华星化工估值模型案例Excel

工控行业新项目初始评估表格模板

工控行业新项目初始评估表格模板新项目初始评估表格模板项目名称:项目目标:项目背景:项目规模:项目周期:评估日期:评估人员:1. 项目可行性分析1.1 技术可行性1.1.1 技术门槛:项目所需要的技术是否已经成熟或者需要依靠新技术进行开发。

1.1.2 技术支持:项目所需要的技术是否有专业的技术人员支持和维护。

1.1.3 技术成本:项目所需要的技术是否需要高成本来进行研发和实现。

评估结果:1.2 市场可行性1.2.1 市场需求:市场对于此类工程项目的需求是否大,并且是否存在商业价值。

1.2.2 竞争情况:市场上是否已存在类似的产品或服务,如果有,项目是否有足够的优势进行竞争。

1.2.3 市场营销:项目是否能够进行有效的市场宣传,让更多的客户了解并愿意使用。

评估结果:1.3 经济可行性1.3.1 投资预算:项目需要的资金是否符合现有的预算,或者是否能够得到资本市场的支持。

1.3.2 利润预期:项目的预期收益是否能够满足开发者的预期。

1.3.3 资金回收期:项目需要多久能够回收全部成本,进入盈利状态。

评估结果:2. 项目进展计划分析2.1 项目流程和组织架构:项目的实施流程和组织架构是否清晰,是否能够顺利实施。

2.2 项目执行计划:项目实施的具体计划、时间节点和关键事件是否合理可行。

2.3 项目管理能力:项目执行者是否具备足够的管理能力,能够有效地跟踪进度和解决问题。

评估结果:3. 风险分析3.1 技术风险:项目所面临的技术风险是什么,可能会导致哪些问题和影响。

3.2 市场风险:市场风险包括市场需求变化、竞争加剧、市场营销策略错误等,可能会导致项目失败。

3.3 经济风险:经济风险涉及到资金来源问题、预算超支、收益不达预期等,需要评估可能会对项目造成的影响。

评估结果:4. 评估结论根据以上分析,我们得出以下结论:(1)项目可行性分析,项目可行性评估为(….),项目具有可行性。

(2)项目进展计划分析,项目进展计划评估为(....),计划合理、可行。

超强大公司估值模型,收入预期EXCEL模板

2012E 3,404 22.4% 2,315 119 32.0% 30.64 85.11 (13.31) 0.00 14.48 0.00

2014E 5,930 32.0% 4,092 208 31.0% 53.37 148.25 (24.69) 0.00 32.34 0.00

6.00 1,744.87 5.00 3.00 0.00 1,746.87 366.84 21.0% 1,380.03 1,379.03 1.00 18.7% 19.5% 1,305.52 1.056 19.5% 275.81 3,729.00 137.90 4,694.32 18.69%

79 发行在外股份数量(百万股) 34 基本每股收益(元) 35 稀释每股收益(元)

6.00 742.86 5.00 3.00 0.00 744.86 156.42 21.0% 588.44 587.44 1.00 21.1% 23.3% 1,305.52 0.450 -5.1% 117.49 1,414.03 58.74 1,825.24 21.15%

6.00 873.78 5.00 3.00 0.00 875.78 183.91 21.0% 691.87 690.87 1.00 20.3% 17.6% 1,305.52 0.529 17.6% 138.17 1,825.24 69.09 2,308.84 20.32%

EPS增长率 股利 期初未分配利润 提取盈余公积 期末未分配利润 销售净利润率%

1,004.25 0.2930 0.2930

60.25 1,825.24

1,043.99 23.78%

投资估算财务预测投资分析与企业估值EXCEL模版

投资估算财务预测投资分析与企业估值EXCEL模版投资估算、财务预测、投资分析与企业估值是对企业进行财务分析和评估的重要工具,其中包括了投资估算、财务预测、投资分析以及企业估值四个方面的内容。

