财务成本管理英语

财务管理英语词汇

financial management 财务管理chief financial officer 首席财务官hurdle rate 最低报酬率capital structure 资本结构cash dividend 现金股利dividend-payout ratio 股利支付率financial risk 财务风险earnings per share 每股盈余net present value 净现值stock option 股票期权earnings per share 每股收益time value of money 货币时间价值simple interest 单利annuity 年金future value 终值present value 现值compound interest 复利capital 本金d iscount rate 折现率opportunity cost 机会成本cost of capital 资本成本ordinary annuity 普通年金annuity due 先付年金deferred annuity 递延年金perpetuity 永续年金liquidity ratio 流动性比率nominal interest rate 名义利率marker value 市场价值intrinsic value 内在价值discounted cash flow valuation 折现现金流量模型earnings before interest and taxes 息税前利润par value 票面价值dividend payout 股利支付率dividend discount model 股利折现模型diversifiable risk可分散风险market risk 市场风险expected return 期望收益volatility 流动性权益融资equity financial债务融资debt financial利润最大化profit maximization股东财富最大化shareholders wealth maximization 每股收益最大化maximization of earning per share 11、投资报酬return on investment风险溢价risk premium货币市场money market偿债基金sinking fund1.financial markets 金融市场2.资本结构capital structure3.risk premium 风险报酬4.净现金流量net cash flow5.credit policy 信用政策6.终值future value7.moral hazard 道德风险8.收账政策collection policy1.chief financial officer 首席财务官2.财务管理financial management3.credit standard 信用标准4.流动性liquidity5.earnings before interest and taxes 息税前利润6.市场价值market value7.capital assets pricing model资本资产定价模型8.每股收益earnings per share。

财经英语单词--财务成本管理

PART I Fundamentals to Financial Management第一部分财务管理导论Section I Fundamentals to Financial Management第一节财务管理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财富最大化e.g. Shareholder wealth maximization is a fundamental principle of financial management. In financial management we assume that the objective of the business is to maximize shareholder wealth. This is not necessarily the same as maximizing profit.【讲解】(1)maximization[,mæksimai'zeiʃən]n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-]n.最小化(3)maximize['mæksɪmaɪz]v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量 adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量 adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回顾【译】股东财富最大化是财务管理的基本原则。

在财务管理中我们假定企业的目标就是实现股东财富最大化。

中英文对照,专业名词,财务成本管理

中英文对照,专业名词,财务成本管理第一部分财务治理导论Section I Fundamentals to Financial Management第一节财务治理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财宝最大化e.g. Shareholder wealth maximization is a fundamental principle of fi nancial management. In financial management we assume that the objectiv e of the business is to maximize shareholder wealth. This is not necessari ly the same as maximizing profit.【讲解】(1)maximization [,mæksimai'zeiʃən] n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-] n.最小化(3)maximize ['mæksɪmaɪz] v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回忆【译】股东财宝最大化是财务治理的差不多原则。

在财务治理中我们假定企业的目标确实是实现股东财宝最大化。

中英文对照,专业名词,财务成本管理(完整版)

PART I Fundamentals to Financial Management第一部分财务管理导论Section I Fundamentals to Financial Management第一节财务管理概述1.profit maximization*利润最大化1-1 EPS maximization* 每股收益最大化【讲解】EPS, earnings per share 每股收益1-2 Maximization of shareholders wealth* 股东财富最大化e.g. Shareholder wealth maximization is a fundamental principle of financial management. In financial management we assume that the objective of the business is to maximize shareholder wealth. This is not necessarily the same as maximizing profit.【讲解】(1)maximization[,mæksimai'zeiʃən]n.最大化,极大化(2)minimization [,minimai'zeiʃən, -mi'z-]n.最小化(3)maximize['mæksɪmaɪz]v. 最大化,取……最大值,达到最大值(4)minimize ['mɪnɪmaɪz] v. 最小化(5)minimum n.最小值,最小量 adj.最小的,最低的(6)maximum n. 极大,最大限度,最大量 adj.最高的,最多的(7)the same as 和……一样,与……相同学习成果回顾【译】股东财富最大化是财务管理的基本原则。

