公司理财课程课程讲解第9章

《公司理财》罗斯笔记

错误!未定义书签。

错误!未定义书签。

错误!未定义书签。

第一篇 综述企业经营活动中三类不同的重要问题:1、资本预算问题(长期投资项目)2、融资:如何筹集资金?3、短期融资和净营运资本管理第一章 公司理财导论1.1什么是公司理财?1。

1。

1资产负债表 ()++=+流动资产固定资产有形无形流动负债长期负债+所有者权益=流动资产-流动负债净营运资本短期负债:那些必须在一年之内必须偿还的代款和债务; 长期负债:不必再一年之内偿还的贷款和债务。

资本结构:公司短期债务、长期债务和股东权益的比例。

1。

1。

2资本结构 债权人和股东V (公司的价值)=B (负债的价值)+S (所有者权益的价值)如何确定资本结构将影响公司的价值。

1.1。

3财务经理财务经理的大部分工作在于通过资本预算、融资和资产流动性管理为公司创造价值。

两个问题:1. 现金流量的确认:财务分析的大量工作就是从会计报表中获得现金流量的信息 (注意会计角度与财务角度的区别)2. 现金流量的时点3. 现金流量的风险1.2公司证券对公司价值的或有索取权负债的基本特征是借债的公司承诺在某一确定的时间支付给债权人一笔固定的金额。

债券和股票时伴随或依附于公司总价值的收益索取权。

1.3公司制企业 1。

3.1个体业主制1。

3。

2合伙制1。

3.3公司制有限责任、产权易于转让和永续经营是其主要优点.1。

4公司制企业的目标1.4。

1代理成本和系列契约理论的观点代理成本:股东的监督成本和实施控制的成本1.4.2管理者的目标管理者的目标可能不同于股东的目标。

Donaldson提出的管理者的两大动机:①(组织的)生存;②独立性和自我满足.1。

4.3所有权和控制权的分离—-谁在经营企业?1.4。

4股东应控制管理者行为吗?促使股东可以控制管理者的因素:①股东通过股东大会选举董事;②报酬计划和业绩激励计划;③被接管的危险;④经理市场的激烈竞争.有效的证据和理论均证明股东可以控制公司并追求股东价值最大化。

