IAS14 Segment Reporting

HK GAAP vs IFRS

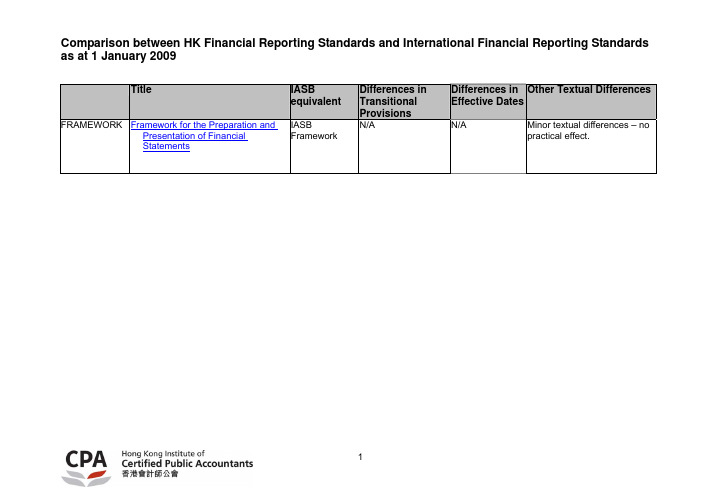

as at 1 January 20091TitleIASBequivalentDifferences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences FRAMEWORK Framework for the Preparation andPresentation of Financial StatementsIASBFrameworkN/AN/AMinor textual differences – no practical effect.as at 1 January 20092HKFRS No.TitleIFRS No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HKFRS 1First-time Adoption of Hong Kong Financial Reporting StandardsIFRS 1NoNo, except para 47EA specifies that paras 23and 27 to 30 of HKFRS 1 (IFRS 1) are effective for AP beginning on or after 1 January 2005 (1 January 2004).Minor textual differences – no practical effect.HKFRS 1 Revised First-time Adoption of Hong Kong Financial Reporting StandardsIFRS 1 Revised NoNo, except para 39A specifies that paras B2 to B6 and D18 of HKFRS 1 (IFRS 1) are effective for AP beginning on or after 1 January 2005 (1 January 2004). Minor textual differences – no practical effect. HKFRS 2 Share-based Payment IFRS 2No No No HKFRS 3Business Combinations IFRS 3 NoExcept for limitedretrospective application as per para 85, HKFRS 3 (IFRSNoas at 1 January 20093HKFRS No. Title IFRS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences 3) is effective for businesscombinations for which theagreement date is on or after 1 January 2005 (31 March 2004).HKFRS 3 Revised Business Combinations IFRS 3 Revised No No NoHKFRS 4 Insurance Contracts IFRS 4 No No NoHKFRS 5 Non-current Assets Held for Sale and Discontinued OperationsIFRS 5No No No HKFRS 6 Exploration for and Evaluation of Mineral ResourcesIFRS 6 No No NoHKFRS 7 Financial Instruments: Disclosures IFRS 7 No No NoHKFRS 8 Operating Segments IFRS 8 No No NoImprovements to HKFRSs Improvements to HKFRSs Improvements to IFRSsNo No Noas at 1 January 20094HKAS No. Title IAS No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HKAS 1 Presentation of Financial Statements IAS 1NoNo*Minor textual differences – explanation of legalrequirements which do not give rise to differences.HKAS 1 RevisedPresentation of Financial Statements IAS 1 Revised No No Minor textual differences –explanation of legalrequirements which do not give rise to differences.HKAS 2 Inventories IAS 2 No No* No HKAS 7Cash Flow StatementsIAS 7NoHKAS 7 (IAS 7) is effective for AP beginning on or after 1January 2005 (1 January 1994). NoHKAS 8Accounting Policies, Changes in Accounting Estimates and ErrorsIAS 8 NoNo* Minor textual differences – nopractical effect.as at 1 January 20095HKAS No.TitleIAS No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HKAS 10 Events after the Balance Sheet Date IAS 10NoNo*Minor textual differences – explanation of legalrequirements which do not give rise to differences.HKAS 11 Construction Contracts IAS 11 NoHKAS 11* (IAS 11) is effective for AP beginning on or after 1 January 2005 (1 January 1995). Noas at 1 January 20096HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 12 Income Taxes IAS 12 NoHKAS 12* (IAS 12) is effective for AP beginning on or after 1 January 2005 (1 January 1998 with certain amendments effective for AP beginning on or after 1 January 2001).The explanatory guidance and illustrative examples set out in the boxes within the body of HKAS 12 contain material that is expanded on that in IAS 12 and considered to be more user-friendly. HKAS 14 Segment Reporting IAS 14 NoHKAS 14* (IAS 14) is effective for AP beginning on or after 1 January 2005 (1 July 1998).Noas at 1 January 20097HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 16 Property, Plant and Equipment IAS 16HKAS 16 has the following additional transition provisions. 1. Para 80Aexempting certain entities that carried their PPE atrevalued amounts before 30September 1995 and have notrevalued since that date from making regular revaluation.2. Para 80B allowingthose not-for-profit entities that previously took advantage of the exemption under SSAP 17 to deem the carrying amount of an item of PPE immediately before applying HKAS 16 on its effective date (or earlier) as the cost of that item. No* Noas at 1 January 20098HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 17 LeasesIAS 17 No No* No HKAS 18Revenue IAS 18 No HKAS 18* (IAS 18) is effective for AP beginning on or after 1 January 2005 (1 January 1995).NoHKAS 19Employee Benefits IAS 19 HKAS 19 has an additional paragraph 153A specifying that the transitional provisions set out in paragraphs 154 to 156 of HKAS 19 apply only when an entity had not previously appliedSSAP 34 (May 2003). HKAS 19* (IAS 19) is effective for AP beginning on or after 1 January 2005 (1 January 1999 with certain amendmentscommencing later).Noas at 1 January 20099HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 20Accounting for Government Grants and Disclosure of Government AssistanceIAS 20IAS 20 has anadditional transitional provision (para 40)allowing an entityadopting IAS 20 for the first time to apply the accounting provisions of IAS 20 only to grants or portions of grants becoming receivable or repayable after the effective date of IAS 20. HKAS 20* (IAS 20) is effectivefor AP beginning on or after 1 January 2005 (1 January 1984). No HKAS 21The Effects of Changes in Foreign Exchange RatesIAS 21No No* Noas at 1 January 200910HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 23Borrowing Costs IAS 23 HKAS 23 has an additional transitional provision (para 30) allowing entities that expense all borrowing costs to apply new policy prospectively. IAS 23 has anadditional transitional provision (para 30) permitting entities that expensed borrowing costs to capitalize borrowing costs prospectively.HKAS 23*(IAS 23) is effective for AP beginning on or after 1 January 2005 (1 January 1995). NoHKAS 23 RevisedBorrowing Costs IAS 23 Revised No No NoHKAS 24 Related Party DisclosuresIAS 24 No No*NoHKAS 26Accounting and Reporting by Retirement Benefit PlansIAS 26NoHKAS 26 (IAS 26) is effective for AP beginning on or after 1January 2005 (1 January 1988).HKAS 26 has an appendix giving guidance on preparing financial statements of MPFschemes and ORSO schemes in accordance with the standard.as at 1 January 200911HKAS No.TitleIAS No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HKAS 27Consolidated and Separate Financial StatementsIAS 27 NoNo*Minor textual differences – explanation of legalrequirements which do not give rise to differences.HKAS 27 RevisedConsolidated and Separate Financial StatementsIAS 27 Revised No No Minor textual differences –explanation of legalrequirements which do not give rise to differences.HKAS 28 Investments in Associates IAS 28 No No* NoHKAS 29Financial Reporting inHyperinflationary EconomiesIAS 29NoHKAS 29 (IAS 29) is effective for AP beginning on or after 1 January 2005 (1 January 1990). Noas at 1 January 200912HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 31 Interests in Joint Ventures IAS 31 NoNo* NoHKAS 32Financial Instruments: Presentation IAS 32 HKAS 32 has an additional transitional provision (para 97)allowing an entity not to present comparative information if such information is not available. No NoHKAS 33Earnings per Share IAS 33 No No* NoHKAS 34Interim Financial Reporting IAS 34 No HKAS 34* (IAS 34) is effective for AP beginning on or after 1 January 2005 (1 January 1999).Noas at 1 January 200913HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 36Impairment of Assets IAS 36 HKAS 36 (IAS 36) para 139 specifies that an entity shall apply HKAS 36 (IAS 36) (a) to goodwill and intangible assets acquired in businesscombinations for which theagreement date is on or after 1January 2005 (31 March 2004); and(b) to all other assetsprospectively from the beginning of the first annual period beginning on or after 1January 2005 (31 March 2004).HKAS 36 (IAS 36) is effective for AP beginning on or after 1 January 2005 (31 March2004). Noas at 1 January 200914HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 37Provisions, Contingent Liabilities and Contingent AssetsIAS 37 IAS 37 has anadditional transitional provision (para 93)allowing an entity not to adjust opening balance of retained earnings for the