金融经济学第二章补充习题

金融学精编版第二版[货币银行学]第2章课后答案

![金融学精编版第二版[货币银行学]第2章课后答案](https://img.taocdn.com/s3/m/c4057f35f78a6529657d5339.png)

第二章信用1.你过去对于信用这个经济范畴是怎样理解的?应该怎样界定信用较好?答:(1)过去对信用这个经济范畴的理解是,信用相当于“借贷”或“债”的概念,等等。

(2)按照下面的方式来界定信用比较好:信用这个经济范畴是指借贷行为。

从逻辑上推论,私有财产是的出现是借贷关系存在的前提条件。

这种经济行为的形式特征是以收回为条件的付出,或以归还为义务的取得;而且贷者之所以贷出,是因为有权取得利息,借者之所以可能借入,是因为承担了支付利息的义务。

现实生活中有时也有无利息的借贷,但这是由于某种政治目的或经济目的而采取的免除利息的优惠,是一般中的特殊。

西方不少国家的银行对企业的活期存款也往往不支付利息,但存款者可以享受银行的有关服务和取得贷款的某些权利,实际上还是隐含有利息的。

2.经济学意义上的“信用”,与日常生活和道德规范里的“信用”,有没有关系,是怎样的关系?答:道德范畴中的“信用”指的是诚信,是经济主体通过诚实履行自己承诺而取得他人的信任。

从经济意义上看,信用的含义就转化和延伸为以借贷为特征的经济行为,是以还本付息为条件的,体现着特定的经济关系。

它既区别于一般商品货币交换的价值运动形式,又区别于财政分配等其他特殊的价值运动形式,是不发生所有权变化的价值单方面的暂时让渡或转移。

这两个范畴的信用密切相关。

诚信是交易、支付和借贷活动得以顺利进行的基础。

借贷活动是以收回为条件的付出,或以归还为义务的取得;而且贷者之所以贷出,是因为有权取得利息,借者之所以可能借入,是因为承担了支付利息的义务。

如果没有当事人之间的最基本的信任,就不会发生借贷活动。

诚信是借贷活动的基础。

如果失信成为信用行为中的主导方面,借贷活动就会萎缩甚至中断。

而借贷活动的发展,使得经济活动参与者日益意识到诚信的重要性,进而使诚信成为经济生活的重要准则之一。

3.为什么说在现代经济生活中,信用联系几乎无所不在,以至可以称为“信用经济”?能否谈谈你本人的体验?答:(1)将现代经济说成信用经济是对现代经济的一种描述。

金融学第二版课后习题答案

金融学第二版课后习题答案金融学第二版课后习题答案金融学是一门研究金融市场、金融机构和金融工具的学科,它对于理解和解决现代金融问题具有重要意义。

而课后习题则是帮助学生巩固所学知识、提高解决问题能力的重要工具。

本文将为读者提供金融学第二版课后习题的答案,以帮助读者更好地理解金融学的概念和理论。

第一章:金融的基本概念和职能1. 金融的基本概念是指金融的定义和范围。

金融的定义是指金融活动和金融制度的总称。

金融的范围包括金融市场、金融机构和金融工具等。

2. 金融的职能是指金融对于经济发展和社会进步的作用。

金融的主要职能包括储蓄和融资、支付和结算、风险管理和信息中介等。

第二章:金融市场1. 金融市场的分类包括货币市场、资本市场和衍生品市场等。

货币市场是指短期资金融通的市场,资本市场是指长期资金融通的市场,衍生品市场是指金融衍生品交易的市场。

2. 金融市场的功能包括资源配置、风险管理和信息传递等。

资源配置是指将资金从供给者转移给需求者的过程,风险管理是指通过金融市场进行风险的转移和分散,信息传递是指金融市场通过价格和交易信息传递经济信息。

第三章:金融机构1. 金融机构的分类包括银行、非银行金融机构和金融市场机构等。

银行是最重要的金融机构,它包括商业银行、中央银行和政策性银行等。

2. 金融机构的职能包括储蓄和融资、支付和结算、风险管理和信息中介等。

储蓄和融资是指金融机构接受存款并提供贷款的过程,支付和结算是指金融机构提供支付和结算服务的过程,风险管理是指金融机构通过风险评估和风险转移来管理风险,信息中介是指金融机构通过收集、加工和传递信息来提供金融服务。

第四章:金融工具1. 金融工具的分类包括货币工具、债券、股票和衍生品等。

货币工具是指短期借贷和短期投资的金融工具,债券是指借款人向债权人发行的债务凭证,股票是指公司向股东发行的所有权凭证,衍生品是指衍生自其他金融资产的金融工具。

2. 金融工具的特点包括流动性、收益性和风险性等。

金融学各章练习题电子教案

金融学各章练习题第1章货币与货币制度、选择题:1、“金银天然不是货币,但货币天然是金银”是指(C )A、货币就是金银B、金银就是货币C、金银天然地最时宜于充当货币D、金银不是货币2、货币在发挥( A )职能时,可以用观念上的货币。

