外文翻译--研发费用资本化和盈余管理:以意大利上市公司为例.

研发投入资本化与盈余管理

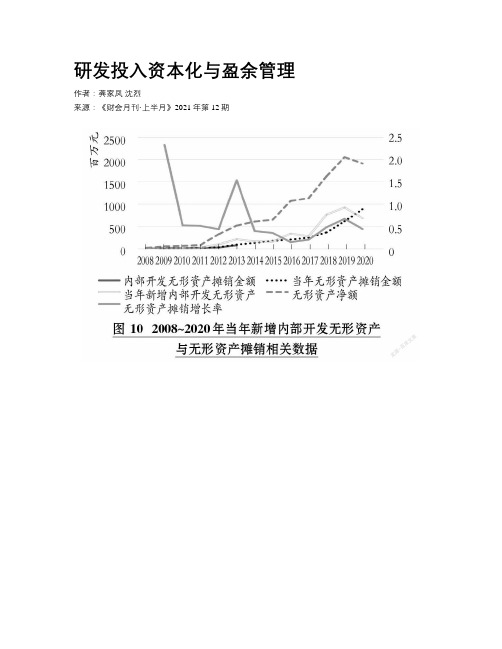

研发投入资本化与盈余管理作者:龚家凤沈烈来源:《财会月刊·上半月》2021年第12期【摘要】研发投入资本化的制度安排,除了能够激发企业研发活力、提升创新能力,还给盈余管理提供了空间,因而成为各利益相关者关注的重点。

选择“人工智能第一股”KXF公司作为研究对象,对其管理层借助研发资本化进行盈余管理的动机、手段和影响研究,结果表明:研发投入资本化与净利润的变动存在反向关系,说明可能存在盈余管理行为; 管理层为掩盖收入后续增长疲乏、避免利润下降进行盈余管理,而业绩压力强化了该动机; 盈余管理能够粉饰业绩,达到使业绩平稳增长的目的,但盈余管理行为会给未来业绩增长带来较大的“副作用”。

【关键词】研发投入;资本化;盈余管理;人工智能【中图分类号】 F276.6 【文献标识码】A 【文章编号】1004-0994(2021)23-0041-9一、引言“推动互聯网、大数据、人工智能和实体经济深度融合”,在党的“十九大”已经上升为国家战略[1] 。

2021年,作为“十四五”规划的开局之年,人工智能已经成为推动国家发展的中坚力量,涉及安防、政务、交通、教育、医疗等在内的多个领域,具体应用包括智慧政法、智能互联网汽车、智能服务机器人、智能语音交互系统、视频图像身份识别、智慧医疗等。

在当前保持高质量经济发展的背景下,人工智能企业面临着激烈的竞争,要想在市场竞争中占有一席之位,创新策源能力是关键[2] ,无形资产具有一定的独特性和难以模仿性,其正是人工智能企业核心竞争力的异质性资源[3] 。

这些企业在语音识别、视觉识别、自动化技术等的研发及与实体经济的融合上迎来了巨大发展机遇,同时也面临着严峻挑战。

根据我国现行会计准则的规定,无形资产是企业拥有或控制的没有实物形态的可辨认非货币性资产,包括土地使用权、专利权、著作权、商标权、非专利技术和特许权。

我国《企业会计准则第6号——无形资产》规定,无形资产的内部研发活动分为研究阶段和开发阶段,由于研究阶段具有较大的不确定性,将无形资产的研发投入全部作为费用化处理,计入当期损益,抵减了企业当期利润; 开发阶段具备形成新产品的基本条件,其研发投入符合资本化条件的可资本化处理,在达到预定用途后满足无形资产确认条件时,可确认为无形资产,后续在一定年限内进行摊销,因此对当期利润没有直接影响,内部开发无形资产资本化的处理能够满足企业短期提高净利润的需求。

研发支出资本化与盈余管理

研发支出资本化与盈余管理当今经济环境复杂多变,经济与科技都在高速发展。

企业要想在变幻莫测的市场中可持续地发展,就需要提高科技创新、加强研发投资,从而获取战略性的竞争优势。

如今大多数企业都意识到研发投资对企业发展和竞争的至关重要的作用,越发注重对研发项目的投资。

在研发投资备受瞩目的大环境下,企业对其研发投资的确认、计量和披露等会计处理对企业的财务报告有着重要影响。

针对研发支出采用不同的会计处理不仅影响着会计报表的真实性和可比性,而且可能会影响企业乃至整个国家的科技进步与发展。

为了经济健康发展,制定正确合理的研发投资相关的会计政策显得尤为重要。

我国现行会计准则中研发支出资本化的会计政策改变了原有的研发支出全部费用化的做法,根据具体的研发支出资本化确认条件,将满足确认条件的研发支出进行资本化会计处理,并形成一项资产。

许多学者认为研发支出资本化会计政策能够有效减少研发支出费用化会计政策所引起的一些盈余管理行为。

而且研发支出资本化会计政策为企业提供利于科研创新的宽松环境,对研发投资比例较大的企业财务业绩有所改善,能够提高企业研发创新的积极性。

然而,研发支出资本化会计政策的资本化确认条件存在很多界定判断不明确的地方,过多依赖于会计人员的专业判断。

并且企业向外界披露关于自身研发活动的信息很少,企业相关利益者和监管机构对企业的研发活动了解不多并难以监管。

这样研发支出资本化很可能成为企业盈余管理的一大途径。

本文结合盈余管理理论对现行会计准则中研发支出资本化会计政策进行剖析,认为研发支出资本化会计政策在抑制某方面盈余管理行为的同时,企业很可能会利用研发支出资本化会计政策进行多种方式的盈余管理。

本文结合实证方法和实验方法两种研究方法,对研发支出资本化与盈余管理的问题进行深入研究分析。

首先,本文以2007年至2012年沪深两市A股上市公司为研究样本,将盈余管理行为进行细分为应计利润盈余管理、操纵经营活动现金流的真实盈余管理、操纵产品成本的真实盈余管理、操纵斟酌性费用的真实盈余管理以及综合的真实盈余管理;通过扩展琼斯模型和Roychowdhury的真实盈余管理模型分别计算出样本公司的应计盈余管理程度、操纵经营活动现金流的真实盈余管理程度、操纵产品成本的真实盈余管理程度、操纵斟酌性费用的真实盈余管理程度以及综合的真实盈余管理程度;再将研发支出资本化分别与这五方面的盈余管理程度进行模型回归分析。

