5600) =8,000(F) 8000/64000=12.5%3. Direct material price varianceActual quantity *(standard price –actual price)5600*(10-11) =5,600(A) 5600/64000=8.75%4. Direct labor total variance(Standard hours of actual production*standard rate ph) –(actual hours*actual rate ph)2*1600*9-35,200=6400(A) 6400/28800=22.22%5. Direct labor efficiency varianceStandard rate ph*(standard hours of actual production- actual hours)9*(1,600*2-3,520) =2880(A) 2880/28800=10%6. Direct labor rate varianceActual hours*(standard rate ph-actual rate ph)3520*(9-10) =3,520(A) 3520/28800= 12.22%7. Total overhead varianceTotal standard overhead for actual production- total actual overheads (1600*2-3,200) - (8,200-8,600) =400(A) 400/ (3200+8200) =3.51 %。

HND-财政预算OUTCOME-34报告

A financial analysis report for Tricol plcOutcome 3and4Class;10E6Name:Ma bodaSCN:Candidate Num:22IntroductionTo operate better in financial aspect, the management of Tricol plc asked me to analyze their financial condition then make recommendations for them.FindingsPart A(ⅰ) Flex budget in line with actual activity(ⅱ) Variances calculationDirect material total variance(Standard units of actual production*standard price) -(actual quantity*actual price) (4 kg*1,600*£10) -£61,600 =£2,400 (F)Rate of significance: (3.75%)Direct material usage varianceStandard price*(standard units of actual production -actual quantity)£10*[ (4kgⅹ1,600) -5,600kg]= £8,000 (F)Rate of significance (12.5%)Direct material price varianceActual quantity * (standard price -actual price)5,600kg*[£10 -(£61,600/ 5,600kg) ]= £(5,600) (A)Rate of significance: (8.75%)Direct labour total variance(Standard hours of actual production*standard rate ph) - (actual hours*actual rate ph) [ (2hrs*1,600) *£9]-£35,200=£(6,400) (A)Rate of significance: (22.22%)Direct labour efficiency varianceStandard rate ph* (standard hours of actual production -actual hours)£9*(2hrs*1,600-3,520hrs)=(2,880) (A)Rate of significance: (10%)Direct labour rate varianceActual hours*(standard rate ph – actual rate ph)3,520hrs*(£9*-£35,200/3,520hrs)= £(3,520) (A)Rate of significance: (12.22%)Total overhead varianceTotal standard overhead for actual production -total actual overheads(£18,000/12+£2,500+£2,200+£2,000)- (£1,500+£2,500+£2,200+£2,400)=£(400) (A)Rate of significance: (3.5%)(ⅲ) Report about variancesDirect material varianceThe direct material total variance can be analyzed in two aspects which are direct material volume and direct material price.For volume side, as calculated above, the budget volume is 6400kg; the actual volume is 5600kg.So there is 800kg variance which is favorable and each unit variance is0.5kg.The likely reason causing the variance comes from three aspects.First of all, the company upgraded the production machinery recently, and new machine may use materials efficiently, so it reduced the waste of materials.Secondly, the company switched suppliers and using higher-grade materials can decrease waste of materials too.Finally, the company has concluded a higher-than-expected wage settlement forproduction operatives, which will maintain employees with higher skills as well as decrease turnover of employees, and it also can increase efficiency in using materials.For price aspect, the budget price is £10 per kg, and the actual price is £11per kg, it is adverse that one pound over the budget price.The company switching suppliers may cause the increase of negotiation cost.There may be a long-term relationship between Tricol plc and its old suppliers, so the suppliers may take lots of discounts to the firm.After changing suppliers, the discount may disappear.Furthermore, higher grade materials increased unit price.Overall, the total material variance is favorable.£8,000 -£5,600=£2,400.Direct labour varianceThe direct labour total variance is composed of direct labour efficiency variance and direct labour rate variance.The budget direct labour hours are 3,200hrs and the actual labour hours are 3,520 hrs.There are more 320hrs needed than the budget, and each unit is 0.2hrs, which it is obviously adverse.The company upgrading the production machinery may need time for employees to adopt it.Also, employees need training time.The rebuild process of machinery consumed time too.In a word, the chargeable hours have increased.The budget direct laour hours rate is £9 per hour, the actual hours rate is £10 per hour.It is adverse that one pound higher than budgeted.It is possible caused by both internal and external factors.Higher-than-expected wage settlement may be internal reason for the variance, and new machinery may be needed to recruit new employees to operate the machinery, which also can increase the expense.For external factors, the changing of labour market may increase labour cost; the government legislation alsocan increase the labour cost, for example minimum pay.Both direct labour efficiency and direct labour rate variances are adverse, so the direct labour total variance is adverse.✧Overhead varianceAs calculated above, total overhead variance is caused by administration and insurance.Each factor has £200 variance, so the total overhead variance is £400 and it is adverse.During the process of changing supplier, the company needed more expense on public relationship or negotiation, in addition, in order to maintain the new machinery, administration cost will be increased too.For insurance aside, the improvement of machinery will need more insurance fees to cover, which also contributes to the increase of insurance fee of new employees.Part B◆Selection and application of two investment appraisal techniquesAs the company is keen to recoup the cost of the investment within five years, I will choose Payback period and Net Present Value to help me complete the appraisal.In order to fulfill the appraisal easily, there are some assumptions listed below should be considered before the appraisal.⑴ All revenue and inflow are assumed cash flow⑵ All investment cost incurred in year 0⑶ No uncertainty is considered⑷ Do not consider inflation and taxation⑸ Market rate of return is expected rate of return⑹ Rate of return is varying along with timeNote: req uire 40,000/320,000 in year 5= 1/8*year=1.5 moths Payback=4 years 1.5 moths◆Recommendation about investmentAccording to Payback Period analysis, the investment cost can be recouped in year 4 and 1.5 moths.In other words, the period is under company’s expectation.The project can be executed.However, according to Net Present Value analysis, in terms of present value, within five years, what the NPV will bring net result is net cash loss but not net cash surplus.In general, the company should consider time value and other factors, so the project should not be executed.