A、价值尺度B、流通手段 C贮藏手段D、支付手段3、信用货币的产生源于货币的哪种职能?( D)A价值尺度 B、流通手段 C、贮藏手段D、支付手段4、典型意义上的贮藏手段是针对( D )而言的。

A、信用货币B、电子货币C、银行券D、金银条块5、商品价值的实现要通过货币的何种职能?( B )A价值尺度 B流通手段 C支付手段 D世界货币6、下述行为中,哪个属于货币执行流通手段职能?( B)A、分期付款购房B、饭馆就餐付帐C、缴纳房租、水电费D、企业发放职工工资7、建立货币制度最关键的步骤是( A )A、确定币材B、通货铸造C、确定发行与流通程序D、黄金储备充足8、在以下几种货币制度中,相对稳定的货币制度是( C )A、银本位B、金银复本位C、金本位D、金块本位9、规定黄金由政府储存,居民可在银行券达到规定的数额时才可兑换黄金的是哪种货币制度?( C )A、平行本位制B、金汇兑本位制C、金块本位制D、纸币本位制10、如果国家规定的金银比价为1:10,而市场形成的比价为1:16,这时市场中的( A )将逐渐被驱除。

A金币 B、银币 C、银行券 D、其他11、格雷欣法则起作用是在( C )下。

A、跛行本位制B、平行本位制C、双本位制D、金本位制12、格雷欣法则中,被称为劣币的是( B )A、市场价格>法定价格B、市场价格<法定价格C、市场价格=法定价格D、都不是13、目前各国划分货币层次的主要依据普遍是金融资产的( B )A、安全性B、流动性C、收益性D、全都是二、多项选择题1、货币的两个基本职能是( AB )A、价值尺度B、流通手段C、支付手段D、贮藏手段E、世界货币2、纸币的特点是( ABCDE )A、产生于货币的价值尺度职能B、它本身无价值C、它是货币符号D、它需要强制流通E、它也具有与其他商品相交换的能力3、当今信用货币的主要构成有( ABCD )。

金融经济学(王江)习题解答讲解学习

金融经济学(王江)习题解答金融经济学习题解答王江(初稿,待修改。

未经作者许可请勿传阅、拷贝、转载和篡改。

)2006 年 8 月第2章基本框架2.1 U(c) 和V (c) 是两个效用函数,c2 R n+,且V (x) = f(U(x)),其中f(¢) 是一正单调函数。

证明这两个效用函数表示了相同的偏好。

解.假设U(c)表示的偏好关系为º,那么8c1; c22R N+有U(c1) ¸ U(c2) , c1 º c2而f(¢)是正单调函数,因而V (c1) = f(U(c1)) ¸ f(U(c2)) = V (c2) , U(c1) ¸ U(c2)因此V(c1)¸V(c2),c1ºc2,即V(c)表示的偏好也是º。

2.2* 在 1 期,经济有两个可能状态a和b,它们的发生概率相等:ab考虑定义在消费计划c= [c0;c1a;c1b]上的效用函数:U(c) = log c0 + 1 (log c1a + log c1b)³´U(c) =1c01¡°+211c11a¡°+1c11b¡°1¡°1¡°1¡°U(c) = ¡e¡ac0¡21¡e¡ac0+e¡ac0¢证明它们满足:不满足性、连续性和凸性。

解.在这里只证明第一个效用函数,可以类似地证明第二、第三个效用函数的性质。

(a) 先证明不满足性。

假设c¸c0,那么有c0 ¸ c00; c1a ¸ c01a; c1b ¸ c01b而log(¢)是单调增函数,因此有log(c0) ¸ log(c00); log(c1a) ¸ log(c01a); log(c1b) ¸ log(c01b)因而U(c)¸U(c0),即cºc0。

金融学 第二章-信用-习题与答案

四简答题

比较商业信用与银行信用的特点,二者兼有怎样的联系?

