外文文献翻译译稿和原文【范本模板】

外文文献翻译模板

外文文献翻译模板广东工业大学华立学院本科毕业设计(论文)外文参考文献译文及原文系部管理学部专业人力资源管理年级 2008级班级名称 08人力资源管理1班学号 150********学生姓名王凯琪指导教师2012年 5 月目录1 外文文献译文 (1)2 外文文献原文 (9)德国企业中老化的劳动力和人力资源管理的挑战本文的主要目的就是提供一个强加于德国公司的人力资源管理政策上的人口变化主要挑战的概况。

尽管更多方面的业务受到人口改变的影响,例如消费的改变或储蓄和投资,还有资金的花费,我们把注意力集中劳动力老龄化促使人事政策的变化上。

涉及广泛的人力资源管理政策,以有关进行创新和技术变化的招募问题为开端。

1 老化的劳动力及人力资源管理由于人口的变化,公司劳动力的平均年龄在未来将会更年长。

因此,劳动力高于50的年龄结构占主导地位的集团不再是一个例外,并将成为一个制度。

在此背景下,年长的工人的实际份额,以及最优份额,部分是由企业特征的差异加上外在因素决定的。

2 一般的挑战尽管增加公众对未来人口转型带来的各种挑战的意识,公司对于由一个老化劳动力引起的问题的意识仍然是相当低的。

事实上,只有25%的公司预计人口统计的变化在长远发展看来将会导致严重的问题。

然而,现在越来越多关于老化劳动力呈现的挑战和潜在的解决方案的文献。

布施提出了一种分析老员工一般能力的研究文集,并给出有关于年长工人的人力资源政策的实例。

目前,华希特和萨里提出一篇关于研究公司对于提前退休的态度和延长工作生涯的态度的论文。

在这些研究中,老员工的能力通常被认为是不同的,并不逊色,同时指出一个最优的劳动力取决于不同的公司的特殊要求。

一般来说,然而由于越来越缺少合格的员工,人口统计的变化将使得在各种人事政策方面上的压力逐渐增加。

特别是,没有内部人力资源部门的中小型企业,因此缺乏足够的特殊的基础设施,则面临着严峻的挑战。

与他们正常的大约两到五年的计划水平相反,他们将越来越多地要处理长期的个人问题和计划。

外文原文及译文--模板

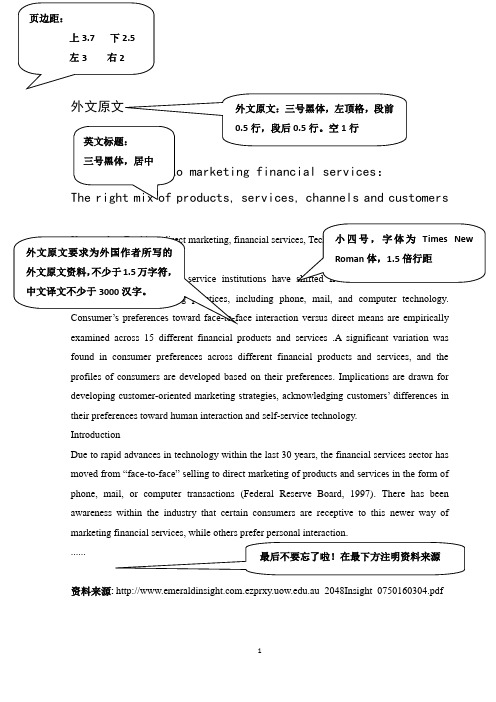

have phone, mail, and computer technology.interaction versus direct means are empirically examined across 15 different financial products and services .A significant variation was found in consumer preferences across different financial products and services, and the profiles of consumers are developed based on their preferences. Implications are drawn for developing customer-oriented market ing strategies, acknowledging customers’ differences in their preferences toward human interaction and self-service technology.IntroductionDue to rapid advances in technology within the last 30 years, the financial services sector has moved from “face -to-face” selling to direct marketing of products and services in the form of phone, mail, or computer transactions (Federal Reserve Board, 1997). There has been awareness within the industry that certain consumers are receptive to this newer way of marketing financial services, while others prefer personal interaction.......资料来源: .ezprxy .au_2048Insight_0750160304.pdf外文译文关键词银行,直销,金融服务,科技,自助服务摘要 今天的金融服务机构也从原来的传统的面对面的销售,以直接的销售手法,包括电究了全国15金融产品和服务,导言由于技术的突飞猛进,在过去30年中,金融服务业已经从“面对面”的销售对象直接在市场上销售的产品和服务的形式,电话,邮件,或电脑交易(联邦储备局,1997年)。

