1-ACCA F8 Introduction

acca各科考试大纲

acca各科考试大纲ACCA各科考试大纲是ACCA考试的重要参考,它详细说明了每门考试科目的内容、考试形式和评分标准。

以下是一些ACCA主要科目的考试大纲概述:1.F1《商业与科技》:本科目涵盖了商业组织、管理、营销、信息技术等方面的知识,旨在测试考生对商业运营和科技应用的理解能力。

2.F2《管理会计》:本科目主要涉及管理会计的基本概念、成本分类、预算编制、差异分析等内容,旨在培养考生的管理会计技能和决策能力。

3.F3《财务会计》:本科目主要考察财务会计的基本原则、财务报表的编制和解读、会计政策的选择等方面,旨在培养考生的财务会计技能和财务报告分析能力。

4.F4《公司法与商法》:本科目主要涉及公司法、合同法、商法等法律领域的基本概念和原则,旨在培养考生的法律意识和商业法律应用能力。

5.F5《业绩管理》:本科目涵盖了业绩评估、成本管理、预算控制等方面的内容,旨在培养考生的业绩管理技能和成本控制能力。

6.F6《税务》:本科目主要涉及税务法规、税务筹划、税务申报等方面的知识,旨在培养考生的税务处理能力和税务筹划能力。

7.F7《财务报告》:本科目是F3的延伸,更深入地探讨了财务报告的编制和分析,包括合并报表、财务分析等内容,旨在培养考生的高级财务报告技能和分析能力。

8.F8《审计与认证业务》:本科目主要涉及审计程序、内部控制评估、风险管理等方面的知识,旨在培养考生的审计技能和风险管理能力。

9.F9《财务管理》:本科目涵盖了投资决策、融资决策、资本结构管理等方面的内容,旨在培养考生的财务管理技能和资本运作能力。

10.P级科目(P1-P7):这些科目是ACCA的高级阶段课程,涵盖了更专业、更深入的领域,如高级业绩管理(P1/P3)、高级财务管理(P2)、高级税务(P6)、高级审计与鉴证(P7)等。