在财务管理中我们假定企业的目标就是实现股东财富最大化。

财务成本管理英语08

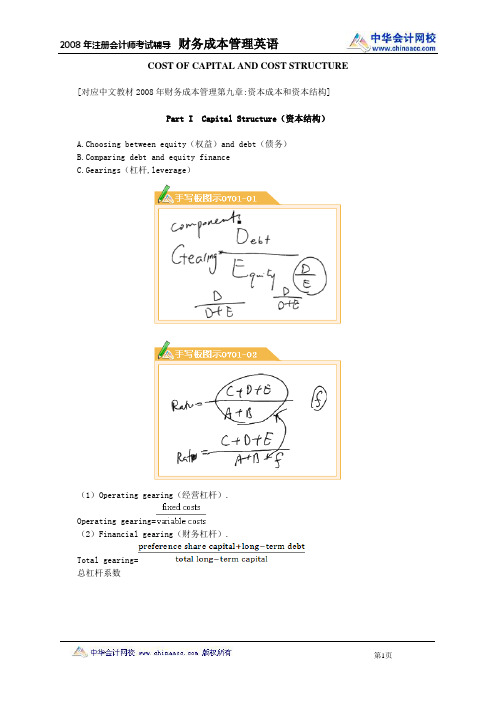

COST OF CAPITAL AND COST STRUCTURE [对应中文教材2008年财务成本管理第九章:资本成本和资本结构]Part I Capital Structure(资本结构)A.Choosing between equity(权益)and debt(债务)paring debt and equity financeC.Gearings(杠杆,leverage)(1)Operating gearing(经营杠杆).Operating gearing=(2)Financial gearing(财务杠杆).Total gearing=总杠杆系数Equity gearing=Income gearing=收入杠杆系数Here debt interest includes preference dividend.(利息金额包含优先股股利在内)D. Weighted Average Cost of Capital(WACC)(加权平均资本成本)Part II Cost of Capital(资本成本)1.The cost of equity, the cost of debt and the weighted average cost of capital1.1 The concept of a weighted average cost of capitalCost of equityCost of debtIrredeemableRedeemable K is the IRR of the related flows: initial market value, annual interestfinal redemption.1.2 Market or book weights(市值或账面价值)ExampleThe accounts of Apollo plc reveal(揭示)the following capital structure: Ordinary shares 2,000,000Reserves 3,000,00010% debentures 1,000,0006,000,000Market values of the above are as follows:Ordinary shares 3.75 each ex div(除权)Debenture stock 80The cost of equity is estimated to be 20%, the cost of debt is 7.5%(after tax).What is the weighted average cost of capital using book weights?SolutionEquity(ordinary shares+reserves)2000000+3000000 5000000Debt 1000000Total 6000000Proportions 5/6 Equity 1/6 DebtCombined cost of capital(5/6 x 20%)+(1/6 x 7.5%)= 17.92%3.Operating gearing(经营杠杆)Operating gearing(also called operational gearing)measures the cost structure(fixed and variable)of the firm. Firms with high levels of fixed costs are usually described as having high operating gearing.经营杠杆度量的是公司的成本结构,即固定成本和变动成本之间的关系.固定成本占比较大的公司称之为经营杠杆系数较高.Firms with high operating gearing are risky as fixed cost payments must be made no matter the level of contribution.具有较高经营杠杆系数的公司风险较大,原因在于无论边际贡献如何,均须承担相关固定成本.ExampleConsider two firms:Firm A Firm Bm mSales 5 5Variable costs 3 1Fixed costs 1 3EBIT(Earnings before interest and tax)1 1What would be the impact(影响)of a 10% increase in sales volume on the EBIT of each firm?Firm A New EBIT=(5m-3m)×1.1-1=1.2m i.e. a 20% increase.Firm B New EBIT=(5m-1m)×1.1-3=1.4m i.e. a 40% increase.Operating gearingFirmA FirmBAlternatively:FirmA FirmBB carries a higher operating gearing because it has higher fixed costs. Its operating earnings are more volume sensitive.公司B具有较高的经营杠杆系数,因为其固定成本占比较高.它的经营收入具有数量敏感性.Part III Further Aspects of WACC(加权平均成本的进一步探究)3 CAPM and the cost of capital3.1 Modigliani and Miller 1963In a world with corporation tax the benefit to the general company of the tax shield on debt interest must be included in our analysis. Thus:Assuming debt is risk free and that β debt is therefore zero:=0假定债务无风险,故βdebtDiscount rates for capital investment appraisal should be related to the systematic risk of the project in question. In a similar way it could also be argued that they ought also to be related to the gearing level of the project.