earliest period presented and to restate comparative information for the period in which IAS 37 is first adopted.HKAS 37* (IAS 37) is effective for AP beginning on or after 1January 2005 (1 July 1999).HKAS 37 contains additional Hong Kong examples 3A, 8A,12 and 13 in Appendix C. No comparable examples are included in Appendix C to IAS37 – no practical effect.as at 1 January 200915HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 38 Intangible Assets IAS 38HKAS 38 (IAS 38) para 130 specifies that an entity shall apply HKAS 38 (IAS 38): (a) to the accounting for intangible assets acquired in businesscombinations for which theagreement date is on or after 1January 2005 (31 March 2004); and (b) to the accountingfor all otherintangible assets prospectively from thebeginning of the first annual period beginning on or after 1 January 2005 (31 March 2004).HKAS 38 (IAS 38) is effective for AP beginning on or after 1 January 2005 (31 March2004). Noas at 1 January 200916HKAS No. Title IAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 39Financial Instruments: Recognition and MeasurementIAS 39HKAS 39 does not permit retrospective application except in certain limited circumstances whereas IAS 39 generally requires retrospective application. Accordingly, thetransitional provisions in HKAS 39 aredifferent from those in IAS 39. For details, please refer to the Standards.No Noas at 1 January 200917HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HKAS 40Investment Property IAS 40 HKAS 40 has the following additional transitional provisions:HKAS 40 paras 80A on fair value modelPara 80A of HKAS 40 requires an entity that has previously applied SSAP 13 (2000) for non-leaseholdinvestment properties and chooses to use the fair value model to reflect the effect of applying HKAS 40 on its effective date (or earlier) as an adjustment to the opening balance of retained earnings for the period in which HKAS 40 is first applied.No* Noas at 1 January 200918HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual DifferencesPara 80A also encourages the entity to adjust the comparativeinformation if the entity has previouslydisclosed publicly fair value of thoseproperties but requires the entity to disclose the fact if otherwise.HKAS 40 paras 83A and 83B on cost modelParas 83A and 83B of HKAS 40 allow an entity to take thecarrying amount of the investment property under SSAP 13 (2000) as the deemed cost on the date that HKAS 40 is first applied. Any adjustments, includingas at 1 January 200919HKAS No.TitleIAS No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differencesthe reclassification of any amount previously held in revaluation reserve, are to be made to the opening balance of retained earnings. Depreciation on deemed costcommences from the opening balance sheet date.HKAS 41Agriculture IAS 41 No HKAS 41* (IAS 41) is effective for AP beginning on or after 1 January 2005 (1 January 2003).Noas at 1 January 200920HK(IFRIC)-Int No.Title IFRIC No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HK(IFRIC)-Int 1Changes in ExistingDecommissioning, Restoration and Similar Liabilities IFRIC 1 NoNoMinor textual differences – no practical effect. HK(IFRIC)-Int 2Members’ Shares in Co-operative Entities and Similar InstrumentsIFRIC 2No No No HK(IFRIC)-Int 4Determining whether an Arrangement contains a LeaseIFRIC 4No No No HK(IFRIC)-Int 5Rights to Interests arising fromDecommissioning, Restoration and Environmental Rehabilitation Funds IFRIC 5 NoNoNoHK(IFRIC)-Int 6Liabilities arising from Participating in a Specific Market – Waste Electrical and Electronic EquipmentIFRIC 6No No Noas at 1 January 200921HK(IFRIC)-Int No. TitleIFRIC No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HK(IFRIC)-Int 7Applying the Restatement Approach under HKAS 29 Financial Reporting inHyperinflationary EconomiesIFRIC 7NoNoNoHK(IFRIC)-Int 8Scope of HKFRS 2 IFRIC 8 No No No HK(IFRIC)-Int 9Reassessment of Embedded DerivativesIFRIC 9NoNoNoHK(IFRIC)-Int 10 Interim Financial Reporting and ImpairmentIFRIC 10No No No HK(IFRIC)-Int 11HKFRS 2 – Group and Treasury Share TransactionsIFRIC 11 NoNoNoHK(IFRIC)-Int 12 Service Concession ArrangementsIFRIC 12 No No No HK(IFRIC)-Int 13Customer Loyalty ProgrammesIFRIC 13No No No HK(IFRIC)-Int 14HKAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their InteractionIFRIC 14 NoNoNoas at 1 January 200922HK(IFRIC)-Int No. Title IFRIC No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HK(IFRIC)-Int 15 Agreements for the Construction of Real EstateIFRIC 15 No No No HK(IFRIC)-Int 16 Hedges of a Net Investment in a Foreign OperationIFRIC 16 No No No HK(IFRIC)-Int 17Distributions of Non-cash Assets to OwnersIFRIC 17 NoNoNoas at 1 January 200923HK(SIC)-Int No.TitleSIC No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HK(SIC)-Int 10Government Assistance –No Specific Relation to Operating ActivitiesSIC-10 NoHKAS-Int 10*(SIC 10) is effective for AP beginning on or after 1 January 2005 (1 August 1998).No HK(SIC)-Int 12Consolidation – Special PurposeEntitiesSIC-12 NoHKAS-Int 12*(SIC 12) is effective for AP beginning on or after 1 January 2005 (1 July 1999).No HK(SIC)-Int 13 Jointly Controlled Entities – Non-Monetary Contributions byVenturersSIC-13 NoHKAS-Int 13*(SIC 13) is effective for AP beginning on or after 1 January 2005 (1 January 1999).Noas at 1 January 200924HK(SIC)-Int No.Title SIC No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HK(SIC)-Int 15Operating Leases – Incentives SIC-15NoHKAS-Int 15* (SIC 15) is effective for lease terms beginning on or after 1 January 2005 (1 January 1999).No HK(SIC)-Int 21Income Taxes – Recovery of Revalued Non-Depreciable AssetsSIC-21 NoHKAS-Int 21*(SIC 21) is effective for AP beginning on or after 1 January 2005 (on 15 July 2000).No HK(SIC)-Int 25Income Taxes – Changes in the TaxStatus of an Enterprise or its ShareholdersSIC-25 NoHKAS-Int 25*(SIC 25) is effective for AP beginning on or after 1 January 2005 (on 15 July 2000).Noas at 1 January 200925HK(SIC)-Int No.Title SIC No.Differences in Transitional Provisions Differences in Effective DatesOther Textual Differences HK(SIC)-Int 27Evaluating the Substance ofTransactions Involving the Legal Form of a LeaseSIC-27 NoHKAS-Int 27*(SIC 27) is effective for AP beginning on or after 1 January 2005 (on 31 December 2001).No HK(SIC)-Int 29Service Concession Arrangements:DisclosuresSIC-29 NoHKAS-Int 29* (SIC 29) is effective for AP beginning on or after 1 January 2005 (on 31 December 2001).No HK(SIC)-Int 31Revenue – Barter TransactionsInvolving Advertising ServicesSIC-31 NoHKAS-Int 31*(SIC 31) is effective for AP beginning on or after 1 January 2005 (on 31 December 2001).Noas at 1 January 200926HK(SIC)-Int No.Title SIC No.Differences in Transitional ProvisionsDifferences in Effective DatesOther Textual Differences HK(SIC)-Int 32Intangible Assets – Web Site Costs SIC-32NoHKAS-Int 32* (SIC 32) is effective for AP beginning on or after 1 January 2005 (on 25 March 2002).Noas at 1 January 200927HK-Int No.TitleInternational - Int No. Differences in TransitionalProvisionsDifferences in Effective DatesOther Textual DifferencesHK-Int 1The Appropriate Accounting Policies for Infrastructure Facilities No equivalent interpretationunder IFRS.N/A N/AN/A HK-Int 3Revenue – Pre-completion Contracts for the Sale of Development Properties No equivalent interpretation under IFRS.N/A N/A N/A HK-Int 4Leases – Determination of the Length of Lease Term in respect of Hong Kong Land LeasesNo equivalent interpretationunder IFRS.N/A N/AN/ANotes* These Hong Kong pronouncements might have additional wording or paragraph(s) specifying that: (i) if an entity decides to early adopt a Standard, the entity is not required to apply all the Standards effective for the same date for that period; (ii) if an entity decides to early adopt a Standard, the entity is required to apply the relevant Interpretation for that period; (iii) early adoption is encouraged; or (iv) the previous version of the Standard is withdrawn.SIC-7 Introduction of the Euro is not adopted in Hong KongThe paragraph numbers in HKFRSs generally correspond to the paragraph numbers in IFRSs.。

