外商投资企业外方权益确认表审核业务约定书-中英对照

外商投资企业外方权益确认表审核业务约定书

外商投资企业外方权益确认表审核业务约定书甲方:乙方:XXXX会计师事务所有限公司甲方(以下简称“贵公司”)与XXXX会计师事务所有限公司(以下简称“本所”)的对外商投资企业外方权益确认表(以下简称“外方权益确认表”)审核业务约定书用以明确我们提供服务的性质和范围,双方的责任及义务,有关服务收费的约定以及其他保证我们专业服务能够达到与贵公司共同商定目标的条款和条件。

1.业务范围与目标本所接受贵公司委托,对贵公司管理当局20 年12月31日外方权益确认表进行审核,并就上述外方权益确认表是否在所有重大方面符合国家外汇管理局法规规定的编报要求发表意见。

本所将根据国家外汇管理局XX省分局闽汇【2012】46号的规定对外方权益确认表实施审核工作。

2. 贵公司管理层的责任及义务贵公司及其管理层有责任保证审核资料的真实性、合法性及完整性,且有责任妥善备存和本业务有关的全部资料;为本所派出的有关工作人员提供必要的工作条件及合作,并保证所提供资料的真实性和完整性;贵公司有责任确保本所不受限制地接触任何与本业务有关的记录、文件和所需的其他信息;按本约定书的约定及时足额支付服务费用。

(如为第三方承担年度报表审计,应要求公司协助提供相关审计底稿)3. 本所的责任及义务本所的责任是根据国家外汇管理局XX省分局X汇【2012】46号的规定和本约定书的要求,对外方权益确认表实施并对实施程序的结果提出审核结论。

除非我们事先得到贵公司的同意,对在执行审核业务过程中知悉的商业秘密及贵公司提供的审核资料我们将严格保相关程序,密,当然按法律和报告披露要求的揭示除外。

4. 报告和报告的使用本所按照国家外汇管理局XX省分局X汇【2012】46号的规定和本约定书的要求出具报告;本所出具的报告仅供贵公司为向国家外汇管理部门报送外方权益确认表时使用。

5. 收费本次服务的收费是根据本所专业人员在本次工作中所负责任的程度、工作量及所需的工作技能确定的。

中外合资企业章程中英对照版

中外合资企业章程中英对照版第一章总则Chapter 1 General Provision第二章宗旨、经营范围Chapter 2 The Purpose l Scope and Scale of the Business 第三章投资总额和注册资本Chapter 3 Total Amount of Investment and the Registered Capital 第四章董事会Chapter 4 The Board of Directors第五章经营管理机构Chapter 5 Business Management Office第六章财务会计Chapter 6 Finance and Accounting第七章利润分配Chapter 7 Profit Sharing第八章职工Chapter 8 Staff and Workers第九章工会组织Chapter 9 The Trade Union Organization第十章期限、终止、清算Chapter 10 Duration, Termination and Liquidation of the Jint Venture Company第十一章规章制度Chapter 11 Rules and Regulations第十二章适用法律Chapter 12 Applicable Law第十三章附则Chapter 13 Supplementary Articles第一章总则Chapter 1 General Provision第一条根据《中华人民共和国中外合资企业法》,和中国×公司(以下简称甲方)与×国×××公司)合资经营合同,特制订本合营公司章程。

Article 1 In accordance with the "Law of the People's Republic of China on joint Venture Using Chinese and ForeignInvestment" and the contract signed on in_________ ,china, by,×Co. (hereinafter referred to as Party A). and ×××Co.,Ltd. (hereinafar referred to as Party A), to set up a joint venture,×× Limited Liability Company (hereinafter referred to asjoint venture company), the Articles of Association hereby is formulated.第二条合营公司中文名称为:××有限公司Article 2 The names of the joint venture company shall be ××Limited Liability Company.缩写为:Its abbreviation is ______________.合营公司的法定地址为:The Legal address of the joint venture company is at 第三条甲、乙双方的名称、法定地址为:Article 3 The names and legal addresses of each parties are as follows:甲方:中国×公司,其法定地址为Party A: × Co. , China, and its legal address is 乙方:×国×××公司,其法定地址为party B: ××× Co., Ltd, and its legal address is 第四条合营公司的组织形式为有限责任公司。

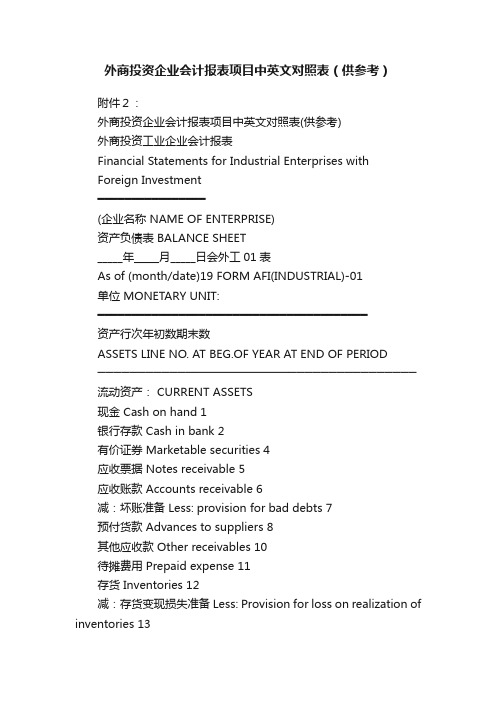

外商投资企业会计报表项目中英文对照表(供参考)