资本投资评价使用的折现率应反映该项目的系统风险.同样地其也应反映该项目的杠杆水平.ExampleHubbard, an all equity(融资方式为权益资金))food manufacturing firm, is about to embark (转型)upon a major diversification in the consumer electronics industry(电子行业). Its current equity beta is 1.2, whilst the average equity βof electronics firms is 1.6. Gearing in the electronics industry averages 30% debt, 70% equity. Corporate debt is considered to be risk free.R m =25%, Rf=10%, corporation tax rate=30%(notation as before).Required:What would be a suitable discount rate for the new investment if Hubbard were to finance the new project in each of the following ways?问:若该公司采用下述融资结构以支持此新项目,则合适的折现率是多少?(a)Entirely by equity(b)By 30% debt and 70% equity(c)By 40% debt and 60% equity?SolutionIn all three situations the best approach is to treat the project as a 'mini-firm' and tailor(调整,修改)the discount rate to reflect its level of systematic business risk and financial risk(财务风险).(a)Project financed entirely by equityTo reflect the business risk of the new venture we should start with the equity ,βof the electronics industry, i.e. 1.6.As our project is to be ungeared we should then remove the financial risk element.The pure cost of equity(and hence WACC in the all equity ease)would then be:The project should be evaluated at a rate of 28.45%.(b)Project financed by 30% debt, 70% equityIn this case the observed equity beta of the electronics industry would reflect the level of business risk and financial risk of the project. No adjustments are therefore required.在此情况下电子行业的β系数反应了该项目的商业风险和财务风险.无需进一步调整.To obtain a suitable discount rate we must simply weight the cost of equity and the cost of debt, hence:Suitable discount rate for project=(34%×0.7)+(7%×0.3)=25.9%(c)Project financed by 40% debt and 60% equityIn this case the equity beta of the electronics industry reflects a lower level of gearing than that for the proposed project. The simplest procedure is to take a two step approach to the gearing adjustment.Step 1 Calculate the equity beta for an ungeared electronics company(as in(a)).β=1.23equity ungearedThis is a measure of the pure systematic risk of electronics companies.We now adjust this pure beta in the light of the given financial gearing ratio.Step 2 Work out the equation 'backwards' to calculate the cost of equity for an electronics company with 60% equity and 40% debtThe cost of equity for such a firm would then be:The cost of dcbt would be as before.And suitable discount rate for the project would be:风险调整后净现值(risk adjusted NPV)。