Chapter 9公司理财共8页word资料

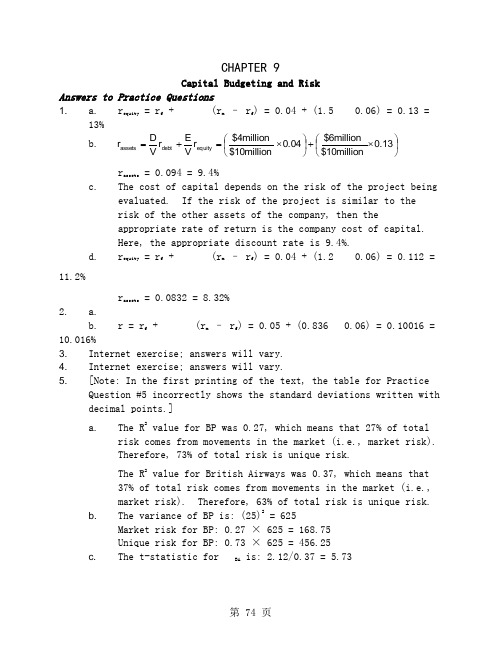

CHAPTER 9Capital Budgeting and RiskAnswers to Practice Questions1.a. r equity = r f +(r m – r f ) = 0.04 + (1.5 0.06) = 0.13 =13% b. ⎪⎭⎫ ⎝⎛⨯+⎪⎭⎫ ⎝⎛⨯=+=0.13$10million $6million 0.04$10million $4million r V E r V D r equity debt assetsr assets = 0.094 = 9.4%c.The cost of capital depends on the risk of the project being evaluated. If the risk of the project is similar to the risk of the other assets of the company, then theappropriate rate of return is the company cost of capital. Here, the appropriate discount rate is 9.4%.d.r equity = r f + (r m – r f ) = 0.04 + (1.2 0.06) = 0.112 =11.2%r assets = 0.0832 = 8.32% 2. a. b. r = r f + (r m – r f ) = 0.05 + (0.836 0.06) = 0.10016 = 10.016% 3. Internet exercise; answers will vary. 4. Internet exercise; answers will vary. 5. [Note: In the first printing of the text, the table for PracticeQuestion #5 incorrectly shows the standard deviations written with decimal points.]a. The R 2 value for BP was 0.27, which means that 27% of totalrisk comes from movements in the market (i.e., market risk). Therefore, 73% of total risk is unique risk.The R 2 value for British Airways was 0.37, which means that 37% of total risk comes from movements in the market (i.e., market risk). Therefore, 63% of total risk is unique risk. b.The variance of BP is: (25)2 = 625Market risk for BP: 0.27 × 625 = 168.75Unique risk for BP: 0.73 × 625 = 456.25c.The t-statistic for BA is: 2.12/0.37 = 5.73This is significant at the 1% level, so that the confidence level is 99%.d.r BA = r f +BA(r m – r f ) = 0.05 + [2.12 (0.12 – 0.05)]= 0.1984 = 19.84%e. r BA = r f + BA (r m – r f ) = 0.05 + [2.12 (0 – 0.05)] =–0.0560 = –5.60% 6. Internet exercise; answers will vary. 7.The total market value of outstanding debt is £100 million. Thecost of debt capital is 7.5 percent. For the common stock, the outstanding market value is:£40 2 million = £80 million. The cost of equity capital is11 percent. Thus, Lorelei’s weighted -average cost of capital is: r assets = 0.0906 = 9.06%8.a.r BN = r f + BN (r m – r f ) = 0.035 + (0.53 0.08) = 0.0774= 7.74%r IND = r f + IND (r m – r f ) = 0.035 + (0.49 0.08) = 0.0742 = 7.42%b.No, we can not be confident that Burlington’s true beta is not the industry average. The difference between BN and IND (0.04) is less than one standard error (0.20), so we cannot reject the hypothesis that BN = IND .c.Burlington’s beta might be different from the industry beta for a variety of reasons. For example, Burlington’s business might be more cyclical than is the case for the typical firm in the industry. Or Burlington might have more fixed operating costs, so that operating leverage is higher. Another possibility is that Burlington has more debt than is typical for the industry so that it has higher financial leverage.9. a.The threat of a coup d’état means that the expected cash flow is less than $NZ900 million. The threat could alsoincrease the discount rate, but only if it increases market risk.b.If New Zealand Marine proceeds with the construction of the supply submarine and the Republic then fails to make the final $NZ900 million payment, then New Zealand Marine can sell the submarine to another buyer for $NZ600 million. Therefore, the expected cash flow for the year 2 payment is: (0.20 $NZ600 million) + (0.80 $NZ900 million) = $NZ840 millionAssum e that New Zealand Marine’s co sts are incurred equally in Year 0, Year 1 and Year 2, and that the cash flows areabout as risky as the rest of the company’s business . Then:PV = – 400 + 500 + (– 400/1.10) + (– 400 +840)/1.102 = +100or $NZ100 million10.a.If you agree to the fixed price contract, operating leverage increases. Changes in revenue result in greater thanproportionate changes in profit. If all costs are variable, then changes in revenue result in proportionate changes in profit. Business risk, measured by assets , also increases as a result of the fixed price contract. If fixed costs equal zero, then: assets = revenue . However, as PV(fixed cost) increases, assets increases.b. With the fixed price contract:PV(assets) = PV(revenue) – PV(fixed cost) – PV(variable cost)9(1.09)(0.09)$10million)6%,10years factor annuity $10million 0.09$20million PV(assets)⨯-⨯-=( PV(assets) = $97,462,710Without the fixed price contract:PV(assets) = PV(revenue) – PV(variable cost)0.09$10million0.09$20million PV(assets)-== $111,111,111 11.a. Expected daily production =(0.20) + 0.8[(0.4 x 1,000) + (0.6 x 5,000)] =2,720 barrelsExpected annual cash revenues = 2,720 x 365 x $15 =$14,892,000b. The possibility of a dry hole is a diversifiable risk andshould not affect the discount rate. This possibilityshould affect forecasted cash flows, however. See Part (a). Ratio of ’s Correlatio nBetaBrazil 6.29 0.5 3.15 Egypt 5.67 0.5 2.84 India 6.10 0.5 3.05 Indonesia 7.29 0.5 3.65 Mexico 3.92 0.5 1.96 Poland 3.21 0.5 1.61 Thailand 6.32 0.5 3.16 South Africa4.04 0.5 2.02The betas increase compared to those reported in Table 9.2 because the returns for these markets are now more highly correlated with the U.S. market. Thus, the contribution to overall market risk becomes greater.12.The information could be helpful to a U.S. company considering international capital investment projects. By examining the beta estimates, such companies can evaluate the contribution to risk of the potential cash flows.A German company would not find this information useful. The relevant risk depends on the beta of the country relative to the portfolio held by investors. German investors do not invest exclusively, or even primarily, in U.S. company stocks. They invest the major portion of their portfolios in German company stocks.13. The opportunity cost of capital is given by:r = r f +(r m – r f ) = 0.05 + (1.20.06) = 0.122 = 12.2%Therefore:CEQ 1 = 150(1.05/1.122) = 140.37CEQ 2 = 150(1.05/1.122)2 = 131.37CEQ 3 = 150(1.05/1.122)3 = 122.94CEQ 4 = 150(1.05/1.122)4 = 115.05CEQ 5 = 150(1.05/1.122)5 = 107.67a 1 = 140.37/150 = 0.9358a 2 = 131.37/150 = 0.8758a 3 = 122.94/150 = 0.8196a 4 = 115.05/150 = 0.7670a 5 = 107.67/150 =0.7178From this, we can see that the a t values decline by a constant proportion each year:a 2/a 1 = 0.8758/0.9358 =0.9358a 3/a 2 = 0.8196/0.8758 = 0.9358a 4/a 3 = 0.7670/0.8196 = 0.9358a 5/a 4 = 0.7178/0.7670 =0.935814. a. Using the Security Market Line, we find the cost of capital:r = 0.07 + [1.5 (0.16 – 0.07)] = 0.205 = 20.5%Therefore:b.=40(1.07/1.20535.52CEQ1) ==60(1.07/1.205CEQ47.312)2 ==50(1.07/1.205CEQ35.013)3 =c.0.8880=35.52/40a1=0.7885=47.31/60a2==35.01/50a0.70023=d. Using a constant risk-adjusted discount rate is equivalentdecreases at a constant compounded rate.to assuming that at15. At t = 2, there are two possible values for the project’s NPV:Therefore, at t = 0:Challenge Questions1.It is correct that, for a high beta project, you should discount all cash flows at a high rate. Thus, the higher the risk of the cash outflows, the less you should worry about them because, the higher the discount rate, the closer the present value of these cash flows is to zero. This result does make sense. It is better to have a series of payments that are high when the market is booming and low when it is slumping (i.e., a high beta) than the reverse.The beta of an investment is independent of the sign of the cash flows. If an investment has a high beta for anyone paying out the cash flows, it must have a high beta for anyone receiving them. If the sign of the cash flows affected the discount rate, each asset would have one value for the buyer and one for the seller, which is clearly an impossible situation.2.a. Since the risk of a dry hole is unlikely to be market-related, we can use the same discount rate as for producing wells. Thus, using the Security Market Line:r nominal = 0.06 + (0.9 0.08) = 0.132 = 13.2%We know that:(1 + r nominal ) = (1 + r real )(1 + r inflation )Therefore:b.c.Expected income from Well 1: [(0.20) + (0.8 3million)] = $2.4 millionExpected income from Well 2: [(0.20) + (0.82million)] = $1.6 millionDiscounting at 8.85 percent gives:d.For Well 1, one can certainly find a discount rate (and hence a “fudge factor”) that, when applied to cash flows of $3 million per year for 10 years, will yield the correct NPV of $5,504,600. Similarly, for Well 2, one can find the appropriate discount rate. However, these two “fudge(3.1914)](3million)million 101.28853millionmillion 10NPV 101tt1⨯+-=+-=∑=[factors” will be different. Specifically, Well 2 will havea smaller “fudge factor” bec ause its cash flows are moredistant. With more distant cash flows, a smaller additionto the discount rate has a larger impact on present value.3. Internet exercise; answers will vary.4. 希望以上资料对你有所帮助,附励志名言3条:5. 1、上帝说:你要什么便取什么,但是要付出相当的代价。

《公司理财》罗斯笔记(已矫正)