外商投资企业会计报表项目中英文对照表(供参考)附件2:外商投资企业会计报表项目中英文对照表(供参考)外商投资工业企业会计报表Financial Statements for Industrial Enterprises withForeign Investment━━━━━━━━━━━━━━━━(企业名称 NAME OF ENTERPRISE)资产负债表 BALANCE SHEET_____年_____月_____日会外工01表As of (month/date)19 FORM AFI(INDUSTRIAL)-01单位 MONETARY UNIT:━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━资产行次年初数期末数ASSETS LINE NO. AT BEG.OF YEAR AT END OF PERIOD────────────────────────────────────────流动资产: CURRENT ASSETS现金 Cash on hand 1银行存款 Cash in bank 2有价证券 Marketable securities 4应收票据 Notes receivable 5应收账款 Accounts receivable 6减:坏账准备 Less: provision for bad debts 7预付货款 Advances to suppliers 8其他应收款 Other receivables 10待摊费用 Prepaid expense 11存货 Inventories 12减:存货变现损失准备Less: Provision for loss on realization of inventories 13一年内到期的长期投资Long-term investments maturing within one year 15 其他流动资产 Other current assets 16 流动资产合计 Total current assets 17长期投资:LONG-TERM INVESTMENTS:长期投资 Long-term investments 18一年以上的应收款项 Receivables collectible after one year 20 固定资产:FIXED ASSETS:固定资产原价 Fixed assets-cost 21减:累计折旧 Less: Accumulated depreciation 22固定资产净值 Fixed assets-net value 23固定资产清理 Disposal of fixed assets 27在建工程:CONSTRUCTION IN PROGRESS:在建工程 Construction in progress 28无形资产:INTANGIBLE ASSETS:场地使用权 Land occupancy right 29工业产权及专有技术 Industry property rights and proprietary technology 30其他无形资产 Other intangible assets 31无形资产合计 Total intangible assets 32其他资产:OTHER ASSETS:开办费 Organization expense 33筹建期间汇兑损失 Exchange loss during startup period 34递延投资损失 Deferred loss on investments 35递延税款借项 Deferred tax charges 36其他递延支出 Other deferred expense 37待转销汇兑损失 Unamortized exchange loss 38其他资产合计 Total other assets 40资产总计 TOTAL ASSETS 41负债及所有者权益LIABILITIES AND OWNER'S EQUITY流动负债:CURRENT LIABILITIES:短期借款 Short-term loans 42应付票据 Notes payable 43应付账款 Accounts payable 44应付工资 Accrued payroll 45应交税金 Taxes payable 46应付股利 Dividends payable 47预收货款 Advances from customers 48其他应付款 Other payables 50预提费用 Accrued expense 51职工奖励及福利基金Staff and workers' bonus and we lfare fund 52 一年内到期的长期负债Long-term liabilities due within one year 53 其他流动负债 Other current liabilities 54流动负债合计 Total current liabilities 55长期负债: LONG-TERM LIABILITIES:长期借款 Long-term loans 56应付公司债 Debentures payable 57应付公司债溢价(折价) Premium (discount)on debentures payable 58 一年以上的应付款项 Payables due after one year 59 长期负债合计 Total long-term liabilities 60其他负债:OTHER LIABILITIES:筹建期间汇兑收益 Exchange gain during start-up period 61 递延投资收益 Deferred gain on investments 62递延税款贷项 Deferred tax credits 63其他递延贷项 Other deferred credits 64待转销汇兑收益 Unamortized exchange gain 65其他负债合计 Total other liabilities 66负债合计 Total liabilities 67所有者权益:OWNER'S EQUITY:资本总额(货币名称及金额______)Registered capital(currency and amount________)实收资本(非人民币货币资本期末金额_______) 68Paid-in capital(amount of non-RMB currency at end of period_________) 其中:中方投资(非人民币货币资本期末金额_________) 69Including: Chinese investments (amount of non-RBM currency at endof period______)外方投资( 非人民币货币资本期末金额________) 70Foreign investments (amount of non-RMB currency at end of period______) 减:已归还投资 Less: Investments returned 71 资本公积 Capital surplus 72储备基金 Reserve fund 74企业发展基金 Enterprise expansion fund 75利润归还投资 Profit capitalized on return of investments 76 本年利润 Current year net income 77未分配利润 Undistributed profit 78所有者权益合计 T otal owner's equity 80负债及所有者权益总计TOTAL LIABILITIES AND OWNER'S EQUITY 81━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━附注:NOTES:1.受托加工材料 Customers' materials to be processed ______;2.受托代销商品 Consignment-in ______;3.代管商品物资 Goods held for others ______;4.由企业负责的应收票据贴现 Notes receivable discounted with recourse ________;5.租入固定资产 Fixed assets under operating lease ________;6.本年支付的进口环节税金Current year payment of importtaxes ________.