这些科目旨在培养考生在专业领域的高级技能和知识应用能力。

ACCA F8 双语教材

Course NotesACCA Paper F8Audit and AssuranceFrom June 2016 Tutor detailsJ A N U A R Y 2 0 1 6 R E L E A S E第一直觉教育www.fi_No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of First Intuition Publishing Ltd.Any unauthorised reproduction or distribution in any form is strictly prohibited as breach of copyright and may be punishable by law.© First Intuition Publishing Ltd, 2016第一直觉教育www.fi_第一直觉教育www.fi_ContentsPageContentsiii 1 Accounting standards v 2 Overview of the syllabus v 3 Approach to examining the syllabus v 4 Exam technique v 5 Study planner vi 1: Audit framework and regulation1 1 The concept of audit and other assurance engagements 12 External audits3 3 Corporate governance 54 Professional ethics and ACCA’s Code of Ethics and 95 Internal audit and governance and the 126 The scope of the internal audit function, outsourcing and internal audit 13 2: Planning and risk assessment17 1 Overview diagram17 2 Obtaining and accepting audit engagements 18 3 Objective and general principles of audit planning 19 4 Planning an audit19 5 Understanding the entity and its environment 20 6 Assessing the risks of material misstatements 21 7 Materiality, fraud, laws and regulations 22 8 Analytical procedures 24 9 Interim and final audits 25 10 Audit documentation 26 3: Internal control 27 1 Introduction27 2 The use of internal control systems by auditors 28 3 Transaction cycles 30 4 IT controls34 5 Tests of control versus substantive procedures 35 4: Audit evidence37 1 The use of assertions by auditors 37 2 Audit procedures38 3 The audit of specific items 40 4 Audit sampling and other means of testing 49 5 Computer-Assisted Audit Techniques 50 6 The work of others51 7 Not-for-profit organisations535: Review and reporting 551Subsequent events 55 2Going concern 57 3Written representations 59 4Audit finalisation and the final review 60 5Audit reports 60 6Application to scenarios 66 7Reports to Management 68Solutions to Class lecture examples 69Chapter 5 69第一直觉教育www.fi_第一直觉教育www.fi_1 Accounting standardsThe accounting knowledge that is assumed for Paper F8 is the same as that examined in Paper F3. Therefore, candidates studying for Paper F8 should refer to the Accounting Standards listed under Paper F3.2 Overview of the syllabusThe syllabus headings are the same as the titles of each chapter in these course notes: (1) Audit framework and regulation (2) Planning and risk assessment (3) Internal control (4) Audit evidence(5)Review and reporting3 Approach to examining the syllabusAs with all other ACCA exams, F8 is a three-hour exam with an additional 15 minutes’ reading and planning time.The Examiner for F8 is Pami Bahl.All the questions in the F8 exam are compulsory. Section A consists of 12 objective test questions. Section B consists of six longer questions. The bulk of these questions will be discursive but some questions involving the calculation and interpretation of some basic ratios will be set from time to time.Section TopicMarks Section A Four 1 mark objective test questions covering any area in the syllabus. Eight 2 mark objective test questions covering any area in the syllabus 4 16 Section BFour 10 mark questions on any area of the syllabus.40 Two 20 mark questions covering potentially any area of the syllabus, but with heavier emphasis on planning and risk assessment, internal control, audit evidence and review and reporting.404 Exam techniqueThe exam is 180 minutes long and totals 100 marks. Therefore, you should allocate 1.8 minutes for each mark, or 36 minutes for Section A in total, 18 minutes for each 10-mark question and 36 minutes for each 20-mark question. Some longer questions will have subsections which should also be broken up. How long it takes to answer each objective test question will vary depending on the length of the question, but you should aim to complete the whole of Section A within the 36 minutes allocated to it. Every part of every question must be attempted.As an approximate guide, in Section B every paragraph should contain 1 valid point which will earn 1 mark. You should try to keep your paragraphs to less than four lines of writing.Leave a line between each paragraph written, giving the marker the opportunity to give you maximum marks.The use of columns may work well for those questions where there are two parts of the question e.g. if the question asks for risks and controls that would mitigate those risks or audit procedures, and the reason for carrying them out.5Study plannerThe chapter number refers to the chapter of these Course Notes. The time is a guide as to how longyou should spend on this subject, including question practice. Tick each session off when you havecompleted it.Try and complete each study session in order so that you learn each topic in turn. Some sessions arelonger than others, but make sure you take a break between sessions.Read the relevant chapter of the course notes. It is essential that you try the questions from theQuestion Bank where indicated. You will not pass the exam if you don’t attempt the questions. Don’t forget, if you get stuck you can contact your tutor to ask for advice. Tick off each chapter when youhave completed it.Attempt the course examThe course exam will give you a feel for how well you have grasped the syllabus content, and will also show you if you are lacking in exam technique.RevisePractise lots of questions from the Question Bank and read the Examiner’s Comments and ExamSmarts, so that you can find out what the Examiner is looking for in your written answers.You should consider booking a First Intuition revision course at this stage, to improve your examskills, particularly if you scored below 50% in the course exam. Our revision courses are question-based, and will help you improve your exam technique. We also include a Mock Exam, giving youanother chance to practise under real exam conditions.If you complete all the sessions before you have received the course exam please email your tutor torequest it or check to download it.第一直觉教育www.fi_第一直觉教育www.fi_第一直觉教育www.fi_PERrelevanceQuestionpractice Tick when completeChapter SubjectFirst Intuition tutor guidanceTime (min) 4Audit evidenceThis chapter deals with substantive testing.Make sure you know at least four audit tests for each of the key items in the statement of financial position and make sure you understand what financial statement assertions they are testing.It is important to understand the difference between a test of control and a substantive test – both in theory and in practice P017 3 hours on the chapter and 3½ hours on thequestionsAll OT Q’s Q29 Q30 Q32 Q33 Q365Review and reportingThis chapter focuses on the closing stages of the audit and the auditor’s report to shareholders.It is essential to be familiar with each different type of audit opinion and when it would be appropriate to use them.PO183 hours on the chapter and4 hours on the questionsAll OT Q’s Q38 Q42 Q43 Q45 Q46 Q495.1 Practical Experience Requirements (PER) and Performance ObjectivesACCA requires students to have 36 months’ practical experience in order to become members. Part of the practical experience requirements is achieving performance objectives that demonstrate that you can apply what you’ve learnt when studying to real-life, work activities.ACCA has set out 20 performance objectives in 9 areas. You are required to achieve 13 performance objectives – all 9 Essentials performance objectives and any 4 Options performance objectives. ACCA has provided guidance on which objectives are strongly linked to which exam. The relevant objectives for F8, comprise Essentials objectives and Options objectives:Manage self (relevant for all exams) (Essentials)Communicate effectively (relevant for all exams) (Essentials)Use information and communications technology (relevant for all exams) (Essentials)Prepare and collect evidence for audit (relevant for F8 and P7)Evaluate and report on audit (relevant for F8 and P7)第一直觉教育www.fi_1 The concept of audit and other assurance engagementsAn audit is an evaluation of an organisation, system or process. Audits are performed to ascertain the validity and reliability of information, and also provide an assessment of a system's internal control.In the context of a company and its accounting records, the external audit is an “independentexamination and expression of opinion on the financial statements of an entity”. Many organisations(particularly companies) are legally required to have an external audit.The purpose of the external audit is for the auditor to obtain sufficient appropriate audit evidence on which to base the audit opinion. This opinion states that the financial statements give a ‘true and fairview’ of the position, performance (and cash flows) of the entity. This opinion is prepared for thebenefit of shareholders and can be seen as helping to prevent these investors from being defrauded.There is no strict legal definition of “true and fair” but essentially it means that the financialstatements contain no significant/material errors.“True” can be considered as stating that the information in the financial statements is factual andcomplies with accounting standards.“Fair” refers to information being clear, impartial and unbiased, reflecting the substance oftransactions, rather than the legal form.An audit is considered necessary for all but the smallest companies because there is often a distinction between those people that own the company – the shareholders – and those people that run the day- to-day operations of the company – the directors.In this sense, the directors are considered to be the “stewards” of the company – they are accountable to the owners for the way the performance of the company.第一直觉教育www.fi_审计和其他认证业务的概念审计是对一个组织、系统或过程的评估。