外文文献原稿和译文

外文文献原稿和译文原稿1. IntroductionOver the past two decades, organizations of all types have increasingly acknowledged the importance of customer satisfaction and loyalty. The marketing literature suggests that the long term success of a firm is clearly based on its ability to rapidly respond to changing customer needs and preferences (Narver &Slater, 1990; Webster, 1992). A key motivation for the increasing emphasis on customer satisfaction is that higher customer satisfaction can lead to have a stronger competitive position resulting in higher market share and profitability (Fornell, 1992), reduced price elasticity, lower business cost, reduced failure cost, and mitigated cost of attracting new customers (Chien, Chang, & Su, 2003).The principal focus of this study is on evaluating the efficiency of customer satisfaction and loyalty (CS&L) for existing mobile phone brands in Turkish mobile phone sector. Since the early1990s, with the launch of the mobile phones, there has been a remarkable development both in their product sophistication and their rapid and widespread adoption. With more than three billion subscribers around the world, the extent of mobile phone diffusion in emerging markets has been increasingly larger than that in developed countries (Kalba, 2008). Turkey, being one of the fastest emerging market economies in the world, adopted mobile phone technology in 1994. Since then, there has been a considerable increase in the level of mobile phone ownership, where the number of mobile phone users in the country is expected to reach around70 million by the end of 2013, representing a penetration rate of over 90% (RNCOS, 2010). The significant rise in mobile phone usage can partially be attributed to the fact that Turkey has the youngest population in Western Europe. Turkey currently has the 6th largest young mobile phone user base in the world, with more than 11million subscribers underthe age of 25, providing a very lucrative market for mobile phone companies (Euro monitor International,2010). It should however be noted that the penetration in this market at present is still below the EU average, indicating that the mobile phone sector is not saturated yet, and there is still space for new investors. Currently, there exist nearly more than 10 major mobile phone companies operating in the Turkish mobile phone sector, each having a relatively large product line. As of 2010, the top five mobile phone brands were Nokia, Samsung, LG, Motorola and Sony Ericsson and together they account for nearly 75% of overall market sales. As a new comer, phone is rapidly increasing its market share, but as of the start of this study, did not have a significantly large presence. In terms of market share, Nokia has been undisputedly the market leader (36.4% of sales) with Samsung featuring second (19.5%) and LG ranking third (10.1%) (Patron Turk,2010).Commensurate to its widespread diffusion globally, there has been a growing worldwide academic interest in mobile phone usage which focuses mainly on examining its contribution to social life, user preferences and its ergonomic features (Bag chi, Kirs, & Lopez, 2008). A number of empirical studies were also conducted within the context of Turkish mobile phone sector. The topics of these studies ranged from examining motivation of use (Dedeoglu,2004; Oscan & Kodak, 2003) to mobile phone selection (Isiklar &Buyukozkan, 2007), from customer satisfaction (Turkyilmaz &Ozkan, 2007) to brand loyalty (Simsek & Noyan, 2009).The methodology used in study to evaluate the relative CS&Lefficiency of mobile phone brands is based on data envelopment analysis (DEA). The traditional DEA technique has long been utilized as an invaluable tool in the field of operations research and management science to solve problems in wide range of industries(Hu, Lai, & Huang, 2009; Lee, 2009; Lin, Lee, & Chiu, 2009) as well as in not-for-profit organizations (Mahajan, 1991; Wu, Liang, &Chen, 2009; Zhang, Huang, Lin, & Yu, 2009); but its diffusion into the field of marketing and related disciplines has been relatively slow. For instance, in the marketing field, DEA has recently been employed as a powerful tool for data analysis in measuring efficiency in retailing sector (Charnes, Cooper, Learner, & Phillips,1985; Donthu & Yoo, 1998; Keh, 2000; Keh & Chu, 2003; Thomas,Barr, Cron, &Slocum, 1998), evaluating website marketing efficiency(Shuai & Wu, 2011), benchmarking marketing productivity(Donthu, Hershberger, & Osmonbekov, 2005; Kamakura, Ratchford,& Agrawal, 1988), and measuring relative market efficiency(Murthi, Srinivasan, & Kalyanaram, 1996) or service quality(Athanassopoulos, 1997; Soteriou & Staurinides, 1997). The assessment of CS&L has always been a major research item on the agenda of researchers in the marketing and related fields, because the issue of how efficiently a firm manages its marketing processes and their relationship with their customers is central to its ability to gain competitive edge vis-à-vis its rivals. The DEA approach adopted in this study illustrates how differences in CS&L efficiency between various mobile phone brands can be ascertained empirically, and thus helps management determine proper policies and courses of action.The rest of the paper is organized as follows. Section 2 reviews the recent literature on customer satisfaction and customer loyalty studies. Section 3 provides an in-depth description of our research methodology. Section 4 presents the results of our analysis. The last section (Section 5) summarizes our findings, describes managerial implications of the study and provides the concluding remarks.2. Background literatureWhile customer satisfaction has been defined in various ways, the high-level conceptualization that appears to have gained the widest acceptance states that satisfaction is a customer’s post purchase evaluation of a product or service (Cronin & Taylor,1992; Westbrook & Oliver, 1991). Customer satisfaction is also generally assumed to be a significant determinant of repeat sales, positive word-of-mouth, and customer loyalty. It has also long been considered as one of the key antecedents of creating brand loyalty (Cronin, Brady, & Hult, 2000; Dick & Basu, 1994; Fornell,Michael, Eugene, Jaesung, & Barbara, 1996; Syzmanski & Henard,2001). Satisfied customers return and buy more, and they tell other people about their experiences, both positive and negative (Fornellet al., 1996).Building on Hirschman’s (1970) exit-voice theory, weakly dissatisfied consumers would be of primary importance to a firm. While strongly dissatisfied consumers generally choose the exit option (i.e., they leave the firm), the weakly dissatisfied customers tendto stay loyal to the firm and rather employ the voice option, which implies overt complaints as an attempt to change the firm’practices or offerings (Fornell &Wernerfelt, 1988). Thereby, proper handling of customer complaints may ensure that weakly dissatisfied consumers remain loyal, and serve as an exit barrier (Fornell,1992; Halstead & Page, 1992). The impact of loyal customers is considerable; for many industries the profitability of a firm increases proportionally with the number of loyal customers and up to 60% of sales to new customers can be attributed to the word of mouth referrals (Reichheld & Sasser, 1990).Within the existing literature on customer satisfaction research, various customer satisfaction models were developed based on a cumulative view of satisfaction. To this end, a number of customer satisfaction indices (CSIs) were designed with most prominent of those being Swedish Customer Satisfaction Barometer (SCSB), the American Customer Satisfaction Index (ACSI) and European Customer Satisfaction Index (ECSI). Of these CSIs, we employed the ECSI model as the backbone of our CS&L efficiency model in this study due to its recent popularity in the literature and its comprehensiveness in CS&L coverage. The ECSI is a structural model based on the assumptions that customer satisfaction is derived by a number of factors such as perceived quality, perceived value, expectations of customers, and image of a firm. These factors are the antecedents of overall customer satisfaction (Turkyilmaz &Ozkan, 2007). The model also estimates the results when a customer is satisfied or not. The four antecedents of customer satisfaction may also have direct effects on customer loyalty(Johnson, Gustafson, Andreessen, Lervik, & Cha, 2001). Each construct in the ECSI model is a latent construct which is operational zed by multiple indicators (Chien et al., 2003; Fornell,1992). The underlying constructs of the ECSI model are explained as follows:The image construct evaluates the underlying image of the company. Image refers to the brand name and the kind of associations customers obtain from the product/company (Andreassen &Lindestad, 1998). Martensen, Kristiansen, and Rosholt (2000)argue that image is an important dimension of the customer satisfaction model. Image is a consequence of being reliable,professional and innovative, having contributions to society, and adding prestige to its user. It is anticipated that image has a positive effecton customer satisfaction, customer expectations and customer loyalty.Customer expectations are the consequences of prior experience with the company’s products (Rotondaro, 2002). This construct evaluates customer expectations for overall quality, for product and service quality, and for fulfillment of personal needs. The customer expectations construct is expected to have a direct and positive relationship with customer satisfaction (Anderson, Fornell, &Lehmann, 1994).Perceived quality is evaluation of recent consumption experience by the market served. This construct evaluates customization and reliability of a given product or service. Customization is the degree to which a product or service meets a customer’s requirements, and reliability is the degree to which firm’s offering is reliable, standardized, and free from deficiencies. Perceived quality is expected to have a positive effect on customer satisfaction (Fornellet al., 1996).Perceived value is the perceived level of product quality relative to the price paid by customers. Perceived value is the rating of the price paid for the quality perceived and a rating of the quality perceived for the price paid (Fornell et al., 1996). Perceived value structure provides an opportunity for comparison of the firms according their price-value ratio (Anderson et al., 1994). In the model, perceived value is expected to have a positive impact on satisfaction.Customer satisfaction construct indicates how much customers are satisfied, and how well their expectations are fulfilled. This construct evaluates overall satisfaction level of customers, fulfillment of their expectations, and company’s performance versus the ideal provider.Customer loyalty is the ultimate factor in the ECSI model. Loyalty is measured by repurchase intention, price tolerance and intention to recommend products or services to others. It is expected that better image and higher customer satisfaction should increase customer loyalty.3. MethodologyThis section presents the research methodology adopted in this study. The following subsections explain the survey instrument, the data collection procedure, and the DEA model.3.1. Survey instrumentThe DEA model of CS&L, which is shown in Fig. 1, consists of the aforementioned constructs which are based on previous research and prominent theories in the field of consumer behavior. The constructs of the CS&L model are unobservable (latent) variables indirectly described by a set of observable variables which are called manifest variables or indicators. The constructs and their constituent items are shown in Table 1. The use of multiple measures for each construct increases the precision of the estimate as compared to an approach of relying on a single measure. In our CS&L efficiency model, all four antecedents of customer satisfaction and loyalty which include image, customer expectations, perceived quality and perceived value were treated as input variables, while the two constructs, namely customer satisfaction and customer loyalty were considered as output variables.The survey questionnaire was designed using a three-step process. First, the consumer behavior literature was extensively reviewed for the manifest variables. Secondly, the questionnaire items were prepared in Turkish and refined through a series of discussions with two senior marketing managers of a prominent mobile phone company and a number of experienced academics in the field of consumer behavior. Finally, the survey questionnaire was subjected to extensive pre-testing and refinement based on a pilot study of 30 mobile phone users. Feedback from this pilot study indicated that some questions were ambiguous, difficult to understand,or irrelevant for mobile phone sector. This pilot study also served as a practical exercise for interviewers. The final questionnaire contained a total of 23 items pertaining to the CS&L. These23 items appeared to have face validity as to what should be measured. All the items were measured on 10-point scales, with anchors ranging from 1 denoting a very negative view and 10indicating a very positive view. Relying on 10-point scales enables customers to make better discriminations (Andrews, 1984).译文1.介绍在过去的二十年中,所有类型的组织都越来越多地承认了客户满意度和忠诚度的重要性。