━━━━━━━━━━━━━━━━━━━━企业名称 NAME OF ENTERPRISE利润表 INCOME STATEMENT_____年度_____季度_____月份For the year(or quarter, month) ended(month/date)19________会外工02表 FORM AFI(INDUSTRIAL)-02单位:MONETARY UNIT:━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━项目行次本期数本年累计数上年同期累计数ITEMS LINE NO. CURRENT PERIOD CURRENT YEAR CUMULATIVE LAST YEAR CUMULATIVE────────────────────────────────────────产品销售收入 Sales 1其中:出口产品销售收入 Including: Export Sales 2减:销售折扣与折让 Less: Sales discounts and allowances 3产品销售净额 Net sales 4减:产品销售税金 Less: Sales tax 5产品销售成本 Cost of sales 6其中:出口产品销售成本 Including: Cost of export sales 7产品销售毛利Gross profit 8减:销售费用 Less: Selling expense 9管理费用 General and administrative expense 10财务费用 Financial expense 11其中:利息支出(减利息收入) 12Including:Interest expense(less interest income)汇兑损失(减汇兑收益)Exchange loss(less exchange gain) 13产品销售利润 Income from main operation 14加:其他业务利润 Add: Income from other operations 15营业利润Operating income 16加:投资收益 Add: Investment income 17营业外收入 Non-operating income 18减:营业外支出 Less: Non-operating expense 19加:以前年度损益调整 20Add: Adjustment to prior year's income and expense利润总额 Income before tax 21减:所得税 Less: Income tax 22净利润 Net income 23━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━附注:NOTES:出口产品销售收入:(1)非人民币货币名称和金额Export sales: Non-RMB currency(name and amount)折合记账本位币金额Translated into recording currency (amount)(2)非人民币货币名称和金额Non-RMB currency(name and amount)折合记账本位币金额Translated into recording currency (amount)━━━━━━━━━━━━━━━━━━(企业名称 NAME OF ENTERPRISE )财务状况变动表STATEMENT OF CHANGES IN FINANCIAL POSITION_______年度For the year ended December 31,19________会外工03表FORM AFI(INDUSTRIAL)-03单位 MONETARY UNIT:━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━流动资金来源和运用行次金额SOURCES AND APPLICATIONS OF WORKING CAPITAL LINE NO. AMOUNT━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━一、流动资金来源 SOURCES OF WORKING CAPITAL1.本年净利润Current year net income 1加:不减少流动资金的费用和损失: Add: Amounts not affecting working capital(1)固定资产折旧Depreciation of fixed assets 2(2)无形资产及其他资产摊销(减:其他负债转销)Amortization of intangible assets 3and other assets(less amortization of other liabilities)(3)固定资产盘亏(减盘盈)Fixed assets under book amount(less over) 4(4)处理固定资产损失(减收益)Loss on disposal of fixed assets(less gain) 5(5)长期投资溢价摊销(减折价摊销)Amortization of premium on long-term investments (less amortization of discount) 6(6)应付公司债折价摊销(减溢价摊销)Amortization of discount on debentures payable (less amortization of discount) 7(7)捐赠固定资产支出 Expenditure on donation of fixed assets 8(8)递延税款 Deferred taxes 9(9)其他不影响流动资产的费用和损失 10Other expense & losses not affecting working capital小计 SUB-TOTAL 122.其他来源:Other sources:(1)固定资产清理收入(减清理费用)Proceeds from disposal of fixed assets (less expense) 13(2)收回长期投资Realization of long-term investments 14(3)减少固定资产Decrease of fixed assets 15(4)减少无形资产 Decrease of intangible assets 16(5)增加长期借款Increase of long-term loans 17(6)发行公司债 Issuance of debentures 18(7)增加其他负债 Increase of other liabilities 19(8)增加储备基金和企业发展基金 Increase of reserve fund andenterprise expansion fund 20(9)增加资本 Increase of capital 21(10)增加资本公积 Increase of capital surplus 22(11)弥补亏损 Recovery of loss 23小计 SUB-TOTAL 25流动资金来源合计 TOTAL SOURCES OF WORKING CAPITAL 26二、流动资金运用 APPLICATIONS OF WORKING CAPITAL1.利润分配 Distribution of profit(1)职工奖励及福利基金Staff and workers' bonus and welfare fund 27(2)储备基金 Reserve fund 28(3)企业发展基金 Enterprise expansion fund 29(4)股利 Dividends 30(5)利润归还所有者投资 Profit capitalized on return of owner's investments 31(6)利润增资 Profit reinvestments 32小计 SUB-TOTAL 342.其他运用 Other applications:(1)增加固定资产 Increase of fixed assets 35(2)增加无形资产及其他资产Increase of intangible assets and other assets 36(3)增加长期投资 Increase of long-term investments 37(4)偿还长期借款 Repayment of long-term loans 38(5)收回公司债 Repayment of company debentures 39(6)减少其他负债 Decrease of other liabilities 40(7)归还所有者投资(扣除利润归还所有者投资)Investments returned to owners 41(less profit capitalized on return of owner's investments)(8)减少资本公积 Decrease of capital surplus 42(9)减少储备基金和企业发展基金Decrease of reseverve fund and enterprise expansion fund 43小计 SUB-TOTAL 45流动资金运用合计TOTAL APPLICATIONS OF WORKING CAPITAL 46流动资金增加净额 NET INCREASE OF WORKING CAPITAL 47 ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━流动资金各项目的变动行次金额CHANGES IN WORKING CAPITAL ITEMS LINE NO. AMOUNT ────────────────────────────────────────一、流动资产本年增加数 INCREASE OF CURRENT ASSETS1.现金 Cash on hand 482.银行存款 Cash in bank 493.有价证券 Marketable securities 504.应收票据 Notes receivable 515.应收账款 Accounts receivable 52减:坏账准备Less: Provision for bad debts 536.预付货款 Advances to suppliers 547.其他应付款Other receivables 558.待摊费用 Prepaid expense 569.存货 Inventories 57减:存货变现损失准备 Less: Provision for loss on realization of inventories 58流动资产增加净额 NET INCREASE OF CURRENT ASSETS 61二、流动负债本年增加数 INCREASE OF CURRENT LIABILITIES1.短期借款 Short term loans 622.应付票据 Notes payable 633.应付账款 Accounts payable 644.应付工资 Accrued payroll 655.