对于ACCA考试科目中F8的题型分析

对于ACCA考试科目中F8的题型分析关于ACCA考试科目中,各科都考哪些题型呢?中公财经网小编就以F8为例给大家简单介绍一下吧。

(一)客观题(Objective test questions/OT questions)客观题是指这些单一的,题干较短的,并且自动判分的题目。

每道客观题的分值为2分,考生必须回答的完全正确才可以得分,即使回答正确一部分,也不能得到分数。

(二)案例客观题(OT case questions)案例客观题是ACCA引入的新题型,每道案例客观题都是由一组与一个案例相关的客观题组成的,因此要求考生从多个角度来思考一个案例。

这种题型能很好的反映出考生将如何在实践中完成这些任务。

案例客观题会出现在2016年9月份的笔试中,这意味着CBEs考试和笔试的格式在本次考试中将完全一致。

(三)主观题(Constructed response questions/CR qustions)考生将使用电子表格程序和文字处理程序去完成主观题的回答。

就像笔试中的主观题一样,答案最终将由专家判分。

今天就奉上同学回忆出的12月ACCA F8科目考试真题,勇敢的童鞋赶紧来测试一下,你到底能否考过F8吧!Section A部分真题第一道案例选择题印象比较深,是关于professional ethical,考了fundamental professional ethical 和threat。

第二道是关于payroll system,考了audit procedure,completeness,understatement test,其中还有一道计算payroll expense。

第三道问了audit opinion,还有SP,有overstatement test。

Section B部分真题第一道大题,有16分的audit risk(identify and response)找出8个,factors toconsider set up internal audit department 4分,how internal audit effecton fraud and errors 2分,SP hot review and cold review 4分,SP for wages andsalary on completeness and existence 4分。

accaf8考试注意事项

accaf8考试注意事项

哎呀呀,ACCA F8 考试可不能掉以轻心啊!要想顺利通过,这些注意事项你可得牢记呀!

