美国原产地规则之实质转变规则(英文版)

原产地规则

案例2:欧盟对我国彩电反倾销

• 欧盟1994年发起针对我国原产的大屏幕彩电的反倾销调 查就是一个典型案例。当时我国向欧盟出口的大屏幕彩电 共计51.5万台,为欧盟2450万台彩电消费总量的2.1%, 超过了2%的最低限额。但实际上其中3家中日合资企业 出口的11.7万台采用了日本产显像管。按照欧 盟彩电原 产地标准的规定,彩电原产地应依显像管的原产地而定, 即11.7万台采用日本产显像管组装的彩电应视为原产于日 本。这样,另外采用中国产显像管取得“中国国籍”的 39.8万台彩电仅占到了欧盟消费总量的1.6%, 低于2% 的最低限额,从而不能构成欧盟对我国彩电提起反倾销诉 讼的前提条件。然而依照我国彩电原产地标准,彩电只要 在我国境内进行“插件、焊接和装配”工序即可视为中国 原产。欧盟在进行反倾销调查时,按照中国的原产地规则 标准,将这11.7万台彩电判定为原产于中国。结果,上述 中日合资企业的11.7万台彩电,包括中国的39.8万台彩电 都被欧盟征收28.8%的反倾销税,导致我国彩电丧失确定的原则,以确定生产或制 造货物的国家或地区的具体规 定

原产地规则的标准:

• 整件生产标准。即产品完全是受惠国 生产和制造,不含有进口的和产地不 明的原材料和部件。 • 实质性改变标准。是适用于确定有两 个或两个以上国家参与生产的产品的 原产国的标准。

原产地规则应用国际贸易的一些范畴 • • • • • • • • 贸易统计 差别关税的计征: 地区经济一体化的互惠措施 进口配额的管理 反倾销(反补贴)诉案的审理 原产地标记的监管 政府采购中货物的原产地判定 涉及濒危动植物的保护

作用

• 世界大多数国家根据进口产品的不同来源, 分别给予不同的待遇。在实行差别关税的 国家,进口货物的原产地是决定其是否享 受一定的关税优惠待遇的重要依据之一。 在采取禁运、反倾销、进出口数量限额、 贸易制裁、联合抵制、卫生防疫管制、外 汇管制等贸易措施中,只有在对进口货物 的原产地能够作出准确的判定时,其贸易 措施才能真正发挥作用。因此,在许多情 况下,原产地规则都是国家贸易政策的重 要组成部分,具有广泛的多方面的作用。

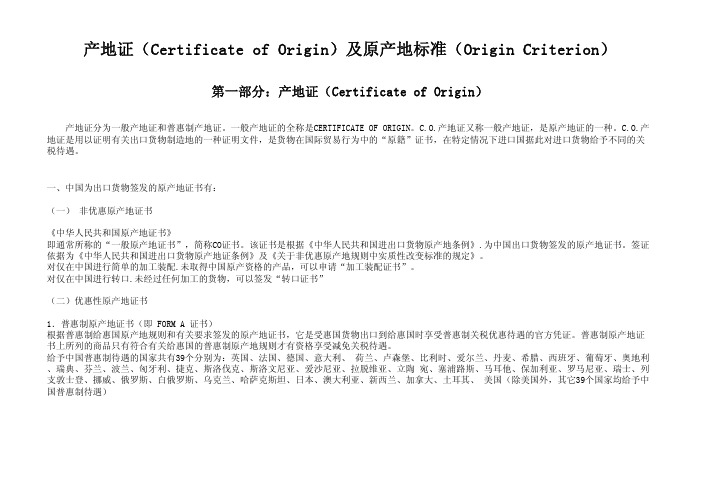

产地证(Certificate of Origin)及原产地标准(Origin Criterion)

产地证(Certificate of Origin)及原产地标准(Origin Criterion)第一部分:产地证(Certificate of Origin)产地证分为一般产地证和普惠制产地证。

一般产地证的全称是CERTIFICATE OF ORIGIN。

C.O.产地证又称一般产地证,是原产地证的一种。

C.O.产地证是用以证明有关出口货物制造地的一种证明文件,是货物在国际贸易行为中的“原籍”证书,在特定情况下进口国据此对进口货物给予不同的关税待遇。

一、中国为出口货物签发的原产地证书有:(一) 非优惠原产地证书《中华人民共和国原产地证书》即通常所称的“一般原产地证书”,简称CO证书。

该证书是根据《中华人民共和国进出口货物原产地条例》.为中国出口货物签发的原产地证书。

签证依据为《中华人民共和国进出口货物原产地证条例》及《关于非优惠原产地规则中实质性改变标准的规定》。

对仅在中国进行简单的加工装配.未取得中国原产资格的产品,可以申请“加工装配证书”。

对仅在中国进行转口.未经过任何加工的货物,可以签发“转口证书”(二)优惠性原产地证书1.普惠制原产地证书(即 FORM A 证书)根据普惠制给惠国原产地规则和有关要求签发的原产地证书,它是受惠国货物出口到给惠国时享受普惠制关税优惠待遇的官方凭证。