1、第一篇中的两个现金流量表,共同比报表。

2、第二篇中的几个计算、增长机会、股利增长模型。

包尔得文那个例子重点看,做投资决策一般都是那个例子改的。

实物期权。

如果你到了复试,而刚好遇到一个想问这方面的老师,他们有可能让你评价这一篇的财务指标,无疑罗斯写的一切都不如现金流折现。

但是如果现金流就无敌了,那么其他指标有什么存在意义吗?这些要有一点自己的思考。

3、第三第四篇不多说,全是重点。

一点一点整理,课后题一道一道看。

论坛上有中英文的答案,不过那个中文答案有不少计算错的,别全信。

他的思路一般是对的。

有题不会的话再发上来帖子问。

4、第五篇大多是概念,有税情况下租赁的NPV是重点。

5、第六篇中期权定价公式、权证、可转化债券估价、还有衍生品的应用方式。

这里的除了概念之外,就是你要知道这些东西是干嘛的,还有使用了会带来那些结果。

6、第七篇我们没讲过,第八篇我自己看的,也没讲,不好说什么是重点。

本书的重点在第三四篇,那是全文都得细细看的。

另外名词都是随机的,说不好哪些是重点第一篇综述企业经营活动中三类不同的重要问题:1、资本预算问题(长期投资项目)2、融资:如何筹集资金?3、短期融资和净营运资本管理第一章公司理财导论1.1什么是公司理财?资产负债表()++=+流动资产固定资产有形无形流动负债长期负债+所有者权益流动资产-流动负债净营运资本=短期负债:那些必须在一年之内必须偿还的代款和债务;长期负债:不必再一年之内偿还的贷款和债务。

资本结构:公司短期债务、长期债务和股东权益的比例。

资本结构债权人和股东V(公司的价值)=B(负债的价值)+S(所有者权益的价值)如何确定资本结构将影响公司的价值。

财务经理财务经理的大部分工作在于通过资本预算、融资和资产流动性管理为公司创造价值。

两个问题:1.现金流量的确认:财务分析的大量工作就是从会计报表中获得现金流量的信息(注意会计角度与财务角度的区别)2.现金流量的时点3.现金流量的风险1.2公司证券对公司价值的或有索取权负债的基本特征是借债的公司承诺在某一确定的时间支付给债权人一笔固定的金额。

【精品】罗斯《公司理财》中文版第九版课件

2.1资金时间价值观念

资金时间价值计算中的几个特殊问题

不等额系列款项现值的计算:为求得不等额的系列付 款的现值之和,可以先计算每次付款的复利现值, 然后加总。

年金与不等额的系列付款混合情况下的现值:如果在 一组不等额的系列款项中,有部分是连续发生的 等额付款,则可分段计算其年金现值及复利现值, 然后加总。

公司理财学

第一章 公司理财的基本问题

本章内容

1.1 企业组织与企业目标 1.2 公司理财目标与价值理论 1.3 公司理财的主要内容 1.4 公司理财的原则与职能 1.5 公司理财环境

本章学习目标

了解现代企业组织的不同类型、企业的性质 和目标,熟悉企业尤其是公司理财的主要目 标,理解企业价值理论的主要内容,掌握现 代企业理财的主要内容,并对企业理财的职 能和原则有一个基本的认识。

方法一:把递延年金视为n期普通年金,求出递延期末的年金现 值,然后再将此现值用复利调整到第一期期初。

方法二:假设递延期中也有收付款项,则应先求出(m+n)期的 年金现值,然后扣除实际并未发生收付的递延期(m)的年 金现值,即可得出递延年金的现值。

2.1资金时间价值观念

永续年金是指无限期等额支付的年金。实际经济生活 中可以将利率较高、持续期较长的年金视为永续 年金。

运用概率方法计量单项资产的风险及风险报酬,其具 体步骤和计算公式如下:

确定概率及概率分布 计算期望值。报酬率的期望值 计算方差和标准

方差

标准差

2.2风险与收益权衡观念

计算变异系数。

可以用于不同期望值的随机

变量风险的比较。

计算风险报酬率 。

险报酬率=风险报酬系数×变异系数

精编版罗斯《公司理财》中文版第九版课件资料

现值是指未来一定时间的特定货币按一定利率折算 到现在的价值。

终值是指现在一定数额的资金按一定的利率计算的 一定时间后的价值。

2.1资金时间价值观念

复利终值与现值

复利终值,是指一次性的收、付款项经过若干期的使用 后,所获得的包括本金和利息在内的未来价值。

因为永续年金无终止时间,所以不存在终值问题,永续 年金推倒公式如下:

2.1资金时间价值观念

资金时间价值计算中的几个特殊问题

不等额系列款项现值的计算:为求得不等额的系列付 款的现值之和,可以先计算每次付款的复利现值, 然后加总。

年金与不等额的系列付款混合情况下的现值:如果在 一组不等额的系列款项中,有部分是连续发生的 等额付款,则可分段计算其年金现值及复利现值, 然后加总。

式中: 是第j种证券的预期报酬率; 是第j种证券在全部投 资额中的比重;m是组合中证券种类总数。

2.2风险与收益权衡观念

组合投资的风险及度量。证券组合的风险不仅仅取决 于组合内各种证券的风险,还取决于各个证券之 间的关系。投资组合报酬率概率分布的标准差的 计算公式为:

式中:m是组合内证券种类总数; 是第j种证券在投资总额中 占的比例; 是第k种证券在投资总额中占的比例; 是第j种 证券与第k种证券报酬率的协方差。

1.4公司理财的原则与职能

公司理财原则

资金合理配置原则 财务收支平衡原则 成本-效益原则 风险与收益均衡原则 利益关系协调原则

1.4公司理财的原则与职能

公司理财职能

财务预测 财务决策 财务预算 财务控制 财务分析

1.5公司理财环境

公司理财的宏观环境

经济环境

公司理财-罗斯Ch09最新版本ppt课件

Initial investment

–the sum of the cash received and the change in value of the asset divided by the original investment.

