会计学原理-约翰·J·怀尔德版-上海交通大学-05

大型语言模型 原理 实现与发展

三、大型语言模型的发展趋势

7、可持续发展:大规模训练和部署大型语言模型对计算资源和能源的需求巨 大,可持续发展问题将受到重视,包括研究更高效的训练方法、采用绿色能源等。

三、大型语言模型的发展趋势

8、法规与政策:随着大型语言模型的商业化和普及,相关法律法规和政策也 将逐步完善,以确保其合理使用和监管。

三、大型语言模型的发展趋势

5、应用领域拓展:大型语言模型在对话系统、机器翻译、摘要生成等领域已 经取得了显著成果,未来还可能应用于情感分析、智能写作助手等更多场景。

三、大型语言模型的发展趋势

6、人工智能伦理与公平性:随着大型语言模型的普及,其可能带来的偏见和 歧视问题将引起更多。如何在训练和使用过程中确保公平性和多样性将成为重要 议题。

四、理论与实践的结合

四、理论与实践的结合

《会计学原理》注重理论与实践的结合。约翰 J怀尔德通过实例和案例分析, 使读者更好地理解会计学的原理和应用。他强调了会计人员在实践中应该具备的 专业技能和道德素养,这对于培养合格的会计人才具有重要意义。

五、结论

五、结论

总的来说,约翰 J怀尔德的《会计学原理》是一本经典的会计学教材,它以 真实、公正、透明的原则为核心,注重理论与实践的结合。通过学习这本书,我 们可以更好地理解会计学的原理和应用,为未来的职业发展打下坚实的基础。

一、引言

一、引言

波动率是金融市场中的关键变量,对于投资决策、风险管理以及资产定价等 方面具有重要意义。在R语言中,有许多统计和机器学习模型可用于预测波动率。 本次演示将重点ARCH模型和HAR RV模型。

二、ARCH模型

二、ARCH模型

自回归条件异方差模型(ARCH)是一种用于预测波动率的统计模型。它假设 波动率具有条件异方差性,即波动率在给定过去信息的情况下具有恒定的方差。 在R中实现ARCH模型,我们可以使用rugarch包。下面是一个简单的示例代码:

约翰怀尔德 会计学原理

约翰怀尔德会计学原理全文共四篇示例,供读者参考第一篇示例:约翰怀尔德(John Wild)是一位著名的会计学家,他对会计学原理的研究和贡献被广泛认可。

他在他的著作中系统地探讨了会计学的基本原理和理论,帮助人们更好地理解和应用会计学知识。

会计学原理是会计学的基础,是会计科学的根本。

约翰怀尔德在他的著作中详细阐述了会计学原理的重要性,并提出了许多深刻的见解。

他指出,会计学原理是指导会计学实践的准则和规则,其作用是维护会计学的准确性、可靠性和公正性。

在他的著作中,约翰怀尔德强调了会计学原理在企业经营管理中的重要性。

他认为,只有建立在正确的会计学原理基础之上的会计信息才能为企业决策提供准确的参考。

他还指出,遵循正确的会计学原理可以帮助企业提高内部管理效率,加强企业的风险控制能力,提高企业的经营绩效。

约翰怀尔德的著作对会计学原理的研究和理解做出了重要贡献。

他的思想为会计学界和企业管理者提供了宝贵的启示,对促进会计学的发展和提升会计学的实践水平具有重要意义。

希望更多的人可以关注会计学原理的研究,深入理解和应用约翰怀尔德等会计学家的研究成果,为企业的可持续发展和社会的进步做出更大的贡献。

第二篇示例:约翰·怀尔德是一位著名的会计学家,他对会计学原理的研究和贡献被誉为经济学领域的里程碑之一。

怀尔德的研究不仅深刻地影响了当代会计学的发展,也为未来的学者们提供了重要的启示。

本文将对怀尔德的会计学原理进行介绍和分析。

怀尔德认为,会计学原理是会计学的基础,是会计学家应该遵循的核心准则。

在怀尔德看来,会计学原理主要包括:货币计量、持续经营、历史成本、收入确认、费用匹配等几个方面。

这些原则不仅是会计师在日常工作中的行为准则,也是保障会计信息质量和经济运作有序的重要基础。

货币计量原则是指所有的财务信息应该用货币单位进行衡量和记录。

怀尔德认为,货币单位是衡量财务状况和经营业绩的唯一标准,只有将所有的资产、负债、收入和支出都转化为货币单位,才能使这些信息具有可比性和可信度。

会计学入门读物哪本比较好?