普惠制原产地证书上所列的商品只有符合有关给惠国的普惠制原产地规则才有资格享受减免关税待遇。

给予中国普惠制待遇的国家共有39个分别为:英国、法国、德国、意大利、 荷兰、卢森堡、比利时、爱尔兰、丹麦、希腊、西班牙、葡萄牙、奥地利、瑞典、芬兰、波兰、匈牙利、捷克、斯洛伐克、斯洛文尼亚、爱沙尼亚、拉脱维亚、立陶 宛、塞浦路斯、马耳他、保加利亚、罗马尼亚、瑞士、列支敦士登、挪威、俄罗斯、白俄罗斯、乌克兰、哈萨克斯坦、日本、澳大利亚、新西兰、加拿大、土耳其、 美国(除美国外,其它39个国家均给予中国普惠制待遇)2.《亚太贸易协定》(原称《曼谷协定》)原产地证书(FORM B 证书)《亚太贸易协定》原产地证书根据《亚太贸易协定》的要求签发.在协定成员 国之间就特定产品享受互惠减免关税待遇的官方证明文件,签证依据为《亚太贸易协定》原产地规则及《亚太贸易协定原产地证书签发和核查程序》。

WTO规则中英文教程第十七章 WTO原产地规则_OK

2021/6/30

11

(一)原产地的认定标准及相应要求 (Determining Criteria of Origin and Corresponding Requirement)

• 在原产地的认定时涉及两类产品,一类是“完 全原产”(wholly obtained)的产品,另一类是发 生“实质性改变”(substantial transformation)的 产品。对前者原产地的认定勿需赘述,对后者 原产地的认定则较为复杂,其认定标准有三种:

countervailing duties,safeguard measures, origin

marking requirements and any discriminatory

quantitative restrictions or tariff quotas. They shall

also include rules of origin used for government

2021/6/30

10

(二)其他规则

• Rules of origin are based on a positive standard. Rules of origin that state what does not confer origin (negative standard) are permissible as part of a clarification of a positive standard or in individual cases where a positive determination of origin is not necessary.

原产地规则

原产地规则一、原产地规则概述“货物的原产地”(The origin ofgoods)是指某一特定产品的原产国或原产地区,即货物的生产来源地。

根据各国的原产地规则和国际惯例,原产国(地)是指某一特定货物的完全生产国(地);当一个以上的国家(地区)参与了某一货物的生产时,那个对产品进行了最后的实质性加工的国家(地区)即为原产国(地)。

原产地规则是各国(地区)为了确定商品原产地和地区而采取的法律、规章和普遍适用的行政命令。

其目的是以此确定该商品在进出口贸易中应享受的待遇。

原产地规则的内容一般包括原产地标准和书面说明。

随着国际贸易的发展,原产地规则在国际贸易中的地位日益重要,研究探讨乃至统一原产地规则逐渐成为国际社会普遍关心和重视的问题。

围绕着原产地规则问题,关贸总协定进行了长期的努力,并于1993年12月15日签署乌拉圭回合最后文件时,将《原产地规则协议》正式列入最后文件的附件。

二、《原产地规则协议》内容简介原产地规则协议由前言、四个部分(9个条款)和两个附录构成。

第一部分是定义与适用范围;第二部分是关于实施原产地规则的规定,涉及过渡期和过渡期后的规定;第三部分是通知、审查、协商和争端解决的程序安排;第四部分是原产地规则的协调,附录一是有关原产地规则技术委员会的内容;附录二是关于优惠的原产地规则的共同宣言。

具体内容包括如下:(一)定义与适用范围1、原产地规则的定义原产地规则是指任何成员方为确定货物原产地而实行的普遍适用的法律、法规和行政管理决定,且此种原产地规则与导致授予超出《1994年关贸总协定》第一条的关税优惠的契约性或自治性贸易体制无关。

2、原产地规则的适用范围它包括所有非优惠的商业政策措施,如1994年关贸总协定第一、二、三、十一和十三条下的最惠国待遇;第六条的反倾销和反补贴税;第十九条的保障措施;第九条的原产地标记要求;任何歧视性的数量限制或关税配额。

此外,还包括为政府采购和贸易统计而使用的原产地规则。

关于“原产地”商品贸易中“原”与“源”的区分运用

关于“原产地”商品贸易中“原”与“源”的区分运用作者:富尧来源:《对外经贸实务》2008年第08期读同心出版社2000年出版的《季羡林人生漫笔》,其中关于《糖史》一书有这样的论述,“糖是一种微末的日用食品,平常谁也不会重视它。