研发费用资本化和盈余管理 英文

Garen Markarian,Lorenzo Pozza,Annalisa Prencipe,International Jou rnal of Accounting2008-3 爱思唯尔期刊Capitalization of R&D Costs and Earnings Management:Eviden ce from Italian Listed CompaniesABSTRACT: The capitalization of research and development (R&D) costs is a controversial accounting issue because of th e contention that such capitalization is motivated by incenti ves to manipulate earnings. Based on a sample of Italian list ed companies, this study examines whether companies' decision s to capitalize R&D costs are affected by earnings-management motivations. Italy provides a natural context for testing ou r hypothesized relationships because Italian GAAP allows for the capitalization of R&D costs. Using a Tobit regression mod el to test our hypotheses, we show that companies tend to use cost capitalization for earnings-smoothing purposes. The hyp othesis that firms capitalize R&D costs to reduce the risk of violating debt covenants is not supported. KEY WORDS: Earnin gs management, Cost capitalization, R&D accounting, Earnings smoothing, Debt covenants, Italian companies1 Introduction In the current era of globalization, a high ly relevant issue facing regulators, academics, and practitioners is the determination of an appropriate accounting treatm ent for research and development (R&D) costs. International A ccounting Standards discuss accounting for R&D costs in IAS N o. 38 “Intangible Assets” (IASB, 2004; IASB, 2004). Paragrap h 54 of this standard states that no intangible asset arising from research (or from the research phase of an internal pro ject) shall be recognized as an asset; and that research expe nses shall be expensed in the income statement when they are incurred. Concerning development costs, paragraph 57 states t hat an intangible asset arising from development (or from the development phase of an internal project) shall be recognize d if, and only if, an entity can demonstrate all of the follo wing: (a) the technical feasibility of completing the intangi ble asset so that it will be available for use or sale; (b) i ts intention to complete the intangible asset and use or sell it; (c) its ability to use or sell the intangible asset; (d) how the intangible asset will generate probable future econo mic benefits; (e) the availability of adequate technical, fin ancial, and other resources to complete the development and t o use or sell the intangible asset; (f) its ability to measur e reliably the expenditure attributable to the intangible ass et during its development. Although IAS 38 allows companies to capitalize development costs, the inherent subjectivity of the validation process permits management to exercise discret ion in deciding whether the conditions of IAS 38 have been sa tisfied. In essence, IAS 38 gives management considerable fle xibility regarding the treatment of development costs.US GAAP takes a stricter approach to the issue. SFAS No. 2—Accounting for Research and Development Costs (FASB, 1974)—requires that all R&D expenditures be expensed in the curre nt period. The only exception to the full expensing rule is s tated in SFAS No. 86. The exception relates to the capitaliza tion of software development costs (FASB, 1985). At the inter national level, certain national accounting standards (e.g., those of Italy) allow flexibility for the capitalization of R &D costs when some conditions are satisfied. These are condit ions similar to those required by IAS.The capitalization of R&D costs has always been a controve rsial accounting issue. Supporters of capitalization report r esults suggesting that R&D is a long-lived asset that influen ces future profitability (e.g., Bublitz and Ettredge, 1989, J anuary; Sougiannis, 1994, January; Ballester et al., 2003). A lso, R&D costs are positively related to market value (Hirschey and Weygandt, 1985, Spring; Shevlin, 1991, January; Sougia nnis, 1994, January) and yield value-relevant information to investors (e.g., Aboody and Lev, 1998; Lev and Zarowin, 1999; Healy et al., 2002; Monahan, 2005). Supporters of expensing are fewer. They stress the lack of reliable evidence of futur e economic benefits (e.g., FASB, 1974; Association for Invest ment Management and Research, 1993; Kothari et al., 2002) or refer to the benefits of consistency and comparability, point ing out that such benefits trump the costs identified by the supporters of capitalization. Additionally, reliability and t he risk of earnings-management policies are underscored by su pporters of the most conservative accounting treatment. In pa rticular, expensing is preferable to capitalization because i t increases the objectivity of financial statements. That is, it eliminates the opportunity for managers to capitalize cos ts of projects that have low probabilities of success or to d elay impairment of R&D assets ( Nelson et al., 2003; Schilit, 2002). The debate surrounding the most effective accounting method for R&D costs supplements other literature that examin es the trade-off between relevance (i.e., the predictive abil ity) and reliability (i.e., the representative faithfulness) of accounting information (FASB, 1980; AICPA, 1994; IASB, 2004; IASB, 2004). Thus far, empirical research on R&D costs has focused mainly on the relevance side of the trade-off, while little has been written about the reliability side that is, the possibility that R&D costs are subject to earnings manage ment.However, a few studies have indeed shown that R&D expendit ures are subject to real earnings management. In short, this means that companies cut their R&D investments in order to ac hieve their earnings goals (e.g., Perry and Grinaker, 1994; B ushee, 1998; Mande et al., 2000). But there is still a paucit y of research that explores the motives behind the accounting treatment of R&D costs within a setting where flexibility is allowed. Testing whether companies engage in earnings manage ment through R&D cost accounting can significantly contribute to the debate around the best treatment for such costs. This debate has recently been raised within the convergence proje ct by US GAAP and IAS/IFRS. Illustrating that R&D cost capita lization is motivated by incentives to manipulate earnings wo uld support the current U.S. GAAP position, which does not al low the capitalization of such costs. On the contrary, showin g that companies do not use R&D cost accounting for earnings-management purposes would support the approach now stated byIAS/IFRS, in which capitalization is allowed under certain co nditions. This study contributes to this debate by providing empirical evidence on the motivations for R&D cost capitaliza tion. We hypothesize that the decision to capitalize R&D expe nditures is related to two primary motivations: income smooth ing and debt contracting. We test our hypotheses using a samp le of firms listed on the Milan Stock Exchange. Multivariate results indicate that firms use capitalization of R&D costs t o smooth earnings, while there is no support for the debt-cov enant hypothesis. These results are robust within a variety o f firm characteristics, such as firm size, risk, opportunitie s for growth, profitability, governance characteristics, indu strial membership, and time control. The paper proceeds as fo llows. Section 2 introduces accounting in Italy and the insti tutional background relating to R&D accounting. Section 3 dis cusses the previous literature. Section 4 presents the hypoth eses andis followed by the research methods in Section 5. Section 6 presents the results and Section 7 concludes the study. 2 R &D accounting in Italy Italian accounting regulation has alwa ys allowed for some flexibility in the capitalization of R&Dcosts. This allowance is similar to that of IAS. Accounting f or intangibles, including R&D costs, is regulated by Principi o Contabilen. 24 (Accounting Standard No. 24). This standard distinguishes three different types of R&D costs as follows: 1) “Basic research,” which consists of studies, surveys, and experiments that do not refer to a specific project; this ty pe of R&D cost is normally carried out for the general utilit y of a company (e.g., market research, updating, etc.);2) “Applied research,” which consists of studies, surveys, and experiments that refer to specific projects;3) “Development,” which consists of the application of re search results to specific materials, tools, products, and pr ocesses preceding production.The costs for basic research are to be expensed in the inc ome statement. However, costs related to applied R&D can be c apitalized if the following conditions are met: a) the costs refer to a project for the realization of a clearly defined p roduct or process; b) the costs are identifiable and measurab le; c) the project to which the costs refer is technically fe asible; d) the company owns the necessary resources to comple te and exploit the project; and e) the costs are recoverable through the revenues generated by exploiting the project. Itis evident that the conditions stated by the Italian accounti ng standards are similar to those stated by IAS for developme nt costs. In fact, the definition of applied research under I talian standards also fits into the definition of development costs provided by IAS 38. The Italian standards differ from IAS in that they do not require R&D capitalization when the a bovementioned conditions occur, leaving flexibility in the ha nds of the companies. However, this difference is more formal than substantive. Given the subjectivity in assessing the oc currence of some of the conditions, it seems that, even under IAS, companies that prefer immediate expensing can easily ju stify this approach—even when the aforementioned conditions are met. Concerning the amortization of R&D costs, the Italia n accounting standards require that the amortization be carri ed out over a period of no longer than five years beginning f rom the moment the outcome (product or process) is ready to b e used. The Italian Civil Code (art. 2426) states that the ca pitalization of R&D costs shall be authorized by the collegio sindacale (statutory auditors) and that it is not possible t o pay dividends until there are enough retained earnings to c over the carrying amount of the capitalized R&D costs. This s tipulation limits the incentive to capitalize R&D costs for the purpose of increasing the amount of dividends paid. The Ci vil Code also requires that R&D activities be discussed in th e relazione sulla gestione (management discussion and analysi s section); however, there is no clear requirement as to what quantitative or qualitative disclosures should be relayed wi th regard to the capitalization of R&D costs. Finally, the Ci vil Code states that information regarding the amortization s chedules of such R&D costs be provided in the explanatory not es of the financial statements. 3 Earnings management and spe cific accrualsEarnings management is defined as a “purposeful interventi on in the external financial-reporting process, with the intent of obtaining some private gain” (Schipper, 1989, p. 92). In generally accepted terms, earnings manageme nt occurs “when managers use judgment in financial-reporting and in structuring transactions to alter financial reports to either mislead some stakeholders about the underlying econom ic performance of the company or to influence contractual out comes that depend on reported accounting numbers” (Healy & Wa hlen, 1999, p. 368). The large amount of research carried out thus far indicates that managers exercise discretion and man age earnings using a wide variety of methods, ranging from carrying out special transactions (so-called real earnings mana gement) to the manipulation of accruals. Several of the main incentives for earnings management include debt covenants, bo nus plans, and income smoothing. The debt-covenant hypothesis suggests that managers have an incentive to manage earnings in order to avoid violating covenants in debt contracts, whic h are typically stated in terms of accounting numbers or rati os. The bonus-plan hypothesis suggests that managers manage e arnings in order to maximize compensation. Healy (1985) shows that managers tend to reduce earnings if they fall either ab ove or below bonus-plan bounds. In contrast, they tend to inc rease earnings when they fall between the two bounds. Finally, the income-smoothing hypothesis suggests that firms aspire t o reduce earnings fluctuations.Empirical earnings-management studies find support for the abovementioned motives in a variety of contexts. Many of the se studies test the relationship between aggregate accruals a nd incentives for earnings management (e.g., Healy, 1985; DeA ngelo, 1986; Dechowet al., 1995). As an alternative approach, other studies focus on single items, suggesting that income from specific accruals is related in a systematic way to earn ings-management incentives. Among these latter studies, McNichols and Wilson (1988) show that companies manage their bad-d ebt provisions according to the bonus-plan hypothesis (Healy, 1985). Zucca and Campbell (1992) examine discretionary asset write-downs, showing that companies use these accruals eithe r for “big bath” strategies or for earnings smoothing. Franc is, Hanna, and Vincent (1996) confirm that earnings-managemen t incentives play a significant role in explaining goodwill w rite-offs and restructuring charges. Other studies focus on a llowances for deferred taxes (e.g., Miller and Skinner, 1998; Schrand and Wong, 2003). These studies provide mixed results. Finally, Dowdell and Press (2004) analyze the in-process R&D write-offs, but they do not find evidence to support their b onus-plan hypothesis. In line with the aforementioned studies on earnings management and specific accruals, this study aim s at testing whether the decision to capitalize or to expense R&D costs (when flexibility exists) is affected by earnings-management motives. 4 Hypotheses development Previous researc h investigates three main incentives for earnings management: earnings smoothing, debt covenant, and bonus-plan incentives. In this study, we focus on the first two since disclosure of data on the existence and structure of bonus plans by Italia n companies is limited. The income-smoothing hypothesis suggests that a manager's accounting discretion is driven by his o r her desire to reduce income-stream variability (Fudenberg a nd Tirole, 1995). The process of smoothing serves to moderate year-to-year fluctuations in income by shifting earnings fro m peak years to less successful periods. This process lowers the peaks and makes earnings fluctuations less volatile (Cope land, 1968).Income smoothing has been viewed both as a positive strate gy, whereby managers transmit privateinformation to investors (e.g., Gordon, 1964, April; Beidl eman, 1973; Ronen and Sadan, 1981; Tucker and Zarowin, 2006), and as a manipulative practice driven by opportunistic aims ( Gordon, 1964, April; Imhoff, 1977, Spring ;Kamin and Ronen, 1978). In this study, we do not intend to argue for either o ne of these two views. Rather, we test whether R&D cost capit alization is used for purposes of earnings smoothing.。