IFRS8–OPERATINGSEGMENTS:国际财务报告准则8–经营分部

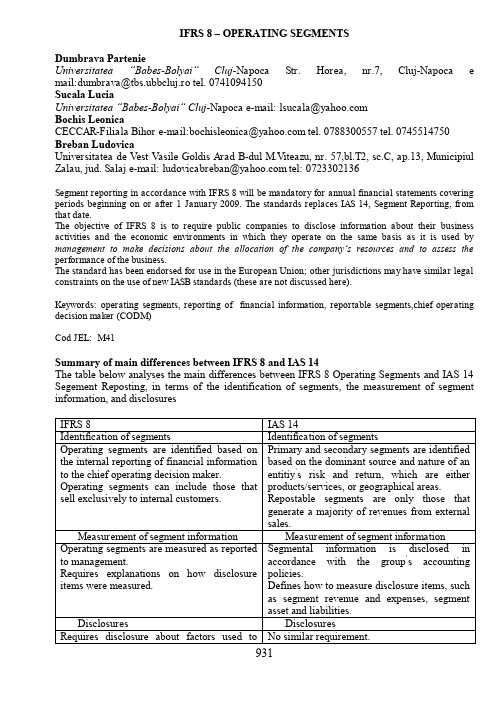

IFRS 8 – OPERATING SEGMENTSDumbrava PartenieUniversitatea “Babes-Bolyai” Cluj-Napoca Str. Horea, nr.7, Cluj-Napoca e mail:********************.rotel.0741094150Sucala LuciaUniversitatea “Babes-Bolyai” Cluj-Napocae-mail:*****************Bochis LeonicaCECCAR-FilialaBihore-mail:**************************.0788300557tel.0745514750 Breban LudovicaUniversitatea de Vest Vasile Goldis Arad B-dul M.Viteazu, nr. 57,bl.T2, sc.C, ap.13, Municipiul Zalau,jud.Salaje-mail:***************************:0723302136Segment reporting in accordance with IFRS 8 will be mandatory for annual financial statements covering periods beginning on or after 1 January 2009. The standards replaces IAS 14, Segment Reporting, from that date.The objective of IFRS 8 is to require public companies to disclose information about their business activities and the economic environments in which they operate on the same basis as it is used by management to make decisions about the allocation of the company‟s resources and to assess the performance of the business.The standard has been endorsed for use in the European Union; other jurisdictions may have similar legal constraints on the use of new IASB standards (these are not discussed here).Keywords: operating segments, reporting of financial information, reportable segments,chief operating decision maker (CODM)Cod JEL: M41Summary of main differences between IFRS 8 and IAS 14The table below analyses the main differences between IFRS 8 Operating Segments and IAS 14 Segement Reposting, in terms of the identification of segments, the measurement of segment information, and disclosuresNot all entities are required to disclose segment information in accordance with IFRS 8. IFRS 8 applies to entities that are public or are in the process of going public. If the listed parent company financial statements are presented together with a group‘s financial statements, no separate segmental information is required for the parent.The questions and answers below clarify which entities are required to present segment information, and the requirements for companies who choose to present segment information even when not required to do so by the standard.Are segment disclosures only required in the consolidated financial statements of a group? Paragraph 2 of IFRS 8 , no, an entity whose debt or equity instruments are traded in a public market is required to present segment desclosures in its individual financial statements. Segment information is also required in the consolidated financial statements of a group, when the parent‘s debt or equity instruments are traded in a public market. If the parent‘s individual financial statements are presented together with the group‘s consolidated financial statements, separate segmental disclosures for the parent are not required.Is an entity whose securities are not yet listed, but which contemplates a public offering of its debt or equity securities in the future, required to provide disclosures under IFRS 8?Only entities or groups which file or are in the process of filing their individual or the group‘s financial statements with a regulatory body for the purpose of issuing to the public debt or equity instruments would need tom comply with IFRS 8.Can an entity that is not under the scope of IFRS 8 report segmental information?Entities outside the scope will not need to comply with IFRS 8 –but may choose to do so. Information about segments that is produced on a voluntary basis but that is not compliant with IFRS 8 cannot be described as segment information.Operating segmentsOperating segments are basis of the reportable segments disclosed in the financil statements. This section also highlights the importance of the concept of the chief operating decision maker (CODM) for the identification of operating segments. An operating segment is defined in IFRS 8 as a component of an entity:- that engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity);- whose operating results are regularly reviewed by the entity,s CODM to make decision about resources to be allocated to the segment and assess its performance, and,for which discrete financial information is available.IFRS 8 indicates that a component should have its own revenue streams as well as incur expenses. Corporate division which earn no or only incidental revenues would not be operating segements, such as head office cost centres.The CODM is not meant to be title, but identifies a function. The CODM allocates the resourcesto and assesses the performance of the operating segments of the entity or the group. The CODM would generally be the most senior level of management in the entity, such as the chief executive officer, chief operating officer or a group of executive officers, such as the board.In the UK, the CODM will often be the board of directors collectively, but could be a sub-est of the board or an individual.If multiple sets of segment data are reviewed by the CODM, factors such as the nature of the business activities of the components, the existence of managers allocated to the components or the basis of the presentation of the information to the board should be considered to determine what the operating segments are. If none of these provides a conclusive answer, the analysis of segments that provides the most useful information in respect of the nature and financial effectsof the business activities should be the basis for identification of the operating segments.Under IAS 14 the primary reporting segment format is identified based on an entity‘s internal organisational and management structure and its system of internal financial reporting to key n management personnel. The primary reporting segment is either based on product/services or geographical areas. Under IFRS 8 the operating segments are identified based on the reporting of divisional results to the CODM. The principles of identification under IAS 14 and IFRS 8 are thus similar, but an analysis to determine the operating segments under IFRS 8 is still required, and these may well be different from the IAS 14 segments.Reportable segmentsOperating segments are identified based on the internal reporting of financial information to the CODM. Reportable segments are those actually disclosed in the financial statements. Operating and reportable segments are not always identical. The following questions and answers look at when operating segments can be aggregated or combined for reporting in the financial statements. The question is, when may operating segments be aggregated?Two or more operating segments may be aggregated if certain conditions are met:- The segment have similar economic characteristics, such as similar long-term average gross margins;- Aggregation allows the users of financial statements to evaluate the nature andfinancial effects of the business activities;- and segments are similar in each of the following respects: the nature of the products and services, the nature of the production processes, the type or class of c ustomer for their products and services, the methods used to distribute their products or provide their services, and if applicable, the nature of the regulatory environment, for example, banking, insurance or public utilities. The fact that operating segments have been aggregated should be disclosed. Operating segment information needs to be disclosed separately for each operating segment, including each aggregated operating segment, if they exceed certain quantitative thresholds.However an entity should ensure that all operating segments have been appropriately identified and the aggregation criteria have been met. The entity-wide disclosures, in accordance with paragraphs 32 to 34 of IFRS 8, are still required. It is important to ensure that the segments selected for reporting purposes are consistent with other reported information included in the annual report such as KIPs. Differences between narrative reporting and segmental financial reporting may confuse users of the financial statements. IFRS 8 does not prescribe a minimum ormaximum number of segments an entity should report as this is dependent on the individual entity‘s circumstances. Reporting too many segments may however not be practical or helpful to