9-2

9.1 RETURNS

Dollar Return = Dividend + Change in Market Value

percentage return =

dollar return

beginning market value

= dividend +change in market value beginning market value

= dividend yield +capital gains yield

9-3

4 15%

= .095844 = 9.58%

So, our investor made 9.58% on his money for four years, realizing a holding period return of 44.21%

1.4421 = (1.095844)4

9-9

HOLDING PERIOD RETURN: EXAMPLE

Quite well. You invested $25 × 100 = $2,500. At the end of the year, you have stock worth $3,000 and cash dividends of $20. Your dollar gain was $520 = $20 + ($3,000 – $2,500). $520

holding period return = = (1+ r1) (1+ r2 ) (1+ rn ) 1

(完整版)罗斯《公司理财》重点知识整理

第一章导论1. 公司目标:为所有者创造价值公司价值在于其产生现金流能力。

2. 财务管理的目标:最大化现有股票的每股现值。

3. 公司理财可以看做对一下几个问题进行研究:1. 资本预算:公司应该投资什么样的长期资产。

2. 资本结构:公司如何筹集所需要的资金。

3. 净运营资本管理:如何管理短期经营活动产生的现金流。

4. 公司制度的优点:有限责任,易于转让所有权,永续经营。

缺点:公司税对股东的双重课税。

第二章会计报表与现金流量资产 = 负债 + 所有者权益(非现金项目有折旧、递延税款)EBIT(经营性净利润) = 净销售额 - 产品成本 - 折旧EBITDA = EBIT + 折旧及摊销现金流量总额CF(A) = 经营性现金流量 - 资本性支出 - 净运营资本增加额 = CF(B) + CF(S)经营性现金流量OCF = 息税前利润 + 折旧 - 税资本性输出 = 固定资产增加额 + 折旧净运营资本 = 流动资产 - 流动负债第三章财务报表分析与财务模型1. 短期偿债能力指标(流动性指标)流动比率 = 流动资产/流动负债(一般情况大于一)速动比率 = (流动资产 - 存货)/流动负债(酸性实验比率)现金比率 = 现金/流动负债流动性比率是短期债权人关心的,越高越好;但对公司而言,高流动性比率意味着流动性好,或者现金等短期资产运用效率低下。

对于一家拥有强大借款能力的公司,看似较低的流动性比率可能并非坏的信号2. 长期偿债能力指标(财务杠杆指标)负债比率 = (总资产 - 总权益)/总资产 or (长期负债 + 流动负债)/总资产权益乘数 = 总资产/总权益 = 1 + 负债权益比利息倍数 = EBIT/利息现金对利息的保障倍数(Cash coverage radio) = EBITDA/利息3. 资产管理或资金周转指标存货周转率 = 产品销售成本/存货存货周转天数= 365天/存货周转率应收账款周转率 = (赊)销售额/应收账款总资产周转率 = 销售额/总资产 = 1/资本密集度4. 盈利性指标销售利润率 = 净利润/销售额资产收益率ROA = 净利润/总资产权益收益率ROE = 净利润/总权益5. 市场价值度量指标市盈率 = 每股价格/每股收益EPS 其中EPS = 净利润/发行股票数市值面值比 = 每股市场价值/每股账面价值企业价值EV = 公司市值 + 有息负债市值 - 现金EV乘数 = EV/EBITDA6. 杜邦恒等式ROE = 销售利润率(经营效率)x总资产周转率(资产运用效率)x权益乘数(财杠)ROA = 销售利润率x总资产周转率7. 销售百分比法假设项目随销售额变动而成比例变动,目的在于提出一个生成预测财务报表的快速实用方法。

罗斯《公司理财》中文版第九版课件-PPT精选文档307页

上述公式同资本资产定价模型完全一致,因此CAPM可以视作APT特殊 的单因素模型。

第三章 利率与证券估价

1 -46

本章内容

3.1利率及其决定因素 3.2 债券估价 3.3 股票估价

不可分散风险:又称系统风险或市场风险,是指由于某 种因素导致股票市场上所有的股票都出现价格变动 的现象,会给一切证券投资者带来损失的可能性。

2.2风险与收益权衡观念

β系数与投资组合的收益

系统风险对个别股票的影响程度,可由该股票价格变动的历史 数据和市场价格的历史数据计算分析得出,通常用β系数来

表示。

2.2风险与收益权衡观念

证券市场线

单一证券的风险和收益之间的关系可由证券市场线(SML)来描述

2.2风险与收益权衡观念

资本资产定价模型揭示了风险与收益的关系。必要收益率等 于无风险收益率加上风险溢酬,公式如下:

套利定价模型(APT)指出多种风险因素共同影响收益,证 券之间的相关性就是由这些共同的风险因素造成的。

由于资金在不同时点的价值不同,所以资金时间 价值的表现形式就有两种:现值和终值。

现值是指未来一定时间的特定货币按一定利率折算 到现在的价值。

终值是指现在一定数额的资金按一定的利率计算的 一定时间后的价值。

2.1资金时间价值观念

复利终值与现值

复利终值,是指一次性的收、付款项经过若干期的使用 后,所获得的包括本金和利息在内的未来价值。

复利终值计算公式为如下形式:

其中,现值为P,利率为i,第n年的终值为Fn 复利现值是复利终值的逆运算

2.1资金时间价值观念

(完整版)公司理财学习笔记

公司财务课程学习笔记一、学习内容(30分)1. 学习目标直接目标:能够具体掌握公司财务的基本理论、基础知识和基本方法,提高运用公司财务知识分析和解决实际问题的能力以及动手操作能力。

最终目标:(1)通过对本门课程的学习,能够对公司财务方面的基本知识、基本概念、基本理论有较全面的理解和较深刻的认识,对财务管理、资本预算、证券投资等基本范畴有较系统的掌握,并且能够了解和接触到世界上主流公司财务理论和最新研究成果、实务运作的机制及最新发展。

(2)能够系统地理解和掌握公司财务的基本理论和基本方法,具有从事经济和管理工作所必需公司财务专业知识以及运用会计专业知识分析和解决实际问题的基本技能。

2.章节重点及关键词第一章导论章节重点:要了解《公司财务》这本书所讲解的大致内容,同时掌握金融与财务的概述知识,了解财务管理的主要环节以及目标,了解财务管理理论的发展现状。