◆Factors impact on the investment should be consideredVarious factors will impact on result of investment.I will outline factors should be considered when the management reviewing my recommendation in financial and non-financial factors.✧Financial factorAs distribution arm is financial long-term beneficial project, it can be used inlong-term period and bring benefits continuous.The investment cost is £1,000,000, which can be considered a large investment.So it more likely needs long period payback period.The management should focus on longer cash flows for longer periodof future.On the other hand, Net Present Value in year five is (28,000) only take 2.8% percents of the investment cost, it is more likely surplus in year six.Another financial factor is source of million pounds.If it is internal source, the management mainly concentrate on opportunities cost.If it is cost of capital or cost of capital taking much weight of the source, the management must pay cost of the source firstly, the marketing rate of return likely low for the company, in addition, the management should use higher discounted cash flow.Non-financial factorThe investment must be consistence with company’s strategic plan.As Tricol is a plc, it must take social responsibility such as obeying government policy, minimizing impact on environment and minimizing impact on natives.ConclusionFor real competition is more complex and fierce, in order to make accurate decisions, management should consider more factors during the decision-making; furthermore, the management should use more tools to help them such as IRR, DCF.。

【HND】财政预算OUTCOME2-

Part1(1)(2) The variances are calculated as followed:DIRECT MATERIAL TOTAL VARIANCE(STANDARD UNITS OF ACTUAL PRODUCTION×STANDARD PRICE) —(ACTUAL QUANTITY×ACTUAL PRICE)[(4kg×1,600)×£10]—£61,600=£64,000—£61,600=£2,400 (F)DIRECT MATERIAL PRICE VARIANCEACTUAL QUANTITY×(STANDARD PRICE—ACTUAL PRICE)5,600kgs×(£10—£61,600/5,600kgs)=5,600kgs×(£10—£11)= £5,600 (A) DIRECT MATERIAL USAGE VARIANCESTANDADR PRICE×(STANDARD UNITS OF ACTUAL PROCUTION—ACTUAL UNITS)£10×[(4kg×1,600)—5,600kgs]= £8,000 (F)DIRECT LABOUR TOTAL VARIANCE(STANDARD HOURS OF ACTUAL PRODUCTION×STANDARD RATE ph) —(ACTUAL HOURS×ACTUAL RATE ph)[(2hours×1,600)×£9]—£35,200=£2,8800—£35,200=£6,400 (A)DIRECT LABOUR RATE VARIANCEACTUAL HOURD×(STANDARD RATE p.h. —ACTUAL RATE ph)3,520hrs×(£9—£35,200/3,520hrs)=3,520hrs×(£9—£10)= £3,520 (A)DIRECT LABOUR EFFICIENCY VARIANCEACTUAL HOURS×(STANDARD HOURS OF ACTUAL PRODUCTION—ACTUAL HOURS)£9×[(2hours×1,600)—3,520hrs]= £9×320=£2,880 (A)OVERHEAD TOTAL VARIANCETotal Standard Overhead for actual production—Total Actual Overheads£2×1,600+£2,000+£2,500+£1,500+£2,200—(£3,200+£2,200+£2,500+£1,500+£2,400)=400 (A)(3) In the first part, we have calculated cost variances for Tricol plc at June. It totally produced 4,400 adverse variance that include £2,400 favorable material variance, £6,400 adverse labor variance and £400 adverse overheads variance. All these variances have exceeded the rate of significance of 3%.Direct material total variance can be divided into two components: the direct material usage variance and the direct material price variance. Direct material total variance ofTricol plc in June is £2,400 (F) with the rate of significance of 3.75%( The level of significance of Direct Material Total Variance=400/64,000=3.75%). The direct material usage variance is the favorable variances in £8,000, a rate of significance is 12.5%( The level of significance of Direct Material Usage Variance =8,000/64,000=12.5%), the possible reasons for this variance may be the company use higher quality raw material and higher grade workforce. the direct material price variance is £5,600 (A), and a rate of significance is 8.75%( The level of significance of Direct Material Price Variance=5,600/64,000=8.75%). The reason is the company has switched supplier and using higher-grade materials; and because the fluctuations of exchange rate in the international market react on price of the raw materials. Similar with direct material total variance, the Direct Labour Total Variance was made up by the Direct Labour Rate Variance and Direct Labour Efficiency Variance. It is a adverse variance of Tricol plc in June (£6,400) with the rate of significance of 18.18% (The level of significance of Direct Labour Total Variance =6,400/35,200=18.18%). The direct labor efficiency variance is the adverse variance in £2,880, and a rate of significance is 8.18% (The level of significance of Direct Labour Efficiency Variance =2,880/35,200=8.18%). The reason for this variance may be the company lowers its workforce grade and also the morale. Possibly it is that the company conducts the pay rise which is higher than expected for production operatives, or it lack qualified and skilled labor to operate the upgraded machinery lead a adverse variance in the direct labor rate, at £3,520 , with a rate of significance as 10% (The level of significance of Direct Labour Rate Variance =3,520/35,200=10%).The overheads total variance in June was £400 which was a adverse variance. The level of significance of Overhead=400/12,200=3.3%. There are two factors cause this. First, the insurance fee exceed anticipated budget. Second, there occur extra administration overheads.For all the variance above, there are some recommendations presented in the follows: All the variances rate of significance are more than 3%, so a detail analysis of all the aspects should be taken, and find out a settlement for this problem, as to eliminate theadverse variances and holding the favorable variances. The company has recently concluded a higher-than-excepted wage, however, the labor efficiency decreased. The management needs to do a farther research.Considering the adverse variance of material price, the purchasing department endeavor to negotiate with the supplier about the extra discount, if it signs a long-term and large purchasing contract with the supplier; or search for new supplier who can provide the same higher-grade material with relative lower price.Appendix1. Payback Period:Year Annual Cash Flow Cumulative0 (£1,000,000) (£1,000,000)1 £160,000 (£840,000)2 £160,000 (£680,000)3 £320,000 (£360,000)4 £320,000 (£40,000)5 £320,000 £280,000Payback period = 4 years and 1.5 months (40,000/320,000) 2. Discounted Cash Flow:Year PV factor - 10% Cash Flow NPV Cumulative0 1.000 (£1,000,000) (£1,000,000) (£1,000,000)1 0.909 £160,000 £145,440 (£854,560)2 0.826 £160,000 £132,160 (£722,400)3 0.751 £320,000 £240,320 (£482,080)4 0.683 £320,000 £218,560 (£263,520)5 0.621 £320,000 £198,720 (£64,800)Net Present Value for the Project = £-64,800Part 21.There are some key assumptions should be clearly stated(1)The management should assume that the given ‘market rate of return’ will notvary.