先说备考阶段,那得像盖高楼一样稳扎稳打呀!不能三天打鱼两天晒网,比如知识点得反复温习,这就好比给大脑不断充电!还有练习题,不能只做一遍就不管了,得多刷几遍,就像给技能打磨抛光!

到了考试的时候,千万别慌张呀!你想想,一慌是不是脑子就容易乱?就像开车时猛踩刹车容易失控一样。

认真读题是关键,别匆匆忙忙就下笔,难道你能闭着眼睛走路吗?

还有啊,时间分配可不能马虎!别在一道难题上死磕,那会让你后面的题目没时间做的呀,这就跟赶路错过了美景一样可惜。

哎呀,答题要条理清晰呀,让阅卷老师一目了然。

不能乱糟糟的,就像房间不收拾找不到东西一样。

注意书写规范,别字迹潦草,难道你希望老师费力去猜你的答案吗?

ACCA F8 考试可不是闹着玩的,这关系着你的未来呀!一定要认真对待,就像对待珍贵的机会一样。

总之啊,这些注意事项一定要牢记在心,别等考完了才后悔!。

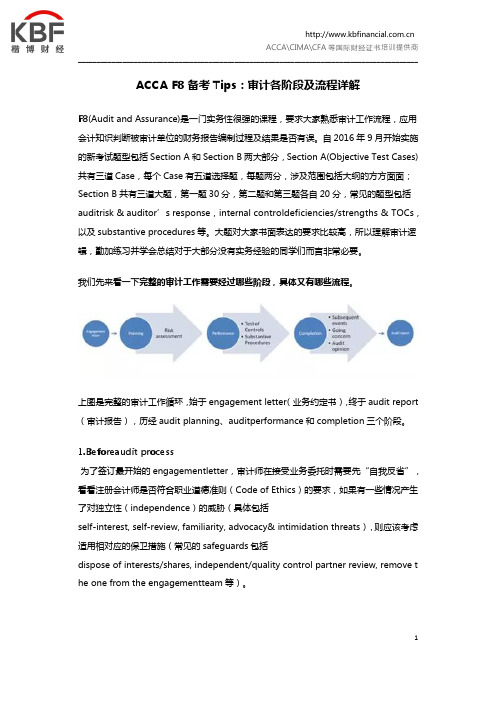

ACCA F8备考Tips:审计各阶段及流程详解

ACCA F8备考Tips:审计各阶段及流程详解F8(Audit and Assurance)是一门实务性很强的课程,要求大家熟悉审计工作流程,应用会计知识判断被审计单位的财务报告编制过程及结果是否有误。

自2016年9月开始实施的新考试题型包括Section A和Section B两大部分,Section A(Objective Test Cases)共有三道Case,每个Case有五道选择题,每题两分,涉及范围包括大纲的方方面面;Section B共有三道大题,第一题30分,第二题和第三题各自20分,常见的题型包括auditrisk & auditor’s response,internal controldeficiencies/strengths & TOCs,以及substantive procedures等。

大题对大家书面表达的要求比较高,所以理解审计逻辑,勤加练习并学会总结对于大部分没有实务经验的同学们而言非常必要。

我们先来看一下完整的审计工作需要经过哪些阶段,具体又有哪些流程。

上图是完整的审计工作循环,始于engagement letter(业务约定书),终于audit report (审计报告),历经audit planning、auditperformance和completion三个阶段。

1.Beforeaudit process为了签订最开始的engagementletter,审计师在接受业务委托时需要先“自我反省”,看看注册会计师是否符合职业道德准则(Code of Ethics)的要求,如果有一些情况产生了对独立性(independence)的威胁(具体包括self-interest, self-review, familiarity, advocacy& intimidation threats),则应该考虑适用相对应的保卫措施(常见的safeguards包括dispose of interests/shares, independent/quality control partner review, remove t he one from the engagementteam等)。

