Chapter 8 & 9 Pronouns 章振邦语法 上外

普通化学 第八章 沉淀溶解平衡

Example 2

实验测得4.6gBa(OH)2可溶于0.250L水中,试求Ba(OH)2 的Ksp⊙。

解:

Ba(OH

)2 溶解度为:s

4.6 171 0.250

0.1076(mol

•

L1 )

K

sp

[

Ba(OH

)2

]

4s3

4

(0.1076)3

4.98 103

2022/9/29

Solubility product of hard-dissolved electrolyte

2s

s

Ksp⊙[Mg(OH)2] = c2 (Ag+)c (CrO2-) = (2s)2 ·s = 4s3

s3

K

sp

4

3 1.121012 4 6.54105 (mol • L1)

2022/9/29

Solubility product of hard-dissolved electrolyte

8

General Chemistry

Chapter 8 Precipitation-dissolution Equilibrium

(4)

Fe(OH)3(s)

平衡浓度/(mol·L-1)

Fe3+(aq) + 3OH-(aq)

s

3s

Ksp⊙[Fe(OH)3] = c(Fe3+)c3(OH-) = s·(3s)3 = 27s4

11

General Chemistry

Example 3

Chapter 8 Precipitation-dissolution Equilibrium

已知298K时,ΔfGm⊙(AgCl)=-109.80kJ·mol-1, ΔfGm⊙(Ag+)= 77.12 kJ·mol-1, ΔfGm⊙(Cl-)= -132.26 kJ·mol-1, 求298K时AgCl的溶度积Ksp⊙。

8-国民经济账户体系

Chapter 8 国民经济账户体系

28

SNA的账户设置

序号 国民经济总体

机构部门 国外(V)

0 货物和服务账户 ——

I

生产账户

货物和服务账户

II

收入分配和使用账户

初始收入和经常 转移账户

III

积累账户

积累账户

IV

资产负债表

资产负债表

Chapter 8 国民经济账户体系

29

I. 生产账户

I.1

生产账户

21.Earn from

67 18.Payoff to

22.borrowing

56 19.lending

total

663 total

credit 499 95 69 663

❖ 以上构成一个小型的国民经济账户体系。

❖ 国民经济账户不仅具备收付式平衡表的一般特点, 还具有下面的优点:表内总计平衡,表外借贷对 应,数据相互验证,便于观察分析。

18

(二)账户中的平衡项

❖ 交易账户的平衡项大多出现在左边; ❖ 资产负债账户,平衡项是净值,出现在账户右边; ❖ 积累账户中的非交易账户,平衡项为净值的变化,

出现在账户右边。

Chapter 8 国民经济账户体系

19

(二)账户中的平衡项

❖ 平衡项在账户形式上的作用 ▪ 使单个账户得以平衡 ▪ 使相邻账户得以连接

16

账户两方的术语

❖对于增加一个部门之经济价值的交易,SNA 采用 来源(resources)这样的术语。例如,工资与薪金 是其接受单位或部门的来源。按照惯例,来源放在 经常账户的右方。

❖ 账户的左方被称为使用(uses),使用是指减少一个 部门之经济价值的交易。仍以工资与薪金为例,对 于支付的单位或部门而言,它们是使用。

Chapter 8 Language in Use语言的使用

• Focal points:

• Speech Act Theory言语行为理论 • The Theory of Conversational Implicature会话含义

• Teaching difficulties:

• Speech Act Theory • The Cooperative Principle and its four maxim

An Introduction To Pragmatics

• Development

• a comparatively new branch of study in the area of linguistics • Developed in the 1960s and 1970s resulted from the expansion of the study of linguistics, especially that of semantics • Morris first proposed the word ―pragmatics‖ in his ―Foundations of the Theory of Signs ‖ : • the study of semiotics includes three parts: • syntax (sign---sign); semantics (sign---word); pragmatics (sign---its user). • 1977 Journal of Pragmatics published in Holland signified the start of pragmatics

• The scope of pragmatic study includes ―speech act theory‖, ―context‖, ―principle of conversation‖ etc.