可是‘糖’这个字在西欧各国的语言中都是外来语,来自同一个梵文字sarkara,这充分说明了,欧美原来无糖,糖的原产地是印度。

”笔者认为这段话中“原产地”一词的运用有待商榷。

原产地的英文是country of origin,指货物的“国籍”,在长期的国际贸易实践中形成了以“实质性改变”作为判定多国生产产品原产地的原则,其在确定对一种产品适用何种贸易措施、贸易救济或贸易优惠时被广泛应用。

(一)实质性改变原则来自美国1886年的Hartranft V. Wiegmann案。

该案争论的焦点是进口的清洗及磨光后的贝壳是否是贝壳制品(Manufactured Shells)。

当时美国对贝壳免征进口税,对贝壳制品则需征收35%的从价税。

最高法院最后判定清洗及磨光后的贝壳仍为贝壳,清洗及磨光后的贝壳并非具有不同的名称、特征或用途的一项不同的新产品。

由此案例形成“实质性改变”的判定原则,指这种改变形成了一种完全不同的“新”产品。

随着原产地规则的不断发展完善,“实质性改变”已成为原产地制度的基石。

对于多国生产的产品,以最后发生实质性改变的国家作为这种产品的原产地。

例如从日本进口木柄,从俄罗斯进口刷毛,在中国加工成木刷出口到韩国,由于木柄和刷毛的功能发生的“实质性改变”,因此木刷的原产地应为中国。

但“实质性改变”原则过于笼统,各国在海关操作中常采用以下三种标准:税则归类改变标准、从价百分比标准和制造或者加工工序标准。

我国判定糖的原产地采用“制造或加工工序标准”,即完成混合及烹煮等主要工序的国家即为这批糖的原产地。

这与季羡林先生的原意极不相符。

例如从印度进口甘蔗,在中国生产加工成蔗糖或其他糖类,再出口到印度,此时这批糖的原产地是中国;而不像文章中所说“糖的原产地是印度”。

美墨加协定(usmca)对原产地规则的修订及其影响分析

美墨加协定(USMCA)对原产地 规则的修订及其影响分析何蓉连增郭正琪内容提要: 2018年11月30日,美国、墨西哥和加拿大三国签署了《美国—墨西哥—加拿大协定》,简称“美墨加协定(USMCA)”,正式替代“北美自由贸易协定(NAFTA)”。

美墨加新协定保留了原协定(NAFTA)的大部分内容,但在一些关键部分进行了改动,主要调整和修订了原产地规则、市场准入和劳工等方面的内容。

其中,原产地规则是自由贸易协定的核心,与自贸区内各成员国的经济利益紧密相关。

本文将着重于研究美墨加协定中原产地规则的修订及产生的影响,并在此基础上为我国参与的自由贸易区原产地规则的进一步完善提出建议,为更好地实施自贸区战略提供参考。

关 键 词: 美墨加协定;原产地规则;修订作者简介: 何蓉,博士,北京外国语大学国际商学院副教授,研究领域为国际贸易。

连增,通讯作者,博士,北京外国语大学国际商学院讲师,研究领域为国际贸易。

郭正琪,北京外国语大学国际商学院2018级硕士研究生,研究领域为国际贸易规则。

(北京,100089)中图分类号: F74 文献识别码: A 文章编号: 2096-4536(2019)06-0048-17一、引言由于美国与墨西哥、加拿大之间巨大的贸易逆差,以及北美自由贸易协定的原有条款已无法满足美国经济贸易发展的需要,美国重启了美墨加自贸协定谈判, 2018年11月30日,美国、墨西哥和加拿大一致达成新的贸易协定——美国–墨西哥–加拿大协定(The United States-Mexico-Canada Agreement,USMCA),至此,1994年签署的北美自由贸易协定(North American Free Trade Agreement,NAFTA)正式成为历史。

美墨加协定(USMCA)对原产地规则的修订及其影响分析 —美墨加协定(USMCA)保留了原北美自贸协定的主要框架,在部分章节中做了调整和补充。

关于“原产地”商品贸易中“原”与“源”的区分运用——从季羡林先生对“原产地”一词的笔误说起

,

糖是

。

一

实质 性 改变 原 则 过 于 笼 统 各 国在 海 关

、

平 常谁 也 不 会 重 视 它

可是

,

操 作 中 常 采 用 以 下 三 种 标 准 :税 则 归 类 改 变 标 准

从 价 百 分 比标 准和 制造 或 者 加

工 工

糖

’

这 个 字 在 西 欧 各 国 的 语 言 中都 是 外 来 语

泰国

为 此 鲁 先 生根 据 产 品 质 量 法 和 消 费者 权 益

,

木柄 从 俄 罗斯进

,

,

口

刷 毛 在 中国 加 工 成

,

保 护 法 的相 关 规 定

将沃 尔玛告上 法庭

,

。

浦东新

木刷 出 口 到韩 国

由于 木 柄 和 刷 毛 的 功 能 发 生 的

区 法 院 经 审理 后 认 为

被告沃 尔玛 销售 的狮王 牌

35 %

口

,

f a c tu

)