答:与公司、企业的经营活动直接联系的信用有两种形式:商业信用和银行信用。

(1)商业信用:典型的商业信用是工商企业以赊销方式对购买商品的工商企业所提供的信用。不仅在各国国内交易中广泛存在,并且也广泛存在于国际贸易之中,对于推动商品交易和经济增长有着重要意义。在典型的商业信用中,实际包括两个同时发生的经济行为:买卖行为和借贷行为。就买卖行为来说,在发生商业信用之际就已完结,即该产品从工厂所有变成商店所有,就与通常现款买卖一样,而在此之后,它们之间只存在一定货币金额的债权债务关系。

A信托信用B银行信用

C商业信用D国家信用

9商业信用是企业之间由于( )而相互提供信用。

A生产联系B产品调剂

C货物交换D商品交易

10诸多信用形式中,最基本的信用形式是( )。

A国家信用B商业信用

C消费信用D银行信用

11.信用工具具有以下( )特征。

A变现力B本金的安全性

C收益率D偿还期

12下列属于直接金融工具的是( )。

A商业承兑汇票B大额可转让定期存单

C银行债券D企业债券

四、问答题

比较商业信用与银行信用的特点,二者间有怎样的联系?

第四部分同步练习题参考答案

一、名词解释

1.信用:指借贷行为,这种经济行为的形式特征是以收回为条件的付出,或以归还

为义务的取得;而且贷者之所以贷出,是因为有权取得利息,借者之所以可能借入,

精品文档就在这里各类专业好文档值得你下载教育管理论文制度方案手册应有尽有精品文档第二章信用第一部分本章内容结构信用是以偿还和付息为基本特征的借贷行为属于商品货币关系的一个经济范畴

金融经济学 课后习题答案

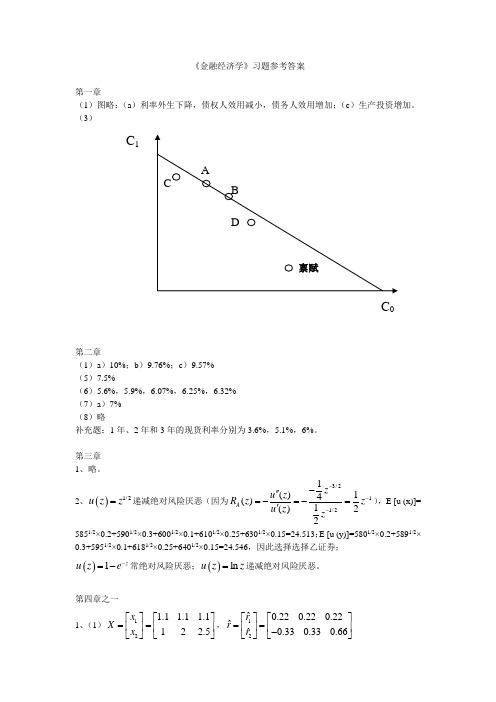

《金融经济学》习题参考答案第一章(1)图略:(a )利率外生下降,债权人效用减小,债务人效用增加;(c )生产投资增加。

(3)第二章(1)a )10%;b )9.76%;c )9.57%(5)7.5%(6)5.6%,5.9%,6.07%,6.25%,6.32%(7)a )7%(8)略补充题:1年、2年和3年的现货利率分别为3.6%,5.1%,6%。

第三章1、略。

2、()1/2u z z =递减绝对风险厌恶(因为3/211/21()14()1()22A z u z R z z u z z ----''=-=-='),E [u (x)]= 5851/2×0.2+5901/2×0.3+6001/2×0.1+6101/2×0.25+6301/2×0.15=24.513;E [u (y)]=5801/2×0.2+5891/2× 0.3+5951/2×0.1+6181/2×0.25+6401/2×0.15=24.546,因此选择选择乙证券;()1z u z e -=-常绝对风险厌恶;()ln u z z =递减绝对风险厌恶。

第四章之一1、(1)12 1.1 1.1 1.112 2.5x X x ⎡⎤⎡⎤==⎢⎥⎢⎥⎣⎦⎣⎦,12ˆ0.220.220.22ˆˆ0.330.330.66r r r ⎡⎤⎡⎤==⎢⎥⎢⎥-⎣⎦⎣⎦C 0C 1(2)价格13.5;()()0.220.220.22ˆˆ0.330.670.1470.2930.5130.330.330.67T p r w r ⎡⎤===-⎢⎥-⎣⎦2、(1)0.20.5r ⎛⎫= ⎪⎝⎭,211222120.010.0030.0030.09V σσσσ⎛⎫⎛⎫== ⎪ ⎪⎝⎭⎝⎭(2)()0.2ˆ()0.6210.37931.3%0.5T p E rw r ⎛⎫=== ⎪⎝⎭, ()20.010.0030.6210.6210.3790.01820.0030.090.379P σ⎛⎫⎛⎫== ⎪⎪⎝⎭⎝⎭第四章之二例4.3.2.11196.1232.3886.74632.3817.5929.91586.7469.91574.557V ---⎛⎫ ⎪=- ⎪ ⎪-⎝⎭A=10.756,B=2.21,C=69.846,D=38.72,3.2770.6511.626g ⎛⎫ ⎪=- ⎪ ⎪-⎝⎭,14.1223.76610.346h -⎛⎫ ⎪= ⎪ ⎪⎝⎭3.27714.122ˆ0.651 3.766[]1.62610.346p p w E r -⎛⎫⎛⎫ ⎪ ⎪=-+ ⎪ ⎪ ⎪ ⎪-⎝⎭⎝⎭例4.3.2.2()()22ˆˆ[]0.15410.0140.008p p r E r σ--=例4.3.4.1H=1.462,ˆˆ[]4% 1.21()p p E rr σ=+第五章(6)a )2 1.29AM AM M σβσ==甲甲甲,2 1.53AM AM M σβσ==乙乙乙 b )iiic )A=117.037,B=27.111,C=523.457,D=493.827。