通过这些工具,可以帮助投资者更好地了解和评估企业的财务状况和潜在回报。

在进行投资估算时,投资者需要对投资项目的相关成本进行估算。

这包括项目的初始投资、运营成本、项目周期内的现金流入和流出等。

这些成本的估算可以使用Excel模板来实现。

通过填写各项成本的信息,模板可以自动计算出整个项目的成本,并给出相应的指标和预测。

在进行财务预测时,投资者需要根据历史数据和市场趋势来预测企业的财务状况。

这包括营业收入、净利润、资产负债表、现金流量表等指标的预测。

通过使用Excel模板,可以方便地输入历史数据和市场预测,模板会自动计算出预测指标,并给出相应的图表和分析。

在进行投资分析时,投资者需要根据财务数据和其他相关信息来评估投资项目的可行性和风险。

这包括计算投资回报率、现金流量贴现率、内部收益率等指标,以及进行敏感性分析。

通过使用Excel模板,可以方便地计算出这些指标,并进行敏感性分析,以评估投资项目的风险和回报。

最后,在进行企业估值时,投资者需要基于企业的财务数据和市场情况来评估企业的价值。

这包括使用财务指标来计算企业的净资产价值、市净率、市盈率等指标,以及进行相应的比较和分析。

通过使用Excel模板,可以方便地计算出这些指标,并进行企业估值和风险评估。

总之,投资估算、财务预测、投资分析与企业估值是投资者进行投资决策和评估的重要工具。

通过使用Excel模板,可以方便地进行各项计算和分析,提高投资者的决策效率和准确性。

同时,敏感性分析也可以帮助投资者评估投资项目的风险和回报,为投资决策提供参考。

利用Excel构建企业价值评估模型初探

4 =E14 =F11*¥B¥5 =F12*¥B¥6 =F11+F13 =F12- F13

5 =F14 =G11*¥B¥5 =G12*¥B¥6 =G11+G13 =G12- G13

6 =G14 =H11*¥C¥5 =H12*¥C¥6 =H11+H13 =H12- H13

注: 投资资本是营业流动资金、厂房设备净额( 已扣除折旧) 以及其他资产净额( 净非流动无息负债) 的总和。 ①NPV(¥B¥8,C15:G15); ② - PV(¥C¥8,¥B¥4,,H15/(¥C¥8- ¥C¥7))。

表 2 中 , B16 单 元 格 的 计 算 公 式 为 NPV ( ¥B¥8,

C15:G15) 。NPV ( ) 称为净现值函数, 其语法为 NPV

( rate, value1, value2, …) , 功能为在未来连续期间的现

金 流 量 ( value1, value2, … ) 及 贴 现 率 ( rate) 的 条 件 下 ,

PV( rate, nper, pmt, fv, type) , 功 能 为 一 次 性 偿 还 额 ( fv)

的现值( 该函数有两种功能, 在此处采用的是其第二种

功能) 。但在 FCFF 估价法计算式中所应用数据的含义

为企业所获得的自由现金流量, 与偿还额的含义相反,

符号相异。因此, 需对现值函数取负值。在本案例中, 其

( 安徽商贸职业技术学院, 芜湖 241003) ( Anhui Business College of Vocational Technology, Wuhu 241003, China)

摘要: Excel 是一个功能强大、技术先进、使用方便的表格式数据综合管理与分析软件工具。我 们可以在企业价值评估中

实验一、用Excel做利润估计模型

《管理信息系统》课程

实验一、用Excel作利润估计模型一个公司需要对它的产品进行利润估计。

预计该产品的生命期为5年,总产量为50000个。

其他情况如下:

(1)产品单价:第1年为5.5元,考虑到通货膨胀率,以后每年估计以5%的速率上涨。

(2)销售成本:第1年是当年销售额的65%,以后按2%的速率递减。

(3)各年度中销售量占总产量的百分比为:10%,22%,32%,22%,14%。

(4)其他费用第1年为2000元,第2年后为上年度费用的5%递增。

(5)毛利为销售额和销售成本之差。

(6)推销费用按销售额的16%计算。

问题:

1.请用Excel做出该模型,输出下表,计算公司的总利润是多少?每年利润及其占总利润的百分比是多少?每年销售额占总额的百分比是多少?

2.如果第1年价格定为每件产品售价5元或6元,对公司分别会产生何种影响?