应交税金 Tax payable 666.应付股利 Dividends payable 677.预收货款 Advances from customers 688.其他应付款Other liabilities 699.预提费用 Accrued expense 7010.职工奖励及福利基金 Staff and workers' bonus and welfare fund 71流动负债增加净额 NET INCREASE OF CURRENT LIABILITIES 74 流动资金增加净额 NET INCREASE OF WORKING CAPITAL 75 ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━企业名称 NAME OF ENTERPRISE利润分配表STATEMENT OF PROFIT APPROPRIATION AND DISTRIBUTION________年度会外工02表附表1For the year ended December 31,19______ FORM AFI(INDUSTRIAL)-02 Sub.1 单位 MONETARY UNIT:━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━项目行次本年实际上年实际ITEMS LINE NO. ACTUAL THIS YEAR ACTUAL LAST YEAR────────────────────────────────────────净利润 Net income 1减:职工奖励及福利基金Less: Staff and workers' bonus and welfare fund 2储备基金 Reserve fund 3企业发展基金 Enterprise expansion fund 4利润转作投资 Profit reinvestments 5加:年初未分配利润 Add: Undistributed profit at beginning of year 7 已弥补亏损 Recovery of loss 8可供所有者分配的利润Profit available for distribution to owners 10 减:已分配股利 Less: Dividends declared 11 其中:中方股利 Including: Chinese dividends 12外方股利 Foreign dividends 13利润归还投资 Profit capitalized on return of investments 14 年末未分配利润 Undistributed profit at end of year 15━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━(企业名称 NAME OF ENTERPRISE)应交增值税明细表STATEMENT OF VALUE ADDED TAX PAYABLE______年_____月会外工01表附表6For the year(or month) ended(month)______ FORM AFI(INDUSTRIAL)-01 Sub.6 单位 MONETARY UNIT:━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━项目行次本月数本年累计数ITEMS LINE NO CURRENT MONTH CURRENT YEARCUMULATIVE AMOUNT────────────────────────────────────────一、应交增值税:VAT payable:1.年初未抵扣数(用“-”号反映)Amount not yet deducted at beginningof year(Represented by a “-”sign)2.销项税额 VAT on sales出口退税 VAT refund for exported goods进项税额转出 Amount transfer out fromVAT on purchase转出多交增值税 Transfer out overpaid VAT3.进项税额 VAT on purchase已交税金VAT paid减免税款Tax reduced and exempted出口抵减内销产品应纳税额 VAT payable ondomestic sales offset against VAT on purchasefor export sales转出未交增值税 Transfer out unpaid VAT4.期末未抵扣数(用“-”号反映)Amount not yet deducted at end of period(Represented by a “-”sign)二、未交增值税VAT unpaid1.年初未交数(多交数以“-”号反映)Amount unpaid at beginning of year(Amount overpaid represented bya “-” sign)2.本期转入数(多交数以“-”号反映)Amount transfer inat current period(Amount overpaid represented by a “-” sign)3.本期已交数 Amount paid at current period4.期末未交数(多交数以“-”号反映)Amount unpaid at end of period(Amount overpaid represent ed by a “-” sign)━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━各行业特有的项目(一)外商投资旅游企业:Tourism Enterprises with Foreign Investment━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━项目 ITEMS────────────────────────────────────────营业收入:Revenues:客房 Rooms餐饮 Food and beverage公寓 Apartments写字楼 Office building商场 Department store其他 Other营业收入合计 Total revenues营业税金 Sales tax客房 Rooms餐饮 Food and beverage公寓 Apartments写字楼 Office building商场 Department store其他 Other营业税金合计 Total sales tax营业成本:Operating cost:餐饮成本 Food and beverage cost商品成本 Merchandise cost其他成本 Other cost营业成本合计 Total operating cost工资及福利:Salaries, wages and employee benefits客房 Rooms餐饮 Food and beverage公寓 Apartments写字楼 Office building商场 Department store其他 Other工资及福利合计 T otal salaries, wages and employee benefits营业费用: Operating expense:客房 Rooms餐饮 Food and beverage公寓 Apartments写字楼 Office building商场 Department store其他 Other营业费用合计 Total operating expense营业毛利:Gross Operating Profit by Department:客房 Rooms餐饮 Food and beverage公寓 Apartments写字楼 Office building商场 Department store其他 Other各营业部门营业毛利合计Total Gross Operating Profit by Department不分配费用:Unallocated expense:工资及福利:Salaries, wages and employee benefits:行政管理 Administrative and general市场推广 Marketing能源维修 Energy and maintenance cost工资及福利合计 T otal salaries, wages and employee benefits 行政管理及公共费用:A&G and public expense行政管理 Administrative and general市场推广 Marketing能源维修 Energy and maintenance cost行政管理及公共费用合计 Total A&G and public expense不分配费用合计 T otal Unallocated expense营业毛利 Gross Operation Profit非经营费用 Fixed charges营业利润 Operating income加:投资收益 Add: Investment income营业外收入 Non-operating revenues减:营业外支出 Less: Non-operating expense加:以前年度损益调整 Add: Adjustment of prior year's income and expense 利润总额 Income before tax减:所得税 Income tax净利润 Net income━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━会外旅02表 FORM AFT(Tourism)-02━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━本期实际 Current period's actual本期预算 Current period's plan上年同期 Same period last year本年累计 current year cumulative上年累计 Last year cumulative百分比% Percentage %委托银行收款 Collections entrusted to the bank预付定金 Prepaid deposit预收定金 Deposit received in advance应付工资及福利 Accrued Payroll and employee benefits(二)外商投资施工企业:Construction Enterprises with Foreign Investment1.