2021 年注册会计师《财务成本管理英语》资本成本与资本结构

第01讲资本成本与资本结构Part 1 核心词汇Part 2 重难点讲解—资本成本(一)普通股成本的估计(二)优先股成本的估计(三)债务成本的估计特殊债券的成本估计(四)加权平均资本成本(WACC)【例题·2017年考题】甲公司为扩大产能,拟平价发行分离型附认股权证债券进行筹资,方案如下:债券每份面值1000元,期限5年,票面利率5%。

每年付息一次。

同时附送20份认股权证。

认股权证在债券发行3年后到期,到期时每份认股权证可按11元的价格购买1股甲公司普通股股票。

甲公司目前有发行在外的普通债券,5年后到期,每份面值1000元,票面利率6%,每年付息一次,每份市价1020元(刚刚支付过最近一期利息)公司目前处于生产的稳定增长期,可持续增长率5%。

普通股每股市价10元。

公司企业所得税率25%。

要求:(1)计算公司普通债券的税前资本成本。

(2)计算分离型附认股权证债券的税前资本成本。

(3)判断筹资方案是否合理,并说明理由,如果不合理,给出调整建议。

『正确答案』(1)令税前资本成本为iAssume Pre-tax cost of capital is i1020=1000×6%×(P/A,i,5)+1000×(P/F,i,5)当i=4%时,等式右边=1000×6%×4.4518+1000×0.8219=1089When i equals 4%, the right side of the equation=1000×6%×4.4518+1000×0.8219=1089 continuing当i=6%时, 等式右边=1000×6%×4.2124+1000×0.7473=1000When i equals 6%, the right side of the equation =1000×6%×4.2124+1000×0.7473=1000 列出等式:Write out the equality :(i-4%)/(6%-4%)=(1020-1089)/(1000-1089)i=4%+[(1020-1089)/(1000-1089)]×(6%-4%)=5.55%(2)第3年末行权支出=11×20=220(元)Exercise expenditure at the end of the third year=11×20=220(yuan )取得股票的市价=10×(F/P,5%,3)×20=231.525(元)The market price of the acquired stock=10×(F/P,5%,3)×20=231.525(yuan )行权现金净流入=231.5325-220=11.525(元)Net cash inflow when option are exercised= 231.5325-220=11.525(yuan )令税前资本成本为k,Assume Pre-tax cost of capital is K1000=1000×5%×(P/A,K,5)+11.525×(P/F,K,3)+1000×(P/F,K,5)K=5%时,等式右边=1000×5%×4.3295+11.525×0.8638+1000×0.7835=1009.93(元)When K equals 5%, the right side of the equation =……K=6%时,等式右边=1000×5%×4.2124+11.525×0.8396+1000×0.7473=967.60(元)When K equals 6%, the right side of the equation =……(K-5%)/(6%-5%)=(1000-1009.93)/(967.60-1009.93)K=5%+[(1000-1009.93)/(967.60-1009.93)]×(6%-5%)=5.23%(3)该筹资方案不合理,原因是附认股权证债券的税前资本成本低于普通债券的税前资本成本。

财务管理专业英语(吐血整理)

Topic1:1、Financial management is an integrated decision-making process concerned with acquiring, financing, and managing assets to accomplish some overall goal within a business entity.财务管理是为了实现一个公司总体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

2、Making financial decisions is an integral part of all forms and sizes of business organizations from small privately-hold forms to large publicly-traded corporations.做财务决策对于所有形式和规模的商业组织,无论是小型私人公司还是大型公开上市公司,都是不可分割的一部分。

3、In today’s rapidly changing environment, the financ ial manager must have the flexibility to adapt to external factors such as economic uncertainty, global competition, technological change, volatility of interest and exchange rates, changes in laws and regulations, and ethical concerns.在当今瞬息万变的环境中,财务经理必须具备足够的灵活性以适应外部因素,如经济的不确定性、国际竞争、技术变革、利息波动、汇率变动、法律法规变化以及商业道德问题。

