税务原理课后答案01

税法原理试题及答案解析

税法原理试题及答案解析一、单项选择题(本题共10小题,每小题2分,共20分。

每小题只有一个正确答案,请将答案填入括号内。

)1. 税法的基本原则不包括()。

A. 税收法定原则B. 税收公平原则C. 税收效率原则D. 税收自由原则答案:D解析:税法的基本原则通常包括税收法定原则、税收公平原则和税收效率原则。

税收法定原则要求税收的征收和使用必须基于法律的规定;税收公平原则强调税收负担的分配应当公平合理;税收效率原则要求税收制度应当促进经济效率,减少对经济活动的扭曲。

税收自由原则并不是税法的基本原则之一。

2. 以下哪项不是增值税的特点?()A. 多环节征税B. 税负转嫁性C. 避免重复征税D. 单一环节征税答案:D解析:增值税是一种多环节征税的税种,其特点包括税负转嫁性,即税负可以通过价格机制转嫁给消费者;避免重复征税,即在商品或服务的每个增值环节只征税一次;单一环节征税并不是增值税的特点,而是增值税力求避免的现象。

3. 个人所得税的征收方式不包括以下哪项?()A. 源泉扣缴B. 自行申报C. 预扣预缴D. 事后追缴答案:D解析:个人所得税的征收方式包括源泉扣缴、自行申报和预扣预缴。

源泉扣缴是指在支付所得时由支付方代扣代缴税款;自行申报是指纳税人自行向税务机关申报并缴纳税款;预扣预缴是指在所得支付前,由支付方预先扣缴税款。

事后追缴并不是个人所得税的征收方式。

4. 企业所得税的税率为()。

A. 15%B. 20%C. 25%D. 30%答案:C解析:根据中国现行税法,企业所得税的一般税率为25%。

对于符合条件的小型微利企业,可能适用更低的税率。

5. 以下哪项不是消费税的征税对象?()A. 烟草B. 高档化妆品C. 粮食D. 高档手表答案:C解析:消费税的征税对象通常包括一些特定的消费品,如烟草、高档化妆品和高档手表等。

粮食一般不属于消费税的征税对象。

6. 土地增值税的计税依据是()。

A. 土地使用权转让收入B. 土地使用权转让成本C. 土地增值额D. 土地面积答案:C解析:土地增值税的计税依据是土地增值额,即土地使用权转让收入减去取得土地使用权所支付的金额、开发土地的成本、费用等。

税法基本原理练习试卷1(题后含答案及解析)

税法基本原理练习试卷1(题后含答案及解析)题型有:1. 单项选择题单项选择题共40题,每题1分。

每题的备选项中,只有l个最符合题意。

1.税收具有强制性、无偿性,固定性的特征,其核心是()。

A.强制性B.固定性C.确定性D.无偿性正确答案:D 涉及知识点:税法基本原理(一)2.税收法律体系的核心是()。

A.征税主体B.税收法律关系的对象C.纳税主体D.税收法律关系的内容正确答案:D 涉及知识点:税法基本原理(一)3.税收法律关系产生的标志是()。

A.征税主体课税行为的发生B.纳税主体应税行为的出现C.国家颁布新税法,而产生新的征纳行为D.税收法律关系的内容发生变化正确答案:B 涉及知识点:税法基本原理(一)4.在收益课税中,税率形式多采用()。