固定资产及临时设施 Fixed assets and temporary installation2.临时设施 Temporary installation3.临时设施摊销 Amortization of temporary installation4.临时设施净值 Net value of temporary installation5.临时设施清理 Disposal of temporary installation6.专项工程 Specific construction project7.工程结算收入 Revenues8.工程结算税金 Sales tax9.工程结算成本 Cost of sales10.工程结算毛利 Gross profit11.工程结算利润 Income from main operation12.会外施01表 FORM AFC(Construction)-01(三)外商投资商品流通企业Commercial Enterprises with Foreign Investment:1.商品销售收入 Sales2.商品销售收入净额 Net sales3.商品销售成本 Cost of sales4.进货费用 Purchase expense5.商品销售毛利 Gross profit6.代购代销收入 Income from purchase and sales commission7.主营业务毛利 Gross profit from main operation8.销货费用 Selling expense9.主营业务利润 Income from main operation10.会外商01表 FORM AFC(Commercial)-01(四)外商投资房地产企业Real Estate Enterprises with Foreign Investment:1.在建开发产品 Work in progress2.递延出租收入 Deferred rental income3.经营收入 Revenues4.经营税金 Sales tax5.经营成本 Operating cost6.经营毛利 Gross profit7.经营利润 Income from main operation8.非人民币货币经营收入 Non-RMB revenues9.会外房01表 FORM AFR(Real Estate)-01(五)外商投资租赁企业Lease Enterprises with Foreign Investment:1.预付租赁资产款 Advances to lessor2.低值易耗品:Low-value consumables3.一年内到期的长期投资及长期应收款Long-term investments and receivables maturing within one year4.应收租赁款 Lease payment receivables5.未实现租赁收益 Unearned lease income6.应收转租赁款 Sub-lease payment receivables7.逾期未收租赁款 Lease payment receivables past due8.长期投资及长期应收款合计 T otal long-term investments and long-term receivables9.经营租赁资产 Assets under operating lease10.经营租赁资产原价 Original cost of assets under operating lease11.经营租赁资产折旧 Depreciation of assets under operating lease12.经营租赁资产净值Net value of assets under operating lease13.租赁保证金 Deposit from lessee14.应付转租赁租金 Sub-lease payment payables to lessor15.营业收入 Revenues16.利息收入 Interest revenues17.手续费收入 Service fee revenues18.营业税金 Sales tax19.营业支出 Operating expenditure20.利息支出 Interest expense21.营业毛利 Gross profit22.非人民币货币营业收入 Non-RMB operating income23.会外租01表 FORM AFL(Lease)-01(六)外商投资交通企业:Transportation Enterprises with Foreign Investment:1.主营业务收入 Revenues2.营业税金 Sales tax3.营业成本 Operating cost4.主营业务毛利 Gross profit5.主营业务利润 Income from main operation6.会外交01表 FORM AFT(Transportation)-01(七)外商投资银行:Banks with Foreign Investment:1.现金及银行存款 Cash on hand and cash in bank2.贵金属 Precious metal3.存放中央银行款项 Deposits and required reserve in central bank4.存放同业款项 Deposits in other banks5.存放联行款项 Deposits in correspondent banks6.拆出资金 Loans to other banks7.短期贷款 Short-term loans8.进出口押汇Acceptance of draft under letter of credit for imports and exports9.应收利息 Interest receivable10.坏账准备 Bad debt provision for interest receivable11.贴现 Discount12.中长期贷款 Medium or long-term loans13.逾期贷款 Past due loans14.贷款呆账准备 Bad debt provision for loan principals15.短期存款 Short-term deposits16.短期储蓄存款 Short-term savings deposits17.向中央银行借款 Borrowings from central bank18.同业存放款项 Deposit from other banks19.联行存放款项 Deposit from correspondent banks20.拆入资金 Loans from other banks21.应解汇款 Amounts payable on wire transfers received22.发行短期债券 Issuance of short-term debentures payable23.长期存款 Long-term deposits24.长期储蓄存款 Long-term savings deposits25.保证金 Margin(held by bank in financial transactions)26.发行长期债券 Issuance of long-term debentures payable27.营业收入 Revenues28.利息收入 Interest revenues29.金融企业往来收入Revenues from transactions with financial institutions30.手续费收入 Service fee revenues31.其他营业收入 Other operating revenues32.营业支出 Operating expenditure33.利息支出 Interest expense34.金融企业往来支出 Expense from transactions with financial institutions35.手续费支出 Service fee expense36.营业费用 Operating expense37.其他营业支出 Other operating expenditure38.营业税金 Sales tax39.会外银01表 FORM AFB(Bank)-01(八)外商投资农业企业Agricultural Enterprises with Foreign Investment:1.会外农01表 FORM AFA(Agriculture)-01(九)外商投资服务企业Service Enterprises with Foreign Investment:1.营业收入 Revenues2.营业税金 Sales tax3.营业成本 Operating cost4.营业费用 Operating expense5.营业毛利 Gross profit6.会外服01表 FORM AFS(Service)-01。