上交大《金融学》第二章 课后习题答案

第二章信用复习思考题1.什么是信用?信用是如何产生的?所谓信用就是以偿还和付息为特征的借贷行为,具体来说就是商品或货币的所有者,把商品或货币让渡给需要者,并约定一定时间内由借者还本付息的行为。

私有制出现以后,社会分工不断发展,大量剩余产品不断出现。

私有制和社会分工使得劳动者各自占有不同的劳动产品,剩余产品的出现则使交换行为成为可能。

随着商品生产和交换的发展,商品流通出现了矛盾,“一手交钱一手交货”的方式由于受到客观条件的限制经常发生困难。

例如,一些商品生产者出售商品时,购买者却可能因自己的商品尚未卖出而无钱购买。

于是赊销即延期支付的方式应运而生。

赊销意味着卖方对买方未来付款承诺的信任,意味着商品的让渡和价值实现发生时间上的分离。

这样,买卖双方除了商品交换关系之外,又形成了一种债权债务关系,即信用关系。

当赊销到期、支付货款时,货币不再发挥其流通手段的职能而只充当支付手段,这种支付是价值的单方面转移。

正是由于货币作为支付手段的职能,使得商品能够在早已让渡之后独立地完成价值的实现,从而确保了信用的兑现。

整个过程实质上就是一种区别于实物交易和现金交易的交易形式,即信用交易后来,信用交易超出了商品买卖的范围。

作为支付手段的货币本身也加入了交易过程,出现了借贷活动。

从此,货币的运动和信用关系联结在一起,并由此形成了新的范畴——金融。

现代金融业正是信用关系发展的产物。

在市场经济发展初期,市场行为的主体大多以延期付款的形式相互提供信用,即商业信用;在市场经济较发达时期,随着现代银行的出现和发展,银行信用逐步取代了商业信用,成为现代经济活动中最重要的信用形式。

总之,信用交易和信用制度是随着商品货币经济的不断发展而建立起来的;进而,信用交易的产生和信用制度的建立促进了商品交换和金融工具的发展;最终,现代市场经济发展成为建立在错综复杂的信用关系之上的信用经济。