(2)Managers should ignore the impact of taxation and inflation on the abovefigures.(3)The figures of expect revenue which appear in this report are net cash flow,after paid off all relevant costs.(4)Assuming that the total cost of the project will be payable at the beginning. 2.The calculation and analysis of two investment appraisal technique.(1) Payback Period:Payback as a method of investment appraisal measures the number of years it is expected to take to recover the cost of the original investment. Payback period is 4 years and 1.5 months. In the 5th year after the investment, the huge investment will get a complete return, and obtain the net present value of the return at £280,000 from this project. So, the payback is applicable.(2) Discounted Cash Flow:With this technique, the company would not return their investment. The market rate of return on investment projects is 10%, the Tricol plc will not recover its investment over the next 5 years, the net present value of the return is £935,200, and the net present value for the project is a negative numerical that means a loss of £64,800. So the DCF technique indicted that this investment was not appeared to be profitable.3.On the basis of the above investment appraisal analysis, the management shouldbe recommended that the planned investment should not go ahead. Because net present value for the Project is £-64,800. That is to say the company can not recover the original investment. However, the present value of the return shall not be used for completely indicate the recovery of the cost, so the recommendation is that the management should think the following additional factors over.4.Some other factors which the management should consider.This planned investment may have a long-term revenue return after 5 years.For example, the motor vehicles may have residual values and the land or buildings will have a longer useful life. The management could consider the revenue for longer than 5 years.●The management would consider that whether the invest plan has fit thecompany’s overall corporate strategy.●The financial condition should also be considered. Is the company hassufficient funds? In another words, does the current cash flow position can support such an investment.。

HND财政预算OUTCOME34报告

A financial analysis report for Tricol plcOutcome 3and4Class;10E6Name:Ma bodaSCN:125099297Candidate Num:22IntroductionTo operate better in financial aspect, the management of Tricol plc asked me to analyze their financial condition then make recommendations for them.FindingsPart A(ⅰ) Flex budget in line with actual activityTricol plc Flexed Budget for JuneOriginal budget FlexedbudgetActualresultsVariance2000 units 1600 units 1600unitsF/A££££Direct material 80,000 64,000 61,600 2,400 F Direct labor 36,000 28,800 35,200 6,400 A Variable productionoverhead4,000 3,200 3,200 0 Fixed costDepreciation 1,500 1,500 1,500 0 Rent and rates 2,500 2,500 2,500 0 Administration overhead 2,000 2,000 2,200 200 A Insurance costs 2,200 2,200 2,400 200 A Total 128,200 104,200 108,600 4,400 A(ⅱ) Variances calculationDirect material total variance(Standard units of actual production*standard price) -(actualquantity*actual price)(4 kg*1,600*£10) -£61,600 =£ 2,400 (F)Rate of significance: (3.75%)Direct material usage varianceStandard price*(standard units of actual production - actual quantity) £ 10*[ (4kgⅹ1,600) -5,600kg]= £8,000 (F)Rate of significance (12.5%)Direct material price varianceActual quantity * (standard price - actual price)5,600kg*[£ 10 -(£61,600/ 5,600kg) ]= £ (5,600) (A)Rate of significance: (8.75%)Direct labour total variance(Standard hours of actual production*standard rate ph) - (actual hours*actual rate ph)[ (2hrs*1,600) *£9]-£35,200=£(6,400) (A)Rate of significance: (22.22%)Direct labour efficiency varianceStandard rate ph* (standard hours of actual production - actual hours) £9*(2hrs*1,600-3,520hrs)=(2,880) (A)Rate of significance: (10%)Direct labour rate varianceActual hours*(standard rate ph – actual rate ph)3,520hrs*(£9*-£35,200/3,520hrs)= £(3,520) (A)Rate of significance: (12.22%)Total overhead varianceTotal standard overhead for actual production - total actual overheads (£18,000/12+£2,500+£2,200+£2,000)- (£1,500+£2,500+£2,200+£2,400)=£(400) (A)Rate of significance: (3.5%)(ⅲ) Report about variancesDirect material varianceThe direct material total variance can be analyzed in two aspects which are direct material volume and direct material price.For volume side, as calculated above, the budget volume is 6400kg; the actual volume is 5600kg. So there is 800kg variance which is favorable and each unit variance is 0.5kg. The likely reason causing the variance comes from three aspects. First of all, the company upgraded the production machinery recently, and new machine may use materials efficiently, so it reduced the waste of materials. Secondly, the company switched suppliers and using higher-grade materials can decrease wasteof materials too. Finally, the company has concluded ahigher-than-expected wage settlement for production operatives, which will maintain employees with higher skills as well as decrease turnoverof employees, and it also can increase efficiency in using materials.For price aspect, the budget price is £10 per kg, and the actual priceis £11per kg, it is adverse that one pound over the budget price. The company switching suppliers may cause the increase of negotiation cost. There may be a long-term relationship between Tricol plc and its old suppliers, so the suppliers may take lots of discounts to the firm. Afterchanging suppliers, the discount may disappear. Furthermore, higher grade materials increased unit price.Overall, the total material variance is favorable. £8,000 -£5,600=£2,400.Direct labour varianceThe direct labour total variance is composed of direct labour efficiency variance and direct labour rate variance.The budget direct labour hours are 3,200hrs and the actual labour hours are 3,520 hrs. There are more 320hrs needed than the budget, and each unit is 0.2hrs, which it is obviously adverse. The company upgrading the production machinery may need time for employees to adopt it. Also, employees need training time. The rebuild process of machinery consumed time too. In a word, the chargeable hours have increased.The budget direct laour hours rate is £9 per hour, the actual hours rate is £10 per hour. It is adverse that one pound higher than budgeted. It is possible caused by both internal and external factors.Higher-than-expected wage settlement may be internal reason for the variance, and new machinery may be needed to recruit new employees to operate the machinery, which also can increase the expense. For external factors, the changing of labour market may increase labour cost; the government legislation also can increase the labour cost, for example minimum pay.Both direct labour efficiency and direct labour rate variances are adverse, so the direct labour total variance is adverse.