公司核心第八章习题

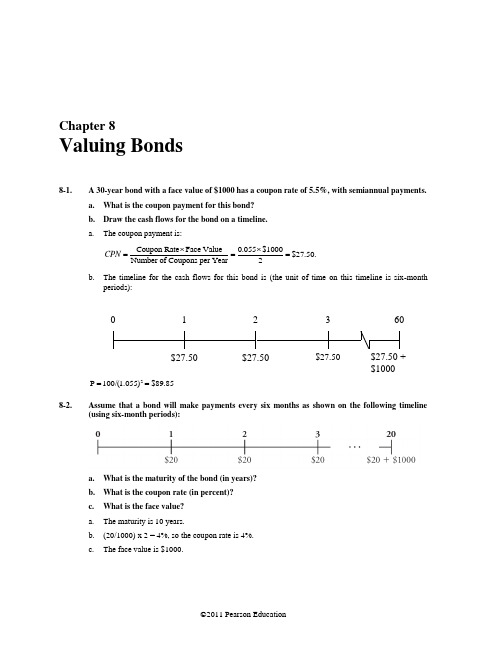

Chapter 8Valuing Bonds8-1.A 30-year bond with a face value of $1000 has a coupon rate of 5.5%, with semiannual payments. a. What is the coupon payment for this bond? b. Draw the cash flows for the bond on a timeline. a. The coupon payment is:Coupon Rate Face Value 0.055$1000$27.50.Number of Coupons per Year 2CPN ⨯⨯===b. The timeline for the cash flows for this bond is (the unit of time on this timeline is six-monthperiods):2P 100/(1.055)$89.85==8-2.Assume that a bond will make payments every six months as shown on the following timeline(using six-month periods):a. What is the maturity of the bond (in years)?b. What is the coupon rate (in percent)?c. What is the face value? a. The maturity is 10 years.b. (20/1000) x 2 = 4%, so the coupon rate is 4%.c. The face value is $1000.1 $27.50 02 $27.503 $27.5060$27.50 +$1000Berk/DeMarzo •Corporate Finance, Second Edition 1078-3.The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value):a. Compute the yield to maturity for each bond.b. Plot the zero-coupon yield curve (for the first five years).c. Is the yield curve upward sloping, downward sloping, or flat?a. Use the following equation.1/nn n FV 1YTM P ⎛⎫+= ⎪⎝⎭1/1111001YTM YTM 4.70%95.51⎛⎫+=⇒= ⎪⎝⎭1/2111001YTM YTM 4.80%91.05⎛⎫+=⇒= ⎪⎝⎭1/3331001YTM YTM 5.00%86.38⎛⎫+=⇒= ⎪⎝⎭1/4441001YTM YTM 5.20%81.65⎛⎫+=⇒= ⎪⎝⎭ 1/5551001YTM YTM 5.50%76.51⎛⎫+=⇒= ⎪⎝⎭b. The yield curve is as shown below.Zero Coupon Yield Curve4.64.855.25.45.60246Maturity (Years)Y i e l d t o M a t u r i t yc. The yield curve is upward sloping.108 Berk/DeMarzo• Corporate Finance, Second Edition8-4. Suppose the current zero-coupon yield curve for risk-free bonds is as follows:a. What is the price per $100 face value of a two-year, zero-coupon, risk-free bond?b. What is the price per $100 face value of a four-year, zero-coupon, risk-free bond?c. What is the risk-free interest rate for a five-year maturity? a.2P 100(1.055)$89.85==b. 4P 100/(1.0595)$79.36==c. 6.05%8-5.In the box in Section 8.1, reported that the three-month Treasury bill sold for a price of $100.002556 per $100 face value. What is the yield to maturity of this bond, expressed as an EAR?410010.01022%100.002556⎛⎫-=- ⎪⎝⎭8-6.Suppose a 10-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading for a price of $1034.74.a. What is the bond’s yield to maturity (expressed as an APR with semiannual compounding)?b. If the bond’s yield to maturity changes to 9% APR, what will the bond’s price be? a.2204040401000$1,034.747.5%(1)(1)(1)222YTM YTM YTM YTM +=+++⇒=+++Using the annuity spreadsheet: NPER Rate PV PMT FVExcel Formula Given: 20 -1,034.74 40 1,000Solve For Rate: 3.75%=RATE(20,40,-1034.74,1000)Therefore, YTM = 3.75% × 2 = 7.50% b.2204040401000$934.96..09.09.09(1)(1)(1)222PV L +=+++=+++ Using the spreadsheetWith a 9% YTM = 4.5% per 6 months, the new price is $934.96NPER Rate PV PMT FV Excel Formula Given: 20 4.50% 40 1,000 Solve For PV: (934.96) =PV(0.045,20,40,1000)Berk/DeMarzo • Corporate Finance, Second Edition 1098-7.Suppose a five-year, $1000 bond with annual coupons has a price of $900 and a yield to maturity of 6%. What is the bond’s coupon rate?25C CC 1000900C $36.26, so the coupon rate is 3.626%.(1.06)(1.06)(1.06)+=+++⇒=+++We can use the annuity spreadsheet to solve for the payment. NPER Rate PV PMT FV Excel Formula Given: 5 6.00% -900.00 1,000Solve For PMT: 36.26 =PMT(0.06,5,-900,1000)Therefore, the coupon rate is 3.626%.8-8.The prices of several bonds with face values of $1000 are summarized in the following table:For each bond, state whether it trades at a discount, at par, or at a premium. Bond A trades at a discount. Bond D trades at par. Bonds B and C trade at a premium.8-9.Explain why the yield of a bond that trades at a discount exceeds the bond’s coupon rate. Bonds trading at a discount generate a return both from receiving the coupons and from receiving a face value that exceeds the price paid for the bond. As a result, the yield to maturity of discount bonds exceeds the coupon rate.8-10.Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield to maturity of 6.75%.a. Is this bond currently trading at a discount, at par, or at a premium? Explain.b. If the yield to maturity of the bond rises to 7% (APR with semiannual compounding), whatprice will the bond trade for? a. Because the yield to maturity is less than the coupon rate, the bond is trading at a premium. b. 2144040401000$1,054.60(1.035)(1.035)(1.035)++++=+++NPER Rate PV PMT FV Excel Formula Given: 14 3.50% 40 1,000Solve For PV:(1,054.60)=PV(0.035,14,40,1000)8-11.Suppose that General Motors Acceptance Corporation issued a bond with 10 years until maturity, a face value of $1000, and a coupon rate of 7% (annual payments). The yield to maturity on this bond when it was issued was 6%. a. What was the price of this bond when it was issued?b. Assuming the yield to maturity remains constant, what is the price of the bond immediatelybefore it makes its first coupon payment? c. Assuming the yield to maturity remains constant, what is the price of the bond immediatelyafter it makes its first coupon payment?110 Berk/DeMarzo • Corporate Finance, Second Editiona. When it was issued, the price of the bond was1070701000P ...$1073.60.(1.06)(1.06)+=++=++b. Before the first coupon payment, the price of the bond is970701000P 70...$1138.02.(1.06)(1.06)+=++=++c. After the first coupon payment, the price of the bond will be970701000P ...$1068.02.(1.06)(1.06)+=+=++8-12.Suppose you purchase a 10-year bond with 6% annual coupons. You hold the bond for fouryears, and sell it immediately after receiving the fourth coupon. If the bond’s yield to maturity was 5% when you purchased and sold the bond,a. What cash flows will you pay and receive from your investment in the bond per $100 facevalue? b. What is the internal rate of return of your investment?a. First, we compute the initial price of the bond by discounting its 10 annual coupons of $6 and finalface value of $100 at the 5% yield to maturity.NPER Rate PV PMT FV Excel Formula Given:10 5.00%6 100Solve For PV:(107.72)= PV(0.05,10,6,100)Thus, the initial price of the bond = $107.72. (Note that the bond trades above par, as its coupon rate exceeds its yield.)Next we compute the price at which the bond is sold, which is the present value of the bonds cash flows when only 6 years remain until maturity.NPER Rate PV PMT FV Excel Formula Given: 6 5.00%6 100Solve For PV:(105.08)= PV(0.05,6,6,100)Therefore, the bond