users. Reportable segments may change as a result of: an entity changing its internal organization or reporting structure, an operating segment increasing in importance and meeting the significance test, or an operating segment no longer meeting the significance test. When reporting segments change because of a change in the internal organization or reporting structure, the comparative information for prior periods has to be restated to reflect the new reporting segments, unless the necessary information is not available and the cost to develop it would be excessive. If prior periods cannot be restated, then in the year of change the current period needs to be disclosed based on the new and old reportable segment bases, unless the information is not available and the cost to develop it would be excessive.Measurement and disclosureUnder IFRS 8, reportable segments are measured as they are reported to the CODM, and they therefore do not necessarily comply with IFRS generally. Similarly, disclosures required by IFRS 8 are generally based on the information reported to de CODM. One of the main differences between IAS 14 and IFRS 8 is that under IFRS 8 the segment results are disclosed in the financial statements as they are used by the CODM for the purposes of making decisions about allocating resources to the segment and assessing performance. Similarly only those assets and liabilities that are included in the measures of the segment‘s assets and segment‘s liabilities that are used by the CODM shall be reported for that segment. Reconciliations from the segment results and segments assets and liabilities to the entity‘s results and entity‘s assets and liabilities respectively need to be presented. The reported measures to be disclosed should be those that management believes are determined in accordance with the measurement principles most consistent with those used in measuring the corresponding amounts in the entity‘s financial statements.If the CODM does not review a measure of liabilities no such measure needs to be disclosed. A measure of assets is required, however this would only reflect the amounts that are used by the CODM. If no asset information is reviewed by the CODM, the measure would be nil, and hence non-disclosure is deemed to be compliant with IFRS 8.The amount of each segment item reported should be the measure reported to the CODM for the purpose of making decision about the allocation of resources and the assessment of performance. When reported to the CODM allocations of costs, revenues, assets and liabilities should be included in these measures. Allocations should be made on a reasonable basis. An entity should report its measure of profit or loss for each reportable segment. The following items should also be disclosed, if reviewed by or regularly provided to the CODM, whether or not they are included in the measure of the segments results: external revenues, intra-segment revenues, gross interest revenue and expense, depreciation and amortization, material items of income and expense as disclosed under paragraph 97 of IAS 1, the entity‘s interest in associates and joint ventures accounted for by the equity method, income tax expense or income, and other material non-cash items.IFRS 8 also contains disclosure requirements applicable to all entities, regardless of whether, or in what format, the information is reported to the CODM. The information needs to be presented in accordance with the entity‘s accounting policies.Interaction of IFRS 8 with other standardsThere are important interactions between IFRS 8 and IFRS 5 Discontinued Operations and Assets Held for Sale and IAS 36 Impairment of Assets. Segmental reporting is also a requirement under IAS 34 Interim Financial Reporting, although less detail is required.The components identified as discontinued operations in accordance with IFRS 5 may either qualify as a segment under IFRS 8 or may be included within an operating segment also containing continuing operations. The information to be disclosed under IFRS 8 will mainly depend on whether the information for discontinued operations is separately reported to andreviewed by the CODM, within its own operating segment. An entity has to present a reconciliation from the segments results to the entity‘s profit or loss before discontinued operations, unless the results of discontinued operations were allocated to the segment. In accordance with IFRS 5, the reporting segment which inclused the discontinued operation should be identified and disclosed.Although to a lesser degree of detail and only by entities which are under the scope of IFRS 8 for their annual reporting. The following disclosures are required: amounts of revenues from external customers and intra-segment revenues, if included in the measure of segment profit or loss reviewed by the chief operating decision maker or otherwise regularly provided to the chief operating decision maker, amount of the measure of segment profit or loss, amount of total assets for which there has been a material change from the amount disclosed in the last annual financial statements in the basis of segmentation or in the basis of measurement of segment profit or loss. On publication of IFRS 8, IAS 36 was amended to state that the c ash generating unit, or group of such units, to wich goodwill is allocated for the purpose of the goodwill impairment test cannot be larger than an operating segment identified under IFRS 8. Prior to the issuance of IFRS 8, the equivalent requirement in IAS 36 stated that the cash generating unit or group of such units, to which goodwill is allocated, cannot be larger than a segment based on the entity‘s primary or secondary reporting format determined under IAS 14 and the operating segments identified under IFRS 8 pre-aggregation may therefore require the reallocations of goodwill for impairement test purposes on adoption of IFRS 8. IAS 36 provides guidance on the reallocagtion of goodwill resulting from a change in the composition of cash generating units.IAS 36 also contains additional disclosure requirements for entities within the scope of IFRS 8: The amount of impairment losses or reversed impairment losses recognized in profit or loss and in other comprehensive income by segment; for each material impairment loss or reversal of impairment loss, the segment to which the relevant asset or cash generating unit belongs. TransitionIFRS 8 is effective for annual financial statements for periods beginning on or after 1 January 2009. Early application is permitted and since IFRS 8 has been endorsed for use in the European Union, UK based entities can adopt this standard early for their financial reporting. If an entity provides segmental disclosures under IFRS 8, the fact should be disclosed.If an entity applies IFRS 8 from its effective date, that is to annual periods beginning on or after 1 January 2009, the entitiy‘s first IFRS 8 compliant segmental data is provided in its interim financial report in accordance with IAS 34 Interim Financial Reporting.The proposed improvement by the IASB, Issue 3, in the exposure draft, Proposed Improvements to IFRS, published by the IASB in October 2008, is a clarification regarding the disclosure of a measure of segments assets, if such a measure is not reviewed by the CODM. The proposal is that if the measure is not reviewed by the CODM, non-disclosure in compliant with IFRS 8. The proposed amendment would not change the IFRS, but only the basis of conclusion. The proposed improvement would become effective from 1 January 2010, although earlier application would be permitted.REFERENCES1. International Financial Reporting Standards, 2007,The Body of Expert and Licensed Accountants ofRomania Published, Bucharest2. IAS 14 – Segment Reporting3. IFRS 8 – Operating Segments, the Institute of Chartered Accountants in England and Wales (ICAEW)4. /ecifrsstudy。

IASB与FASB经营分部准则趋同及差异

IASB与FASB经营分部准则趋同及差异作者:陈玉媛来源:《财会通讯》2009年第03期国际会计准则理事会(IASB)于2006年11月30日发布了《国际财务报告准则第8号——经营分部》(IFRS8——operatingsegment),该准则取代了《国际会计准则第14号—分部报告》(IAS 14 SegmentReporting),并对报告期始于2009年1月1日或以后日期的年度财务报表生效,准则也允许被提前采用。

IFRS 8一经生效,国际财务报告准则与美国公认会计原则下的分部报告除些许细微的差异外将基本实现趋同。

本文拟分四个部分来论述分部报告在IASB与FASB的趋同及存在的差异。

一、分部报告的内容及重要作用(一)分部报告的内容分部报告是指对一些在不同行业或不同地区都有业务的企业,按其经营业务的不同性质或经营业务的地理范围分别编制、报出的财务报告。