3.讨论对该模型和预测系统可能的改进。

要求:将以上实验过程、内容及问题分析,填写实验报告。

FinancialAnalysisExcelTemplates企业估值模板-lboval

FinancialAnalysisExcelTemplates企业估值模板-lboval44MERGER LBO __ON __ET44INPUT SHEET: MERGER LBO __ONSTEP 1: Estimate the total cost of the deal Price per share= # shares outstanding (mil)= Total cost of the deal= 201 21.9 6201.9 Debt outstanding currently (mil)= Other costs (Investment banker etc.)= 1800 0STEP 2: Define how the deal will be financed Repayment schedule ( as % of principal) Source Equity Pfd. STOCK Debt: Type 1 Debt: Type 2 Debt: Type 3 Debt: Type 4 Amount 1000 0 1700 3500 0 0 Int. rate NA 0.00% 16.00% 18.00% 0.00% 0.00% 12.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 10.00% 0.00% 10.00% 0.00% 10.00% 0.00% 10.00% 0.00% 20.00% 0.00% 20.00% 1 2 3 4 5 6 7 8 9Interest rate on debt remaining in terminal year=Suggestion: For the first run, enter an arbitrary schedule; Check cashflows to equity; If -'ve modify schedule;STEP 3: Define rates of future growth 1 RevenuesDepreciation (See below) Cap. Spending (See below) Working Cap : % of Revenue 14.00% 14.00% 14.00% 16.00% 2 14.00% 14.00% 14.00% 16.00% 3 14.00% 14.00% 14.00% 16.00% 4 14.00% 14.00% 14.00% 16.00% 5 14.00% 14.00% 14.00% 16.00% 6 8.00% 8.00% 8.00% 16.00% 7 8.00% 8.00% 8.00% 16.00% 8 8.00% 8.00% 8.00% 16.00% 9 8.00% 8.00% 8.00% 16.00% 10 8.00% 8.00% 8.00% 16.00%INPUT SHEET: MERGER LBO __ONPrice per share=# shares outstanding (mil)=Total cost of the deal=Debt outstanding currently (mil)=Other costs (Investment banker etc.)=STEP 2: Define how the deal will be financedRepayment schedule ( as % of principal)SourceEquityPfd. STOCKDebt: Type 1Debt: Type 2Debt: Type 3Debt: Type 4Suggestion: For the first run, enter an arbitrary schedule; Check cashflows to equity; If -'ve modify schedule;STEP 3: Define rates of future growthRevenuesDepreciation (See below)Cap. Spending (See below)WorkingCap : % of Revenue45MERGER LBO __ON __ET45COGS: % of Revenues85.68%85.68%85.68%85.68%85.68%85.68%85.68%85.68%85.68%85.68%Default values= If you do not enter rates, the growth rates in depreciation, capital spending = growth rate in revenues. The default values for COGS and Working Capital come from Step 6 below.STEP 4: __ __TION Current T.Bill rate= Ordinary tax rate= 8.00% 40.00% Market risk premium= Current beta of firm= 8.50% 1.05STEP 5: __ ASSETS TO BE SOLD (Enter the year in which assets will be sold and market value and CF to the firm from those assets) 1 Assets sold: Mkt. Value Assets sold: Revenues Assets sold: COGS (%) Assets sold: Depreciation Assets sold: Capital Spending $0 $0 0.00% $0 $0 2 $0 $0 0.00% $0 $0 3 $0 $0 0.00% $0 $0 4 $0 $0 0.00% $0 $0 5 $0 $0 0.00% $0 $0 6 $0 $0 0.00% $0 $0 7 $0 $0 0.00% $0 $0 8 $0 $0 0.00% $0 $0 9 $0 $0 0.00% $0 $0 10 $0 $0 0.00% $0 $0 [ Enter the market value of