was sold for a price of $105.08. The cash flows from the investment are therefore as shown in the following timeline.Berk/DeMarzo • Corporate Finance, Second Edition 111b. We can compute the IRR of the investment using the annuity spreadsheet. The PV is the purchaseprice, the PMT is the coupon amount, and the FV is the sale price. The length of the investment N = 4 years. We then calculate the IRR of investment = 5%. Because the YTM was the same at the time of purchase and sale, the IRR of the investment matches the YTM. NPER Rate PV PMT FV Excel Formula Given: 4 –107.72 6 105.08Solve For Rate: 5.00% = RATE(4,6,-107.72,105.08)8-13.Consider the following bonds:a. What is the percentage change in the price of each bond if its yield to maturity falls from 6% to 5%?b. Which of the bonds A –D is most sensitive to a 1% drop in interest rates from 6% to 5% andwhy? Which bond is least sensitive? Provide an intuitive explanation for your answer. a. We can compute the price of each bond at each YTM using Eq. 8.5. For example, with a 6% YTM,the price of bond A per $100 face value is15100P(bond A, 6% YTM)$41.73.1.06== The price of bond D is101011100P(bond D, 6% YTM)81$114.72..06 1.06 1.06⎛⎫=⨯-+= ⎪⎝⎭ One can also use the Excel formula to compute the price: –PV(YTM, NPER, PMT, FV). Once we compute the price of each bond for each YTM, we can compute the % price change as Percent change =()()()Price at 5% YTM Price at 6% YTM .Price at 6% YTM -The results are shown in the table below.Coupon Rate Maturity Price at Price at Percentage Change(annual payments)(years)6% YTM 5% YTM A 0%15$41.73$48.1015.3%B 0%10$55.84$61.399.9%C 4%15$80.58$89.6211.2%D8%10$114.72$123.177.4%Bondb. Bond A is most sensitive, because it has the longest maturity and no coupons. Bond D is the leastsensitive. Intuitively, higher coupon rates and a shorter maturity typically lower a bond’s interest rate sensitivity.112 Berk/DeMarzo • Corporate Finance, Second Edition8-14.Suppose you purchase a 30-year, zero-coupon bond with a yield to maturity of 6%. You hold the bond for five years before selling it.a. If the bond’s yield to maturity is 6% when you sell it, what is the internal rate of return ofyour investment? b. If the bond’s yield to maturity is 7% when you sell it, what is the internal rate of return ofyour investment? c. If the bond’s yield to maturity is 5% when you se ll it, what is the internal rate of return ofyour investment? d. Even if a bond has no chance of default, is your investment risk free if you plan to sell itbefore it matures? Explain. a. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0625 = 23.30. Return = (23.30 / 17.41)1/5– 1 = 6.00%. I.e., since YTM is the same at purchase and sale, IRR = YTM. b. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0725 = 18.42. Return = (18.42 / 17.41)1/5– 1 = 1.13%. I.e., since YTM rises, IRR < initial YTM. c. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0525 = 29.53. Return = (29.53 / 17.41)1/5– 1 = 11.15%. I.e., since YTM falls, IRR > initial YTM. d. Even without default, if you sell prior to maturity, you are exposed to the risk that the YTM maychange.8-15.Suppose you purchase a 30-year Treasury bond with a 5% annual coupon, initially trading at par. In 10 years’ time, the bond’s yield to maturity has risen to 7% (EAR).a. If you sell the bond now, what internal rate of return will you have earned on yourinvestment in the bond? b. If instead you hold the bond to maturity, what internal rate of return will you earn on yourinvestment in the bond? c. Is comparing the IRRs in (a) versus (b) a useful way to evaluate the decision to sell the bond?Explain. a. 3.17% b. 5%c. We can’t simply compare IRRs. By not selling the bond for its current price of $78.81, we willearn the current market return of 7% on that amount going forward.8-16.Suppose the current yield on a one-year, zero coupon bond is 3%, while the yield on a five-year, zero coupon bond is 5%. Neither bond has any risk of default. Suppose you plan to invest for one year. You will earn more over the year by investing in the five-year bond as long as its yield does not rise above what level?The return from investing in the 1 year is the yield. The return for investing in the 5 year for initialprice p 0 and selling after one year at price p1 is 101pp -. We have05151,(1.05)1.(1)p p y ==+Berk/DeMarzo • Corporate Finance, Second Edition 113So you break even when41105545/41/41(1)110.031(1.05)(1.05) 1.03(1)(1.05)1 5.51%.(1.03)p y y p y y +-=-===+=-=For Problems 17–22, assume zero-coupon yields on default-free securities are as summarized in the following table:8-17.What is the price today of a two-year, default-free security with a face value of $1000 and an annual coupon rate of 6%? Does this bond trade at a discount, at par, or at a premium?221260601000...$1032.091(1.04)(1)(1)(1.043)N N CPN CPN CPN FV P YTM YTM YTM ++=+++=+=+++++This bond trades at a premium. The coupon of the bond is greater than each of the zero coupon yields, so the coupon will also be greater than the yield to maturity on this bond. Therefore it trades at a premium8-18.What is the price of a five-year, zero-coupon, default-free security with a face value of $1000? The price of the zero-coupon bond is51000$791.03(1)(10.048)NN FV P YTM ===++ 8-19.What is the price of a three-year, default-free security with a face value of $1000 and an annual coupon rate of 4%? What is the yield to maturity for this bond? The price of the bond is223124040401000...$986.58.1(1.04)(1)(1)(1.043)(1.045)N N CPN CPN CPN FV P YTM YTM YTM ++=+++=++=++++++ The yield to maturity is2...1(1)(1)NCPN CPN CPN FVP YTM YTM YTM +=++++++234040401000$986.58 4.488%(1)(1)(1)YTM YTM YTM YTM +=++⇒=+++8-20.What is the maturity of a default-free security with annual coupon payments and a yield to maturity of 4%? Why?The maturity must be one year. If the maturity were longer than one year, there would be an arbitrage opportunity.114 Berk/DeMarzo • Corporate Finance, Second Edition8-21.Consider a four-year, default-free security with annual coupon payments and a face value of $1000 that is issued at par. What is the coupon rate of this bond? Solve the following equation:2344111110001000(1.04)(1.043)(1.045)(1.047)(1.047)$46.76.CPN CPN ⎛⎫=++++ ⎪+++++⎝⎭=Therefore, the par coupon rate is 4.676%.8-22.Consider a five-year, default-free bond with annual coupons of 5% and a face value of $1000. a. Without doing any calculations, determine whether this bond is trading at a premium or at adiscount. Explain. b. What is the yield to maturity on this bond?c. If the yield to maturity on this bond increased to 5.2%, what would the new price be? a. The bond is trading at a premium because its yield to maturity is a weighted average of the yieldsof the zero coupon bonds. This implied that its yield is below 5%, the coupon rate. b. To compute the yield, first compute the price.2122345...1(1)(1)50505050501000$1010.05(1.04)(1.043)(1.045)(1.047)(1.048)NN CPN CPN CPN FVP YTM YTM YTM +=+++++++=++++=+++++The yield to maturity is:2...1(1)(1)505010001010.05... 