外文翻译上市公司财务舞弊原因及对策

外文翻译上市公司财务舞弊原因及对策在当今复杂多变的经济环境中,上市公司财务舞弊问题日益严重,不仅损害了投资者的利益,破坏了市场的公平和透明,也给整个经济社会带来了负面影响。

本文旨在深入探讨外文翻译上市公司财务舞弊的原因,并提出相应的对策,以维护市场的健康稳定发展。

一、外文翻译上市公司财务舞弊的原因(一)利益驱动利益是导致外文翻译上市公司财务舞弊的首要原因。

公司管理层为了达到个人或团体的经济利益,如获取高额薪酬、奖金、股票期权等,可能会操纵财务数据。

此外,公司为了满足上市要求、获得融资、避免退市等,也会不惜通过舞弊手段来美化财务报表。

(二)公司治理结构不完善公司内部治理结构的缺陷为财务舞弊提供了机会。

如果董事会、监事会等监督机制失效,管理层权力过大且缺乏有效制衡,就容易出现财务舞弊行为。

同时,内部审计部门独立性不足,无法发挥有效的监督作用,也使得财务舞弊难以被及时发现和制止。

(三)外部监管不力证券监管部门的监管力度不足,法律法规不够健全,对财务舞弊行为的处罚力度不够严厉,使得上市公司违法成本较低。

此外,审计机构、评级机构等第三方中介机构未能尽职尽责,也在一定程度上纵容了财务舞弊行为的发生。

(四)压力与动机公司面临的业绩压力、市场竞争压力以及来自股东和投资者的期望压力,都可能促使管理层采取不正当手段来达到预期的财务目标。

例如,当公司业绩不佳时,为了稳定股价、避免投资者恐慌抛售,管理层可能会选择财务舞弊。

(五)财务人员职业道德缺失部分财务人员缺乏职业操守和道德底线,为了个人利益或者迫于上级压力,参与或协助财务舞弊。

他们可能故意篡改财务数据、编制虚假财务报告,严重违背了会计职业的诚信原则。

(六)信息不对称上市公司与投资者之间存在信息不对称,投资者难以获取公司真实、准确、完整的财务信息。

这种信息差距使得上市公司更容易进行财务舞弊,而投资者难以察觉和防范。

二、外文翻译上市公司财务舞弊的对策(一)完善公司治理结构建立健全的公司治理机制,优化董事会结构,增强董事会的独立性和专业性。

研发支出资本化、项目责任与真实盈余管理

研发支出资本化、项目责任与真实盈余管理【摘要】本文采用实验研究方法,检验了研发支出会计政策与项目责任这两个因素对真实盈余管理的影响。

研究发现,研发支出资本化、项目经理对项目承担高度责任这两种情况,都可能会导致经理采取过度投资形式的声誉驱动的真实盈余管理,并且当研发支出资本化且经理承担高度项目责任时,与项目挂钩的个人薪酬会加大项目经理过度投资的可能性。

【关键词】研发支出资本化费用化盈余管理过度投资一、引言当今社会,企业的研发活动对企业竞争和发展至关重要。

企业研发活动的确认、计量及披露将直接影响企业的财务报告和经济活动。

制定科学的研发支出会计政策能够更好地鼓励企业对高新科技的探索与投资,真正提升企业核心竞争力,甚至提高整个国家的科技创新水平。

2007年之前我国的企业会计准则规定研发支出全部费用化。

2007年1月1日开始实施的新会计准则中明确规定,我国研发支出分为研究阶段支出和开发阶段支出,其中研究阶段支出在当期全部费用化,开发阶段支出实行有条件的资本化。

这体现了我国会计准则的国际趋同,也是对以前完全费用化的会计处理进行的修正。

新会计准则的研发支出有条件资本化的会计政策在某些方面抑制了盈余管理行为,但同时在某些方面又为盈余管理提供了方便。

国内外有大量经验证据表明,当研发支出费用时,企业很有可能通过削减研发支出来调节盈余,以达到避免亏损、平滑收益、提高薪酬等目的。

也有经验证据(Lev和Zarowin,1999;Oswald 和Zarowin,2007)表明,研发支出资本化会计政策能抑制住削减研发支出的倾向,并且有很好的市场信号传递作用。