2.商业信用的特点、局限性有哪些?商业信用的特点商业信用的特点表现为以下几点:(1)商业信用的债权债务人都是企业经营者。

《金融学》第二章答案金融系统

《金融学》第二章答案金融系统CHAPTER 2THE FINANCIAL S YS TEMObjectivesTo provide a conceptual framework for understanding how the financial system works and how it changes over time.To understand the meaning and determinants of rates of return on different classes of assets.Outline2.1 What Is the Financial System?2.2 The Flow of Funds2.3 The Functional Perspective2.4 Financial Innovation and the “Invisible Hand”2.5 Financial Markets2.6 Financial Market Rates2.7 Financial Intermediaries2.8 Financial Infrastructure and Regulation2.9 Governmental and Quasi-Governmental OrganizationsSummaryThe financial system is the set of markets and intermediaries used by households, firms, and governments to implement their financial decisions. It includes the markets for stocks, bonds, and other securities, as well as financial intermediaries such as banks and insurance companies.Funds flow through the financial system from entities that have a surplus of funds to those that have a deficit.Often these fund flows take place through a financial intermediary.There are six core functions performed by the financialsystem:1.To provide ways to transfer economic resources through time, across borders, and among industries.2.To provide ways of managing risk.3.To provide ways of clearing and settling payments to facilitate trade.4.To provide a mechanism for the pooling of resources and for the subdividing of shares in variousenterprises.5.To provide price information to help coordinate decentralized decision-making in various sectors of the economy.6.To provide ways of dealing with the incentive problems created when one party to a transaction hasinformation that the other party does not or when one party acts as agent for another.The fundamental economic force behind financial innovation is competition, which generally leads to improvements in the way financial functions are performed. The basic types of financial assets traded in markets are debt, equity, and derivatives.Debt instruments are issued by anyone who borrows money—firms, governments, and households.Equity is the claim of the owners of a firm. Equity securities issued by corporations are called common stocks.Derivatives are financial instruments such as options and futures contracts that derive their value from the prices of one or more other assets.An interest rate is a promised rate of return, and there are as many different interest rates as there are distinct kinds of borrowing and lending. Interest rates vary depending on the unitof account, the maturity, and the default risk of the credit instrument. The nominal interest rate is the promised amount of money you receive per unit you lend.The real rate of return is defined as the nominal interest rate you earn corrected for the change in the purchasing power of money. For example, if you earn a nominal interest rate of 8% per year and the rate of price inflation is also 8% per year, then the real rate of return is zero.There are four main factors that determine rates of return in a market economy:the productivity of capital goods—expected rates of return on mines, dams, roads, bridges, factories, machinery, and inventories,the degree of uncertainty regarding the productivity of capital goods,time preferences of people—the preference of people for consumption now versus consumption in the future, and risk aversion—the amount people are willing to give up in order to reduce their exposure to risk.Indexing is an investment strategy that seeks to match the returns of a specified stock market index.Financial intermediaries are firms whose primary business is to provide customers with financial products that cannot be obtained more efficiently by transacting directly in securities markets. A mong the main types of intermediaries are banks, investment companies, and insurance companies. Their products include checking accounts, loans, mortgages, mutual funds, and a wide range of insurance contracts.Solutions to Problems at End of Chapter1. Do you agree with Adam Smith’s view that society canrely more on the “invisible hand” than on government to promote economic pros perity?Student answers will vary of course.SAMPLE ANSWER:The communist system is the exact opposite of Adam Smith’s invisible hand. And of course we have recently seen the downfall of many of the communist countries around the world. In the communist world, it was believed that government could make better decisions promoting economic prosperity than individuals could. Clearly this system failed to promote economic prosperity. It seems that Adam Smith’s view was that competitive market systems as a whole (rather than government) could best allocate resources to promote economic prosperity. However, a completely unfettered capitalist society such as in the late 1800s in the Western world may n ot have been the perfect system either as the invisible hand helped the “rich get richer” while the poor and needy had no formal assistance. This outraged the moral fabric of society and government programs were eventually set up to formally address thisi ssue of general welfare and “fairness”.2. How does the financial system contribute to economic security and prosperity in a capitalist society?In a capitalist society, it is the price system which helps make capital resource decisions. Capital flows to those operations which can employ it to earn the highest rate of return. This therefore allocates capital to its most productive use, thereby enhancing society’s economic prosperity.In addition, the financial system has markets and intermediaries which transfer risks from those who are least willing to bear it to those who are most willing to bear it. This benefits society as a whole withoutcosting it anything. In addition, by allowing individuals to reduce or eliminate risks, it fosters an atmosphere of undertaking business ventures which also benefits society.3. Give an example of how each of the six functions of the financial system are performed more efficiently today than they were in the time of Adam Smith (1776).Clearing and settling payments:In Adam Smith’s day, just as today there was paper and coin currency. However, due to technological innovations (primarily the computer) today there are many additional forms of payment settlement such as personal checks, credit cards, debit cards and electronic transfer of funds. In addition, certain credit cards and traveler’s checks are accepted everywhere in the world making currency exchange a relic of the past. Pooling resources and subdividing shares:In Adam Smith’s day, most businesses were s mall and were financed by sole proprietorships. Therefore the need to pool resources to finance large investments was not as prevalent or as important as it is today. Again, the technological revolution of computers and telephones allow for