4.77%.(1)(1)NN CPN CPN CPN FVP YTM YTM YTM YTM YTM YTM +=+++++++=++⇒=++c. If the yield increased to 5.2%, the new price would be:2...1(1)(1)50501000...$991.39.(1.052)(1.052)NNCPN CPN CPN FV P YTM YTM YTM +=+++++++=++=++8-23.Prices of zero-coupon, default-free securities with face values of $1000 are summarized in thefollowing table:Suppose you observe that a three-year, default-free security with an annual coupon rate of 10% and a face value of $1000 has a price today of $1183.50. Is there an arbitrage opportunity? If so, show specifically how you would take advantage of this opportunity. If not, why not?First, figure out if the price of the coupon bond is consistent with the zero coupon yields implied by the other securities.Berk/DeMarzo • Corporate Finance, Second Edition 115111000970.87 3.0%(1)YTM YTM =→=+ 2221000938.95 3.2%(1)YTM YTM =→=+ 3331000904.56 3.4%(1)YTM YTM =→=+According to these zero coupon yields, the price of the coupon bond should be:231001001001000$1186.00.(1.03)(1.032)(1.034)+++=+++ The price of the coupon bond is too low, so there is an arbitrage opportunity. To take advantage of it:Today1 Year2 Years3 Years Buy 10 Coupon Bonds 11835.00 +1000 +1000 +11,000 Short Sell 1 One-Year Zero +970.87 1000Short Sell 1 Two-Year Zero +938.95 1000Short Sell 11 Three-Year Zeros +9950.16 11,000 Net Cash Flow 24.988-24.Assume there are four default-free bonds with the following prices and future cash flows:Do these bonds present an arbitrage opportunity? If so, how would you take advantage of this opportunity? If not, why not?To determine whether these bonds present an arbitrage opportunity, check whether the pricing is internally consistent. Calculate the spot rates implied by Bonds A, B, and D (the zero coupon bonds), and use this to check Bond C. (You may alternatively compute the spot rates from Bonds A, B, and C, and check Bond D, or some other combination.)111000934.587.0%(1)YTM YTM =⇒=+2221000881.66 6.5%(1)YTM YTM =⇒=+3331000839.62 6.0%(1)YTM YTM =⇒=+Given the spot rates implied by Bonds A, B, and D, the price of Bond C should be $1,105.21. Its price really is $1,118.21, so it is overpriced by $13 per bond. Yes, there is an arbitrage opportunity.To take advantage of this opportunity, you want to (short) Sell Bond C (since it is overpriced). To match future cash flows, one strategy is to sell 10 Bond Cs (it is not the only effective strategy; any multiple of this strategy is also arbitrage). This complete strategy is summarized in the table below.Today 1 Year 2Years 3Years Sell Bond C 11,182.10 –1,000 –1,000–11,000Buy Bond A –934.58 1,0000 0 Buy Bond B –881.66 0 1,0000 Buy 11 Bond D –9,235.82 0 0 11,000Net Cash Flow130.04Notice that your arbitrage profit equals 10 times the mispricing on each bond (subject to rounding error).8-25.Suppose you are given the following information about the default-free, coupon-paying yield curve:a. Use arbitrage to determine the yield to maturity of a two-year, zero-coupon bond.b. What is the zero-coupon yield curve for years 1 through 4?a. We can construct a two-year zero coupon bond using the one and two-year coupon bonds asfollows. Cash Flow in Year: 1 2 3 4 Two-year coupon bond ($1000 Face Value) 100 1,100 Less: One-year bond ($100 Face Value) (100) Two-year zero ($1100 Face Value) - 1,100Now, Price(2-year coupon bond) = 21001100$1115.051.03908 1.03908+=Price(1-year bond) =100$98.04.1.02= By the Law of One Price:Price(2 year zero) = Price(2 year coupon bond) – Price(One-year bond)= 1115.05 – 98.04 = $1017.01Given this price per $1100 face value, the YTM for the 2-year zero is (Eq. 8.3)1/21100(2)1 4.000%.1017.01YTM ⎛⎫=-= ⎪⎝⎭b. We already know YTM(1) = 2%, YTM(2) = 4%. We can construct a 3-year zero as follows:Cash Flow in Year:1 2 3 4Three-year coupon bond ($1000 face value) 60 60 1,060 Less: one-year zero ($60 face value) (60) Less: two-year zero ($60 face value) - (60) Three-year zero ($1060 face value) -- 1,060Now, Price(3-year coupon bond) = 2360601060$1004.29.1.0584 1.0584 1.0584++=By the Law of One Price:Price(3-year zero) = Price(3-year coupon bond) – Price(One-year zero) – Price(Two-year zero) = Price(3-year coupon bond) – PV(coupons in years 1 and 2)= 1004.29 – 60 / 1.02 – 60 / 1.042 = $889.99.Solving for the YTM:1/31060(3)1 6.000%.889.99YTM ⎛⎫=-= ⎪⎝⎭Finally, we can do the same for the 4-year zero:Cash Flow in Year:1 2 3 4Four-year coupon bond ($1000 face value) 120 120 120 1,120 Less: one-year zero ($120 face value) (120) Less: two-year zero ($120 face value) — (120) Less: three-year zero ($120 face value) — — (120) Four-year zero ($1120 face value) —— —1,120Now, Price(4-year coupon bond) = 2341201201201120$1216.50.1.05783 1.05783 1.05783 1.05783+++=By the Law of One Price:Price(4-year zero) = Price(4-year coupon bond) – PV(coupons in years 1–3)= 1216.50 – 120 / 1.02 – 120 / 1.042 – 120 / 1.063 = $887.15. Solving for the YTM:1/41120(4)1 6.000%.887.15YTM ⎛⎫=-= ⎪⎝⎭Thus, we have computed the zero coupon yield curve as shown.8-26.Explain why the expected return of a corporate bond does not equal its yield to maturity. The yield to maturity of a corporate bond is based on the promised payments of the bond. But there is some chance the corporation will default and pay less. Thus, the bond’s expected return is typically less than its YTM.Corporate bonds have credit risk, which is the risk that the borrower will default and not pay all specified payments. As a result, investors pay less for bonds with credit risk than they would for an otherwise identical default-free bond. Because the YTM for a bond is calculated using the promised cash flows, the yields of bonds with credit risk will be higher than that of otherwise identical default-free bonds. However, the YTM of a defaultable bond is always higher than the expected return of investing in the bond because it is calculated using the promised cash flows rather than the expected cash flows.8-27.Grummon