同时,还有一些研究(Suzanne Landry,2003;Nicholas Seybert,2009;许罡和朱卫东,2010;李世新和张燕,2011)表明,企业会利用研发支出资本化这一会计政策进行盈余管理。

研发支出费用化和资本化这两种会计政策选择会以不同方式影响盈余,我国新会计准则中的研发支出会计政策的变更导致企业的盈余管理方式发生了变化。

浅谈研发支出资本化、盈余管理及财税问题影响研究

浅谈研发支出资本化、盈余管理及财税问题影响研究作者:张宁来源:《商情》2020年第40期【摘要】随着当今研究开发活动的日益增多,研发支出已经成为大家普遍关心的问题,本文将主要采用文献调查法,对研发支出资本化和盈余管理及财税展开进一步的研究,对两者的关系进行梳理,并且归纳总结出目前存在的问题并提出有效的解决措施,以便为今后的相关工作提供重要参考。

【关键词】研发支出; 盈余管理; 资本化一、研发支出和盈余管理的综合概述(一)研发支出的相关定义研发就是研究和开发的总称,世界各组织对其定义都有所不同,联合国的权威组织将其定义成一种创新活动。

研发支出就是指某企业在研发阶段所产生的所有费用,包括:资产的摊销、折旧、人工费用、租金等所有内容。

企业的研发主要是针对现有服务或是产品的升级改造,提出全新的服务,以此来实现优化产业结构的主要目的。

(二)盈余管理的相关定义关于盈余管理的基本定义,大致分为两类,一类是认为盈余管理的主要目标是实现企业利益的最大化,从而对财务盈余活动进行人为干预。

另外一种说法是说,盈余管理实际上是企业在一定政策范围内对相关会计信息的合理调整。

就目前研究的成果表明,我国的许多学者都一致认为盈余管理是一种欺骗性的行为,企业在日常管理中应该尽可能避免盈余管理。

盈余管理又可以分为真实盈余和应计盈余,主要是根据处理方法不同而进行划分的。

真实盈余和应计盈余最大的区别在于,真实盈余可以对企业的现金流造成影响。

二、存在的问题(一)支出资本化的相关界定主观性比较明显由于行业间存在明显的差异性,因此行业内部项目不同,其研发进度也存在差异,这种情况就容易导致目前执行的新型会计准则对研发支出相关研究的划分主观意识比较强,会计人员在实际工作中随意性比较大,自由操作空间比较大。

对于一些特殊行业,其研发支出占有特别大的比重,会计人员需要结合实际情况,对研究进行科学界限划定,由此可以看出,支出资本化对会计人员的专业技能有极高的要求,会计人员的业务水平直接影响着工作质量。

外文翻译 公司股权结构对盈余稳健性的影响(中英文)

公司股权结构对盈余稳健性的影响:来自中国的证据The Effects of Corporate Ownership Structure on Earnings Conservatism: Evidence from China原文出处:Asian Journal of Finance & Accounting ISSN 1946-052X 2010, Vol. 2, No. 1: E3译文:本文研究企业的所有制结构对收入保守主义的增量效应,研究中国上市公司的数据。

我们采用的概念有巴苏(1997)保守主义定义盈余稳健性和采用条件的实证模型,Ball和Shivakumar(2005年)来衡量发展程度的盈利保守主义。

我们的实证结果显示,公司的盈利具有较高的非流通股股东有较低的盈余稳健性。

与以前的研究中,这种一致点表明,该公司与国家和集中的所有权结构更可能依赖于私人通信,以减少信息不对称和内部解决代理问题,从而创造一个低的盈余稳健性的需求。

本研究结果有助于我们了解公司的所有权结构的性能影响在新兴市场和后共产主义市场的盈利。

关键词:盈余稳健性,非流通股股东,股权结构,后共产主义研究,股权分置,国家所有制1。

介绍在20世纪90年代,中国发射了上海证券交易所和随后的深圳证券交易所上市。

除了允许国有企业(国有企业)取得外国资本证券交易所的建立,其目的是提高性能的国有企业通过在资本市场的压力和问责制。

然而,由于政治和经济问题及可能的外资收购的地方国有企业,中国政府拒绝了一个完整的企业私有化,并打算保留其立场作为企业的东主,为了抢占资源分配的控制范围内国家(Allen等,2005)。

该国目前有一些共产主义元素和一些适用范围更广共产党党内监督的资本主义分子,从这个意义上我们主要是在未知的水域。

斯洛文尼亚的后共产主义哲学家齐泽克(2010年),中国的资本主义和共产主义,而独特的合成比是不稳定的,一直是广泛成功的实验,已经持续了30年之久。

外文翻译--加纳上市公司资本结构对盈利能力的实证研究(节选)