会计学入门读物哪本比较好?会计学入门读物哪本比较好?会计学入门读物哪本比较好?国内的教材感觉都比较枯燥,为了提高对此学科的兴趣,暂且决定先从国外的教材开始入门。

我自己也查阅到了一些国外的会计学教材,我先列举自己查阅到的书籍,还请会计界的各位前辈帮我做些参考。

《会计学原理》作者:约翰·J.怀尔德(貌似这两个版本是一样的,好像就是中英文的区别?)《会计学原理》韦安特《会计学》查尔斯·T·亨格瑞《会计学》查尔斯·T·亨格瑞(这两个貌似是先后版本不同,但价格差距很大,第8版是59.3,第六版是119.5,这是怎么回事?)《财务会计教程》查尔斯·T·亨格瑞《会计学基础》罗伯特·N.安东尼(这个好像也是版本相同,只是中英文的区别?)《会计学:数字意味着什么》戴维?马歇尔(这个好像也是版本相同,只是中英文的区别?)请教各位会计界的前辈以上哪本作为会计学的入门读物更好?如果还有更好的书籍作为会计学的入门读物还请各位前辈推荐指教,先谢过!(本人非专业人士!)(注:本人不是为了考证,我只是想对此学科入门之前,先提高对此学科的兴趣,而后系统性的对此学科有所认知。

因此,我非常需要一个趣味性较强而又在知识上综合连贯的书或教材或者是一份书单,谢谢!)会计学入门读物哪本比较好?国内的教材感觉都比较枯燥,为了提高对此学科的.兴趣,暂且决定先从国外的教材开始入门。

我自己也查阅到了一些国外的会计学教材,我先列举自己查阅到的书籍,还请会计界的各位前辈帮我做些参考。

《会计学原理》作者:约翰·J.怀尔德工商管理经典译丛?会计与财务系列:会计学原理(第19版)/约翰?J?怀尔德 (John J.Wild)-图书<="" bdsfid="102" i="">普通高等教育"十一五"国家级规划教材?教育部高校工商管理类教材指导委员会双语教学推荐教材?工商管理经典教材?会计与财务系列?会计学原理(第19版)(英文版)/崔学刚<="" bdsfid="104" i=""> (貌似这两个版本是一样的,好像就是中英文的区别?)《会计学原理》韦安特会计学原理(附光盘1张)/韦安特<="" bdsfid="109" i="">《会计学》查尔斯·T·亨格瑞会计学(第8版)/查尔斯·T·亨格瑞(Charles T.Horngren)-图书<=""bdsfid="113" i="">《会计学》查尔斯·T·亨格瑞会计学(第6版)(套装上下册)/享格瑞<="" bdsfid="116" i=""> (这两个貌似是先后版本不同,但价格差距很大,第8版是59.3,第六版是119.5,这是怎么回事?)《财务会计教程》查尔斯·T·亨格瑞财务会计教程(第8版)/亨格瑞<="" bdsfid="120" i="">。

会计学原理-约翰·J·怀尔德版-上海交通大学-04

FastForward Work Sheet For Month Ended December 31, 2007 Unadjusted

Trial Balance Dr. Cr. 4,350 9,720 2,400 26,000 Adjustments Dr. Cr. f 1,800 b a c e 250 1,050 100 375 210

Cash Accounts receivable Supplies Prepaid insurance Equipment Accum. depr. - Equip. Accounts payable Salaries payable Unearned consulting revenue C. Taylor, Capital C. Taylor, Withdrawals Consulting revenue Rental revenue Depr. expense Salaries expense Insurance expense Rent expense Supplies expense Utilities expense Totals Net income