中注协发布《外商投资企业外方权益确认表审核指导意见》

中注协发布《外商投资企业外方权益确认表审核指导意见》本刊记者

【期刊名称】《财务与会计》

【年(卷),期】2012(000)007

【摘要】不久前,中注协印发了《外商投资企业外方权益确认表审核指导意见》(以下简称《审核指导意见》)。

《审核指导意见》以《中国注册会计师其他鉴证业务准则第3101号——历史财务信息神计或审阅以外的鉴证业务》为框架,结合外方权益确认表审核的特点,

【总页数】1页(P27-27)

【作者】本刊记者

【作者单位】《财务与会计:综合版》编辑部

【正文语种】中文

【中图分类】F279.244.3

【相关文献】

1.外商投资企业外方权益验资询证实务与操作 [J], 肖继五;张蕾

2.中注协发布《关于规范为拟设立会计师事务所合伙人或者股东出具证明工作的指导意见》 [J],

3.外商投资企业外方权益验资询证实务与操作 [J], 肖继五;张蕾

4.中注协发布关于注册会计师行业积极做好医药卫生体制改革专业服务工作的指导意见 [J],

5.抢抓机遇求突破服务改革促发展——中注协发布关于注册会计师行业积极做好医药卫生体制改革专业服务工作的指导意见 [J], 钟标

因版权原因,仅展示原文概要,查看原文内容请购买。

外资企业合同通用条款范本中英文对照资料全

常见的合同通用条款GENERAL TERMS AND CONDITIONS OF CONTRACTDATED日期CONTRACT NAME合同名称by and between合同双方PARTY A NAMEPARTY A甲方名称and与PARTY B NAMEPARTY B乙方名称TABLE OF CONTENTPRELIMINARY STATEMENT前言1. DEFINITIONS定义2. [OPERATIVE CLAUSES] 具体操作条款3. CONDITIONS PRECEDENT如有必要,根据交易具体情况设定相应先决条件4. REPRESENTATIONS AND WARRANTIES 陈述和担保[保证]5. TERM合同期限6. TERMINATION合同终止7. CONFIDENTIALITY保密义务8. BREACH OF CONTRACT违约9. FORCE MAJEURE不可抗力10. SETTLEMENT OF DISPUTES争议的解决11. APPLICABLE LAW 适用法律12. MISCELLANEOUS PROVISIONS其他规定THIS CONTRACT(“Contract”)is made in [city and province], China on this day of ,200 by and between [Party A name],[Party A entity form] established and existing under the laws of China, with its legal address at [address](hereinafter r eferred to as “Party A”), and [Party B name], [Party B entity form] organized and existing under the laws of [Party Bjurisdiction of incoporation] with its legal address at [address] (hereinafter referred to as “Party B”). Party A and Party B shall hereina fter be referred to individually as a “Party ” and collectively as the “Parties”.本合同于年月日由以下两方在[地点]签订:[甲方名称],一家根据中华人民共和国法律组建及存续的[甲方组织形式],法定地址为[甲方法定地址](以下简称“甲方”):[乙方名称],一家根据[乙方所在国]法律组建及存续的[乙方组织形式],法定地址为[乙方法定地址](以下简称“乙方”)。

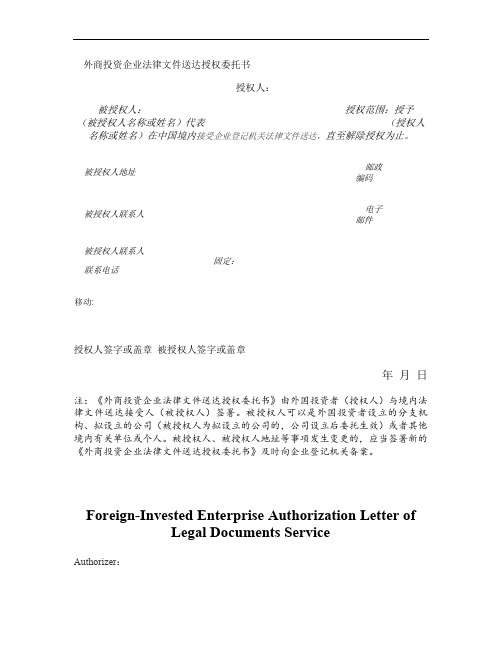

外商投资企业法律文件送达授权委托书中英文对照.

外商投资企业法律文件送达授权委托书授权人:被授权人:授权范围:授予(被授权人名称或姓名)代表(授权人名称或姓名)在中国境内接受企业登记机关法律文件送达,直至解除授权为止。

被授权人地址邮政编码被授权人联系人电子邮件被授权人联系人联系电话固定:移动:授权人签字或盖章被授权人签字或盖章年月日注:《外商投资企业法律文件送达授权委托书》由外国投资者(授权人)与境内法律文件送达接受人(被授权人)签署。