A.定额税率B.平均税率C.边际税率D.累进税率正确答案:D 涉及知识点:税法基本原理(一)5.调节纳税人税收负担的纵向公平问题,税率形式多为()。

A.比例税率B.累进税率C.边际税率D.固定税率正确答案:B 涉及知识点:税法基本原理(一)6.为了解决超额累进税率计算复杂的问题,累进税率表中一般规定有()。

A.平均税率B.速算扣除数C.固定税额D.边际税率正确答案:B 涉及知识点:税法基本原理(一)7.计税基数是相对数时,超倍累进税率实际上是()。

A.超额累进税率B.超率累进税率C.全额累进税率D.边际税率正确答案:B 涉及知识点:税法基本原理(一)8.计税基数是绝对数时,超倍累进税率实际上是()。

A.超额累进税率B.超率累进税率C.全额累进税率D.边际税率正确答案:A 涉及知识点:税法基本原理(一)9.定额税率的一个重要特点是()。

A.与课税对象的数量无关B.不受课税对象价值量变化的影响C.与课税对象数额成正比D.分税目确定便于发挥调节作用正确答案:B 涉及知识点:税法基本原理(一)10.在比例税率条件下,边际税率与平均税率的关系是()。

A.边际税率大于平均税率B.边际税率等于平均税率C.边际税率小于平均税率D.边际税率略高于平均税率正确答案:B 涉及知识点:税法基本原理(一)11.在各种形式的纳税期限中,商品课税通常采用的形式是()。

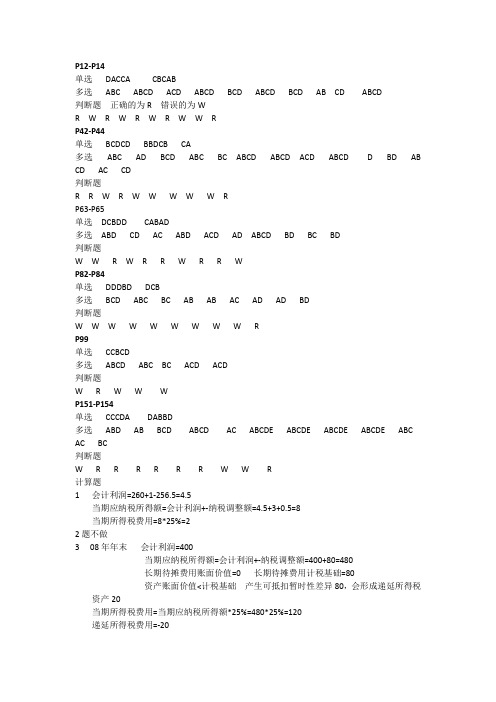

税务会计学(第14版)习题参考答案

税务会计学(第14版)习题参考答案第1章税务会计概念框架技能题一、单项选择题1.A2.C3.D4.B5.D二、多项选择题1.ABC2.ACD3.ABCD4.BCD5.ACD三、判断题1.√2.×3.√4.×第2章纳税基础一、单项选择题1.B2.D3.A4.B5.D二、多项选择题1.ABD2.ABCD3.BD4.ABD5.ABCD三、判断题1.×2.√3.×4.√5.×第三章增值税会计技能题一、单项选择题1.B2.A3.A4.B5.C6.B二、多项选择题1.AC2.ABC3.CD4.ABCD5.CD6.ABD三、判断题1.×2.√3.×4.×5.×6.√四、计算题1. 销项税额=(800×280+500×280)×13%+ 60 000÷(1+13%)×13%=54 222.65(元)进项税额=18 200(元)销售使用过的小汽车应缴纳的增值税额= 100 000÷(1+3%)×2%=1 941.75(元)当月应纳增值税 =54 222.65+1 941.75-18 200=37 964.4(元)2.(1)增值税销项税额=113÷(1+13%)×13%+[3000000+8000÷(1+13%)]×13%+150000×13%+58000÷(1+13%)×13%+34800÷(1+13%)×13%=421 109.46(元)(2)进项税额=3000×9%+100 000×13%+4000×3%+200 000×13%=39 390(元)(3)增值税应纳税额=(421 109.46-39 390)+24360÷(1+3%)×2%=382 192.47(元)3.销项税额=(290+300+110)÷(1+9%)×9%+106÷(1+6%)×6%=57.8+6=63.8(万元)不得抵扣的进项税额=当期无法划分的全部进项税额×(当期简易计税方法计税项目销售额+非增值税应税劳务营业额+免征增值税项目销售额)÷(当期全部销售额+当期全部营业额)=30×(80+60+70)÷(290+300+110+106+80+60+70)=6.2(万元)当月可以抵扣的进项税额=30-6.2=23.8(万元)增值税应纳税额=63.8-23.8=40(万元)4.(1)业务(1)餐饮企业的外卖行为属于餐饮服务。