关键词:1、金融活动的三个层次涉及到三个不同的主体:政府、企业、家庭,分别对应着财政金融、公司财务与个人理财。

2、金融研究内容:人们是如何跨期分配稀缺的资源的,特别是投资是现在进行的而收益是未来的现金流量以及未来的现金流量是不确定的。

3、金融研究的主要问题包括:公司财务(金融)、投资(资产定价)、金融市场与金融中介、宏观层次:财政、货币银行。

第二章财务管理基础章节重点了解时间价值的概念,掌握时间价值以及年金的相关计算,重点掌握时间价值的应用,即债券与股票定价,掌握分离定理。

关键词1、时间价值:指不承担任何风险,扣除通货膨胀补偿后随时间推移而增加的价值。

也就是投资收益扣除全部风险报酬后所剩余的那一部分收益。

2、单利:指在规定期限内只就本金计算利息,每期的利息收入在下一期不作为本金,不产生新的利息收入。

计算公式为: 错误!未找到引用源。

其中P是初始投资价值,F是期末价值,t 是计息3、复利:指每期的利息收入在下一期转化为本金,产生新的利息收入。

下一期的利息收入由前一期的本利和共同生成。

罗斯《公司理财》第9版精要版英文原书课后部分章节答案

CH5 11,13,18,19,2011.To find the PV of a lump sum, we use:PV = FV / (1 + r)tPV = $1,000,000 / (1.10)80 = $488.1913.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for r, we get:r = (FV / PV)1 / t– 1r = ($1,260,000 / $150)1/112– 1 = .0840 or 8.40%To find the FV of the first prize, we use:FV = PV(1 + r)tFV = $1,260,000(1.0840)33 = $18,056,409.9418.To find the FV of a lump sum, we use:FV = PV(1 + r)tFV = $4,000(1.11)45 = $438,120.97FV = $4,000(1.11)35 = $154,299.40Better start early!19. We need to find the FV of a lump sum. However, the money will only be invested for six years,so the number of periods is six.FV = PV(1 + r)tFV = $20,000(1.084)6 = $32,449.3320.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for t, we get:t = ln(FV / PV) / ln(1 + r)t = ln($75,000 / $10,000) / ln(1.11) = 19.31So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. Fro m now, you’ll wait:2 years + 19.31 years = 21.31 yearsCH6 16,24,27,42,5816.For this problem, we simply need to find the FV of a lump sum using the equation:FV = PV(1 + r)tIt is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get:FV = $2,100[1 + (.084/2)]34 = $8,505.9324.This problem requires us to find the FVA. The equation to find the FVA is:FVA = C{[(1 + r)t– 1] / r}FVA = $300[{[1 + (.10/12) ]360 – 1} / (.10/12)] = $678,146.3827.The cash flows are annual and the compounding period is quarterly, so we need to calculate theEAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get:EAR = [1 + (APR / m)]m– 1EAR = [1 + (.11/4)]4– 1 = .1146 or 11.46%And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.11462 + $1,360 / 1.11464 = $2,320.3642.The amount of principal paid on the loan is the PV of the monthly payments you make. So, thepresent value of the $1,150 monthly payments is:PVA = $1,150[(1 – {1 / [1 + (.0635/12)]}360) / (.0635/12)] = $184,817.42The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is:$240,000 – 184,817.42 = $55,182.58This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be:Balloon payment = $55,182.58[1 + (.0635/12)]360 = $368,936.5458.To answer this question, we should find the PV of both options, and compare them. Since we arepurchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is thesame as the interest rate of the loan. The PV of leasing is:PV = $99 + $450{1 – [1 / (1 + .07/12)12(3)]} / (.07/12) = $14,672.91The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is:PV = $23,000 / [1 + (.07/12)]12(3) = $18,654.82The PV of the decision to purchase is:$32,000 – 18,654.82 = $13,345.18In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be:$32,000 – PV of resale price = $14,672.91PV of resale price = $17,327.09The resale price that would make the PV of the lease versus buy decision is the FV of this value, so:Breakeven resale price = $17,327.09[1 + (.07/12)]12(3) = $21,363.01CH7 3,18,21,22,313.The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice thisproblem assumes an annual coupon. The price of the bond will be:P = $75({1 – [1/(1 + .0875)]10 } / .0875) + $1,000[1 / (1 + .0875)10] = $918.89We would like to introduce shorthand notation here. Rather than write (or type, as the case may be) the entire equation for the PV of a lump sum, or the PVA equation, it is common to abbreviate the equations as:PVIF R,t = 1 / (1 + r)twhich stands for Present Value Interest FactorPVIFA R,t= ({1 – [1/(1 + r)]t } / r )which stands for Present Value Interest Factor of an AnnuityThese abbreviations are short hand notation for the equations in which the interest rate and the number of periods are substituted into the equation and solved. We will use this shorthand notation in remainder of the solutions key.18.The bond price equation for this bond is:P0 = $1,068 = $46(PVIFA R%,18) + $1,000(PVIF R%,18)Using a spreadsheet, financial calculator, or trial and error we find:R = 4.06%This is the semiannual interest rate, so the YTM is:YTM = 2 4.06% = 8.12%The current yield is:Current yield = Annual coupon payment / Price = $92 / $1,068 = .0861 or 8.61%The effective annual yield is the same as the EAR, so using the EAR equation from the previous chapter:Effective annual yield = (1 + 0.0406)2– 1 = .0829 or 8.29%20. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are four months until the next coupon payment, so two months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $74/2 × 2/6 = $12.33And we calculate the clean price as:Clean price = Dirty price – Accrued interest = $968 – 12.33 = $955.6721. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are two months until the next coupon payment, so four months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $68/2 × 4/6 = $22.67And we calculate the dirty price as:Dirty price = Clean price + Accrued interest = $1,073 + 22.67 = $1,095.6722.To find the number of years to maturity for the bond, we need to find the price of the bond. Sincewe already have the coupon rate, we can use the bond price equation, and solve for the number of years to maturity. We are given the current yield of the bond, so we can calculate the price as: Current yield = .0755 = $80/P0P0 = $80/.0755 = $1,059.60Now that we have the price of the bond, the bond price equation is:P = $1,059.60 = $80[(1 – (1/1.072)t ) / .072 ] + $1,000/1.072tWe can solve this equation for t as follows:$1,059.60(1.072)t = $1,111.11(1.072)t– 1,111.11 + 1,000111.11 = 51.51(1.072)t2.1570 = 1.072tt = log 2.1570 / log 1.072 = 11.06 11 yearsThe bond has 11 years to maturity.31.The price of any bond (or financial instrument) is the PV of the future cash flows. Even thoughBond M makes different coupons payments, to find the price of the bond, we just find the PV of the cash flows. The PV of the cash flows for Bond M is:P M= $1,100(PVIFA3.5%,16)(PVIF3.5%,12) + $1,400(PVIFA3.5%,12)(PVIF3.5%,28) + $20,000(PVIF3.5%,40)P M= $19,018.78Notice that for the coupon payments of $1,400, we found the PVA for the coupon payments, and then discounted the lump sum back to today.Bond N is a zero coupon bond