被授权人可以是外国投资者设立的分支机构、拟设立的公司(被授权人为拟设立的公司的,公司设立后委托生效)或者其他境内有关单位或个人。

被授权人、被授权人地址等事项发生变更的,应当签署新的《外商投资企业法律文件送达授权委托书》及时向企业登记机关备案。

Foreign-Invested Enterprise Authorization Letter ofLegal Documents ServiceAuthorizer:Authorizee:Limits of Authority:Author: (name or full name of authorizee represent (name or full name of authorizer to accept legal documents service of enterprise registration institution within China.Address of AuthorizeePost CodeContactor of AuthorizeeE-mailTel of Contactor of Authorizee Fixed-line Phone:Mobile Phone:Authorizer’s Signature or Seal Authorizee’s Signature or SealDateNote:”Foreign-Invested Enterprise Authorization Letter of Legal Documents Service” is to be dully executed by foreign investor (collectively the “authorizer” and agent for the legal documents service within the People’s Republic of China (the “autho rizee”. The authorizee may be appointed among any appropriate branch, company already established or intended to be established by foreign investors (and in case of a company intended to be established, such authority come into effect only after the company is successfully established or any other entity or individual within the People’s Republic of China. A new Foreign-Invested Enterprise Authorization Letter of Legal Documents Service shall be executed for the change of authorizee, address of the authorizee, etc. The authorizee shall also be filed with the competent company registry office for the record.。

外方权益审计约定书

外方权益确认表审核业务约定书委托方: (以下简称甲方)受托方: (以下简称乙方)甲乙双方经协商,就甲方委托乙方执行审核业务达成如下约定:一、委托审核的范围、目的甲方委托乙方对本单位2011年外商投资企业外方权益确认表进行审核,并出具审核报告。

二、委托双方的责任甲方:按照国家外汇管理的有关规定编制外商投资企业外方权益确认表,真实、完整,编制的外商投资企业外方权益确认表,以及提供的资料的真实、合法、完整,并对该确认表充分披露的有关信息负责。

乙方:按照中国注册会计师制定的《外商投资企业外方权益确认表审核指导意见》的要求进行审核,出具审核报告,并对出具的审核报告负责。

三、委托双方的义务甲方:1、及时为乙方的审核工作提供其所要求的全部会计资料和其他有关资料;2、为乙方派出的有关工作人员提供必要的工作条件;3、按本业务约定书的规定支付审核费用。

由于甲方原因导致审核报告无法出具的,应根据乙方完成的工作量,支付相应的费用。

乙方:1、按照约定时间完成审核业务,出具审核报告;2、对在执行业务过程中知悉的商业秘密保密。

四、审核收费根据物价局规定的收费标准,经双方协商,本项审核业务收费额(或预计)金额为人民币元。

五、审核报告的使用责任乙方向甲方出具审核报告一式二份,由甲方分发使用,专门用于向国家外汇管理部门报送外商投资企业外方权益确认表时使用,不得用于其他用途。

由于使用审核报告不当所造成的后果与乙方及其注册会计师无关。

乙方向甲方出具审核报告的审核责任,并不能替代、减轻或免除甲方的会计责任。

六、本业务约定书一式两份,甲乙双方各执一份,具有同等法律效率。

本业务约定书自签订之日起生效。

七、违约责任甲乙双方按照《中华人民共和国合同法》的规定承担违约责任八、其他约定事项甲方:乙方:会计师事务所(盖章)(盖章)法定代表人或授权代表法定代表人或授权代表(签章)(签章)2012年 5月 12日 2012年 5月 12日。

审计业务约定书(中英文)

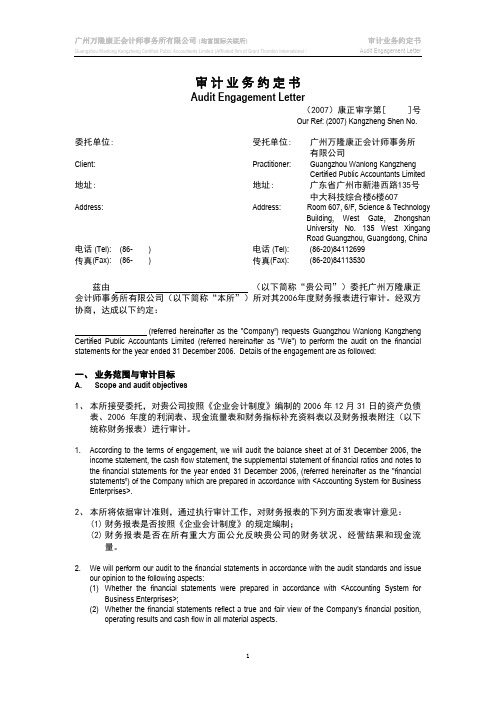

审计业务约定书Audit Engagement Letter(2007)康正审字第[ ]号Our Ref: (2007) Kangzheng Shen No.委托单位: 受托单位: 广州万隆康正会计师事务所有限公司Client: Practitioner: Guangzhou Wanlong KangzhengCertified Public Accountants Limited 地址: 地址: 广东省广州市新港西路135号中大科技综合楼6楼607 Address: Address: Room 607, 6/F, Science & TechnologyBuilding, West Gate, ZhongshanUniversity No. 135 West XingangRoad Guangzhou, Guangdong, China 电话 (Tel): (86- ) 电话 (Tel): (86-20)84112699传真(Fax): (86- ) 传真(Fax): (86-20)84113530兹由(以下简称“贵公司”)委托广州万隆康正会计师事务所有限公司(以下简称“本所”)所对其2006年度财务报表进行审计。