Chapter_01会计学原理答案 principles of accounting 19th edition john j.wild 人大出版社

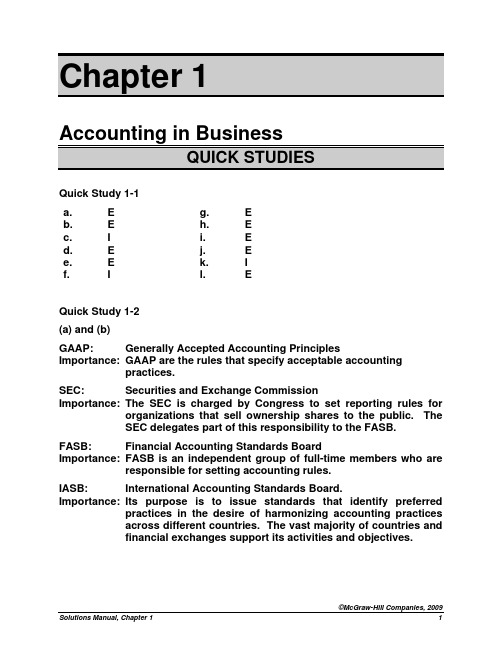

Importance: GAAP are the rules that specify acceptable accounting

practices.

SEC:

Securities and Exchange Commission

Importance: The SEC is charged by Congress to set reporting rules for

To illustrate, many companies base compensation of managers on the amount of reported income. When the choice of an accounting method affects the amount of reported income, the amount of compensation is also affected. Similarly, if workers in a division receive bonuses based on the division’s income, its computation has direct financial implications for these individuals.

Quick Study 1-7

Assets

=

$375,000 (b) $250,000

$185,000

Liabilities (a) $125,000

$ 90,000 $ 60,000

+

Equity

$250,000

$160,000

(c) $125,000

Quick Study 1-8

Assets

会计学原理约翰·J·怀尔德版上海交通大学

Information useful to help the enterprise achieve its goal, objectives and mission.

Types of Accounting Information

Financial Tax

Managerial

Integrity of Accounting Information

提供商品或服务所有者雇员和供应商顾顾客客债权人人目标和战略投资融资经营短期项目?现金?应收账款?存货长期项目?土地?建筑物?设备?专利?股票和债券短期项目?银行?供应商?员工?政府长期项目?长期债权人?股东采购销售生产管理企业活动概述importanceofaccounting

课程要求--教材与辅助资料

Financial Statements

Internal Users

• • • • • • • •

Board of Directors (董事会) Chief Executive Officer Chief Financial Officer Vice Presidents Business Unit Managers Plant Managers Store Managers Line Supervisors

• Conceptual Chapter Objectives • Analytical Chapter Objectives • Procedural Chapter Objectives

The Accounting Process

Economic Activities

Accounting links decision makers with economic activities and with the results of their decisions.

会计学原理 约翰·J·怀尔德 Chap005

P1

Purchase Discounts

On May 7, Jason, Inc. purchased $27,000 of merchandise inventory on account, credit terms are 2/10, n/30.

Dr. 27,000 Cr. 27,000

4-4

C1

Merchandising Activities

Service organizations sell time to earn revenue.

Examples: Accounting firms, law firms and plumbing services

Revenues

Minus

4-10

P1

Merchandise Purchases

Invoice

Main Source, Inc.

614 Tech Avenue Nashville, TN 37651

S o l d T o

Invoice

Date 5/4/09 Number 358-BI

Name: Barbee, Inc. Attn: Tom Bell Address: One Willow Plaza Cookeville, Tennessee 38501 Terms 2/10,n/30 Description 250 Backup System Ship: FedEx Prepaid Quanity Price 500 $ 54.00

4-7

C2

Operating Cycle for a Merchandiser

Begins with the purchase of merchandise and ends with the collection of cash from the sale of merchandise. Cash Sale

会计学原理-约翰·J·怀尔德版-上海交通大学-09

Jul. 31 Cash 500 Accounts Receivable - Webster

500

To record cash collections on account

Cash Accounts Receivable - Matrix

800 800

To record cash collections on account

© The McGraw-Hill Companies, Inc., 2007

C1

Sales on Credit

On July 31, Barton, Co. collects $500 from Webster, Co., and $800 from Matrix, Inc. on account.

Chapter 9

Accounting for Receivables

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2007

Conceptual(概念上的) (概念上的) Learning Objectives

C1: Describe accounts receivable and how they occur and are recorded C2: Describe a note receivable and the computation of its maturity(到期) date and interest C3: Explain how receivables can be converted to(转 变为) cash before maturity

Accounting for bad debts that result from credit sales.