with a $20,000 par value, therefore, the price of the bond is the PV of the par, or:P N= $20,000(PVIF3.5%,40) = $5,051.45CH8 4,18,20,22,24ing the constant growth model, we find the price of the stock today is:P0 = D1 / (R– g) = $3.04 / (.11 – .038) = $42.2218.The price of a share of preferred stock is the dividend payment divided by the required return.We know the dividend payment in Year 20, so we can find the price of the stock in Year 19, one year before the first dividend payment. Doing so, we get:P19 = $20.00 / .064P19 = $312.50The price of the stock today is the PV of the stock price in the future, so the price today will be: P0 = $312.50 / (1.064)19P0 = $96.1520.We can use the two-stage dividend growth model for this problem, which is:P0 = [D0(1 + g1)/(R –g1)]{1 – [(1 + g1)/(1 + R)]T}+ [(1 + g1)/(1 + R)]T[D0(1 + g2)/(R –g2)]P0= [$1.25(1.28)/(.13 – .28)][1 – (1.28/1.13)8] + [(1.28)/(1.13)]8[$1.25(1.06)/(.13 – .06)]P0= $69.5522.We are asked to find the dividend yield and capital gains yield for each of the stocks. All of thestocks have a 15 percent required return, which is the sum of the dividend yield and the capital gains yield. To find the components of the total return, we need to find the stock price for each stock. Using this stock price and the dividend, we can calculate the dividend yield. The capital gains yield for the stock will be the total return (required return) minus the dividend yield.W: P0 = D0(1 + g) / (R–g) = $4.50(1.10)/(.19 – .10) = $55.00Dividend yield = D1/P0 = $4.50(1.10)/$55.00 = .09 or 9%Capital gains yield = .19 – .09 = .10 or 10%X: P0 = D0(1 + g) / (R–g) = $4.50/(.19 – 0) = $23.68Dividend yield = D1/P0 = $4.50/$23.68 = .19 or 19%Capital gains yield = .19 – .19 = 0%Y: P0 = D0(1 + g) / (R–g) = $4.50(1 – .05)/(.19 + .05) = $17.81Dividend yield = D1/P0 = $4.50(0.95)/$17.81 = .24 or 24%Capital gains yield = .19 – .24 = –.05 or –5%Z: P2 = D2(1 + g) / (R–g) = D0(1 + g1)2(1 + g2)/(R–g2) = $4.50(1.20)2(1.12)/(.19 – .12) = $103.68P0 = $4.50 (1.20) / (1.19) + $4.50 (1.20)2/ (1.19)2 + $103.68 / (1.19)2 = $82.33Dividend yield = D1/P0 = $4.50(1.20)/$82.33 = .066 or 6.6%Capital gains yield = .19 – .066 = .124 or 12.4%In all cases, the required return is 19%, but the return is distributed differently between current income and capital gains. High growth stocks have an appreciable capital gains component but a relatively small current income yield; conversely, mature, negative-growth stocks provide a high current income but also price depreciation over time.24.Here we have a stock with supernormal growth, but the dividend growth changes every year forthe first four years. We can find the price of the stock in Year 3 since the dividend growth rate is constant after the third dividend. The price of the stock in Year 3 will be the dividend in Year 4, divided by the required return minus the constant dividend growth rate. So, the price in Year 3 will be:P3 = $2.45(1.20)(1.15)(1.10)(1.05) / (.11 – .05) = $65.08The price of the stock today will be the PV of the first three dividends, plus the PV of the stock price in Year 3, so:P0 = $2.45(1.20)/(1.11) + $2.45(1.20)(1.15)/1.112 + $2.45(1.20)(1.15)(1.10)/1.113 + $65.08/1.113 P0 = $55.70CH9 3,4,6,9,153.Project A has cash flows of $19,000 in Year 1, so the cash flows are short by $21,000 ofrecapturing the initial investment, so the payback for Project A is:Payback = 1 + ($21,000 / $25,000) = 1.84 yearsProject B has cash flows of:Cash flows = $14,000 + 17,000 + 24,000 = $55,000during this first three years. The cash flows are still short by $5,000 of recapturing the initial investment, so the payback for Project B is:B: Payback = 3 + ($5,000 / $270,000) = 3.019 yearsUsing the payback criterion and a cutoff of 3 years, accept project A and reject project B.4.When we use discounted payback, we need to find the value of all cash flows today. The valuetoday of the project cash flows for the first four years is:Value today of Year 1 cash flow = $4,200/1.14 = $3,684.21Value today of Year 2 cash flow = $5,300/1.142 = $4,078.18Value today of Year 3 cash flow = $6,100/1.143 = $4,117.33Value today of Year 4 cash flow = $7,400/1.144 = $4,381.39To find the discounted payback, we use these values to find the payback period. The discounted first year cash flow is $3,684.21, so the discounted payback for a $7,000 initial cost is:Discounted payback = 1 + ($7,000 – 3,684.21)/$4,078.18 = 1.81 yearsFor an initial cost of $10,000, the discounted payback is:Discounted payback = 2 + ($10,000 – 3,684.21 – 4,078.18)/$4,117.33 = 2.54 yearsNotice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Year 1 and Year 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Year 3 to get the fractional portion of the discounted payback.If the initial cost is $13,000, the discounted payback is:Discounted payback = 3 + ($13,000 – 3,684.21 – 4,078.18 – 4,117.33) / $4,381.39 = 3.26 years6.Our definition of AAR is the average net income divided by the average book value. The averagenet income for this project is:Average net income = ($1,938,200 + 2,201,600 + 1,876,000 + 1,329,500) / 4 = $1,836,325And the average book value is:Average book value = ($15,000,000 + 0) / 2 = $7,500,000So, the AAR for this project is:AAR = Average net income / Average book value = $1,836,325 / $7,500,000 = .2448 or 24.48%9.The NPV of a project is the PV of the outflows minus the PV of the inflows. Since the cashinflows are an annuity, the equation for the NPV of this project at an 8 percent required return is: NPV = –$138,000 + $28,500(PVIFA8%, 9) = $40,036.31At an 8 percent required return, the NPV is positive, so we would accept the project.The equation for the NPV of the project at a 20 percent required return is:NPV = –$138,000 + $28,500(PVIFA20%, 9) = –$23,117.45At a 20 percent required return, the NPV is negative, so we would reject the project.We would be indifferent to the project if the required return was equal to the IRR of the project, since at that required return the NPV is zero. The IRR of the project is:0 = –$138,000 + $28,500(PVIFA IRR, 9)IRR = 14.59%15.The profitability index is defined as the PV of the cash inflows divided by the PV of the cashoutflows. The equation for the profitability index at a required return of 10 percent is:PI = [$7,300/1.1 + $6,900/1.12 + $5,700/1.13] / $14,000 = 1.187The equation for the profitability index at a required return of 15 percent is:PI = [$7,300/1.15 + $6,900/1.152 + $5,700/1.153] / $14,000 = 1.094The equation for the profitability index at a required return of 22 percent is:PI = [$7,300/1.22 + $6,900/1.222 + $5,700/1.223] / $14,000 = 0.983We would accept the project if the required return were 10 percent or 15 percent since the PI is greater than one. We would reject the project if the required return were 22 percent since the PI is less than one.CH10 9,13,14,17,18ing the tax shield approach to calculating OCF (Remember the approach is irrelevant; the finalanswer will be the same no matter which of the four methods you use.), we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = ($2,650,000 – 840,000)(1 – 0.35) + 0.35($3,900,000/3)OCF = $1,631,50013.