经双方协商,达成以下约定:(referred hereinafter as the "Company”) requests Guangzhou Wanlong Kangzheng Certified Public Accountants Limited (referred hereinafter as "We") to perform the audit on the financial statements for the year ended 31 December 2006. Details of the engagement are as followed:一、业务范围与审计目标A. Scope and audit objectives1、本所接受委托,对贵公司按照《企业会计制度》编制的2006年12月31日的资产负债表、2006年度的利润表、现金流量表和财务指标补充资料表以及财务报表附注(以下统称财务报表)进行审计。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

外商投资企业外方权益确认表审核业务约定书Audit Engagement LetterFor the Statement of Foreign Equity in Foreign-invested Enterprises甲方Party A:乙方Party B: Grant Thornton兹由甲方委托乙方对201X年度外商投资企业外方权益确认表(以下简称“外方权益确认表”)进行审核,经双方协商,达成以下约定:Party A hereby appoints Party B to perform the audit on statement of foreign equity in foreign-invested enterprises (referred hereinafter as "Statement of Foreign Equity") for the year ended December 31,201X. After consultation, both parties have reached the following agreements. Details of the engagement are as followed:一、审核的目标和范围1. The Objectives and Scope of the Audit乙方接受甲方委托,根据国家外汇管理的法律、法规和中国注册会计师协会制定的《外商投资企业外方权益确认表审核指导意见》,对甲方编制的201X年度外方权益确认表进行审核,并就甲方外方权益确认表的编制是否在所有重大方面按照国家外汇管理的有关规定编制提出审核结论。

According to the terms of engagement, Party B will conduct an audit of the Statement of Foreign Equity as at December 31, 201X, prepared by Party A in accordance with the relevant state regulations on foreign exchange and Audit Guidance on Statement of Foreign Equity in Foreign-invested Enterprises set out by the Chinese Institute of Certified Public Accountants. And express an opinion as to whether the Statement of Foreign Equity is prepared, in all material respects, in accordance with the relevant state regulations on foreign exchange.二、甲方的责任2. Responsibilities of Party A1、根据《中华人民共和国会计法》及国家外汇管理的相关法规的规定,甲方及甲方负责人有责任保证外方权益情况相关会计资料的真实性和完整性。

因此,甲方管理层有责任妥善保存和提供外方权益情况相关会计记录(包括但不限于会计凭证、会计账簿及其他会计资料),这些记录必须真实、完整地反映甲方的外方权益及外汇收支情况。

2.1 Under the Accounting Law of the People's Republic of China and the relevant state regulations on foreign exchange, it is the responsibility of Party A and its management to ensure the truthfulness and completeness of Party A’s accounting information of foreign equity. Accordingly, management is responsible for maintaining and providing proper accounting records relating to the statement of foreign equity, (including but not limited to accounting vouchers, ledgers and other accounting information). These records must reflect completely andaccurately the foreign equity and foreign exchange receipts and payments of Party A.2、按照国家外汇管理的有关规定编制外方权益确认表是甲方管理层的责任,这种责任包括:2.2 The management of Party A is responsible for the preparation of the Statement of Foreign Equity in accordance with the relevant state regulations on foreign exchange, including the following responsibilities:(1)按照国家外汇管理的有关规定真实、完整地编制外商投资企业外方权益确认表;(a) the Statement of Foreign Equity should be prepared accurately and completely in accordance with the relevant state regulations on foreign exchange;(2)设计、执行和维护必要的内部控制,以使外方权益确认表不存在重大错报。

(b) the necessary design, implementation, and maintenance of effective internal controls to enable the preparation of Statement of Foreign Equity that is free from material misstatement.3、及时为乙方的外方权益情况审核工作提供与审核有关的所有记录、文件和所需的其他信息(在20××年×月×日之前提供审核所需的全部资料,如果在审核过程中需要补充资料,亦应及时提供),并保证所提供资料的真实性和完整性。

2.3 Providing Party B with all information relevant to audited statement of foreign equity such as records, documentation and othermatters on a timely basis (with additional information for the purpose of the audit by the end of [date] [month] 201x) and ensuring the truthfulness and completeness of all the information provided.4、确保乙方不受限制地接触其认为必要的甲方内部人员和其他相关人员。

2.4 Granting Party B unrestricted access to personnel within PartyA and other relevant persons whom PartyB consider necessary in order to obtain audit evidence.5、甲方管理层对其做出的与审核有关的声明予以书面确认。

2.5 Written representations by the management of Party A on fulfillment of its responsibilities which Party B consider necessary audit evidence should be provided;6、为乙方派出的有关工作人员提供必要的工作条件和协助,乙方将于外勤工作开始前提供主要事项清单。

2.6 Provision of the necessary working environment and assistanceto Party B’s staff during the audit. Party B will provide a list of main matters prior to the commencement of on-site work.7、按照本约定书的约定及时足额支付审核费用以及乙方人员在审核期间的交通、食宿和其他相关费用。

2.7 Promptly and fully settle audit fee and expenses for transportation, meals and accommodations, and other related out-of-pocket expenses incurred during the audit by the staff of Party B in accordance with the terms specified in the engagement letter.8、乙方的审核不能减轻甲方及甲方管理层的责任。

2.8 Party B’s audit responsibility doe s not alleviate the responsibilities of Party A and its management.9、协调与审核涉及的内部审计人员和其他员工的工作。

(不是必备条款,在情况需要时考虑增加的业务约定条款。

)2.9 Coordinate the audit work with internal audit staff and other personnel within Party A.10、协调(同意)乙方与甲方前任注册会计师的沟通。