。

者对不 同原产地 的商 品 的 印象存在 显 著差异

极 大 地 影 响到 他 们 的购 买 决 策

。

,

并

税 对 贝 壳制 品 则 需 征 收

近 年 来 由于 商 品

。

的从价 税

。

最 高 法 院 最 后 判 定 清 洗及 磨 光 后

,

原 产地 标 记 错 误 而 引发 的 争端 也 曰 益 增加

原 产地 的原 则 其 在 确定 对

,

糖 类 再 出 口 到 印 度 此 时这 批 糖 的 原 产 地 是 中 国 ;

而 不 像 文 章 中所 说

种产 品适用 何种 贸 易

原产地规则分类

原产地规则分类

原产地规则主要可以分为以下几大类:

1.完全获得原产地资格规则:要求产品全部由起源国生产或取得原产资格,如"全生产"规则和"完全取得资格"规则。

2.实质性转变规则:要求经过后续加工的产品,其属性或名称已经实质性改变,可获得原产地资格,如美国的"实质性转变"规则。

3.特定加工规则:要求产品必须经历某一特定生产过程,如烹煮、淬火、香辛料处理等,才能取得原产地资格,如欧盟的"最后制作国"规则。

4.投入价值提高规则:要求国内材料和劳动力投入超过产品价格或成本的一定比例,产品才能取得原产地资格,如美国的"转化率"规则。

5.非起源材料限量规则:规定产品中非原产地材料所占的价值或重量比例不超过一定限额,产品才能获得原产地资格,如欧盟的"非原产地材料总值"规则。

6.特惠原产地规则:给与最不发达国家优惠的原产地规则,要求最少的国内加工工艺或非原产地材料占比较低的比例,产品就可以取得原产地资格,便于这些国家出口产品。

这些规则是根据产品取得原产地资格所需的国内加工工艺强度和投入材料的数量而分类的,目的是限制非原产国企业通过简单加工就获取原产地资格和利益的行为。

不同国家和地区根据自身产业政策会选用或混合使用不同类型的原产地规则。

以上分类和说明可以帮助我们理解原产地规则的基本框架及各类规则的具体内容。

也欢迎您提出宝贵意见,以便进一步扩充和完善这个分类

1/ 1。

CPTPP、RCEP、美国原产地规则的对比

收稿日期:2022-01-19作者简介:张华宇(1999-),男,江苏徐州人,学生,研究方向:国际贸易;刘晓伟(1979-),男,湖南衡阳人,讲师,硕士,研究方向:国际贸易。

C PTPP 、R C EP 、美国原产地规则的对比张华宇,刘晓伟(苏州经贸职业技术学院,江苏苏州215009)摘要:原产地规则在国际贸易中具有举足轻重的地位,它是区域自由贸易协定必不可少的组成部分。

目前,全球覆盖范围最广最具影响力的两大跨区域自由贸易协定—C PT PP (全面进步的跨太平洋伙伴关系协定,日本主导)和R C EP (区域全面经济伙伴关系协定,东盟主导)以及作为全球第一大经济国的美国,在原产地标准上都做了详细规定。

全面了解这三大原产地规则的主要内容与特点对于国际经贸相关从业者和研究者是十分必要的,而本文则通过对C PT PP 、R C EP 、美国原产地规则的主要内容进行梳理归纳,为关注者提供一个较全面的对比分析框架。

关键词:原产地规则;C PT PP ;R C EP ;美国法中图分类号:F740文献标识码:A文章编号:1005-913X (2022)05-0019-05C om pari son of C PT PP,R C E P and U S R ul es of O ri gi nZ hang H uayu ,Li u X i aow ei(Suzhou I ns t i t ut e ofT r ade&C om m er ce,Suzhou J i angs u215009)A bs t ract :R ul es of or i gi n ar e of gr eat i m por t ance i n i nt er nat i onalt r ade;t hey ar e al s o an i ndi s pens abl e par tofr egi onal f r ee t r ade agr eem ent s .A t pr es ent ,t he t w o t r ans -r egi onal f r ee t r ade agr eem ent sw i t h t he m os text ens i ve cover age and t he m os t i nf l uent i ali nf l uence i n t he w or l d —C PT PP(C om pr ehens i ve and Pr ogr es s i ve T r ans -Paci f i c Par t ner s hi p,l ed by J apan)and R C EP (R egi onal C om pr ehens i ve Econom i c Par t ner s hi p,l ed by A SEA N ),as w el l as t he W or l d's l ar ges t econom y,t he U ni t ed St at es ,have m ade det ai l ed r ul es on or i gi n s t andar ds .I t i s ver y neces s ar y f orpr act i t i oner sand r es ear cher sr el at ed t o i nt er nat i onal econom y and t r ade t o f ul l y under s t and t he m ai n cont ent s and char act er i s t i csoft he t hr ee r ul esofor i gi n.T hi spaper ,by s or t i ng out t he m ai n cont ent s of C PT PP,R C EP,U S r ul es of or i gi n,pr ovi des a r el at i vel y com pr ehens i ve com par at i ve anal ys i s f r am ew or k f ort he f ol l ow er s .K ey w ords:R ul esofO r i gi n;C PT PP;R C EP;U .S.C.A原产地规则(Count r y ofor i gi n)是一国根据国家法令或国际协定确定的原则制定并实施的,以确定生产或制造货物的国家或地区的具体规定,是该国针对进口商品实施贸易差别待遇的法律依据。