global capital marke ts to efficiently finance today’s much larger businesses. Today these companies can access huge pools of money around the world and find the cheapest source of financing for large scale projects.Transfer economic resources: Today there is a worldwide financial system which facilitates the transfer of resources and risk from one individual to another and from one point in time to another. In Adam Smith’s day, although there were financial markets which played a limited role, they were localized, small and much less efficient and innovative than they are today.Managing risk: Of course during Adam Smith’s day individuals and businesses faced many of the same risks they dotoday (risk of property damage, risk of financial loss, risk of crop failure etc.) Ho wever, there were limited means to offset this risk. There were some insurance companies in place at that time, however, they concentrated on managing business risk rather than personal risk and certainly there was not the same type of insurance. A good ex ample is that in Adam Smith’s day, there was no unemployment insurance. In Adam Smith’s day, there was very little a farmer could do about reducing his risk of crop failure or lower crop prices. Today there are a vast number of markets and securities which can be used to offset individual and business risk as well as a huge network of insurance companies whose role is to transfer risk from those who want to reduce risk to those who want to take on more risk.Price information: During Adam Smith’s day, info rmation traveled slowly. Of course, there were no phones, televisions or radios. News traveled by newspaper and by the mail. Today, information travels around the worldinstantaneously. Due primarily to the growth and innovation in computer and telephone t echnology, information about security prices and performance is known at virtually the same time everywhere around the world.Incentive problems: As discussed above, today’s financial sy stem is large, innovative and global. In Adam Smith’s day, while there were problems of moral hazard and adverse selection (but less of a principal-agent problem) there was not the same financial system and sophistication to deal with these problems as there is today.4. How does a competitive stock market accomplish the result that Adam Smith describes? Should the stock market be regulated? How and why?Student answers will vary.SAMPLE ANSWER:Adam Smith talked about free and competitive markets as a system which allocates capital to its most productive use and greatest value. In a competitive stock market, prices are set through supply and demand. Those companies returning the highest return will be rewarded with the highest prices (or cheapest source of financing). Those companies which are under performing will not be allocated as much capital because they are not as productive. Because the universe of possible investments is huge and because it is at times difficult for investors to discern which companies are the most productive employers of capital, regulation shou ld be required to make sure relevant and standardized information is disseminated to potential investors. This would include regulation on disclosure and also insider trading and stock manipulation. However other forms of market regulation are perhaps not so important from a market efficiency point of view and may even impede society’s overall financial welfare.5. Would you be able to get a student loan without someone else offering to guarantee it?Since most students do not have any earning power (yet) or source of savings or other capital, it is doubtful any intermediary would take that credit risk at any reasonable interest rate.6. Give an example of a new business that would not be able to get financing if insurance against risk were not available.EXAMPLES:Chemical companyChild safety products companyAirlineBankHospitalEnvironmental consultingHazardous waste disposal7. Suppose you invest in a real-estate development deal. The total investment is $100,000. You invest $20,000 of your own money and borrow the other $80,000 from the bank. Who bears the risk of this venture and why?The $20,000 of my own money is considered the equity capital and the $80,000 is debt financing. In general it is the equity investors who absorb the primary risk of business failure. This is because if the business goes bankrupt, I will unlikely get any or my money back as the debt holders get paid back before I do. However, the debt holder also faces some risk that it will not even get back all its principal and interest. So lenders do share some of the business risk along with the equity investors.8. You are living in the United States and are thinking of traveling to Germany 6 months from now. You can purchase an option to buy marks now at a fixed rate of $0.75 per mark 6 months from now. How is the option like an insurance policy?An option means you have a choice. In this example you can choose to buy the marks at $0.75 in 6 months but you do not have to. You will only buy the marks at this price if it is cheaper for you to do so (if the spot market at that time is higher). Therefore, like an insurance policy you are protected against a potential loss. You know that the maximum price you will have to pay is $0.75 per mark and that you are protected against any higher price. Presumably you will have to pay something for the price of that option and that can be equated to an insurance premium.9. Give an example of how the problem of moral hazard might prevent you from getting financing for something you want to do. Can you think of a way of overcoming this problem?SAMPLE ANSWER:Suppose I want to start a biotechnology business and I need a lot of financing. The trouble is, I do not want to disclose my technology secrets to potential equity and debt investors. I will have great difficulty raising financing. But I could do the following: At a minimum, I could require all potential lenders and investors to sign agreements saying they will not disclose any of my secrets. Secondly, I could share some of my equity with potential lenders (equity-kickers) and investors (stock and stock options). At least that way they will not be motivated to disclose my secrets to others. Finally, if I decided I did not want to share secrets, I could give collateral in my new plant to the debt lenders and that might make them more comfortable with the issue of moral hazard.10. Give an example of how the problem of adverse selection might prevent you from getting financing for something you want to do. Can you think of a way of overcoming this problem?SAMPLE ANSWER:Suppose I want to start a car leasing business. Initially my plan was to purchase several automobiles and lease them out at attractive annual rates. However, potential lenders were worried that my business would attract individuals who drive great