the asset sold; Enter the EBIT, Depreciation and Capital Spending of the asset; Only in the year sold]STEP 6: ENTER __TION ON __ INCOME __NT Revenues = Current EBIT = Current Int. Exp= Current Deprec'n= $10,000 $892.00 $200.00 $540.00 COGS as % of Revenue= Current Capital Spending= Working Cap. as % of Revenues= Interest rate on Debt Currently= 85.68% $438.00 16.00% 12.00% (Default = 1 - (EBIT+Depreciation)/Revenues)COGS: % of RevenuesDefault values= If you do not enter rates, the growth rates in depreciation, capital spending = growth rate in revenues. values for COGS and Working Capital come from Step 6 below.Current T.Bill rate=Ordinary tax rate=Market risk premium=Current beta of firm=STEP 5: __ ASSETS TO BE SOLD (Enter the year in which assets will be sold and market value and CF to the firm from those assets) Assets sold: Mkt. ValueAssets sold: RevenuesAssets sold: COGS (%)Assets sold: Depreciation[ Enter the market value of the asset sold; Enter the EBIT, Depreciation and Capital Spending of the asset; Only in the year sold]Revenues =Current EBIT =Current Int. Exp=Current Deprec'n=COGS as % of Revenue=Current Capital Spending=Working Cap. as % of Revenues=Interest rate on Debt Currently=46MERGER LBO __ON __ET46__WS FROM LBO PRE- LBO __ Revenues COGS Depreciation EBIT -Int: Type 1 -Int: Type 2 -Int: Type 3 -Int: Type 4 Taxable Income - Taxes Net Income + Deprec'n CF from Oper. - Capital Sp. - WC Chg - Prin. Rep:1 - Prin. Rep:2 - Prin. Rep:3 - Prin. Rep:4 - Pref. Div + Asset Sales CF to Equity $10,000 $8,568 $540 $892 $200 $0 $0 $0 $692 $277 $415 $540 $955 $438 $196 $0 $0 $0 $0 $0 $0 $321 1 $11,400 $9,768 $616 $1,017 $272 $630 $0 $0 $115 $46 $69 $616 $685 $499 $224 $0 $0 $0 $0 $0 $0 ($39) 2 $12,996 $11,135 $702 $1,159 $272 $630 $0 $0 $257 $103 $154 $702 $856 $569 $255 $0 $0 $0 $0 $0 $0 $32 3 $14,815 $12,694 $800 $1,322 $272 $630 $0 $0 $420 $168 $252 $800 $1,052 $649 $291 $0 $0 $0 $0 $0 $0 $112 4 $16,890 $14,471 $912 $1,507 $272 $630 $0 $0 $605 $242 $363 $912 $1,275 $740 $332 $0 $350 $0 $0 $0 $0 ($147) AFTER LBO 5 $19,254 $16,497 $1,040 $1,717 $272 $567 $0 $0 $878 $351 $527 $1,040 $1,567 $843 $378 $0 $350 $0 $0 $0 $0 ($5) 6 $20,794 $17,817 $1,123 $1,855 $272 $504 $0 $0 $1,079 $432 $647 $1,123 $1,770 $911 $246 $0 $350 $0 $0 $0 $0 $263 7 $22,458 $19,242 $1,213 $2,003 $272 $441 $0 $0 $1,290 $516 $774 $1,213 $1,987 $984 $266 $0 $350 $0 $0 $0 $0 $387 8 $24,255 $20,781 $1,310 $2,164 $272 $378 $0 $0 $1,514 $605 $908 $1,310 $2,218 $1,062 $287 $0 $700 $0 $0 $0 $0 $168 9 $26,195 $22,444 $1,415 $2,337 $272 $252 $0 $0 $1,813 $725 $1,088 $1,415 $2,502 $1,147 $310 $0 $700 $0 $0 $0 $0 $344 10 $28,291 $24,239 $1,528 $2,524 $272 $126 $0 $0 $2,126 $850 $1,275 $1,528 $2,803 $1,239 $335 $0 $700 $0 $0 $0 $0 $529 RevenuesCOGSDepreciationEBIT -Int: Type 1 -Int: Type 2 -Int: Type 3 -Int: Type 4Taxable Income - TaxesNet Income + Deprec'nCF from Oper. - Capital Sp. - WC Chg - Prin. Rep:1 - Prin. Rep:2 - Prin. Rep:3 - Prin. Rep:4 - Pref. Div + Asset SalesCF to Equity47MERGER LBO __ON __ET47+ Pref. Div + Int (1-t) + Princ. Rep CF to firm$0 $120 $0 $441$0 $541 $0 $502$0 $541 $0 $573$0 $541 $0 $653$0 $541 $350 $744$0 $503 $350 $849$0 $466 $350 $1,079$0 $428 $350 $1,165$0 $390 $700 $1,258$0 $314 $700 $1,359$0 $239 $700 $1,467 $17,828 $19,528Term Value of Equity= Term Value of Firm=MERGER LBO __ON __ET + Pref. Div+ Int (1-t) + Princ. RepCF to firm474748MERGER LBO __ON __ET48__ __RE AND COSTS OF EQUITY/__ PRE-LBO __ Debt: Type 1 Debt: Type 2 Debt: Type 3 Debt: Type 4 Pfd. Div Equity D/E D/(D+E+Pfd) Pfd/(D+E+Pfd) $1,800 $0 $0 $0 $0 $4,402 40.89% 29.02% 0.00% 1 $1,700 $3,500 $0 $0 $0 $1,000 520.00% 83.87% 0.00% 2 $1,700 $3,500 $0 $0 $0 $1,069 486.47% 82.95% 0.00% 3 $1,700 $3,500 $0 $0 $0 $1,223 425.09% 80.96% 0.00% 4 $1,700 $3,500 $0 $0 $0 $1,475 352.54% 77.90% 0.00% 5 $1,700 $3,150 $0 $0 $0 $1,838 263.91% 72.52% 0.00% AFTER-LBO 6 $1,700 $2,800 $0 $0 $0 $2,365 190.29% 65.55% 0.00% 7 $1,700 $2,450 $0 $0 $0 $3,012 137.78% 57.94% 0.00% 8 $1,700 $2,100 $0 $0 $0 $3,786 100.36% 50.09% 0.00% 9 $1,700 $1,400 $0 $0 $0 $4,694 66.04% 39.77% 0.00% 10 $1,700 $700 $0 $0 $0 $5,782 41.51% 29.33% 0.00%Beta Cost of Equity Interest rate WACC1.05 16.93% 12.00% 14.10%3.47 37.53% 17.35% 14.78%3.30 36.08% 17.35% 14.79%2.99 33.45% 17.35% 14.80%2.63 30.33% 17.35% 14.81%2.18 26.51% 17.30% 14.81%1.81 23.35% 17.24% 14.83%1.54 21.09% 17.18% 14.84%1.35 19.48% 17.11% 14.86%1.18 18.01% 16.90% 14.88%1.05 16.95% 16.58% 14.90%Cum Cost of Eq. Cum WACC1.__-__ 1.__-__2.__-__3.__-__4.__-__5.__-__6.__-__7.__-__8.__-__ 10.__-__ 1.__-__ 1.__-__ 1.__-__ 1.__-__ 1.__-__ 2.__-__ 2.__-__ 3.__-__ 3.__-__ 3.__-__Cum Cost of Eq.Cum WACC1.__-__1.__-__2.__-__3.__-__4.__-__5.__-__6.__-__7.__-__8.__-__0.__-__.__-__1.__-__1.__-__1.__-__.__-__2.__-__2.__-__3.__-__3.__-__3.__-__49MERGER LBO __ON __ET49__ OF THE MERGER/LBO __SPV of CF Equity Investors All Investors $1,974 $9,148Investment $1,000 $6,200Decision ACCEPT THE DEAL ACCEPT THE DEALCashflow to Equity Investors Average FCFE = Maximum FCFE = Minimum FCFE= Std. Deviation of FCFE= $164 $529 ($147) $214Leverage D/E Ratio before LBO = D/E Ratio after LBO = D/E Ratio in year 5= D/E Ratio in year 10 = 40.89% 520.00% 190.29% 24.09%Beta Beta before LBO = Beta after LBO = Beta in year 10 = 1.05 3.47 0.96__ OF THE MERGER/LBO __S50MERGER LBO __ON __ET50100.00% 20.00%After yr 10 8.00% 8.00% 8.00% 16.00%51MERGER LBO __ON __ET5185.68%TermYear$30,554$26,179$1,650$2,725$204$0$0$0$2,521$1,009$1,51 3$1,650$3,163$1,338$362$0$0$0$0$0$0$1,462$0$122$0$1,58554MERGER LBO __ON __ET54Term Year $1,700 $0 $0 $0 $0 $7,057 24.09% 19.41% 0.00%。