Corporation has issued zero-coupon corporate bonds with a five-year maturity. Investors believe there is a 20% chance that Grummon will default on these bonds. If Grummon does default, investors expect to receive only 50 cents per dollar they are owed. If investors require a 6% expected return on their investment in these bonds, what will be the price and yield to maturity on these bonds? Price =5100((1)())67.251.06d d r -+=Yield=1/510018.26%67.25⎛⎫-= ⎪⎝⎭8-28.The following table summarizes the yields to maturity on several one-year, zero-couponsecurities:a. What is the price (expressed as a percentage of the face value) of a one-year, zero-couponcorporate bond with a AAA rating? b. What is the credit spread on AAA-rated corporate bonds? c. What is the credit spread on B-rated corporate bonds? d. How does the credit spread change with the bond rating? Why? a. The price of this bond will be10096.899.1.032P ==+b. The credit spread on AAA-rated corporate bonds is 0.032 – 0.031 = 0.1%.c. The credit spread on B-rated corporate bonds is 0.049 – 0.031 = 1.8%.d. The credit spread increases as the bond rating falls, because lower rated bonds are riskier.8-29.Andrew Industries is contemplating issuing a 30-year bond with a coupon rate of 7% (annual coupon payments) and a face value of $1000. Andrew believes it can get a rating of A from Standard and Poor’s. However, due to recent financial difficulties at the company, Standard and Poor’s is warni ng that it may downgrade Andrew Industries bonds to BBB. Yields on A-rated, long-term bonds are currently 6.5%, and yields on BBB-rated bonds are 6.9%. a. What is the price of the bond if Andrew maintains the A rating for the bond issue? b. What will the price of the bond be if it is downgraded? a. When originally issued, the price of the bonds was3070701000...$1065.29.(10.065)(1.065)P +=++=++b. If the bond is downgraded, its price will fall to3070701000...$1012.53.(10.069)(1.069)P +=++=++8-30.HMK Enterprises would like to raise $10 million to invest in capital expenditures. The companyplans to issue five-year bonds with a face value of $1000 and a coupon rate of 6.5% (annual payments). The following table summarizes the yield to maturity for five-year (annualpay) coupon corporate bonds of various ratings:a. Assuming the bonds will be rated AA, what will the price of the bonds be?b. How much total principal amount of these bonds must HMK issue to raise $10 million today,assuming the bonds are AA rated? (Because HMK cannot issue a fraction of a bond, assume that all fractions are rounded to the nearest whole number.) c. What must the rating of the bonds be for them to sell at par?d. Suppose that when the bonds are issued, the price of each bond is $959.54. What is the likelyrating of the bonds? Are they junk bonds?a. The price will be565651000...$1008.36.(1.063)(1.063)P +=++=++b. Each bond will raise $1008.36, so the firm must issue:$10,000,0009917.139918 bonds.$1008.36=⇒This will correspond to a principle amount of 9918$1000$9,918,000.⨯=c. For the bonds to sell at par, the coupon must equal the yield. Since the coupon is 6.5%, the yieldmust also be 6.5%, or A-rated. d. First, compute the yield on these bonds:565651000959.54...7.5%.(1)(1)YTM YTM YTM +=++⇒=++Given a yield of 7.5%, it is likely these bonds are BB rated. Yes, BB-rated bonds are junk bonds.8-31.A BBB-rated corporate bond has a yield to maturity of 8.2%. A U.S. Treasury security has ayield to maturity of 6.5%. These yields are quoted as APRs with semiannual compounding. Both bonds pay semiannual coupons at a rate of 7% and have five years to maturity.a. What is the price (expressed as a percentage of the face value) of the Treasury bond?b. What is the price (expressed as a percentage of the face value) of the BBB-rated corporatebond? c. What is the credit spread on the BBB bonds? a. 103535 1000...$1,021.06 102.1%(1.0325)(1.0325)P +=++==++b.103535 1000...$951.5895.2%(1.041)(1.041)P +=++==++ c. 0. 178-32.The Isabelle Corporation rents prom dresses in its stores across the southern United States. It has just issued a five-year, zero-coupon corporate bond at a price of $74. You have purchased this bond and intend to hold it until maturity. a. What is the yield to maturity of the bond?b. What is the expected return on your investment (expressed as an EAR) if there is no chanceof default? c. What is the expected return (expressed as an EAR) if there is a 100% probability of defaultand you will recover 90% of the face value? d. What is the expected return (expressed as an EAR) if the probability of default is 50%, thelikelihood of default is higher in bad times than good times, and, in the case of default, you will recover 90% of the face value? e. For parts (b –d), what can you say about the five-year, risk-free interest rate in each case? a.1/51001 6.21%74⎛⎫-= ⎪⎝⎭b. In this case, the expected return equals the yield to maturity.c.1/51000.91 3.99%74⨯⎛⎫-= ⎪⎝⎭d. 1/51000.90.51000.51 5.12%74⨯⨯+⨯⎛⎫-= ⎪⎝⎭e. Risk-free rate is 6.21% in b, 3.99% in c, and less than 5.12% in d.AppendixProblems A.1–A.4 refer to the following table:A.1.What is the forward rate for year 2 (the forward rate quoted today for an investment that beginsin one year and matures in two years)? From Eq 8A.2,22221(1) 1.055117.02%(1) 1.04YTM f YTM +=-=-=+A.2.What is the forward rate for year 3 (the forward rate quoted today for an investment that begins in two years and matures in three years)? What can you conclude about forward rates when the yield curve is flat? From Eq 8A.2,3333222(1) 1.05511 5.50%(1) 1.055YTM f YTM +=-=-=+When the yield curve is flat (spot rates are equal), the forward rate is equal to the spot rate.A.3.What is the forward rate for year 5 (the forward rate quoted today for an investment that begins in four years and matures in five years)? From Eq 8A.2,5555444(1) 1.04511 2.52%(1) 1.050YTM f YTM +=-=-=+When the yield curve is flat (spot rates are equal), the forward rate is equal to the spot rate.A.4.Suppose you wanted to lock in an interest rate for an investment that begins in one year and matures in five years. What rate would you obtain if there are no arbitrage opportunities? Call this rate f 1,5. If we invest for one-year at YTM1, and then for the 4 years from year 1 to 5 at rate f 1,5, after five years we would earn 1YTM 11f 1,54with no risk. No arbitrage means this must equal that amount we would earn investing at the current five year spot rate:(1 + YTM 1)(1 + f 1,5)4 + (1 + YTM 5)5.。