外文参考文献译文及原文【范本模板】

广东工业大学华立学院本科毕业设计(论文)外文参考文献译文及原文系部城建学部专业土木工程年级 2011级班级名称 11土木工程9班学号 23031109000学生姓名刘林指导教师卢集富2015 年5 月目录一、项目成本管理与控制 0二、Project Budget Monitor and Control (1)三、施工阶段承包商在控制施工成本方面所扮演的作用 (2)四、The Contractor’s Role in Building Cost Reduction After Design (4)一、外文文献译文(1)项目成本管理与控制随着市场竞争的激烈性越来越大,在每一个项目中,进行成本控制越发重要。

本文论述了在施工阶段,项目经理如何成功地控制项目预算成本。

本文讨论了很多方法。

它表明,要取得成功,项目经理必须关注这些成功的方法.1。

简介调查显示,大多数项目会碰到超出预算的问……功控制预算成本.2.项目控制和监测的概念和目的Erel and Raz (2000)指出项目控制周期包括测量成……原因以及决定纠偏措施并采取行动。

监控的目的就是纠偏措施的。

.。

标范围内。

3.建立一个有效的控制体系为了实现预算成本的目标,项目管理者需要建立一……被监测和控制是非常有帮助的。

项目成功与良好的沟通密。

决( Diallo and Thuillier, 2005).4.成本费用的检测和控制4.1对检测的优先顺序进行排序在施工阶段,很多施工活动是基于原来的计……用完了。

第四,项目管理者应该检测高风险活动,高风险活动最有。

..重要(Cotterell and Hughes, 1995)。

4.2成本控制的方法一个项目的主要费用包括员工成本、材料成本以及工期延误的成本。

为了控制这些成本费用,项目管理者首先应该建立一个成本控制系统:a)为财务数据的管理和分析工作落实责任人员b)确保按照项目的结构来合理分配所有的……它的变化-—在成本控制线上准确地记录所有恰..。