✧Overhead varianceAs calculated above, total overhead variance is caused by administration and insurance. Each factor has £200 variance, so the total overhead variance is £400 and it is adverse. During the process of changing supplier, the company needed more expense on public relationship or negotiation, in addition, in order to maintain the new machinery, administration cost will be increased too. For insurance aside, the improvement of machinery will need more insurance fees to cover, which also contributes to the increase of insurance fee of new employees.Part B◆Selection and application of two investment appraisal techniquesAs the company is keen to recoup the cost of the investment within five years, I will choose Payback period and Net Present Value to help me complete the appraisal.In order to fulfill the appraisal easily, there are some assumptions listed below should be considered before the appraisal.⑴ All revenue and inflow are assumed cash flow⑵ All investment cost incurred in year 0⑶ No uncertainty is considered⑷ Do not consider inflation and taxation⑸ Market rate of return is expected rate of return⑹ Rate of return is varying along with timeTricol plc Payback period for project distribution armYear Net cash flow Cumulative Cash Flow££Cash Flow Year 0 (1,000,000) (1,000,000) Cash Inflow Year 1 160,000 (840,000)Year 2 160,000 (680,000)Year 3 320,000 (360,000)Year 4 320,000 (40,000)Year 5 320,000 280,000 Net Cash Benefit Year 5 280.000 Note: req uire 40,000/320,000 in year 5= 1/8*year=1.5 mothsPayback=4 years 1.5 mothsTricol plc Net Present Value for project distribution armPresent Value Annual cash flow Present valuefactors at 10%£££Year 0 (1,000,000) 1.000 (1,000,000) Year 1 160,000 0.909 145,440Year 2 160,000 0.826 132,160Year 3 320,000 0.751 240,320Year 4 320,000 0.683 218,560Year 5 320,000 0.621 198,720 935,200 NPV (64,800)◆Recommendation about investmentAccording to Payback Period analysis, the investment cost can be recouped in year 4 and 1.5 moths. In other words, the period is under company’s expectation. The project can be executed. However, according to Net Present Value analysis, in terms of present value, within five years, what the NPV will bring net result is net cash loss but not net cash surplus. In general, the company should consider time value and other factors, so the project should not be executed.◆Factors impact on the investment should be consideredVarious factors will impact on result of investment. I will outline factors should be considered when the management reviewing my recommendation in financial and non-financial factors.✧Financial factorAs distribution arm is financial long-term beneficial project, it can be used inlong-term period and bring benefits continuous. The investment cost is £1,000,000, which can be considered a large investment. So it more likely needs long period payback period. The management should focus on longer cash flows for longer period of future. On the other hand, Net Present Value in year five is (28,000) only take 2.8% percents of the investment cost, it is more likely surplus in year six. Another financial factor is source of million pounds. If it is internal source, the management mainly concentrate on opportunities cost. If it is cost of capital or cost of capital taking much weight of the source, the management must pay costof the source firstly, the marketing rate of return likely low for the company, in addition, the management should use higher discounted cash flow.Non-financial factorThe investment must be consistence with company’s strategic plan. As Tricol is a plc, it must take social responsibility such as obeying government policy, minimizing impact on environment and minimizing impact on natives.ConclusionFor real competition is more complex and fierce, in order to make accurate decisions, management should consider more factors during the decision-making; furthermore, the management should use more tools to help them such as IRR, DCF.。

sqahnd财政预算34.docx

Contents1.0 Introduction ...................................................................................................................... - 2 -2.0 The flexed budget ............................................................................................................. - 2 -3.0 Calculate the Materials variances, Labour variances and the Total overhead.....- 2 -3.1Direct the materials variances , labour variances and the total overhead....- 2 -3.2Variance analysis ................................................................................................... - 3 -4.0 The recommendations for management (variances) ........................................................ - 4 -5.0 Using four different methods to evaluate the financial .................................................... - 5 -5.1Identify the accounting rate of return ..................................................................... - 5 -5.2Identify the payback .............................................................................................. - 5 -5.3Identify the Net present value ................................................................................ - 5 -5.4Identify the Internal rate of return ......................................................................... - 6 -6.0 Recommendations for investment decision ...................................................................... - 6 -7.0 Conclusion ........................................................................................................................ - 7 -8.0 Appendices ....................................................................................................................... - 7 -1.0 IntroductionThis report will divided into two parts. Part A and Part B. In Part A,First of all, I will prepare a flexed budget in line with actual activity. Second, this will including the Materials variances, Labour variances and total overhead. At the same time, I will identify a minimum of one possible cause of the each variance. Finally, according to data analysis, there have been some recommendations to management of Matteck PLC. In Part B, It will have four different ways to evaluate financial performance and give recommendations for Matteck PLC. These ways are ARR ,Payback, NPV and IRR.Part A2.0 The flexed budgetFor Flex budged of Matteck PLC, we can see the Appendix 1.3.0 Calculate the Materials variances, Labour variances and the Total overhead.3.1Direct the materials variances , labour variances and the total overhead・This section shows the Appendix 2.3.2Variance analysis.Material price variance:The material price variance is £32,000(F). According to the data analysis, it is £2/kg less expensive-2-than planned. The possible reasons can be divided into three points: first, they could replace raw materials, using a lower - grade material. Second, the supplier to provide some discount for this batch of raw materials. Finally, learn from the case, the company has managed to locate new materials from an overseas. Due to the product from overseas, according to different exchange rate, the material will reduce the price.Material usage variance:The material usage variance is £30,000(A). The possible reasons include the effects of raw materials and the influence of the machine. If the company using poor quality raw materials, it may be more difficult to work. This will increase the waste materials. At the same time, the case shows that the company's new machinery can be fully used in the second week. The delay time may have caused the machine to use more materials than planned.Material total variance:The material total variance is 2,000(F). Case shows that the company's raw materials are from overseas suppliers. This will reduce some costs. Which leads to the material price variance is 32,000 (F). On the other hand, the company has introduced a new machine, the influence of machine installed time, caused some wasted of materials. This makes the material usage variance is €30000 (A). Even if The company's material total variance is 2000 (F). The company's management still should pay attention to The utilization of raw materials.Labour efficiency variance:The Labour efficiency variance is 10,000(F). The possible reasons could include the new machine to improve staff work cfYiciency. Using new machine can less labour hours. At the same lime , the case shows that the company has had to employ more highly qualified staff. They can increase theworking efficiently through the higher skill.Labour Rate Variance:The Labour rate variance is 15,000(A). Through the calculation, the labour rate is £1.50 per hour higher than original. The possible reasons is £1.50 per hour higher than planned. The cost of direct labour is adverseness for this firm.Labour Total Variance:the Labour total variance is 5,000(A). The reasons of variance, the company has introduced the newmachine, As the result the direct labor efficiency variance is favorable which is 10.000(F). On other hand, the labour rate is higher than standard labour rate. Finally, lead to the labour total variance is adverse,4.0 The recommendations for management (variances)・1.The company should be had a variety of data investigation to set up complete data system. At the same time, through the difierent variance, the company can know more about the market information.2.The company should intensify the performance monitor for statTbecause the lower performance will accelerate waste of material and then lead to the material usage is increase, the performance monitor can help the company shrink the variance.3.Management: the company can provide some motivation policies to motivate the staft' that is work hard and enhance the work enthusiastic of the staff. This can improve the staff work efficiency.Part B5.0 Using four different methods to evaluate the financial. 5.1 Identify the accounting rate of return ・ARRAverage profit= 3,300,0005=660,000Accounting rate of retum==26.4%The cases show that the company should have an accounting rate of return of at least 15%, through calculation, the ARR is 26.4%. Therefore, the data has meet company standards.5.2 Identify the payback.The company hopes to recover the cost of the investment within 4 four years. In fact, they just use 3 years 341 days, (see Appendix 3.)5.3 Identify the Net present value.The NPV method calculates the present values of cash inflows and outflows and establishes whether. Basically, NPV provides an objective for evaluating and selecting investment projects. Moreover, it takes into account required rate of return of company and then takes into account time value of money. But there are substantial660,000 2,500,000uncertainly factors in our world. For instance the inflation and deflation, the exchange rate. When the Matteck's cost of capital is 10%. The NPV is (46200). The NPV value less than 0. The company should not invest this project. ( see Appendix 4.)5.4Identify the Internal rate of return.When the present value is 5%, the internal rate of return is 9.39%. Which less than 10% of company slandard.thcrcfore,the company should not invest this project.(see Appendix 5)6.0 Recommendations for investment decision.1.According the four method, The ARR and Payback are both implement for this project, but the NPV and IRR are not implemented for this Project. In this case ,thc company should focus on the NPV and IRR.2.By calculates the net present values, it seems that the deficit, which means that the annual cash flows are not enough to allow more interest to be deducted and still repay the original investment. This investment is unworthy .3.Within five years. All the market factors are changeable. The information will have different change. And there are maybe some other situations occurred. So the Matteck PLC should not concern with the project.7.0 ConclusionThe report can help the company make the flex budget, and then by variances analysis and use the-6-four methods to evaluate the financial. Through the recommendations can help the company choose the best investment to gain the maximum profits.8.0 Appendices8.1Appendix 18.2Appendix 2-7-。

HND SQA 财政预算outcome3 答案