税务会计课后习题参考答案

递延所得税负债增加189000-144000=45000

借:所得税费用-递延所得税费用45000

贷:递延所得税负债45000

当期应纳税所得额=会计利润+-纳税调整额=5000000-136363.63=4863636.37

当期所得税费用=4863636.37*33%=1605000

借:所得税费用-当期所得税费用1605000

贷:应交税费-应交所得税1605000

2006年会计利润=5000000

管理用设备账面价值=1800000计税基础=1145454.55

产生应纳税暂时性差异654545.45递延所得税负债654545.45*33%=216000

当期所得税费用=320*25%=80

5会计利润=1170000

公益救灾性捐赠限额=1170000*12%=140400需调增3000000-140400=2859600

当期应纳税所得额=会计利润+-纳税调整额=1170000+30000+2859600=4059600

当期所得税费用=4059600*25%=1014900

当期所得税费用=4918181.82*33%=1623000

借:所得税费用-当期所得税费用1623000

贷:应交税费-应交所得税1623000

2007年会计利润=10000000

管理用设备账面价值=1500000计税基础=818181.82

产生应纳税暂时性差异681818.18递延所得税负债681818.18*33%=225000

当期所得税费用=10081818.18*25%=2520454.55

税法基本原理试题及参考答案1.doc

一、单项选择题1. 下列选项中,不属于税法适用原则的是()。

A. 法律优位原则B.新法优于旧法原则C. 实质课税原则D.程序优于实体原则2. 下列选项中,不属于税收法律主义的具体原则的是()oA. 课税要素法定原则B. 课税要素明确原则C. 依法纳税原则D. 依法稽征原则3. 下列有关税法解释中,可以作为办案的直接依据的是()oA. 税法司法解释B. 税法行政解释C. 限制解释C. 扩充解释4. 税种的不同最重要的是取决于()oA. 计税依据B.课税对象C.纳税义务人D.税目5. 下列有关比例税率的表述中,正确的是()oA. 不同征税对象或不同税目,不论数额大小只规定一个比例的税率,税额与课税对象成正比关系B. 同一征税对象或同一税目,不论数量大小只规定一个比例的税率,税额与课税对象成反比关系C. 同一征税对象或同一税目,不论数额大小只规定一个比例的税率,税额与课税对象成正比关系D. 同一征税对象或同一税目,不论数额大小只规定一个比例的税率,税额与课税对象成反比关系6. 减免税的基本形式中,使用范围最为广泛的是()oA. 税基式减免B.税率式减免C.税额式减免D.定额减免7. 税务所和纳税人张某和李某在缴纳税款上发生了争议,必须在缴纳有争议的税款后,税务复议机关才能受理李某的复议申请,这体现了税法适用原则中的()。

A. 新法优于旧法原则B. 特别法优于普通法原则C. 程序优于实体原则D. 实体从旧,程序从新原则8. 以下关于税务规章的制定程序,正确的是()oA. 立项、起草、审查、决定、公布B. 立项、审查、起草、决定、公布C. 立项、起草、审查、决定、公布D. 立项、决定、公布、审查、起草9. 我国税收立法的主要形式是()oA. 税收法律B.税收行政法规C.税务规章D.税务行政规范10. 根据税法的适用原则,下列说法错误的有()。