中文3150字,2100单词,10800英文字符出处:Abor J. The effect of capital structure on profitability: an empirical analysis of listed firms in Ghana[J]. Journal of Risk Finance, 2005, 6(November):438-445.外文翻译The effect of capital structure on profitability : an empirical analysis of listed firms in GhanaAuthor:Joshua AborIntroductionThe capital structure decision is crucial for any business organization. The decision is important because of the need to maximize returns to various organizational constituencies, and also because of the impact such a decision has on a firm’s ability to deal with its competitive environment. The capital structure of a firm is actually a mix of different securities. In general, a firm can choose among many alternative capital structures. It can issue a large amount of debt or very little debt. It can arrange lease financing, use warrants, issue convertible bonds, sign forward contracts or trade bond swaps. It can issue dozens of distinct securities in countless combinations; however, it attempts to find the particular combination that maximizes its overall market value.A number of theories have been advanced in explaining the capital structure of firms. Despite the theoretical appeal of capital structure, researchers in financial management have not found the optimal capital structure. The best that academics and practitioners have been able to achieve are prescriptions that satisfy short-term goals. For example, the lack of a consensus about what would qualify as optimal capital structure has necessitated the need for this research. A better understanding of the issues at hand requires a look at the concept of capital structure and its effect on firm profitability. This paper examines the relationship between capital structure and profitability of companies listed on the Ghana Stock Exchange during the period 1998-2002. The effect of capital structure on the profitability of listed firms in Ghana is a scientific area that has not yet been explored in Ghanaian finance literature.The paper is organized as follows. The following section gives a review of the extant literature on the subject. The next section describes the data and justifies the choice of the variables used in the analysis. The model used in the analysis is then estimated. The subsequent section presents and discusses the results of the empirical analysis. Finally, the last section summarizes the findings of the research and also concludes the discussion.Literature on capital structureThe relationship between capital structure and firm value has been the subject of considerable debate. Throughout the literature, debate has centered on whether there is an optimal capital structure for an individual firm or whether the proportion of debt usage is irrelevant to the individual firm’s value. The capital structure of a firm concerns the mix of debt and equity the firm uses in its operation. Brealey and Myers (2003) contend that the choice of capital structure is fundamentally a marketing problem. They state that the firm can issue dozens of distinct securities in countless combinations, but it attempts to find the particular combination that maximizes market value. According to Weston and Brigham (1992), the optimal capital structure is the one that maximizes the market value of the firm’s outstanding shares.Fama and French (1998), analyzing the relationship among taxes, financing decisions, and the firm’s value, concluded that the debt does not concede tax benefits. Besides, the high leverage degree generates agency problems among shareholders and creditors that predict negative relationships between leverage and profitability. Therefore, negative information relating debt and profitability obscures the tax benefit of the debt. Booth et al. (2001) developed a study attempting to relate the capital structure of several companies in countries with extremely different financial markets. They concluded that the variables that affect the choice of the capital structure of the companies are similar, in spite of the great differences presented by the financial markets. Besides, they concluded that profitability has an inverse relationship with debt level and size of the firm. Graham (2000) concluded in his work that big and profitable companies present a low debt rate. Mesquita and Lara (2003) found in their study that the relationship between rates of return and debt indicates a negative relationship for long-term financing. However, they found a positiverelationship for short-term financing and equity.Hadlock and James (2002) concluded that companies prefer loan (debt) financing because they anticipate a higher return. Taub (1975) also found significant positive coefficients for four measures of profitability in a regression of these measures against debt ratio. Petersen and Rajan (1994) identified the same association, but for industries. Baker (1973), who worked with a simultaneous equations model, and Nerlove (1968) also found the same type of association for industries. Roden and Lewellen (1995) found a significant positive association between profitability and total debt as a percentage of the total buyout-financing package in their study on leveraged buyouts. Champion (1999) suggested that the use of leverage was one way to improve the performance of an organization.In summary, there is no universal theory of the debt-equity choice. Different views have been put forward regarding the financing choice. The present study investigates the effect of capital structure on profitability of listed firms on the GSE.MethodologyThis study sampled all firms that have been listed on the GSE over a five-year period (1998-2002). Twenty-two firms qualified to be included in the study sample. Variables used for the analysis include profitability and leverage ratios. Profitability is operationalized using a commonly used accounting-based measure: the ratio of earnings before interest and taxes (EBIT) to equity. The leverage ratios used include:. short-term debt to the total capital;. long-term debt to total capital;. total debt to total capital.Firm size and sales growth are also included as control variables.The panel character of the data allows for the use of panel data methodology. Panel data involves the pooling of observations on a cross-section of units over several time periods and provides results that are simply not detectable in pure cross-sections or pure time-series studies.A general model for panel data that allows the researcher to estimate panel data with great flexibility and formulate the differences in the behavior of the cross-section elements is adopted. The relationship between debt and profitability is thus estimated in the following regression models:ROE i,t =β0 +β1SDA i,t +β2SIZE i,t +β3SG i,t + ëi,t (1)ROE i,t=β0 +β1LDA i,t +β2SIZE i,t +β3SG i,t + ëi,t (2)ROE i,t=β0 +β1DA i,t +β2SIZE i,t +β3SG i,t + ëi,t (3)where:. ROE i,t is EBIT divided by equity for firm i in time t;. SDA i,t is short-term debt divided by the total capital for firm i in time t;. LDA i,t is long-term debt divided by the total capital for firm i in time t;. DA i,t is total debt divided by the total capital for firm i in time t;. SIZEi ,tis the log of sales for firm i in time t;. SGi ,tis sales growth for firm i in time t; and. ëi ,tis the error term.Empirical resultsTable I provides a summary of the descriptive statistics of the dependent and independent variables for the sample of firms. This shows the average indicators of variables computed from the financial statements. The return rate measured by return on equity (ROE) reveals an average of 36.94 percent with median 28.4 percent. This picture suggests a good performance during the period under study. The ROE measures the contribution of net income per cedi (local currency) i nvested by the firms’ stockholders; a measure of the efficiency of the owners’ invested capital. The variable SDA measures the ratio of short-term debt to total capital. The average value of this variable is 0.4876 with median 0.4547. The value 0.4547 indicates that approximately 45 percent of total assets are represented by short-term debts, attesting to the fact that Ghanaian firms largely depend on short-term debt for financing their operations due to the difficulty in accessing long-term credit from financial institutions. Another reason is due to the under-developed nature of the Ghanaian long-term debt market. The ratio of total long-term debt to total assets (LDA) also stands on average at 0.0985. Total debt to total capital ratio(DA) presents a mean of 0.5861. This suggests that about 58 percent of total assets are financed by debt capital.The above position reveals that the companies are financially leveraged with a large percentage of total debt being short-term.Table I.Descriptive statisticsMean SD Minimum Median Maximum ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ROE 0.3694 0.5186 -1.0433 0.2836 3.8300SDA 0.4876 0.2296 0.0934 0.4547 1.1018LDA 0.0985 0.1803 0.0000 0.0186 0.7665DA 0.5861 0.2032 0.2054 0.5571 1.1018SIZE 18.2124 1.6495 14.1875 18.2361 22.0995SG 0.3288 0.3457 20.7500 0.2561 1.3597━━━━━━━━━━━━━━━━━━━━━━━━━━━━━Regression analysis is used to investigate the relationship between capital structure and profitability measured by ROE. Ordinary least squares (OLS) regression results are presented in Table II. The results from the regression models (1), (2), and (3) denote that the independent variables explain the debt ratio determinations of the firms at 68.3, 39.7, and 86.4 percent, respectively. The F-statistics prove the validity of the estimated models. Also, the coefficients are statistically significant in level of confidence of 99 percent.The results in regression (1) reveal a significantly positive relationship between SDA and profitability. This suggests that short-term debt tends to be less expensive, and therefore increasing short-term debt with a relatively low interest rate will lead to an increase in profit levels. The results also show that profitability increases with the control variables (size and sales growth). Regression (2) shows a significantly negative association between LDA and profitability. This implies that an increase in the long-term debt position is associated with a decrease in profitability. This is explained by the fact that long-term debts arerelatively more expensive, and therefore employing high proportions of them could lead to low profitability. The results support earlier findings by Miller (1977), Fama and French (1998), Graham (2000) and Booth et al. (2001). Firm size and sales growth are again positively related to profitability.The results from regression (3) indicate a significantly positive association between DA and profitability. The significantly positive regression coefficient for total debt implies that an increase in the debt position is associated with an increase in profitability: thus, the higher the debt, the higher the profitability. Again, this suggests that profitable firms depend more on debt as their main financing option. This supports the findings of Hadlock and James (2002), Petersen and Rajan (1994) and Roden and Lewellen (1995) that profitable firms use more debt. In the Ghanaian case, a high proportion (85 percent) of debt is represented by short-term debt. The results also show positive relationships between the control variables (firm size and sale growth) and profitability.Table II.Regression model results━━━━━━━━━━━━━━━━━━━━━━━━━━━━━Profitability (EBIT/equity)Ordinary least squares━━━━━━━━━━━━━━━━━━━━━━━━━━━━━Variable 1 2 3SIZE 0.0038 (0.0000) 0.0500 (0.0000) 0.0411 (0.0000)SG 0.1314 (0.0000) 0.1316 (0.0000) 0.1413 (0.0000)SDA 0.8025 (0.0000)LDA -0.3722(0.0000)DA -0.7609(0.0000)R² 0.6825 0.3968 0.8639SE 0.4365 0.4961 0.4735Prob. (F) 0.0000 0.0000 0.0000━━━━━━━━━━━━━━━━━━━━━━━━━━━━ ConclusionsThe capital structure decision is crucial for any business organization. The decision is important because of the need to maximize returns to various organizational constituencies, and also because of the impact such a decision has on an organization’s ability to deal with its competitive environment. This present study evaluated the relationship between capital structure and profitability of listed firms on the GSE during a five-year period (1998-2002). The results revealed significantly positive relation between SDA and ROE, suggesting that profitable firms use more short-term debt to finance their operation. Short-term debt is an important component or source of financing for Ghanaian firms, representing 85 percent of total debt financing. However, the results showed a negative relationship between LDA and ROE. With regard to the relationship between total debt and profitability, the regression results showed a significantly positive association between DA and ROE. This suggests that profitable firms depend more on debt as their main financing option. In the Ghanaian case, a high proportion (85 percent) of the debt is represented in short-term debt.译文加纳上市公司资本结构对盈利能力的实证研究作者:乔舒亚阿博尔论文简介资本结构决策对于任何商业组织都是至关重要的。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