distances each year. Rather than buy their own car and lose significant value, they would lease my cars and take a new one each year. I would not be able to obtain financing for this business until I instituted annual mileage restrictions. This alteration in the business plan was enough to make the lenderscomfortable with the potential problem of adverse selection.11. Give an example of how the principal-agent problem might prevent you from getting financing for something you want to do. Can you think of a way of overcoming this problem?SAMPLE ANSWER:Suppose you want to start a personal care products company. However, you have the idea for the business, but you do not want to actually run the business. To do that you have hired an executive from a competitor. He will own no equity in the business but will be paid a salary of $100,000 to start up the business.Trouble with this example is that the executive you have hired has little incentive to make the business really work other than his salary (which presumably he could earn at many different companies). What if this executive is really a spy? It may be difficult to get financing for this venture. The way to solve the problem is if you the owner decide to run the business (you certainly are motivated for it do well) or at a minimum, grant your new employee stock or stock options in the business.12. Why is it that a country’s postage stamps are not as good a medium of exchange as its paper currency? Postage stamps would be much easier to copy (to counterfeit) than paper currency which has intricate designs and is made of special fibers (not easily duplicated). Secondly, postage stamps would not be as durable as paper currency and because of their other use, could easily stick to other items! Finally, because postage stamps are used for another purpose, one might run out of them and have to make a special trip to the post office to get more. Of course, the post office is not as convenient as an ATM machine for getting a new supply of currency.13. Who is hurt if I issue counterfeit U.S. dollars and use them to purchase valuable goods and services?If this were done in great size, everyone would be hurt through the inflation that would result in the increased money supply. However, if done in a s mall amount, the individuals accepting the currency are taking on the risk (without knowing it) that the dollars will not be accepted by others as a medium of exchange.14. Some say the only criterion to use in predicting what will serve as money in the future is the real resource cost of producing it, including the transaction costs of verifying its authenticity. According to this criterion what do you think will be the money of the future?SAMPLE ANSWER:Payments via electronic transfer may become the medium of choice. It is a very cheap way to create currency. The biggest challenge will be to create security systems that do not allow for tampering and fraud. Once this is done and once most individuals and retail establishments have access to the system (through bank accounts and linking computer systems) then this should become the “currency” of choice.15. Should all governments issue debt that is indexed to their domestic price level? Is there a moral hazard problem that citizens face with regard to their public officials when government debt is fixed in units of the domestic currency?The answer is that all governments should issue debt that is indexed to their domestic price level. This is due to the fact that if debts are not indexed to the domestic price level, governments have the incentive to print money to repay those debts, thereby increasing domestic inflation which negatively impacts all ofsociety.16. Describe your country’s sy stem for financing higher education. Wh at are the roles played by households, voluntary non-profit organizations, businesses and government?SAMPLE ANSWER:In the United States, the vast majority of higher education is paid for by individuals through savings. These sums can be supplemented in whole or in part by government-guaranteed loans and through student loans and scholarships provided by universities themselves as well as by private foundations such as those provided by the Fulbright scholarship.17. Describe your country’s system for fin ancing residential housing. What are the roles played by households, businesses and government?SAMPLE ANSWER:In the United States individuals and individual borrowings from savings and loans, commercial banks and mortgage lending companies finance the vast majority of residential housing through individual equity savings. The government guarantees a certain amount of low income mortgages and local governments finance some low-income housing. Businesses play a role through the lending business as well as through the financial markets which provide liquidity for portfolios of certain standardized mortgages.18. Describe your country’s system for financing new enterprises. What are the roles played by households, businesses and government?SAMPLE ANSWER:In the United States, the vast majority of new enterprises is financed through individual savings and through initial publicofferings made to the general public. These sources of financing are augmented by established firms which spend research and development (R&D) dollars developing new products and businesses and by venture capital institutions which also provide start-up financing.19. Describe your country’s system for financing medical research. What are the roles played by voluntary non-profit organizations, businesses and government?SAMPLE ANSWER:In the United States, medical research is financed both by non-profit organizations (such as universities and medical facilities as well as organizations such as the American Heart Association) as well as by businesses such as Merck, Johnson & Johnson and Genentech. The government is involved in research grants, primarily to universities.20. Assume there are only two stocks traded in the stock market, and you are trying to construct an index to show what has happened to stock prices. Let us say that in the base year the prices were $20 per share for stock 1 with 100 million shares outstanding and $10 for stock 2 with 50 million shares outstanding. A year later, the prices are $30 per share for stock 1 and $2 per share for stock 2. Using the two different methods explained in the chapter, compute stock indexes showing what has happened to the overall stock market. Which of the two methods do you prefer and why? (See appendix that follows.) DJI-Type Index = Average of Current Prices/Average of Base Prices * 100 = 106.67S&P-Type Index = (Weight of Stock 1 * Current Price of Stock 1 / Base Price of Stock 1 + Weight of Stock 2 * Current Price of Stock 2/Base Price of Stock 2) * 100 = 124The S&P-Type Index accurately reflects what has happened to the total market value of all stocks.。