USMCA原产地规则变化对中国的影响及其启示

[基金项目]本文系 2019 年上海市教委本科重点课程项目《管理学》[沪教委高(2019)39 号]。 [作者简介]林黎(1983—),女,上海外国语大学贤达经济人文学院高级经济师;研究方向:工商管理。

R F REIGN PRACTICE IN

ECONOMIC ELATIONS AND TRADE

国际规则与标准化

的 《北美自由贸易协定》(NAFTA)。 地规则对于成员方引资以及促进核 准,如核心零部件的原产地价值量

《美墨加协定》基本上保留了 NAFTA 心技术回流能够起到一定的推动作 含量为 75%,主要零部件的含量标

的基本框架,但内容涵盖更为广泛, 用。总体看,USMCA 对原产地规则的 准是 70%,附加零部件的价值含量

的贸易保护措施,其内容的修订引 在北美各国经济体系中占据重要地 外的国家向这两国出口汽车的份额

起了广泛的关注,对中国外贸出口 位。NAFTA 和 USMCA 均对汽车原产 基本持平。可见,美国汽车对加拿

及全球经济走势必然会产生深远的 地规则进行了细致的规定,涵盖了 大、墨西哥两国的市场依赖度有所

影响。

doi:10.3969/j.issn.1003-5559.2020.07.010

国际规则与标准化

原产地规则变化对中国的影响及其启示

■ 林 黎 上海外国语大学贤达经济人文学院

摘 要:《美墨加协定》对汽车、纺织业原产地规则做了较大的调整,不仅提升了区域价值含量标准,还设 定了劳工价值含量标准及相关贸易实施机制。USMCA 原产地规则的变化,对中国汽车零部件,纺织品、服装 及其原料对北美出口会造成一定冲击,对来自于北美的整车进口也会有一定影响。原产地规则作为隐性的区 域贸易保护政策,对进出口及投资有重要导向作用。因此,我国在对外自贸区构建谈判中,应该借鉴 USMCA 的做法,适当提升原产地标准的设定,同时提升原产地标准设定的针对性,为特殊行业提供特殊保护。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