外文翻译--研发费用资本化和盈余管理:以意大利上市公司为例研发费用资本化和盈余管理:以意大利上市公司为例摘要:研发费用的资本化一直以来都是个有争议的会计问题,因为资本。

意大利上市公司,本研究探讨研发费用受到管理动机。

因为意大利准则允许研发资本化意大利提供了利用回归模型表明,倾向于费用资本化IASB,2004)第38号“无形资产”中,讨论了研发费用的会计处理方法。

在第54章标准中规定,没有经过调查的无形资产研究费用是不能被确认为资产的,这类研发支出应在其发生时确认为费用。

至于企业开发阶段的费用,在国际会计准则第38号第57段指出,当且仅当企业可证明以下所有各项时,开发活动(或内部项目开发阶段)产生的无形资产才可予确认:(1)无形资产的成功开发在技术上是可行的;(2)有意完成该无形资产并使用或销售它;(3)有能力使用或销售该无形资产;(4)该无形资产可以产生可能的未来收益;(5)为完成该无形资产的开发,并使用或销售该无形资产,有足够的技术、资金和其他资源的支持;(6)对归集于该无形资产开发阶段的支出,能够可靠的计量。

虽然国际会计准则第38条允许公司将开发费用资本化,但由于研发过程中所固有的主观性,管理者有权决定是否满足国际会计准则第38条的条件。

从本质上讲,国际会计准则第38条赋予管理者在开发费用方面有相当大的灵活性。

美国会计准则对这一问题有严格的规定,在财务会计准则(FASB,1974)第2号“研发费用”中要求所有的研发费用在当期列为支出。

唯一例外的是,会计准则(FASB,1985)在第86号规定,涉及软件开发的费用可以资本化。

在国际上,某些国家的会计准则(例如意大利的)规定,当一些条件得到满足的时候允许灵活使用研发费用资本化。

这些都是与国际会计准则所要求相似的文件。

研发费用资本化一直是个有争议的会计问题。

资本化支持者的报告结果表明,研发是一项长期资产未来盈利能力的重要影响因素(例如,Bublitz和Ettredge,1989;Sougiannias,1994;Ballester等,2003);此外,研发费用金额与企业市场价值之间是正相关的(Hirschey和Weyanandt,1985;Shevlin,1991;Sougiannis,1994)。

而费用化的支持者相对较少。

他们强调研发活动对未来经济利益做出贡献缺乏可靠的证据(例如,FASB,1974;AIMR,1993;Kothari等,2002);或者指出相较于资本化,费用化对信息一致性和可比性的好处。

另外,最保守的费用化处理支持者强调了财务信息可靠性和盈余管理政策的要求,特别是费用化提高了财务报表的客观性,消除了因管理人员进行费用资本化处理而产生的研发资产减值的可能性(Nelson等,2003;Schilit,2002)。

参考其他文献也可以发现,争议围绕何为最有效的研发费用会计处理方法,研究则主要权衡会计信息之间在相关性(即预测能力)和可靠性(即真实性)上的关系(FASB,1980;AICPA,1994;IASB,2004)。

到目前为止,研发费用的实证研究主要集中在相关性的权衡,而甚少提及可靠性方面,这可能使研发费用受到盈余管理的限制。

此外,一些研究也表明,研发支出确实受到盈余管理的限制,即企业为了实现其盈利目标而降低他们的研发投资金额(例如,Perry和Grinaker,1994;Bushee,1998;Mande等,2000)。

而且,缺乏关于允许研发费用资本化灵活使用的会计处理的研究。

测试企业是否通过研发费用会计处理从事盈余管理,可以显著促进全世界对这种费用的最佳处理方法的辩论。

近来提出的这种辩论,在美国财务会计准则和国际会计准则、国际财务报告准则中逐渐显现。

这说明,操纵盈余作为研发费用资本化的动机,将使目前美国公认的会计准则坚持拒绝这类费用资本化的立场。

相反,也显示出企业不使用研发费用的会计处理方法进行盈余管理,将支持现在的国际会计准则、国际财务报告准则的规定,使资本化在一定条件下是允许的。

这项研究有助于为这一论点提供关于费用资本化动机的经验证据。

我们推测,政府决定利用研发支出有两个主要动因:平稳收入和债务契约。

我们测试的假设使用的是在米兰证券交易所上市公司的抽样调查数据。

多种结果表明:该公司利用把研发费用资本化来平稳收入,虽然目前还不支持债务契约假说。

这些结果全面体现了企业内部的各种特征,如企业规模,风险,增长机会,盈利能力,管理特点,产业结构和时间控制。

文章编排如下。

第二部分介绍了意大利的会计与研发核算制度背景。

第三部分讨论以前的文献。

第四部分提出了假说,然后第五部分是研究方法。

第六部分提出结果,第七部分对研究进行了总结。

2 意大利的研发费用会计处理制度意大利会计制度一直允许企业灵活运用研发费用资本化,这与国际会计准则类似。

无形资产的会计处理由会计准则第24号规定,将研发费用区分为如下三种不同类型:1)“基础研究”,其中包括研究,调查和试验,不涉及具体项目。

这种类型的研发费用通常是一个公司的一般效用探索(例如,市场研究,服务更新等);2)“应用研究”,其中包括研究,调查和实验,是指具体项目;3)“发展”,其中包括将研究成果应用到特定的材料、工具、产品和生产工艺上。

基础研究费用应在损益表中扣除。

然而,如果满足以下条件,有关研发费用可以资本化:(a)费用明确为产品或工艺的实现所耗费的;(b)费用是可以识别和衡量的;(c)该项目的费用是应用在技术上的;(d)公司拥有必要的资源来完成和利用该项目;(e)通过开发该项目产生的收益,可以补偿费用的损耗。

很明显,由意大利会计准则规定的开发成本条件与国际会计准则的规定类似。

事实上,意大利标准下“应用研究”中的定义,也符合国际会计准则第38条提供的开发费用的定义。

意大利标准不同于国际会计准则之处在于,当发生上述情况时,公司也可以不使用灵活性来进行研发费用资本化。

但是,这种差异相当正常。

从对一些条件评估的主观性来看,即使在国际会计准则下,当上述条件得到满足时,公司偏好费用化的这种做法也是很明显的。

有关研发费用分摊,意大利的会计准则要求进行摊销的时间为从开始使用最长不超过五年。

意大利法典(第2426条)中collegio sindacale(审计条例)提出研发费用的资本化应被审核而且它不能用于支付股息,直到有足够的盈利来掩盖研发费用资本化的账面价值。