企业估值模型之财务预测分析excel模板

2018 Est 2,000 8 16,000 18,920 6,931 11,988 29,264 3,382 -20,658 -5,164 -15,493 -82% -5,349

2019 Est 2,000 12 24,000 32,636 12,358 21,200 2,285 5,580 13,335 3,334 10,001 31% 4,652

60,000 50,000 40,000 30,000 20,000 10,000 -10,000 净现金流

2015 Est -1,853

2016 Est -6,544

2017 Est 6,648

2018 Est 13,304

2019 Est 14,107

2020 Est 24,109

2021 Est 53,431

24,924 44,887 74,463 127,204

BOT+等离子装置销售NPV

80,000 60,000 63,701

-2,048 7,731 17,332 63,701

40,000 17,332 20,000 -2,048 -20,000 NPV,3年 NPV,4年 NPV,5年 NPV,7年 7,731

2020 Est 2,000 12 24,000 37,532 12,581 77,774 2,627 44,588 39,096 9,774 29,322 78% 33,974

2015 Est -5,112 3,259 -1,853

2016 Est -11,976 5,432 -6,544

2017 Est -15,080 21,728 6,648

15%

10%

2017 Est 2,056 788 2,578 144 384 2,050 512 1,537 75%

wind公司价值估值模型表格

wind公司价值估值模型表格英文回答:Valuation models are used to estimate the value of a company, such as Wind Corporation. There are several valuation models that can be used to determine the value of a company, including the discounted cash flow (DCF) model, the price-to-earnings (P/E) ratio model, and the comparable company analysis (CCA) model.The DCF model is a widely used valuation model that estimates the present value of a company's future cash flows. It takes into account the company's projected cash flows, the discount rate, and the terminal value. By discounting the projected cash flows back to their present value, the DCF model provides an estimate of the company's intrinsic value.The P/E ratio model is a simpler valuation model that compares a company's price-to-earnings ratio with its peersin the industry. The P/E ratio is calculated by dividing the company's market price per share by its earnings per share. By comparing the company's P/E ratio with the industry average, an estimate of the company's value can be derived.The CCA model is another commonly used valuation model that compares a company's financial metrics, such as revenue, earnings, and cash flow, with those of similar companies in the industry. By identifying comparable companies and analyzing their financial performance, an estimate of the company's value can be determined.In addition to these valuation models, there are other factors that can influence the value of a company. These include the company's growth prospects, market conditions, industry trends, and competitive landscape. It is important to consider these factors when performing a valuation analysis.中文回答:估值模型用于估计公司的价值,例如Wind公司。

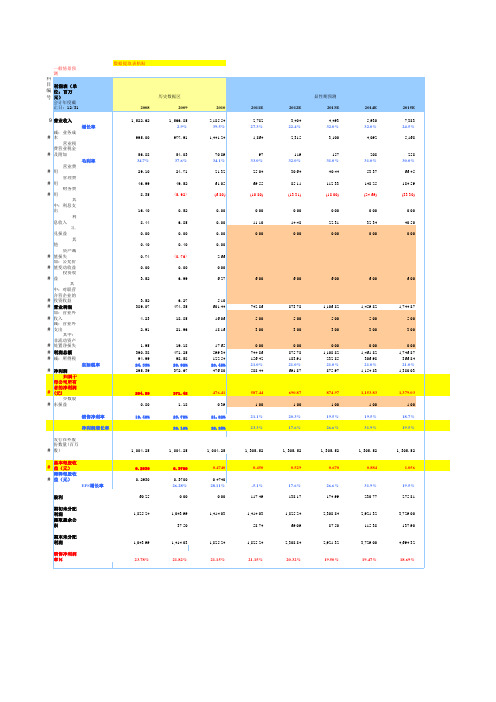

华星化工估值模型案例excel(xls18页).xls

2005A 35,524.00

41.47% 4,577.00 13.66% 2,371.00 10.43%

8.68% 0.365 19.66

1.71 11.03

2006E 48,675.93

37.02% 8,108.46 77.16% 3,522.90 48.58% 11.67%

0.542 13.23

50.00 3,648.24 2,135.69

784.38 5,267.29

0.00 5,237.29 3,522.90 4,070.69

2206E 35,559.58 10,837.12

0.00 4,449.46

565.90

37.02% 48.58% 77.16% 62.16% 24.26% 26.85% 11.67% 10.26%

增长率% 37.62% 37.02% N/A 9.94% 37.02%

NOPLAT

2004 25,110.00

6,468.00 55.00

1,929.00 1,146.00

197.00 3,251.00

0.00 3,245.00 2,147.00 2,281.31

2005 35,524.00

7,873.00 -49.00

2,596.00 1,496.00

221.00 3,511.00

一般情景预测

公司名称

分析日期 总股本

华星化工

2006/04/18 6,500.00

代码

流通A股 A股股价

002018

2,000.00 7.17

流通B股 B股股价

Word模板指标输出 主营收入(万元) 主营收入增长率 EBITDA(万元) EBITDA增长率 净利润(万元) 净利润增长率 ROE EPS(元) P/E P/B EV/EBITDA

估值模型EXCEL实例Valuationmodel(内含十个相连的表)

估值模型EXCEL实例Valuationmodel(内含十个相连的

表)