外文文献及译文模板

原文与译文原文:A More Complete Conceptual Framework for SME FinanceAllen N. Berger Board of Governors of the Federal Reserve SystemGregory F. Udell Kelley School of Business, Indiana University,1. Financial institution structure and lending to SMEsThe research literature provides a considerable amount of evidence on the effects of financial institution structure on SME lending, although as noted above, the findings rarely go beyond the distinction between transactions lending technologies versus relationship lending to parse among the very different transactions technologies. Here, we briefly review the findings with regard to the comparative advantages of large versus small institutions (subsection A), foreign-owned versus domestically-owned institutions (subsection B), state-owned versus privately-owned institutions (subsection C) and market concentration (subsection D).A. Large versus small institutionsThere are a number of reasons why large institutions may have comparative advantages in employing transactions lending technologies which are based on hard information and small institutions may have comparative advantages in using the relationship lending technology which is based on soft information. Large institutions may be able to take advantage of economies of scale in the processing of hard information, but be relatively poor at processing soft information because it is difficult to quantify and transmit through the communication channels of large organizations (e.g., Stein 2002). Under relationship lending, there may be agency problems created within the financial institution because the loan officer that has direct contact over time with the SME is the repository of soft information that cannot be easily communicated to the management or owners of the financial institution. This may give comparative advantages in relationship lending to small institutionswith lower agency costs within the institution because they typically have less separation (if any) between ownership and management and fewer overall layers of management (e.g., Berger and Udell 2002). Finally, it is often argued that large institutions are relatively disadvantaged at relationship lending to SMEs because of organizational diseconomies with also providing transactions loans and other wholesale services to large corporate customers (e.g., Williamson 1967, 1988).The empirical literature on this topic usually does not observe the lending technologies used by large and small institutions, but rather draws conclusions about these technologies from the characteristics of the SME borrowers and contract terms on credits issued to these SMEs by institutions of different sizes. In most cases, the research is based on data from U.S. banks and SMEs. Large institutions are found to lend to larger, older, more financially secure SMEs (e.g., Haynes, Ou, and Berney 1999). It is often argued that these findings are consistent with large institutions lending to relatively transparent and relatively safe borrowers that are more likely to receive t ransactions credits. Large institutions are also found to charge lower interest rates and earn lower yields on SME loan contracts (e.g., Berger, Rosen, and Udell 2003, Berger 2004, Carter, McNulty, and Verbrugge 2004). It is contended that these results may reflect that large institutions lend to safer borrowers and/or employ lending technologies with lower operating costs, which are more likely to be transactions loans. In addition, large institutions are found to have temporally shorter, less exclusive, more impersonal, and longer distance relationships with their SME loan customers (e.g., Berger, Miller, Petersen, Rajan, and Stein forthcoming). These findings are argued to suggest weaker relationships with borrowers for large institutions, which are indicative of transactions loans. Finally, large institutions appear to base their SME credit decisions more on strong financial ratios than on prior relationships (e.g., Cole, Goldberg, and White 2004, Berger, Miller, Petersen, Rajan, and Stein forthcoming). It is argued that both the dependence on strong financial ratios and the non-dependence on prior relationships for large institutions are indicative of the use of transactions lending technologies.We argue that these findings are not as clear-cut in their support of thecomparative advantages by institution size as they might at first seem. For the most part, prior authors appear to treat transactions lending technologies as a collective whole that may be adequately represented by just one of these technologies, financial statement lending. This is not necessarily the case. We agree that the findings that SME credits by large institutions tend to be associated with weaker lending relationships and less often based on prior relationships and are indeed consistent with the predicted comparative disadvantage of large institutions in relationship lending. However, we do not agree with the contentions in the prior literature that greater SME transparency, safer SME borrowers, lower rates and yields, and possible lower operating costs and greater reliance on financial ratios for large institutions provide strong support for the hypothesis that these institutions have comparative advantages in transactions lending technologies. Although greater transparency, safer borrowers, lower rates, lower operating costs, and greater reliance on financial ratios are indicative of the use of the financial statement lending technology, they are not necessarily indicative of the types of loans or borrowers associated with the other transactions lending technologies. That is, these other transactions technologies may not necessarily be used to lend to SMEs that are less opaque or safer than relationship borrowers, may not have lower rates or smaller processing costs than relationship loans, and may not be based on stronger financial ratios than the relationship lending technology.To illustrate, note that two of the transactions lending technologies that are often used by large U.S. banks are not consistent with these characteristics. As indicated above, small business credit scoring appears to be employed by large U.S. banks to lend to SMEs that are relatively opaque and risky, and these loans have relatively high interest rates. As discussed further below, this technology is based largely on the personal credit of the SME owner, rather than on strong financial ratios of the firm. Similarly, as discussed below, the asset-based lending technology employed by many large banks is generally used to lend to relatively opaque and risky borrowers at relatively high interest rates. These loans typically involve relatively high processing costs of monitoring the accounts receivable and inventory pledged as collateral and the primary information is based on the value of the collateral, rather than strongfinancial ratios of the borrower.Moreover, even to the extent that large institutions may be disadvantaged in relationship lending and tend to lend to more transparent SME borrowers on average than small institutions, this does not necessarily imply that a sizeable presence of small institutions is necessary for significant credit availability for opaque SMEs. A limited amount of additional research finds that the local market shares of large and small U.S. banks have relatively little association with SME credit availability in their markets (Jayaratne and Wolken1999, Berger, Rosen, and Udell 2003).One potential hypothesis that may help explain this finding is that large U.S. banks are able to accommodate many opaque SME loan customers with transactions technologies other than financial statement lending, such as small business credit scoring and asset-based lending. That is, large institutions may have more transparent SME borrowers on average than small institutions because they have more financial statement loans to transparent SMEs than small institutions, but these large institutions may also be able to make credit available to significant numbers of opaque SMEs using the other transactions technologies. This hypothesis is difficult to test because the lending technology is usually unobserved.A second hypothesis may also help explain the finding of little association between the market shares of large and small institutions and SME credit availability. Large institutions may be disadvantaged at serving a significant subset of opaque SMEs, but market forces may be efficient in sorting these opaque SMEs to small institutions in the market that serve these borrowers using the relationship lending technology. The empirical evidence on the effects of U.S. bank mergers and acquisitions (M&As) on SME lending provides some support for this second hypothesis, although the lending technologies and the opacity of the borrowers is typically not observed in these studies. The studies find that large institutions reduce their SME lending after M&As, but that other banks in the same local markets appear to respond by increasing their own supplies of SME credit substantially (e.g., Berger, Saunders, Scalise, and Udell 1998, Berger, Goldberg, and White 2001, Averyand Samolyk 2004). As well, new small banks are often created in these markets that provide additional boosts to the local supply of SME credit (Berger, Bonime, Goldberg, and White 2004).The finding that the availability of credit to SMEs does not appear to depend in an important way on the market presence of large versus small institutions in the U.S. does not necessarily apply to other nations because of other differences in the financial institution structures of these nations or lending infrastructures in these nations that limit competition for SME credits. In an international comparison, greater market shares for small banks are found to be associated with higher SME employment, as well as more overall bank lending (Berger, Hasan, and Klapper 2004). These findings hold for both developed and developing nations, hold with controls included for some other aspects of the financial institution structure (e.g., shares of foreign-owned and state-owned banks, bank concentration), and hold with controls for some aspects of the lending infrastructure (e.g., regulation, legal system).B. Foreign-owned versus domestically-owned institutionsFor a number of reasons, foreign-owned institutions may have comparative advantages in transactions lending and domestically-owned institutions may have comparative advantages in relationship lending. Foreign-owned institutions are typically part of large organizations, and so all of the logic discussed above regarding large institutions generally applies to foreign-owned institutions as well. Foreign-owned institutions may also face additional hurdles in relationship lending because they may have particular difficulties in processing and transmitting soft information over greater distances, through more managerial layers, and having to cope with