ACCA考经分享F8应该怎样过

ACCA F8 审计该怎么学?ACCA经验分享大家好,我是杨雯婧,2015年12月的ACCA考试成绩已经出来一段时间了,但现在回忆起出成绩的时候,还尚能感受到当时查成绩时候的忐忑不安,因为当时非常不确定自己的F8是不是可以考过。

这个学期开始上ACCA F8课程的时候觉得比较吃力,无论是课本、讲义还是试卷全部都是单词,跟F4很相似,这是一科需要背诵的科目,而且需要背的知识点还有很多,这对于喜欢计算的我来说是一个挑战,但是人生有挑战才精彩。

f8一开始上课的时候觉得比较吃力,一是完全找不到重点,二是完全没有实践的经验,审计是一科讲究实践经验的科目。

但是泽稷网校ACCA老师在上第一节课的时候安慰我们,跟着老师来,该记忆的知识点及时记,讲完一章做相关题目通过考试是完全没问题的。

我还记得我刚开始做题目的时候觉得完全不知道怎么下手,不知道如何用专业的词语、短语去描述相关审计步骤、审计方法,这时候需要积累,需要去记、去背讲义上、真题答案上的写法,这样等到自己写的时候就有词语可以写,就不会知道怎么讲出来,但是不知道怎么写。

在刚开始学习ACCA F8这门科目的时候,要做到所有讲义上的知识点都覆盖,分清楚哪些是需要一字不差的背诵下来的、哪些知识点需要记住关键词但是不需要背下来的还有哪些只需要了解的看到可以选出来的,需要背诵的找个本子将这些记录下来,有规律的记忆,比如一周两到三次,这样等到复习的时候就会轻松很多,需要记住关键词的可以把问题写在本子上,然后记住关键词,可以用自己的话把答案写出来,需要了解的只需要平时多翻看就可以了。

ACCA F8的选择题,因为刚改革没多久,所以真题不是很多,那就只有bpp练习册上的选择题,F8的选择题相对的不是很难,但是需要细心与仔细还有对知识概念的清楚理解,如果对知识点的比较模糊只知道大概,在做选择题的时候就觉得这个选项也对,但是那个选项也差不多,这样就会拖延时间。

选择题在考前多做几遍,把自己的错题找出来,根据错题追溯到知识点上,然后再找同类的题再次练习,或者把错题汇总一起隔一段时间再做一次。

ACCAF8英语版简介

ACCA F8 Audit framework and regulation1、The concept of audit and other assurance engagementsAn audit is an evaluation of an organisation, system or process. Audits are performed to ascertain the validity and reliability of information, and also provide an assessment of a system's internal control.In the context of a company and its accounting records, the external audit is an “independent examination and expression of opinion on the financial statements of an entity”. Many organisations (particul arly companies) are legally required to have an external audit.The purpose of the external audit is for the auditor to obtain sufficient appropriate audit evidence on which to base the audit opinion. This opinion states that the financial statements give a ‘true and fair view’ of the position, performance (and cash flows) of the entity. This opinion is prepared for the benefit of shareholders and can be seen as helping to prevent these investors from being defrauded.There is no strict legal definition o f “true and fair” but essentially it means that the financial statements contain no significant/material errors.“True” can be considered as stating that the information in the financial statements is factual and complies with accounting standards.“Fair” refers to information being clear, impartial and unbiased, reflecting the substance of transactions, rather than the legal form.An audit is considered necessary for all but the smallest companies because there is often a distinction between those people that own the company – the shareholders – and those people that run the day- to-day operations of the company – the directors.In this sense, the directors are considered to be the “stewards ” of the company – they are accountable to the owners for the way the performance of the company.1.1 Assurance engagementsAssurance engagements (of which an external audit is an example) are simply assignments where a practitioner expresses a conclusion designed to give confidence about the outcome of a particular subject matter.The five elements of an assurance engagement are:(a) A three-party relationship:(i) A practitioner (i.e. an accountant) who is the professional who will review the subject matter and provide the assurance(ii) A responsible party, which is the organisation responsible for preparing the subject matter to be reviewed(iii) Intended user, who is the person who requires the assurance report.(b) An appropriate subject matter. The subject matter is the data that the responsible party has prepared and which requires verification (e.g. financial statements).(c) Suitable criteria. The subject matter is compared to the criteria in order for it to be assessed and an opinion provided (e.g. accounting standards).(d) Sufficient appropriate evidence has to be obtained by the practitioner in orderto give the required level of assurance.Company Owned by Run by Shareholders Financial statements Directors Independent examination Opinion Auditor(e) A written assurance report given by the practitioner to the intended user and the responsible party.1.2 Explain the level of assurance provided by audit and other review assignmentsThere are two levels of assurance that an assurance engagement can provide, depending on the amount of work performed.1.2.1 Limited level of assuranceThis is a form of negative assurance, whereby the auditors state that “nothing has come to their attention” that causes them to believe that the subject matter is not free from material misstatement. This level of assurance is commonly used for forecasts (e.g. a cash flow forecast), where the auditor cannot “vouch” the accuracy of the data because the data cannot be tested against actual known figures.第一直觉教育版权所有。