最新修改

增加了FCFE估值、DDM估值、APV估值、EVA估值和AE估值。

原先的估值对应FCFF估值。

其他估值模型有些数是链接到F 更改了自由现金流定义=EBIT×(1-所得税率)+折旧-资本支出-非现金性流动资本变化

预测前首先需要自己输入的数据

3主营收入及成本:各公司收入及成本的预测方法不尽相同,需要分析师自己做

4预测假设:各种假设条件

5固定资产预测:历史折旧和摊销

7损益表及利润分配:2003-2004A利润数据

8资产负债表:2003-2004历史数据

7损益表及利润分配、8资产负债表:无公式的单元格需要手动填入,如一些特殊会计科目

DCF估值(FCFF):分析日期、股本结构,假设条件中的“第二阶段增长率、长期增长率、应付债券利率、β”。

注意:第二阶段(2010其他估值模型:各假设条件(第二阶段年数也不可更改)11输出结果:2003-2004年经营活动现金流量、投资活动现金流量、融资活动现金流量。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

增长率% 37.62% 37.02% N/A 9.94% 37.02%

存货 长期投资 固定资产 无形资产 总资产 无息负债 有息负债 少数股东权益 股东权益

净营运资本 投入资本 IC

8,949.00 0.00 12,883.00 996.00 40,013.00 9,030.00 4,670.00 0.00 25,920.00 14,604.00 16,252.00

2008E 14,371.60 17,156.30 32.73% 9,667.15 38,271.86 46,605.00 11,977.94 10.48% 42,058.62

2007E

2008E

39.50% 87.54% 64.62% 78.89% 27.80% 27.25% 18.59% 17.96% 8.31%

2006E 48,675.93 37.02% 8,108.46 77.16% 3,522.90 48.58% 11.67% 0.542 13.23 1.54 6.94

2007E 67,905.18 39.50% 13,348.07 64.62% 6,606.93 87.54% 18.59% 1.016 7.05 1.31 3.88

每股指标 报表EPS 经常性EPS 每股红利 每股经营现金流 每股净资产

2003 0.47 0.08 1.95

2004 0.33 0.03 3.99

2005 0.36 0.10 4.20

2006E 0.54 0.10 1.26 4.64

流动性 净负债 / 权益 总负债 / 总资产 流动比率 速动比率

41.74% N/A 35.37% -10.00% 37.24% 52.73% 74.07% N/A 10.45% N/A 27.86%

现金流量表(万元) 净利润 折旧摊销 净营运资金增加 经营活动产生现金流 投资活动产生现金流 融资活动产生现金流 现金净增(减)

2004 2,147.00 579.00 13,925.00 1,372.00 -3,986.00 4,458.00 1,844.00

2005 2,371.00 845.00 -12,180.00 4,894.00 -1,156.00 -4,756.00 -1,018.00

2006E 3,522.90 2,056.79 -5,746.80 8,161.47 -12,500.00 7,266.65 2,928.12

增长率% 48.58% 143.41% N/A 66.76% N/A N/A N/A

41.47% 10.43% 13.66% 8.24% 22.22% 5.28% 8.68% 8.22% -2.28%

37.02% 48.58% 77.16% 62.16% 24.26% 26.85% 11.67% 10.26% 0.63%

价值比率 P/E EV / 收入 EV / EBITDA EV / EBIT EV / NOPLAT EV / IC P/B Dividend Yield (%)

指标说明: EV=股权价值+债权价值—现金 EBITDA = EBIT + 折旧 + 摊销 EBIT = 营业利润+财务费用 NOPLAT = EBIT ×(1-所得税率)= EBIT - 所得税(只考虑核心业务,扣除非经常性损益) IC(invested capital)= 股东权益 + 长期借款 + 短期借款 + 应付债券 + 少数股东权益-现金-短期投资-长期投资 ROIC = NOPLAT / IC × 100% OPFCF = EBITDA - 税收 - 净资本性支出- 营运资本的增加 WACC = [(Ke×Ve)+(Kd×Vd)] / (Ve+Vd)

2005 3,732.00 4,577.00 31.63% 2,551.49 31,033.00 46,605.00 11,771.00 10.50% 50,467.00

2006E 6,051.67 8,108.46 32.73% 4,070.69 39,678.80 46,605.00 20,489.52 9.63% 56,257.40

一般情景预测 公司名称 分析日期 总股本 华星化工 2006/04/18 6,500.00 代码 流通A股 A股股价 002018 2,000.00 7.17 流通B股 B股股价

Word模板指标输出 主营收入(万元) 主营收入增长率 EBITDA(万元) EBITDA增长率 净利润(万元) 净利润增长率 ROE EPS(元) P/E P/B EV/EBITDA 估值结果汇总 估值方法 FCFF FCFE DDM APV AE EVA