U.S. Origin Rules in Uncertain Times——Substantially Transformed美国原产地规则之实质转变规则Until the Trump administration’s war on trade, many companies did not consider country of origin to be of critical importance to their import process. Certainly, country of origin questions were, and remain, important for determining whether goods are subject to import restraints (quotas) or for qualification under various free trade agreements and special duty programs such as 9801 or 9802; and it is of critical importance when we consider whether certain goods and materials are subject to Antidumping or Countervailing duties, but, for much of the goods that are imported, it was a non-issue. But no longer. Un der the Trump administration’s war on trade, we must now contend with and consider whether the goods we import are subject to additional duties under Section 201, 232 and the overwhelming impact of section 301 duties on goods from China. Companies are asking about whether they can shift their supply chain to take advantage of more favorable countries, and if so, how far down the supply chain the shift must occur.Whose Responsibility is It to Determine Country of Origin?Section 484 of the Tariff Act, as amended (19 U.S.C. - 1484), obligates an importer of record (IOR) to use reasonable care when entering or classifying imported merchandise, assessing duties, reporting accurate trade statistics and determining whether any other applicable legal requirement has been met. Determining and reporting the origin of imported goods falls within the scope of section 1484, both for purposes of duty preference claims as well as complying with basic entry requirements for reporting the correct country of origin of imported merchandise. (CBP Form 7501 "Entry Summary" Instructions: Detailed instructions on completing CBP Form 7501. ) False statements with respect to origin can result in the assessment of penalties under 19 U.S.C. -1592. Additionally, errors made with respect to the country of origin can result in the loss of special duty privileges, detention or exclusion of goods at the time of admission, or a demand for redelivery of the articles to Customs custody. Articles that are not timely returned to Customs custody are subject to liquidated damages equal to the value of the unreturned articles. Goods that are improperly marked or not marked in accordance with the country of origin marking statute (19 U.S.C. - 1304) can also be assesseda special “marking duty” equal to 10 percent of the value of the mis-marked goods.In United States v. Golden Ship Trading Company, 25 C.I.T. 40 (2001) the government sued an importer of t-shirts from the Dominican Republic, claiming that the true country of origin of the t-shirts was China and not the Dominican Republic as reported. The government sought a monetary penalty for negligence. The importer argued that it was not negligent in misrepresenting the origin of the t-shirts because she relied on the information provided by the exporter and accepted his representations that the Dominican Republic was the country of origin of the t-shirts. The court, however, determined that the importer, Ms. Wu, failed to exercise reasonable care because she failed to verify the information contained in the entry documents related to country of origin. The court explained that under the definition of reasonable care, Ms. Wu had the responsibility to at least undertake an effort to verify the information on the entry documents. The court said that there is a distinct difference between legitimately attempting to verify the entry information and blindly relying on the exporter’s assertions. Had Ms. Wu inquired as to the origin of the imported t-shirts or, at minimum, attempted to check the credentials and business operations of the exporter, she could make an argument that she attempted to exercise reasonable care and competence to ensure that the statements on the entry documents were accurate, but she had not. The court found that Ms. Wu’s failure to at tempt to verify the entry document information shows she did not act with reasonable care, and had, therefore, attempted to negligently introduce merchandise into the commerce of the United States in violation of 19 U.S.C.- 1592 (a)(1)(A). Because of this, she was required to pay a civil penalty for her negligence. Understanding the U.S. Country of Origin RulesFor non-preferential duty treatment, the U.S. country or origin (COO) rules follow the U.S. country of origin marking rules laid out in section 134 of the Customs Regulations. (19 CFR Part 134, et seq.)These rules provide that the “country of origin” of a good is the country in which the good is wholly manufactured, produced, or grown. Such an article is said to be "wholly the growth or product" of that country and as such, it is considered to be “originating” in that country. Similarly, articles that are processed or manufactured exclusively in a country from materials that have been wholly grown or produced in that same country are also considered to be "wholly the product or manufacture" of that country.When an article is not wholly the growth, product, or manufacture of that country, that is, when the product incorporates or reflects materials orprocessing, or both, which are attributable to two or more countries, origin determinations become more problematic. In such cases, the impact of materials or articles that originate in a country other than the country of final processing must be considered when determining the country of origin of the finished good.If the article in question is not wholly manufactured, produced, or grown within a single country, then we must consider the source or origin of any component or material that is used in the manufacture, production, or assembly of the good, and whether the further work or material added to an article in a subsequent country effected a “substantial transformation” on that part, component or material, so as to render such other country the “country of origin” of the end product. (19 CFR Part 134.1)U.S. Customs” Country of Origin RegulationsA common misconception by importers and the trade is that Part 102 of the Customs Regulations provides for general non-preferential origin rules. This is not the case. The preamble to Part 102 of the Customs Regulations provides that this part sets forth rules for determining the country of origin of imported goods for the purposes the North American Free Trade Agreement (NAFTA), the United States-Morocco Free Trade Agreement regulations; the United States-Bahrain Free Trade Agreement, and for determining the country of origin of textile and apparel products.The Substantial Transformation RuleFirst set forth a century ago by the U.S. Supreme Court in Anheuser-Busch Brewing Ass’n v. United States, 207 U.S. 556, 562 (1908) the “substantial transformation” rule has been applied throughout the United States customs laws to determine the origin of goods for such varied purposes as: admissibility, eligibility for preferential trade programs, country of origin marking, drawback of duties, administration of the U.S. textile import program, American goods returned, and government procurement under the Trade Agreements Act of 1979.The essence of the substantial transformation rule is that a product cannot be said to originate in the country of exportation if it was not manufactured there. The question, therefore, has been whether operations performed on products in the country of exportation are of such a substantial nature so as to justify the conclusion that the resulting product is a manufacture of that country. In Anheuser-Busch Brewing Ass’n the Supreme Court said: "[m]anufacture implies a change, but every change is not manufacture * * *.There must be transformation; a new and different article must emerge, 'having a distinctive name, character, or use.'"In United States v. Gibson-Thomsen Co., Inc., 27 C.C.P.A. 267 (C.A.D. 98) (1940) the Court of Customs & Patent Appeals held that a product undergoes a "substantial transformation" if, as a result of further manufacturing or processing, the product loses its identity and is transformed into a new product having "a new name, character, and use." As observed in Tropicana Products, Inc. v. United States (6 C.I.T. 155, 159, 789 F. Supp. 1154,1157 (1992)) substantial transformation is a concept of major importance in administering the customs and trade laws."Complexity and Confusion AboundsAccording to Customs, the substantial transformation rule of Gibson-Thomsen (the change of “name, character, and use" test) has been difficult for the importing community, Customs, and the courts to apply, and that the rule has often resulted in a lack of predictability and certainty to its decisions. At the root of this frustration is the fact that the Gibson-Thomsen substantial transformation rule must to be applied on a case-by-case basis, often involving subjective judgments as to what constitutes a new and different article, or whether certain processing resulted in an article with a new name, character, or use.The concepts and rules surrounding substantial transformation can be confusing for the uninitiated. Very often, importers mistakenly base their conclusion on a local or “Regional Value Content” (RVC), or a change or shift in tariff classification, as evidence of a substantial transformation for purposes of determining origin. While these concepts have their place in determining the origin of goods for specific preferential trade programs, they have limited application when determining the origin of goods for general origin determinations. (Many of the current U.S. preferential trade programs, such as NAFTA, Chile (CLFTA), Singapore (SGFTA) Australia (AUFTA), Bahrain (BHFTA), Morocco (MAFTA), Oman (OMFTA), CAFTA-DR, Peru (PETPA), Korea (KORUS), Colombia (COTPA), and Panama (PATPA apply a tariff shift and/or a RVC requirement for determining the origin of goods. See CBP Side-by-Side Comparison of Free Trade Agreements and Selected Preferential Trade Legislation Programs--Non-Textile. While other trade preference programs, such as Israel (ILFTA), Jordan (JOFTA), GSP, AGOA and CBERA all base their origin rule on the traditional substantial transformation rule and the change of “name, character, and use" test first enunciated in Anheuser-Busch Brewing Ass’n and in Gibson-Thomsen Co., Inc.)The Substantial Transformation Rule: Variations on a ThemeWhile the traditional substantial transformation rule and the change of “name, character, and use" test remains the lodestone of country of origin determinations, it is not without its variations.A Change in Name by Itself, Not so MuchFor instance, A name change, for example, is not always considered determinative. (United States v. International Paint Co., 35 C.C.P.A. 87, 93-94, C.A.D. 376 (1948)) Although it is clear that a change in name from "wire rod" to "wire" occurred in Superior Wire v. United States (when only a change in name is found, "such a change has rarely been dispositive"), this fact alone is not necessarily determinative of a substantial transformation. (Superior Wire, Div. of Superior Prods. Co. v. United States, 11 C.I.T. 608 (1987), aff'd, 867 F.2d 1409 (CAFC, 1989)) It may be supportive, however, of a finding of substantial transformation, as it did in Ferrostaal Metals v. United States, 11 C.I.T. 470; 664 F. Supp. 535 (1987). The name criterion is generally considered the least compelling of the factors that will support a finding of substantial transformation. National Juice Producers, ("a change in the name of the product is the weakest evidence of a substantial transformation"). Uniroyal, Inc. v. United States, 3 C.I.T. 220, 542 F. Supp. 1026 (1982), aff'd, 702 F.2d 1022 (CAFC, 1983) and United States v. International Paint Co. ("Under some circumstances a change in name would be wholly unimportant and equally so is a lack of change in name under circumstances such as [in this drawback case]."). See Ferrostaal Metals Corp., and Superior Wire.A Focus on Change in Use or CharacterIn recent years Customs and the courts have concentrated on change in use or character of the components or materials when processed into finished goods, and sometimes finding other various subsidiary tests appropriate to consider, depending on the situation at hand. (Energizer Battery, Inc. v. United States, 190 F. Supp. 3d 1308) Courts have held that when the properties and uses of a product are predetermined by the material from which it was made, no substantial transformation occurs. For example, in Superior Wire, wire rod in coils was shipped to Canada where it was drawn into wire. The court determined that the drawing operation did not result in a substantial transformation, pointing out that the properties of the wire rod and its uses were determined by the chemical content of the rod and the cooling processes used in its manufacture, and therefore, the wire rod dictated the final form of the finished wire."Character" is defined as the "mark, sign [or] distinctive quality" of a thing. Webster's Third New Int'l Dictionary of the English Language Unabridged (2002) at 376. For courts to find a change in character, there often needs to be a substantial alteration in the characteristics of the article or components. See, e.g., Ran-Paige Co., Inc. v. United States, 35 Fed. Cl. 117 (1996) and National Hand Tool Corp. v. United States, 16 C.I.T. 308 (1992). Changes that are deemed cosmetic are insufficient for a finding of substantial transformation. See, e.g., Superior Wire. The court previously has found a change in character when a "continuous hot-dip