multiple economic, cultural, language, and regulatory environments (e.g., Buch 2003). Moreover, in developing nations, foreign-owned institutions headquartered in developed nations may have additional advantages in transactions lending to some SMEs because of access to better information technologies for collecting and assessing hard information. For example, some foreign-owned institutions use a form of small business credit scoring to lend to SMEs in developing nations based on the SME’s industry.Other institutions provide home-nation training for loan officers stationed in developing nations (Berger,Hasan, and Klapper 2004).There is very little empirical evidence on SME lending by foreign-owned institutions in developed nations, although some research finds that these institutions tend to have a wholesale orientation (e.g., DeYoung and Nolle 1996), and in some cases tend to specialize in serving multinational corporations headquartered in their home nation, presumably using transactions technologies applied to hard information (e.g., Goldberg and Saunders 1981). Some evidence also is consistent with the hypothesis that foreign-owned institutions may have difficulty processing local soft information needed to provide cash management services, although this finding is based on data from multinational corporations (e.g., Berger, Dai, Ongena, and Smith 2003). In most cases, the research on bank efficiency in developed nations suggests that the disadvantages of foreign ownership outweigh the disadvantages on average, although it is not known how much of this is attributable to the lending function (e.g., DeYoung and Nolle 1996, Berger, DeYoung, Genay, and Udell 2000).The empirical findings regarding foreign-owned institutions in developing nations are quite different. Foreign-owned banks usually appear to be more profitable and efficient than domestically-owned banks on average in these nations (e.g., Claessens, Demirguc-Kunt, and Huizinga 2001, Martinez Peria and Mody 2004), although one study finds roughly equal performance after controlling for a number of different types of governance and governance change (Berger, Clarke, Cull, Klapper, and Udell forthcoming). The better performance of foreign-owned banks in developing nations relative to developed nations may be due to the better technology access noted above, or some combination of better access to capital markets, superior ability to diversify risks, or greater managerial experience. There is also evidence on the effects of foreign-owned institutions on SME credit availability in developing nations. In most of the studies, foreign-owned banks individually or larger shares for these banks are associated with greater credit availability for SMEs (e.g., Dages, Goldberg, and Kinney 2000, Clarke, Cull, and Martinez Peria 2002, Beck, Demirguc-Kunt, and Maksimovic 2004, Berger, Hasan, and Klapper 2004, Clarke, Cull, Martinez Peria, and Sanchezforthcoming), although one study finds that foreign-owned banks may have difficulty in supplying SME credit (e.g., Berger, Klapper, and Udell 2001). As above for the U.S. data, the lending technologies are generally unobserved, and there is even less information available about the characteristics of the SME borrowers or contract terms from which to infer these technologies. Although the foreign-owned institutions almost surely use transactions technologies, it is usually not known which among the technologies is employed or the opacity of the borrowers served.C. State-owned versus privately-owned institutionsState-owned institutions may be expected to have comparative advantages in transactions lending and privately-owned institutions may be expected to have comparative advantages in relationship lending simply because state-owned institutions are typically larger. There are also a number of additional arguments with regard to the general ability of state-owned institutions to affect the supply of funds available to creditworthy SMEs through any lending technology. State-owned institutions generally operate with government subsidies and often have mandates to supply additional credit to SMEs or entrepreneurs in general, or to those in specific industries, sectors, or regions. Although in principle, this might be expected to improve funding of creditworthy SMEs, it could have the opposite effect in practice because these institutions may be inefficient due to a lack of market discipline. Much of their funding to SMEs may be to firms that are not creditworthy because of this inefficiency. The credit recipients may also not be creditworthy because the lending mandates do not necessarily require the funding be applied to positive net present value projects, or that the loans be expected to be repaid at market rates. As well some of the funds may be channeled for political purposes, rather than for economically creditworthy ends (e.g., Sapienza forthcoming). State-owned institutions may also provide relatively weak monitoring of borrowers and/or refrain from aggressive collection procedures as part of their mandates to subsidize chosen borrowers or because of the lack of market discipline. In nations with substantial state-owned banking sectors, there may also be significant spillover effects that discourage privately-owned institutions from SME lending due to “crowding out” effects of subsidized loans from state-owned institutions or poor credit cultures that are perpetuatedby the state-owned presence.The empirical findings –which are generally either cross-section studies of many nations or focused on one or a few developing nations –are generally consistent with the negative performance effects of state ownership. Studies of general performance typically find that individual state-owned banks are relatively inefficient and that large shares of state bank ownership are typically associated with unfavorable macroeconomic consequences (e.g., Clarke and Cull 2002, La Porta, Lopez-de-Silanes, and Shleifer 2002, Barth, Caprio, and Levine 2004, Berger, Hasan, and Klapper 2004, Berger, Clarke, Cull, Klapper, and Udell forthcoming). The evidence also generally suggests that less SME credit is available in nations with large market shares for state-owned banks (e.g., Beck, Demirguc-Kunt, and Maksimovic 2004, Berger, Hasan, and Klapper 2004). As well, nonperforming loan rates at state-owned banks tend to be very high, consistent with lending to SMEs with negative net present value loans, weak monitoring of loan customers, and/or lack of aggressive collection procedures (e.g., Hanson 2004, Berger, Clarke, Cull, Klapper, and Udell forthcoming). Consistent with these findings of generally negative consequences of state ownership, studies of the effects of bank privatization in both developed nations (e.g., Verbrugge, Megginson, and Owens 2000, Otchere and Chan 2003) and developing nations (e.g., Clarke, Cull, and Megginson forthcoming) typically find improvements in performance following the elimination of state ownership. Similar to the case for foreign-owned institutions, state-owned institutions likely generally use transactions technologies, but there is little information available on the technologies employed or data from which to infer these technologies.D. Market concentrationGreater market concentration of financial institutions may either reduce or increase the supply of credit available to creditworthy SMEs. Under the traditional structure-conduct-performance (SCP) hypothesis, greater concentration results in reduced credit access through any lending technology. This may occur in several ways as institutions in more concentrated markets may exercise greater market power. These institutions may choose to raise profits through higher interest rates or fees on loans to SMEs; they maychoose to reduce risk or supervisory burden by tightening credit standards for SMEs; and/or they may choose to be less aggressive in finding or serving creditworthy SMEs, taking advantage of a “quiet life” afforded to managers by the market power. Alternatively, institutions in more concentrated markets may increase SME access to credit using one of the lending technologies, relationship lending. Greater concentration may encourage institutions to invest in lending relationships because the SMEs are less likely to find alternative sources of credit in the future. Market power helps the institution enforce a long-term implicit contract in which the borrower receives a subsidized interest rate in the short term, and then compensates the institution by paying a higher-than-competitive rate in a later period (Sharpe 1990, Petersen and Rajan 1995).Although both theories may apply simultaneously, empirical studies have not come to consensus as to which of these may dominate empirically and whether the net supply of SME credit is lower or higher in concentrated markets. Some studies of the SCP hypothesis using U.S. data found that higher concentration is associated with higher SME loan interest rates (e.g., Hannan 1991, Berger, Rosen, and Udell 2003). Although this finding may appear to support the SCP hypothesis, it may also be consistent with the alternative hypothesis of an expansion of relationship lending if relationship loans tend to have higher interest rates on average than transactions loans. Relationship loans do not necessarily have higher average rates, as argued above, but we cannot rule out this possibility. As above for the empirical literatures on large versus small, foreign-owned versus domestically-owned, and state-owned versus privately-owned institutions, much of the difficulty in interpreting the effects of market concentration arises because the lending technologies are generally unobserved.A number of recent studies have looked instead to testing these hypotheses by examining the effects of banking market concentration and other indicators of market power such as regulatory restrictions on competition (part of the lending infrastructure discussed further below) on SMEs and general economic performance. The empirical results are mixed. Some of the studies find unfavorable effects from high banking market concentration andrestrictions on competition (e.g., Jayaratne and Strahan 1998, Black and Strahan 2002, Berger, Hasan, and Klapper 2004), others find favorable effects of bank concentration (e.g., Petersen and Rajan 1995, Cetorelli and Gambera 2001, Zarutskie 2003, Cetorelli 2004, Bonaccorsi di Patti and Dell’Ariccia forthcoming), and still others find the effects may differ with the lending infrastructure or economic environment (e.g., DeYoung, Goldberg, and White 1999, Beck, Demirgüç-Kunt, and Maksimovic 2004).FROM: Prepared for presentation at the World Bank Conference on Small and Medium Enterprises: Overcoming Growth ConstraintsWorld Bank, MC 13-121October 14-15, 2004译文:一个更加完整概念框架的中小企业融资Allen N. Berger 美国联邦储备局Gregory F. Udell 印地安那大学商学院1.金融机构对中小企业贷款和结构这个研究提供了大量的影响金融机构对中小企业贷款质量的证据,如上文提到的,结果几乎超越两者之间的区别与关系型贷款借给技术交易中非常不同的解析交易技术。