9.30% 38.87% 28.53% 32.75% 31.16% 60.30% 21.35% 25.26% 14.78%

2007E 7.05 0.76 3.88 4.78 7.11 1.28 1.31 2.69%

2008E 5.08 0.57 2.45 2.93 4.35 1.10 1.08 3.73%

11,801.00 0.00 29,587.00 210.00 55,787.00 15,644.00 11,771.00 0.00 27,322.00 2,424.00 31,033.00

16,726.45 151.00 40,051.21 189.00 76,559.78 23,892.86 20,489.52 0.00 30,177.41 -3,322.80 39,678.80

Kd = 债务成本 = 平均债务利率(1-税率)=(短期借款×短期借款利率+长期借款×长期借款利率+长期应付债券×长期 (1-所得税率) Ve = 股本价值 = 股价×总股本 (H股、B股按各自股价×汇率转换为人民币计算,非流通股按A股计算) Vd = 债务价值=短期借款+长期借款+应付债券 Ke = Rf + β (Rm-Rf) 营运资本 = 流动资产 - 流动负债 公司自由现金流 FCFF = EBIT× (1-所得税率)+折旧-资本支出-非现金性流动资本变化 股权资本自由现金流 FCFE = 税前利润× (1-所得税率)+折旧-资本支出-非现金性流动资本变化+新增债务-债务偿还

2003 0.04 49.22% 1.10 0.57

2004 -0.37 35.22% 2.27 1.49

2005 0.14 51.02% 1.10 0.60

2006E 0.32 60.58% 0.91 0.48

输出到Word模板中的三张表(输出2004-2008年) 利润表(万元) 主营业务收入 主营业务利润 其他业务利润 营业费用 管理费用 财务费用 营业利润 投资收益 利润总额 净利润 NOPLAT 2004 25,110.00 6,468.00 55.00 1,929.00 1,146.00 197.00 3,251.00 0.00 3,245.00 2,147.00 2,281.31 2005 35,524.00 7,873.00 -49.00 2,596.00 1,496.00 221.00 3,511.00 0.00 3,468.00 2,371.00 2,551.49 2006E 48,675.93 11,785.61 50.00 3,648.24 2,135.69 784.38 5,267.29 0.00 5,237.29 3,522.90 4,070.69 增长率% 37.02% 49.70% N/A 40.53% 42.76% 254.92% 50.02% N/A 51.02% 48.58% 59.54%

增长率% 39.50% 59.90% 0.00% 39.50% 39.50% 24.16% 87.04% N/A 87.54% 87.54% 78.89%

2008E 74,220.52 23,090.88 100.00 5,562.80 3,256.48 701.41 13,670.19 0.00 13,640.19 9,175.16 9,667.15

2007E 1.02 0.19 1.18 5.47

2008E 1.41 0.27 2.02 6.61

2007E 0.15 59.70% 1.08 0.59

2008E -0.11 52.61% 1.32 0.75

2007E 67,905.18 18,844.87 50.00 5,089.47 2,979.39 973.86 9,852.14 0.00 9,822.14 6,606.93 7,282.18

资产负债表(万元) 流动资产 货币资金 短期投资 应收帐款 其他应收款

2004 26,134.00 14,338.00 0.00 1,730.00 233.00

2005 25,839.00 7,909.00 0.00 4,047.00 413.00

2206E 35,559.58 10,837.12 0.00 4,449.46 565.90

2003 15.11 1.62 9.40 9.40 13.83 3.56 3.68 1.16%

2004 21.71 1.47 9.17 10.71 16.19 2.27 1.80 0.48%

2005 19.66 1.42 11.03 13.52 19.78 1.63 1.71 1.39%

2006E 13.23 1.16 6.94 9.30 13.82 1.42 1.54 1.43%

估值结果 20.64 16.38 2.86 17.99 10.10 16.33

估 值 区 间 17.08 - 14.90 - 2.63 - 14.90 - 9.65 - 14.21 -

23.62 19.09 3.29 20.13 10.94 18.10

EVA AE APV DDM FCFE FCFF 0.00 5.00 10.00 15.00 20.00 25.00

EBIT EBITDA 所得税率 NOPLAT IC Ve Vd WACC EV

2003 3,473.00 3,473.00 32.01% 2,361.42 9,162.00 32,265.00 2,700.00 11.55% 32,649.00