对一些有着多种经营业务或多个地区分部的大企业来说,其各个分部的利润率、发展机会、未来前景和投资风险都可能存在很大的差别。

因此,信息的使用者不仅要看总体的会计报表,还需要参看分部的资料,以正确评价企业的机会与风险。

(二)分部报告的重要作用证券市场的有效运转和股份公司的健康发展都离不开会计信息披露制度的建立和健全。

随着全球经济一体化的发展和跨行业、跨地区企业集团的涌现,分部财务信息的披露越来越受到人们的关注,并成为会计信息披露制度的一个重要组成部分。

对于股东,分部报告能够大大提高其对企业未来现金流量及潜在盈利能力预测的准确性;对于债权人,可借助分部报告对未来现金流量的预测来评估企业短期变现能力和长期偿债能力,以确定其信贷决策;对宏观管理当局,分部信息则有助于其了解、校正经济统计的相关数据,修正产业政策和地区政策,评判企业在境内、境外的活动。

二、IASB与FASB分部报告中的趋同背景及历程(一)分部报告的趋同背景1998年12月,联合国贸易和发展委员会提交了一份名为《会计披露在东亚金融危机中所扮演的角色:应吸取的教训》的研究报告,对亚洲金融危机的一般特征、金融危机爆发的直接原因、会计在金融危机预警中应发挥的作用、与金融危机有关的国际会计准则等做了深入的研究,提出了各种有助于提高会计披露质量和透明度的建议。

航图讲解(英语)5

50

Boundaries

International boundary QNH/QNE boundary Time zone boundaries

QNH QN E

51

The navigation frequency COP

COP Magnetic route bearings True in the Northern Domestic Airspace of Canada

说明

•阴影框(导航设施为 航线和航路的组成部 分)、频率、识别标 志、摩尔斯代码、 DME功能、导航设施 的作用范围

13

导航设施识别

说明

•VOR或TAC/DME 天 线不安装在一起时

图中导航设施KQ、 ZGC和YM均为偏离 航路的导航设施,其 导航设施识别同样包 括名称、频率、识别 代码和DME功能等, 只是没放在方框里

Airway/Route

Diversionary Route, Weekend Route (Europe)

OTR Oceanic Transition Route

22

Overlying High AltitudeAirway/Route

Fig2.52 High Altitude roue on low altitude chart

Standard outbound length h≤14000ft(4250m) t=1min h>14000ft(4250m) t=1.5mins Non-standard outbound time Diamond-shaped box DME distance

31

4. Minimum Holding Altitude

Unit 1 Introduction of accounting

IASB’s predecessor had issued 41 IASs. IASB issued IFRSs.

IAS 1 presentation of financial statements 财务报表的列报 IAS 2 inventories 存货 IAS 7 statement of cash flows 现金流量表 IAS 8 accounting polices, changes in accounting estimates and errors 会计政策,会计估计变更与错误

Double entry bookkeeping 复式记 账法

Eg. Pay ¥5000 to buy iphone, show the transaction in T account.

Dr Bank Cr Dr Asset Cr

iphone 5000

iphone

5000

Debit side Increase in: Asset (statement of financial position) Expense (income statement)

Accounting equation 会计等式

Asset = liability + owner’s equity 资产=负债+所有者权益 Assets – Liabilities = Net assets 资产 – 负债 = 净资产 Pg.35 Statement of financial position (Balance Sheet) 资产负债表

Key terms

Assets 资产 Net assets 净资产 Liability 负债 Equity 权益 Income 收益 Revenue and gains 收入和得利 Expense 费用 Loss 损失 Borrowing 借款 Double entry bookkeeping 复式记账法

2. 国际会计准则中文版

国际会计准则2003年9月19日国际会计准则(IAS)目录Framework for the Preparation and Presentation of Financial Statements (3)Preface (24)Procedure and Objective of IASB (27)IAS 1: Presentation of Financial Statements (33)IAS 2: Inventories (55)IAS 7: Cash Flow Statements (62)IAS 8: Net Profit or Loss for the Period, Fundamental Errors and Changes in Accounting Policies (73)IAS 10: Events After the Balance Sheet Date (82)IAS 11: Construction Contracts (93)IAS 12: Income Taxes (101)IAS 14: Segment Reporting (134)IAS 15: Information Reflecting the Effects of Changing Prices (150)IAS 16: Property, Plant and Equipment (155)IAS 17: Leases (169)IAS 18: Revenue (180)IAS 19: Employee Benefits (188)IAS 20: Accounting for Government Grants and Disclosure of Government Assistance (227)IAS 21: The Effects of Changes in Foreign Exchange Rates (233)IAS 22: Business Combinations (244)IAS 23: Borrowing Costs (270)IAS 24: Related Party Disclosures (275)IAS 26: Accounting and Reporting by Retirement Benefit Plans (280)IAS 27: Consolidated Financial Statements (288)IAS 28: Investments in Associates (294)IAS 29: Financial Reporting in Hyperinflationary Economies (301)IAS 30: Disclosures in the Financial Statements of Banks and Similar Financial Institutions (308)IAS 31: Financial Reporting of Interests in Joint Ventures (319)IAS 32: Financial Instruments: Disclosure and Presentation (328)IAS 33: Earnings per Share (351)IAS 34: Interim Financial Reporting (365)IAS 35: Discontinuing Operations (376)IAS 36: Impairment of Assets (385)IAS 37: Provisions, Contingent Liabilities and Contingent Assets (410)IAS 38: Intangible Assets (426)IAS 39: Financial Instruments: Recognition and Measurement (452)IAS 40: Investment Property (504)IAS 41: Agriculture (520)Framework for the Preparation and Presentation of Financial Statements编制和呈报财务报表的基本框架The IASB Framework is a conceptual accounting framework that sets out the concepts that underlie the preparation and presentation of financial statements for external users. It was approved in 1989. The IASB Framework assists the IASB:l in the development of future International Accounting Standards and in its review of existing International Accounting Standards; andl in promoting the harmonisation of regulations, accounting standards and procedures relating to the presentation of financial statements by providing a basis for reducing the number of alternative accounting treatments permitted by International Accounting Standards.In addition, the Framework may assist:l preparers of financial statements in applying International Accounting Standards and in dealing with topics that have yet to form the subject of an International Accounting Standard;l auditors in forming an opinion as to whether financial statements conform with International Accounting Standards;l users of financial statements in interpreting the information contained in financial statements prepared in conformity with International Accounting Standards; andl those who are interested in the work of IASB, providing them with information about its approach to the formulation of accounting standards.The Framework is not an International Accounting Standard and does not define standards for any particular measurement or disclosure issue.In a limited number of cases there may be a conflict between the Framework and a requirement within an International Accounting Standard. In those cases where there is a conflict, the requirements of the International Accounting Standard prevail over those of the Framework.世界上许多企业都编制并且向外部使用者呈报财务报表。

正大集团新准则讲座

要点解读

– 不同存货可变现净值的确定 产成品、商品和用于出售的材料等直接用于出售的商品存货, 在正常生产经营过程中,应当以该存货的估计售价减去估计 的销售费用和相关税费后的金额确定其可变现净值。 用于生产的材料、在产品或自制半成品等需要经过加工的材 料存货,在正常生产经营过程中,应当以所生产的产成品的 估计售价减去至完工时估计将要发生的成本、估计的销售费 用以及相关税费后的金额确定其可变现净值。

16 IAS 18 Revenue IAS 19 Employee Benefits

IASs 1-41

IAS 20 Accounting for government grants and disclosure of government assistance

IAS 21 The effects of changes in foreign exchange rates IAS 23 Borrowing costs IAS 24 Related Party Disclosures IAS 26 Accounting and reporting by retirement benefit plans IAS 27 Consolidated and separate financial statements IAS 28 Investments in associates IAS 29 Financial reporting in hyperinflationary economics IAS 30 Disclosures in the financial statements of banks and