IntroductionThis report shows the variances of direct material total, usage, price, direct labor total, rate, efficiency, and total overhead by a table and of flexed budget. And also give the recommendation and conclusion.Flex budgetVariances analysisThe direct material usage variance is 8000(F), it shows that the flexed budget is£8,000 more than the actual cost,as a result of the using of higher-grade materials and changing of the way of production.The direct material price variance is 5600(A), which means that the actual price is£5600 more than the flexed budget price, because of the Tricol PLC had changed their supplier and purchase the higher-grade material lead to the price raised from £10 per/kg to£11 per/kg.The direct material total = direct material usage – direct material price.As calculated above, 8000-5600=2400, the direct material total variance is£2400.The direct labor rate variance is 3520(A), which means that the actual labor rate is£3520 more than the flexed budget, caused by the company supplied a higher-than-expected wage, the labor cost raised from£9 per hour to£10 per hour, and may because Some employees still apprentices, with poor efficiency.The direct labor efficiency variance is 2880(A), as to say, the actual labor efficiency is£2880 more than flexedbudget efficiency.It may be because the machine on the production line equipment getting old and it influence the efficiency of employees at the time of production, or maybe the culture of the company is not so well at current time, which result in reduced efficiency.The direct labor total variance is 6400(A) caused by the labor rate variance and efficiency variance. It shows that the actual total labor is £6400 more than the flexed budget total labor.The total overhead variance is 400(A) that means the actual total overhead is £400 more than flexed budget, which caused by the changing of administration overhead and insurance cost both. These two things may change by the company change the salary of the management, and they may add extra insurances for the employees or the machinery.ConclusionThere is a policy of the company in which the company applies a rate of significance of 3% for any Variance analysis. According to the data above, we can clearly seethat all the actual variances are higher than 3%, it may caused by the actual production for June was 80% of the target amount, and there are some respects had been changed in the factory.RecommendationI’d give some advices to Tricol Plc for improving their business.●To improve the efficiency not only by increase thesalary but also change the way of production.●The company may discuss with the new supplier to lowerraw material prices.●Training a group of experienced staff.Appendix1. Direct material total variance(Standard units of actual production *standard price) - (actual quantity* actual price)10*4*1600- 61600=2,400(F) 2400/64000=3.75%2. Direct material usage varianceStandard price*(standard units of actual production –actual units)10*(4*1600-5600) =8,000(F) 8000/64000=12.5%3. Direct material price varianceActual quantity *(standard price –actual price)5600*(10-11) =5,600(A) 5600/64000=8.75%4. Direct labor total variance(Standard hours of actual production*standard rate ph) –(actual hours*actual rate ph)2*1600*9-35,200=6400(A) 6400/28800=22.22%5. Direct labor efficiency varianceStandard rate ph*(standard hours of actual production- actual hours)9*(1,600*2-3,520) =2880(A) 2880/28800=10%6. Direct labor rate varianceActual hours*(standard rate ph-actual rate ph)3520*(9-10) =3,520(A) 3520/28800= 12.22%7. Total overhead varianceTotal standard overhead for actual production- total actual overheads(1600*2-3,200) - (8,200-8,600) =400(A) 400/ (3200+8200) =3.51 %。

HND财政预算报告outcome 1

Beijing Institute of Technology SQA HND AssignmentTable of contentsIntroduction (3)Part A (3)Part B (5)Conclusion (6)Reference (6)Appendix (7)IntroductionThis report is for Tricol plc which makes a range of furniture and kitchenware. One of the most popular products is the Zupper expandable table. It will do some variance analysis in the Part A. It will includes direct material usage, direct material price, direct labor rate direct, labor efficiency and total overhead. Some suggestions will be given following the analysis. In Part B, there will take two methods to analyze the project that is whether to accept. It will discuss the advantages and disadvantages of the two methods, finding out the best methods that is suit for the company. At last, some other factors such as environment, technology, legal, and customers will be discussed for the managers. Furthermore, some needed appendixes will be followed the report.Part AVariance analysis and reportingOnce the variances have been calculated, they should be analyzed to find what the problems are. The criterion that the rate of variance needs to be analyzed is more than 3%, and according to the Appendix 3, as a result, it needs to analyze all the variances.Direct material usage:According to the Appendix 2, the variance of direct material usage is favorable, which is about £8000 and the rate of direct material usage variance reaches 12.5%. This is a high level and it may due to the two reasons such as higher quality materials and higher grade workforce. The company chooses the higher quality materials could reduce the spoilages during the producing. And it could reduce the inferiors in the finish products. To reduce the materials is as a result. Giving the labor higher workforce may reduce the mistakes by labors during the producing that will reduce the rejection rate and save the materials.Direct material priceAccording to the Appendix 2, the variance of direct material price is adverse, which is about £5600 and at the rate of 8.75%. There may be two reasons for this result. One is higher quality materials. Because of the higher quality, this kind of materials will be more expensive than other low quality materials. It will increase the costs of the materials. Also, the loss of discounts will be another reason to make the material price increase. Tricol may cooperate with a new supplier; company may not get the discounts received because of the low reliance.Direct labor rateAccording to the Appendix 2, the variance of direct labor rate is £3520 in adverse, and at the rate of 12.2%. There may be also two reasons for this result. One is salary increase award. Company made the labor rate become £10 per hour, which is higher than standard labor rate for £1 per hour. This could encourage the staffs to work hard and improve their efficiency and reduce the mistakes. Another reason may be the unplanned overtime. For this situation, company may pay more wages to the staffs for their overtime work.Direct labor efficiencyAccording to the Appendix 2, the variance of direct labor efficiency is adverse with £2880 in the rate of 10%. There are two reasons for this. One is may be the low morale. Because the company let its labors to work