财务成本管理英语

INVESTMENT APPRAISAL[对应中文教材2008年财务成本管理第五章:投资管理](已动用资本回报率)or ARR(会计收益率)(Accounting Rate of Return)(回收期法)Payback period=Initial payment/Annual cash inflow, payback is not always an exact number of years Most common formula:ROCE=EBIT (after depreciation)/ initial capital costsC NPV(净现值法)(1) Basic assumptions:·cash outlay occurs in year 0 (now).·cash flows occur at the end of the year.·if a cash flow occurs at the beginning of a year, it is assumed to occur at the end of the previous year.D IRR(内含报酬率法)(1)Basic principle: IRR is the cost of capital at which the NPV is zero, if the expected IRR is higher than a target rate of return; the project is financially worth undertaking.(2)Selection between IRR and NPV: when a choice has to be made between mutually exclusive projects, in such case the NPV should be selected, because higher NPV can maximize shareholder’s wealth.DefinitionThe discount rat which, when applied to the cash flows of a project, gives an NPV of zero.OrThe break-even interest rate for a project.It is the maximum rate of interest that you could afford to pay on a project without making a loss.FeaturesAdvantages -Takes into account the time value of money-Relative measure-More readily understood than NPVDisadvantages -May not be unique – projects can have more than one IRR- May rank projects incorrectly – for mutually exclusive projects or whenFunds are short supply- Cannot cope with changing rates of interestThe method of calculation depends upon whether or not the project has even cash flows.Even cash flowsConsider an investment of £ that generates net cash earnings of £10m for 5 years The IRR is the discount rate that gives a NPV of zero. This means that the IRR is the Rate that will discount five installments of £10m to a present value of £. This in turnMeans that the IRR is the discount rate for which the 5year annuity factor is . A The project’s IRR has been found via a cumulative discount fac tor (annuity factor)givenBy:Annuity factorat the IRR=for the life of the projectUneven cash flowsThese have to be found by trial and error or by estimating using two present values.Where:A=lower rate chosen=NPV at rate AB=higher rate=NPV at rate BIt helps to get A and B as close to the true IRR as possible, but it doesn’t matter whetherthe resultant NPVs are positive, negative or one of each.Some students prefer to use a common sense approach rather than a formula. Seeing by nowMuch NPV has fallen (from to) as the discount rate has risen from A to B, They find how much more the discount rate needs to rise to bring the NPV to zero.Whether the formula is used or common sense, the calculation assumes a linear relationshipBetween NPV and discount rate. In fact the relationship is not linear, hence the calculationIs only approximate and (unless you have been lucky when guessing which discount rates touse)you should not quote IRR’s calculated in this way to many, not to any,decimal places –unless the examiner asks you.IRR of a perpetuityThe present value of a perpetuity is the annual cash flow divided by the discount rate (expressed as a decimal. From this it follows that:the IRR of a perpetuity ==100Perpetuity: 永续年金Method of presentationA simple calculation such as those for Woods can be done on a single line. For larger projectstwo possibilities exist:(i) the cash budget approach(ii) the tabular approach.(1)Cash budget approachTime 0 1 2 3£’000£’000£’000£’000Investment (X)—— XAdvertising (X)(X) - -Working capital (X)- - XMaterials (X)(X)(X)-Labour —(X)(X)(X)Overheads —(X)(X)(X)Revenue ———X————Net cash flow (X)(X)(X) X————y% Discount factor 1 X X XPresent value (X)(X)(X)XNet present value (£’000)XThe cash budget approach is suitable for short projects with lots of different cash flowsWhich change from year to year.(2) Tabular approachTime Cash flow y% Discount Present value£’000£’000£’0000 Investment (X) 1 (X)0 and 1 Advertising (X)X (X)0 Working capital (X) 1 (X)0-9 Materials (X) 1 (X)1-10 Labour and overheads (X)X (X)1-10 Revenue X X X10 Sales proceeds X X X10 WC recovery X X X—Net present value (£’000)XThe tabular approach is suitable for long projects with lots of different cash flows that areThe same from year to year (enabling annuity factors to be used).Picking the right figuresWhen carrying out discounted cash flow analysis it is important to select the right figures.Ignore:costs – amounts that have already been spent– not a cash flowvalues – not a cash flow–incremental fixed costs (look out for the words “reapportioned fixed overheads”) costs – taken into account by the discounting processInclude:Those cash flows that are specifically received or incurred as a result of the acceptance of the project(future–incremental–cash flows).Asset replacement decisionFactors to be considered when making replacement decision are as follows:·capital cost of new equipment;·operating costs, increased repair and maintenance costs;loss of productivity;lower of quality and quantity of output;One application of discounted cash flow is to make decisions concerned with the replacement ofMachinery. This applies to short – life assets that will need to be replaced in perpetuity (. motorCars or photocopiers). As a machine gets older, it is likely to cost more to keep it running and itsScrap value will decrease. The aim is to find the optimal replacement cycle for the machine,. how often it should be replaced - before it becomes uneconomic to own.A simple approach would involve finding the total cost of keeping an asset for 1,2,3 years, etc,Then finding an average annual cost.DCF VersionNow, each possible replacement cycle is treated as a project (1-year, 2-year, or 3-year project).You calculate the NPV of each project (rather than just the total cost).Instead of dividing the NPV’s by 1,2,or 3, they’re divided by the 1,2, or 3-year annuity factorTo find an equivalent annual cost.Equivalent annual cost =。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