会计学原理-约翰·J·怀尔德版-上海交通大学-15

Dec. 18 Cash 30,000 Long-Term Investment - AFS Gain on Sale of Investment

Sold 1,000 Apex shares

25,000 5,000

P3

Financial Reporting Available-for-Sale Securities

4,500 4,500

To adjust AFS securities to market

P4

Accounting for Influential Investments

Investor Ownership of Investee Shares Outstanding Equity Method 20% Consolidated Financial Statements 50% 100%

P1

Accounting Basics for Equity Securities

On May 6, 2008, Matrix, Inc. purchased 10,000 shares of Apex, Inc. common stock for $250,000 in the open market. The securities are classified by manager of Matrix as “available-for-sale” (AFS).

Cost or Market Value Method 0%

{

In some cases, influence or control may exist with less than 20% ownership.

P3

Valuing and Reporting Available-forSale Securities

会计学原理-约翰·J·怀尔德版-上海交通大学-11

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2007

Analytical Learning Objectives

A1: Compute the times interest earned(收入利 息比) ratio and use it to analyze liabilities

Uncertainty in When to Pay

Uncertainty in How Much to Pay

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2007

C2

Known (Determinable) Liabilities

Accounts Payable Sales Taxes Payable

C1

Current and Long-Term Liabilities

Current Liabilities as a Percent of Total Liabilities

Raw lings Sporting Goods Apple Computer AMF Bow ling Cannondale

McGraw-Hill/Irwin

Expected not to be paid within one year or the company’s operating cycle, whichever is longer.

© The McGraw-Hill Companies, Inc., 2007

$20,000 × 6% × (90 ÷ 360) = $300

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2007

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

P4: Define and prepare multiple-step and single-step income statements

P5: Appendix 5A: Record and compare merchandising transactions using both periodic and perpetual inventory systems

Dr.

Jun. 20 Merchandise Inventory

14,000

Cas h

Purchase merchandise for cash

Cr. 14,000

P1

Trade Discounts

Used by manufacturers and wholesalers to offer better prices for greater quantities purchased.

Purchases

Cash sales

Account receivable

Merchandise inventory

Merchandise inventory

Hale Waihona Puke Credit salesC3

Inventory Systems

Beginning inventory

+

Net cost of purchases

For Year Ended December 31, 2007

Net sales Cost of goods sold Gross profit Operating expenses Net income

$ 150,000 80,000

$ 70,000 46,500

$ 23,500

Operating Cycle for a

Procedural Learning Objectives

P1: Analyze and record transactions for merchandise purchases using a perpetual system

P2: Analyze and record transactions for merchandise sales using a perpetual system

C1

Merchandising Activities

Service organizations sell time to earn revenue.

Examples: Accounting firms, law firms and plumbing services

Revenues

Minus

Equals Expenses

Analytical Learning Objectives

A1: Compute the acid-test ratio and explain its use to assess liquidity

A2: Compute the gross margin ratio and explain its use to assess profitability

= Merchandise

available for sale

Ending inventory

+

Cost of goods sold

P1

Merchandise Purchases

On June 20, Jason, Inc. purchased $14,000 of Merchandise Inventory paying cash.

C2

Merchandiser

Begins with the purchase of merchandise and ends with the collection of cash from the sale of merchandise.

Cash Sale

Purchases

Credit Sale

Cash collection

C2: Identify and explain the inventory asset of a merchandising company

C3: Describe both perpetual and periodic inventory systems

C4: Analyze and interpret cost flows and operating activities of a merchandising company

Chapter 5

Accounting for Merchandising Operations

Conceptual Learning Objectives

C1: Describe merchandising activities and identify income components for a merchandising company

Example

Matrix, Inc. offers a 30% trade discount on orders of 1,000 units or more of their popular product Racer. Each

Net income

C1

Merchandising Activities

Merchandising Companies

Manufacturer

Wholesaler

Retailer

Customer

Reporting Income of a

P2

Merchandiser

Merchandising companies sell products to earn revenue.

Examples: sporting goods, clothing, and auto parts stores

Net Sales

Minus Cost of Equals

Goods Sold

Gross Profit

Minus

Expenses

Equals

Net Income

Merchandising Company Income Statement