外文文献原稿和译文(模板)

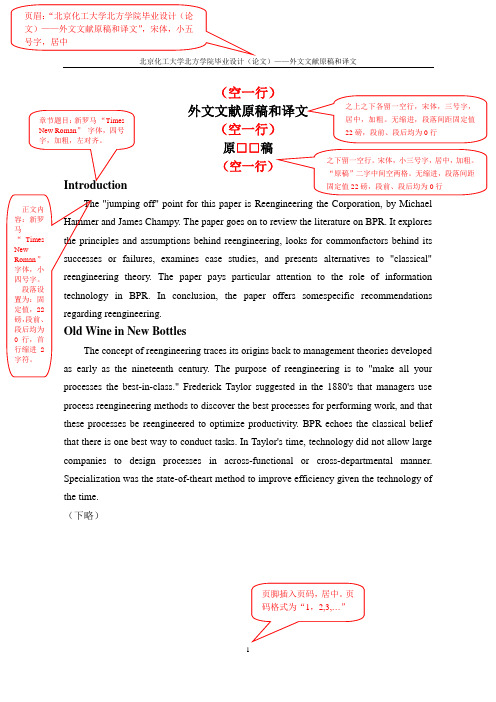

北京化工大学北方学院毕业设计(论文)——外文文献原稿和译文(空一行) 外文文献原稿和译文 (空一行) 原□□稿(空一行) IntroductionThe "jumping off" point for this paper is Reengineering the Corporation, by Michael Hammer and James Champy. The paper goes on to review the literature on BPR. It explores the principles and assumptions behind reengineering, looks for commonfactors behind its successes or failures, examines case studies, and presents alternatives to "classical" reengineering theory. The paper pays particular attention to the role of information technology in BPR. In conclusion, the paper offers somespecific recommendations regarding reengineering. Old Wine in New Bottles The concept of reengineering traces its origins back to management theories developedas early as the nineteenth century. The purpose of reengineering is to "make all your processes the best-in-class." Frederick Taylor suggested in the 1880's that managers use process reengineering methods to discover the best processes for performing work, and that these processes be reengineered to optimize productivity. BPR echoes the classical belief that there is one best way to conduct tasks. In Taylor's time, technology did not allow large companies to design processes in across-functional or cross-departmental manner. Specialization was the state-of-theart method to improve efficiency given the technology of the time.(下略)之上之下各留一空行,宋体,三号字,居中,加粗。

英文文献全文翻译

英文文献全文翻译全文共四篇示例,供读者参考第一篇示例:LeGuin, Ursula K. (December 18, 2002). "Dancing at the Edge of the World: Thoughts on Words, Women, Places".《世界边缘的舞蹈:关于语言、女性和地方的思考》Introduction:In "Dancing at the Edge of the World," Ursula K. LeGuin explores the intersection of language, women, and places. She writes about the power of words, the role of women in society, and the importance of our connection to the places we inhabit. Through a series of essays, LeGuin invites readers to think critically about these topics and consider how they shape our understanding of the world.Chapter 1: LanguageConclusion:第二篇示例:IntroductionEnglish literature translation is an important field in the study of language and culture. The translation of English literature involves not only the linguistic translation of words or sentences but also the transfer of cultural meaning and emotional resonance. This article will discuss the challenges and techniques of translating English literature, as well as the importance of preserving the original author's voice and style in the translated text.Challenges in translating English literature第三篇示例:Title: The Importance of Translation of Full English TextsTranslation plays a crucial role in bringing different languages and cultures together. More specifically, translating full English texts into different languages allows for access to valuable information and insights that may otherwise be inaccessible to those who do not speak English. In this article, we will explore the importance of translating full English texts and the benefits it brings.第四篇示例:Abstract: This article discusses the importance of translating English literature and the challenges translators face when putting together a full-text translation. It highlights the skills and knowledge needed to accurately convey the meaning and tone of the original text while preserving its cultural and literary nuances. Through a detailed analysis of the translation process, this article emphasizes the crucial role translators play in bridging the gap between languages and making English literature accessible to a global audience.IntroductionEnglish literature is a rich and diverse field encompassing a wide range of genres, styles, and themes. From classic works by Shakespeare and Dickens to contemporary novels by authors like J.K. Rowling and Philip Pullman, English literature offers something for everyone. However, for non-English speakers, accessing and understanding these works can be a challenge. This is where translation comes in.Translation is the process of rendering a text from one language into another, while striving to preserve the original meaning, tone, and style of the original work. Translating afull-length English text requires a deep understanding of both languages, as well as a keen awareness of the cultural andhistorical context in which the work was written. Additionally, translators must possess strong writing skills in order to convey the beauty and complexity of the original text in a new language.Challenges of Full-text TranslationTranslating a full-length English text poses several challenges for translators. One of the most significant challenges is capturing the nuances and subtleties of the original work. English literature is known for its rich and layered language, with intricate wordplay, metaphors, and symbolism that can be difficult to convey in another language. Translators must carefully consider each word and phrase in order to accurately convey the author's intended meaning.Another challenge of full-text translation is maintaining the author's unique voice and style. Each writer has a distinct way of expressing themselves, and a good translator must be able to replicate this voice in the translated text. This requires a deep understanding of the author's writing style, as well as the ability to adapt it to the conventions of the target language.Additionally, translators must be mindful of the cultural and historical context of the original work. English literature is deeply rooted in the history and traditions of the English-speaking world, and translators must be aware of these influences in orderto accurately convey the author's intended message. This requires thorough research and a nuanced understanding of the social, political, and economic factors that shaped the work.Skills and Knowledge RequiredTo successfully translate a full-length English text, translators must possess a wide range of skills and knowledge. First and foremost, translators must be fluent in both the source language (English) and the target language. This includes a strong grasp of grammar, syntax, and vocabulary in both languages, as well as an understanding of the cultural and historical context of the works being translated.Translators must also have a keen eye for detail and a meticulous approach to their work. Every word, sentence, and paragraph must be carefully considered and translated with precision in order to accurately convey the meaning of the original text. This requires strong analytical skills and a deep understanding of the nuances and complexities of language.Furthermore, translators must possess strong writing skills in order to craft a compelling and engaging translation. Translating a full-length English text is not simply a matter of substituting one word for another; it requires creativity, imagination, and a deep appreciation for the beauty of language. Translators mustbe able to capture the rhythm, cadence, and tone of the original work in their translation, while also adapting it to the conventions of the target language.ConclusionIn conclusion, translating a full-length English text is a complex and challenging task that requires a high level of skill, knowledge, and creativity. Translators must possess a deep understanding of both the source and target languages, as well as the cultural and historical context of the work being translated. Through their careful and meticulous work, translators play a crucial role in making English literature accessible to a global audience, bridging the gap between languages and cultures. By preserving the beauty and complexity of the original text in their translations, translators enrich our understanding of literature and bring the works of English authors to readers around the world.。