overtime for the unplanned goals and the high workforce will make the staffs unsatisfied. The second reason is that there may be shortage of skilled labor, which results in more labor hours and labors to finish the goals.Total overheadAccording to the Appendix 2, the variance of total overhead is £400 in adverse, and at the rate of 3.51%. It may due to the higher insurance, and higher administration. Company may spend too much on the insurance of its staffs. Some wages of the managers may be higher.Recommendation for the managementThe direct material usage is a good sign for the company. Company should continue to reduce the spoilages during its producing. However, the price of the materials are little higher. It is not a good sign. Company may purchase the lower quality materials from the new supplier. And try the best to get some discount received. The price of materials should be lower than before but quality could not be too lower. This action will reduce the costs in the materials and insurance the low rejection rate. According to the labor, company should not raise the employees’wages easily to motivate the staffs and it should not do much the unplanned overtime. Because of the much unplanned overtime, the staffs may against this action and become morale. So, company should reduce the unplanned overtime and use the other ways to encourage its staffs often. However, in order to finish the unplanned overtime, the company may hire some new employees to work. But there is shortage of skilled labor. Company should give them some training to improve their skills. The total overhead is not very good for the company. The insurance and administration may be higher for the company. Company should go to the greatest extent of reducing the costs in the insurance. It may be possible for company get some discount allowed form theinsurance company. And control the spending in the managing.Part BAssumptionThe premise of payback period methodsIdentify all of the costs of initial investment. Assume that they will be paid now. Find the cash inflow for each project. Add up cash flows each year until cost of project covered. Pick the project with the shortest payback period. If the payback period is only one year then it should be compared with an internal figureThe premise of discounted cash flow techniqueUncertainty does not exist. There is no inflation. The appropriate discount rate to use is known, to avoid unnecessary calculations. When undertaking DCF questions, the discount rates have been computed for you, and are given in the discount tables .Unlimited funds can be raised at a competitive rate.Analyzing payback period methodAccording to the payback period method, the original capital that the company invest is £1,000,000 and there are 5 years for the company to get the return that is the budgeted payback period. According to the program, 4 years and 1.5 months that the company will get its all investments. At the last year, company will get the return about £280,000. As a result, based on the period method, the project will be profitable and is worth to invest.Analyzing discounted cash flow techniqueIf the company uses the discounted cash flow technique, according to the peogram, the investment is £1,000,000, and the net present value is 10%. The budgeted payback period is 5 years. After 5 years, the NPV for the project will be £-64,800. It shows that the return is less than the investment. It will be the loss of £64,800 to invest this project. So this project will not be profitable and is not worth to invest.RecommendationAccording to the two methods, it is not difficult to find that the company would better to choose the payback period method. The company chooses payback period method could get the profit of £280,000 and less 5 years could get the all investment. And for the discounted cash flow technique, it will cost 5 years and loss £64,800 at last of the project. So, based on the profit, the company would better to choose thepayback period method.Consideration of other factorsFirst, the environment is one factor that the managers should to consider. Tricol makes a range of furniture and kitchenware. It may make pollute during the producing. If the company does not pay attention to the environment, it may get some fine.Technology is one factor that the managers should to consider about. If the company uses the new technology and equipment in the project, it could improve its productivity. And improve its profitability.The company should also think about the legal. The company should insure that the project is not against the legal. If not, company may be punished by the government and even be banded.At last, company should consider its customers. It should consider that its products, making by the project, will be attracted by the customers. If no customers like it, they may get little profit for the project.ConclusionAs an advisor for the company, this report can help the company make the flex budget and variances and use the two methods to analysis the investment and help the company choose the best method. This will help company make much profit. ReferenceSQA, preparing Financial Forecast (version 3),China Modern Economic Publishing House, 2004./definition/direct-labor-efficiency-variance.html/wiki/Payback_period/terms/d/dcf.aspThe calculation of the variances would be:1.Direct material total variance(standard units of actual production × standard price) – (actual quantity × actual price)[(4kg × 1600) ×£10]–£61600=£64000–£61600=£2400 ( F )2.Direct material usage variancestandard price × (standard units of actual production-actual units)=£10 × (4kg × 1600-5600kg)=£10 × 800kg=£8000 (F)3.Direct material price varianceactual quantity × (standard price-actual price)=5600kg × (£10-£11)=5600kg ×£1=£5600 (A)4.Direct labor total variance(standard hours of actual production × standard rate ph)-(actual hours × actual rate ph)[(2h×1600) ×£9]-(3520h ×£10)=(3200h ×£9)-£35200=£28800-£35200=£6400(A)5.Direct labor rate varianceactual hours × (standard rate ph-actual rate ph)3520h × (£9-£10)=3520h ×£1=£3520(A)6.Direct labor efficiency variancestandard rate ph × (standard hours of actual production-actual hours)£9×[2h×1600-3520h]=£9×(3200h-3520h)=£9×320h=£2880(A)7.Total overhead variance(budgeted variable overhead + budgeted fixed overhead-(actual variable overhead + actual fixed overhead)(£3200+£8200)+(£3200+£8600)=£11400(A)-£11800(A)=£400(A)Appendix 3Variance ratio:The rate for direct material total variances is £ 2400/£ 64000×100%=3.75% The rate of direct material usage variance is £ 8000/£ 64000×100%=12.5% The rate of direct material price variance is £ 5600/£ 64000×100%=8.75% The rate of direct labor variance is 6400/28800×100%=22.2%The rate of direct labor rate variance is £ 3520/£ 28800×100%=12.2%The rate of direct labor efficiency variance is £ 2880/£ 28000×100%=10% The rate of total overhead variance is £ 400/(£ 3200+8600)×100%=3.51%Payback Period:Discounted Cash Flow:。