财务成本管理英语 Company number:【0089WT-8898YT-W8CCB-BUUT-202108】INVESTMENT APPRAISAL[对应中文教材2008年财务成本管理第五章:投资管理](已动用资本回报率)or ARR(会计收益率)(Accounting Rate of Return)(回收期法)Payback period=Initial payment/Annual cash inflow, payback is not always an exact number of years Most common formula:ROCE=EBIT (after depreciation)/ initial capital costsC NPV(净现值法)(1) Basic assumptions:·cash outlay occurs in year 0 (now).·cash flows occur at the end of the year.·if a cash flow occurs at the beginning of a year, it is assumed to occur at the end of the previous year.D IRR(内含报酬率法)(1)Basic principle: IRR is the cost of capital at which the NPV is zero, if the expected IRR is higher than a target rate of return; the project is financially worth undertaking.(2)Selection between IRR and NPV: when a choice has to be made between mutually exclusive projects, in such case the NPV should be selected, because higher NPV can maximize sharehold er’s wealth.DefinitionThe discount rat which, when applied to the cash flows of a project, gives an NPV of zero.OrThe break-even interest rate for a project.It is the maximum rate of interest that you could afford to pay on a project without making a loss.FeaturesAdvantages -Takes into account the time value of money-Relative measure-More readily understood than NPVDisadvantages -May not be unique – projects can have more than one IRR- May rank projects incorrectly – for mutually exclusive projects or whenFunds are short supply- Cannot cope with changing rates of interestThe method of calculation depends upon whether or not the project has even cash flows.Even cash flowsConsider an investment of £ that generates net cash earnings of £10m for 5 years The IRR is the discount rate that gives a NPV of zero. This means that the IRR istheRate that will discount five installments of £10m to a present value of £. Thisin turnMeans that the IRR is the discount rate for which the 5year annuity factor is . A The project’s IRR has been found via a cumulative discount factor (annuityfactor) givenBy:Annuity factorat the IRR=for the life of the projectUneven cash flowsThese have to be found by trial and error or by estimating using two present values.Where:A=lower rate chosen=NPV at rate AB=higher rate=NPV at rate BIt helps to get A and B as close to the true IRR as possible, but it doesn’tmatter whetherthe resultant NPVs are positive, negative or one of each.Some students prefer to use a common sense approach rather than a formula. Seeingby nowMuch NPV has fallen (from to) as the discount rate has risen from A to B, They find how much more the discount rate needs to rise to bring the NPV to zero.Whether the formula is used or common sense, the calculation assumes a linear relationshipBetween NPV and discount rate. In fact the relationship is not linear, hence the calculationIs only approximate and (unless you have been lucky when guessing which discount rates touse)you should not quote IRR’s calculated in this way to many, not toany,decimal places –unless the examiner asks you.IRR of a perpetuityThe present value of a perpetuity is the annual cash flow divided by the discount rate(expressed as a decimal. From this it follows that:the IRR of a perpetuity ==100Perpetuity: 永续年金Method of presentationA simple calculation such as those for Woods can be done on a single line. For larger projectstwo possibilities exist:(i) the cash budget approach(ii) the tabular approach.(1)Cash budget approachTime012 3£’000£’000£’000£’000Investment(X)—— XAdvertising(X)(X) --Working capital(X)--XMaterials (X)(X)(X)-Labour —(X)(X)(X)Overheads —(X)(X)(X)Revenue ———X————Net cash flow (X)(X)(X) X————y% Discount factor1X X XPresent value(X)(X)(X)XNet present value (£’000)XThe cash budget approach is suitable for short projects with lots of different cash flowsWhich change from year to year.(2) Tabular approachTime Cash flow y% Discount Present value£’000£’000£’000 0Investment(X)1(X)0and 1 Advertising(X)X(X)0Working capital(X)1(X)0-9Materials(X)1(X)1-10Labour and overheads(X)X(X)1-10Revenue X X X10Sales proceeds X X X10WC recovery X X X—Net present value (£’000)XThe tabular approach is suitable for long projects with lots of different cash flows that areThe same from year to year (enabling annuity factors to be used).Picking the right figuresWhen carrying out discounted cash flow analysis it is important to select the right figures.Ignore:costs – amounts that have already been spent– not a cash flowvalues – not a cash flow–incremental fixed costs (look out for the words “reapportioned fixed overheads”)costs – taken into account by the discounting processInclude:Those cash flows that are specifically received or incurred as a result of the acceptance of the project(future–incremental–cash flows).Asset replacement decisionFactors to be considered when making replacement decision are as follows:·capital cost of new equipment;·operating costs, increased repair and mai ntenance costs;loss of productivity;lower of quality and quantity of output;One application of discounted cash flow is to make decisions concerned with the replacement ofMachinery. This applies to short – life assets that will need to be replaced in perpetuity (. motorCars or photocopiers). As a machine gets older, it is likely to cost more to keep it running and itsScrap value will decrease. The aim is to find the optimal replacement cycle for the machine,. how often it should be replaced - before it becomes uneconomic to own.A simple approach would involve finding the total cost of keeping an asset for1,2,3 years, etc,Then finding an average annual cost.DCF VersionNow, each possible replacement cycle is treated as a project (1-year, 2-year, or 3-year project).You calculate the NPV of each project (rather than just the total cost).Instead of dividing the NPV’s by 1,2,or 3, they’re divided by the 1,2, or 3-year annuity factorTo find an equivalent annual cost.Equivalent annual cost =。