外文文献译文——参考范例

本科毕业设计(论文)外文参考文献译文及原文学院自动化学院专业电气工程及其自动化(电力系统自动化方向)年级班别2011级3班学号学生姓名指导教师2015年3月10日通过对磁场的分析改进超高压变电站扩展连接器的设计Joan Hernández-Guiteras a, Jordi-Roger Ribaa,⇑, LuísRomeralba UniversitatPolitècnica de Catalunya, Electrical Engineering Department, 08222 Terrassa, Spainb UniversitatPolitècnica de Catalunya, Electronic Engineering Department, 08222 Terrassa, Spain摘要:在世界上很多的国家,电力需求的增长比输电容量的发展更快。

由于环境的限制、社会的担忧以及经济上的投入,建设新的输电线路是一项严峻的挑战。

除此以外,输电网经常要承担接近额定容量的负载。

因此,提高输电系统的效率和可靠性受到了关注。

这项研究主要针对一个400KV,3000A,50Hz的超高压变电站扩展连接器,用于连接两个母线直径均为150mm的变电站。

该变电站连接器是一个四线制的铝导线,为母线之间的相互电能传输提供了路径。

前期的初步试验显示:电流在输电线路中的不平衡分布,主要是受到了距离的影响。

应用一个三维的有限元素法,可以改进设计,以及对改进前后两个版本的连接器的电磁性能和热性能进行评估比较。

这份报告中将提出:在实验室条件下的检验已经验证了仿真方法的准确性。

这也许将会是促进变电站连接器设计进程的一个很有价值的工具。

因此,将不仅仅提高其热性能,还将提高其可靠性。

关键词:变电站连接器、超高压、电力传输系统、有限单元法、数值模拟、临近效应、热学分析1.引入全球能源需求的频繁增长,连同分散的和可再生能源份额的增长促进超高压和特高压电力传输系统[1]的建设和研究。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

外文文献翻译译稿1卡尔曼滤波的一个典型实例是从一组有限的,包含噪声的,通过对物体位置的观察序列(可能有偏差)预测出物体的位置的坐标及速度。

在很多工程应用(如雷达、计算机视觉)中都可以找到它的身影。

同时,卡尔曼滤波也是控制理论以及控制系统工程中的一个重要课题。

例如,对于雷达来说,人们感兴趣的是其能够跟踪目标.但目标的位置、速度、加速度的测量值往往在任何时候都有噪声。

卡尔曼滤波利用目标的动态信息,设法去掉噪声的影响,得到一个关于目标位置的好的估计.这个估计可以是对当前目标位置的估计(滤波),也可以是对于将来位置的估计(预测),也可以是对过去位置的估计(插值或平滑).命名[编辑]这种滤波方法以它的发明者鲁道夫。

E。

卡尔曼(Rudolph E. Kalman)命名,但是根据文献可知实际上Peter Swerling在更早之前就提出了一种类似的算法。

斯坦利。

施密特(Stanley Schmidt)首次实现了卡尔曼滤波器。

卡尔曼在NASA埃姆斯研究中心访问时,发现他的方法对于解决阿波罗计划的轨道预测很有用,后来阿波罗飞船的导航电脑便使用了这种滤波器。

关于这种滤波器的论文由Swerling(1958)、Kalman (1960)与Kalman and Bucy(1961)发表。

目前,卡尔曼滤波已经有很多不同的实现.卡尔曼最初提出的形式现在一般称为简单卡尔曼滤波器。

除此以外,还有施密特扩展滤波器、信息滤波器以及很多Bierman, Thornton开发的平方根滤波器的变种.也许最常见的卡尔曼滤波器是锁相环,它在收音机、计算机和几乎任何视频或通讯设备中广泛存在。

以下的讨论需要线性代数以及概率论的一般知识。

卡尔曼滤波建立在线性代数和隐马尔可夫模型(hidden Markov model)上.其基本动态系统可以用一个马尔可夫链表示,该马尔可夫链建立在一个被高斯噪声(即正态分布的噪声)干扰的线性算子上的。

系统的状态可以用一个元素为实数的向量表示.随着离散时间的每一个增加,这个线性算子就会作用在当前状态上,产生一个新的状态,并也会带入一些噪声,同时系统的一些已知的控制器的控制信息也会被加入。

同时,另一个受噪声干扰的线性算子产生出这些隐含状态的可见输出。

卡尔曼滤波是一种递归的估计,即只要获知上一时刻状态的估计值以及当前状态的观测值就可以计算出当前状态的估计值,因此不需要记录观测或者估计的历史信息.卡尔曼滤波器与大多数滤波器不同之处,在于它是一种纯粹的时域滤波器,它不需要像低通滤波器等频域滤波器那样,需要在频域设计再转换到时域实现。

卡尔曼滤波器的状态由以下两个变量表示:,在时刻k的状态的估计;,误差相关矩阵,度量估计值的精确程度.卡尔曼滤波器的操作包括两个阶段:预测与更新。

在预测阶段,滤波器使用上一状态的估计,做出对当前状态的估计。

在更新阶段,滤波器利用对当前状态的观测值优化在预测阶段获得的预测值,以获得一个更精确的新估计值。

预测(预测状态)(预测估计协方差矩阵)更新首先要算出以下三个量:(测量余量,measurement residual)(测量余量协方差)(最优卡尔曼增益)然后用它们来更新滤波器变量x与P:(更新的状态估计)(更新的协方差估计)使用上述公式计算仅在最优卡尔曼增益的时候有效。