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Preparing Financial ForecastsOutcome 3&4IntroductionThis report shows the variances of direct material total, usage, price, direct labor total, rate, efficiency, and total overhead by a table and of flexed budget. And also give the recommendation and conclusion.Flex budgetVariances analysisThe direct material usage variance is 8000(F), it shows that the flexed budget is£8,000 more than the actual cost, as a result of the using of higher-grade materials and changing of the way of production.The direct material price variance is 5600(A), which means that the actual price is£5600 more than the flexed budget price, because of the Tricol PLC had changed their supplier and purchase the higher-grade material lead to the price raised from £10 per/kg to£11 per/kg.The direct material total = direct material usage – direct material price. As calculated above, 8000-5600=2400, the direct material total variance is£2400.The direct labor rate variance is 3520(A), which means that the actual labor rate is£3520 more than the flexed budget, caused by the company supplied a higher-than-expected wage, the labor cost raised fro m£9 per hour to£10 per hour, and may because Some employees still apprentices, with poor efficiency.The direct labor efficiency variance is 2880(A), as to say, the actual labor efficiency is£2880 more than flexed budget efficiency.It may be because the machine on the production line equipment getting old and it influence the efficiency of employees at the time of production, or maybe the culture of the company is not so well at current time, which result in reduced efficiency.The direct labor total variance is 6400(A) caused by the labor rate variance and efficiency variance. It shows that the actual total labor is £6400 more than the flexed budget total labor.The total overhead variance is 400(A) that means the actual total overhead is £400 more than flexed budget, which caused by the changing of administration overhead and insurance cost both. These two things may change by the company change the salary of the management, and they may add extra insurances for the employees or the machinery.ConclusionThere is a policy of the company in which the company applies a rate of significance of 3% for any Variance analysis. According to the data above, we can clearly see that all the actual variances are higher than 3%, it may caused by the actual production for June was 80% of the target amount, and there are some respects had been changed in the factory.RecommendationI’d give some advices to Tricol Plc for improving their business.●To improve the efficiency not only by increase the salary but alsochange the way of production.●The company may discuss with the new supplier to lower rawmaterial prices.●Training a group of experienced staff.Appendix1. Direct material total variance(Standard units of actual production *standard price) - (actual quantity* actual price)10*4*1600- 61600=2,400(F) 2400/64000=3.75%2. Direct material usage varianceStandard price*(standard units of actual production –actual units)10*(4*1600-5600) =8,000(F) 8000/64000=12.5%3. Direct material price varianceActual quantity *(standard price –actual price)5600*(10-11) =5,600(A) 5600/64000=8.75%4. Direct labor total variance(Standard hours of actual production*standard rate ph) –(actual hours*actual rate ph)2*1600*9-35,200=6400(A) 6400/28800=22.22%5. Direct labor efficiency varianceStandard rate ph*(standard hours of actual production- actual hours)9*(1,600*2-3,520) =2880(A) 2880/28800=10%6. Direct labor rate varianceActual hours*(standard rate ph-actual rate ph)3520*(9-10) =3,520(A) 3520/28800= 12.22%7. Total overhead varianceTotal standard overhead for actual production- total actual overheads (1600*2-3,200) - (8,200-8,600) =400(A) 400/ (3200+8200) =3.51 %IntroductionI’m going to calculate some periods in order to help Trical Plc make correct decision about the new investment. These periods include: the pay back period, ARR and NPV.Assumptions●There is no taxation and inflation, by which the accounting statementsand the value of money would be effected.●The appropriate discount rate is known in able to calculate easier.●The company has enough money to pay the total cost in order toavoid the chain broken of capital happen.The payback periodARRNPV The calculation of net present value at 10%AnalysisPayback is the simplest method to appraise if the investment and project will make profit. Payback measures the number of years it is expected to take to recover the cost of the original investment. The shortest payback period of investment or project will be chosen. However, payback period is based on the accounting statements, inflation may be ignored in this method. The Tricol Plc would recover the initial fixed investment within 5 years, which means the company should accept the plan.ARR is another traditional investment and project appraisal method, according to the average annual profits to the capital investment formed as percentage to know if the investment is worthwhile. However the time value of money will be ignored and length of project lift and size of project not specifically considered in ARR. The figure of ARR of Tricol Plc is 25.6%.NPV method calculates the cash inflow and outflow’s present value. And the inflow should greater than the outflow because of the existing of resent value present value provides an objective basis for evaluating and selecting investment projects. And it takes account of both magnitude and timing of expected cash flows in each period of a project’s life. According to the calculate above, the Tricol Plc’s NPV is (£64,800), less than 0. So the company should reject the business plan.ConclusionI suggest that the Tricol Plc use the payback period, although the NPV is less than 0, but the company can pay their investment back in 5 years, which is very efficiency if it’s a long-term business.Otherwise, the management of board should consider other factors of the business, for example the inflation in the country, the government policy, and the external financial environment.If all the factors are considered and the investment is worthwhile, the company can go ahead the business.。