7

IFRS的全球运用状况

– 05年欧盟25国开始采用; – 06年将有100个国家和地区采用; – 估计2019年将有150国家和地区采用。

ifrs8国际财务报告准则8号

IFRS8 International Financial Reporting Standard8Operating SegmentsIn April2001the International Accounting Standards Board(IASB)adopted IAS14Segment Reporting,which had originally been issued by the International Accounting Standards Committee in August1997.IAS14Segment Reporting replaced IAS14Reporting Financial Information by Segment,issued in August1981.In November2006the IASB issued IFRS8Operating Segments to replace IAS14.IAS1 Presentation of Financial Statements(as revised in2007)amended the terminology used throughout IFRSs,including IFRS8.Other IFRSs have made minor consequential amendments to IFRS8.They include Improvements to IFRSs(issued April2009),IAS24Related Party Disclosures(issued November 2009),IFRS10Consolidated Financial Statements(issued May2011),IAS19Employee Benefits (issued June2011)and Annual Improvements to IFRSs2010–2012Cycle(issued December2013).IFRS Foundation A287IFRS8C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL FINANCIAL REPORTING STANDARD8OPERATING SEGMENTSCORE PRINCIPLE1 SCOPE2 OPERATING SEGMENTS5 REPORTABLE SEGMENTS11 Aggregation criteria12 Quantitative thresholds13 DISCLOSURE20 General information22 Information about profit or loss,assets and liabilities23 MEASUREMENT25 Reconciliations28 Restatement of previously reported information29 ENTITY-WIDE DISCLOSURES31 Information about products and services32 Information about geographical areas33 Information about major customers34 TRANSITION AND EFFECTIVE DATE35 WITHDRAWAL OF IAS1437 APPENDICESA Defined termB Amendments to other IFRSsFOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONAPPROVAL BY THE BOARD OF IFRS8ISSUED IN NOVEMBER2006BASIS FOR CONCLUSIONSAPPENDICESA Background information and basis for conclusions of the US FinancialAccounting Standards Board on SFAS131B Amendments to the Basis for Conclusions on other IFRSsDISSENTING OPINIONSIMPLEMENTATION GUIDANCEAPPENDIXAmendments to other Implementation GuidanceA288IFRS FoundationIFRS8 International Financial Reporting Standard8Operating Segments(IFRS8)is set out inparagraphs1–37and Appendices A and B.All the paragraphs have equal authority. Paragraphs in bold type state the main principles.Definitions of terms are given in the Glossary for International Financial Reporting Standards.IFRS8should be read in the context of its core principle and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8 Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.IFRS Foundation A289IFRS8IntroductionReasons for issuing the IFRSIN1International Financial Reporting Standard8Operating Segments sets out requirements for disclosure of information about an entity’s operating segmentsand also about the entity’s products and services,the geographical areas inwhich it operates,and its major customers.IN2Achieving convergence of accounting standards around the world is one of the prime objectives of the International Accounting Standards Board.In pursuit ofthat objective,the Board and the Financial Accounting Standards Board(FASB)in the United States have undertaken a joint short-term project with theobjective of reducing differences between International Financial ReportingStandards(IFRSs)and US generally accepted accounting principles(US GAAP)that are capable of resolution in a relatively short time and can be addressedoutside major projects.One aspect of that project involves the two boardsconsidering each other’s recent standards with a view to adopting high qualityfinancial reporting solutions.The IFRS arises from the IASB’s consideration ofFASB Statement No.131Disclosures about Segments of an Enterprise and RelatedInformation(SFAS131)issued in1997,compared with IAS14Segment Reporting,which was issued in substantially its present form by the IASB’s predecessorbody,the International Accounting Standards Committee,in1997.IN3The IFRS achieves convergence with the requirements of SFAS131,except for minor differences listed in paragraph BC60of the Basis for Conclusions.Thewording of the IFRS is the same as that of SFAS131except for changes necessaryto make the terminology consistent with that in other IFRSs.Main features of the IFRSIN4The IFRS specifies how an entity should report information about its operating segments in annual financial statements and,as a consequential amendment toIAS34Interim Financial Reporting,requires an entity to report selectedinformation about its operating segments in interim financial reports.It alsosets out requirements for related disclosures about products and services,geographical areas and major customers.IN5The IFRS requires an entity to report financial and descriptive information about its reportable segments.Reportable segments are operating segments oraggregations of operating segments that meet specified criteria.Operatingsegments are components of an entity about which separate financialinformation is available that is evaluated regularly by the chief operatingdecision maker in deciding how to allocate resources and in assessingperformance.Generally,financial information is required to be reported on thesame basis as is used internally for evaluating operating segment performanceand deciding how to allocate resources to operating segments.IN6The IFRS requires an entity to report a measure of operating segment profit or loss and of segment assets.It also requires an entity to report a measure ofA290IFRS FoundationIFRS8segment liabilities and particular income and expense items if such measuresare regularly provided to the chief operating decision maker.It requiresreconciliations of total reportable segment revenues,total profit or loss,totalassets,liabilities and other amounts disclosed for reportable segments tocorresponding amounts in the entity’s financial statements.IN7The IFRS requires an entity to report information about the revenues derived from its products or services(or groups of similar products and services),aboutthe countries in which it earns revenues and holds assets,and about majorcustomers,regardless of whether that information is used by management inmaking operating decisions.However,the IFRS does not require an entity toreport information that is not prepared for internal use if the necessaryinformation is not available and the cost to develop it would be excessive.IN8The IFRS also requires an entity to give descriptive information about the way the operating segments were determined,the products and services provided bythe segments,differences between the measurements used in reporting segmentinformation and those used in the entity’s financial statements,and changes inthe measurement of segment amounts from period to period.IN9An entity shall apply this IFRS for annual periods beginning on or after 1January2009.Earlier application is permitted.If an entity applies this IFRSfor an earlier period,it shall disclose that fact.Changes from previous requirementsIN10The IFRS replaces IAS14Segment Reporting.The main changes from IAS14are described below.Identification of segmentsIN11The requirements of the IFRS are based on the information about the components of the entity that management uses to make decisions aboutoperating matters.The IFRS requires identification of operating segments onthe basis of internal reports that are regularly reviewed by the entity’s chiefoperating decision maker in order to allocate resources to the segment andassess its performance.IAS14required identification of two sets ofsegments—one based on related products and services,and the other ongeographical areas.IAS14regarded one set as primary segments and the otheras secondary segments.IN12A component of an entity that sells primarily or exclusively to other operating segments of the entity is included in the IFRS’s definition of an operatingsegment if the entity is managed that way.IAS14limited reportable segmentsto those that earn a majority of their revenue from sales to external customersand therefore did not require the different stages of vertically integratedoperations to be identified as separate segments.Measurement of segment informationIN13The IFRS requires the amount reported for each operating segment item to be the measure reported to the chief operating decision maker for the purposes ofallocating resources to the segment and assessing its performance.IAS14IFRS Foundation A291IFRS8required segment information to be prepared in conformity with the accountingpolicies adopted for preparing and presenting the financial statements of theconsolidated group or entity.IN14IAS14defined segment revenue,segment expense,segment result,segment assets and segment liabilities.The IFRS does not define these terms,but requiresan explanation of how segment profit or loss,segment assets and segmentliabilities are measured for each reportable segment.DisclosureIN15The IFRS requires an entity to disclose the following information:(a)factors used to identify the entity’s operating segments,including thebasis of organisation(for example,whether management organises theentity around differences in products and services,geographical areas,regulatory environments,or a combination of factors and whethersegments have been aggregated),and(b)types of products and services from which each reportable segmentderives its revenues.IN16IAS14required the entity to disclose specified items of information about its primary segments.The IFRS requires an entity to disclose specified amountsabout each reportable segment,if the specified amounts are included in themeasure of segment profit or loss and are reviewed by or otherwise regularlyprovided to the chief operating decision maker.IN17The IFRS requires an entity to report interest revenue separately from interest expense for each reportable segment unless a majority of the segment’s revenuesare from interest and the chief operating decision maker relies primarily on netinterest revenue to assess the performance of the segment and to make decisionsabout resources to be allocated to the segment.IAS14did not require disclosureof interest income and expense.IN18The IFRS requires an entity,including an entity with a single reportable segment,to disclose information for the entity as a whole about its products andservices,geographical areas,and major customers.This requirement applies,regardless of the entity’s organisation,if the information is not included as partof the disclosures about segments.IAS14required the disclosure of secondarysegment information for either industry or geographical segments,tosupplement the information given for the primary segments.A292IFRS FoundationIFRS8 International Financial Reporting Standard8Operating SegmentsCore principle1An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects of the businessactivities in which it engages and the economic environments in which itoperates.Scope2This IFRS shall apply to:(a)the separate or individual financial statements of an entity:(i)whose debt or equity instruments are traded in a public market(a domestic or foreign stock exchange or an over-the-countermarket,including local and regional markets),or(ii)that files,or is in the process of filing,its financial statementswith a securities commission or other regulatory organisation forthe purpose of issuing any class of instruments in a publicmarket;and(b)the consolidated financial statements of a group with a parent:(i)whose debt or equity instruments are traded in a public market(a domestic or foreign stock exchange or an over-the-countermarket,including local and regional markets),or(ii)that files,or is in the process of filing,the consolidated financialstatements with a securities commission or other regulatoryorganisation for the purpose of issuing any class of instrumentsin a public market.3If an entity that is not required to apply this IFRS chooses to disclose information about segments that does not comply with this IFRS,it shall notdescribe the information as segment information.4If a financial report contains both the consolidated financial statements of a parent that is within the scope of this IFRS as well as the parent’s separatefinancial statements,segment information is required only in the consolidatedfinancial statements.Operating segments5An operating segment is a component of an entity:(a)that engages in business activities from which it may earn revenues andincur expenses(including revenues and expenses relating to transactionswith other components of the same entity),IFRS Foundation A293IFRS8(b)whose operating results are regularly reviewed by the entity’s chiefoperating decision maker to make decisions about resources to beallocated to the segment and assess its performance,and(c)for which discrete financial information is available.An operating segment may engage in business activities for which it has yet toearn revenues,for example,start-up operations may be operating segmentsbefore earning revenues.6Not every part of an entity is necessarily an operating segment or part of an operating segment.For example,a corporate headquarters or some functionaldepartments may not earn revenues or may earn revenues that are onlyincidental to the activities of the entity and would not be operating segments.For the purposes of this IFRS,an entity’s post-employment benefit plans are notoperating segments.7The term‘chief operating decision maker’identifies a function,not necessarily a manager with a specific title.That function is to allocate resources to and assessthe performance of the operating segments of an entity.Often the chiefoperating decision maker of an entity is its chief executive officer or chiefoperating officer but,for example,it may be a group of executive directors orothers.8For many entities,the three characteristics of operating segments described in paragraph5clearly identify its operating segments.However,an entity mayproduce reports in which its business activities are presented in a variety ofways.If the chief operating decision maker uses more than one set of segmentinformation,other factors may identify a single set of components asconstituting an entity’s operating segments,including the nature of thebusiness activities of each component,the existence of managers responsible forthem,and information presented to the board of