红楼梦第八回内容概括200字

红楼梦第八回内容概括200字英文回答:In Chapter 8 of "Dream of the Red Chamber," Jinling is depicted as a bustling metropolis brimming with vibrant markets, exquisite gardens, and opulent teahouses. Jia Baoyu and his entourage embark on an expedition to explore the city's wonders. Along the way, they encounter a groupof young women playing in the street, and Baoyu becomes infatuated with one of them, named Xiangling.While visiting the Grand View Garden, Baoyu and his companions stumble upon a group of nuns, including one named Miaoyu. Her refined and spiritual demeanor fascinates Baoyu, and he develops a deep admiration for her. Meanwhile, the story continues to unfold, offering glimpses into the complex relationships and intrigues within the Jia household.中文回答:红楼梦第八回内容概括:贾宝玉和同伴们游览金陵,见识了繁华的市井、精美的园林、奢华的茶楼等,结识了街边玩耍的少女香菱,宝玉见香菱生得标致,心生爱慕。

Chapter 8 Language and Society

Chapter 8 Language and Society

1. How is language related to society? [1] Language is used to establish and maintain social

relationships. Such as “Good morning!”, “Hi!”, “How’s your family?”, “Nice day today, isn’t it?” [2] the kind of language speakers chooses to use is in part determined by their social background. [3] the structure of lexicon, reflects both the physical and the social environments of a society.

On the one hand, language as an integral part of human being, permeates his thinking and way of viewing the world, language both expresses and embodies cultural reality. On the other, language, as a product of culture, helps perpetuate the culture, and the changes in language uses reflect the cultural changes in return.

自动控制原理第8章

f(x, x) f(x, x) 或 f(x, x) f(x, x)

即 f(x, x)是关于 xx

x

自动控制原理

9

(2)相平面图上的奇点和普通点

相平面上任一点(x, x),只要不同时满足 x 0和 f(x, x) 0 , 则该点的斜率是唯一的,通过该点的相轨迹有且仅有一条, 这样的点称为普通点。

中心点

jω

vortex or center

σ

x

x

中心点

鞍点

jω

x

saddle point

σ

鞍点

x

自动控制原理

21

j λ2 λ1 0

节点 node

j 0

j

0 λ1 λ2

不稳定节点 unstable node

j

0

稳定焦点 stable focus

j

不稳定焦点 unstable focus

j

0

λ1 0 λ2

此系统将具有振荡发散状态。

终将趋于环内平衡点,不会产生自振荡。

自动控制原理

25

例8-3 x 0.5x 2x x2 0

解: x dx 0.5x 2x x2 0 dx

试分析稳定性。

则:

dx dx

0.5x 2x x

x2

0 0

有:

0.5x 2x x2 0

x 0

-2

x

0x

奇点位置:

如果把相变量x视为位移,于是 x 和 x 可以理解为速度和

加速度。在奇点处,由于系统的速度和加速度均为零,因

此奇点就是系统的平衡点equilibrium point 。

自动控制原理

20

系统奇点的分类

服装英语第八章词汇

Chapter 8 Support Materials1.tape 贴边,镶边,牵条2.physical dimension 外形尺寸3.prototype 原型;模型,样板;标样4.prototype cutting 原型裁剪法5.prototype garment 原型服装6.interfacing 内衬,衬布7.interfacing materials 粘衬材料8.interfaced hem 加衬的下摆9.interfaced facing 加衬的挂面10.assembly 组件,装配件11.assembly charts 装配图12.assembly defect 缝制疵病13.assembly details 缝制说明14.assembly drawing装配图15.assembly line 装配线,流水作业装配图16.assembly line sewing process 流水线缝纫加工17.assembly man 装配工18.assembly program 汇编程序《计算机》19.assembly shop (工厂)的组装车间20.grain 布纹,(织物)纹理;(皮革)粗糙面,粒面;谷物色21.grain marking 丝绺标号22.grain side (皮革的)正面,粒面,纹面23.grain straight 织物经向,织物纵向24.hanger appeal 衣架展示25.hanger loop 吊袢26.hanger 衣架,挂钩;(衣领等上的)挂襻,衣袢27.hang dry 悬干,挂干28.returned merchandise rate 退货率《销售》29.returned work 顾客退货《销售》30.return on investment 资金回收,投资收益《管理》31.curled selvedge 卷边,翻边(布疵)32.curl neck 波纹领33.roll collar 翻领34.rolled collar (同turn-down collar)翻领,卷领35.rolled edge handkerchief 滚边手帕36.rolled-edge machine 滚边缝纫机37.rolled hem 卷边下摆38.roll lapel 驳头,卷领39.roll-leg pants 卷裤脚的裤子40.roll line 驳口线,翻折线,折领线41.hand-held 手握式42.hand hemming 手工卷边43.hand-rolled edge 手工滚边44.hand sample 小样45.hand-seam pattern 手缝花样46.full handle 手感丰满47.full-legged trousers 大裤管西裤48.full length skirt 拖地长裙49.full line (同fill silhouette)丰满型,宽松型(轮廓),膨展型(轮廓)50.full lining 全衬里制作,全衬,全夹51.full scale 原尺寸的,足尺寸的;实际尺寸;实物大小52.full shade 饱和色53.partial lining 半夹里,部分夹里54.partial interfacing 局部衬,部分加衬55.partial shipment 分批装船《贸易》56.partial pleats 局部褶饰57.partial-coloured 杂色的58.fashion colour 流行色59.visual effect 视觉效应60.visual arts 视觉艺术;观赏艺术61.visual inspection 目测,肉眼检查62.visual measurement 目测63.visual examination 外观检验,目测检验64.visual sensation 视觉65.visual standard 目测标样66.brand name 商标名称,牌名67.brand-name product 名牌产品68.lightweight fabric 轻质织物,薄型织物,薄料69.light weight lace 轻质花边70.lightweight zipper 细牙拉链71.flexible seam 弹性缝72.bagginess (衣服)局部拱胀73.baggy 宽松下垂的,鼓起的,袋状的74.baggy jeans 宽松牛仔裤75.baggy line 袋状宽大款式76.baggy look 袋形款式77.high count cloth 精细织物,高支纱织物78.free-hanging hem 下摆活络(夹里和面料下摆不缝在一起)79.free-hanging lining下摆活络的夹里80.in-process inspection 半成品检验81.coating 上胶,涂层;涂料;上衣料子82.set-in sleeve 装袖;普通袖,原袖83.set-in pocket 挖袋84.set-in 另外缝上的,装袋的85.needle punched fabric 针刺织物86.needle punching 针刺法87.lead-time 研制周期(设计到投产,或订货到交货)《管理》88.hook 钩扣,钩梭,梭钩89.loop 线环,布环,扣袢,环圈90.enclosed hem edge 滚条下摆,包缝下摆91.enclosed type 封闭式92.top collar 领面93.top covering machine 绷缝机94.top fashion 最新流行款式;最新时装95.top flap 袋盖面96.top fly 门襟,止口97.top fusing collar 硬领,熔衬领98.top fabric 轻薄织物99.top feed 牙脚送布,上送料,上推布100. fused collar 热熔粘合领102. fused hem 粘牵带的底边103. fused interfacing 热熔衬104. fused joint 熔融粘结(非织造布)105. fused seam 压熔缝合106. fusible web 双面粘合衬107. fusing machine粘合熨(压)烫机108. fusing press粘合机,压烫粘合机109. fusion shrinkage 热熔收缩110. sew in 缝合111. sewing action 缝纫动作112. sewing and embroidery scissors 缝纫-绣花剪刀113. sewing inspection 缝制检验114. sewing room 缝纫车间115. sewing station 缝纫工位116. sewing table (缝纫)台板117. shade card 配色样卡118. shade marking 色泽标记119. shade matching 色泽匹配120. shade number 色号121. shade official 公定色泽122. shade range 色谱123. shade sorting 色差分类124. shade standard 色样125. shade ticket 色泽标签126. shade variations 色差127. shade 色泽,色光,色调,色度,明暗程度128. shadow effect 阴阳花纹,阴影效应。

胡壮麟《语言学教程》笔记第8-9章

Chapter 8 Language in Use1. 语义学与语用学的区别1.1 语用学(Pragmatics)Pragmatics is the study of the use of language in communication, particularly the relationships between sentences and the contexts and situations in which they are used.(语用学是研究语言实际运用的学科,集中研究说话人意义、话语意义或语境意义。

)1.2 区别Pragmatics is sometimes contrasted with semantics, which deals with meaning without reference to the users and communicative functions of sentences.(语用学主要研究在特定的语境中说话人所想要表达的意义,语义学研究的句子的字面意义,通常不考虑语境。

)2. 合作原则及其准则(Herbert Paul Grice)2.1. 合作原则(Cooperative Principle)说话人经常在话语中传达着比话语表层更多的信息,听话人也能够明白说话人所要表达的意思。

格莱斯认为一定存在一些管理这些话语产生和理解的机制。

他把这种机制称作合作原则。

2.2. 准则(maxims)数量准则(quantity)①使你的话语如(交谈的当前目的)所要求的那样信息充分。

②不要使你的话语比要求的信息更充分。

质量准则(quality)设法使你的话语真实①不要讲明知是虚假的话②不要说没证据的话关系准则(relation)所谈内容要密切相关方式准则(manner)要清晰。