这一规定限制了利用研发费用增加所支付股息的目的。

民商法也要求在“企业管理讨论和分析”部分对研发活动进行讨论。

最后,民商法规定,研发费用的摊销时间表等方面的信息应在财务报表附注中提供。

3 盈余管理与具体的预提费用盈余管理的定义是“对外部财务报告过程有目的的干预,以获得某种私利的意图”(Schipper,1989,第92页)。

在普遍接受的条款中,盈余管理出现在“当管理人员在财务报告中使用判断和修改交易结构来改变财务报告,向某些利益相关者描述虚假的公司经济表现,或依靠会计报表中的数字来影响合同的结果”(Healy,Wahlen,1999,第368页)。

迄今为止大量的研究已经表明,管理人员行使酌情权并且通过各种方式进行盈余管理,从而在权责发生制下进行特别交易(即所谓真实的盈余管理)。

进行盈余管理的主要诱因包括一些债务契约、奖金计划和平稳收入。

债务契约假说认为,管理层进行盈余管理的动机是为了避免违反债务合同的约定,这是在会计数字或比例方面很典型的说法。

奖金计划假说认为,管理层进行盈余管理是为了最大限度的获取收益。

Healy(1985)认为,如果管理层的收入高于或低于奖金计划的范围,他们往往会降低企业收益。

相反,当他们的收入在两者之间,谈们往往会增加企业收入。

最后,收入平滑假说认为,企业追求利润以减少盈余波动。

盈余管理实证研究的发现支持了在各种环境中的上述动机。

许多研究验证了预提费用与盈余管理激励机制之间的关系。

(例如,Healy,1985;DeAngelo,1986;Jones,1991;Dechow等,1995)。

作为替代方法,其他的研究集中于单一的项目,这表明具体的预提费用与系统的盈余管理激励机制有关。

对后者的研究,McNichols和Wilson(1998)认为公司管理其坏账准备是根据奖金计划假说的。

Zucca和Campbell(1992)通过审查可供出售的资产减值现象,表明企业使用这些预提费用是为了加强战略或盈余平稳。

Francis,Hanna和Vincent(1996)认为盈余管理激励机制在解释商誉注销和重组费用中发挥重要作用。

其他的研究集中在递延税款津贴(例如,Miller和Skinner,1998;Vincent和Wong,2003),它们提供了各自不同的结果。

最后,Dowdell和Press(2004)分析了研发支出减值的过程,但他们没有找到证据支持他们的奖励计划假设。

关于盈余管理和具体的预提费用的结论,与上述研究是一致的。

这项研究的目的,是测试当存在灵活性时,研发费用资本化还是费用化是否受盈余管理动机的影响。

4 理论假设以下研究探讨的是盈余管理的三种主要诱因:盈余平稳、债务契约和奖励计划。

在这项研究中,我们侧重于前两个,因为在意大利公司现存数据中,有关奖励计划的信息披露是有限的。

平稳收入假说认为,管理人员的会计自由裁量权,是由他们的欲望驱使减少收入来源导致的(Fudenberg and Tirole,1995)。

平稳收入的过程是把中期到期末之间的收入波动从高峰转入到不太成功的时期,降低了高峰期收益,使收益波动较小(Copeland,1968)。

平稳收入一直被看作是一个积极的策略,它促使管理者向投资者传递内部信息(例如,Gordon,1964;Beidleman,1973;Romen和Sadan,1981;Tucker 和Zarowin,2006)并通过投机目的来推动实践操作(Gordon,1964;Imhoff,1977;Kamin和Ronen,1978)。