directors.9Generally,an operating segment has a segment manager who is directly accountable to and maintains regular contact with the chief operating decisionmaker to discuss operating activities,financial results,forecasts,or plans for thesegment.The term‘segment manager’identifies a function,not necessarily amanager with a specific title.The chief operating decision maker also may bethe segment manager for some operating segments.A single manager may bethe segment manager for more than one operating segment.If thecharacteristics in paragraph5apply to more than one set of components of anorganisation but there is only one set for which segment managers are heldresponsible,that set of components constitutes the operating segments.10The characteristics in paragraph5may apply to two or more overlapping sets of components for which managers are held responsible.That structure issometimes referred to as a matrix form of organisation.For example,in someentities,some managers are responsible for different product and service linesworldwide,whereas other managers are responsible for specific geographicalareas.The chief operating decision maker regularly reviews the operatingresults of both sets of components,and financial information is available forboth.In that situation,the entity shall determine which set of componentsconstitutes the operating segments by reference to the core principle.A294IFRS FoundationIFRS8 Reportable segments11An entity shall report separately information about each operating segment that:(a)has been identified in accordance with paragraphs5–10or results fromaggregating two or more of those segments in accordance withparagraph12,and(b)exceeds the quantitative thresholds in paragraph13.Paragraphs14–19specify other situations in which separate information aboutan operating segment shall be reported.Aggregation criteria12Operating segments often exhibit similar long-term financial performance if they have similar economic characteristics.For example,similar long-termaverage gross margins for two operating segments would be expected if theireconomic characteristics were similar.Two or more operating segments may beaggregated into a single operating segment if aggregation is consistent with thecore principle of this IFRS,the segments have similar economic characteristics,and the segments are similar in each of the following respects:(a)the nature of the products and services;(b)the nature of the production processes;(c)the type or class of customer for their products and services;(d)the methods used to distribute their products or provide their services;and(e)if applicable,the nature of the regulatory environment,for example,banking,insurance or public utilities.Quantitative thresholds13An entity shall report separately information about an operating segment that meets any of the following quantitative thresholds:(a)Its reported revenue,including both sales to external customers andintersegment sales or transfers,is10per cent or more of the combinedrevenue,internal and external,of all operating segments.(b)The absolute amount of its reported profit or loss is10per cent or moreof the greater,in absolute amount,of(i)the combined reported profit ofall operating segments that did not report a loss and(ii)the combinedreported loss of all operating segments that reported a loss.(c)Its assets are10per cent or more of the combined assets of all operatingsegments.Operating segments that do not meet any of the quantitative thresholds may beconsidered reportable,and separately disclosed,if management believes thatinformation about the segment would be useful to users of the financialstatements.IFRS Foundation A295IFRS814An entity may combine information about operating segments that do not meet the quantitative thresholds with information about other operating segmentsthat do not meet the quantitative thresholds to produce a reportable segmentonly if the operating segments have similar economic characteristics and share amajority of the aggregation criteria listed in paragraph12.15If the total external revenue reported by operating segments constitutes less than75per cent of the entity’s revenue,additional operating segments shall beidentified as reportable segments(even if they do not meet the criteria inparagraph13)until at least75per cent of the entity’s revenue is included inreportable segments.16Information about other business activities and operating segments that are not reportable shall be combined and disclosed in an‘all other segments’categoryseparately from other reconciling items in the reconciliations required byparagraph28.The sources of the revenue included in the‘all other segments’category shall be described.17If management judges that an operating segment identified as a reportable segment in the immediately preceding period is of continuing significance,information about that segment shall continue to be reported separately in thecurrent period even if it no longer meets the criteria for reportability inparagraph13.18If an operating segment is identified as a reportable segment in the current period in accordance with the quantitative thresholds,segment data for a priorperiod presented for comparative purposes shall be restated to reflect the newlyreportable segment as a separate segment,even if that segment did not satisfythe criteria for reportability in paragraph13in the prior period,unless thenecessary information is not available and the cost to develop it would beexcessive.19There may be a practical limit to the number of reportable segments that an entity separately discloses beyond which segment information may become toodetailed.Although no precise limit has been determined,as the number ofsegments that are reportable in accordance with paragraphs13–18increasesabove ten,the entity should consider whether a practical limit has been reached. Disclosure20An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects of the businessactivities in which it engages and the economic environments in which itoperates.21To give effect to the principle in paragraph20,an entity shall disclose the following for each period for which a statement of comprehensive income ispresented:(a)general information as described in paragraph22;A296IFRS FoundationIFRS8(b)information about reported segment profit or loss,including specifiedrevenues and expenses included in reported segment profit or loss,segment assets,segment liabilities and the basis of measurement,asdescribed in paragraphs23–27;and(c)reconciliations of the totals of segment revenues,reported segmentprofit or loss,segment assets,segment liabilities and other materialsegment items to corresponding entity amounts as described inparagraph28.Reconciliations of the amounts in the statement of financial position forreportable segments to the amounts in the entity’s statement of financialposition are required for each date at which a statement of financial position isrmation for prior periods shall be restated as described inparagraphs29and30.General information22An entity shall disclose the following general information:(a)factors used to identify the entity’s reportable segments,including thebasis of organisation(for example,whether management has chosen toorganise the entity around differences in products and services,geographical areas,regulatory environments,or a combination of factorsand whether operating segments have been aggregated);(aa)the judgements made by management in applying the aggregation criteria in paragraph12.This includes a brief description of theoperating segments that have been aggregated in this way and theeconomic indicators that have been assessed in determining that theaggregated operating segments share similar economic characteristics;and(b)types of products and services from which each reportable segmentderives its revenues.Information about profit or loss,assets and liabilities23An entity shall report a measure of profit or loss for each reportable segment.An entity shall report a measure of total assets and liabilities for each reportablesegment if such amounts are regularly provided to the chief operating decisionmaker.An entity shall also disclose the following about each reportablesegment if the specified amounts are included in the measure of segment profitor loss reviewed by the chief operating decision maker,or are otherwiseregularly provided to the chief operating decision maker,even if not included inthat measure of segment profit or loss:(a)revenues from external customers;(b)revenues from transactions with other operating segments of the sameentity;(c)interest revenue;(d)interest expense;(e)depreciation and amortisation;IFRS Foundation A297IFRS8(f)material items of income and expense disclosed in accordance withparagraph97of IAS1Presentation of Financial Statements(as revised in2007);(g)the entity’s interest in the profit or loss of associates and joint venturesaccounted for by the equity method;(h)income tax expense or income;and(i)material non-cash items other than depreciation and amortisation.An entity shall report interest revenue separately from interest expense for eachreportable segment unless a majority of the segment’s revenues are frominterest and the chief operating decision maker relies primarily on net interestrevenue to assess the performance of the segment and make decisions aboutresources to be allocated to the segment.In that situation,an entity may reportthat segment’s interest revenue net of its interest expense and disclose that ithas done so.24An entity shall disclose the following about each reportable segment if the specified amounts are included in the measure of segment assets reviewed bythe chief operating decision maker or are otherwise regularly provided to thechief operating decision maker,even if not included in the measure of segmentassets:(a)the amount of investment in associates and joint ventures accounted forby the equity method,and(b)the amounts of additions to non-current assets1other than financialinstruments,deferred tax assets,net defined benefit assets(see IAS19Employee Benefits)and rights arising under insurance contracts. Measurement25The amount of each segment item reported shall be the measure reported to the chief operating decision maker for the purposes of making decisions aboutallocating resources to the segment and assessing its performance.Adjustmentsand eliminations made in preparing an entity’s financial statements andallocations of revenues,expenses,and gains or losses shall be included indetermining reported segment profit or loss only if they are included in themeasure of the segment’s profit or loss that is used by the chief operatingdecision maker.Similarly,only those assets and liabilities that are included inthe measures of the segment’s assets and segment’s liabilities that are used bythe chief operating decision maker shall be reported for that segment.Ifamounts are allocated to reported segment profit or loss,assets or liabilities,those amounts shall be allocated on a reasonable basis.26If the chief operating decision maker uses only one measure of an operating segment’s profit or loss,the segment’s assets or the segment’s liabilities inassessing segment performance and deciding how to allocate resources,segmentprofit or loss,assets and liabilities shall be reported at those measures.If the 1For assets classified according to a liquidity presentation,non-current assets are assets that include amounts expected to be recovered more than twelve months after the reporting period.A298IFRS FoundationIFRS8chief operating decision maker uses more than one measure of an operatingsegment’s profit or loss,the segment’s assets or the segment’s liabilities,thereported measures shall be those that management believes are determined inaccordance with the measurement principles most consistent with those used inmeasuring the corresponding amounts in the entity’s financial statements.27An entity shall provide an explanation of the measurements of segment profit or loss,segment assets and segment liabilities for each reportable segment.At aminimum,an entity shall disclose the following:(a)the basis of accounting for any transactions between reportablesegments.(b)the nature of any differences between the measurements of thereportable segments’profits or losses and the entity’s profit or loss beforeincome tax expense or income and discontinued operations(if notapparent from the reconciliations described in paragraph28).Thosedifferences could include accounting policies and policies for allocationof centrally incurred costs that are necessary for an understanding of thereported segment information.(c)the nature of any differences between the measurements of thereportable segments’assets and the entity’s assets(if not apparent fromthe reconciliations described in paragraph28).Those differences couldinclude accounting policies and policies for allocation of jointly usedassets that are necessary for an understanding of the reported segmentinformation.(d)the nature of any differences between the measurements of thereportable segments’liabilities and the entity’s liabilities(if not apparentfrom the reconciliations described in paragraph28).Those differencescould include accounting policies and policies for allocation of jointlyutilised liabilities that are necessary for an understanding of thereported segment information.(e)the nature of any changes from prior periods in the measurementmethods used to determine reported segment profit or loss and theeffect,if any,of those changes on the measure of segment profit or loss.(f)the nature and effect of any asymmetrical allocations to reportablesegments.For example,an entity might allocate depreciation expense toa segment without allocating the related depreciable assets to thatsegment.Reconciliations28An entity shall provide reconciliations of all of the following:(a)the total of the reportable segments’revenues to the entity’s revenue.(b)the total of the reportable segments’measures of profit or loss to theentity’s profit or loss before tax expense(tax income)and discontinuedoperations.However,if an entity allocates to reportable segments itemsIFRS Foundation A299。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Factors considered in identifying geographical segments include:

similarity of economic and political conditions; relationships between operations in different geographical areas; proximity of operations; special risks associated with operations in a particular area; exchange control regulations; and the underlying currency risks.

better understand the enterprise's past performance; better assess the enterprise's risks and returns; and make more informed judgments about the enterprise as a whole.

Identifying Reportable Segments

50%

The enterprise's reportable segments are business and geographical segments for which a majority of their revenue is earned from sales to external customers .

Definition

Segment revenue

Revenue, including intersegment revenue, that is directly attributable or reasonably allocable to a segment.

Segment revenue does not include:

Definition

Segment expense

Expenses, including expenses relating to intersegment transactions, that (a) result from operating activities and (b) are directly attributable or reasonably allocable to a segment.

Identifying Reportable Segments

75%

If total external revenue attributable to reportable segments is less than 75% of the total consolidated or enterprise revenue, additional segments should be identified as reportable segments until at least 75% of total consolidated or enterprise revenue is included in reportable segments.

extraordinary items; interest or dividend income, including interest earned on advances or loans to other segments,unless the segment's operations are primarily of a financial nature; or gains on sales of investments or gains on extinguishment of debt unless the segment's operations are primarily of a financial nature.

Definition

Business Segment

A component of an enterprise that (a) provides a single product or service or a group of related products and services and (b) that is subject to risks and returns that are different from those of other business segments.

The objective of this Standard is to establish principles for reporting financial information by segment—information about the different types of products and services an enterprise produces and the different geographical areas in which it operates—to help users of financial statements:

Definition

A reportable segment is a business segment or a geographical segment identified based on the foregoing definitions for which segment information is required to be disclosed by this Standard.

1983.1.1

Effective Date of IAS 14 (1981)

1994

IAS 14 (1981) was reformatted

1997.8

IAS 14 Segment Reporting

1998.7.1

Date of IAS 14 (1997)

Objective

Identifying Reportable Segments

10%

revenue from sales to external customers and from transactions with other segments is 10% or more of the total revenue, external and internal, of all segments; segment result, whether profit or loss, is 10% or more the combined result of all segments in profit or the combined result of all segments in loss, whichever is greater in absolute amount; or assets are 10% or more of the total assets of all segments.

Definition

Segment Expense

an enterprise's share of losses of associates, joint ventures, or other investments accounted for under the equity method; income tax expense; or general administrative expenses, head-office expenses, and other expenses that arise at the enterprise level and relate to the enterprise as a whole.

Definition

Geographical Segment

A component of an enterprise that (a) provides products and services within a particular economic environment and (b) that is subject to risks and returns that are different from those of components operating in other economic environments.

Definition

Segment Result

segment revenue less segment expense. Segment result is determined before any adjustments for minority interest.

Segment Assets and Segment Liabilities

Segment expense does not include:

extraordinary items; interest, including interest incurred on advances or loans from other segments, unless the segment's operations are primarily of a financial nature; losses on sales of investments or losses on extinguishment of debt unless the segment's operations are primarily of a financial nature;

International Accounting Standards