A. 根据实体从旧,程序从新原则,纳税人在新税法公布实施之前发生的纳税义务在新税法公布实施之后进入税款征收程序的,新实体法在原则上不具有约束力B. 根据法律优位原则,税收法律的效力高于税收行政法规的效力,但税收行政法规的效力与税收行政规章的效力相同C. 凡是特别法中做出规定的,排斥普通法的适用,但这种排斥仅就特别法中的具体规定而言D. 实体从旧、程序从新原则的含义包括两个方面,一是实体税法不具备溯及力;二是程序性税法在特定条件下具备一定的溯及力11. 下列选项中,不属于税收法律主义的具体原则的有()。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Suggested SolutionsChapter 1Questions and Problems for Discussion1. Tax payments differ from government fines and penalties because they are not intended todeter or punish unacceptable behavior. Tax payments differ from fees or user chargesbecause they do not entitle the payer to a specific government good or service, such as a postage stamp or a driver’s license. Tax payments also differ from fees or user charges because they are compulsory.2. This payment has characteristics of a tax, a penalty, and a user fee. The compulsorypayment is not specifically punitive but does apply selectively to those companies most likely responsible for the polluted condition of Green River. However, these samecompanies may be the entities that benefit most from the environmental clean-up.3. This payment more closely resembles a fee for a government service than a transaction-based tax because the transaction occurs between a private party and the jurisdiction itself, rather than between private parties engaging in a market transaction. The payment also entitles the payer to a specific benefit (the right to marry under law).4. To the extent that the decline in exterior maintenance reduces the value of Mr. P’sapartment complex, he bears the incidence of the increased property tax. To the extent that the decline reduces the value of adjoining properties or makes the neighborhood lessattractive, the owners of the adjoining properties and the neighborhood residents share the incidence of the tax increase.5. People who do not directly use public schools (such as Mr. and Mrs. K or people who donot have children) indirectly benefit from a public education system for the generalpopulation. Arguably, public education contributes to a skilled workforce and improves the cultural and social environment in which Mr. and Mrs. K live. Based on this argument, Mr.and Mrs. K should not be exempt from the local property tax.6. The consumers who pay the same price for a smaller bar of soap of lesser quality bear theincidence of the new gross receipts tax.7. Real property cannot be hidden or moved, and its ownership (legal title) is a matter ofpublic record. In contrast, personal property is mobile and may be easily concealed.Moreover, jurisdictions may not have an effective means to discover or trace ownership of personal property.8. Arguably, private golf courses beautify the locality and are environmentally more desirablethan other commercial activities. They also may require more acreage than other businesses and, therefore, would be at a competitive disadvantage without a preferential real property tax rate.9. Many jurisdictions that levy property taxes provide an exemption for public institutions,such as state universities or private colleges. If University K is entitled to such anexemption, every commercial building or residence acquired by the University reduces the local jurisdiction’s property tax base.10. Excise taxes are imposed on a much narrower range of consumer goods and services thansales taxes. Consequently, people can more readily avoid purchasing the specific good or service subject to excise tax.11. The Internal Revenue Code is federal statutory law, enacted by Congress and signed by thePresident. Technically, Treasury regulations only interpret and explain the statute and are not laws in their own right. Thus, regulations are less authoritative than the Code itself.However, because Congress authorized the Treasury to write regulations, they are thegovernment’s official interpretation of statutory law. Practically, the regulations carryconsiderable authoritative weight.12. The tax increase may have reduced the aggregate demand for consumer goods and,consequently, municipal residents are buying fewer goods. A second possibility is thatmunicipal residents are traveling to other jurisdictions with lower tax rates or making more purchases through mail order catalogs or on-line.13. From a political perspective, liquor and cigarettes sales make an excellent tax base becauseconsumption of the two products is purely discretionary, and any decline in consumption because of the tax is socially desirable. From an economic