①避免含糊不清②避免歧义③要简练(避免冗长)④要有序3. 言语行为理论(Speech Act Theory)---John Austin3.1. 施为句&叙事句(Performatives & Constatives)施为句是用来做事的,既不陈述事实,也不描述情况,且不能验证真假;叙事句要么用于陈述,要么用于验证,可以验证真假。

铁道儿童每章概括英文8章

铁道儿童每章概括英文8章铁道儿童是一本经典儿童文学作品,共有8章。

下面是每章的简要概括:Chapter 1: The Railway Children。

The story begins with the introduction of the three children, Bobbie, Peter, and Phyllis, who move to the countryside with their mother after their father is mysteriously taken away. They are fascinated by the nearby railway and the passing trains.Chapter 2: Peter's Coal-Mine。

Peter befriends the station porter and learns about the coal-mine and the dangerous work involved. The children also befriend Perks, the porter, and start helping him with small tasks at the station.Chapter 3: The Old Gentleman。

The children encounter an Old Gentleman on the train who helps them in a time of need. They are grateful for his kindness and later discover his connection to theirfather's situation.Chapter 4: The Engine-Burglar。

The children become involved in a mystery when they suspect a man of stealing coal from the railway. They take it upon themselves to prove his innocence and help him.Chapter 5: The Perks and the Fireman。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

宾格or属格? eg. I don’t mind (you, your) smoking here. I am surprised at (him, his) making that mistake. (1) 只用属格 eg. He doesn’t deny his breaking the agreement. deny, defer, postpone… His leaving home is really surprising.

反身代词

Reflexive Pronoun Please read Page 143- 148 Q1. 反身代词作同位语的位置问题? Q2. 表示行为举止好与坏 Q3. 表示自己处于某种不自觉的状态 Q4. 表示一种“想象的”或“仿佛看到的” 情景 Q5. 表示身体状况 Q6. 反身代词作主语 Q7. anyone / no one but + 反身代词

(1) every-, some-, no-, any-复合词 eg. Everyone thinks (he is, they are) the center of the universe. If anybody calls, tell (him, them) I’m out. Everything is ready, (isn’t it, aren’t they)? Something strange happened, didn’t (it, they)? ● Somebody left (his, their) raincoat on this rack; (he, they) will have to come and get it.

ห้องสมุดไป่ตู้

主格or宾格? eg. She doesn’t believe us. His house is much larger than mine. (1) A: Does any of you know where Tom lives? B: Me. What! Me (to) play him at chess? NO! (2) A: Who is knocking at the door? B: It’s (I, me).

代词及其先行项“数”的一致 eg. My brother and I paid a visit to Beijing last month. (We, They) stayed there for one week. Hawaii is also known for the many beautiful islands (it has, they have). My friend and roommate has agreed to lend me (his car, their cars). Neither the members of the cabinet nor the President will reveal (his, their) plans. Dictatorship(独裁) is the one of many evils which tends to perpetuate (itself, themselves).

(2) 中性名词:chair, desk, car, book, country, cat… eg. I bought a new car. (He, She, It) cost me 20,000 dollar. A: How’s your new car? B: Terrific. (He, She, It) is going like a bomb. Look at that bird. (He, She, It) always comes to my window. I took the cat to the hospital yesterday. (He, She, It) didn’t feel well. China is in East Asia. (He, She, It) is one of the largest countries in the world. I love China. (He, She, It) is the most beautiful place in the world. 国家用阴性

(2) 集体名词 eg. The cast is giving (its, their) best performance tonight. No manager should do for his staff what (he, they) could do for (himself, themselves). (3) 复数名词/代词+each eg. They each had (his, their) problems. They had each (his, their) own problems.

-ing作主语

(2) 只用宾格 eg. SVOC: They caught (him, his) cheating on the exam. Everyone wanted (him, his) to be the leader of the movement.

Ex.

9A on P141 1, 3, 4, 6, 7, 8, 9, 10, 11, 14, 15, 17, 18

Ex.7E 1. on the spot 2. from top to bottom 3. on hand 4. at the front 5. in a fashion 6. taken a fancy to 7. in case of 8. took the fancy of 9. in trouble, lend a hand 10. went by the board 11. within reach of 12. on top of 13. In the case of 14. in the shade 15. at a loss 16. in possession of 17. in the possession of 18. under cover 19. burning the midnight oil 20. at short notice

(3) 比较分句 eg. 他和我一样高。 He is as tall as I (am). He is as tall as me. He is taller than us all / them both. (4) 强调句 eg. He did it. → It was he that did it. → It was him that did it.

(1) 通性名词:baby, student, teacher, person, parent… eg. An instructor should offer __ students challenging projects. → An instructor should offer his students challenging projects. → An instructor should offer his or her students challenging projects. → An instructor should offer challenging projects to the students. → Instructors should offer their students challenging projects.

(5) everybody / nobody + but /except + 人称 代词 eg. 除了他没人能解决我们的问题。 Nobody but he can solve our problems. Nobody can solve our problems but him.

(6) 关系分句: who/whom/whoever/whomever eg. She is a woman (who, whom) may become the president of the company some day. She is a woman (who, whom) I believe may become the president of the company some day. They always elected (whoever, whomever) is popular. I will not trust (whoever, whomever) they will elect.

代词及其先行项“性”的一致

eg. Mother is not quite (himself, herself, itself) today. 阴 性 James plans to open (his, her, its) own office in Fresno. 阳 性 That book has lost (his, her, its) cover. 中 性 If a student needs advice about careers, (he, she, it) should consult the career officers. 通 性

21. University 22. church 23. table 24. the university 25. the hospital 26. Prison 27. The train 28. The hovercraft, the boat 29. Hovercraft 30. a taxi 31. school 32. a bus 33. the ferry 34. a cinema 35. The film 36. the Pope 37. a world 38. Language 39. Experience 40. law

Assignment 1. Finish 8A on P127, 8B on P132, 9A on P141,9B on P149 in your textbook. (下周抽查书本) 2. (登陆-注册-英语语法-作 业、答疑)