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation = $560,000/5Annual depreciation = $112,000Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus (or plus) the taxes on the sale of the equipment, so:Aftertax salvage value = MV + (BV – MV)t cVery often the book value of the equipment is zero as it is in this case. If the book value is zero, the equation for the aftertax salvage value becomes:Aftertax salvage value = MV + (0 – MV)t cAftertax salvage value = MV(1 – t c)We will use this equation to find the aftertax salvage value since we know the book value is zero.So, the aftertax salvage value is:Aftertax salvage value = $85,000(1 – 0.34)Aftertax salvage value = $56,100Using the tax shield approach, we find the OCF for the project is:OCF = $165,000(1 – 0.34) + 0.34($112,000)OCF = $146,980Now we can find the project NPV. Notice we include the NWC in the initial cash outlay. The recovery of the NWC occurs in Year 5, along with the aftertax salvage value.NPV = –$560,000 – 29,000 + $146,980(PVIFA10%,5) + [($56,100 + 29,000) / 1.105]NPV = $21,010.2414.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation charge = $720,000/5Annual depreciation charge = $144,000The aftertax salvage value of the equipment is:Aftertax salvage value = $75,000(1 – 0.35)Aftertax salvage value = $48,750Using the tax shield approach, the OCF is:OCF = $260,000(1 – 0.35) + 0.35($144,000)OCF = $219,400Now we can find the project IRR. There is an unusual feature that is a part of this project.Accepting this project means that we will reduce NWC. This reduction in NWC is a cash inflow at Year 0. This reduction in NWC implies that when the project ends, we will have to increase NWC. So, at the end of the project, we will have a cash outflow to restore the NWC to its level before the project. We also must include the aftertax salvage value at the end of the project. The IRR of the project is:NPV = 0 = –$720,000 + 110,000 + $219,400(PVIFA IRR%,5) + [($48,750 – 110,000) / (1+IRR)5]IRR = 21.65%17.We will need the aftertax salvage value of the equipment to compute the EAC. Even though theequipment for each product has a different initial cost, both have the same salvage value. The aftertax salvage value for both is:Both cases: aftertax salvage value = $40,000(1 – 0.35) = $26,000To calculate the EAC, we first need the OCF and NPV of each option. The OCF and NPV for Techron I is:OCF = –$67,000(1 – 0.35) + 0.35($290,000/3) = –9,716.67NPV = –$290,000 – $9,716.67(PVIFA10%,3) + ($26,000/1.103) = –$294,629.73EAC = –$294,629.73 / (PVIFA10%,3) = –$118,474.97And the OCF and NPV for Techron II is:OCF = –$35,000(1 – 0.35) + 0.35($510,000/5) = $12,950NPV = –$510,000 + $12,950(PVIFA10%,5) + ($26,000/1.105) = –$444,765.36EAC = –$444,765.36 / (PVIFA10%,5) = –$117,327.98The two milling machines have unequal lives, so they can only be compared by expressing both on an equivalent annual basis, which is what the EAC method does. Thus, you prefer the Techron II because it has the lower (less negative) annual cost.18.To find the bid price, we need to calculate all other cash flows for the project, and then solve forthe bid price. The aftertax salvage value of the equipment is:Aftertax salvage value = $70,000(1 – 0.35) = $45,500Now we can solve for the necessary OCF that will give the project a zero NPV. The equation for the NPV of the project is:NPV = 0 = –$940,000 – 75,000 + OCF(PVIFA12%,5) + [($75,000 + 45,500) / 1.125]Solving for the OCF, we find the OCF that makes the project NPV equal to zero is:OCF = $946,625.06 / PVIFA12%,5 = $262,603.01The easiest way to calculate the bid price is the tax shield approach, so:OCF = $262,603.01 = [(P – v)Q – FC ](1 – t c) + t c D$262,603.01 = [(P – $9.25)(185,000) – $305,000 ](1 – 0.35) + 0.35($940,000/5)P = $12.54CH14 6、9、20、23、246. The pretax cost of debt is the YTM of the company’s bonds, so:P0 = $1,070 = $35(PVIFA R%,30) + $1,000(PVIF R%,30)R = 3.137%YTM = 2 × 3.137% = 6.27%And the aftertax cost of debt is:R D = .0627(1 – .35) = .0408 or 4.08%9. ing the equation to calculate the WACC, we find:WACC = .60(.14) + .05(.06) + .35(.08)(1 – .35) = .1052 or 10.52%b.Since interest is tax deductible and dividends are not, we must look at the after-tax cost ofdebt, which is:.08(1 – .35) = .0520 or 5.20%Hence, on an after-tax basis, debt is cheaper than the preferred stock.ing the debt-equity ratio to calculate the WACC, we find:WACC = (.90/1.90)(.048) + (1/1.90)(.13) = .0912 or 9.12%Since the project is riskier than the company, we need to adjust the project discount rate for the additional risk. Using the subjective risk factor given, we find:Project discount rate = 9.12% + 2.00% = 11.12%We would accept the project if the NPV is positive. The NPV is the PV of the cash outflows plus the PV of the cash inflows. Since we have the costs, we just need to find the PV of inflows. The cash inflows are a growing perpetuity. If you remember, the equation for the PV of a growing perpetuity is the same as the dividend growth equation, so:PV of future CF = $2,700,000/(.1112 – .04) = $37,943,787The project should only be undertaken if its cost is less than $37,943,787 since costs less than this amount will result in a positive NPV.23. ing the dividend discount model, the cost of equity is:R E = [(0.80)(1.05)/$61] + .05R E = .0638 or 6.38%ing the CAPM, the cost of equity is:R E = .055 + 1.50(.1200 – .0550)R E = .1525 or 15.25%c.When using the dividend growth model or the CAPM, you must remember that both areestimates for the cost of equity. Additionally, and perhaps more importantly, each methodof estimating the cost of equity depends upon different assumptions.Challenge24.We can use the debt-equity ratio to calculate the weights of equity and debt. The debt of thecompany has a weight for long-term