perspective, these sales are agood tax base because the demand for liquor and cigarettes is relatively price inelastic. In other words, people who drink and smoke on a regular basis buy these products regardless of a heavy excise tax.14. The federal income has the broader base. The federal payroll tax is imposed on wages,salaries, and other forms of compensation earned by employees. The federal income tax is imposed on all types of compensation as well as net business profit, investment income, and any other income item from whatever source derived.15. A property tax is a periodic (usually annual) tax levied on the ownership of property andbased on the value of the property on a particular assessment date. A transfer tax is atransaction-based tax levied on the transfer of property from one party to another. Atransfer tax is based on the value of the property at date of transfer.16. If the federal government could “piggy back” a national sales tax on existing state salestax collection systems, the federal government could avoid creating a new federal agency for collecting the tax. In contrast, the federal government would have to create a new collection system for a national VAT. However, a national VAT would be less likely to causejurisdictional conflict between the federal government and the states because states do not depend on VATs as a source of revenue.Application Problems1. a. The statement of facts identifies three taxpayers: Mr. JK, JK Services, and JK Realty.b. The government of the locality in which Mr. JK resides, the state government ofVermont, and the U.S. government have jurisdiction to tax Mr. JK. The localgovernments of the four counties in which JK Services conducts business, the stategovernment of Vermont, and the U.S. government have jurisdiction to tax JK Services.The city of Boston, the state government of Massachusetts, and the U.S. governmenthave jurisdiction to tax JK Realty.2. a. The United States has jurisdiction to tax Mrs. CM because she is a permanent resident.b. The United States has jurisdiction to tax Mrs. CM only on the U.S. source incomegenerated by the Manhattan real estate.c. The United States does not have jurisdiction to tax Mrs. CM.d. The United States has jurisdiction to tax Mrs. CM because she is a citizen.3. a. The tax is $8,300 ($415,000 × 2%).b. The tax is $19,000 ([$500,000 × 2%] + [$225,000 × 4%]).4. Increase in County G’s aggregate assessed property tax value $23,000,000Assessed value of Company LI’s new facility (20,000,000) Net increase in County G’s tax base $3,000,000 Tax rate .04 Net effect on County G’s current year revenue $120,000 5. Jurisdiction A:Volume of sales before rate increase $800,000,000Original tax rate .05Revenue before rate increase $40,000,000Volume of sales after rate increase $710,000,000New tax rate .06Revenue after rate increase $42,600,000Additional revenue ($42,600,000 $40,000,000) $2,600,000Jurisdiction Z:Volume of sales added to tax base $50,000,000Tax rate .05Additional revenue $2,500,0006. a. Value of property purchased in Jurisdiction K $600,000Use tax rate in Jurisdiction H .06Pre credit use tax $36,000Sales tax paid to Jurisdiction K (18,000)Use tax owed to Jurisdiction H $18,000b. Value of property purchased in Jurisdiction L $750,000Use tax rate in Jurisdiction H .06Pre credit use tax $45,000Sales tax paid to Jurisdiction L (48,750)Use tax owed to Jurisdiction H -0-7. a. Mrs. DK owes $658 Pennsylvania use tax ($9,400 × 7%).b. Mrs. DK owes no Pennsylvania use tax because her $823 New York sales tax ($9,400× 8.75%) exceeds $658.c. Mrs. DK owes $188 Pennsylvania use tax ($658 – $470 credit for Virginia sales tax[$9,400 × 5%]).8. a. State R residents who purchase property out-of-state (i.e., through the mail) but use andconsume the property in State R owe the 6 percent use tax.b. The fact that Firm L must collect the State R use tax does not affect the legal liability ofState R residents to pay the tax. However, very few people actually pay a self-assesseduse tax. Thus, State R might collect as much as $1,080,000 additional revenue (6 percent of $18 million sales to State R customers) if Firm L was required to collect use tax atpoint of sale and remit the tax to State R.9. a. Mr. and Mrs. CS are not required to pay sales tax on the purchase of inventory goodsbecause they are not the final consumers of the goods. The hardware store’s retailcustomers must pay the sales tax when they purchase goods. Mr. and