在这项研究中,我们不打算对这两种观点中的任何一种进行讨论。

因为,我们测试的目的是研究研发费用资本化是否用于平稳收入。

Capitalization of R&D Costs and Earnings Management:Evidence from Italian isted CompaniesABSTRACT: The capitalization of research and development R&D costs is a controversial accounting issue because of the contention that such capitalization is motivated by incentives to manipulate earnings. Based on a sample of Italian listed companies, this study examines whether companies' decisions to capitalize R&D costs are affected by earnings-management motivations. Italy provides a natural context for testing our hypothesized relationships because Italian GAAP allows for the capitalization of R&D costs. Using a Tobit regression model to test our hypotheses, we show that companies tend to use cost capitalization for earnings-smoothing purposes. The hypothesis that firms capitalize R&D costs to reduce the risk of violating debt covenants is not supported.KEY WORDS: Earnings management, Cost capitalization, R&D accounting, Earnings smoothing, Debt covenants, Italian companies1 IntroductionIn the current era of globalization, a highly relevant issue facing regulators, academics, and practitioners is the determination of an appropriate accounting treatment for research and development R&D costs. International Accounting Standards discuss accounting for R&D costs in IAS No. 38 “Intangible Assets” IASB, 2004;?IASB, 2004 . Paragraph 54 of this standard states that no intangible asset arising fromresearch or from the research phase of an internal project shall be recognized as an asset; and that research expenses shall be expensed in the income statement when they are incurred. Concerning development costs, paragraph 57 states that an intangible asset arising from development or from the development phase of an internal project shall be recognized if, and only if, an entity can demonstrate all of the following: a the technical feasibility of completing the intangible asset so that it will be available for use or sale; b its intention to complete the intangible asset and use or sell it; c its ability to use or sell the intangible asset; d how the intangible asset will generate probable future economic benefits; e the availability of adequate technical, financial, and other resources to complete the development and to use or sell the intangible asset; f its ability to measure reliably the expenditure attributable to the intangible asset during its development. Although IAS 38 allows companies to capitalize development costs, the inherent subjectivity of the validation process permits management to exercise discretion in deciding whether the conditions of IAS 38 have been satisfied. In essence, IAS 38 gives management considerable flexibility regarding the treatment of development costs.US GAAP takes a stricter approach to the issue. SFAS No. 2―Accounting for Research and Development Costs FASB, 1974 ―requires that all R&D expenditures be expensed in the current period. The only exception to thefull expensing rule is stated in SFAS No. 86. The exception relates to the capitalization of software development costs FASB, 1985 . At the international level, certain national accounting standards e.g., those of Italy allow flexibility for the capitalization of R&D costs when some conditions are satisfied. These are conditions similar to those required by IAS.The capitalization of R&D costs has always been a controversial accounting issue. Supporters of capitalization report results suggesting that R&D is a long-lived asset that influences future profitability e.g., Bublitz and Ettredge, 1989, January; Sougiannis, 1994, January; Ballester et al., 2003 . Also, R&D costs are positively related to market value Hirschey and Weygandt, 1985, Spring; Shevlin, 1991, January;?Sougiannis, 1994, January and yield value-relevant information to investors e.g., Aboody and Lev, 1998; Lev and Zarowin, 1999; Healy et al., 2002;?Monahan, 2005 .Supporters of expensing are fewer. They stress the lack of reliable evidence of future economic benefits e.g., FASB, 1974; Association for Investment Management and Research, 1993;?Kothari et al., 2002 or refer to the benefits of consistency and comparability, pointing out that such benefits trump the costs identified by the supporters of capitalization. Additionally, reliability and the risk of earnings-management policies are underscored by supporters of the most conservative accountingtreatment. In particular, expensing is preferable to capitalization because it increases the objectivity of financial statements. That is, it eliminates the opportunity for managers to capitalize costs of projects that have low probabilities of success or to delay impairment of R&D assets Nelson et al., 2003;?Schilit, 2002 .The debate surrounding the most effective accounting method for R&D costs supplements other literature that examines the trade-off between relevance i.e., the predictive ability and reliability i.e., the representative faithfulness of accounting information FASB, 1980; AICPA, 1994; IASB, 2004; IASB, 2004 . Thus far, empirical research on R&D costs has focused mainly on the relevance side of the trade-off, while little has been written about the reliability side that is, the possibility that R&D costs are subject to earnings management.However, a few studies have indeed shown that R&D expenditures are subject to real earnings management. In short, this means that companies cut their R&D investments in order to achieve their earnings goals e.g., Perry and Grinaker, 1994; Bushee, 1998; Mande et al., 2000 . But there is still a paucity of research that explores the motives behind the accounting treatment of R&D costs within a setting where flexibility is allowed. Testing whether companies engage in earnings management through R&D cost accounting can significantly contribute to the debate around the best treatment for such costs. This debate has recently been raised withinthe convergence project by US GAAP and IAS/IFRS. Illustrating that R&D cost capitalization is motivated by incentives to manipulate earnings would support the current U.S. GAAP position, which does not allow the capitalization of such costs. On the contrary, showing that companies do not use R&D cost accounting for earnings-management purposes would support the approach now stated by IAS/IFRS, in which capitalization is allowed under certain conditions.This study contributes to this debate by providing empirical evidence on the motivations for R&D cost capitalization. We hypothesize that the decision to capitalize R&D expenditures is related to two primary motivations: income smoothing and debt contracting. We test our hypotheses using a sample of firms listed on the Milan Stock Exchange. Multivariate results indicate that firms use capitalization of R&D costs to smooth earnings, while there is no support for the debt-covenant hypothesis. These results are robust within a variety of firm characteristics, such as firm size, risk, opportunities for growth, profitability, governance characteristics, industrial membership, and time control.The paper proceeds as follows. Section 2 introduces accounting in Italy and the institutional background relating to R&D accounting. Section 3 discusses the previous literature. Section 4 presents the hypotheses and is followed by the research methods in Section 5. Section6 presents the results and Section7 concludes the study.2 R&D accounting in ItalyItalian accounting regulation has always allowed for some flexibility in the capitalization of R&D costs. This allowance is similar to that of IAS. Accounting for intangibles, including R&D costs, is regulated by Principio Contabilen. 24 Accounting Standard No. 24 . This standard distinguishes three different types of R&D costs as follows:1 “Basic research,” which consists of studi es, surveys, and experiments that do not refer to a specific project; this type of R&D cost is normally carried out for the general utility of a company e.g., market research, updating, etc. ;2 “Applied research,” which consists of studies, surveys, and experiments that refer to specific projects;3 “Development,” which consists of the application of research results to specific materials, tools, products, and processes preceding production.The costs for basic research are to be expensed in the income statement. However, costs related to applied R&D can be capitalized if the following conditions are met: a the costs refer to a project for the realization of a clearly defined product or process; b the costs are identifiable and measurable; c the project to which the costs refer is technically feasible; d the company owns the necessary resources to complete andexploit the project; and e the costs are recoverable through the revenues generated by exploiting the project.It is evident that the conditions stated by the Italian accounting standards are similar to those stated by IAS for development costs. In fact, the definition of applied research under Italian standards also fits into the definition of development costs provided by IAS 38. The Italian standards differ from IAS in that they do not require R&D capitalization when the abovementioned conditions occur, leaving flexibility in the hands of the companies. However, this difference is more formal than substantive. Given the subjectivity in assessing the occurrence of some of the conditions, it seems that, even under IAS, companies that prefer immediate expensing can easily justify this approach―even when the aforementioned conditions are met.Concerning the amortization of R&D costs, the Italian accounting standards require that the amortization be carried out over a period of no longer than five years beginning from the moment the outcome product or process is ready to be used. The Italian Civil Code art. 2426 states that the capitalization of R&D costs shall be authorized by the collegio sindacale statutory auditors and that it is not possible to pay dividends until there are enough retained earnings to cover the carrying amount of the capitalized R&D costs. This stipulation limits the incentive to capitalize R&D costs for the purpose of increasing the amount ofdividends paid. The Civil Code also requires that R&D activities be discussed in the relazione sulla gestione management discussion and analysis section ; however, there is no clear requirement as to what quantitative or qualitative disclosures should be relayed with regard to the capitalization of R&D costs. Finally, the Civil Code states that information regarding the amortization schedules of such R&D costs be provided in the explanatory notes of the financial statements.3 Earnings management and specific accrualsEarnings management is defined as a “purposeful intervention in the external financial-reporting process, with the intent of obtaining some private gain” Schipper, 1989, p. 92 . In generally accepted terms, earnings management occurs “when managers use judgment in financial-reporting and in structuring transactions to alter financial reports to either mislead some stakeholders about the underlying economic performance of the company or to influence contractual outcomes that depend on reported accounting numbers” Healy & Wahlen, 1999, p. 368 .The large amount of research carried out thus far indicates that managers exercise discretion and manage earnings using a wide variety of methods, ranging from carrying out special transactions so-called real earnings management to the manipulation of accruals. Several of the main incentives for earnings management include debt covenants, bonus plans, and income smoothing. The debt-covenant hypothesis suggests that managershave an incentive to manage earnings in order to avoid violating covenants in debt contracts, which are typically stated in terms of accounting numbers or ratios. The bonus-plan hypothesis suggests that managers manage earnings in order to imize compensation. Healy 1985 shows that managers tend to reduce earnings if they fall either above or below bonus-plan bounds. In contrast, they tend to increase earnings when they fall between the two bounds. Finally, the income-smoothing hypothesis suggests that firms aspire to reduce earnings fluctuations.Empirical earnings-management studies find support for the abovementioned motives in a variety of contexts. Many of these studies test the relationship between aggregate accruals and incentives for earnings management e.g., Healy, 1985; DeAngelo, 1986;?Dechowet al., 1995 . As an alternative approach, other studies focus on single items, suggesting that income from specific accruals is related in a systematic way to earnings-management incentives. Among these latter studies, McNichols and Wilson 1988 show that companies manage their bad-debt provisions according to the bonus-plan hypothesis Healy, 1985 . Zucca and Campbell 1992 examine discretionary asset write-downs, showing that companies use thes e accruals either for “big bath” strategies or for earnings smoothing. Francis, Hanna, and Vincent 1996 confirm that earnings-management incentives play a significant role in explaining goodwill write-offs and restructuring charges. Other studies focus onallowances for deferred taxes e.g., Miller and Skinner, 1998; Schrand and Wong, 2003 . These studies provide mixed results. Finally, Dowdell and Press 2004 analyze the in-process R&D write-offs, but they do not find evidence to support their bonus-plan hypothesis.In line with the aforementioned studies on earnings management and specific accruals, this study aims at testing whether the decision to capitalize or to expense R&D costs when flexibility exists is affected by earnings-management motives.4 Hypotheses developmentPrevious research investigates three main incentives for earnings management: earnings smoothing, debt covenant, and bonus-plan incentives. In this study, we focus on the first two since disclosure of data on the existence and structure of bonus plans by Italian companies is limited.The income-smoothing hypothesis suggests that a manager's accounting discretion is driven by his or her desire to reduce income-stream variability Fudenberg and Tirole, 1995 . The process of smoothing serves to moderate year-to-year fluctuations in income by shifting earnings from peak years to less successful periods. This process lowers the peaks and makes earnings fluctuations less volatile Copeland, 1968 .Income smoothing has been viewed both as a positive strategy, whereby managers transmit private information to investors e.g., Gordon, 1964, April; Beidleman, 1973; Ronen and Sadan, 1981; Tucker and Zarowin, 2006 ,and as a manipulative practice driven by opportunistic aims Gordon, 1964, April; Imhoff, 1977, Spring?;Kamin and Ronen, 1978 . In this study, we do not intend to argue for either one of these two views. Rather, we test whether R&D cost capitalization is used for purposes of earnings smoothing.毕业设计。