debt and a weight for accounts payable. We can use the weight given for accounts payable to calculate the weight of accounts payable and the weight of long-term debt. The weight of each will be:Accounts payable weight = .20/1.20 = .17Long-term debt weight = 1/1.20 = .83Since the accounts payable has the same cost as the overall WACC, we can write the equation for the WACC as:WACC = (1/1.7)(.14) + (0.7/1.7)[(.20/1.2)WACC + (1/1.2)(.08)(1 – .35)]Solving for WACC, we find:WACC = .0824 + .4118[(.20/1.2)WACC + .0433]WACC = .0824 + (.0686)WACC + .0178(.9314)WACC = .1002WACC = .1076 or 10.76%We will use basically the same equation to calculate the weighted average flotation cost, except we will use the flotation cost for each form of financing. Doing so, we get:Flotation costs = (1/1.7)(.08) + (0.7/1.7)[(.20/1.2)(0) + (1/1.2)(.04)] = .0608 or 6.08%The total amount we need to raise to fund the new equipment will be:Amount raised cost = $45,000,000/(1 – .0608)Amount raised = $47,912,317Since the cash flows go to perpetuity, we can calculate the present value using the equation for the PV of a perpetuity. The NPV is:NPV = –$47,912,317 + ($6,200,000/.1076)NPV = $9,719,777CH16 1,4,12,14,171. a. A table outlining the income statement for the three possible states of the economy isshown below. The EPS is the net income divided by the 5,000 shares outstanding. The lastrow shows the percentage change in EPS the company will experience in a recession or anexpansion economy.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 0 0 0NI $14,000 $28,000 $36,400EPS $ 2.80 $ 5.60 $ 7.28%∆EPS –50 –––+30b.If the company undergoes the proposed recapitalization, it will repurchase:Share price = Equity / Shares outstandingShare price = $250,000/5,000Share price = $50Shares repurchased = Debt issued / Share priceShares repurchased =$90,000/$50Shares repurchased = 1,800The interest payment each year under all three scenarios will be:Interest payment = $90,000(.07) = $6,300The last row shows the percentage change in EPS the company will experience in arecession or an expansion economy under the proposed recapitalization.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 6,300 6,300 6,300NI $7,700 $21,700 $30,100EPS $2.41 $ 6.78 $9.41%∆EPS –64.52 –––+38.714. a.Under Plan I, the unlevered company, net income is the same as EBIT with no corporate tax.The EPS under this capitalization will be:EPS = $350,000/160,000 sharesEPS = $2.19Under Plan II, the levered company, EBIT will be reduced by the interest payment. The interest payment is the amount of debt times the interest rate, so:NI = $500,000 – .08($2,800,000)NI = $126,000And the EPS will be:EPS = $126,000/80,000 sharesEPS = $1.58Plan I has the higher EPS when EBIT is $350,000.b.Under Plan I, the net income is $500,000 and the EPS is:EPS = $500,000/160,000 sharesEPS = $3.13Under Plan II, the net income is:NI = $500,000 – .08($2,800,000)NI = $276,000And the EPS is:EPS = $276,000/80,000 sharesEPS = $3.45Plan II has the higher EPS when EBIT is $500,000.c.To find the breakeven EBIT for two different capital structures, we simply set the equationsfor EPS equal to each other and solve for EBIT. The breakeven EBIT is:EBIT/160,000 = [EBIT – .08($2,800,000)]/80,000EBIT = $448,00012. a.With the information provided, we can use the equation for calculating WACC to find thecost of equity. The equation for WACC is:WACC = (E/V)R E + (D/V)R D(1 – t C)The company has a debt-equity ratio of 1.5, which implies the weight of debt is 1.5/2.5, and the weight of equity is 1/2.5, soWACC = .10 = (1/2.5)R E + (1.5/2.5)(.07)(1 – .35)R E = .1818 or 18.18%b.To find the unlevered cost of equity we need to use M&M Proposition II with taxes, so:R E = R U + (R U– R D)(D/E)(1 – t C).1818 = R U + (R U– .07)(1.5)(1 – .35)R U = .1266 or 12.66%c.To find the cost of equity under different capital structures, we can again use M&MProposition II with taxes. With a debt-equity ratio of 2, the cost of equity is:R E = R U + (R U– R D)(D/E)(1 – t C)R E = .1266 + (.1266 – .07)(2)(1 – .35)R E = .2001 or 20.01%With a debt-equity ratio of 1.0, the cost of equity is:R E = .1266 + (.1266 – .07)(1)(1 – .35)R E = .1634 or 16.34%And with a debt-equity ratio of 0, the cost of equity is:R E = .1266 + (.1266 – .07)(0)(1 – .35)R E = R U = .1266 or 12.66%14. a.The value of the unlevered firm is:V U = EBIT(1 – t C)/R UV U = $92,000(1 – .35)/.15V U = $398,666.67b.The value of the levered firm is:V U = V U + t C DV U = $398,666.67 + .35($60,000)V U = $419,666.6717.With no debt, we are finding the value of an unlevered firm, so:V U = EBIT(1 – t C)/R UV U = $14,000(1 – .35)/.16V U = $56,875With debt, we simply need to use the equation for the value of a levered firm. With 50 percent debt, one-half of the firm value is debt, so the value of the levered firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(.50)($56,875)V L = $66,828.13And with 100 percent debt, the value of the firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(1.0)($56,875)V L = $76,781.25c.The net cash flows is the present value of the average daily collections times the daily interest rate, minus the transaction cost per day, so:Net cash flow per day = $1,276,275(.0002) – $0.50(385)Net cash flow per day = $62.76The net cash flow per check is the net cash flow per day divided by the number of checksreceived per day, or:Net cash flow per check = $62.76/385Net cash flow per check = $0.16Alternatively, we could find the net cash flow per check as the number of days the system reduces collection time times the average check amount times the daily interest rate, minusthe transaction cost per check. Doing so, we confirm our previous answer as:Net cash flow per check = 3($1,105)(.0002) – $0.50Net cash flow per check = $0.16 per checkThis makes the total costs:Total costs = $18,900,000 + 56,320,000 = $75,220,000The flotation costs as a percentage of the amount raised is the total cost divided by the amount raised, so:Flotation cost percentage = $75,220,000/$180,780,000 = .4161 or 41.61%8.The number of rights needed per new share is:Number of rights needed = 120,000 old shares/25,000 new shares = 4.8 rights per new share.Using P RO as the rights-on price, and P S as the subscription price, we can express the price per share of the stock ex-rights as:P X = [NP RO + P S]/(N + 1)a.P X = [4.8($94) + $94]/(4.80 + 1) = $94.00; No change.b. P X = [4.8($94) + $90]/(4.80 + 1) = $93.31; Price drops by $0.69 per share.。