Mrs. CS arerequired to collect this tax at point of sale.b. Mr. and Mrs. CS should time their purchases to minimize their inventory on hand as ofDecember 31 of each year, thereby minimizing the book value on which the personalproperty tax is based.10. Firm Q:Sales revenue ($9 ⨯ 12.4 million units) $111,600,000Cost of sales ($6 ⨯ 12.4 million units) (74,400,000)Value added by Firm Q $37,200,000Tax rate .03VAT $1,116,000Firm R:Sales revenue ($10 ⨯ 12.4 million units) $124,000,000Cost of sales ($9 ⨯ 12.4 million units) (111,600,000)Value added by Firm R $12,400,000Tax rate .03VAT $372,000Issue Recognition Problems1. Are Mr. and Mrs. J required to pay the property tax for a full year even though they lived inthe home for only three months of the year? Is there any mechanism for allocating theproperty tax attributable to the period January 1 through October 5 to the former owners?2. Do the fences and lighting represent permanent improvements to real property (corporateheadquarters) so that their value adds to the real property tax base, or can they qualify as personalty that is exempt from real property tax?3. How does each jurisdiction in which the plane is temporarily stored define or identifybusiness tangibles subject to tax? Is jurisdiction based on a minimum number of days of physical presence in the state? Is the annual personal property tax pro rated to reflect the number of days that property is used or stored in the state?4. Does State A have jurisdiction to tax the retirement income that Mrs. O earned while shewas a resident of State A but that she receives while she is a resident of State K?5. Did the sale of the furniture from Vendor V to Business Q occur in State V or in State Q?Does State V have jurisdiction to tax the transaction even though the office furniture was shipped out of state?6. Do Acme Corporation’s activities in States X, Y, and Z give all three states jurisdiction totax Acme’s business income? How much of Acme’s net profit can be taxed by each state with jurisdiction?7. Which of the 14 states has jurisdiction to tax Mr. W’s professional income? How much ofthis total prize money is subject to each state’s personal income tax?8. Does the abatement agreement require BBB Company to repay any of the foregoneproperty taxes or incur any penalty if it terminates its business activity in County K before the end of the abatement period?9. Does the fact that Dempsey Corporation sells goods to U.S. customers give the UnitedStates jurisdiction to tax the Canadian corporation? Is the income generated by Dempsey’s sales to U.S. customers considered U.S. source income subject to federal income tax? 10. When Mr. KW dies, can the United States government claim jurisdiction to impose thefederal estate tax on his net worth? Can an individual who has been a U.S. citizen escape federal taxation by renouncing his citizenship and moving to a foreign country? Research ProblemsThe first three research problems for Chapter 1 are designed to encourage students toexplore internet websites that contain a wealth of information on local, state, and federal taxes. Problem 4 is an exercise to increase students’ awareness of their state’s sales tax and the items on which the tax is imposed.Tax Planning Cases1. WP’s management must compare the tax costs of operating in each jurisdiction.Value of tangible business property $10,000,000Jurisdiction F’s property tax rate .04$400,000Annual gross receipts $2,000,000Jurisdiction F’s gross receipts tax rate .15$300,000Tax cost of operating in Jurisdiction F$700,000Annual gross receipts $2,000,000Jurisdiction G’s gross receipts tax rate .30Tax cost of operating in Jurisdiction G$600,000Based solely on the comparative tax costs, WP should locate its new branch in JurisdictionG.2. Before the tax increase, KTR’s taxable income was $200 million ($10 profit per unit 20million units), its income tax cost was $40 million, and its after-tax profit was $160 million. If KTR’s taxable income does not change, the rate increase from 20 percent to 22 percent would increase the income tax cost to $44 million and decrease after-tax profit to $156million. If KTR increases its profit per unit to $10.20, but sells only 19 million units, itstaxable income will decrease to $193.8 million. Its tax on this income will be $42.636 million, and its after-tax profit will be $151.164 million. Thus, KTR’s owners will maximize after-tax profit if they do not raise the price of their product.。