ACCA F8知识点讲解:梳理审计流程

ACCA F8的知识点比较多,考试更注重细节,往往会让很多考生措手不及。

2018年三月考季,ACCA F8的考试通过率更是惨不忍睹,以39%的通过率,“稳坐”F阶段通过率末尾。

ACCA考试以大学生为重要主体,没有实操经验,在ACCA F8这样对实务经验要求比较高的科目来说,这样的通过率和考试成绩也算正常。

在文章开头中公财经网小编就说过F8知识点繁多,单是了解各个知识点是远远不够的,重要的是要把这些知识点联系起来。

今天,中公财经网小编就带大家一起来梳理一下F8的知识点:审计流程。

上图就是一个完整的审计流程,通俗来解释:Tendering就是审计师和客户合作的开始;为了增进合作关系,就有了client acceptance procedure;确定唯一的合作关系,需要用appointment and engagement letter来证明;通过audit planning更加深入的了解彼此,当在相处过程中发现一些似是而非的问题(ROMM),会通过更加细致的调查(substantive procedure)和确认(audit review),最终确认和解决。

充分了解并体会审计师和客户的这种关系和合作,对理解F8的内容是非常有帮助的。

各位同学们不要被F8历年惨淡的考试通过率吓到,只要用对方法,ACCA F8将不再是你的“拦路虎”。

X。

acca阶段划分

acca阶段划分

ACCA 考试分为四个阶段,每个阶段都需要通过相应的考试才能进入下一阶段:

1. 知识课程(F1-F3):这是 ACCA 考试的第一阶段,主要涉及基础的财务和管理知识,包括财务会计、管理会计、商业法等。

这一阶段的考试主要测试学生对基本概念和原理的理解。

2. 技能课程(F4-F9):这是 ACCA 考试的第二阶段,主要涉及更深入的财务和管理技能,包括财务报告、审计、税务、财务管理等。

这一阶段的考试主要测试学生在实际工作中应用知识的能力。

3. 核心课程(P1-P3):这是 ACCA 考试的第三阶段,主要涉及战略管理和领导能力,包括公司治理、风险管理、战略财务管理等。

这一阶段的考试主要测试学生在复杂的商业环境中做出决策和管理的能力。

4. 选修课程(P4-P7):这是 ACCA 考试的最后一个阶段,学生可以选择自己感兴趣的领域进行深入学习,包括高级财务管理、高级审计与认证业务、高级税务等。

通过完成这四个阶段的考试,学生可以获得 ACCA 资格证书,并成为全球认可的专业会计师。

每个阶段的考试都需要学生具备相应的知识和技能,并且需要进行系统的学习和准备。

ACCA考试经验分享:关于F8的考试经验分享介绍

中公财经培训网:/对于很多的小伙伴来说,进行F8阶段的ACCA考试如果不了解一些考试经验,在备考的时候很可能会走偏路。

下面中公财经小编整理了大神的一些经验分享,具体情况如下所示;学习F8谈不上有什么特别的学习方法。

F8在F6-9中是背诵和记忆相对较多的科目,需要踏实,有计划,有重点的学习。

我是在暑假看网课学习F8,制定一个大致的学习安排计划,认真的执行,不能拖沓。

我生待明日,万事成蹉跎。

看完每节网课后,要通过看书和做题理解和巩固。

在理解的基础上进行背诵,效果会更好,不能死记硬背。

我一般在考前反复记忆该背的知识,熟能生巧。

要有重点的进行学习和复习,因为F8的考察知识点比较固定,考纲变化也比较小,通过syllabus 和past exams去着重学习重点知识,重要的知识点要多花时间去学习,但也不意味着只学习重点,只是其他知识点的掌握程度不用那么高。

我认为学习F8,练习past exams 是效果最好的。

要将自己的答案和考官的答案进行比较,尽可能的向考官的思路靠拢。

要横向和纵向的刷题,不能盲目刷题,很多题目中不同的表述其实考的是相同的知识点,要拓宽自己的思路,熟悉相同知识点的不同考法。

练习的时候注意把控好时间,在后期,重要的是查漏补缺和复习考试概率较高、重点难点问题。

时间管理在考试的时候十分重要,不能一直纠结在不会的题目上。

我在考试的时候会跳过自己不会的题,把容易得分的和自己掌握较好的题目先写好,最后再返回来写不会的题目。

学习的时候也要注意劳逸结合,长时间的学习会降低学习效率,适时的放松。

其次是要保持良好的心态,对自己有信心。

虽然每次写出来的答案和考官的相差甚远,有很多知识点想不到,但是通过自己的不断努力,一点点的弥补自己的不足,看到自己的进步,自信也会一点点增长起来。

学习ACCA不应该抱着通过就好的想法,在F阶段要打好基础,否则未来的路只会更加艰辛。

学习ACCA是孤独而又漫长的过程,当别人在吃喝玩乐的时候,我们要坚定信念继续学习,在奋斗的路上砥砺前行。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

MAIN CAPABILITIES

A) ‘Explaining the nature, purpose, and scope of assurance engagements, including the role of the external audit and its regulatory and ethical framework.’ B) ‘Explaining the nature of internal audit. Describing its role as part of overall performance management, and its relationship with external audit.’ C) ‘Demonstrating how the audit obtains an understanding of the entity and its environment , assesses the risk of material misstatement (whether arising from fraud or other irregularities), and plans an audit of financial statements.’ D) ‘ Describing and evaluating information systems and internal controls to identify and communicate control risks and their potential consequences, and making appropriate recommendations.’ E) ‘ Identifying and describing the work and evidence required to meet the objectives of audit engagements and the application of ISAs.’ F) ‘ Evaluating findings and modifying the audit plan as necessary.’ G) Explaining how conclusions from audit work are reflected in different types of audit report, explaining the elements of each type of report.’

EXAMINATION FORMAT

Format of the paper Q1 scenario-based question Q2 knowledge-based question stick to subject areas 30 10 20each 100

Q3, 4, 5 Total

Time allowed-3 hours

Prepared by Bell Jiang

ZhongXin International Financial Education ACCA F8 Audit and Assurance

Content

Content

Session 1 2 3 4 5 6 7 8 9 10 11 12 Topics Basic Concept Corporate Governance Internal Audit Responsibility Professional Ethics and Acceptance of appointment Audit planning and Risk assessment Documentation Techniques Audit Evidence Internal Control System Audit Procedure Audit review and Completion Other Audit Areas Page 1 13 24 39 45 56 68 79 94 111 135 155

Prepared by Bell Jiang

KEY AREAS OF THE SYLLABUS

The key topics are: � � � � � � � Professional ethics Audit planning and engagement risk Risk identification Reporting on weaknesses Audit work and audit evidence in key balance sheet and income statement areas Audit completion Explanation(not drafting) of audit reports

ZhongXin International Financial Education ACCA F8 Audit and Assurance

Introduction of Paper

INTRODUCTION f the paper is to develop knowledge and understanding of the process of carrying out the assurance engagement and its application in the context of the professional regulatory framework.