galvanizing process transformed a strong, brittle product which cannot be formed into a durable, corrosion-resistant product which is less hard, but formable for a range of commercial applications," Ferrostaal Metals, but not when the "form of the components remained the same" and a heating process "change[d] the microstructure of the material, but there was no change in the chemical composition." While there can be changes in the "characteristics of the material, they d[id] not change the character of the articles." Nat'l Hand Tool, 16 CIT at 311.In other cases, the court has attempted to ascertain the "essence" of a completed article to determine whether an imported article has undergone a change in character as a result of post-importation processing. (See Uniden America Corp. v. United States, 24 CIT 1191, 120 F. Supp. 2d 1091 (2000) a GSP case in which a cordless telephone consisted of 275 parts sourced in the Philippines and third-countries and an A/C adapter imported pre-assembled in China, where the court found that the A/C adapter did not impart the essential character of the cordless telephone and, thus, did not undermine the conclusion that the cordless telephone's other imported parts, once assembled together, had undergone a substantial transformation and were a product of a beneficiary developing country (BDC); see also Uniroyal where the court held that imported shoe uppers were the "essence of the finished shoe" and were not substantially transformed into something different by the addition of an outer sole in the United States.)In analyzing whether there is a change in use, the court has found that such a change occurred when the end use of the imported product was no longer interchangeable with the end use of the product after post-importation processing. (See Ferrostaal Metals where the court found "substantial changes in the use of the [imported cold-rolled] steel sheet as a result of the continuous hot-dip galvanizing process" because "the frequency with which the two types of steel compete with or are interchangeable with each other is 'very limited,' perhaps less than one or two percent.")However, when the end use was predetermined at the time of importation, courts have generally not found a change in use. See, e.g., Nat'l Hand Tool (when post-importation processing primarily consisted of an assemblyprocess, having one predetermined end use at the time of importation does not preclude a finding of substantial transformation; however, based on the totality of the evidence, the court did not find substantial transformation had occurred). See also Ran-Paige (when post-importation processing consisted primarily of attaching handles to pans and covers the court likened it to Nat'l Hand Tool when "plaintiff did not change the use of the components, especially given the fact that the use was predetermined at the time of importation") and see Uniroyal (the court did not find substantial transformation when the imported upper underwent no physical change, "[n]or was its intended use changed. It was manufactured by plaintiff in Indonesia to be attached to an outsole; it was imported and sold to Stride-Rite for that purpose; and Stride-Rite did no more than complete the contemplated process").Consideration of Subsidiary or Additional Factors附加因素的考量In addition to name, character, and use, the courts have also considered from time to time, subsidiary or additional factors, such as the extent and nature of operations performed, value added during post-importation processing, a change from producer to consumer goods, or a shift in tariff provisions. Consideration of subsidiary or additional factors is not consistent, and there is no uniform or exhaustive list of acceptable factors. For example, the court is split on whether to consider value added or costs incurred as a factor. See Superior Wire ("[a]n inquiry that is sometimes treated as a type of cross-check or additional factor to be considered in substantial transformation cases is whether significant value is added or costs are incurred by the process at issue"), but see Nat'l Hand Tool (rejecting value added as a factor because it "could lead to inconsistent marking requirements for importers who perform exactly the same processes on imported merchandise but sell at different prices").An article, however, need not experience a change in name, character, and use to be substantially transformed. All three of these elements need not be met before a court may find substantial transformation. Koru North America v. United States, (1988). SDI Technologies Inc., v. United States (1997). Likewise, components or materials that change in tariff classification is not dispositive, although it also may be supportive. (Belcrest Linens v. United States, 741 F.2d 1368, 1372 (CAFC, 1984)) An inquiry that is sometimes treated as a type of cross-check or additional factor to be considered in substantial transformation cases is whether significant value is added or costs are incurred by the process at issue. See United States v. Murray (1980).Courts have also attempted to distinguish between minor manufacturing and combining operations or simple assembly, and processing that is more complex. See and compare Uniroyal, Belcrest Linens and Ran-Paige.Substantial Transformation and Post-Importation Assemble of ComponentsWhen the post-importation processing consists of assembly, courts have been reluctant to find a change in character, particularly when the imported articles do not undergo a physical change. See, e.g., Uniroyal. In cases in which the post-importation processing entails assembly, courts have considered the nature and complexity of the assembly together with the name, character, or use test in making a substantial transformation determination. See Ran-Paige; Belcrest Linens; Uniroyal. The Federal Circuit, in Belcrest Linens, considered the difference between minor manufacturing and combining operations and substantial transformation when stenciled, marked and embroidered bolts of cloth were cut into individual pieces, scalloped, folded, sewn, pressed and packaged, and found that substantial transformation occurred based on "the extent of the operations performed and whether the parts lose their identity and become an integral part of a new article." Belcrest Linens.When assembly operations, however, are manual and required some "skill and dexterity to put components together with a screw driver" but the names of each article and the form and character of each component remained unchanged, and the use of the imported articles was predetermined at the time of importation, the court concluded that substantial transformation had not occurred. See Nat'l Hand Tool.但是,当组装操作是手动的并且需要一定的“技巧和灵活性用螺丝刀将组件组装在一起”时,而每个商品的名称以及每个组件的形式和特征都保持不变,并且进口商品的使用已在进口时预先确定,则法院认为尚未发生实质性的转变。