使用其他增益的话,公式要复杂一些不变量(Invariant)如果模型准确,而且与的值准确的反映了最初状态的分布,那么以下不变量就保持不变:所有估计的误差均值为零且协方差矩阵准确的反映了估计的协方差:请注意,其中表示的期望值, 。

实例考虑在无摩擦的、无限长的直轨道上的一辆车。

该车最初停在位置0处,但时不时受到随机的冲击。

我们每隔Δt秒即测量车的位置,但是这个测量是非精确的;我们想建立一个关于其位置以及速度的模型。

我们来看如何推导出这个模型以及如何从这个模型得到卡尔曼滤波器。

因为车上无动力,所以我们可以忽略掉B k和u k。

由于F、H、R和Q是常数,所以时间下标可以去掉.车的位置以及速度(或者更加一般的,一个粒子的运动状态)可以被线性状态空间描述如下:其中是速度,也就是位置对于时间的导数。

我们假设在(k− 1)时刻与k时刻之间,车受到a k的加速度,其符合均值为0,标准差为σa 的正态分布。

根据牛顿运动定律,我们可以推出其中且我们可以发现(因为σa是一个标量)。

在每一时刻,我们对其位置进行测量,测量受到噪声干扰.我们假设噪声服从正态分布,均值为0,标准差为σz。

其中且如果我们知道足够精确的车最初的位置,那么我们可以初始化并且,我们告诉滤波器我们知道确切的初始位置,我们给出一个协方差矩阵:如果我们不确切的知道最初的位置与速度,那么协方差矩阵可以初始化为一个对角线元素是B的矩阵,B取一个合适的比较大的数。

此时,与使用模型中已有信息相比,滤波器更倾向于使用初次测量值的信息。

§推§推导后验协方差矩阵按照上边的定义,我们从误差协方差开始推导如下:代入再代入与整理误差向量,得因为测量误差v k与其他项是非相关的,因此有利用协方差矩阵的性质,此式可以写作使用不变量P k|k—1以及R k的定义这一项可以写作:这一公式对于任何卡尔曼增益K k都成立。

如果K k是最优卡尔曼增益,则可以进一步简化,请见下文。

§最优卡尔曼增益的推导卡尔曼滤波器是一个最小均方误差估计器,后验状态误差估计(英文:a posteriori state estimate)是我们最小化这个矢量幅度平方的期望值,,这等同于最小化后验估计协方差矩阵P k|k的迹(trace).将上面方程中的项展开、抵消,得到:当矩阵导数是0的时候得到P k|k的迹(trace)的最小值:此处须用到一个常用的式子,如下:从这个方程解出卡尔曼增益K k:这个增益称为最优卡尔曼增益,在使用时得到最小均方误差.§后验误差协方差公式的化简在卡尔曼增益等于上面导出的最优值时,计算后验协方差的公式可以进行简化。

在卡尔曼增益公式两侧的右边都乘以S k K k T得到根据上面后验误差协方差展开公式,最后两项可以抵消,得到.这个公式的计算比较简单,所以实际中总是使用这个公式,但是需注意这公式仅在使用最优卡尔曼增益的时候它才成立。

如果算术精度总是很低而导致数值稳定性出现问题,或者特意使用非最优卡尔曼增益,那么就不能使用这个简化;必须使用上面导出的后验误差协方差公式。

自适应滤波器是能够根据输入信号自动调整性能进行数字信号处理的数字滤波器。

作为对比,非自适应滤波器有静态的滤波器系数,这些静态系数一起组成传递函数。

对于一些应用来说,由于事先并不知道所需要进行操作的参数,例如一些噪声信号的特性,所以要求使用自适应的系数进行处理。

在这种情况下,通常使用自适应滤波器,自适应滤波器使用反馈来调整滤波器系数以及频率响应。

总的来说,自适应的过程涉及到将代价函数用于确定如何更改滤波器系数从而减小下一次迭代过程成本的算法。

价值函数是滤波器最佳性能的判断准则,比如减小输入信号中的噪声成分的能力。

随着数字信号处理器性能的增强,自适应滤波器的应用越来越常见,时至今日它们已经广泛地用于手机以及其它通信设备、数码录像机和数码照相机以及医疗监测设备中假设医院正在监测一个患者的心脏跳动,即心电图,这个信号受到50 Hz(许多国家供电所用频率)噪声的干扰剔除这个噪声的方法之一就是使用50Hz 的陷波滤波器(en:notch filter)对信号进行滤波。

但是,由于医院的电力供应会有少许波动,所以我们假设真正的电力供应可能会在47Hz 到53Hz 之间波动。

为了剔除47 到53Hz 之间的频率的静态滤波器将会大幅度地降低心电图的质量,这是因为在这个阻带之内很有可能就有心脏跳动的频率分量。

为了避免这种可能的信息丢失,可以使用自适应滤波器。

自适应滤波器将患者的信号与电力供应信号直接作为输入信号,动态地跟踪噪声波动的频率。

这样的自适应滤波器通常阻带宽度更小,这就意味着这种情况下用于医疗诊断的输出信号就更加准确。

扩展卡尔曼滤波器在扩展卡尔曼滤波器(Extended Kalman Filter,简称EKF)中状态转换和观测模型不需要是状态的线性函数,可替换为(可微的)函数。

函数f可以用来从过去的估计值中计算预测的状态,相似的,函数h可以用来以预测的状态计算预测的测量值。

然而f和h不能直接的应用在协方差中,取而代之的是计算偏导矩阵(Jacobian)。

在每一步中使用当前的估计状态计算Jacobian矩阵,这几个矩阵可以用在卡尔曼滤波器的方程中。

这个过程,实质上将非线性的函数在当前估计值处线性化了。

这样一来,卡尔曼滤波器的等式为:预测使用Jacobians矩阵更新模型更新预测如同扩展卡尔曼滤波器(EKF)一样,UKF的预测过程可以独立于UKF的更新过程之外,与一个线性的(或者确实是扩展卡尔曼滤波器的)更新过程合并来使用;或者,UKF的预测过程与更新过程在上述中地位互换亦可.外文文献翻译原文1Kalman filtering, also known as linear quadratic estimation(LQE), isan algorithm that uses a series of measurements observed over time,containing noise(random variations)and other inaccuracies,and producesestimates of unknown variables that tend to be more precise than those based on a single measurement alone. More formally, the Kalman filter operates recursively on streams of noisy input data to produce a statistically optimal estimate of the underlying system state。

The filter is named after Rudolf (Rudy) E. Kálmán,one of the primary developers of its theory。

The Kalman filter has numerous applications in technology。

A common application is for guidance, navigation and control of vehicles,particularly aircraft and spacecraft。