王江《金融经济学》课后习题全部答案

U (c)

=

log

c0

+

1 2

(log

c1a

+

log

c1b)

�

�

U (c)

=

1 1−γ

c10−γ

+

1 2

1 1−γ

c11−a γ

+

1 1−γ

c11−b γ

U (c) = −e−ac0 − 1 �e−ac0 + e−ac0 �

2

证明它们满足�不满足性、连续性和凸性。

解. 在这里只证明第一个效用函数�可以类似地证明第二、第三个效用函数的性 质。

+

(1

−

α)c1b)

≥

α(log(c0� )

+

1 2

log(c1� a)

+

1 2

log(c1� b))

+

(1

−

α)(log(c0)

+

1 2

log(c1a)

+

1 2

log(c1b))

= αU (C�) + (1 − α)U (C) > U (C�)

故凸性成立。

2.3

U

(c)

=

c

−

1 2

a

c2

是一可能的效用函数�其中

(b) 参与者的预算集是 {C ∈ R2+ : c0 = 100 − S, c1 = 1 + S(1 + rF ), S ∈ R}�如果

以当前消费为单位�他的总财富是

w

=

100

+

1 1+rF

。参与者的优化问题就是

金融经济学第二章补充习题

金融经济学第二章补充习题1、假设在明天有两个状态,天晴和下雨。

我们考虑两个消费计划:计划c 是天晴在海滩玩4个小时,下雨就看4个小时电视。

计划c ’是天晴在海滩玩2个小时然后再看2个小时电视,下雨就看4个小时电视。

假设参与者更喜欢c 而不是c ’。

现在,我们提供另两个选择,c ’’和c ’’’:c ’’是天晴在海滩玩4个小时,下雨工作4个小时。

C ’’’是天晴在海滩玩2个小时然后再看2个小时电视,下雨工作4个小时。

他会选择哪一个?依据哪一条公理?下雨的时候具体发生什么对在天晴的时候的偏好是否有影响?2、令()''()/'()R w wu w u w ≡-,假设0w >、'()0u > 、"()0u ≤,证明:如果1λ>,给定效用函数()u 且'()0R w ≥。

定义1()()u w u w λ≡,2()()u w u w ≡,那么12()()R w R w ≥。

3、参与者的初始财富为w ,现在他要承担风险g,g 是有可能取值-b 和b 的公平赌博,0b w <<。

我们用两种方式定义风险补偿:●1[()]()E u w g u w χ+=- ● 2[()]()E u w gu w χ++= 用这两种定义计算的风险补偿,它们相等吗?解释所得到的结论。

4、参与者的初始财富为w 且是严格风险厌恶的。

1g和2g 是两个独立的公平赌博,具有相同的,定义于{,}b b -上的二项分布,其中0/2b w <<。

(a )假设他必须承担风险1g,即他的财富变成1w g + 。

在这种情况下,他的期望效用记为11[()]V E u w g=+ 。

证明风险使得他的情况恶化,即1()V u w <。

(b )现在假设他必须承担的是分散化的风险121()2g g g =+ 。

记这种情况下的期望效用为2[()]V E u w g =+ ,2V 是否是高于1V ?请证明。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

金融经济学第二章补充习题

1、假设在明天有两个状态,天晴和下雨。

我们考虑两个消费计划:计划c 是天晴在海滩玩4个小时,下雨就看4个小时电视。

计划c ’是天晴在海滩玩2个小时然后再看2个小时电视,下雨就看4个小时电视。

假设参与者更喜欢c 而不是c ’。

现在,我们提供另两个选择,c ’’和c ’’’:c ’’是天晴在海滩玩4个小时,下雨工作4个小时。

C ’’’是天晴在海滩玩2个小时然后再看2个小时电视,下雨工作4个小时。

他会选择哪一个?依据哪一条公理?下雨的时候具体发生什么对在天晴的时候的偏好是否有影响?

2、令()''()/'()R w wu w u w ≡-,假设0w >、'()0u > 、"()0u ≤

,证明:如果1λ>,给定效用函数()u 且'()0R w ≥。

定义1()()u w u w λ≡,2()()u w u w ≡,那么12()()R w R w ≥。

3、参与者的初始财富为w ,现在他要承担风险g

,g 是有可能取值-b 和b 的公平赌博,0b w <<。

我们用两种方式定义风险补偿:

●

1[()]()E u w g u w χ+=- ● 2[()]()E u w g

u w χ++= 用这两种定义计算的风险补偿,它们相等吗?解释所得到的结论。

4、参与者的初始财富为w 且是严格风险厌恶的。

1g

和2g 是两个独立的公平赌博,具有相同的,定义于{,}b b -上的二项分布,其中0/2b w <<。

(a )假设他必须承担风险1g

,即他的财富变成1w g + 。

在这种情况下,他的期望效用记为11[()]V E u w g

=+ 。

证明风险使得他的情况恶化,即1()V u w <。

(b )现在假设他必须承担的是分散化的风险121()2

g g g =+ 。

记这种情况下的期望效用为2[()]V E u w g =+ ,2V 是否是高于1V ?请证明。